FORECAST UPDATES

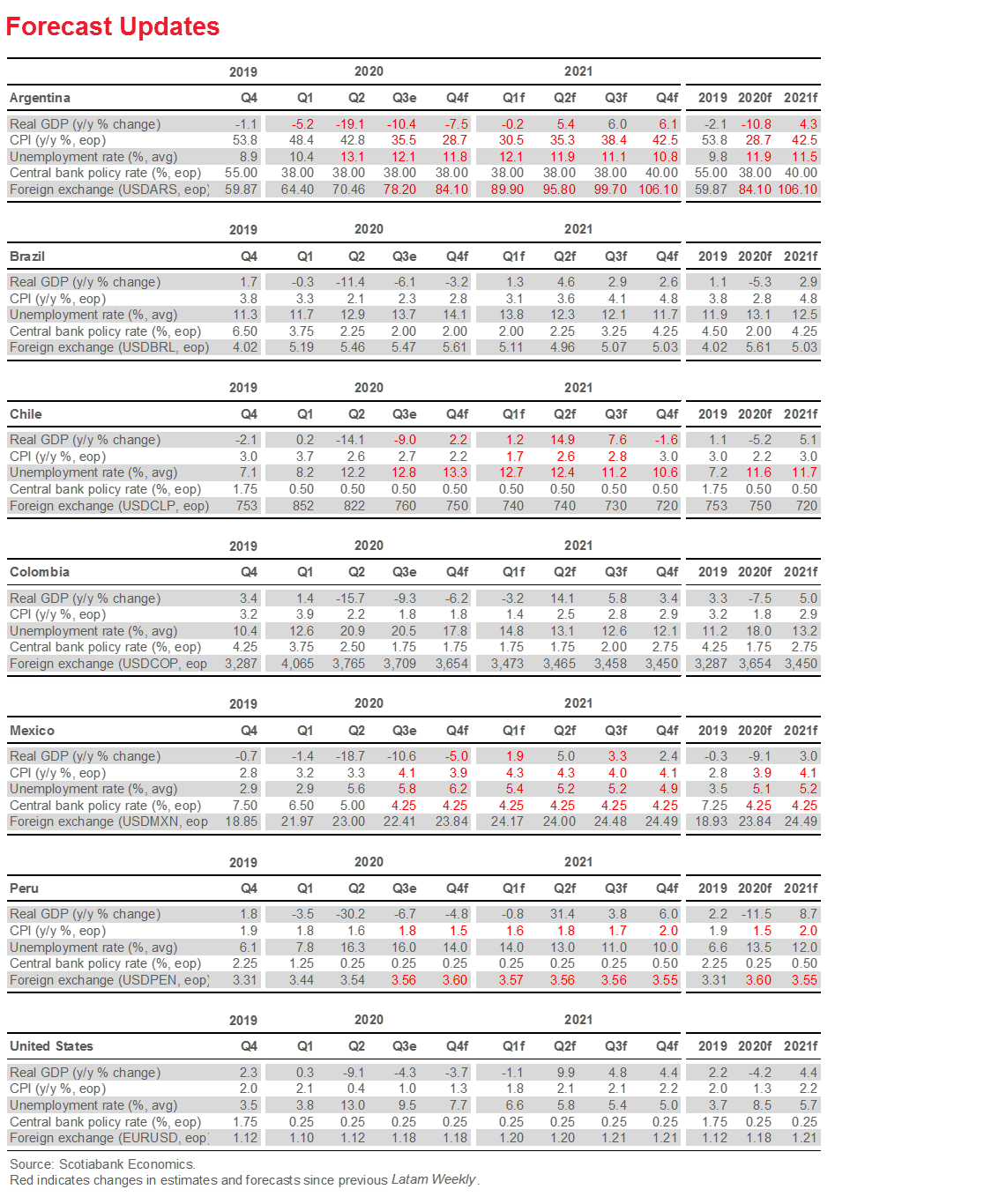

No one theme cuts across our forecast updates beyond fine tuning: we cut our growth forecast further for Argentina, softened the employment outlook for Chile, improved our unemployment outlook for Mexico, and pushed up our inflation forecast for Peru.

ECONOMIC OVERVIEW

New COVID-19 case numbers are starting to cool just as monetary easing cycles have come to an end and real-economy recoveries are starting to moderate, marking an inflection point in Latam.

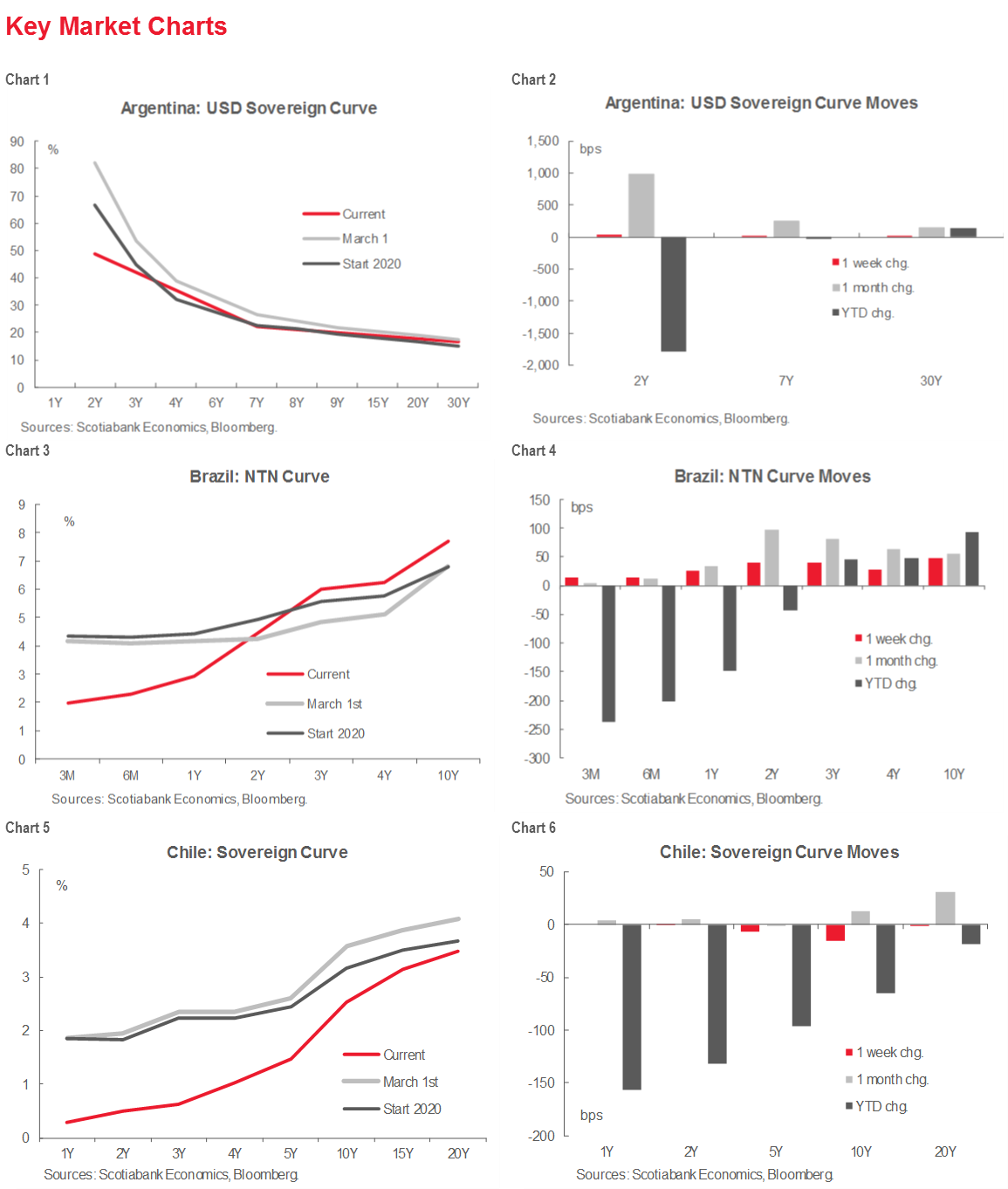

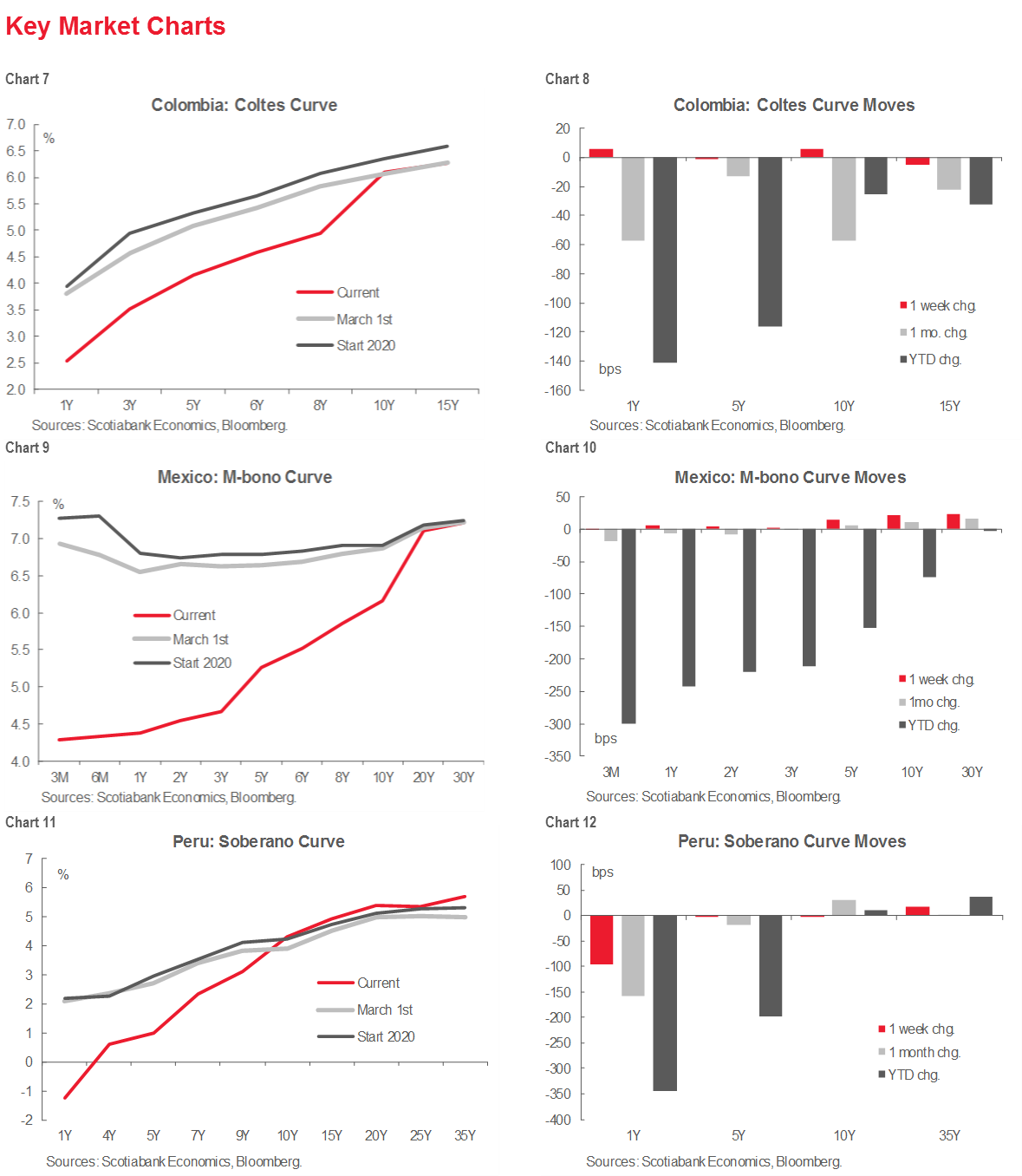

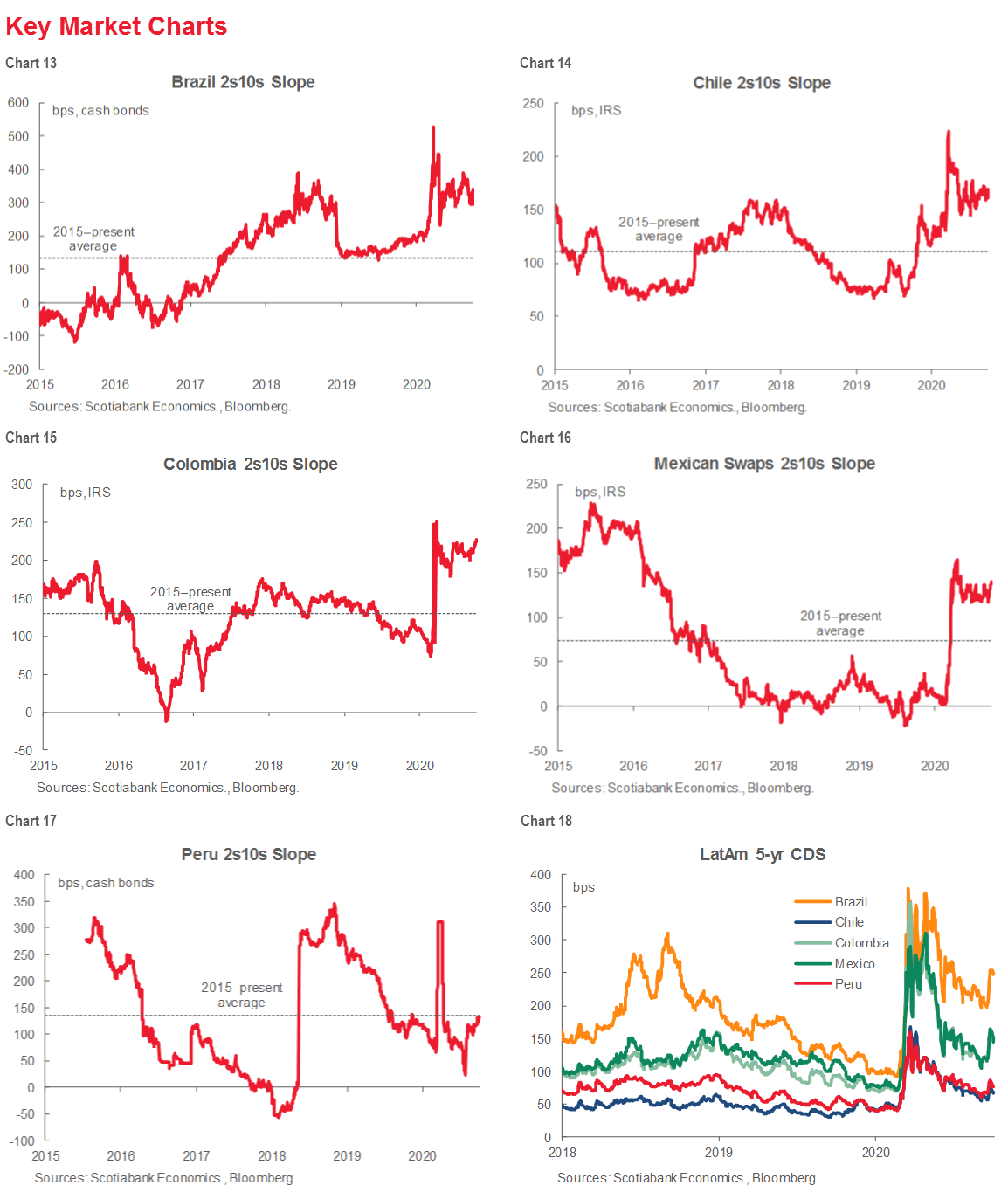

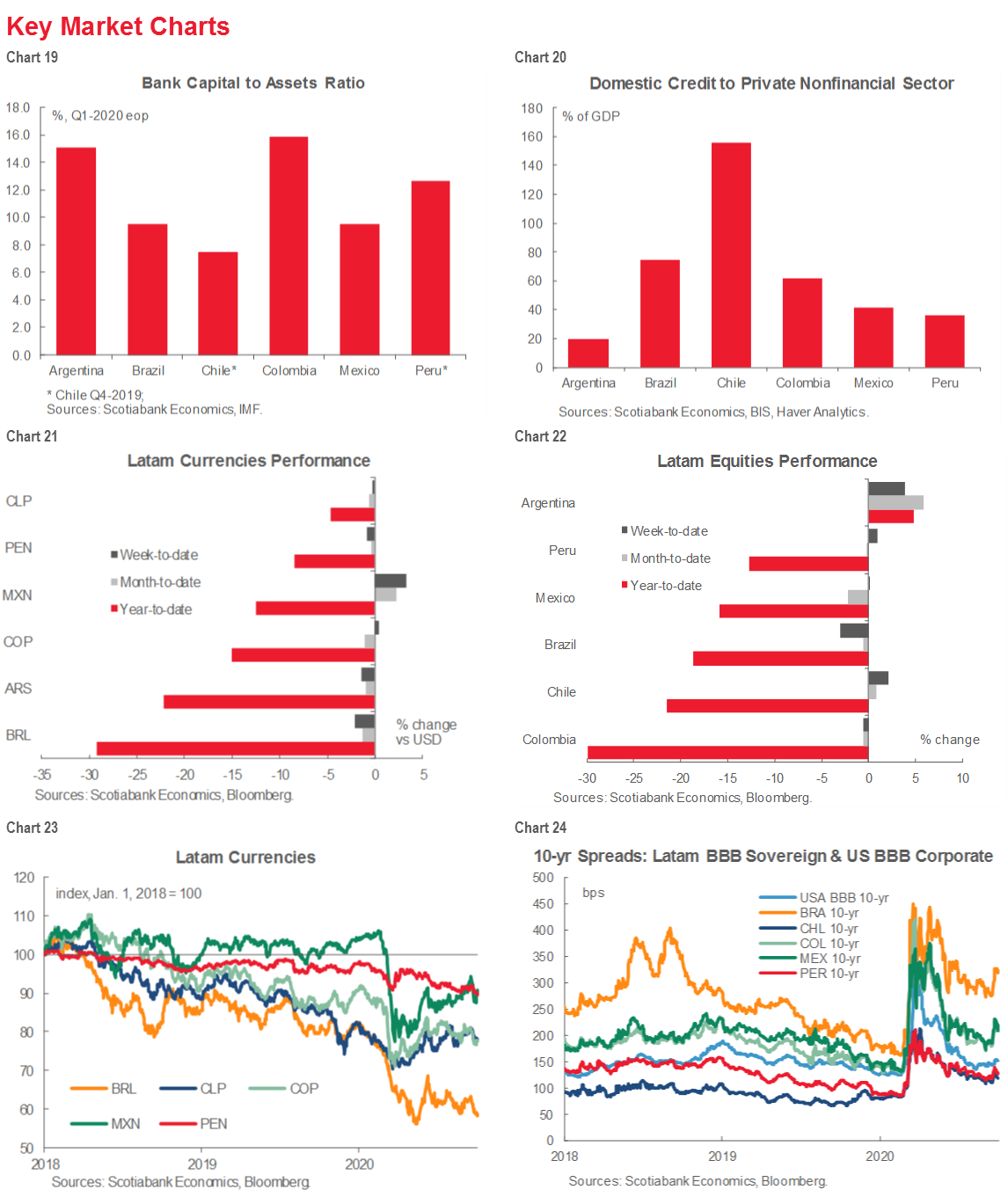

MARKETS REPORT

We review a detailed timeline for Chile’s constitutional process and elections, and look at the potential implications for Chilean assets.

COUNTRY UPDATES

Concise analysis of recent events and guides to the fortnight ahead in the Latam-6: Argentina, Brazil, Chile, Colombia, Mexico, and Peru.

MARKET EVENTS & INDICATORS

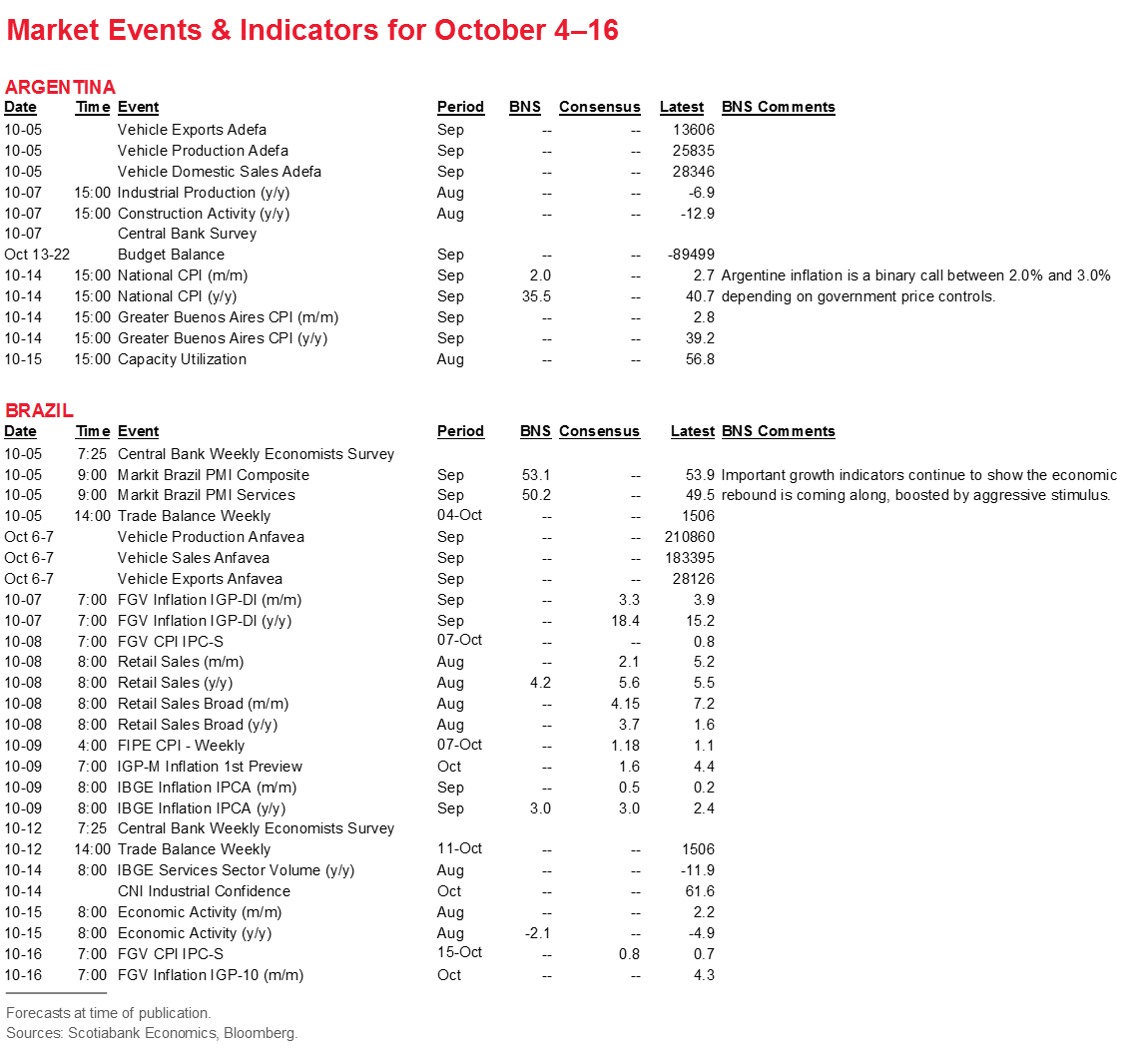

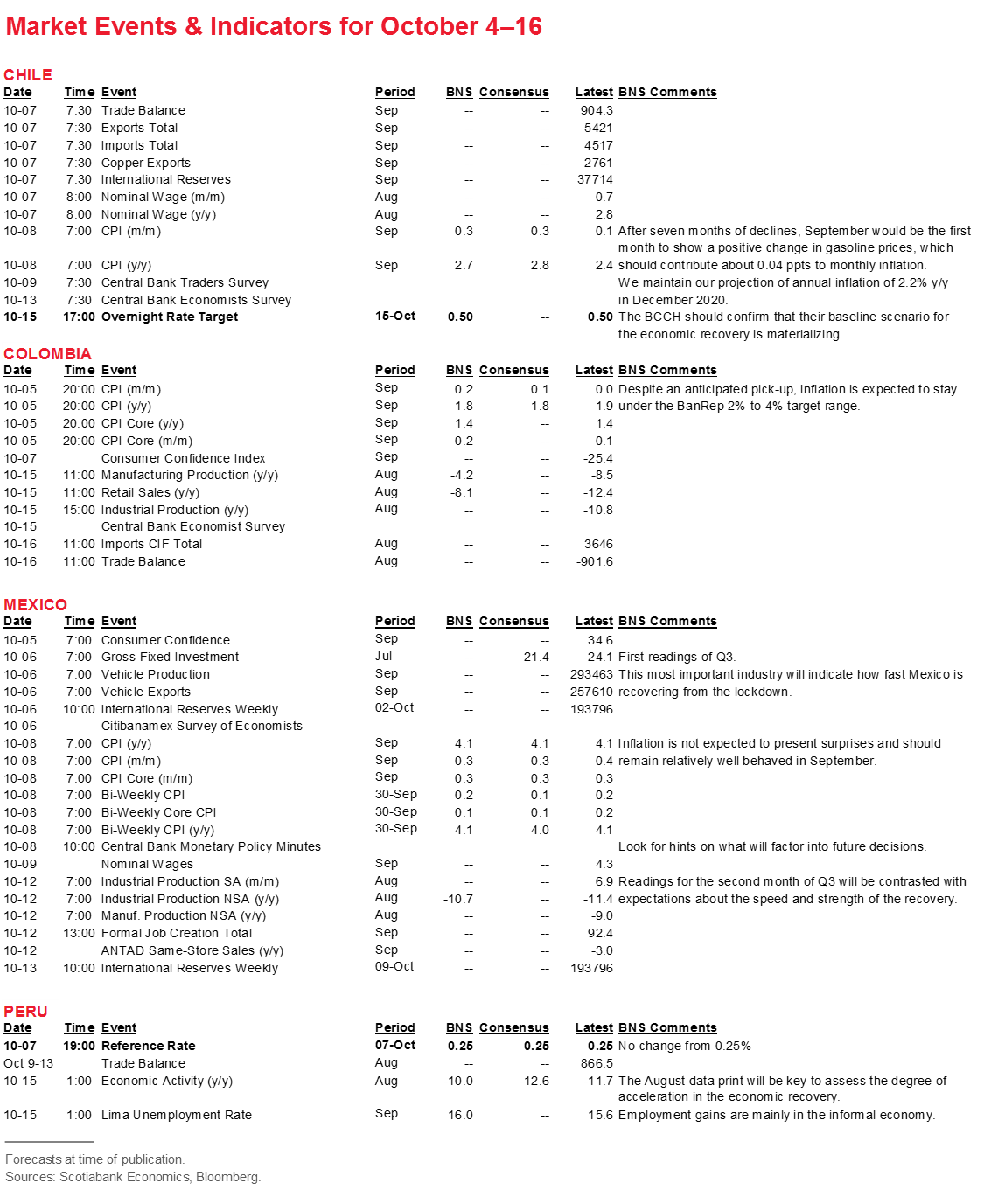

Risk calendar with selected highlights for the period October 4–16 across our six major Latam economies.

Economic Overview: The Hot Spot Starts to Cool

Brett House, VP & Deputy Chief Economist

416.863.7463

Scotiabank Economics

brett.house@scotiabank.com

New COVID-19 incidences are starting to wane across Latam, with the exception of a surge in Argentina.

The post-lockdown rebounds, though well advanced in most countries, are also, predictably, beginning to lose some pace as these economies try to re-open the corners of activity that are hardest to operate under physical distancing.

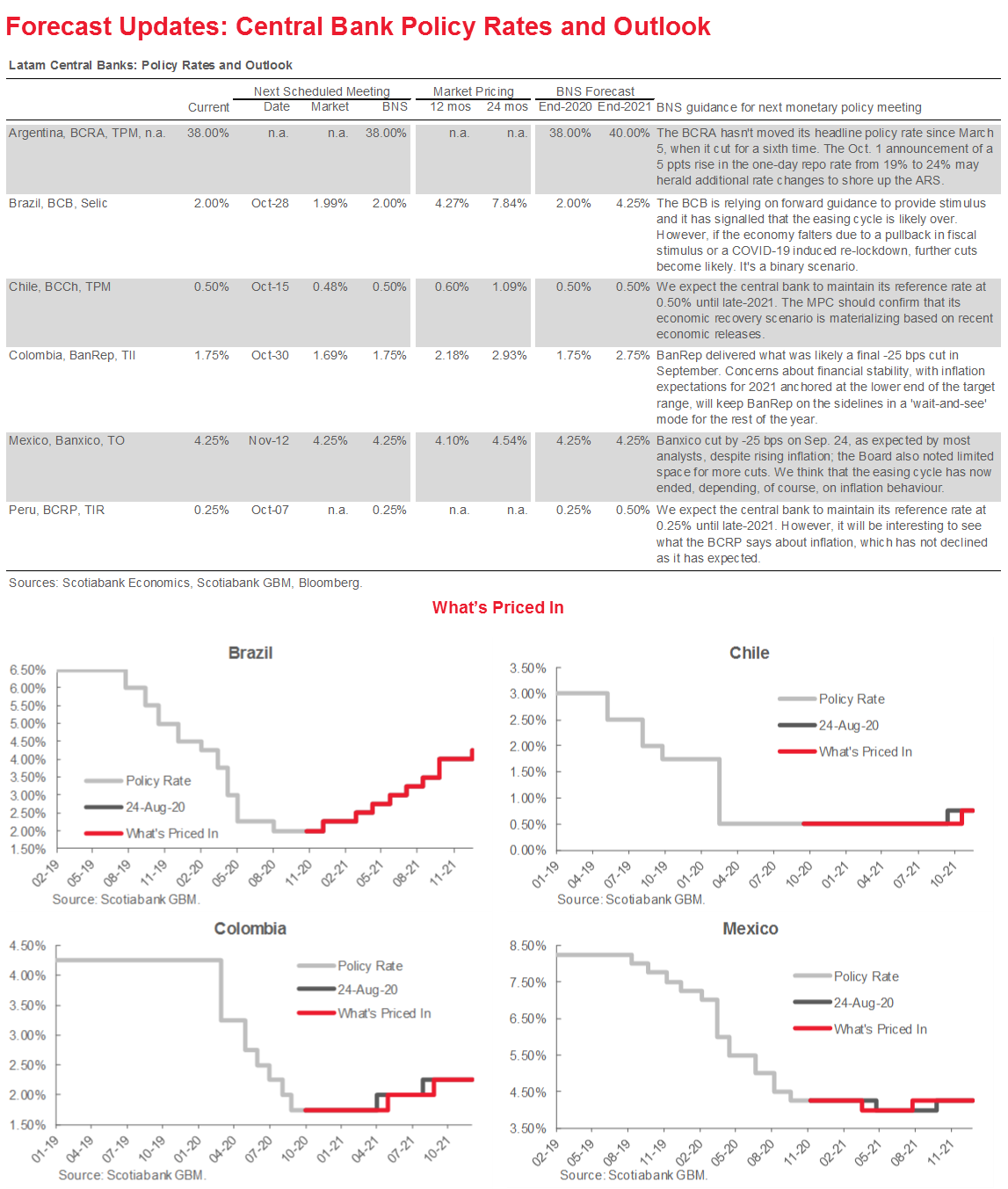

Pending monetary policy decisions are expected to result in a chorus of holds.

MARKET MOVES AND FINE-TUNING FORECASTS

After a strong start to the past week, risk assets stumbled on Friday’s news that US Pres. Trump had contracted COVID-19, which added to worries that the latest US stimulus package could remain stillborn ‘til after the November 3 vote. Across the EM FX complex, two-thirds of currencies were down on the week, but the Mexican peso led EM currencies with a 3.3% rise against the USD (table 1). Several of the Latam-6’s equity markets also managed to end the week on a positive note (table 2).

In response to recent data releases, we fine-tuned a few of our forecasts, which resulted in a marginal shift in our narrative only in Peru. After three consecutive months of upside inflation surprises from Peru in the midst of some unanticipated price stickiness, our team in Lima raised its inflation forecast for end-2020 to 1.5% y/y (previously 1.1% y/y) and end-2021 to 2.0% y/y (previously 1.5%). Still, their forecast profile for the BCRP’s policy rate remains unchanged, with a first increase pencilled in for Q4-2020.

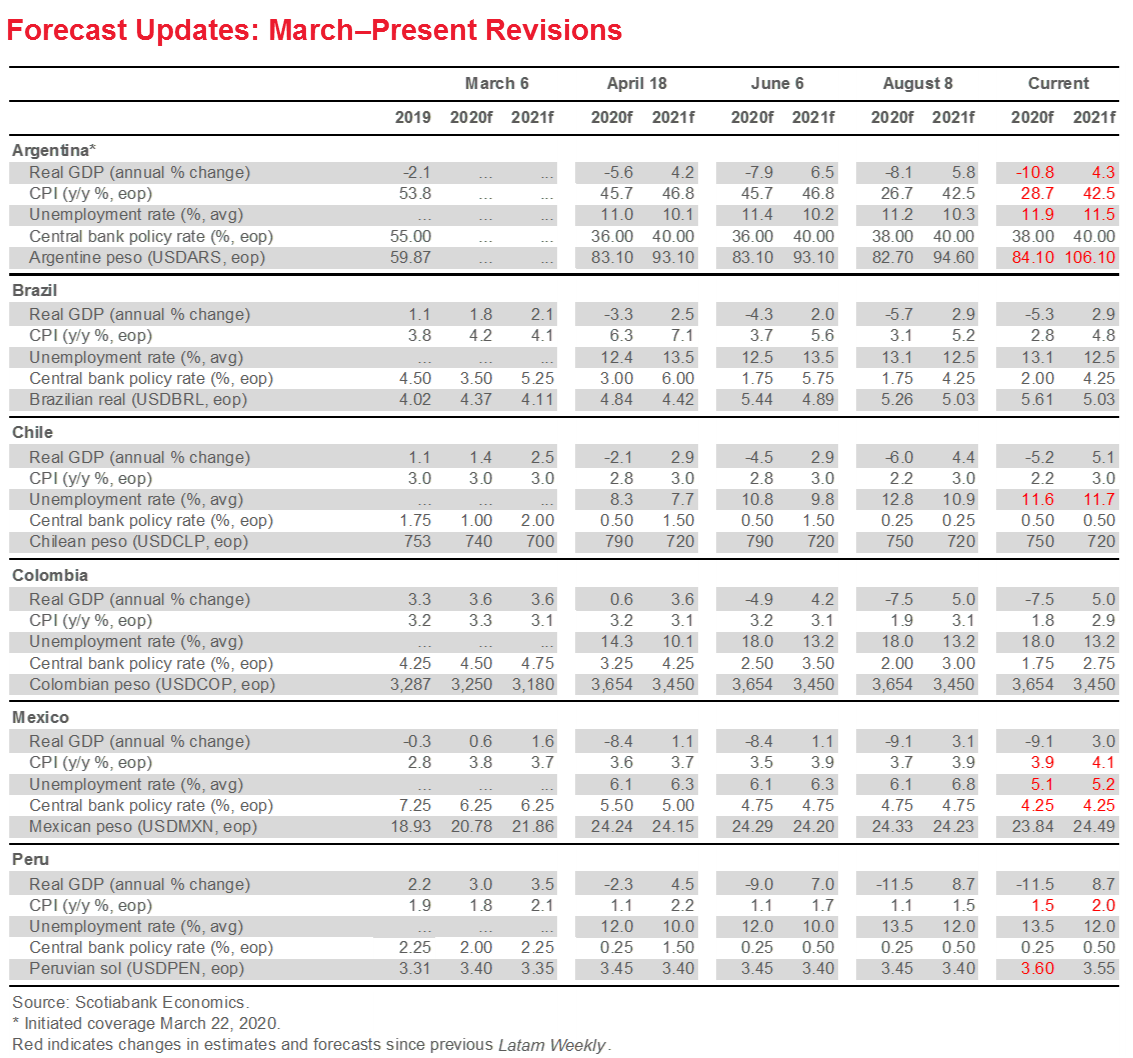

Otherwise, the forecast changes amount to housekeeping updates. In Argentina, we aligned our growth forecast with data tracking a slightly deeper downturn in 2020, shifting from -10.0% y/y to 10.8% y/y, and we muted the recovery in 2021 as we see mounting evidence that the authorities are not prepared to shift their policies to more sustainable stances. Also updating for recent data, we softened the employment outlook for Chile and improved a bit the unemployment outlook for Mexico. All of the forecast changes are summarized in the Forecast Tables on pp. 2 and 3.

ARGENTINA REMAINS A COVID-19 HOTSPOT AS THE OTHERS COOL

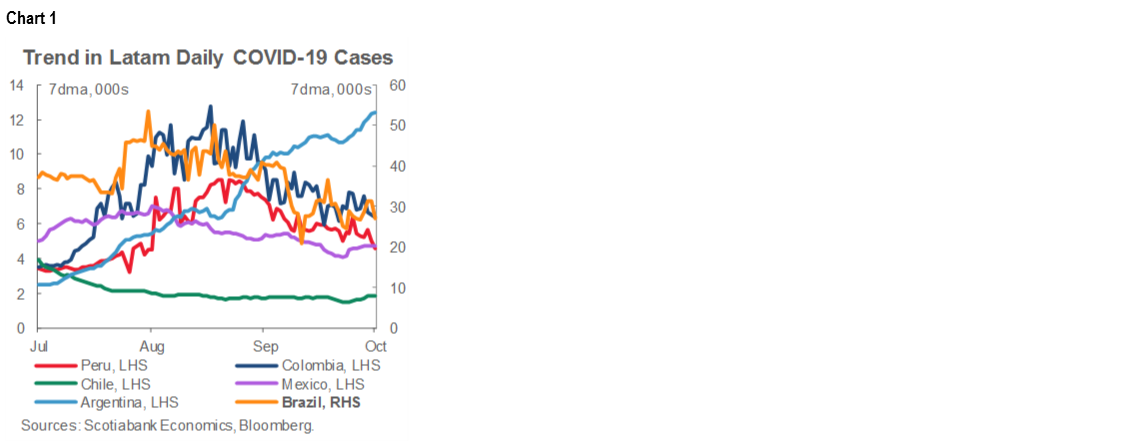

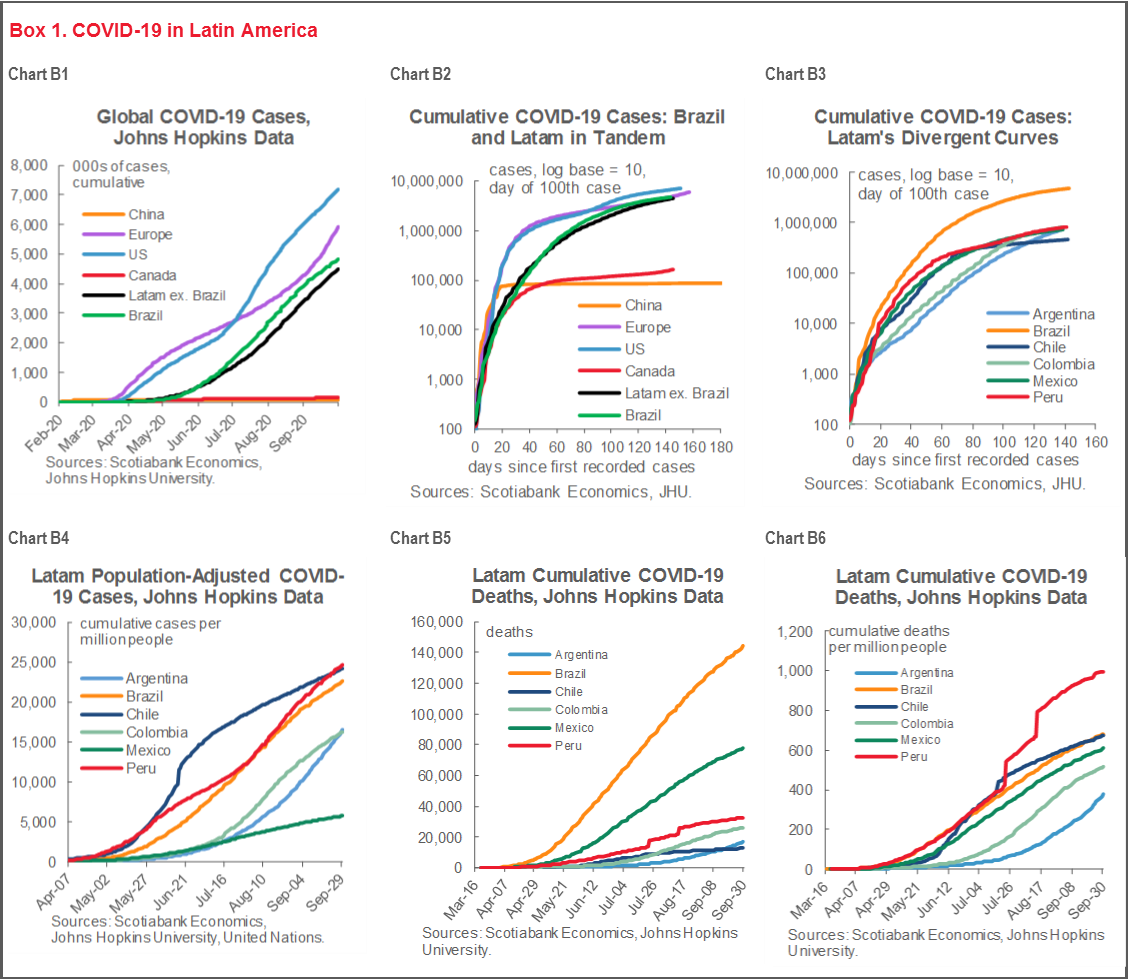

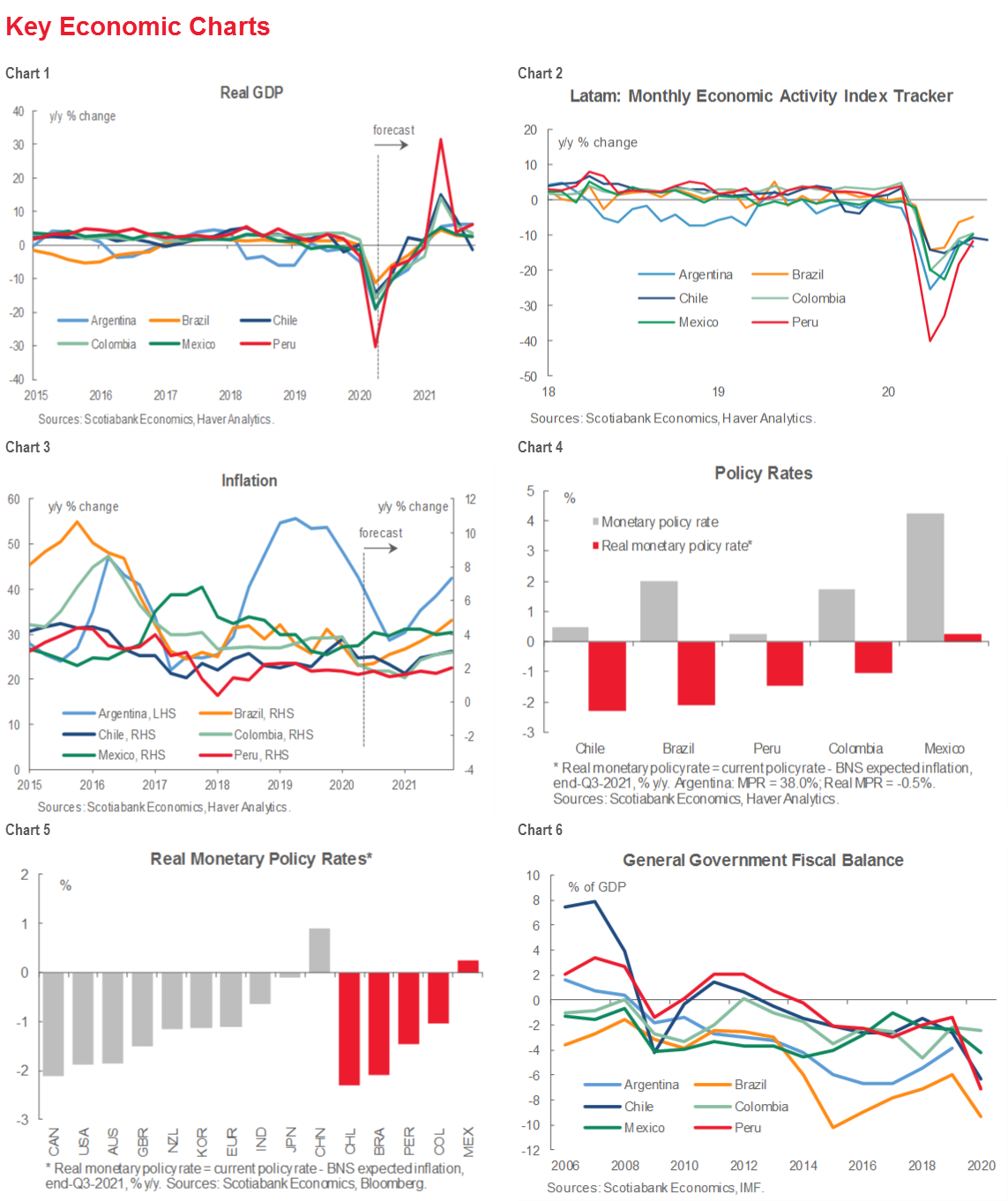

After months of depressing numbers that began to become background noise to markets, new COVID-19 trends across much of Latam have started to improve in recent weeks, and the longstanding regional hotspot has started to cool. Brazil, Colombia, Peru, and to a lesser extent Mexico, have posted marked reductions in new case numbers since mid-August, while Chile has remained steady after a surge in June–July (chart 1). Argentina is the only one of the Latam-6 that has seen a consistent rise in new cases since early-July.

Our standard panel of charts in box 1 implies that Latam’s COVID-19 situation is also starting to show some improvements relative to other major regions. Latam’s COVID-19 curves have started looking relatively flatter against the new surges happening in the US and Europe (charts B1 and B2). Within the Ltam region, both total and per capita COVID-19 curves have flattened a touch for five of the six Latam countries we follow, with Argentina being the obvious exception (charts B3 and B4). Argentina has the sad distinction of being the only country to show a steepening in its curves marking COVID-19-related deaths (charts B5 and B6), though late revisions in Peru keep nudging up its numbers too.

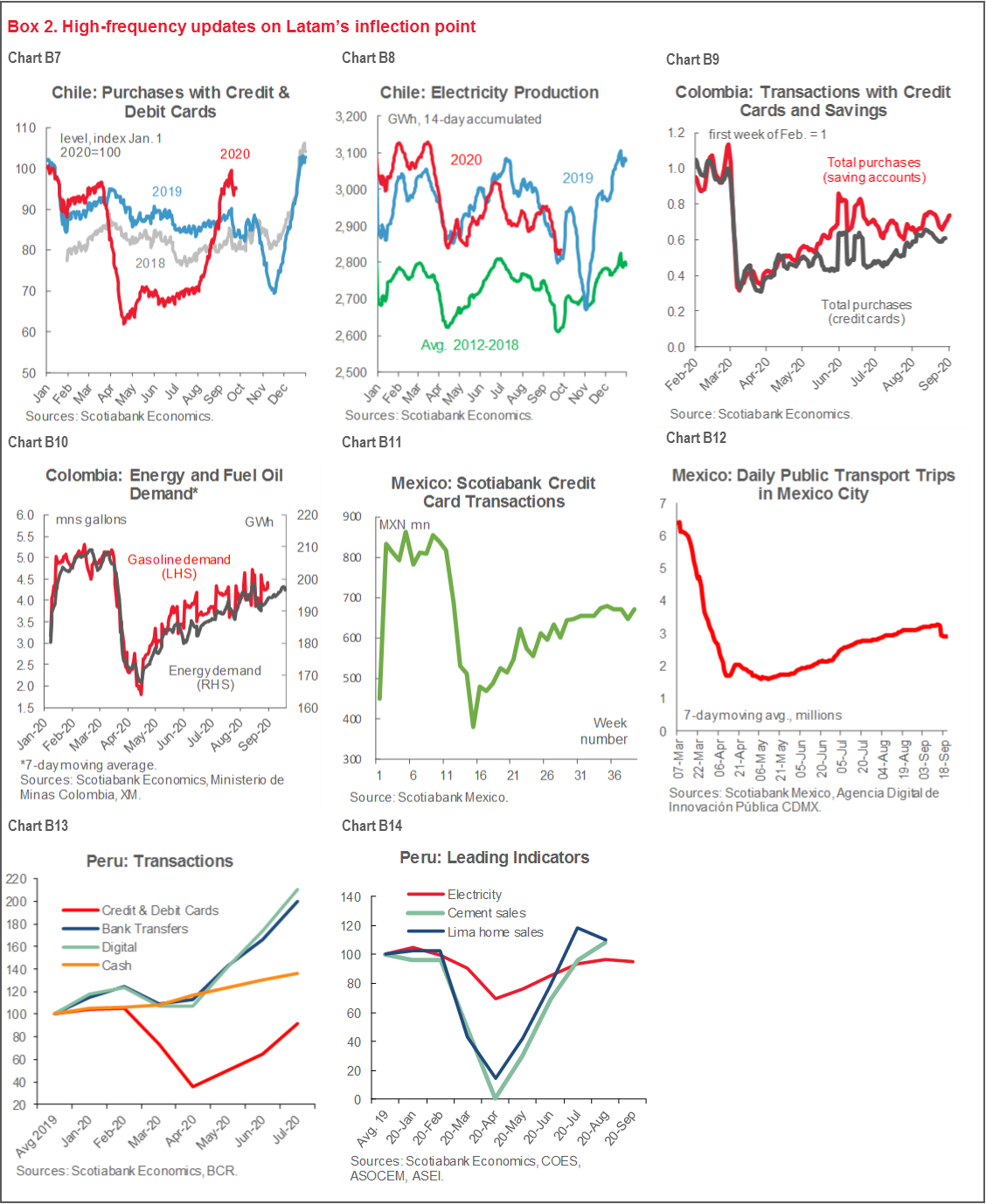

HIGH-FREQUENCY DATA SAY GROWTH MAY BE COOLING TOO

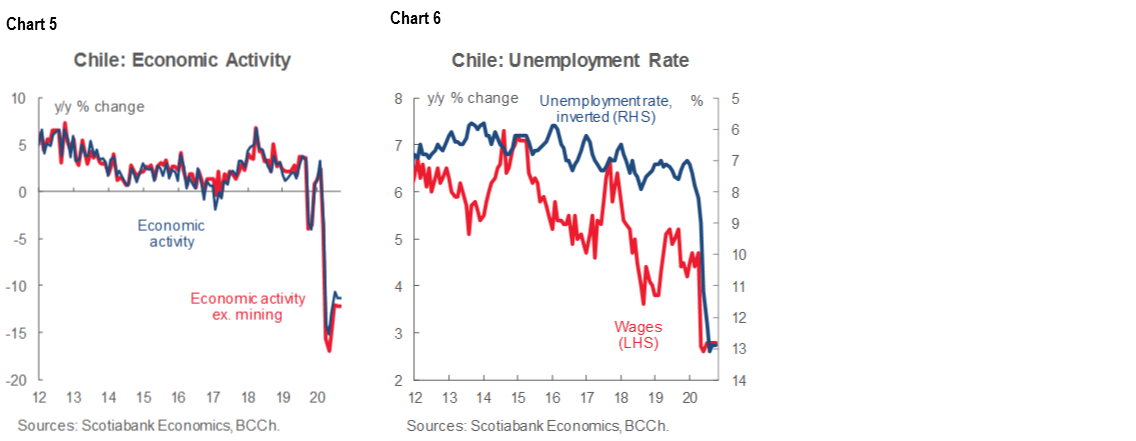

The recovery from the March–April lockdowns had been projected to show some strong initial gains followed by a harder grind as contagion control measures make re-opening some sectors harder than others. Data for August and September are starting to bear out these expectations with mixed readings. In the first of the Latam-6’s monthly GDP prints for August, country-wide growth stumbled in Chile, coming in under expectations and taking the comparison with 2019 down from -10.70% y/y in July to -11.33% y/y (chart 2). Across more timely, higher-frequency indicators, the recovery appears to be progressing, but its pace seems to be levelling off.

In box 2, we collect a range of Scotiabank proprietary and public data for the four Pacific Alliance countries that that paint a varied picture of the current pace of the post-lockdown recoveries.

- Chile. Despite August’s GDP stumble, Scotiabank Chile debt- and credit-card transactions volumes have fully recovered to volumes seen at the beginning of 2020, and are about 11% above levels in September 2019, likely reflecting both reduced use of cash and increased spending financed by pension-account withdrawals (chart B7). Electricity production got back to 2019’s seasonal levels in August and remains well above the lows that followed 2019’s social unrest (chart B8).

- Colombia. Scotia Colpatria data show that debit transactions were still only 71% of February’s levels by September 20, while credit-card transactions were at about 61% of pre-pandemic levels (chart B9). Growth in both appears to have flattened out after VAT holidays concluded and lockdowns tightened in some major cities. Energy and fuel-oil sales, however, continue to make steady progress, and are at 95% and 83% of pre-lockdown levels, respectively (chart B10). Colombia should see further pick-up in all of these series as its new approach to re-opening continues to be rolled out.

- Mexico. Credit-card volumes at Scotiabank Mexico have levelled out at about 78% of pre-pandemic levels and have remained there for several weeks (charts B11). Similarly, public transport trips have stalled at about 46% of their pre-pandemic numbers (chart B12). The plateauing in these high-frequency series may be an early sign of the impact of Mexico’s relatively limited fiscal measures in response to the crisis—and this is reflected in our 3% y/y real GDP growth forecast for 2021.

- Peru. Bank and digital transfers across the Peruvian financial system have soared, both by about 120% from the beginning of 2020 (chart B13). In contrast with most countries, even cash transactions have bounced, but credit-card volumes are still off by about 8% from early-2020 (chart B13). Cement and Lima home sales have fully recovered, and electricity demand is down by only about 5% from the 2019 average (chart B14). With the Phase 4 of re-opening underway, Peru is set to continue growing strongly into 2021.

RESERVE JUDGEMENT

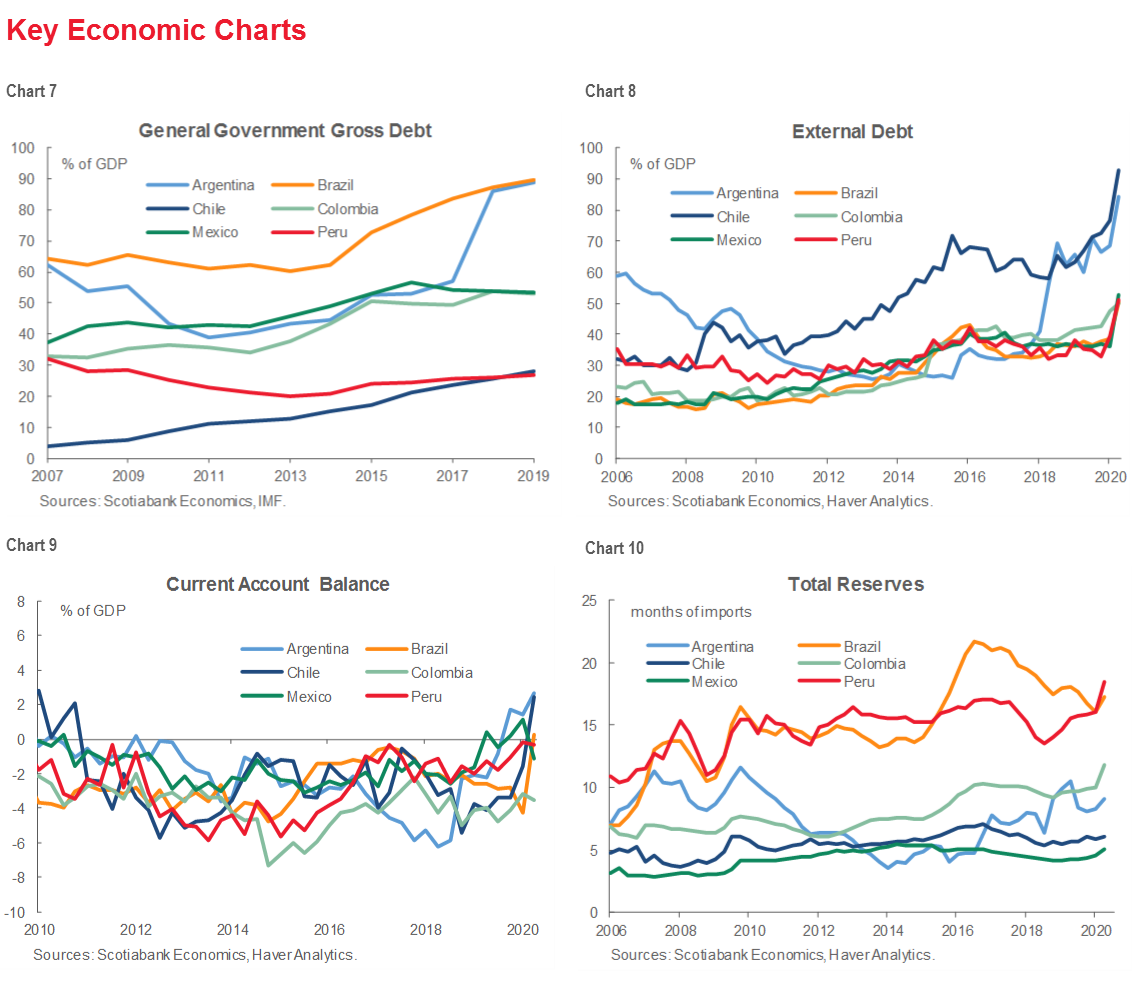

Latam’s major economies retain, in most cases, substantial reserve buffers that, even after massive fiscal stimulus, should leave them well placed to manage their external debt compared with other emerging markets (chart 3). Brazil, Peru, and Colombia have all built substantial FX reserves since the last global crisis, and even after drawdowns this year, Brazil has ample cover for its foreign debt. Mexico’s FX reserve accumulation has progressed over the last decade in line with the emerging-markets average.

Chile has typically placed less emphasis on building reserves owing to the protection provided by its large pension and sovereign wealth funds, but recourse is now more limited, with 10% of the pension funds being withdrawn to support consumption and the SWFs set to be largely drawn down this year. This will merit monitoring as the constitutional process unfolds later this month.

Argentina remains the outlier: it is slowly bleeding reserves, and is set to continue doing so as it tries to stop outflows through controls and boost inflows through temporary and inadequate policy sweeteners. Argentina still needs a deal to rollover—and likely expand—its debt to the IMF to make its external finance sustainable over the next few years.

CENTRAL BANKS: HOLD, HOLD, HOLD

As always, our monetary policy forecasts are summed up in our central bank table and charts on p. 4. We provide a deeper dive below on the key rate decisions and publications coming over the next two weeks, where the common theme is “hold”.

Peru. The BCRP’s Board is scheduled to meet on Wednesday, October 7. Our team in Lima along with a unanimous consensus of analysts expect the Board again to keep the reference rate on hold at 0.25% (chart 4). At its previous meeting on Thursday, September 10, the Board decided to maintain the reference rate at 0.25%, where it has been since the -100 bps cut on April 9. The September meeting was largely a non-event, with little news to report and no significant change in the Board’s characterization of economic conditions or its forward guidance. The Board continued to advise that it “considered it appropriate to maintain a strongly expansionary monetary stance for a prolonged period and so long as the pandemic’s negative effect on inflation and its determinants persist.” The Board also reiterated that it “stands ready to increase monetary stimulus through other instruments.”

Since the September meeting, conditions haven’t changed sufficiently to alter the Board’s stance or its outlook, particularly given that it just issued its last Inflation Report on Friday, September 18. The July economic activity indicator was still down -11.7% y/y despite a 7.5% m/m gain. Inflation surprised to the upside for the third month in a row in September, but at 1.8% y/y it remained below the 2% y/y target (chart 5) and on course to end 2020 at our current forecast of 1.5% y/y (see Forecast Tables, p. 2). Our team in Lima continues to see the reference rate on hold until Q4-2020 (chart 4, again).

Mexico. Banxico is scheduled to release on Thursday, October 8 the minutes from its most recent monetary policy decision on Thursday, September 24, where it unanimously moved to cut the target rate by -25 bps to 4.25%. The September decision marked an 11th consecutive cut by Banxico, for a cumulative -400 bps of easing since the beginning of the cycle. Analysts had expected a mix of votes in view of the risks around inflation, economic activity, and financial markets. Despite the unanimity of the decision, the Board`s relatively short statement emphasized four points, that in the view of our team in Mexico City, point to a hold from here: (1) the balance of risks for inflation remains uncertain; (2) growth risks are skewed downward; (3) advanced economy central banks are set to maintain accommodative policies; and (4) the remaining room for more cuts in Mexico is limited.

Still, the minutes should provide some important colour on the breadth of Board Members’ views on growth, inflation, the country’s fiscal stance, financial stability, and the balance of both domestic and international risks. The minutes may also provide a granular view of how the Board is split between those who see rates on hold going forward, and those who see the possibility of more cuts ahead.

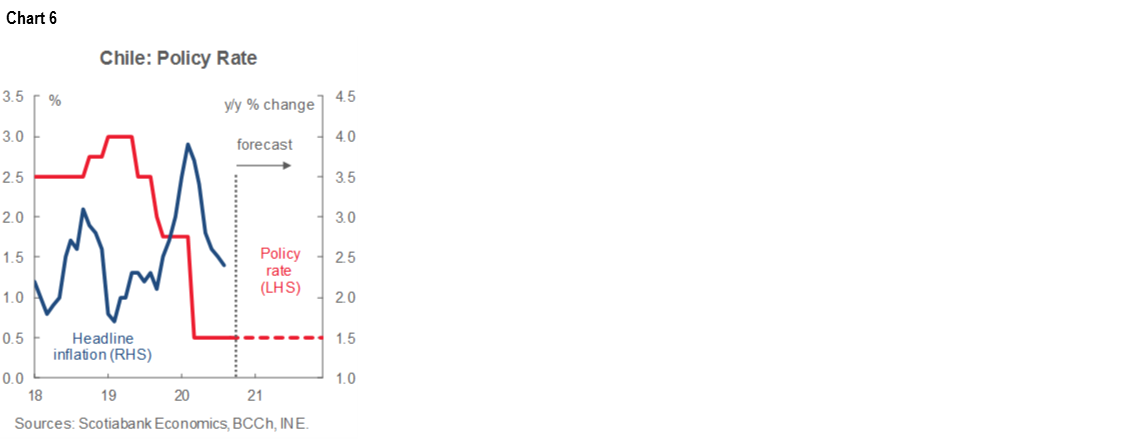

Chile. The BCCh’s Board meets again during October 14–15 and is widely expected to keep its benchmark monetary policy rate on hold at its “technical minimum” of 0.5% (chart 6). At its last meeting on September 1, the Board unanimously decided to maintain the policy rate at 0.5%, where it has been since the Board’s -50 bps cut on March 31. In its statement, the Board observed the emerging stabilization in growth after the June–July bounce, and noted its concern with the labour market’s deterioration and the slowdown in consumer credit growth. In line with its confidence in the recovery and more muted disinflationary pressures (chart 7), the Board indicated that the policy rate would remain at its technical minimum “for a large part” of its forecast horizon, somewhat tighter than its previous indication that it would stay on hold for a “prolonged period”. This could have indicated some improvement in the Board’s reading of Chile’s data, but it didn’t augur for any immediate move given ongoing risks. The ensuing publication of the September Monetary Policy Report confirmed an upgrade in the BCCh staff’s growth forecast range for 2020 from -7.5/-5.5% y/y to -5.5/-4.5% y/y. However, our team in Santiago sees the better part of this range as hard to reach after the August’s weaker-than-expected economic activity reading.

Our Chile economists expect that a slightly downbeat reading on current and near-term economic conditions will accompany a Board decision to hold. We will also be looking for a possible delayed update of the Bank’s annual estimates of Chile structural macroeconomic parameters in coming meetings.

MACRO DATA & RISK EVENTS

Key macro data prints coming over the next two weeks are highlighted and discussed for each country in the Country Updates section that follows the Markets Report. See the back of the Latam Weekly for a summary risk calendar for events during October 4 through 16.

USEFUL REFERENCES

Agenda and registration for the virtual 2020 IMF-World Bank Annual Meetings (events begin October 5): https://meetings.imf.org/en/2020/Annual

Agenda and registration for the 2020 IIF Annual Membership Meeting (Live-Stream, October 12–16, 2020): https://www.iif.com/Events/Meeting-Home-Page?meetingid={C86F7616-C06A-EA11-80E6-000D3A0EE828}

Markets Report: A Timeline for Chile’s New Constitution and its Potential Impact on Chilean Assets

Tania Escobedo Jacob, Associate Director

212.225.6256 (New York)

Latam Macro Strategy

tania.escobedojacob@scotiabank.com

With contributions by Jorge Selaive and Brett House.

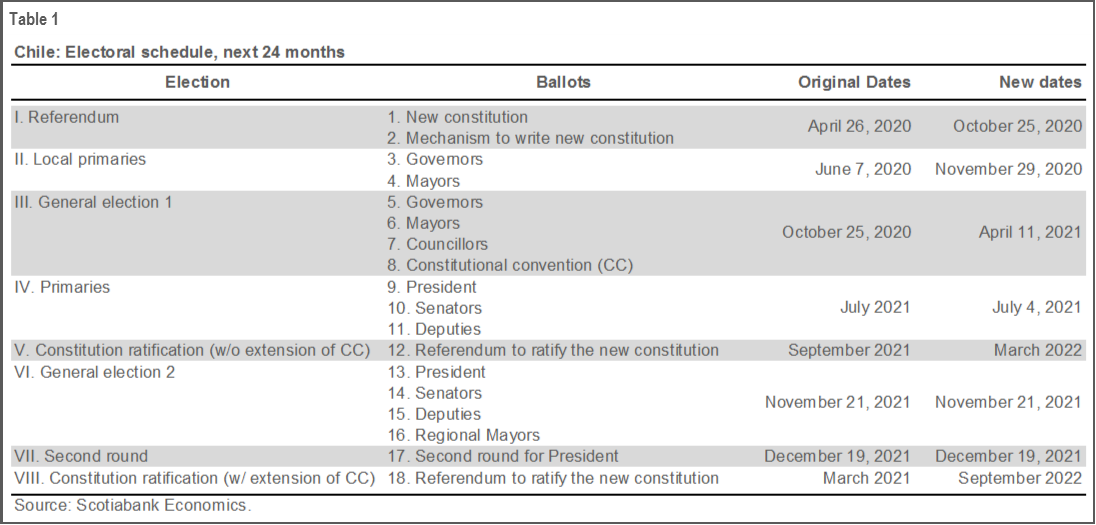

On October 25, Chileans will decide whether or not to re-write their Constitution and the process by which to do so.

We are not expecting a huge deviation from the current institutional framework, but we do anticipate structurally higher levels of public spending that could complicate the fiscal picture in the years to come, taking into account that we are starting from a much weaker point now relative to 2019.

We see space for an additional risk premium in Chilean assets as we go through the long process to write the new constitution.

The Central Bank and the Ministry of Finance could put a lid on any disorderly sell-off in Chilean assets, but we do not think that they will pursue specific levels for yields or spot rates if they run counter to a fundamental re-pricing of risk premiums.

CHILE: A TIMELINE FOR THE NEW CONSTITUTION AND ITS POTENTIAL IMPACT ON CHILEAN ASSETS

On October 25, Chileans will decide whether or not to re-write their constitution and the process by which to do so. Please see table 1 the annex at the end of this section for Chile’s electoral calendar and explanatory details. In general terms, we are not expecting a huge deviation from the current institutional framework. For example, the autonomy of the Central Bank is expected to remain untouched. We do, however, anticipate structurally higher levels of public spending, including larger subsidies in housing, health, education. This could complicate the fiscal picture in the years to come, taking into account that we are starting from a much weaker point now relative to 2019.

WHAT DOES THIS MEAN FOR FINANCIAL MARKETS?

We think markets are underpricing the political risk implied by the constitutional referendum and the long process that will follow.

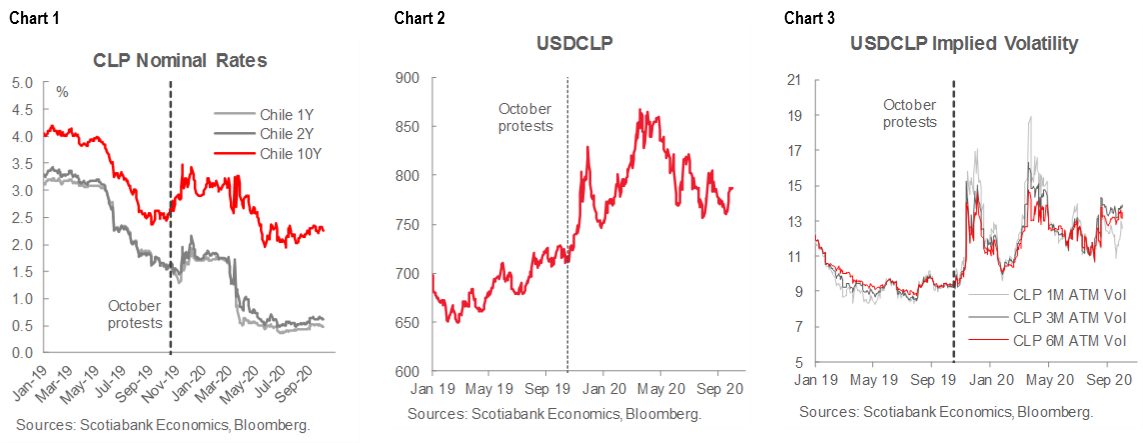

Back in October 2019, the reaction of rates and FX to the escalation of the social protests was sizeable, with short-term rates rising about 80 bps and the 10Y rate widening up to 100 bps (chart 1). The CLP also had a violent reaction, depreciating 15% in the month that followed the first violent protest (chart 2). FX volatility climbed up to 6 ppts as political uncertainty intensified and the idea of a new constitution shook the markets (chart 3).

In 2020, there are significant differences from what we saw in October of last year. The most important change is that the referendum has been on everyone’s radar for almost a year and the market has fully incorporated the scenario where a new constitution will be written. Still, looking at the relative performance of the CLP versus its peers (chart 4), we think there is some degree of complacency around how smoothly the process will go.

The economic crisis might have deepened the perception of inequality. Chile, like the whole world, is going through an unprecedented economic crisis and labour-market shock (chart 5 and 6) that has significantly undermined the disposable income of Chileans. This has increased discomfort among the population despite the efforts of the government to implement social programs.

Market participants are anticipating that protests will be limited by the pandemic but— based on what we have seen recently in countries like Colombia and Mexico—the threat of the virus might not be enough to prevent some crowded demonstrations that might once again get violent.

There is very little cushion to finance large or unexpected changes in fiscal needs. Back in July, the Chilean Congress unexpectedly passed a law that allowed withdrawals of up to 10% from the pension fund system, which took most political analysts and economists by surprise. The impact in the market was not as significant as the Executive anticipated but, politically, it did set a negative precedent, in our view. The Ministry of Finance appeared to have little influence on the decision to authorize the withdrawals, which may have opened a door to more “unorthodox” proposals finding their way into a new constitution even with the requirement of approval by a two-thirds supermajority.

At the same time, the space for more “expensive” reforms is much smaller than it was in 2019, when there was a perception that the government was able to accommodate a fair share of social demands in its spending agenda. Now, after the huge fiscal impulse implemented to mitigate the health and economic effects of the COVID-19 pandemic, Chile’s sovereign wealth funds are almost depleted: only USD 10 bn are left in the SWFs and we are expecting the government to use all of this by the end of 2021. Deficits are expected to balloon to almost 10% of GDP in 2020 and 5% in 2021.

The new constitution could engender substantial structural financial needs for the foreseeable future. The USD 12 bn we are anticipating for bond issuance in 2021 is about 30% higher than the annual amounts we have seen in Chile in recent years, where the cap did not usually surpass USD 8 bn. The higher amounts are in line with the increase in the financing needed to cover the larger deficits ahead—a trend that we think will continue in the coming years.

As we move forward, our economists in Santiago are forecasting an increase in the debt/GDP ratio from the 26% seen in 2019 to 48% in 2023. This would be driven by the fiscal package implemented to boost the economy in response to COVID-19 and the extra spending that resulted from the social protests of 2019. Constitutional considerations could push these numbers higher.

The constitutional referendum scheduled for a few weeks from now on October 25 and the presidential elections coming in 2021 will keep pressure on the government to continue spending. This should leave very little room to find a credible path to fiscal convergence in the medium-term and an increased likelihood of sovereign rating revisions in the coming months. We continue to see pronounced risks of a 1-notch sovereign credit risk downgrade unless a better fiscal consolidation plan is delivered during the next few quarters and/or we see significant positive economic and political surprises.

Taking all of this into account, we see space for an additional risk premium in Chilean assets as we go through the long process to write the new constitution. The spike in political noise and social discomfort added to structurally higher financing needs and the depletion of the sovereign wealth funds will, in our view, maintain the upward trend of issuance in the coming years, validating a higher risk premium in Chile’s yields. If realized, steepeners in the belly of the BTP curve and payers in the longer end one tend to perform.

In FX, we also think there is space for a weakening of the CLP to levels slightly above the USDCLP 800 mark as a first target. This would be a much milder move relative to what we saw in October 2019, in part because 2019’s social unrest and the constitutional process might already priced into current CLP levels.

We acknowledge that the Central Bank and the Ministry of Finance are able to put a lid on any disorderly sell-off in Chilean assets, but we do not think that they will use sovereign bond purchases or USD sales to cap yields or FX spot rates that reflect a fundamental re-pricing of risk premiums.

Annex 1: Details on key dates in Chile’s electoral calendar

I. October 25, 2020: Constitutional referendum

The ballot will pose two questions:

1. Do you want a new constitution? (Yes/No)

2. If you answer is “Yes”, who should be in charge of writing the new constitution?

- A mixed constitutional convention, i.e., 50% parliamentarians, 50% people elected solely for this purpose; or

- A constitutional convention, i.e., 100% people elected solely for this purpose.

Current polls point to an overwhelming “Yes” on the first question and a win for the popular “constitutional convention” on the second question.

“Yes” on the first question will mean that a new constitution will be written completely from scratch—from a blank page, not by making amendments to the existing document.

Why does the mechanism matter? A fully elected constitutional convention (CC) could result in some “overrepresentation” of social sectors that have been heavily involved in recent protests, which could skew the document that results from their deliberations.

II. April 2021: Elections for the members of the constitutional convention

In principle, political parties are meant to propose candidates and members of the convention will be elected by proportional representation (i.e. the percentage of seats each party gains in the constitutional convention would reflect the percentage of people who voted for that party). If this is the case—given the current general political trends and numbers in Chile—there is very little risk of a wave of extreme left or extreme right voting, even after the recent social turmoil.

Given the current crisis, however, there are strong voices calling for an alternative process that could extend representation beyond the major political parties. If this position prevails, it could open the door to the participation of independent candidates, such as social activists and union leaders, who are currently banned from the process.

In any case, as things stand, any article proposed will have to be accepted by a two-thirds majority, which also limits the space for “extreme” proposals to make their way into the new constitution.

The constitutional convention will be elected for 9 months with the possibility of a 3-month extension.

Our take: Despite the noise that will surely come as the convention’s electoral process takes shape, we think that the constitutional convention will end up being a balanced body without a disproportionate representation of extreme political views. Hence, we are not expecting a huge deviation from the current institutional framework.

III. 2022: Ratification of a new constitution

Any new constitution would have to be ratified in an additional referendum, likely in early- or late-2022, as laid out in table 1.

COUNTRY UPDATES

Argentina—Wishful Thinking and Doing

Brett House, VP & Deputy Chief Economist

416.863.7463

brett.house@scotiabank.com

Argentine policymakers continue to adjust their fragile policy framework in a quixotic effort to stem reserve loses, shore up the ARS, and boost USD inflows without addressing the root causes of these challenges.

On Thursday, October 1, the authorities announced a suite of measures intended, in their words, “to stimulate production and exports.” On the tax side, these included:

- Reductions in taxes on metal and mineral exports from 21% to 8%;

- Immediate steps to lower exports on soy beans, meal, and oil in order to push farmers to sell and export products that have been stockpiled from the last growing season. The rates will edge up from 30% in October and return to their previous 33% level in January; and

- Export taxes on some industrial goods will be brought down to zero.

These changes are unlikely to spur either exports or USD inflows when miners, farmers, and manufacturers rightly anticipate that larger devaluations are ahead for the ARS. While the peso continues to gradually slide in value, the current USDARS 76 official cross rate is nowhere near the USDARS 146 level being fetched in the blue-chip swap market. With Argentina’s monetary base set to close 2020 about 42% larger than it ended 2019, minor tinkering with export taxes won’t be enough to induce exporters to stop waiting for the ARS to fall further. Moreover, these changes fail to address a bigger underlying problem: export taxes make no sense in a country that is bleeding reserves and needs to generate FX inflows.

At the same time, the BCRA also announced new guidelines for its conduct of monetary and exchange-rate policy that, despite intentions to the contrary, tended to validate exporters’ expectations that a weaker ARS is ahead. The new decisions include:

- Abandonment of the uniform devaluation mechanism that has allowed the official peso to weaken by about 2.5% a month in favour of a managed float that will permit more FX volatility and, it is thought by central bank, thereby dampen demand for hard currency. Arguably, this will engender even greater upfront demand for USDs;

- A move in the one-day repo rate from 19% to 24% to increase deposit rates and enhance the attractiveness of local ARS financial instruments;

- Authorization of FX futures in RMB to facilitate trade with China, with an explicit warning that this measure should not be used to hoard RMB. The BCRA advised that it would not tap its swap line with the PBOC; and

- Direct foreign investments into Argentina will be allowed to repatriate capital from their first year, which means little since this access is permitted only through the official market.

These tax, monetary policy, and FX measures imply that the authorities intend to continue tweaking the edges of their framework rather than move to a more sustainable policy stance. If they truly wanted to unlock new financing from the IMF, boost exports, and increase net FX inflows, they would move to a more sustainable set of fiscal policies and allow a swift depreciation of the peso. Negotiations with the Fund aren’t likely to be easy or quick.

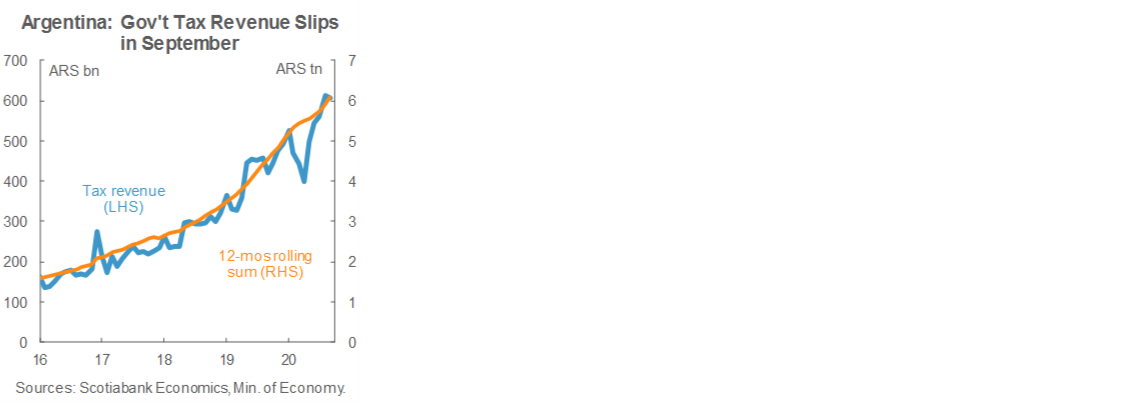

In data out Friday, October 2, government monthly tax revenue slipped from ARS 612 bn in August to ARS 607 bn in September (chart). While a minor setback amidst what was still a 44% y/y increase from September 2019, the collections data underscore the urgency behind the policy changes outlined above. Ciara-Cec, the agricultural chamber, also announced on Friday that crop exports were in September were down -15% y/y and down -13% y/y for the YTD.

In the fortnight ahead, our main focus will be on September inflation data out on Wednesday, October 14: base effects should continue bringing down the annual headline number from 40.7% y/y in August to between 35.5% y/y and 36.8% y/y (i.e., between 2.0% m/m and 3.0% m/m, keeping sequential inflation steady). Real-economy indicators out on Monday, October 5 (September vehicles data) and Wednesday, October 7 (August construction and industrial production) should show further waning in the pace of the recovery owing to extended lockdown measures. COVID-19 numbers have surged in Argentina, in marked contrast to the rest of Latam.

Brazil—Too Much Reliance on the BCB Could Generate Cracks in the Ship

Eduardo Suárez, VP, Latin America Economics

52.55.9179.5174 (Mexico)

esuarezm@scotiabank.com.mx

The BCB has made a valiant effort to prop up the Brazilian economy during the current crisis, cutting the Selic rate by -175 bps since April when the COVID-19 shock properly landed in Brazil, for a total easing of -450 bps since mid-2019. Faced with the dilemma of an economy that is still on very shaky ground from a growth perspective, the coming expiry of the COVID-19 fiscal stimulus over the next quarter, below-target inflation, and—on the other hand—a very vulnerable fiscal situation, the BCB decided at its September 16 Copom meeting to stop cutting the Selic to reduce risks of financial instability and it introduced forward guidance.

At the IMF Annual Meetings in Lima (October 2015), Agustin Carstens was on a panel where he discussed his views on forward guidance. He said that rather than forward guidance, he leaned towards using “conditional guidance” (i.e., outlining how he would react to a certain scenario, rather than tying his hands with an unrestricted commitment), as he could not commit to a path where so many variables are outside his control. Part of the issue is that a core central bank such as the Fed has a much greater power to affect an outcome than an EM central bank does, including the capacity to influence the risk appetite of markets. There are also differences in the fiscal constraints faced by a reserve currency country, and one without that privilege. In addition, there are also the arguments discussed by Carlos Vegh, about the positive correlations between adverse shocks and inflation in emerging markets (i.e., recessions often coincide with inflation shocks), as well as the headaches EMs generally face in their currency markets during crises. Basically, it is not clear that an EM central bank has the capacity to be successful with forward guidance.

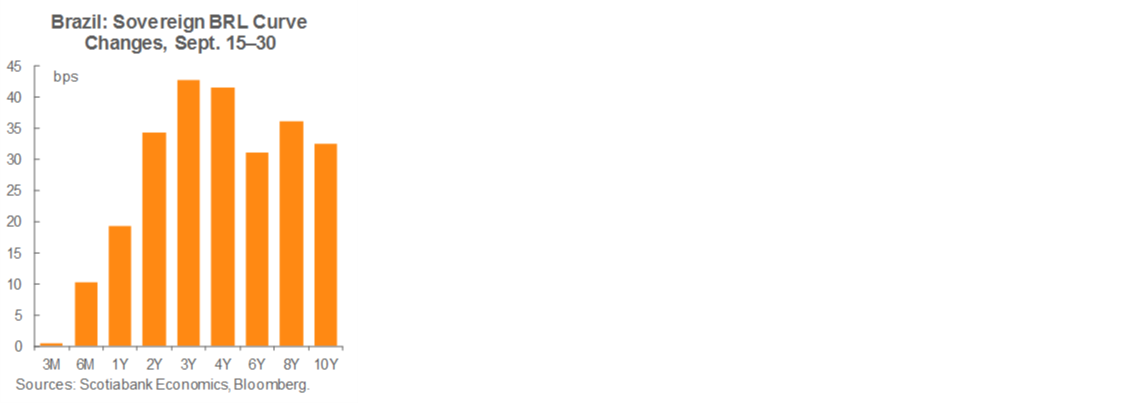

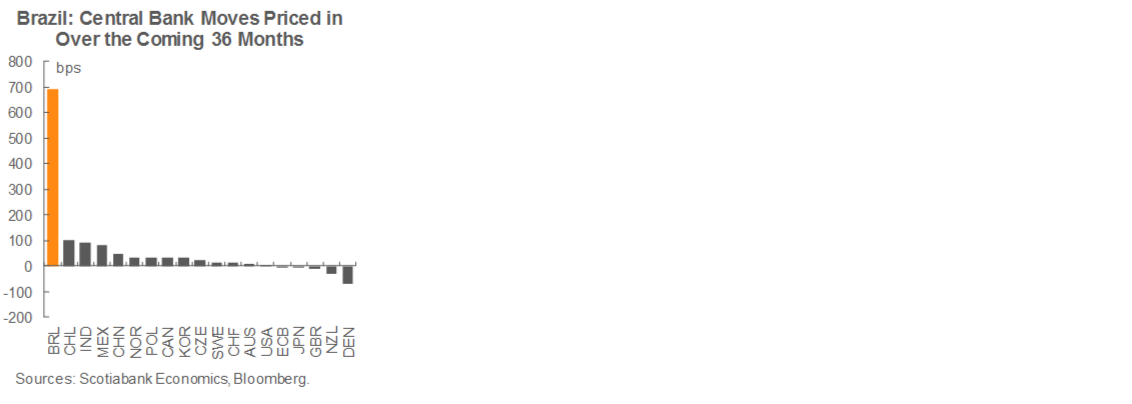

The BCB currently not only has to contend with the external uncertainties, but also with the budget dynamics of Brazil, where fiscal sustainability is vulnerable. Since the BCB’s introduction of forward guidance to provide additional stimulus by pledging rates will remain low for longer, the country’s yield curve has steepened by about 40 bps (first chart). This likely does not reflect market doubts regarding the BCB’s intent. but is rather a reaction to the lack of progress in solving Brazil’s fiscal woes which, in turn, could undermine the BCB’s capacity to keep rates low for long. DI rates are pricing in over 500 bps of hikes in the Selic rate over the next 24 months, directly questioning the BCB’s capacity to stick to its forward guidance (second chart). These concerns are part of the reason why we have a more marked “V” shaped pattern in our Selic rate path than consensus.

We see a binary scenario ahead:

- If the economy does not face another decline owing to the end of stimulus or a relapse into lockdown, either domestically or abroad, we see rates on hold for the short term (i.e., 6–12 months).

- Alternatively, if the economy does decelerate again, and given that fiscal space has now been largely exhausted, we expect the BCB to be forced to cut rates further.

However, under either outcome, we would tend to have an earlier and steeper rate-hike cycle for the BCB. We see fiscal constraints forcing the BCB to tighten the Selic rate earlier and possibly more steeply than consensus anticipates.

Chile—Recovery Slows, but Policy Steps Up

Jorge Selaive, Chief Economist, Chile

56.2.2939.1092 (Chile)

jorge.selaive@scotiabank.cl

Carlos Muñoz, Senior Economist

56.2.2619.6848 (Chile)

carlos.munoz@scotiabank.cl

On Sunday, September 27, Pres. Piñera announced an employment plan that will benefit new hires and the re-instatement of suspended workers, in a context where 97% of the population of the Metropolitan Santiago Region are now free from quarantine measures and able to go back to work. The initiative is focused on generating more job opportunities, especially for women, young people, and workers with disabilities. The Piñera Administration estimates that the plan will require USD 2 bn in funds.

On Tuesday, September 29, Pres. Piñera announced the Budget Law bill for 2021. The bill includes a 9.5% y/y increase in government spending with respect to the adjusted 2020 Budget Law, which would imply an effective fiscal deficit of -4.3% of GDP and a structural fiscal deficit of -4.7% of GDP (versus -9.5% and -3.5% in 2020, respectively). The Ministries that would experience the highest spending growth are expected to be Public Works (up 33.4% y/y), Labour (rising 24.6% y/y), and Housing & Urban Affairs (up 18.1% y/y). Recall also that 2020's budget included resources from a Transitory Emergency Fund, which amounted to USD 5.2 bn. The budget for next year is consistent with a medium-term public spending trajectory that assumes a path of convergence which would close the structural deficit by 2024 and would stabilize sovereign debt at 45% of GDP.

In data received on Wednesday, September 30, the national unemployment rate fell to 12.9% in the moving quarter ended in August, down from 13.1% in the previous moving quarter to July and positively surprising the market, which expected around 13.6%. This print was explained by a somewhat greater improvement in employment than that registered in the active labour force, both of which reduced their rate of annual contraction to -19.4% y/y and -14.5% y/y, respectively. Along these lines, the employment rate increased slightly to 45.7%, reversing the downward trend shown from March to July.

Finally, on October 1, monthly GDP data for August were released. Activity fell -11.3% y/y, showing a monthly expansion of 2.8% m/m which would lead Q3-2020 to a contraction of about -9% y/y. This print was influenced by a slow recovery in services, particularly business services linked to investment. In any case, the recovery of activity continues, with August being the third consecutive month with increases in both total GDP and non-mining activity (chart). There is little doubt that we are in recovery, but the high optimism seen weeks ago is stumbling a bit.

Looking ahead, on October 8, inflation data for September will be published. We forecast that inflation will rise from 0.1% m/m (2.4% y/y) in August to 0.3% m/m (2.7% y/y) in September, in line with the consensus in the Survey of Financial Operators (0.3% m/m), but higher than the consensus in the Survey of Economic Expectations (0.2% m/m). The main positive contributions for the month should come from some food products, such as tomatoes, beef, and pork. Additionally, after seven months of declines, September would be the first month to show a positive change in gasoline prices. All in all, though, we maintain our projection of annual inflation of 2.2% y/y in December 2020.

Next, on October 15, the BCCh will hold its October monetary policy meeting. We expect the Board to maintain the overnight rate at 0.5%, its technical minimum. We anticipate that the Board will indicate that its economic recovery scenario is materializing, albeit at a slower pace than expected after August’s GDP print. The chances that GDP growth for 2020 as a whole will land in the better part of the BCCh’s baseline scenario forecast range (-4.5/-5.5%) are declining. In this context, we do not expect a completely optimistic reading of the outlook —with the Board likely giving an account of the lag in services and investment, activity, while also noting that employment has finally shown some positive signs.

Colombia—Labour Recovery is Key for GDP Recovery

Sergio Olarte, Head Economist, Colombia

57.1.745.6300 (Colombia)

sergio.olarte@co.scotiabank.com

Jackeline Piraján, Economist

57.1.745.6300 (Colombia)

jackeline.pirajan@co.scotiabank.com

COVID-19 will leave a long-term mark on both global GDP and Colombia’s economy. According to the IMF, the world economy will lose USD 10 tn this year (i.e., the equivalent of close to 75% of China’s GDP) due to the virus outbreak. The global labour market recovery will significantly determine the outlook for economic activity. Therefore, deeper damage is likely to be incurred mainly in those countries where labour markets—particularly in the formal sector—do not rebound quickly. The reasoning behind this is as follows: (1) a higher unemployment rate means lower disposable incomes and, therefore, lower household consumption; and (2) slower formal labour-market recovery reduces productivity, which directly hits potential output. Colombia has been characterized as having an unusually high unemployment rate and a high degree of informality. In fact, before the COVID-19 shock, around 60% of the nationwide labour force was informal and about 48% of urban labour was informal. At the same time, the unemployment rate last year was a bit above 10%, well above the Pacific Alliance average (5.7% in 2019). All of this will make it hard for Colombia to get back on its pre-COVID growth path in the coming years (first chart).

After the COVID-19 outbreak, the Colombian nationwide unemployment rate has doubled and employment creation has fallen by around 17% y/y. In April, the month most impacted by the curfews, the Colombian economy lost more than five million jobs, especially in commerce, manufacturing, leisure, and construction. After the government eased mobility restrictions and allowed more activities to resume, employment has seen some gains, especially in the agricultural sector (450,000 new jobs), construction (260,000 new jobs) and commerce (210,000 new jobs). However, the speed of job gains has been slow, and this could jeopardize GDP growth in 2021. The reasons for the slow-motion path to labour recovery are:

1. Economic re-opening has been slower by delays in Colombia’s major cities;

2. Uncertainty about the future prevents companies from thinking about the long run and expanding their employment ranks (second chart), thereby delaying the recovery of household consumption and confidence; and

3. Colombia has very inflexible labour legislation that does not allow companies and people to restore jobs quickly, which also tends to foment informality.

Resolving the first two issues will depend on re-opening strategies that, after October, will speed up in Colombia. The industrial confidence index is already in positive territory and consumer confidence has touched its bottom, especially since household expectations about the economy have improved. Additionally, September's significant re-opening of economic activity helps companies and commerce advance and improve labour demand. However, these efforts will likely yield only partial results since the labour market's inflexibility will stymie further hiring in the formal parts of the economy. For these reasons, we do not expect the unemployment rate to recover to pre-COVID-19 levels next year and this will negatively affect potential output. In our base-case scenario, economic activity recovers gradually and the unemployment rate will still be above 14% at the start of 2021 and average 13.2% for the year. GDP next year will be a bit higher than 2017 levels and is set to stay below its pre-COVID-19 trend over the forecast horizon.

In our view, the only way to speed up the economic recovery would be through a package of Congressional reforms that would make employment more flexible, increase labour mobility, and reduce extra labour costs. As an example, the monthly minimum wage in Colombia is currently ~COP 920,000 (USD 237). However, a company’s actual costs associated with paying the minimum wage are much higher, at COP 1,480,000 (USD 381)—60% higher than the minimum wage itself. This represents a wide margin for improvement. If Colombia could make it simpler and less costly to hire people, it could spur investment, hiring, and growth, thereby creating a virtuous circle that would sustain higher potential GDP.

Mexico—Turbulence Could Lie Ahead

Mario Correa, Economic Research Director

52.55.5123.2683 (Mexico)

mcorrea@scotiacb.com.mx

We are entering the final quarter of the year and a new stage in the COVID-19 economic crisis, during which economic information will be contrasted with present expectations and adjusted accordingly. The current narrative supporting financial markets around the globe is relatively positive and may be detached from some fundamentals, so it could be challenged. Two particular developments will be worth monitoring: first, global consumer spending is likely to continue adjusting to changing prospects for employment and household wealth. Depending on how this goes, firms could delay hiring and investment, or even pursue spending cuts and layoffs; and second, slowing recoveries could lead to credit losses in financial sectors that could test reserve buffers. Of course, there are also other sources of uncertainty on the global scene, including the US election, Brexit, and ongoing geo-political tensions. In Mexico, concerns about a new downgrade in the sovereign’s credit ratings are likely to re-emerge as the country’s public finances continue to deteriorate, Pemex keeps losing money, and energy policy continues to discourage private investment.

The MXN behaviour in the past two weeks is worth noting. After briefly touching levels below USDMXN 21, the Mexican peso lost 7% to reach levels close to USDMXN 22.4. A large part of this adjustment could be explained by an increase in risk perception on global markets, as a second wave of COVID-19 contagion appeared in some regions of the world and produced anxiety about new confinement measures. We should note, however, that the recent MXN depreciation also followed the resignation of the head of CENACE, National Center for Energy Control, which occurred after President Lopez Obrador asked the Energy regulation bodies in Mexico to support the State companies—Pemex and CFE—which constitutes another blow for private investments in the energy sector. Later in the week, the MXN returned to levels close to USDMXN 21.6.

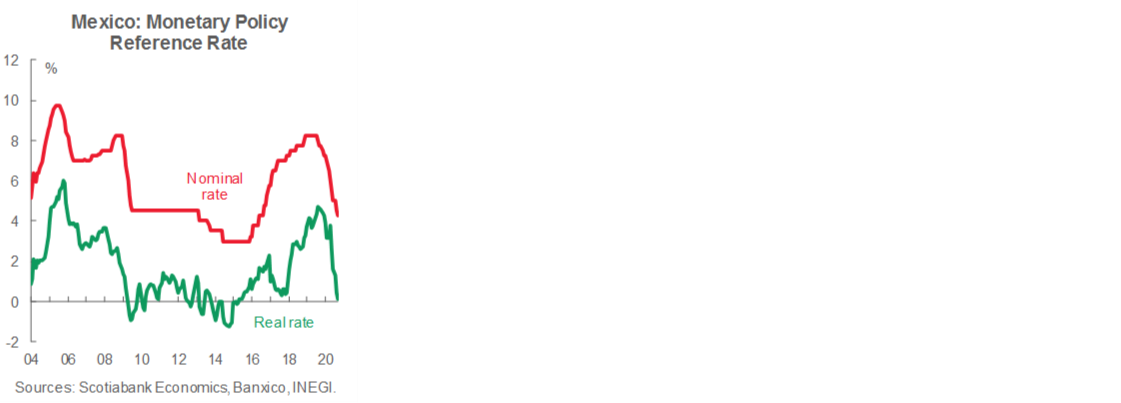

Banco de Mexico cut its reference interest rate by -25 bps to 4.25% in a unanimous decision by the Board on September 24, in line with market expectations, but despite rising inflation. There was a subtle, but relevant, change in the Board’s press release, where it mentioned that available space for additional cuts was limited. Among the most relevant risks to the upside for inflation, Banxico mentioned additional episodes of exchange rate volatility and a high degree of persistence in core inflation—both of which are already a reality. Because of these factors, we think that the easing cycle has now ended, unless there are favourable downside surprises on inflation in the coming months.

Looking at recent data releases, inflation numbers presented mixed results for the first half of September. On the one hand, bi-weekly inflation was basically tame and in line with market forecasts, posting a 0.16% 2w/2w increase in the general index, 0.17% in the core and 0.15% in the non-core. On the other hand, the year-over-year readings remain elevated, with general inflation reaching 4.1% y/y, core inflation hitting 3.99% y/y, and non-core inflation coming in at 4.44% y/y. It is likely that year-over-year readings will remain elevated and above the 4.0% threshold during the coming months

Aggregate supply and demand contracted during Q2 for a fifth consecutive quarter, widening their combined decline from -1.8% y/y in Q1 to -21.6% y/y, the worst contraction on record. Private consumption, the main driver of economic activity on the demand side, registered its largest-ever contraction, going from -0.5% y/y to -20.6% y/y, while gross capital formation (GCF) deepened its contraction to -34.0% y/y from -9.3% y/y in the previous quarter—the sharpest drop in 25 years. Q2’s downturn reflected the impact of activity closures in the second quarter.

Retail and wholesale activity continued to improve in July, but at a modest pace and remained well below pre-pandemic levels. Retail sales growth moderated from 7.8% m/m in June to 5.5% m/m in July and remained down from last year by -12.5% y/y; wholesale sales growth softened from 11.1% m/m to 4.5% m/m, leaving sales off by -10.7% y/y compared with July 2019.

The Global Indicator of Economic Activity (IGAE in Spanish) slowed from 8.95% m/m in June to 5.69% m/m in July despite further progress in Mexico’s gradual re-opening. In annual terms, the contraction improved from -13.18% y/y in June to -9.84% in July, close to market expectations of -10.10% y/y.

Remittances from abroad posted a USD 3.574 bn inflow in the month of August, once again a strong reading that is 9.4% y/y higher than a year ago. These transfers support the consumption of many families within the country, and year to date have amounted to USD 26.4 bn in inflows.

Banco de Mexico published on October 1 the results of its September survey of economic perspectives, which showed a small improvement in expectations: the average market forecast for GDP growth improved to -9.82% y/y from -9.97% y/y in August, while for 2021 the average forecast rose to 3.26% y/y from 3.01% y/y. In contrast, expected inflation for 2020 rose to 3.89% y/y from 3.82% y/y, while for 2021, there was a mild reduction to 3.57% y/y from 3.60% y/y. The reference monetary policy rate for the end of 2021 was revised downwards, to 4.09% from 4.24%, while for 2020 it was left basically unchanged at 4.11%.

Finally, on October 1, the Supreme Court ruled that the President’s public consultation to investigate former presidents was constitutional but would need to be worded differently. This ruling triggered a lot of reactions, many of which denounced foul play by the Court, arguing that the decision was more politically motivated than legally justified. Among responses, there was a letter from the Mexican Bar, stating that “the SCJN (Supreme Court of Justice in the Nation) decided to trade constitutional order for popularity. Adopting a decision without arguments not only turns its back on itself, but also on impartiality; by seeking to avoid confrontation with political power, the Court thereby risks losing its independence”.

Over the next couple of weeks, a new program to boost infrastructure investment is expected to be announced by the Government and private-sector leaders. We will see if this will be large and strong enough to change the currently weakened investment environment. On the economic indicators front, figures for private internal consumption and gross fixed investment for the month of July will be released on October 6, and should reveal how the main components of internal demand started the third quarter. We will also receive on October 8 the minutes of the last monetary policy decision on September 24 that are expected to provide clues about the next actions we can expect from the central bank. Industrial activity for the month of August, out on October 12, will provide valuable information to assess the speed and strength of the economic recovery in Q3, while inflation figures for the month of September, expected on October 8, should show whether core inflation breached the 4% y/y threshold or remained below it. Finally, auto industry numbers for the month of September, due on October 6, will let us know how this key industry closed Q3.

Peru—As Phase 4 Begins Amidst Calmer Politics, We Revise Our Inflation & FX Forecasts

Guillermo Arbe, Head of Economic Research

51.1.211.6052 (Peru)

guillermo.arbe@scotiabank.com.pe

The past two weeks have been much quieter in terms of political noise and Congressional initiatives. Phase 4 of the re-opening began on October 1. The lockdown has now been lifted throughout the country, except for partial restrictions on Sundays and late-night curfews. International flights have been authorized to and from Bolivia, Chile, Colombia, Ecuador, Panama, Paraguay, and Uruguay, from October 5. Tourism-related businesses may operate, as well as artistic activities, non-contact sports, and most family entertainment, albeit at reduced capacity. Schools remain closed, as are cinemas and nightclubs. The government was finally motivated to implement Phase 4, originally scheduled for August, as COVID-19 now shows signs of receding. COVID-related hospital occupancy is currently half of what it was at the height of the pandemic about a month ago, and the mortality rate is down by two-thirds since then.

We are changing our inflation forecasts for 2020 and 2021. After inflation rose from 1.7% y/y in August to 1.8% y/y in September, rather than falling—surprising to the upside for the third consecutive month—we are raising our forecast for inflation to 1.5% y/y from 1.1% y/y for 2020, and to 2.0% y/y from 1.5% y/y for 2021. Moreover, there are increasing signs of resistance to deflation in basic food prices and other goods linked to domestic demand. With the worst of the contraction over, the risk of temporary deflation is fading. Our 2% y/y forecast for 2021 reflects a higher starting point coupled with base effects related to the absence next year of the dip in inflation that occurred in April–May 2020. However, none of this will affect BCRP monetary policy, and we continue to expect the reference rate to remain at 0.25% for the next twelve months at least.

We are also changing our USDPEN year-end FX forecast for 2020 from 3.45 currently to 3.60, and for 2021 from 3.40 to 3.55. The improved external account fundamentals have not played into the market as we had expected and the PEN rate has clearly broken through resistance at 3.60, with no indication of subsiding soon. We continue to expect the PEN to adjust to fundamentals eventually, but this will happen more slowly than we previously thought, and will come off a much higher base. Although it is still possible that a delayed increase in USD flows from mining exports could put USDPEN 3.45 back into play, this has become less likely now that the PEN has broken through technical resistance levels, a move that is likely to feed into further PEN weakness in the short term.

Lima home sales were up 10% y/y in August (according to a local real estate association, Asociación de Empresas Inmobiliarias). Thus, residential real estate is one more market that has returned to pre-COVID-19 levels. Meanwhile, the decline in public investment, which had been the main drag on the economy for months, may have finally turned. Finance Minister María Alva stated recently that public-sector investment should have increased in September (no figures have been released yet). This would be the first sign of positive growth since February and a significant change for government investment to transit from being a drag on the economy to becoming a stimulus to growth.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | carlos.munoz@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Forthcoming |

| Subscribe: | pirajaj@colptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

| COSTA RICA | |

| Website: | Click here to be redirected |

| Subscribe: | estudios.economicos@scotiabank.com |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including, Scotiabanc Inc.; Citadel Hill Advisors L.L.C.; The Bank of Nova Scotia Trust Company of New York; Scotiabank Europe plc; Scotiabank (Ireland) Limited; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Scotia Inverlat Casa de Bolsa S.A. de C.V., Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorised by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorised by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V., and Scotia Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.