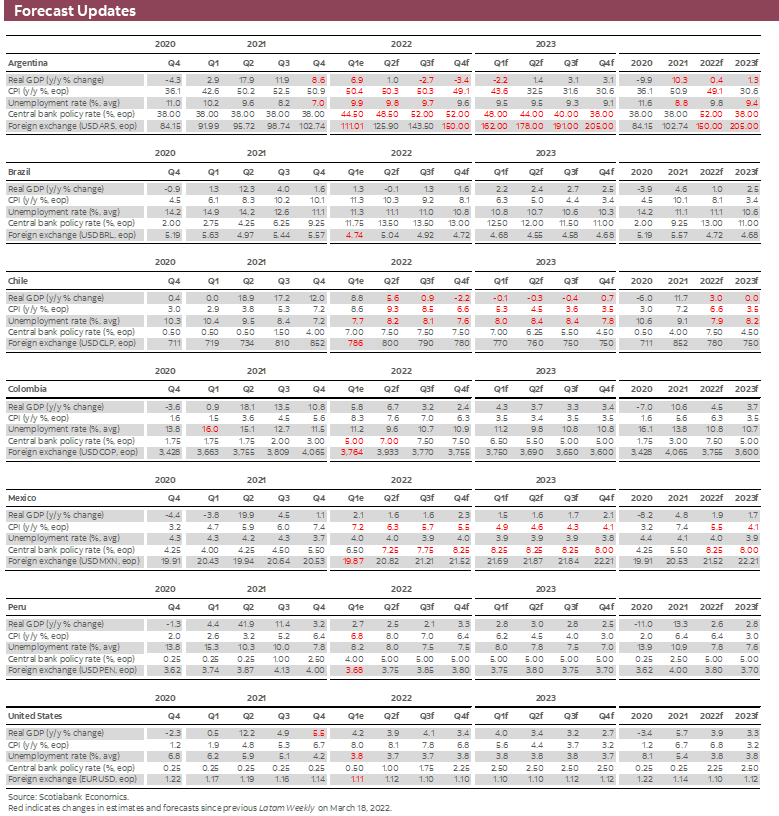

FORECAST UPDATES

- Commodity price shocks resulting from Russia’s invasion of Ukraine and their potential impact on the global economy introduce additional uncertainty to the outlook for the Latam region. In Chile, Scotiabank’s economists now expect a recession later in 2022 as higher interest rates bind. Our other economists update their views of what heightened uncertainty could entail for their economies in the forecast tables below.

ECONOMIC OVERVIEW

- Recent developments have led to increased discussion of recession risks for the advanced economies. In the US, the 2yr/10yr Treasury yield curve briefly inverted this week, possibly signalling recession.

- Inversions of this curve are widely viewed as a useful predictor of recessions. But this perspective has not gone unchallenged. There is a vigorous debate on the efficacy of yield curves in predicting recessions, in general, and in the current context, in particular.

- Regardless of what yield curves say with respect to US or Latam recession risks, other Latam financial markets are not flashing warning signs. Regional currency and equity markets have performed strongly since the start of the year.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Chile, Colombia, Mexico, and Peru.

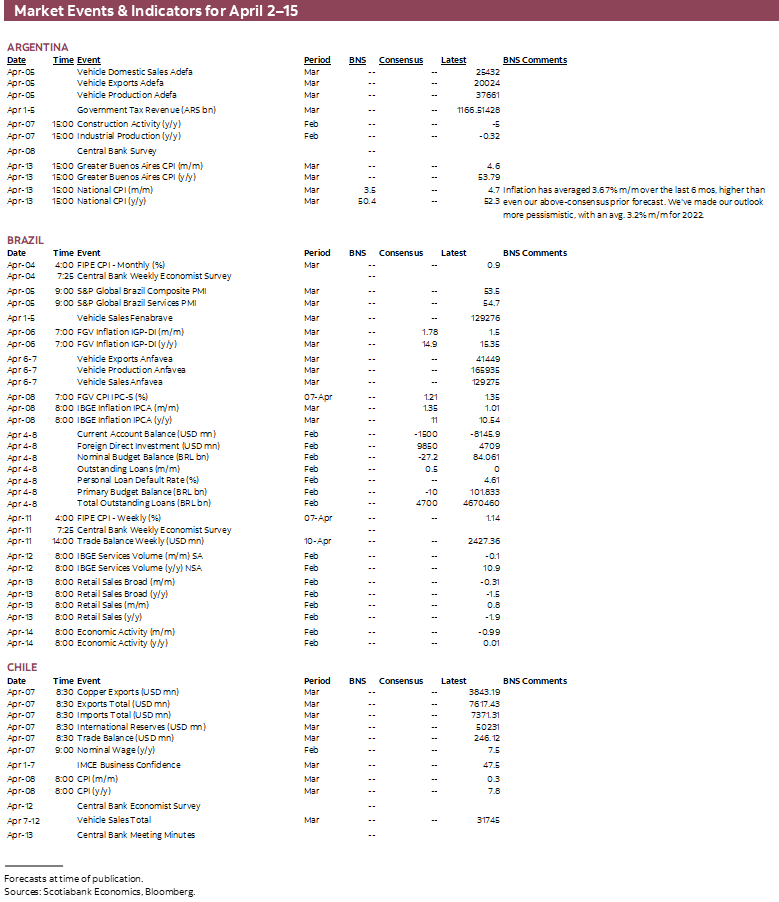

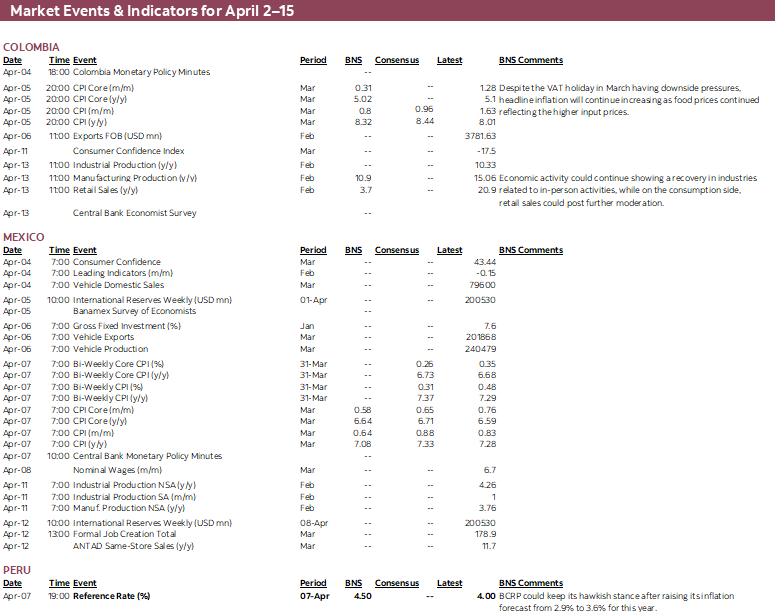

MARKET EVENTS & INDICATORS

- A comprehensive risk calendar with selected highlights for the period April 2–15 across the Pacific Alliance countries, plus their regional neighbours Argentina and Brazil.

James Haley, Special Advisor

416.607.0058

Scotiabank Economics

jim.haley@scotiabank.com

Economic Overview: Recession Risks

- Inversion of the US Treasury 2yr/10yr yield curve—however briefly—this week has focused attention on possible recession risks. Caution is advised in this regard. Models demonstrating the purported powers of this yield curve to accurately forecast recessions may not perform quite so well in the context of historically low interest rates. Time will tell.

- Even more caution is warranted in using Latam sovereign yield curves to assess recession risks. Bond markets in the region are less liquid and less deep, reducing the signal-to-noise ratio from yield curve inversion.

- Regional financial markets, which have performed strongly since the start of the year, with currencies appreciating against the US dollar and equity markets recording strong gains, are not warning of recession. But these gains likely reflect the effect of commodity price shocks that could reverse. And political risk could increase uncertainty, such that assessing recession risks is akin to reading entrails.

READING THE ENTRAILS

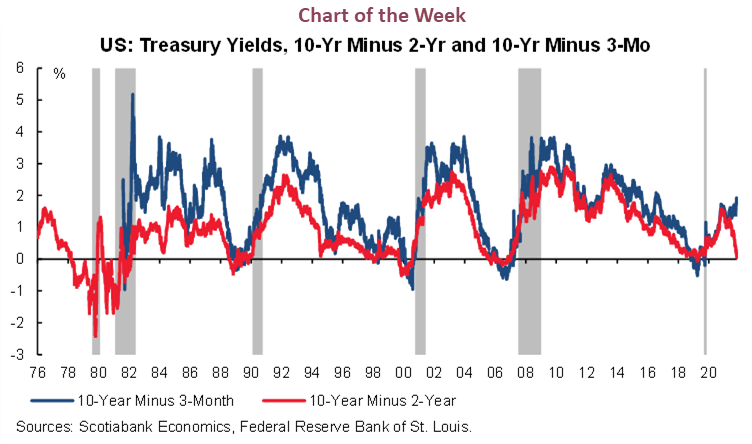

It happened. And by “it,” I mean yield curve inversion. However briefly—ephemeral may be a better description—the yield curve of key US Treasury bonds inverted this week, with the rate on the two-year constant maturity Treasury bond rising above the comparable 10-year bond yield. As noted in last week’s Latam Charts, the significance of this event lies in the forecasting properties attributed to the yield curve. Since then, a plethora of articles have appeared debating the pros and cons of inverted yield curves as recession predictors and why this time may be, or is decidedly not, different.

At the risk of oversimplification, it is fair to say that there is no clear consensus on this question. In part, this difference of opinion may simply reflect the continuing theoretical and empirical debate regarding the predictive power of yield curve inversion. There are several parameters of this debate, including the issue of causation. The fact that yield curve inversions have preceded recessions in the US has become a widely accepted stylized fact. But an inversion of the yield curve does not imply that it causes the subsequent recession in much the same way that the circulation of holiday greeting cards in advance of the holiday does not cause the subsequent festivities. In this respect, while inversion may be a necessary condition for a subsequent recession, it is not necessarily a sufficient condition.

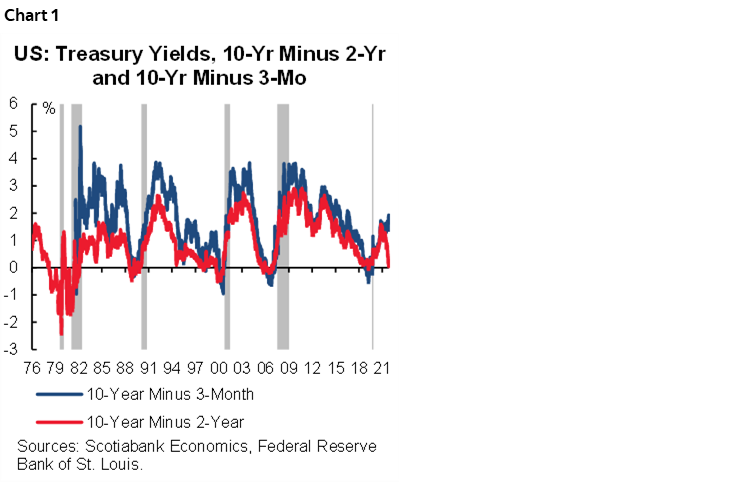

The lack (as yet) of a clear consensus on whether the US economy is headed ineluctably for recession may also reflect the indicator used by participants in the debate. There is no theoretical reason—as far as I am aware—endowing one specific indicator of yield curve slope with the exclusive power to forecast recessions. Over the last four decades or so, the difference between the 10-year Treasury bond yield and the rate on 2-year Treasury bonds performs well in terms anticipating recessions. But so does the difference between the 10-year yield and the 3-month Treasury bill rate (chart 1). Yet the paths of the two yield curve slope indicators are now diverging, with the former approaching the inversion threshold while the latter is widening.

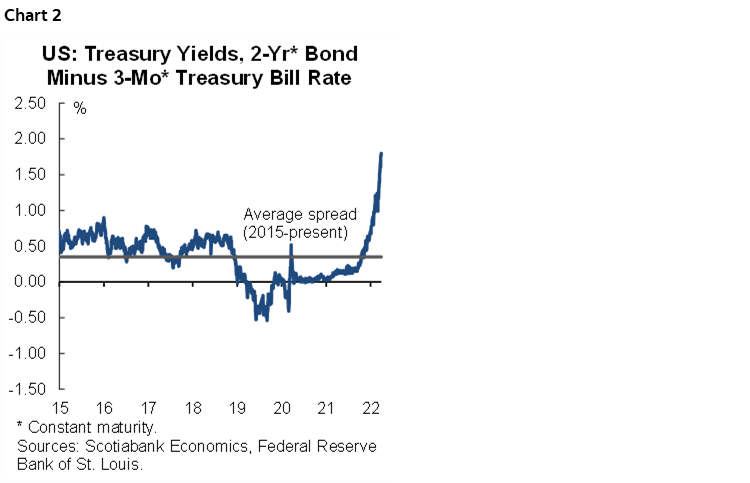

That divergence reflects a sharp increase in the two-year bond. While the ten-year bond yield has also risen since the start of 2022, the two-year rate has jumped by much more, so that the spread between the two is now about 150 basis points, up 100 basis points since the start of the year, and roughly four times the average spread over much of the past decade (chart 2). This difference could be explained by several factors, including adjustment away from the abnormally low interest rate environment that has prevailed in the pandemic (in fact, since the global financial crisis) and the anticipated effects of the unwinding of quantitative easing. And markets are obviously anticipating more aggressive Fed tightening over the next two years. That tightening will be reflected in three-month Treasury Bill rates, as the Fed pulls the trigger on successive rate increases.

In the meantime, longer-term assets are pricing-in those expected rate rises now. This explains why, for example, the ten-year yield has increased since the start of year: higher future short-term rates get baked into current longer-term yields, which are a combination (geometric mean) of current and future short-term rates. But whereas the two-year yield has spiked over 150 basis points, the ten-year rate has risen by just under 90 basis points.

One possible interpretation here is that markets expect short-term rates to rise over the next two years, but not to remain elevated over a longer time horizon. And while this outcome could be the result of a recession, with the Fed first raising interest rates to contain inflation and then reducing them to restore growth once inflation has returned to target, it might equally reflect the expectation that the Fed can control inflation without inducing a recession; that higher rates, combined with well anchored expectations, can deliver a soft landing. Moreover, with interest rates effectively starting from the zero lower bound, any monetary tightening implemented via short-term interest rates will likely cause the yield curve to invert, with or without a subsequent recession. In other words, inversion of the 2yr/10yr curve may signal recession, or it could reflect well anchored inflation expectations. There just may be something to the view that “this time is different.” Time will tell.

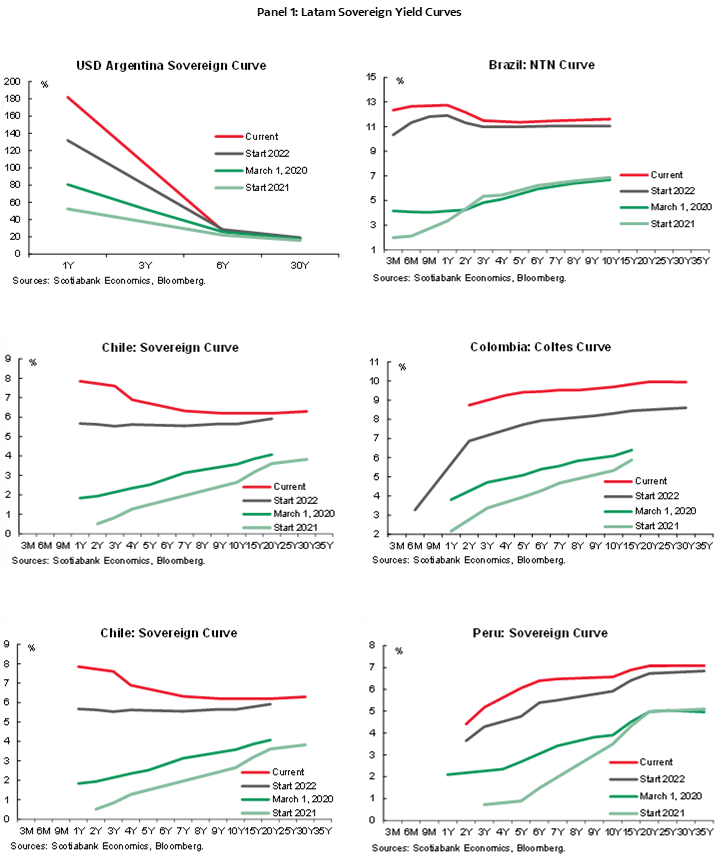

Regardless of the merits of this debate, readers may reasonably be asking what Latam yield curves are signalling in terms of recession risks. A review of the evidence in the panel of sovereign yield curve charts below provides mixed messages. The wary will discount the Argentine curve, which is greatly distorted by protracted monetary instability that will, eventually, require a clear break from the past—possibly under the aegis of the recently approved IMF program. The Brazilian curve, meanwhile, has both shifted up and flattened over the past year as inflation has accelerated and monetary policy rates were raised to contain price pressures. The Chilean yield curve has likewise shifted up; moreover, since the start of the year, it has also inverted. If a negative slope is a good predictor of recession, the warning light is flashing. This is consistent with the call made by the Scotiabank Economics team in Santiago who project a recession later in the year. In contrast, while it has shifted up and flattened relative to the start of year, the curve in Colombia retains a positive slope. The same can be said with respect to the Mexican yield curve. Peru stands apart in this review in that its sovereign yield curve has shifted up more or less uniformly across the maturity spectrum such that it retains a clear positive slope.

The message that these yield curves send with respect to Latam recession risks is thus mixed. Excluding Argentina, there is one case of a clearly negative slope (Chile) and one example of a distinctly upward sloping curve (Peru). However, even where there is clear inversion, caution should be used in inferring recession risks. This is because the “stylized fact” with respect to the predictive power of the bond market in the US (and other advanced economies) has not been well documented in emerging market economies. At the same time, the fact that bond markets in emerging economies are less liquid and less deep could reduce the signal-to-noise ratio of possible inversions. If there is a risk of recession in the Latam region from yield curve inversion, it could well be from what a negative slope in the US curve says about future external demand, rather than any message regarding short-term domestic prospects emitted by domestic bond markets.

Whatever the efficacy of yield curve slopes in predicting recessions, the recent obsession over a possible inversion does put the spotlight on what financial markets are signaling. This attention is warranted. Forward-looking financial markets price-in the future, though in periods of speculative frenzy they may price-in the hereafter as well, including increased risk of recession.

So, what are financial markets telling us about recession risks? The answer to this question also requires separating the signal from the noise. There is much to process. For example, as Scotiabank’s team in Bogota note below, since the start of the year, Latam and global financial markets have been roiled by large shocks that have generated increased volatility. Geopolitical risk has obviously spiked in the wake of Russia’s unwarranted invasion of Ukraine, which has raised questions about the future of globalization. Commodity prices, from oil and metals to wheat and other foodstuffs, have risen. And, as if that wasn’t enough, the Fed has in recent days adopted a more-hawkish tone. Today’s solid job growth numbers do nothing to soften that message.

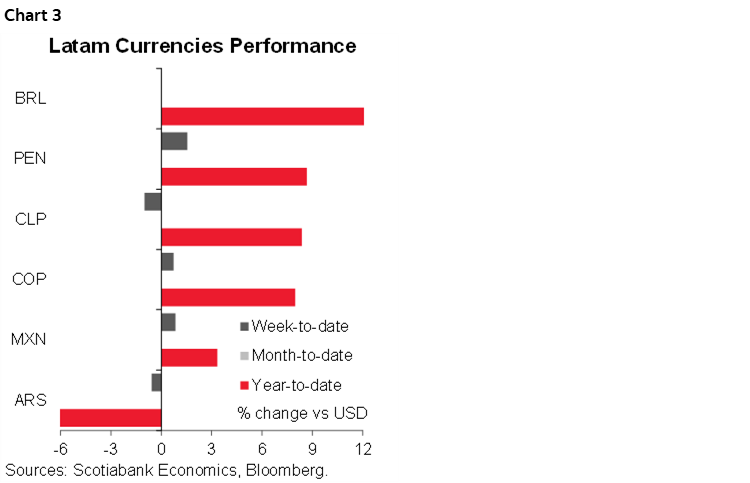

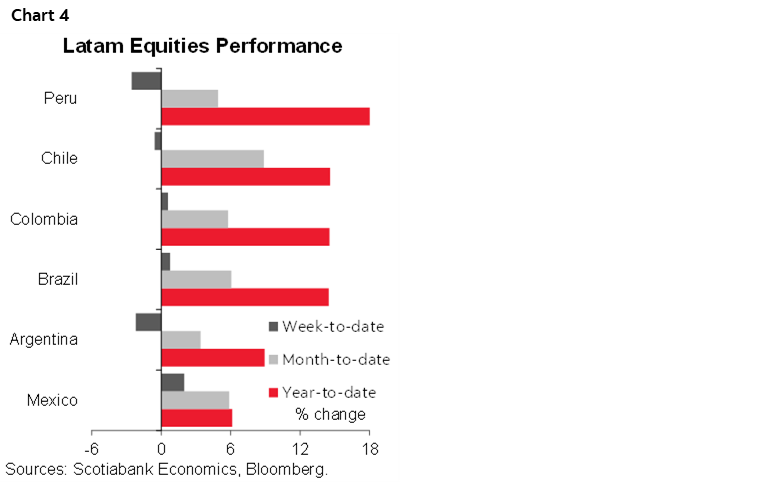

Higher geopolitical risk and a more aggressive Fed would normally be expected to result in risk aversion for emerging market assets, as risk appetite wanes and investors retreat to the safe haven of US dollar-denominated assets. Yet, despite these shifts and shocks, Latam financial markets have been remarkably buoyant since the start of the year. While most other emerging market assets have underperformed, asset markets in the Latam region have risen strongly. With the exception of Argentina’s peso, regional currencies have appreciated against the US dollar (chart 3), led by the Brazilian real, which is up almost 20% since the start of the year.

Similarly, equity markets across the Latam region have risen (chart 4). Peru’s market, which is up roughly 18% on the year, is particularly noteworthy given the remarkable degree of political uncertainty—“noise”—that markets there have had to process. However, as Scotiabank’s team in Lima has consistently pointed out, while recent political instability and the revolving door Cabinet has generated considerable attention, key economic institutions (the central bank and the Finance Ministry) have been largely insulated from that noise. That said, as the team discusses below in the Country Update, that noise may now be beginning to have economic consequences.

Political noise may also be affecting markets elsewhere in the region. In Colombia, political risk may account for the currency’s underperformance relative to the predicted (“fitted”) values of a standard econometric model of the exchange rate (see discussion below). And our team in Mexico City discuss the government’s controversial energy sector proposals in their Country Update, which could have an adverse impact on foreign direct investment.

While political risk factors may be weighing on them, there is little evidence that financial markets are signalling recession risks. In large part, this is because of the favourable terms-of-trade effects from higher commodity prices. This is the common factor driving regional markets, though as noted in the previous Latam Weekly not all countries stand to benefit equally. Moreover, the cautious investor knows that commodity prices are fickle, exhibiting strong mean reversion. A rapid run-up in prices can be followed by equally precipitous collapse.

This discussion could lead the sceptical reader to conclude that assessing recession risks from financial market indicators is about as effective as ancient soothsayers predicting the future from the entrails of a chicken. There may be some truth in that perspective. At this point at least, there is no discernable signal to extract from the noise.

In this regard, Latam policymakers and politicians alike should be asking what the economic prospects for their economies would be if commodity price shocks and the monetary policy response to higher inflation push advanced economies into recession. The prescient among them might answer that what appears to be an extended stretch of prosperity, could prove to be as ephemeral as this week’s yield curve inversion.

PACIFIC ALLIANCE COUNTRY UPDATES

Chile—Policy Rate to Peak at 7.5%, with Cuts Beginning in December 2022; GDP Expected to Grow 3.0% over 2022–23

Jorge Selaive, Head Economist, Chile

+56.2.2619.5435 (Chile)

jorge.selaive@scotiabank.cl

Anibal Alarcón, Senior Economist

+56.2.2619.5465 (Chile)

anibal.alarcon@scotiabank.cl

Waldo Riveras, Senior Economist

+56.2.2619.5465 (Chile)

waldo.riveras@scotiabank.cl

COVID-19 SITUATION CONTINUES TO IMPROVE AND MOBILITY IS ABOVE PRE-COVID LEVELS

The daily number of confirmed COVID-19 cases has continued to slow in recent days. The test positivity rate fell to 7.6%. At the same time, occupancy rates of ICU beds and COVID-19-related death rates are increasing at a slower pace. Meanwhile, the vaccination campaign has reached 94.2% of the eligible population. The rollout of booster (third) doses continues—reaching 13.6 million people—and the new booster dose (fourth) is in progress—with 2.4 million people covered. Overall, mobility has continued to improve in March, which will support the economic activity, mainly services (chart 1).

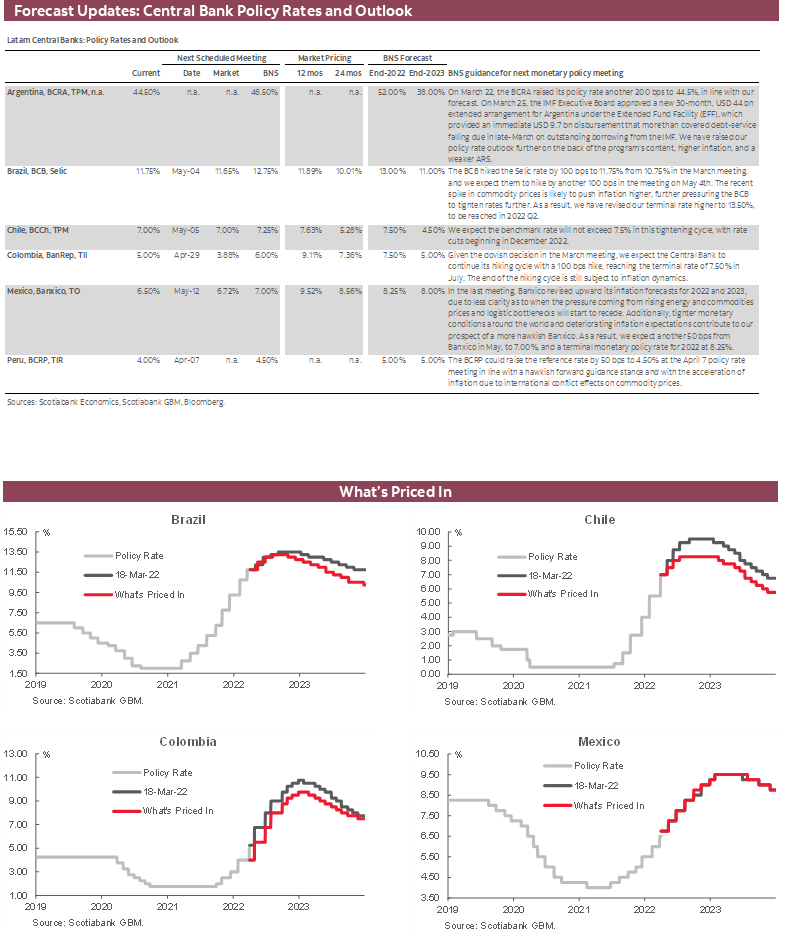

On Tuesday, March 29, the central bank (BCCh) increased the Monetary Policy Rate 150 basis points to 7%, in line with our expectations and below market surveys that anticipated a rate of between 7% and 7.5%. The BCCh confirmed our diagnosis of a slowdown, as indicated by the central bank’s monitoring of indicators for consumption, credit and the perceptions of consumers and business.

Although inflation has motivated the monetary authorities to withdraw stimulus, according to the BCCh, prospects for global GDP growth have diminished and the Russia-Ukraine conflict has introduced new uncertainty with respect to the outlook. The central bank recognizes the effect of higher commodity prices, especially oil, foodstuffs and copper, but notes that thus far the main repercussions have largely been limited to the countries in conflict. In this context, the appreciation of the peso since the previous meeting and the recovery of the local stock market stand out.

In addition, the BCCh released its Monetary Policy Report (MPR) for the first quarter of 2022 on Wednesday, March 30. The MPR’s updated baseline scenario is broadly consistent with Scotiabank’s macroeconomic scenario, though with less inflation and slower GDP growth for 2022. In our view, the central bank is signaling that the benchmark rate will increase by 25 basis points in subsequent meetings, and end 2022 at a maximum level of 7.5%, as in our baseline scenario. The benchmark rate would remain at 7.5% until the start of the easing cycle, which is likely to begin in December 2022 and result in the policy rate at 4.75% in December 2023. In our view, the risks would be that the benchmark rate is below that level by the end of 2023.

Under the BCCh’s baseline scenario, the economy expands around 1.6% in 2022 and 0.3% in 2023, or 1.9% over two years. In our scenario, growth is 3.0% over 2022–2023. Likewise, the central bank projects year-end 2022 inflation of 5.6%, below our projection of 6.6%, and markedly less than the 8% rate of inflation anticipated by the market.

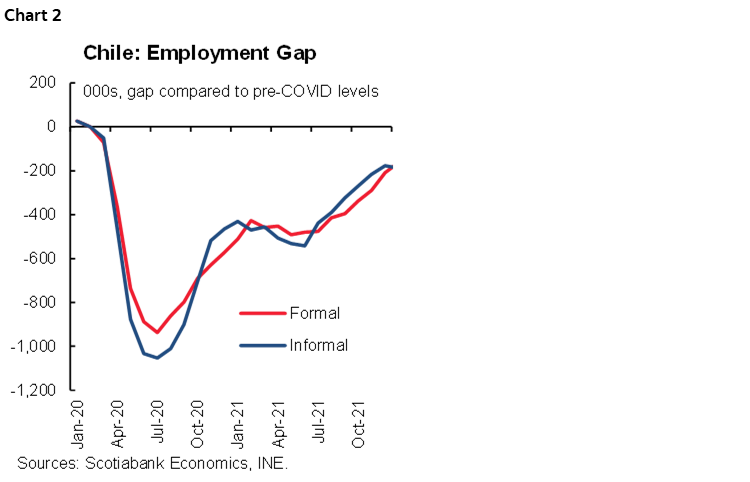

On Wednesday, March 30, the statistical agency released the unemployment rate for the quarter ended in February, which increased to 7.5%, up from the previous level of 7.3%. The rise in the unemployment rate is explained by the labour force growing faster than employment for the second consecutive month. This dynamic is largely attributable to higher participation rates of women, marking a trend that we expect will continue in the coming months given the gradual lifting of health restrictions, the reduction of monetary aid, and the lower liquidity and disposable income of households. As a result of this trend, however, the female unemployment rate increased to 8.3% (up from 7.7% previously) while that of men remained at 6.9%. In the quarter, 56k jobs were created compared to the previous moving quarter (31k men and 25k women), still leaving a gap of 295k jobs to recover compared to pre-COVID-19 levels (chart 2).

CONSTITUTIONAL PROCESS: DRAFT OF THE NEW CONSTITUTION NOW HAS 117 ARTICLES

In the last two weeks, the Assembly approved norms presented in the second report of the Justice Systems commission and norms of the substitute report of the Political System, State Forms and Environment commissions. With this, the latest draft of the new constitution has 117 articles in total. The president of the Convention formally extended the Assembly for up to three months, in accordance with the constitutional powers and the original schedule.

In the fortnight ahead, on Friday April 8, the statistical agency (INE) will publish the consumer inflation (CPI) for March. And on Wednesday April 13, the central bank will release the minutes of the monetary policy meeting held on March 29.

Colombia—Currency Already Pricing-in a Political Risk Premium

Sergio Olarte, Head Economist, Colombia

+57.1.745.6300 Ext. 9166 (Colombia)

sergio.olarte@scotiabankcolpatria.com

Jackeline Piraján, Economist

+57.1.745.6300 Ext. 9400 (Colombia)

jackeline.pirajan@scotiabankcolpatria.com

Latam currencies have been hit by several shocks that have significantly increased volatility. In terms of common shocks for the region, commodity prices, especially energy-related commodities, have risen in response to the Russia-Ukraine conflict. A more-hawkish-than-anticipated Federal Reserve has roiled currency markets. And developed economy recession fears have brought uncertainty to the markets, further increasing volatility.

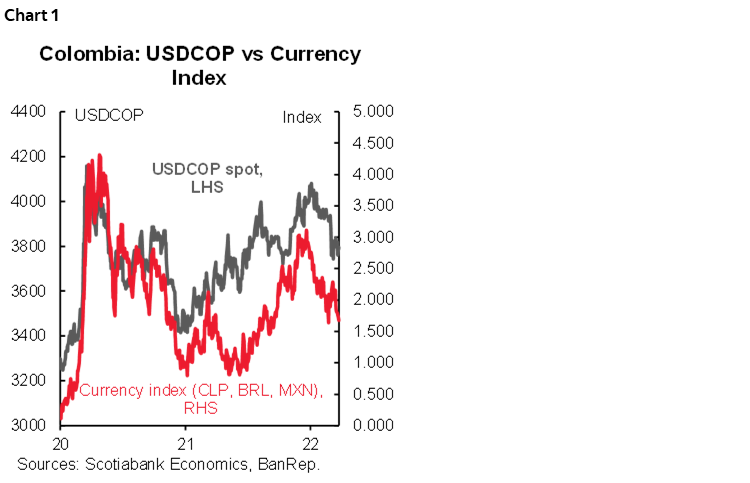

Apparently, however, international shocks have improved risk appetite for Latam currencies, especially those fueled by the impressive increase in commodity prices (Brent has increased 43% YTD, copper 6.22% YTD and silver 7.35% YTD). In fact, our currency index for the region that includes Mexico, Brazil, and Chile has appreciated 38% YTD and 3.4% since Feb 24 when Russia invaded Ukraine. In contrast, the Colombian peso (COP) has appreciated much less on a YTD basis, on the order of 8%, though at +4% it has appreciated more in line with its peers since Feb 24 when the war started (chart 1).

Why has the COP not responded strongly to the improved risk appetite for regional assets? We think the answer is worth discussing.

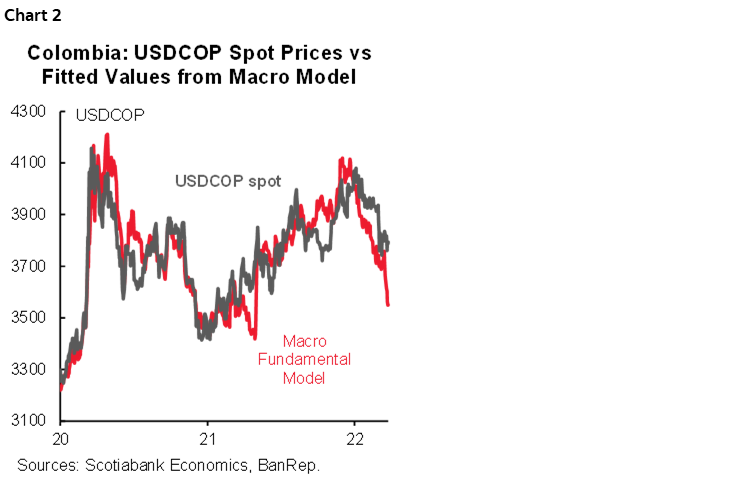

A conventional empirical model of the COP includes a proxy for terms of trade (oil prices), interest rate spread (international interest rates versus domestic rates in the medium/short term), a sovereign risk measure (CDS 5y), and an indicator of regional risk appetite (in our case, a Latam currency index). The fitted level of the USDCOP using current levels of these variables is roughly 3,550 (chart 2). However, since February, the COP spot rate has consistently been about COP 200 above the fitted value, suggesting that the market is not completely pricing-in higher commodity prices that bring more dollars into the Colombian economy and will ease short-run fiscal pressure (as explained in the previous weekly report).

Meanwhile, a robust recovery of Latam economies continues, with domestic rates providing favourable opportunities for carry-trade strategies. However, political uncertainty regarding the electoral season and the possibility of a significant change to the policy framework may have made offshore investors shy of Colombian risk, while domestic investors are diversifying exposure, resulting in capital outflows.

If this presumption is correct, the COP would already be pricing-in political risk and its performance would continue to be affected by the electoral season. This implies that a new intercept (average) will be incorporated into our empirical model of the COP only after the presidential runoff: if the market thinks that the new president will change the historically pro-market environment, the fitted line could well shift higher; alternatively, if the election results in a president with a strong pro-market view, the COP would have room to appreciate around COP200, consistent with the long-term view.

In our base-case scenario, if the war between Russia and Ukraine is resolved, oil prices would fall to a more sustainable level of USD 85 per barrel for Brent, while the interest rate gap between domestic and foreign assets would continue to provide profitably carry-trade opportunities. Meanwhile, on the domestic side, the new government could turn to a more centrist focus, independent of who wins the elections, while the status quo prevails in Congress and the Courts buttressing the COP.

All in all, factoring those considerations into our models leads us to maintain our current forecast of USDCOP 3,755 for the end of the year. That said, volatility will remain high at least until the presidential election is behind us.

Mexico—Important Dates Looming for Mexico’s Power Sector

Eduardo Suárez, VP, Latin America Economics

+52.55.9179.5174 (Mexico)

esuarezm@scotiabank.com.mx

President Lopez Obrador has an ambitious agenda to change the operation of the Mexican power sector. His objective is to strengthen the role of the government in both the generation of power and the future development of the sector by giving state-owned company CFE (Federal Electricity Commission) priority in generation, as well as control of the system’s planning. The government has tried to change the sector’s regulation by decree using a legal reform approved by both houses in the legislative and by subsequently submitting a constitutional reform that has not yet been submitted to a vote. The legal reform was suspended by specialized Federal Court judges Juan Pablo Gomez Fierro and Rodrigo de la Peza Lopez, who ruled that the bill violates the principles of free competition and would create monopolist practices in the power market. With that, the bill’s implementation was blocked, as private players in the sector were essentially granted injunctions against the legal reform.

Key elements of the proposed changes include nationalizing Mexico’s lithium reserves, eliminating the autonomous regulatory bodies—making CFE both regulator and market competitor, granting CFE priority in power distribution, and setting a minimum share of distributed power to CFE. In this respect, increasing control of the power sector seems to be a key priority for the AMLO Administration, and to achieve that goal, two new separate efforts are expected to be announced in the coming two weeks:

- Recently appointed Supreme Court Justice Loretta Ortiz Ahlf, who was nominated to the Supreme Court in 2021 by the current administration, presented a proposal for the Supreme Court to rule on the Constitutionality of the Legislative Reform of the Power Sector that was blocked by the Federal Court and has argued that the proposed legal changes do not violate the Constitution. To rule that the bill is constitutional, four Supreme Court Justices must support it. The ruling on the bill’s constitutionality is expected for April 5. If the constitutionality of the proposed changes is upheld, the lower court’s injunctions would be squashed, meaning the main recourse left for affected private players would be international arbitration.

- The second date to keep an eye on is the week of April 11, when the constitutional reform proposal for the power sector is expected to be submitted for a vote in the legislature. The vote on the bill had previously been expected after gubernatorial elections in the summer but is now expected for the week following the referendum on AMLO’s presidency (April 10).

In addition to renewed efforts to implement changes to the power sector’s regulation, the government is also scheduled to release its update to the 2022 budget’s economic assumptions late in the day on April 1. Assumptions that could be modified include the 4.1% growth assumption for the year (for which consensus is now sub-2%) and interest rates (an average 5.0% rate for 28-day cetes was originally assumed). The Ministry of Finance is scheduled to host a conference call on Monday to discuss its assumptions update.

Peru—Inflation Jumps, as First Signs of a Slowdown in Growth Begin to Appear

Guillermo Arbe, Head Economist, Peru

+51.1.211.6052 (Peru)

guillermo.arbe@scotiabank.com.pe

Mario Guerrero, Deputy Head Economist

+51.1.211.6000 Ext. 16557 (Peru)

mario.guerrero@scotiabank.com.pe

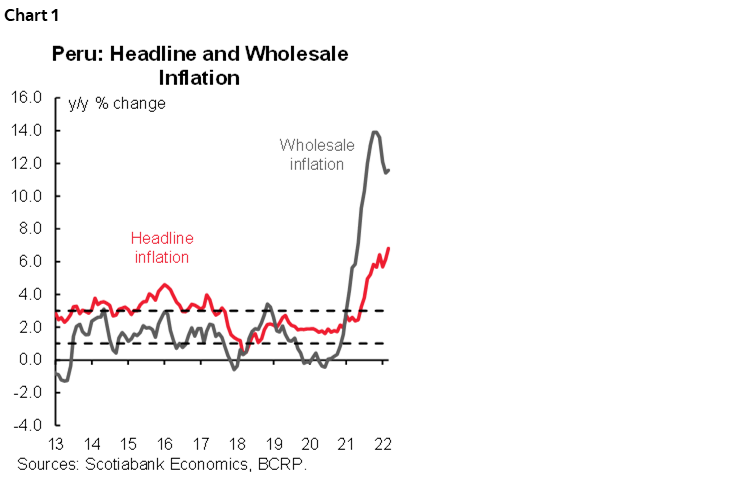

Inflation surprised mildly to the upside, rising 1.5% in March, and 6.8% over the past twelve months (chart 1), according to official sources. This was above both our forecast of 6.5% and the market consensus of 6.2%. To add drama to the data, the 1.5% monthly figure was the highest for a month of March since 1994 (28 years, for those who are wondering).

Although one might be tempted to put part of the blame on a nationwide strike by truck drivers—protesting high fuel prices—that began on March 28, the fact is that the event occurred too late in the month to have had an impact. Inflation in March continued to reflect contagion from abroad on domestic costs, particularly through high prices for energy and foodstuffs. Seasonal factors, namely the start of the school season, also contributed to higher inflation. The impact of commodity prices was reflected in wholesale inflation, which stood at 11.6% over the previous twelve months.

Looking ahead, the transportation strike is beginning to put pressure on food prices in urban areas (although there is as yet little sign of scarcity) and will have an impact beginning in April. Moreover, the transportation strike marks the first domestic source of inflation, which had heretofore seemed entirely driven by external factors.

We expect the lagged effects of these shocks to continue to push inflation up during Q2-2022, reaching a peak in June at around 8% y/y. In this respect, rising inflation reinforces our expectation that the BCRP will raise its policy rate from 4.0% currently to 4.5% on April 14. The question, though, is what comes next—whether the BCRP will increase its rate in May by 50 bps or by 25 bps. We continue to expect the BCRP will end its tightening when the policy rate reaches 5.0%, as the risk of a slowing economy begins to weigh on their decisions.

Just as the risk that President Castillo would be impeached had lifted, a new polarizing issue has emerged. On Monday, March 28, the Constitutional Court ruled that the presidential pardon that former President Pedro Pablo Kuczynski awarded ex-President Alberto Fujimori in 2017 could proceed. The issue is divisive and has been complicated further after the Inter-American Commission on Human Rights issued a “requirement” that Fujimori not be released until it has given its own verdict on the matter. The Castillo Government quickly acquiesced. And until a final decision is made, this will be another front of confrontation between the majority opposition group, Fuerza Popular, and the government.

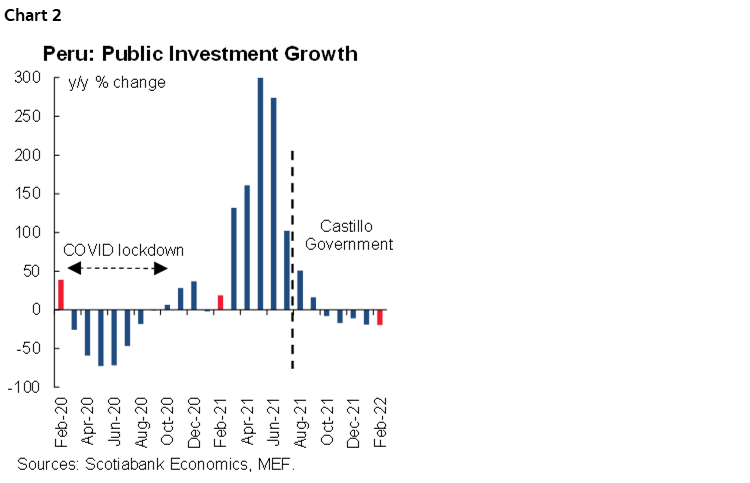

Up to now, Peru’s economy has proved resilient to political events. However, there are signs that this resiliency may be starting to wane. Public investment has fallen for the last five months in year-on-year terms, with a particularly harsh 19.6% y/y decline in February (chart 2). As a result, public investment is no longer the driver of the economy it had been prior to the Castillo Regime. If anything, it has become a drag on the economy. Moreover, the outlook is not encouraging, given concerns that poor public management and the frequent changes in Cabinet members are making it difficult for government institutions to adhere to their investment schedules.

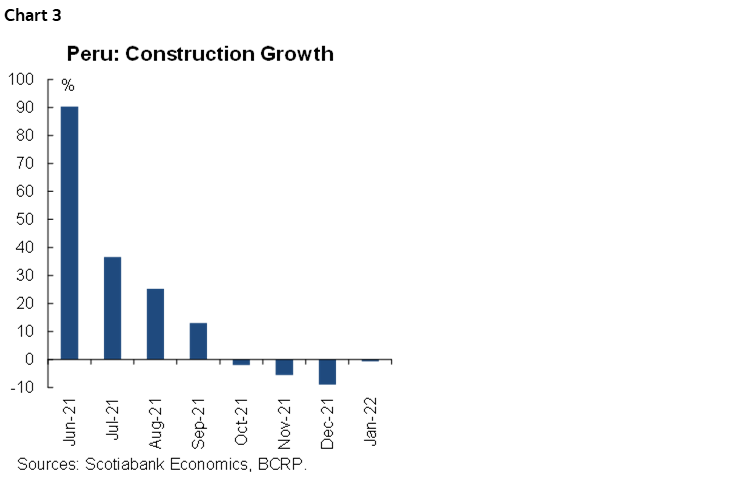

There are other signs of slowing. Construction GDP has declined for four consecutive months to January, in line with negative public investment growth (chart 3). Electricity demand in February was 0.8% below its pre-COVID-19 level (February 2019). In 2022 to date, meanwhile, mobility indicators have declined, except for transit to the workplace.

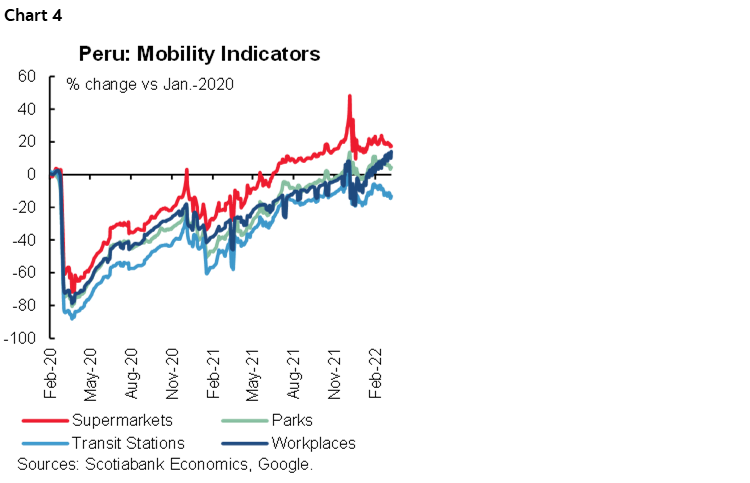

On a positive note, in March 2022, COVID-19 contagion, hospitalization and mortality rates are at their lowest levels since the first weeks of the pandemic, and nearly all mobility restrictions have been lifted (chart 4). This has helped GDP growth, which came in at 2.9% y/y in January. The leading growth sectors were restaurants and hotels, up 30.4%, and transportation, with 9.2% growth, although both were off a low base, as the country was subject to mobility restrictions in January 2021. Both sectors together accounted for 1.2 percentage points of January’s 2.9% GDP growth.

Likewise, mobility restrictions were broadened in February 2021, providing a low base of comparison for GDP growth for February 2022. Given the low base, we are expecting 4.8% growth, although BCRP Governor Julio Velarde has suggested that GDP growth in February could surpass 5%. And yet, growth could fall off quickly afterwards, in line with our forecast of 2.6% for the full year, as the slowdown we are seeing in recent data begins to dominate. The ongoing transportation strike could cause some disruption, depending on its duration.

The FX rate plunged to below 3.70, reaching 3.68 this week. This represents a rather impressive 7.7% appreciation YTD. However, the end of the tax season on Monday will stem the hefty inflow of USD from mining companies for tax purposes. Once this occurs, the FX rate should drift back up towards our year-end forecast of 3.80.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Forthcoming |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

| COSTA RICA | |

| Website: | Click here to be redirected |

| Subscribe: | estudios.economicos@scotiabank.com |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.