- Recent market commentary has focused on the possibility of yield curve inversion—long bond yields falling below rates on shorter-term maturities. The reason for this attention is the purported power of such episodes to predict subsequent recessions.

- For the Latam region, a recession in the US and other advanced countries that weakens external demand would reduce the impact of a positive terms-of-trade shock from higher global commodity prices. Countries for which higher commodity prices translate into a deterioration in the terms of trade would suffer from a twofold shock.

- The connection between yield curve inversion and recession may not be automatic, however. Past episodes of inversion preceding recession were accompanied by large exogenous shocks or an abrupt monetary policy tightening. Regardless, by stoking price pressures and increasing the potential for monetary policy error, the Russian invasion of Ukraine poses a clear and present risk to the global economy.

Anyone following market commentary over the past week or so would have been struck by the increase in references to yield curve inversion. This is the phenomenon of yield curves, which normally slope upwards, reflecting higher interest rates at the long end of the maturity spectrum, reversing slope such that yields on long bonds fall below rates on shorter-term maturities. In the US, the proximate cause for this heightened interest in the slope of yield is the Fed Chair's recent comment that the Fed is prepared to move the policy rate higher, faster, should it be necessary to return inflation to target. To state the obvious, higher short-term rates would increase the likelihood of yield curve inversion.

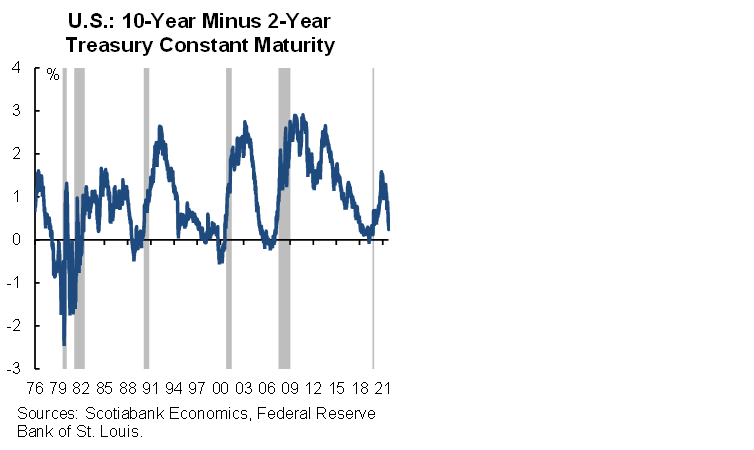

But why the growing concern over the slope of the yield curve? The answer to that question is inverted yield curves are widely believed to be good predictors of forthcoming recessions. As the chart below illustrates, in the US data over the past 45 years, there indeed seems to be a pattern between periods of yield curve inversion, based on the 10-year Treasury yield minus two-year Treasury rate, and subsequent recessions (see adjacent chart). And while we aren't there yet, that spread is now getting perilously close to the negative threshold.

For the Latam region, a US recession would be—not to put too fine a point on it—unwelcome. As noted in the last edition of the Latam Weekly, recent increases in global commodity prices represent a positive terms-of-trade shock to some, but not all, Latam countries. But the positive effects of that shock would be eroded by weaker external demand from a recession in the advanced economies. In this respect, higher commodity price that plunge the global economy into recession are a mixed blessing. And countries not sharing in the positive commodity price shock would be hit by a double whammy—a deterioration in their terms of trade combined with weaker external demand.

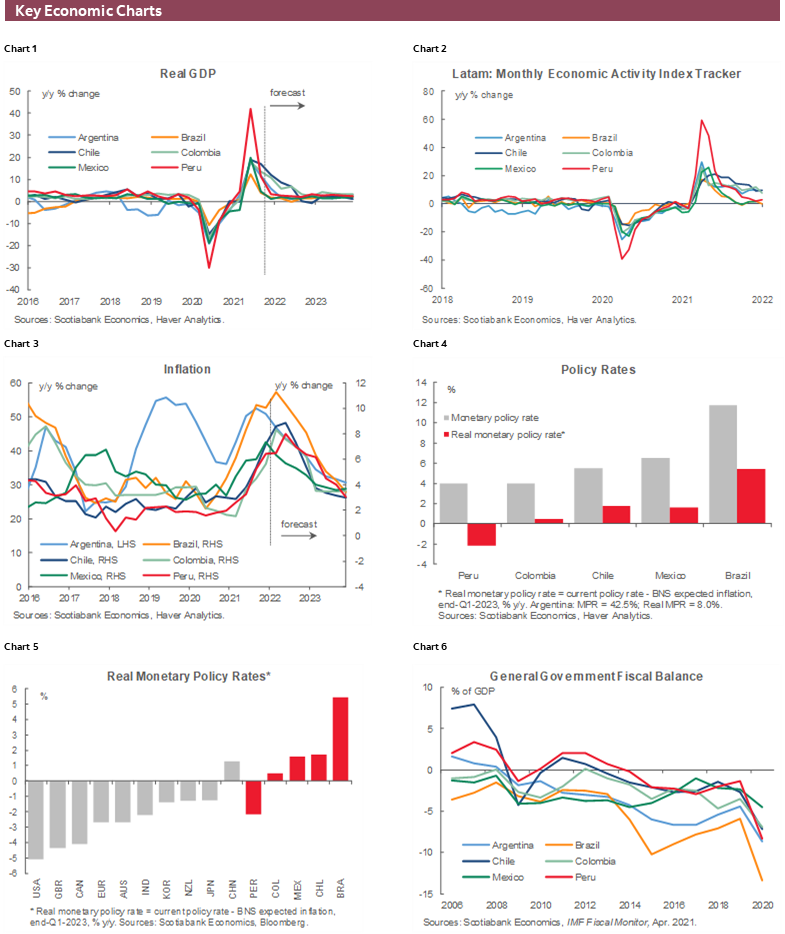

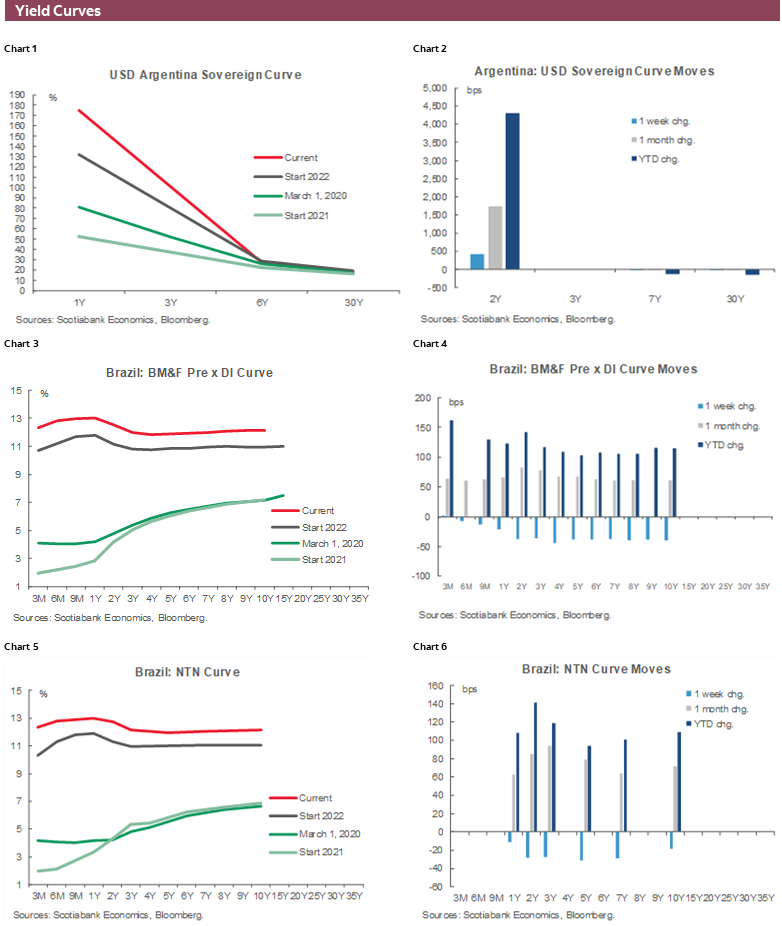

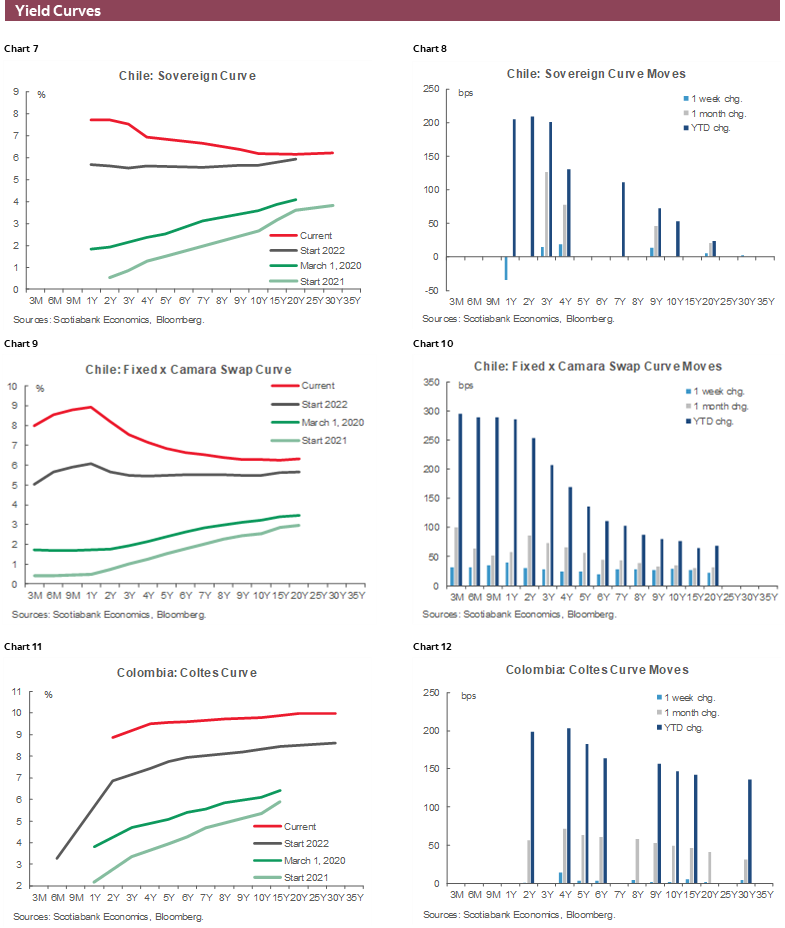

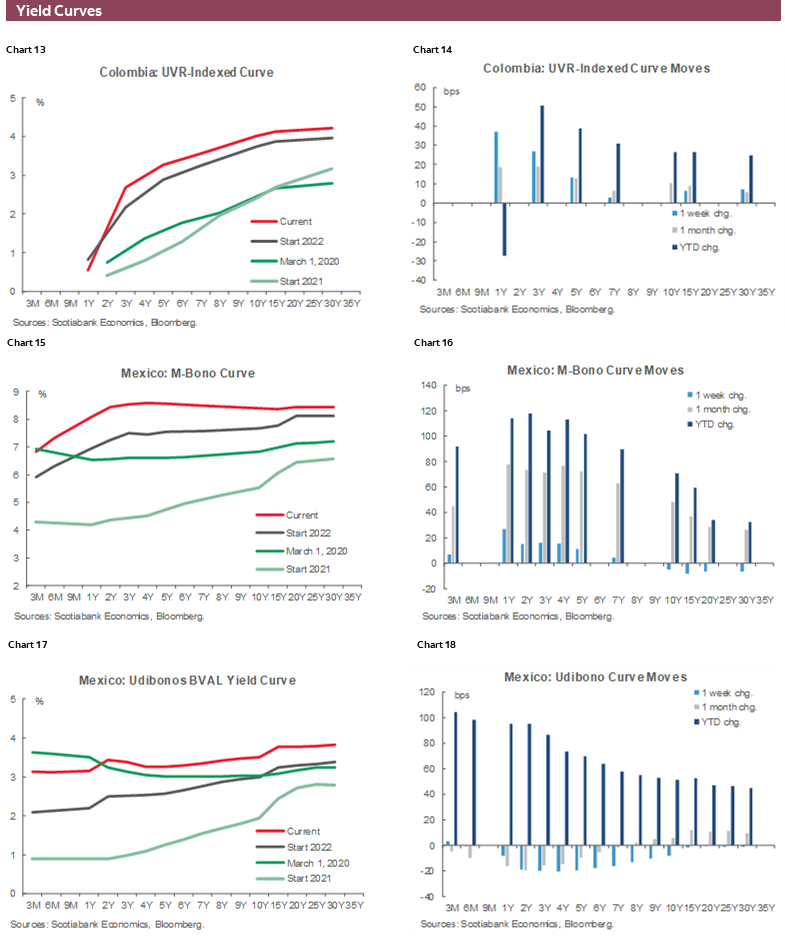

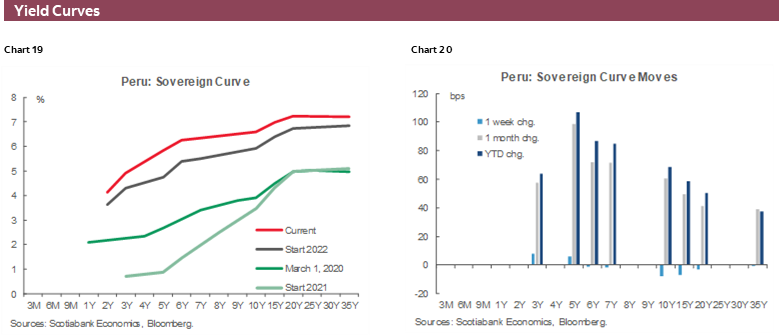

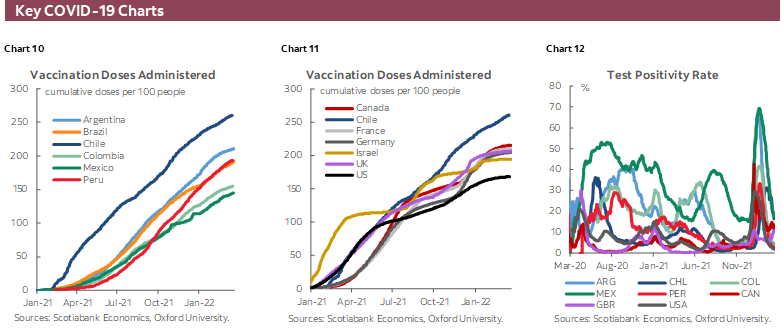

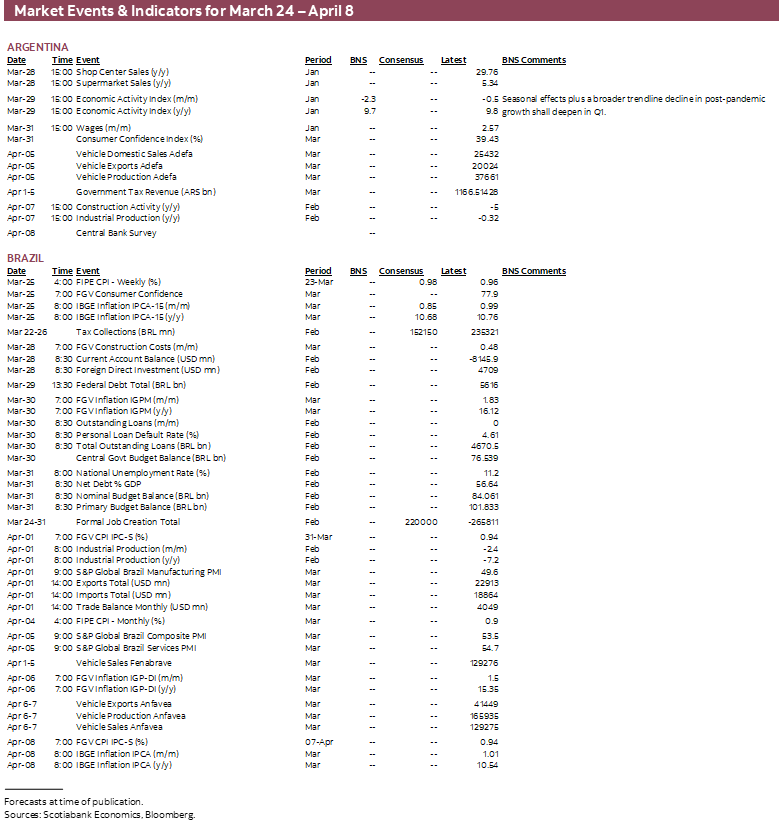

These effects would introduce additional uncertainty with respect to the near-term outlook. As the Key Economic Charts below illustrate, Scotiabank economists in the region project growth to broadly return to pre-pandemic levels (chart 1), consistent with the recent evolution of monthly economic activity indicators (chart 2). Meanwhile, even with higher commodity prices, inflation is expected to return to target, though the timing of that convergence has been pushed back somewhat (chart 3). But reining in those price pressures would require key policy rates, which have already increased over the past year, to increase even further (chart 4). And weaker growth would hamper efforts to restore fiscal balances that had deteriorated in the pandemic (chart 6), while key indicators closely watched by investors, such as debt-to-GDP ratios (chart 7), external debt burdens (chart 8), current account balances (chart 9), and international reserves (chart 10), would weaken.

Before we get too despondent over recession risks, however, it is worth noting that the case for yield curve inversion as a recession predictor is not, as jurists would say, "settled law." Yes, there is a sound theoretical basis for the indicator (provided you accept the theory). And the intuition behind the hypothesis is compelling: inversion occurs, for example, when the central bank tightens sharply, driving short rates up, generating a sharp response in interest-sensitive sectors that leads to recession. This was clearly the case with respect to the Volcker disinflation of the early 1980s, which led to historically high interest rates in the US and around the globe. But yield curve inversion does not inescapably imply a recession is forthcoming.

Most important, while the historical record seems fairly straightforward, a closer inspection provides grounds for a more nuanced view.

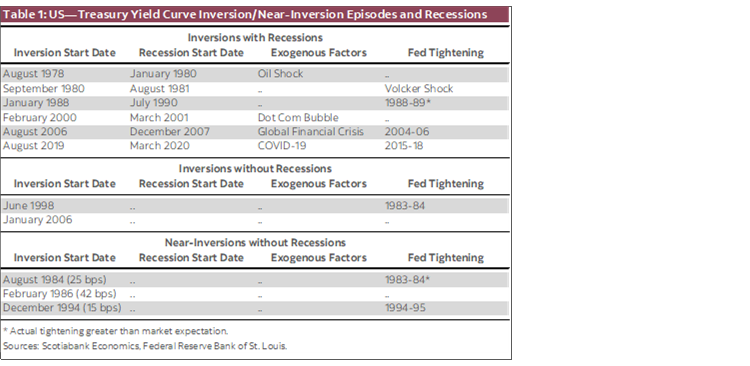

To begin, consider episodes in which yield curve inversion was followed by a recession (table 1, top panel). In all six cases, the slope of the yield curve turned negative in advance of the onset of recession, in some cases, well before, consistent with the hypothesis that forward-looking financial markets anticipate the coming downturn. Going forward, that predictive property may indeed prevail. But the fact that the lead time from the start of yield curve inversion to subsequent recession varies between seven and 31 months should give pause. Moreover, each of these cases was accompanied by a major exogenous shock (e.g., oil price shock) and/or an unexpectedly severe tightening of Fed monetary policy, such as the "Great Disinflation" undertaken by then-Fed Chair, Paul Volcker, in the early 1980s. Though it is possible that a recession would have transpired even in the absence of those exogenous events and monetary policy shocks, these episodes suggest that the connection between inversion and recession may be less tight than would appear at first glance.

Next, consider two cases of yield curve inversion without recessions (table 1, middle panel). In both cases, the negative slope indicator flashed false positive.

Finally, there are three cases of "near inversions" in which the yield on the 10-year US Treasury bond approached, but did not fall below, the two-year yield (table 1, bottom panel). If the yield curve accurately predicts recessions, it is not unreasonable to infer that sharp declines in slope (curve flattening) might likewise signal increased risks of recession, even if the negative slope threshold isn't crossed. In all three cases, however, marked declines in slope were not accompanied by a subsequent downturn in the economy. Two episodes coincided with Fed tightening, one in which the Fed tightened by more than the market expected.

A possible takeaway from this discussion is that, while it may or may not be a good predictor of recession, yield curve inversion is an excellent indicator of the robustness of Fed tightening. And in a world subject to a range of exogenous shocks, the realization of an unexpected event, such as the outbreak of war that drives global commodity prices higher, can result in policy errors.

All of this reinforces the conclusion that Russia'a invasion of Ukraine is an unalloyed threat to the global economy through its effect on inflation, which increases the risks of possible miscalibration of monetary policy. That is, the risk that central banks around the globe fail to thread the needle between insufficient tightening, resulting in in a rise in inflation expectations, and "overshooting" on policy rates, pushing the economy into recession. In fact, some prominent observers now contend that the Fed may have no option but to drive the economy into recession to crush inflation expectations.

For Latam economies, the external financial and economic environment has become more difficult. Yield curve inversion in the US (or their own economies) would not necessarily signal an inevitable recession, but heightens risks of policy miscalculation. Such circumstances increase the importance of sound policy frameworks and strong, credible institutions. Governments in the region should therefore redouble efforts to implement such policies and strengthen these institutions.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Forthcoming |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

| COSTA RICA | |

| Website: | Click here to be redirected |

| Subscribe: | estudios.economicos@scotiabank.com |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.