ECONOMIC OVERVIEW

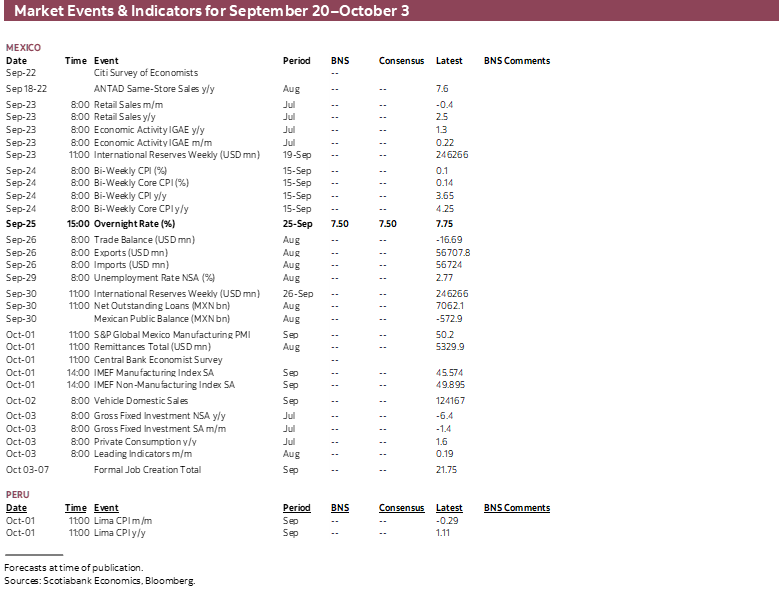

- Mexico has a busy week ahead, with key data including economic activity and mid-month inflation figures accompanied by Banxico’s practically certain 25 bps rate cut on Thursday.

- Chile’s and Brazil’s central banks publish the minutes to their latest rate meetings when both held rates steady as we try to determine the timing of their next respective rate cuts. Colombia’s international trade data should continue to mirror the strength in personal consumption that has been a firm tailwind for growth so far in 2025.

- In today’s Weekly, the team in Mexico discuss recent Pemex developments, from August’s Strategic Plan to this week’s issuance of international debt partly aimed at cleaning up Pemex’s finances.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in Mexico.

MARKET EVENTS & INDICATORS

- A comprehensive risk calendar with selected highlights for the period September 20–October 3 across the Pacific Alliance countries and Brazil.

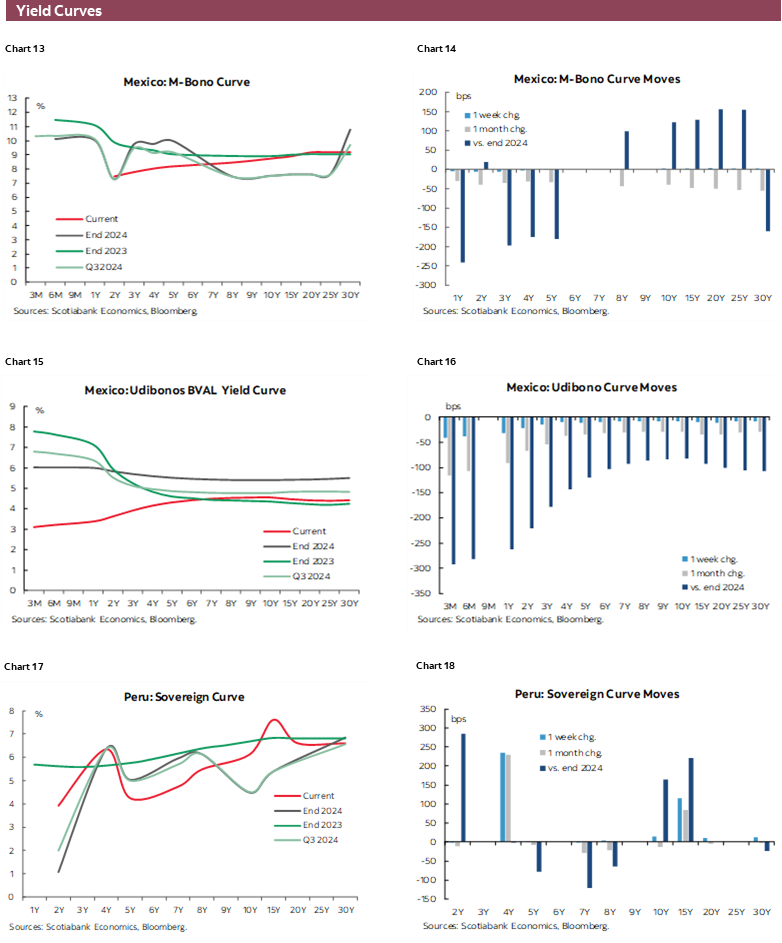

Chart of the Week

ECONOMIC OVERVIEW: MEXICO IN FOCUS, WITH BANXICO CUT AND KEY DATA ON TAP

Juan Manuel Herrera, Senior Economist

+52.55.2299.6675

juanmanuel.herrera@scotiabank.com

- Mexico has a busy week ahead, with key data including economic activity and mid-month inflation figures accompanied by Banxico’s practically certain 25 bps rate cut on Thursday.

- Chile’s and Brazil’s central banks publish the minutes to their latest rate meetings when both held rates steady as we try to determine the timing of their next respective rate cuts. Colombia’s international trade data should continue to mirror the strength in personal consumption that has been a firm tailwind for growth so far in 2025.

- In today’s Weekly, the team in Mexico discuss recent Pemex developments, from August’s Strategic Plan to this week’s issuance of international debt partly aimed at cleaning up Pemex’s finances.

Mexico will hog the spotlight next week in Latam, with a calendar full of key data and Banxico’s Thursday rate decision making up for the uneventful and holiday-shortened week we’ve just had. It is also in focus in today’s Weekly, with our local team discussing recent Pemex developments, from August’s Strategic Plan to this week’s issuance of international debt by Mexico’s government with proceeds partially directed to the state-owned oil company.

Chile will return from a four-day weekend to another fairly quiet calendar when the BCCh’s minutes on Friday will be the focus, while Colombia opens to international trade data, and Peru gets to kick back with nothing on tap. Brazilian markets have the BCBs meeting minutes and monetary policy report as well as mid-month inflation data to contend with.

Outside of Latam, markets will focus on the results of global PMIs on Tuesday that always have room to surprise in either direction, U.S. PCE inflation, and Canadian GDP on the data front, with the week also peppered with a flood of central bank speakers following the recent stream of as-expected rate decisions in the G10—only missing Switzerland’s rate hold next Thursday. U.S. President Trump speaks at the United Nations and the OECD publishes its Interim Economic Outlook that usually lacks private sector projections.

Mexico’s week begins with refreshed forecasts in the Citi survey of economists that may show the median respondent shift their year-end Banxico rate forecast to 7.00% (from 7.50%), as we did last week. Ongoing dovishness within Mexico’s central bank board as well as the significant change in expectations for the Fed in recent weeks, with now three cuts expected by end-2025, point to Banxico rolling out more cuts than previously thought. End-2026 projections for a 6.50% policy rate (as we project) may be left unchanged with a chance that economists include an additional rate cut.

Tuesday brings July retail sales and economic activity figures with both likely to decelerate from moderate expansions of 2.5% and 1.3% year-over-year (y/y) in June, respectively. Retail sales numbers were heavily boosted in June by a 51% y/y surge in online purchase volumes that should normalize in July figures—although the category expanded by over a fifth in the first half of the year, compared to only 1.5% for overall retail sales. As for economic activity (IGAE), the INEGI’s timely indicator of economic activity (IOAE)noted a deeper y/y contraction in output in July at -1.3% from -0.3% in June. The IOAE has consistently undershot the IGAE since 4Q21 by about 1.5ppts on average and the two series tend to have diverge directionally from one month to the next, so don’t bank on an IGAE decline in next week’s data, but it’s somewhat safe to expect another soft GDP print for Mexico.

Weak economic activity data should act to reinforce dovishness within Banxico’s ranks, but we also have to watch the results to H1-Sep CPI data due on Wednesday for how it may influence guidance. In the second half of August, core inflation remained high at 4.3%, decently above the 3.7% reading for headline inflation, with the former expected to remain little changed at this high level while the other may marginally pick up. Within core inflation, services ex. shelter and education remains hot around 5.2% and the recent pickup in core goods inflation to ~4% as of June is also a source of concern.

A 25 bps rate cut is certain next Thursday, and it may take a much hotter than expected reading to significantly influence the thinking at Banxico in regards to forward guidance, however—at least for the four out of five in the board that remain well open to additional cuts. A more dovish / less hawkish Fed has clearly created room for Banxico to follow suit with additional rate cuts to provide additional support to the domestic economy while preserving a healthy rate differential vis-à-vis the U.S.; like the Fed now, Banxico has also been prioritizing economic conditions over upside inflationary risks for several months.

The focus for next week’s decision is to what degree Banxico may acknowledge the additional rate cuts slack that the Fed’s shift has given it, although we may have to wait until the release of the meeting minutes. We’ll also watch whether the Fed’s own cuts have changed Dep Gov Heath’s mind to favour a rate cut next week after being the sole dissenter preferring a rate hold at the early-August decision.

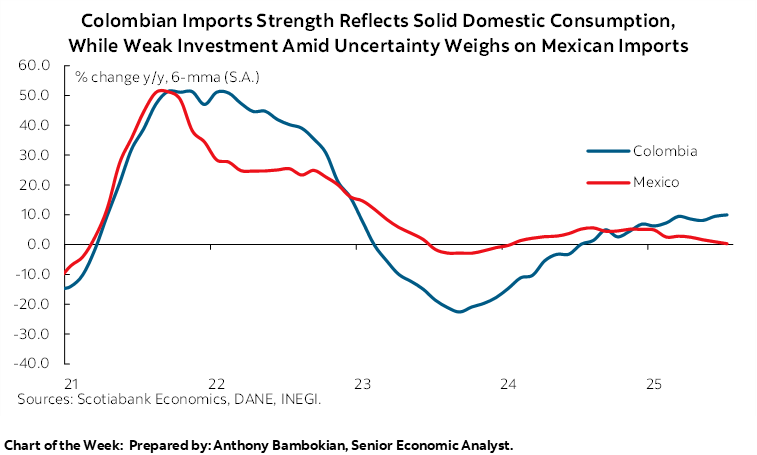

Mexico’s week ends with the release of international trade data for August, with the trade balance generally sitting in positive territory through most of the year outside of a large trade deficit in January in line with seasonal norms. Growth in overall exports has not been materially impacted by U.S. tariffs, averaging a 7% y/y pace in the year-to-July that is roughly on par with growth seen in 2H24, but the significant slowdown in imports to 0.6% y/y YTD (from about 6% y/y on a seven-month rolling basis) reflects a sharp pullback in capital goods imports (of 9.4% y/y YTD) likely associated with caution associated with international trade (a factor that may continue to weigh as we look ahead to the renegotiation of the USMCA).

Colombian international trade data due on Monday should continue to paint a very different story to Mexico’s, as imports to the country have risen by an average of ~10% y/y (in USD and volume terms), reflecting the strength in personal spending that has been a solid driver of Colombian growth in 2025. Meanwhile, exports are growing at a modest clip of 0.5% year-to-date as exports of traditional products fall 11% YTD with declines in oil and coal shipments against a surge in coffee exports (thanks to a surge in the price of beans); industrial exports are expanding by about 10%.

The BCCh and BCB minutes will touch on respective rate cuts and rate holds, with the former keeping policy unchanged on the 9th after having rolled out its first cut of the year in July while the latter kept the Selic rate steady for the third consecutive meeting. From both central banks, we’ll be looking for information on when the next rate cut will come. Chilean markets are currently expecting that the BCCh will also choose to hold at its late-October announcement ahead of the first round of presidential elections on November 16 but follow this with a near-certain 25bps cut in December a few days after the second voting round (if political and market stability allow, of course). Meanwhile, the BCB is seen as holding into at least their first decision of 2026, in January, but we’ll get more colour on those odds from the minutes, the quarterly monetary policy report, as well as mid-Sep CPI data out on Thursday that should show headline inflation remaining around the 5% level.

PACIFIC ALLIANCE COUNTRY UPDATES

Mexico—Pemex 2025–2035: Operational Sustainability, Financial Backing, and the Demand for Measurable Results

Rodolfo Mitchell, Director of Economic and Sectoral Analysis

+52.55.3977.4556 (Mexico)

mitchell.cervera@scotiabank.com.mx

Miguel Saldaña, Economist

+52.55.5123.1718 (Mexico)

msaldanab@scotiabank.com.mx

This week, state-owned oil company Petróleos Mexicanos (Pemex) drew significant attention as the Mexican government continued to reinforce its financial support through a historic placement in international debt markets. Mexico issued $8 billion in dollar-denominated bonds, following a €5 billion (approximately $5.9 billion) euro-denominated offering earlier in the week. The proceeds will be used for general purposes and a capital contribution to Pemex, aimed at repaying, redeeming, and repurchasing part of its outstanding securities. The issuance included notes maturing in 2031, 2033, and 2035, priced at spreads ranging from 123 to 165 basis points over comparable U.S. Treasuries. This effort adds to the $12 billion already raised earlier this year through pre-capitalized securities (P-Caps). However, concerns have been raised that this capital injection will primarily be used to service financial obligations ($24 billion in debt maturing 2025 and 2026, as well as $23 billion in payment to suppliers), limiting Pemex’s operational investment capacity and casting doubt on the viability of its Strategic Plan 2025–2035.

A few weeks ago, the Mexican government unveiled the Pemex Strategic Plan 2025–2035, designed to ensure the company’s financial and operational sustainability, aligned with national energy policy. The plan aims to boost production of liquid hydrocarbons and natural gas, improve efficiency in refining and petrochemicals, expand logistics services, and develop renewable energy projects. It includes an investment of MXN $250 billion through Banobras and commercial banks, along with the issuance of $12 billion in P-Caps, with the goal of reducing Pemex’s total financial debt by 25% by 2030.

Operationally, Pemex seeks to increase liquid hydrocarbon output to 1.8 million barrels per day and natural gas production to 5 billion cubic feet per day by 2028. Key projects include Zama and Trion, strategic gas pipelines, cogeneration plants, and upgrades to the National Refining System. The plan also promotes innovation in energy through solar, wind, and geothermal generation, natural hydrogen production, and lithium extraction from petroleum brines. However, an open question remains: what mechanisms will be implemented to replicate joint venture models for the development of Mexico’s most technically challenging oil fields?

Despite its ambitious scope, skepticism persists regarding the plan’s feasibility. The lack of transparency around which projects will be financed through Banobras and the absence of defined profitability criteria make it difficult to assess the plan’s success. The Mexican think tank México, ¿Cómo Vamos? emphasizes the need to abandon a “uniform investment” logic and instead differentiate between profitable, strategic, and unsustainable initiatives. It also recommends evaluating Pemex using concrete indicators such as reduced financial costs, improved debt maturity profiles, effective use of P-Caps, and lower supplier debt.

In summary, the plan signals a shift in narrative—moving away from the notion of “rescuing” Pemex and acknowledging its structural challenges. However, its success will depend on translating that narrative into measurable and fiscally responsible outcomes. Pemex must not move forward aimlessly, but rather with clear indicators that demonstrate real progress toward sustainability.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Click here to be redirected |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.