FORECAST UPDATES

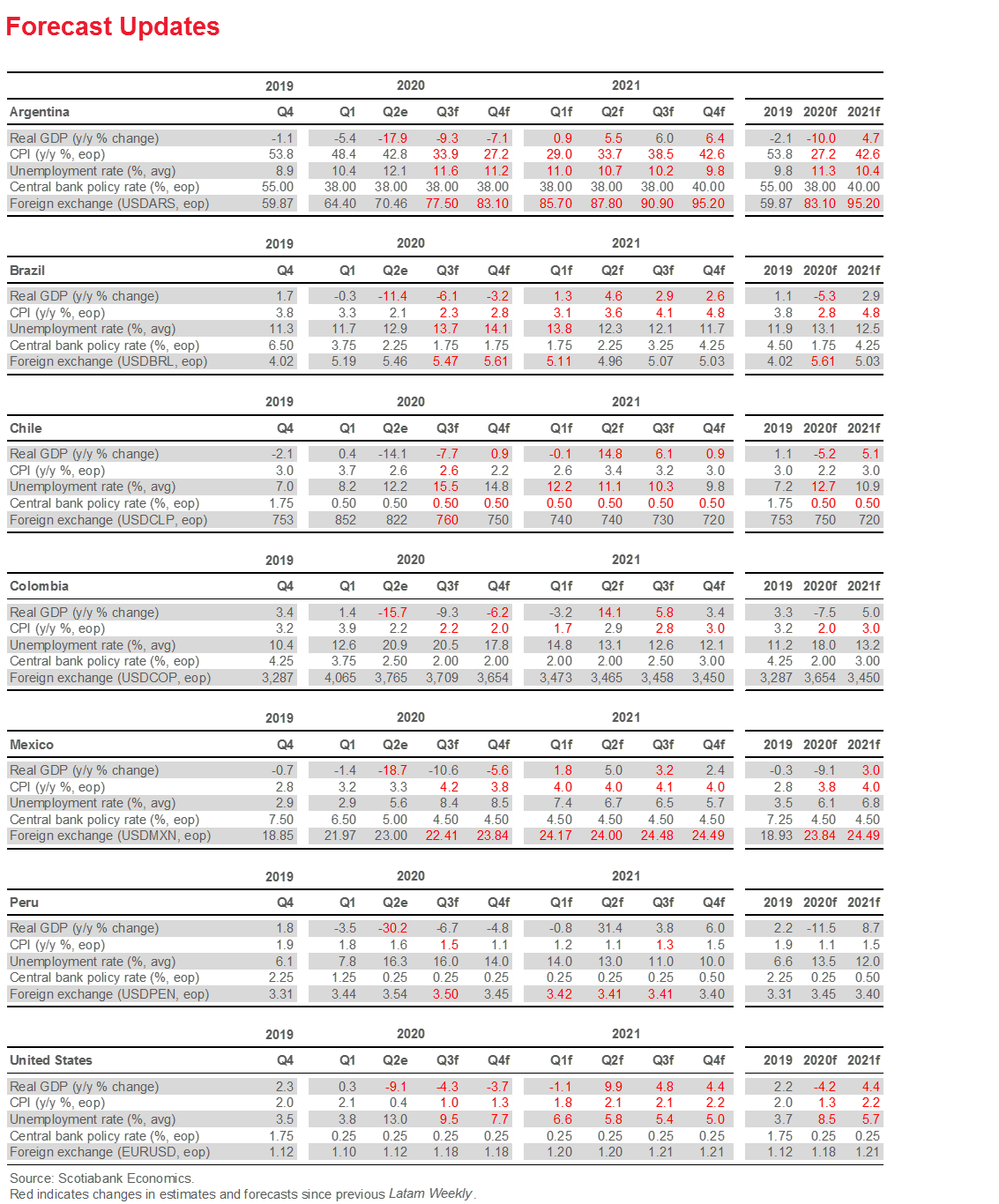

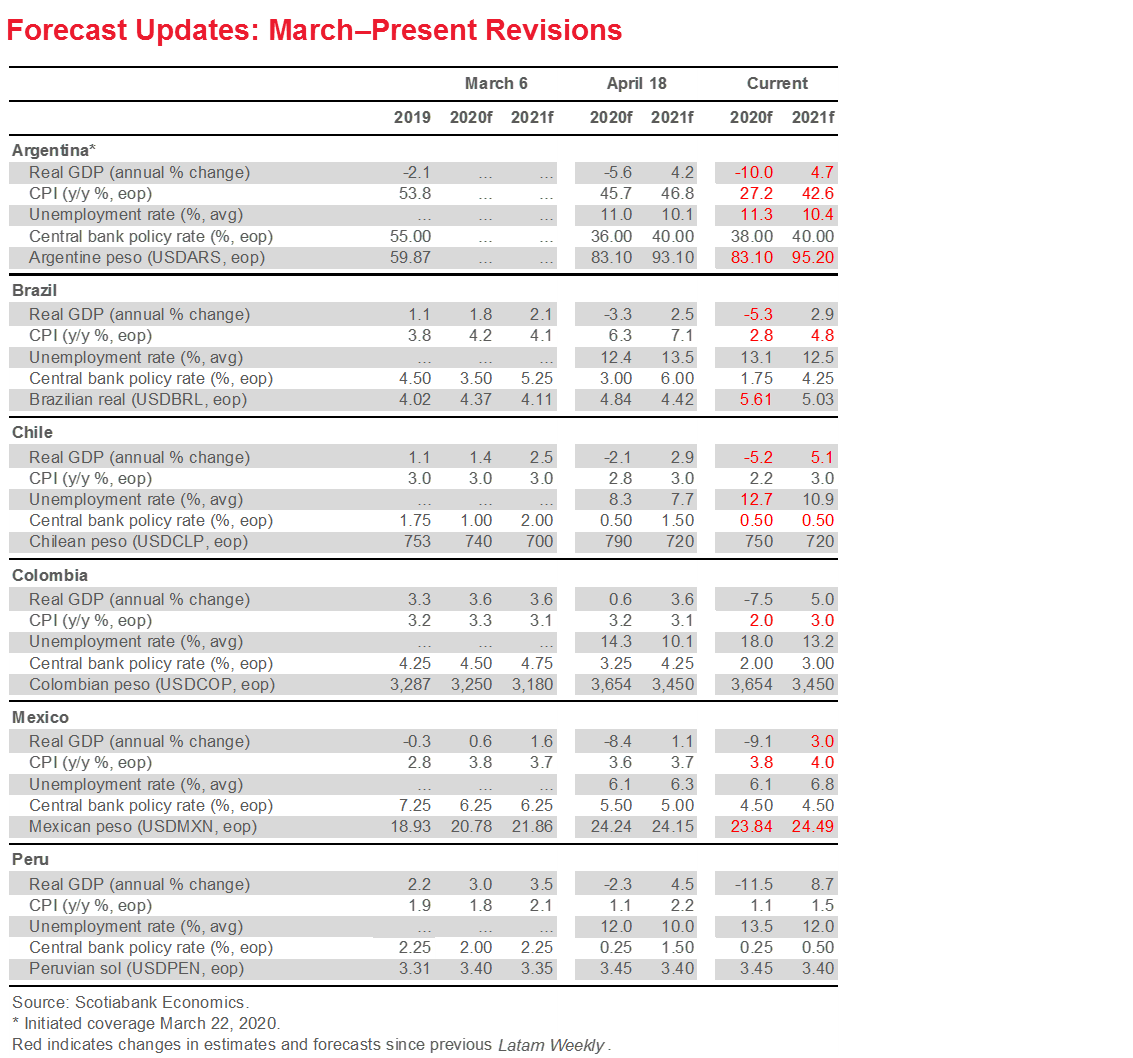

Our 2020 growth outlook has materially strengthened for Chile (from -6.0% y/y to -5.2% y/y) and Brazil (from -5.7% y/y to -5.3% y/y), while our forecast for Argentina has been cut from -8.1% y/y to -10.0% y/y as we mark to the country’s most recent data releases.

ECONOMIC OVERVIEW

We take stock of the first indicators on economic developments in Q3 and what they foreshadow about the road ahead.

MARKETS REPORT

Our macro strategy team looks at prospects for the MXN heading into the US presidential election through a comparative analysis of the peso’s performance in past US election years and some of the comparative specifics of 2020 versus 2016.

COUNTRY UPDATES

Concise analysis of recent events and guides to the fortnight ahead in the Latam-6: Argentina, Brazil, Chile, Colombia, Mexico, and Peru.

MARKET EVENTS & INDICATORS

Risk calendar with selected highlights for the period September 5–18 across our six major Latam economies.

Economic Overview: Soft Prices, Stronger Activity

Brett House, VP & Deputy Chief Economist

416.863.7463

Scotiabank Economics

brett.house@scotiabank.com

Our 2020 growth outlook has materially strengthened for Chile (from -6.0% y/y to -5.2% y/y) and Brazil (from -5.7% y/y to -5.3% y/y), while our forecast for Argentina has been cut from -8.1% y/y to -10.0% y/y as we mark to the country’s most recent data releases.

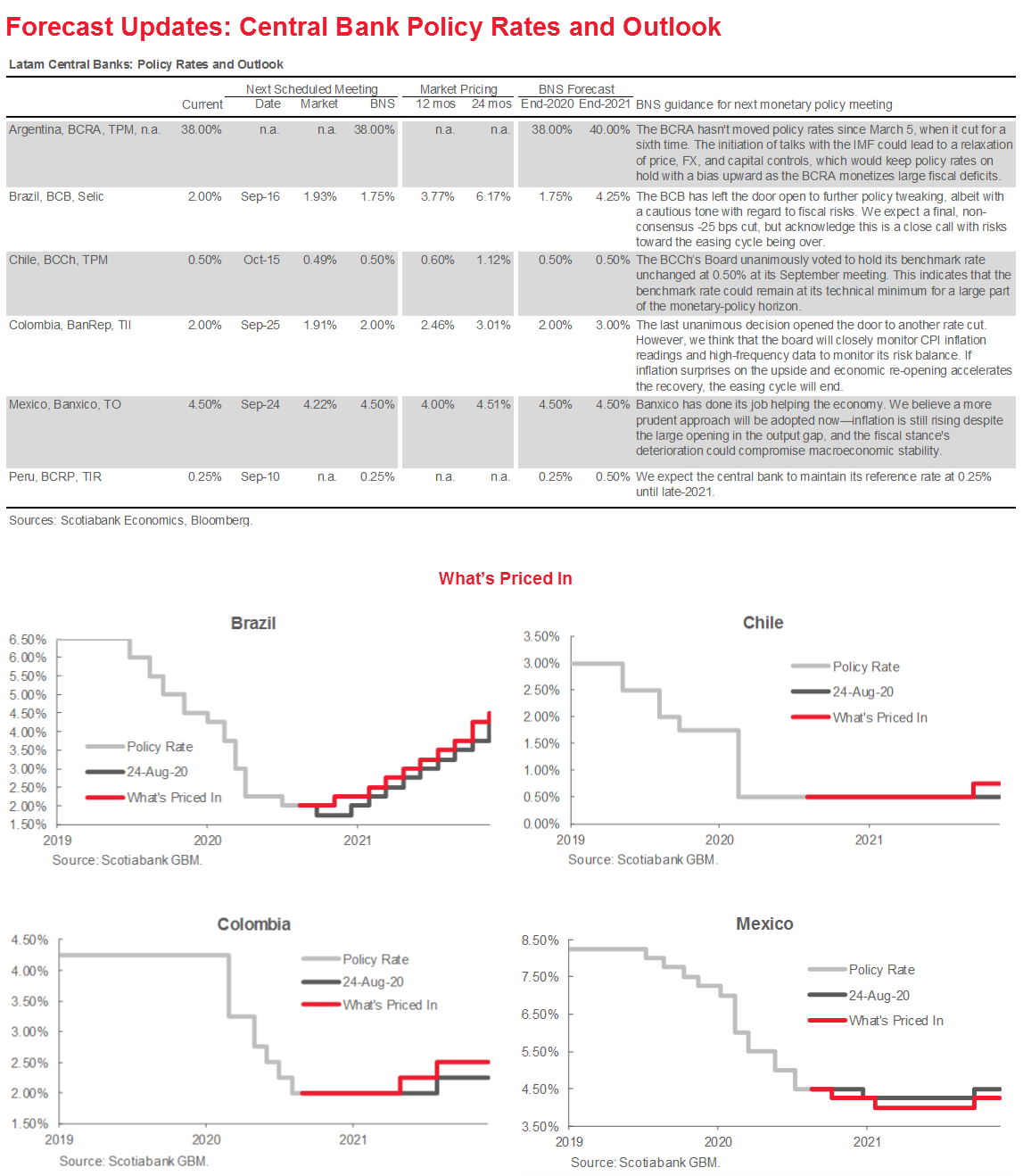

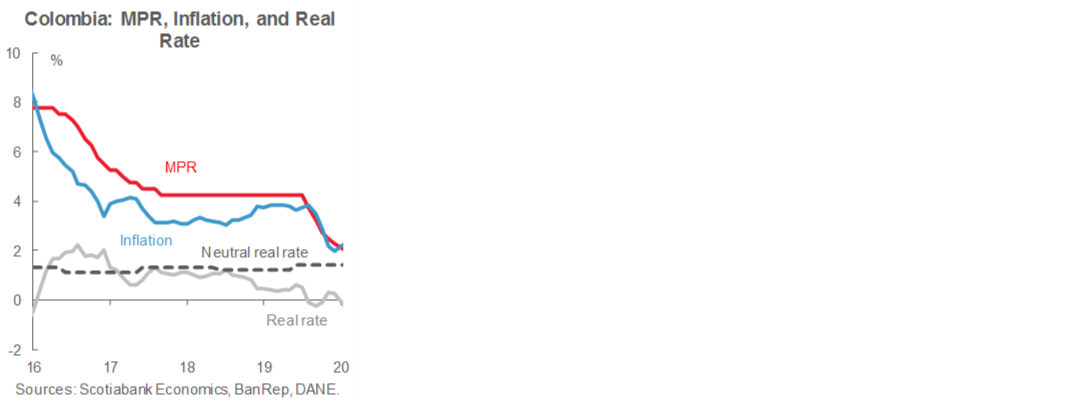

In upcoming monetary policy decisions, Peru’s BCRP is expected to remain on hold, while we anticipate an out-of-consensus final -25 bps cut from Brazil’s BCB.

In new macro data, inflation readings are set to remain subdued even as economic activity picks up further.

MARKET DEVELOPMENTS AND FORECAST UPDATES

Latam risk assets ended the week on a downbeat note following the tech sell-off and souring in general risk sentiment, with Latam equities bearing the brunt of the turn in major markets (table 1). Argentina’s Merval saw little reward for the conclusion of its foreign-law bond swap and the initiation of talks with the IMF, perhaps reflecting expectations that eventual agreement on a borrowing arrangement and adjustment program is likely to feature tighter fiscal constraints. Latam FX, in contrast, saw some support (table 2) from global liquidity, local pension withdrawals, and subsequent rebalancing.

In updates to our forecasts, our 2020 growth outlook has materially strengthened for Chile, rising from -6.0% y/y to -5.2% y/y, echoing the revised forecasts published last week by the BCCh (see Forecast Tables, pp. 2 and 3, and Chile Country Update). Similarly, stronger July and August data in Brazil have motivated us to raise our 2020 real GDP growth forecast from -5.7% y/y to -5.3% y/y. In contrast, our 2020 GDP growth forecast for Argentina has been cut from -8.1% y/y to -10.0% y/y as we mark to the country’s most recent data releases.

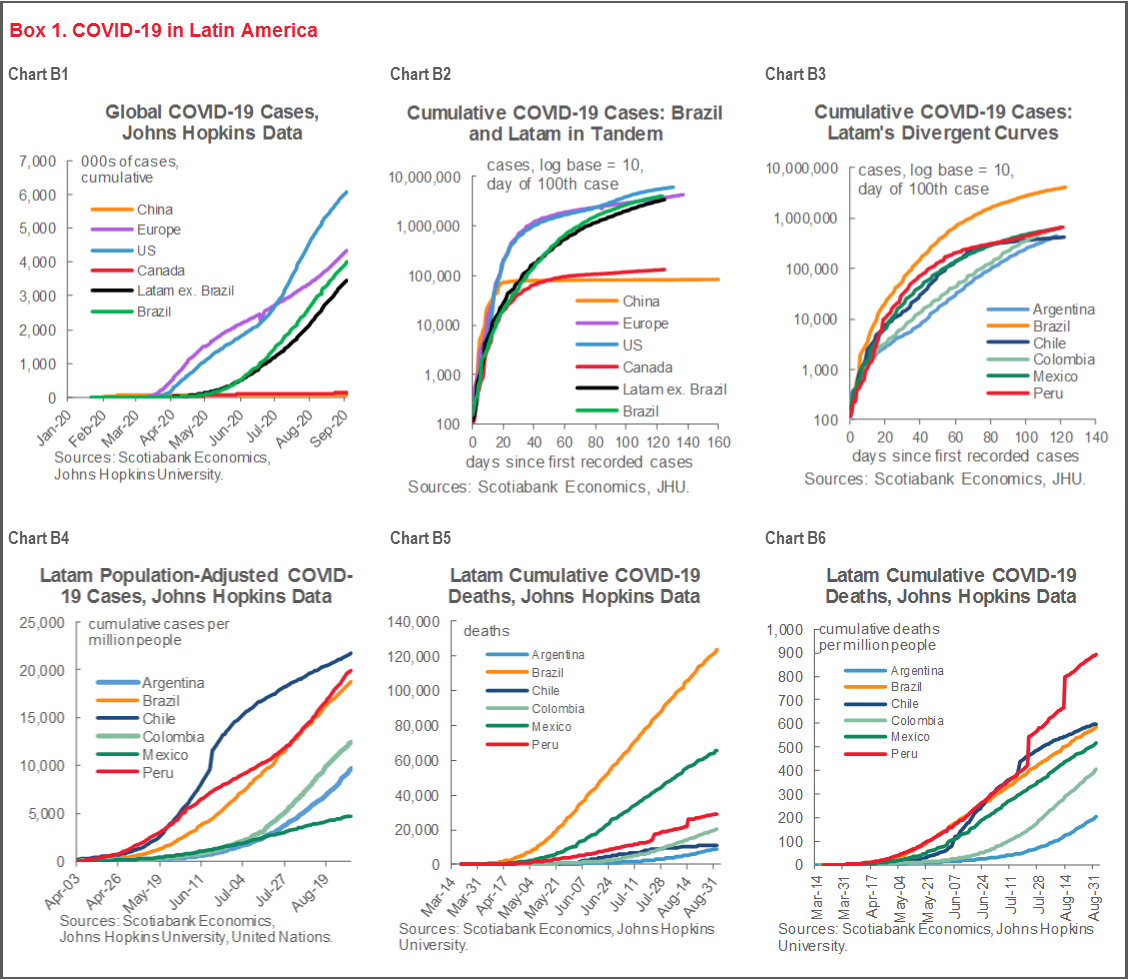

On the pandemic front (see box 1), data revisions continue to retroactively worsen the official numbers in Chile and Peru, while a surge in new positive tests in Argentina has caused both COVID-19 case figures and total deaths to rise meaningfully. Argentina now has the dubious distinction of moving past Chile with what are now the 10th largest COVID-19 case numbers in the world.

FORTNIGHT AHEAD

I. Central banks

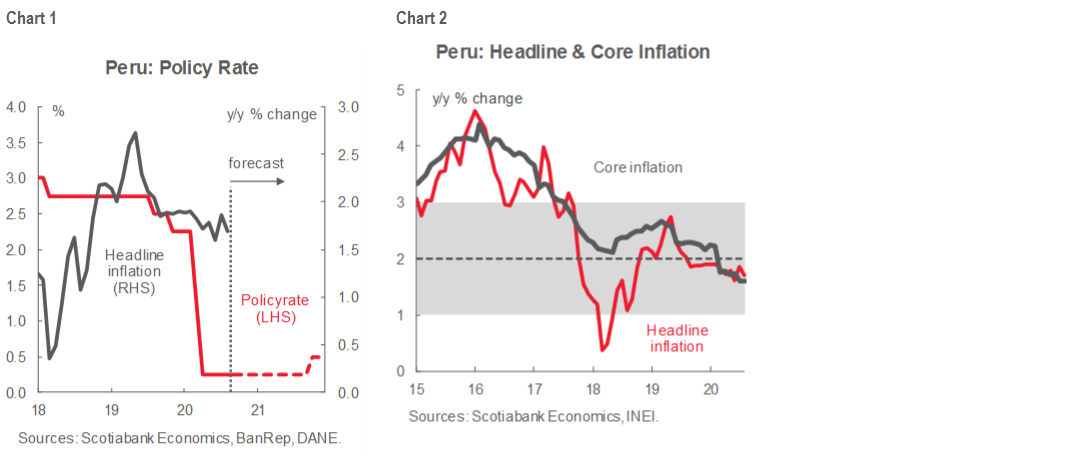

Peru. The Monetary Policy Committee of the BCRP meets on Thursday, September 10, and is universally expected to keep its headline policy rate on hold at 0.25%, where we expect it to remain until late-2021 (chart 1). Despite some improving, and in a few cases, better than previously expected macroeconomic prints since the previous MPC meeting on August 14 (see Peru Country Update), headline and core inflation continue to trend below target and are set to soften a bit further in our forecasts (chart 2 and Forecast Tables, pp. 2 and 3). In the MPC’s August 14 statement, Committee members reiterated their guidance that they would keep monetary policy expansive for “an extended period” and “so long as the negative effects of the pandemic on inflation and its determinants persist.” Any additional easing, if necessary would still come through “other instruments” such as credit and liquidity facilities, rather than through additional reductions in the headline policy rate.

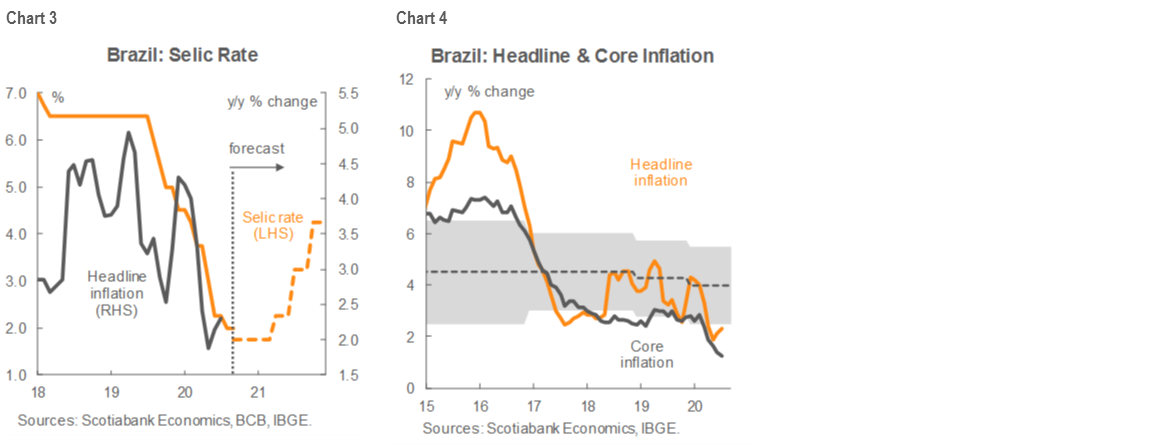

Brazil. The Copom is scheduled to make its next decision on the Selic on Wednesday, September 16: while the consensus points to a hold at 2.00%, we believe that risks are mildly tipped toward a final -25 bps cut to end this easing cycle at 1.75% (chart 3). As our Brazil Country Update details, this will be a tough decision for the BCB. Data for July and August clearly show that the bottom has been passed and the economy is recovering more quickly than previously expected. At the same time, the BRL remains the worst performing major currency so far in 2020, which presents ongoing material risk of pass-through inflation. Nevertheless, IPCA inflation remains below target (chart 4) and we don’t see evidence of mounting price pressures. In a tough call, our Brazil economist believes that the Copom will prioritize lifting growth over still-phantom inflation fears, particularly as fiscal support for the recovery is likely to be ratcheted back.

II. Macro data

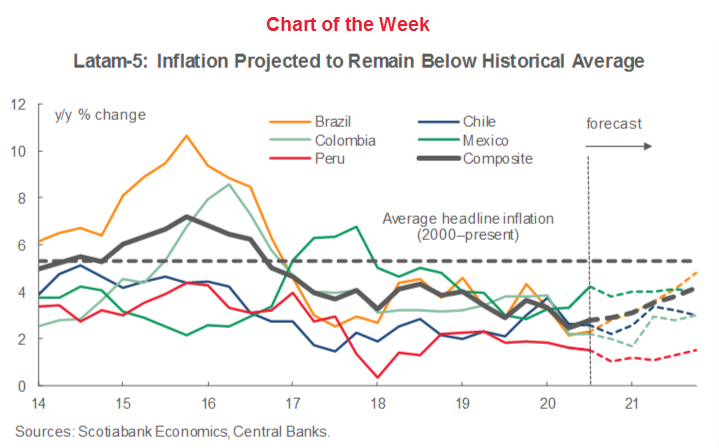

August inflation prints in Brazil, Chile, Colombia, and Mexico dominate the next fortnight along with July GDP proxies for Brazil, Colombia, and Peru. Across the five inflation-targeting regimes (i.e., ex-Argentina), price pressures are expected to remain broadly subdued over our forecast horizon to end-2021 (see the Chart of the Week) even as economic activity continues to pick up, albeit at a slowing pace, from the April-May lows.

Markets Report: MXN and the US Election

Tania Escobedo Jacob, Associate Director

212.225.6256 (New York)

Latam Macro Strategy

tania.escobedojacob@scotiabank.com

The results of the US 2016 presidential election triggered a violent reaction in the Mexican peso; as we approach the height of the campaigning season this year, concerns about what could happen to the Mexican currency this time around are starting to emerge.

We think that the 2016 presidential run was very specific in terms of what it put at stake, regarding commercial ties between Mexico and the US and immigration dynamics; a lot of things have changed between then and 2020.

With less of an MXN-specific shock expected in this election, we think the currency’s performance will reflect the excess of liquidity in the global financial system, which should provide strong support for risk assets, including EM currencies.

We remain constructive on MXN and think that levels closer to USDMXN 21.00 are possible in a recovery phase toward the end of the year.

FOUR YEARS LATER

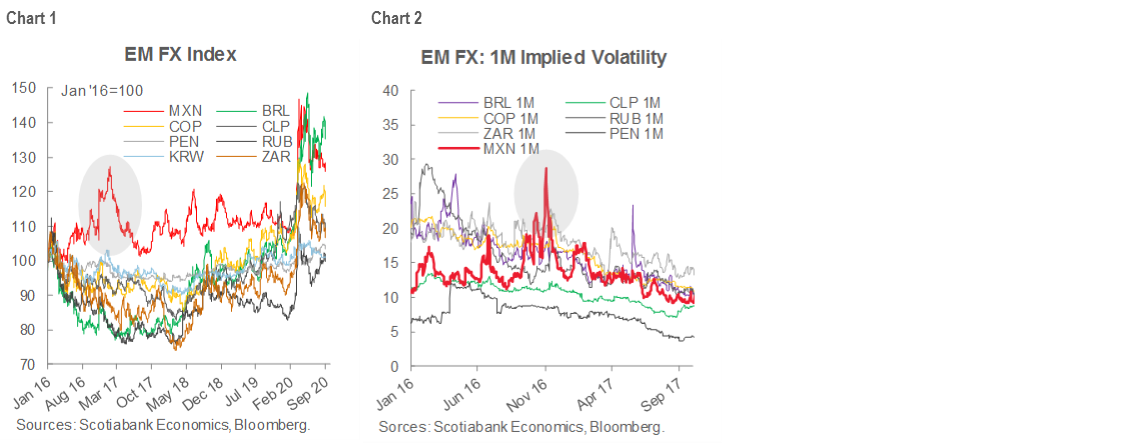

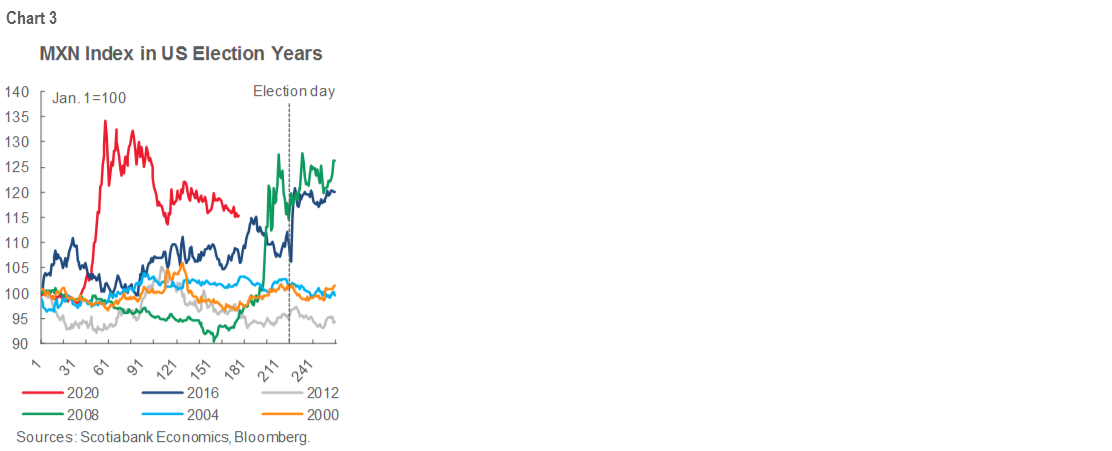

The 2016 US elections triggered a violent reaction in the Mexican peso, which lost 30% from its highest level that year to its weakest point reached just after the inauguration ceremony in January 2017. MXN was by far the worst performing EM currency during that period and has carried that additional risk premium persistently since then (chart 1). The spike in volatility seen in MXN going into and during the aftermath of the 2016 US elections exceeded that of its peers (chart 2), which resulted in a decision by the Banco de Mexico to intervene directly in the market by selling USD spot and by participating in the NDF market for the first time in its history (see here for Banxico’s announcements).

As we approach the US presidential election in November this year, concerns about what could happen to the Mexican currency this time around are starting to emerge. We think that the 2016 presidential run was very specific in terms of the content of the Republican campaign and of what it put at stake regarding commercial ties between Mexico and the US and immigration dynamics. The fact that the final result of the election was not clearly anticipated by the polls made the market reaction more abrupt, especially for Mexican assets.

THINGS HAVE CHANGED SINCE 2016

One of the most feared potential outcomes of the 2016 election—the disintegration of NAFTA—has been avoided and a new trade agreement has been approved by the three countries. The fact that the USMCA has Trump’s seal of approval and that it was thoroughly negotiated with Democrats as well, makes it less vulnerable, at least to material or huge modifications, if the White House changes hands. There will, of course, be some disputes and disagreements (such as the tariffs on steel and aluminum post-USMCA-agreement) that will not be avoided, but the presence of the new framework makes us think that the path of least resistance is for the trade conversation to move further out to Europe and Asia. Some observations on the Mexican labour market made by the Democrats might result in some noise, but the topic has already been addressed by both governments, so further discussion would not come as a surprise either.

On immigration, diplomatic negotiations seem to have reached an equilibrium, with Mexico taking some additional measures to contain flows of people within its borders. A fall in the number of illegal crossings has given the US Administration some leeway to claim that results on that front have been delivered. Of course, there is a very high probability of going back to a more aggressive stance on immigration, particularly as the economic crisis in Mexico and Central America might increase the flow of people in the coming months. The border wall will likely remain front and center within Trump’s rhetoric and we might see some threats of new taxes on remittances, for example, to finance its construction, but unlike the previous election, these headlines would not take the markets by surprise.

The Mexican Administration has set as a priority the maintenance of a close and healthy diplomatic relationship with the US and has, so far, ignored most US statements on controversial topics, such as the border wall. We think the political approach in Mexico will continue to prioritize the preservation of commercial ties with the US economy and will try to avoid conflict as much as possible, especially in relation to campaign-driven statements.

Former Vice-President Biden’s campaign is, in our view, less likely to create an environment of confrontation with Mexico during the campaign. Instead, it is likely to focus more on domestic issues such as the health care system, income re-distribution, and clean energy infrastructure (see here for a summary of the Democratic and Republican platforms).

All in all, we think that with the information made available in the last four years, the effects of the US campaign and election on MXN will be less violent than in 2016 and closer to what we saw in previous elections. To get an idea of what to expect, we look at the behavior of MXN in those periods and its performance relative to peers.

WHAT TO EXPECT NOW…

If we look at the behaviour of MXN in other year US election years, we note that its fluctuations were typically more stable than in 2016 (chart 3). The exception of course, was 2008, but that can be attributed to the global financial turmoil that started in September that year and that resulted in the strengthening of the US dollar. In the three other election years shown, we did not see major variations.

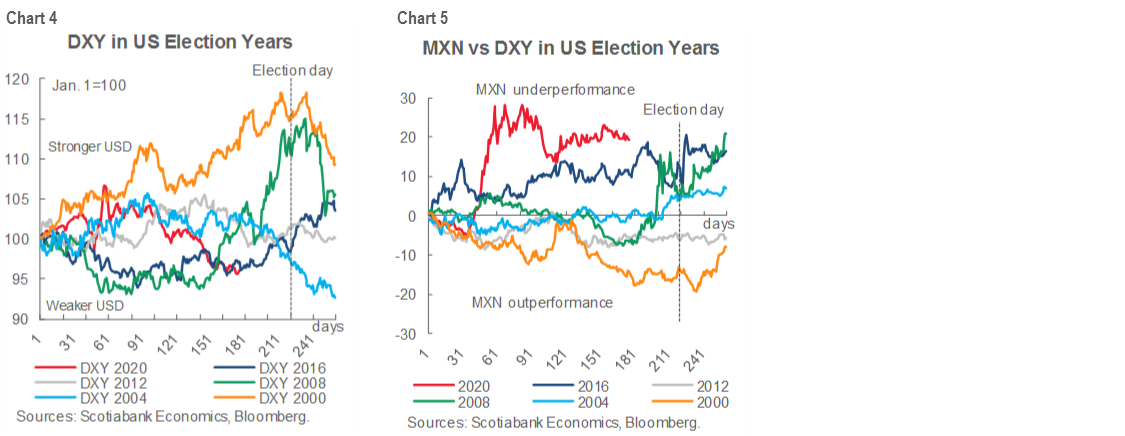

To see how the MXN behaved with respect to other currencies and to see if there is a pattern of a consistent underperformance into a US election, we compare its past fluctuations with that of the DXY and a Latam FX index. When looking at the deviations of MXN from the DXY index (chart 4 and 5) we do not identify a striking trend in any direction. Chart 5 shows the difference in MXN fluctuations, relative to moves in the DXY, and captures any strengthening or weakening beyond what could be explained only by USD trends. If MXN moved one-to-one with the US dollar index, the line would be at zero. Although there is no identifiable pattern going into past US elections, the graph does show evidence of the well accepted notion that in periods of broad dollar strength and market stress, the Mexican peso, being a high beta, EM-risk currency, tends to underperform the DXY index.

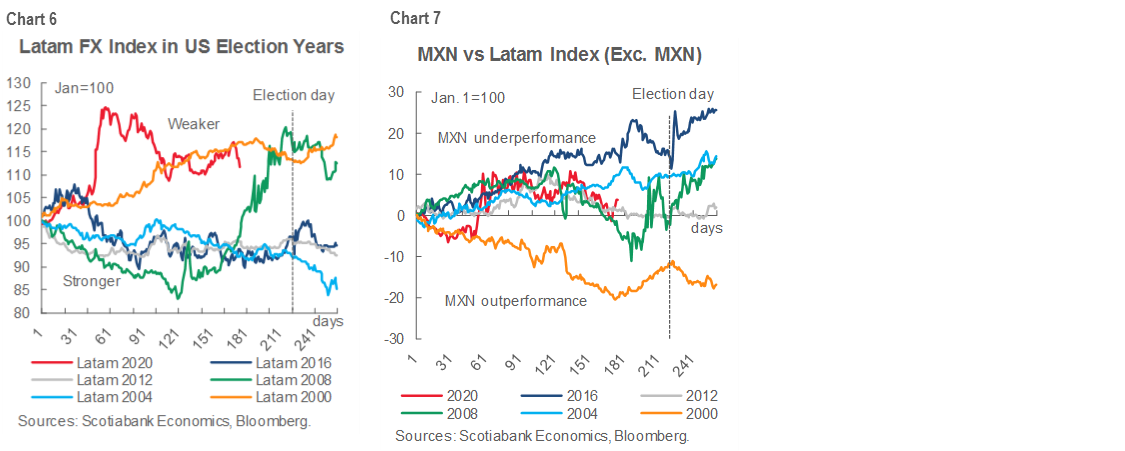

When compared to the Latam FX index (chart 6 and 7), there is also little in terms of a consistent pattern in US election years, but it does confirm that the noise in 2016 was mostly specific to MXN.

With less of an MXN-specific shock expected in this election, we think the currency should behave in line with the overall risk sentiment. Our G10 strategists think that as markets start to focus more intently on the battle for the White House (and Congress) in the coming weeks, uncertainty may provide the USD with a little support. In the longer run, however, broader global economic and monetary policy settings are likely to have more influence on the USD’s direction than who wins the election. In short, we think the USD may benefit somewhat from precautionary positions ahead of the election, even more so considering the accumulation of USD short positions in recent weeks, but that in the end, the excess liquidity available in the global financial system will remain a strong support for risk assets, including EM currencies.

CONCLUSIONS

In conclusion, while the Scotiabank Economics forecast anticipates USDMXN remaining around 24 over the projection horizon to end-2021, Scotiabank’s macro strategy team sees probabilities biased towards lower levels of USDMXN in the coming months, though the magnitude of the rallies is unlikely to be extreme. Levels of USDMXN at 21.00 seem possible in a recovery phase towards the end of 2020, which would represent an unwinding of about half of the MXN losses we saw this year. In a very positive scenario, where global growth proves more resilient than expected and risk appetite recovers quickly, we could see the pair trending to and stabilizing around the USDMXN 20 mark. This would still be well off the pre-crisis highs in the USDMXN 18s range owing to the likely pandemic damage to the economy and to fiscal balances in the coming months. The strategy team’s relatively optimistic view for MXN is driven by the expectation that, although the fundamentals of the Mexican economy will be worse off after the crisis, prices are already accounting for an aggressive mix of “worst case scenarios” (i.e., longer epidemic, extremely sharp recession, L-shaped recovery, and fast fiscal deterioration). In the aftermath of the crisis, the massive injections of cash that central banks have deployed globally will likely prompt a new hunt for yield; Mexican assets and the MXN are likely to benefit.

COUNTRY UPDATES

Argentina—Fundamentals Imply Further ARS Depreciation

Brett House, VP & Deputy Chief Economist

416.863.7463

brett.house@scotiabank.com

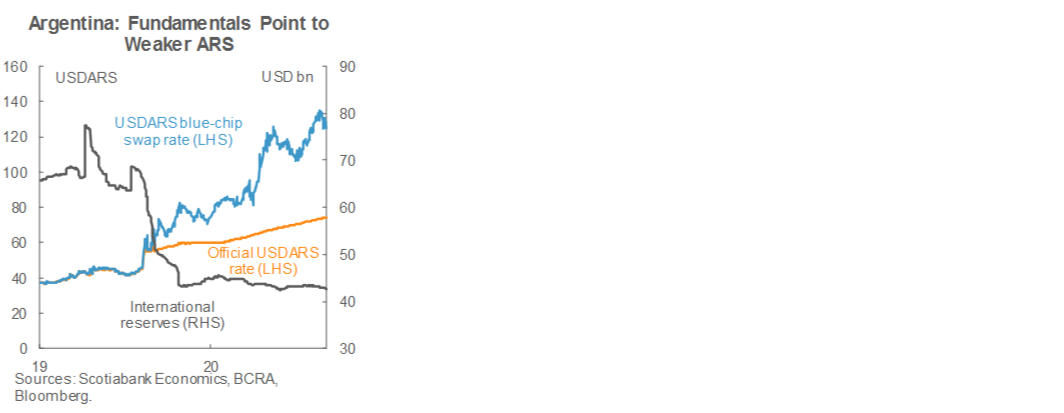

The initiation last week of talks with the IMF on a new borrowing and policy adjustment program almost certainly means that a relaxation, however gradual, of price, FX, and capital controls will be under discussion and in the offing as we move into 2021, which would precipitate accelerated depreciation in the official USDARS exchange rate despite Pres. Fernandez’s protests over the last few days that his administration isn’t contemplating a devaluation. Argentina’s authorities imposed currency controls on September 1, 2019 in response to a slide in the value of the ARS as it became clear that former-President Macri’s administration was likely to be swept from office in the October 2019 elections. The initial controls meant that purchases of more than USD 10,000 would require official approval. The BCRA tightened the limit to USD 200 at the time of the country’s presidential elections on October 27, 2019. Since then, a variety of controls, reviews, and limits on FX and capital-markets transactions has been intensified. As a result, the blue-chip USDARS cross has widened to around twice the official USDARS exchange rate and FX reserves have steadily dripped out of the country (see chart). The blue-chip rate is a far better reflection of underlying fundamentals than the largely fictional official rate, which is little more than a gradual crawling peg that will converge with the blue-chip rate once controls are loosened. We see the official rate moving from the current USDARS 74.32 to around the mid-80s by end-2020 and mid-90s by end-2021 on current conditions (see the Forecast Tables at the front of this report).

Risks point toward a faster and more substantial depreciation under an IMF-supported program; neither a new IMF loan nor recent progress on regularizing Argentina’s relationships with creditors is likely to provide sufficient confidence effects to mitigate the array of macro fundamentals that are weighing on the ARS. Three years of recession have led to wider fiscal deficits which have been financed by the BCRA. As a result, major monetary aggregates have grown by around 50 to 60% y/y through August. Headline inflation is running at over 40% y/y and would be higher were it not for official price controls on major utility fees and government “monitoring” of prices on over 2,000 other goods and services. Although base effects driven by last year’s spike in prices imply that headline y/y inflation prints are likely to come down over the remainder of 2020, inflationary pressures are not softening—if anything, the combination of COVID-19 constrained domestic production, the slide in the blue-chip ARS, and the whir of the BCRA’s printing presses together suggest that sequential month-on-month inflation should move higher into 2021.

Nevertheless, looking at the short-term, economic data and developments over the coming fortnight are likely to be mildly encouraging even though Argentina’s COVID-19 numbers have recently worsened, pushing it ahead of Chile as the country with the 10th greatest numbers of positive cases globally. This week’s swap of defaulted foreign-law bonds is set to be followed by the restructuring of domestic-law debt. July capacity utilization numbers, out on Thursday, September 10, should show a significant improvement while the August government budget balance, set to be delivered some time on or after Monday, September 14, is likely to point to at least a temporary stabilization in public finances. Given the aforementioned controls on prices, FX, and capital transactions, Argentina’s CPI remains an unreliable reflection of underlying inflationary pressures. We have pencilled in 2.00% m/m for the August reading out on Wednesday, September 16, in line with July’s 1.90% m/m. Base effects mean this would bring year-on-year inflation down from 42.4% to 39.7% y/y, even though sequential price growth is firming up.

Brazil—A Tough Decision Looms for the BCB; We Lean Toward a Non-Consensus -25 bps cut

Eduardo Suárez, VP, Latin America Economics

52.55.9179.5174 (Mexico)

esuarezm@scotiabank.com.mx

The Brazilian DI curve is no longer pricing any rate cuts from the BCB. However, our call is that we will get one more -25 bps cut in the upcoming meeting before the BCB ends its easing cycle. We think there are macro data supporting either alternative; this will be a tough decision for the Copom.

Supporting an end to the easing cycle:

· Q2 just showed a -11.4% y/y contraction (by far the strongest contraction since the 1990s), but data for July and August suggest the economy has already bottomed and is recovering rather quickly. July manufacturing PMIs were already back in positive territory (58.2), and the services PMI had recovered about halfway from its worst point (although it was still at 42.5). The strength of the manufacturing PMI, as well as the resilience of mining and agriculture components in GDP, still suggest the economy’s recovery was led by external demand (supported by the strong trade surplus of over USD 8 bn in July). The domestic demand side is also gathering steam, with June retail sales printing at +0.5% y/y. However, the domestic demand bounce is still on shaky footing. The government’s fiscal adjustment hiccup in the Senate, where the continued freeze of civil servant wages proved more difficult than anticipated, is seen as a one-off, and legislative support for the fiscal correction measures seems to be gaining momentum alongside President Bolsonaro’s approval rating—which is now even with his disapproval rating. However, the country’s fiscal stance will likely remain tenuous even with progress on the adjustment, given that the necessary fiscal correction is massive (pre-COVID-19, the general government deficit was likely to be around 7% of GDP, and in the COVID-19 world we’re likely to see a primary deficit of around 10% of GDP, and a general government deficit in the 16–18% of GDP range). The Copom has repeatedly pointed at fiscal risks as one of the main factors capping its easing room.

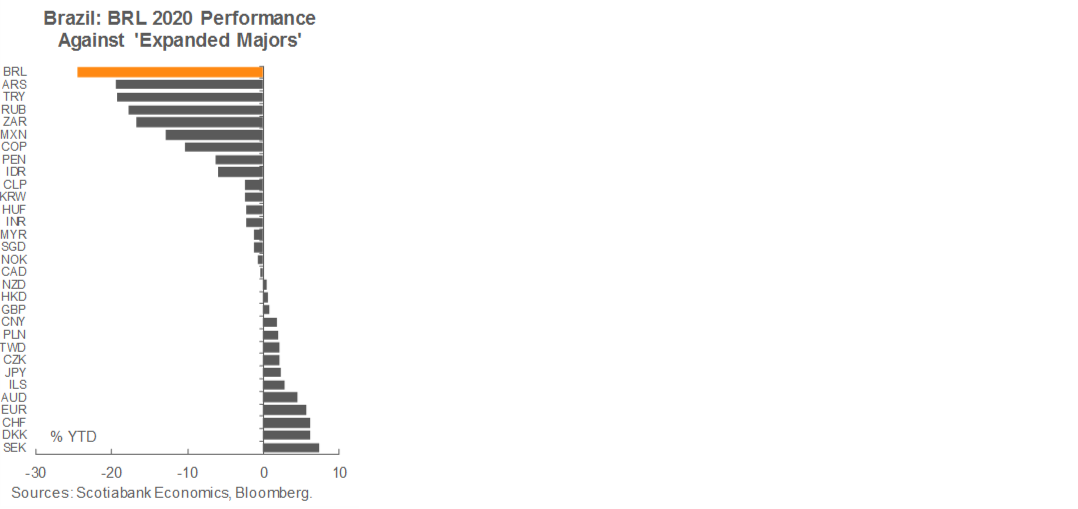

· The BRL is the worst performing currency among Bloomberg’s 31 “Expanded Majors”, down -24.6% YTD. Even though the spectre of FX-inflation pass-through remains invisible so far, it cannot be ruled out—adding an additional warning sign for the BCB.

· Since DI rates are no longer pricing in any rate cuts by the BCB, and as the Copom’s latest statement said, any remaining room for cutting is marginal, in a close decision the central bank may decide it is better not to surprise markets at a time when the BCB is under pressure.

Supporting additional easing:

· Despite the recent rise in IPCA inflation (it is now hovering around 2.3% y/y), its increase has been very gradual, and broadly in line with recovering commodity prices. We have not seen any major evidence of an inflationary spiral taking hold—at least up to this point. In addition, inflation remains at around half the mid-point of the BCB’s target, and despite the -25 bps reduction in the target for next year, the mean expectation in the BCB’s latest Focus Survey has inflation below target in both 2021 and 2022.

· Even though the economy is recovering, we expect that GDP will see negative prints for the remainder of the year. With inflation seemingly under control, we see room for the BCB to continue to support the rebound—prioritizing growth over inflation.

· The extension of the government’s economic crisis package is likely to see the BRL 300 / month support for low-income households halved from now onwards, implying lower fiscal support for still-weak domestic demand. In an environment where the rebound is still uncertain, an additional injection of monetary stimulus could offset the looming decline in fiscal support.

· Even though we doubt the Copom will be playing politics, Bolsonaro’s resurgence in popularity has come at the same time as the economic rebound. This popularity increase appears to be linked to rising support for fiscal adjustment. Hence, supporting the economy could align with the BCB’s desire to see the country’s fiscal stance propped up.

Overall, we think the next Copom meeting will be a close decision between a final -25 bps cut and declaring an end to the cycle. Our sense is that, with the rebound still on shaky legs, one final -25 bps cut is warranted, but the decision is not clear cut.

Chile—GDP to Fall -5.2% in 2020, with a Rebound of 5.1% in 2021

Jorge Selaive, Chief Economist, Chile

56.2.2939.1092 (Chile)

jorge.selaive@scotiabank.cl

Carlos Muñoz, Senior Economist

56.2.2619.6848 (Chile)

carlos.munoz@scotiabank.cl

These past few weeks have been full of tier-1 economic releases. On August 28, employment data was published. The unemployment rate stood at 13.1% in the May–July moving quarter, somewhat above what was expected by consensus (12.8%). This print was affected by a new drop in employed workers (less than previous months), but was partially mitigated by a fall in labour participation. The employment rate, on the other hand, fell to 45%, compared with levels of around 58% at the beginning of the year, and a potential of around 57% for the same period in previous years. A very likely scenario during the coming months is that the unemployment rate remains high and may even experience an increase despite improved activity numbers. The labour market will likely lag behind economic growth despite increased re-opening measures at the national level. Many people could return actively to seeking work (increasing the workforce), but they may not quickly find available positions.

On September 1, monthly GDP data for July was released, and again showed signs of recovery, particularly in non-mining activity, which grew 1.8% m/m seasonally adjusted—its second straight month of expansion. Compared with last year, aggregate economic activity was still down -10.7% y/y, but this was better than anticipated by market consensus (-12.0% y/y). Most notably, the July improvement occurred in a context where quarantine measures were still strict, so for August we anticipate a year-on-year contraction in the single digits. The mining sector continued to show moderate but sustained growth with higher grade of ore recorded in some private sector operations. Despite these gains, the impact of the mining sector on total GDP is still practically nil because of the continuing significant year-on-year contractions in the non-mining sector of the economy

Also, on September 1, the central bank held its Monetary Policy Meeting, which was followed by the release of its Monetary Policy Report (IPoM) on September 2. The BCCh’s Board unanimously voted to hold its benchmark rate unchanged at 0.5% but signaled that it is open to adapting monetary stimulus measures, if necessary. The Board observed that the economy had stabilized after GDP growth in June and July came in better than anticipated in the BCCh’s baseline scenario. In line with the confidence expressed regarding the economic recovery and lower disinflationary pressures, the Board indicated that the BCCh’s benchmark rate would remain at its technical minimum “for a large part” of its monetary-policy horizon. All in all, in the baseline scenario expressed in the IPoM, the CB now expects a GDP contraction in the range of -5.5% to -4.5% y/y for 2020, with a recovery between 4.0% and 5.0% y/y for 2021, very much in line with Scotiabank’s baseline scenario.

Given the improved figures regarding the spread of COVID-19 in Chile, the government announced on August 30 that some parts of Greater Santiago would enter the third phase of the Paso a Paso plan, meaning lower restrictions to mobility and the re-opening of some key services, such as restaurants and coffee shops, along with the permission for social gatherings of up to 50 people. The third phase started Wednesday, September 2.

Next week, we will know the inflation print for August, where we expect a CPI of 0.1% m/m, which implies an annual inflation rate of 2.4%. For year-end, we maintain our projection of 2.2% y/y annual inflation, as the recovery in activity—along with a boost in consumption given the measures implemented to support household income—would put upward pressure on both goods and services prices. In the month of August, pension contributors requested the withdrawal of USD 12 bn from their pension fund accounts. At least half of these funds released by the Pension Fund Administrators would be destined for consumption. For activity, on the other hand, we project that real GDP will fall -5.2% y/y in 2020 (from our previous forecast of -6.0% y/y), as the latest data available have shown resilience in the Chilean economy; we anticipate better figures for August onward given the lifting of lockdown measures. For 2021, we estimate that real GDP will expand 5.1% y/y (from our previous estimate of 4.4% y/y).

Colombia—A 180-Degree Change in Re-opening Strategy: Will It Work?

Sergio Olarte, Head Economist, Colombia

57.1.745.6300 (Colombia)

sergio.olarte@co.scotiabank.com

Jackeline Piraján, Economist

57.1.745.6300 (Colombia)

jackeline.pirajan@co.scotiabank.com

Data in Colombia are behaving in a manner similar to data in the rest of the world. Recovery is highly correlated with the government’s re-opening strategies, especially since, so far, the COVID-19 / oil-price shock has not had much spillover into confidence issues. For instance, BanRep’s liquidity measures have mitigated most possible deteriorations of market confidence that could amplify the effect of the real shock. Therefore, recent news of a more-aggressive-than-expected re-opening strategy in Colombia beginning in September is very relevant in terms of economic recovery and monetary policy response.

On September 1, the government asked the population to exercise self-restraint and social distance with the entry of a lockdown strategy focused on the actual infected and possibly infected populations. The new approach is called "selective isolation" with free mobility and a focus on individual responsibility. However, it will not allow mass gatherings such as concerts and sports events, while regional autonomy remains in place to oversee local re-opening arrangements.

This week, sixteen airports opened for domestic flights; inter-municipal transportation also opened completely, while in Bogota, open-air restaurants are now allowed to operate, and access to some parks and open-air activities is also allowed. This 180-degree change in approach by the Colombian authorities tilts economic activity risks upward for Q4-2020. However, we will watch three things before we decide to change our GDP forecasts:

1) Whether the health system can afford the possible new increase in COVID-19 cases. Otherwise, it is very likely that Bogota and Medellin could again close their borders and reinstate mobility restrictions;

2) Whether some regional restrictions weigh against the recovery pace, especially in Bogota—where the majority of sectors are open, but are working a reduced number of business days; and

3) Whether the demand side of the economy responds as aggressively as the re-opening strategies, and private consumption shows an additional recovery, especially since the urban unemployment rate continues above 24%.

In terms of monetary policy, the August meeting result was as expected. BanRep delivered a -25 bps cut to 2.00% and left the door open to further cuts if needed. We think the BanRep’s Board and staff share our concerns regarding the government’s new re-opening strategies. Therefore, September’s high-frequency data will be critical for BanRep’s next decision (September 25). Energy demand, gasoline demand, debit and credit card transactions, and mobility data are important to follow this month, along with the COVID-19 daily statistics. If economic activity data point to a better-than-expected Q4 and August inflation shows that its downtrend is over (as we expect), we think BanRep will prefer to stay put at 2.00% for the rest of the year.

Mexico—Information Overload

Mario Correa, Economic Research Director

52.55.5123.2683 (Mexico)

mcorrea@scotiacb.com.mx

The last two weeks were loaded with information.

Gross Domestic Product (GDP) figures for Q2-2020 were released, showing the detailed sectoral performance of the economy. GDP contracted -18.7% y/y (versus -18.9% y/y previously advanced). By components, the industrial sector fell -25.7% y/y, while the service sector shrank -16.2% y/y. The agricultural component showed a modest reduction of -0.5% y/y. As expected, there were some dramatic numbers never seen before in sectors such as recreational services (-76.9% y/y), restaurants and hotels (-70.4% y/y), and transport, couriers and warehousing (-39.3% y/y).

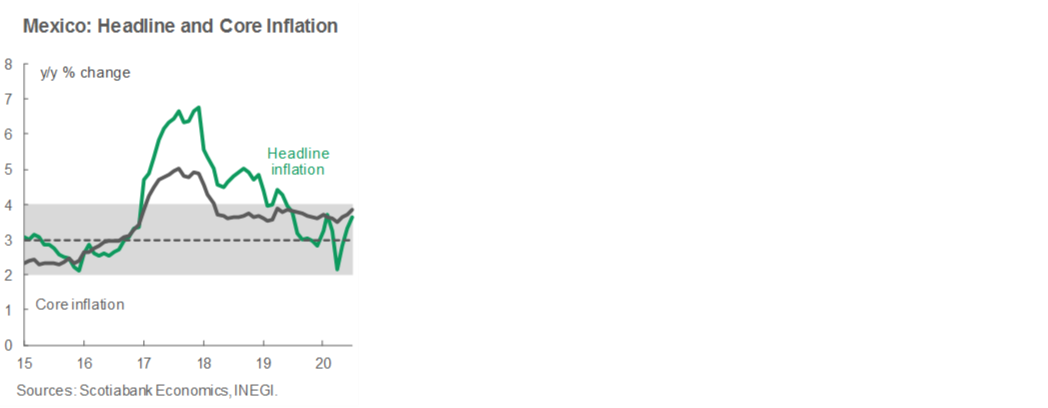

Inflation surprised once again on the upside. The CPI increased 0.24% 2w/2w in the first fortnight of August, surpassing by far the consensus of 0.16%, and the -0.08% printed a year ago. Core inflation came in at 0.18% 2w/2w, exceeding both the 0.15% consensus and the 0.11% recorded a year ago, driven by a 0.26% increase in merchandise prices and by a 0.09% increase in services. Non-core inflation accelerated to 0.43%. In annual terms, headline inflation kept climbing to reach its highest pace since June 2019, increasing from 3.66% y/y to 3.99% y/y, while its core component rose from 3.86% y/y to 3.93% y/y (versus 3.77% y/y a year ago).

Retail sales showed some improvement in June following record collapses in April and May, but still remain well below pre-pandemic levels. Retail sales growth accelerated from 0.8% m/m in May to 7.8% m/m in June, while wholesale sales rebounded from a decrease of -5.1% m/m to 11.1% m/m. In real annual terms, both categories continued to report strong declines: for retail there was a -16.6% y/y drop, from -23.7% y/y in May, in line with market expectations. Meanwhile, wholesale sales saw a stronger improvement, from -25.9% y/y in May to -12.8% y/y in June (versus -4.8%y/y in June 2019).

Balance of payments figures for Q2 showed a nearly even current account (i.e., a USD 5 mn surplus) mainly as a result of a lower deficit in the income and interest component and a stronger surplus on the transfers side. The financial account posted a relatively small surplus of USD 662 mn. Foreign direct investment in Mexico stood at USD 6.6 bn, significantly less than the USD 11.4 bn in the previous quarter, but similar to the USD 6.4 bn recorded a year earlier. It is worth noting that Mexican direct investment abroad, which represents an outflow of capital, was very strong at USD 5.0 bn; while money-market investment posted a USD 8.7 bn outflow.

Banco de Mexico presented its Quarterly Inflation Report on Wednesday, August 26, which contained a detailed account of the performance of the economy during the period of greatest disruption generated by containment measures, along with Banxico’s resultant forecast revisions. The central bank reaffirmed that "in the current situation it is not possible to present a central scenario for forecasting economic activity", so they updated the three scenarios previously presented, with a notable deterioration in the numbers for 2020. The Type V scenario, that we could call relatively optimistic, features a contraction of -8.8% y/y, while the most pessimistic, Type U Deep, contemplates a contraction of -12.8% y/y. By 2021, the Type V and Type U scenarios contemplate a higher growth rate of 5.6% y/y and 1.3% y/y, respectively, likely owing mainly to base effects from 2020. On the other hand, the forecasts for inflation are revised slightly upward over the short term. The revision for Q3 particularly stands out, with increases to 3.9% y/y for both general and underlying inflation, a response to the rebound that has recently been observed in the dynamics of prices. However, within the horizon of influence for monetary policy—from 12 to 24 months—the expectation of inflation declining toward the 3% target is maintained. One of the central arguments for this expectation is that the notable output gap that has opened in the economy will end up being the main determinant for curbing inflation. However, Banxico pointed out that the outlook for inflation remains highly uncertain and without a defined risk balance.

Finally, there is no clear message to drive the anticipation of future monetary policy decisions. Nor is there a more ample analysis of the deterioration of the fiscal position and its possible implications for macroeconomic stability and the conduct of monetary policy—beyond the concern expressed about the possibility of further downgrades to the sovereign and Pemex ratings. By avoiding these topics, Banxico leaves open its options to act as it deems necessary in its next monetary policy decisions.

Banco de Mexico also released on Thursday, August 27, the Minutes of the most recent monetary policy decision On August 13, revealing that the Deputy-Governor Irene Espinosa was the dissenting vote, noting the troublesome increase in inflation as the main argument for the dissent. There is an intense debate about the inflation outlook and right monetary policy response inside the Board, with Mrs Espinosa and Mr Guzman apparently on the hawkish side, Mr Heath and Mr Esquivel in the dovish group, and Mr. Díaz de León in the middle, not clearly on either side. With inflation climbing and public finances deteriorating, a more prudent stance on monetary policy would normally be required, and so we think the Board will take a pause in the easing cycle, but it will be a close call with a potential additional cut in the reference interest rate still ahead.

Trade balance figures for July surprised with a record surplus USD 5.8 bn—the highest ever recorded—surpassing the market consensus expectation of USD 429 mn and a deficit of USD -1.3 bn in the same month last year. This was caused mainly by a stronger decline in imports (-26.1% y/y versus -22.2% y/y in June), while there was a smaller reduction in exports (-8.9% y/y versus -12.8%y/y previously).

Financial activity presented a mixed performance in July, with deposits growing strongly at 8.8% real y/y; while banks’ financing to the private sector barely grew 0.8% y/y. Credit for firms and entrepreneurs slowed from 5.7% y/y in June to 3.9% y/y in July; mortgage lending remained comparatively stable, growing 5.7% real y/y (versus 6.0% in June) and consumer credit deepened its contraction, from -6.0% in June to -9.2% in July, the steepest decline in a decade, signalling a weakened consumer.

Public finance figures deteriorated once again in July, recording a MXN -414.6 bn deficit for the first seven months of the year, larger than the MXN -387.3 bn budgeted for the period and greater than the MXN -153.1 bn deficit observed in the same seven months of 2019. The primary balance saw a MXN 9.8 bn surplus, below the MXN 39.7 bn surplus in the program and well below the MXN 215.8 bn surplus observed in the same period of 2019.

In Banco de Mexico’s latest monthly Survey of Expectations, the average projection for the 2020 real GDP growth rate was virtually unchanged, improving from -10.02% y/y in July’s survey to -9.97% y/y. In the same direction, the average forecast for 2021 changed from 2.88% y/y to 3.01% y/y. Average forecasts for headline and core inflation at end-2020 rose from 3.64% y/y to 3.82% and from 3.72% y/y to 3.82% y/y, respectively. For end-2021, the average headline inflation forecast remained almost unchanged, ticking up slightly from 3.56% y/y to 3.60% y/y, but core inflation moved more substantially from 3.38% y/y to 3.50% y/y. The average USDMXN projection for end-2020 improved from 22.69 to 22.61; for end-2021, the average exchange-rate projection weakened slightly from USDMXN 22.68 to 22.71. As for monetary policy, from the third quarter of 2020 to the third quarter of 2022, the majority of analysts anticipate an interbank funding rate below the current level of 4.50%.

July remittances data printed new records for any month of July at USD 3.5 bn, totalling USD 22.8 bn for the first seven months of the year—increases of 7.2% y/y and 10.0% y/y, respectively. Remittances have remained high following their surge at the beginning of the pandemic-induced lockdowns.

Finally, President Andres Manuel Lopez Obrador presented his second government report, which was considered more a political event than an economic one. He mentioned the fight against corruption, the progress of welfare programs, security achievements, and his handling of the economic fallout from the COVID-19 pandemic, arguing that the economy has fared better than some of its peers. In the speech, he emphasized the government’s frugality, noting that luxuries have been eliminated and that resources saved are being dedicated to advancing the well-being of Mexicans. He also forecast that “the worst is over and now we are rebounding. Lost jobs are already recovering, production is slowly returning to normal, and we are already beginning to grow”. He said that fighting corruption and government austerity have together allowed his administration to save close to MXN 560 bn (approx. USD 25.5 bn). Finally, he stated that “We have faced the pandemic and we are going to get out of the economic crisis without taking on additional external debt and without allocating public money to immoral bailouts.”

For the coming weeks we will have domestic private consumption and investment for June, inflation for August, and industrial activity for July. It is worth noting that July and August numbers will tell us whether the economic recession is well estimated up until now, or whether some forecast corrections will be needed.

Peru—The Slow Return to Normal Continues, but with Fiscal Complications

Guillermo Arbe, Head of Economic Research

51.1.211.6052 (Peru)

guillermo.arbe@scotiabank.com.pe

The week produced a host of new information, mixing hope and concern. To begin with, COVID-19 is finally showing signs of losing ground. Both hospitalizations and the total daily death rate in the country are at their lowest levels in over a month. The government extended the State of Emergency for another month, but announced that international air travel, as well as those sectors of the economy still in lockdown, will resume operations in October.

Early information for July GDP is in line with an -8% m/m to -10% m/m contraction, versus the -18% m/m GDP result in June. Data for August is even more auspicious. Only agriculture, fishing, and financial services—as well as supermarket sales and other selective areas of commerce—are surpassing pre-COVID-19 levels so far. However, electricity, cement demand, and mining are close to pre-COVID-19 levels. The main drag is investment, including public sector investment, which declined -20.5% y/y in August.

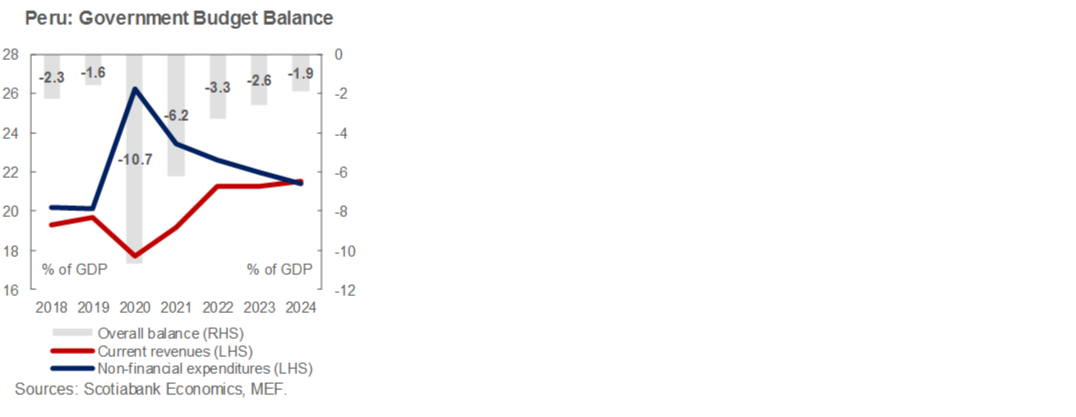

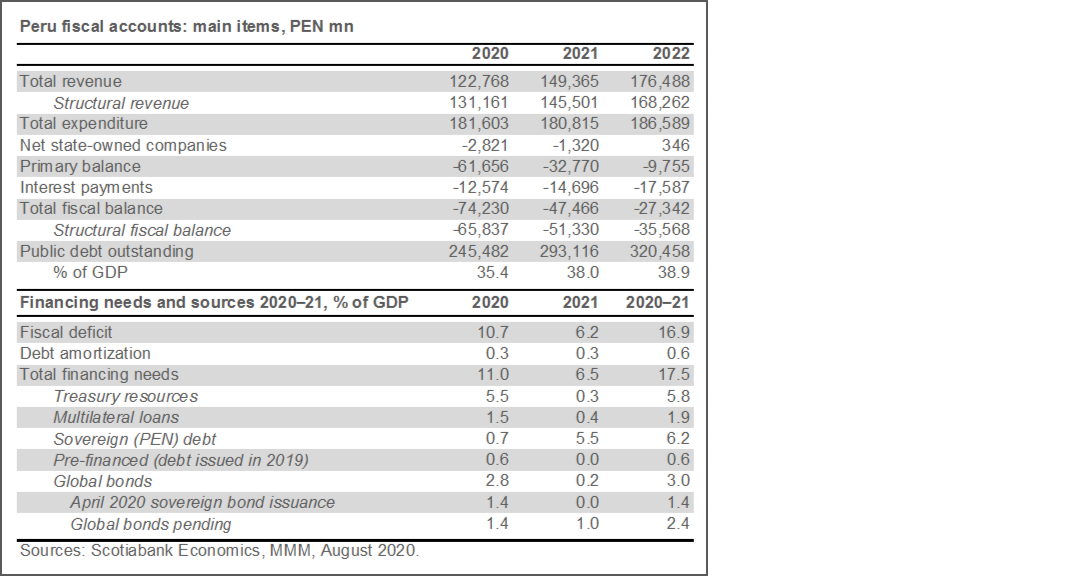

The government updated its fiscal forecasts in its recently released fiscal framework, (Marco Macroeconómico Multianual, MMM). The Ministry of Finance now expects a fiscal deficit of 10.7% of GDP in 2020, and 6.2% in 2021. Thus, a huge fiscal gap will need to be financed over the 2020–21 period. The MMM proposes that part of the financing for the two-year period, equivalent to 5.8% of GDP, is to come from current Treasury resources, mostly reflecting past savings. The government has 14.4% of GDP in total past savings (“financial assets”) of some sort or another, including the Fiscal Stabilization Fund, which currently stands at USD 4.2 bn (2.0% of GDP), down from USD 5.3 bn (2.5% of GDP) at the beginning of the year.

Debt financing needs are high for the 2020–21 period. They include 6.2% of GDP in sovereign (PEN) bonds, 3.0% of global bonds, in addition to 1.9% of GDP in multilateral loans. Of these, the government has already secured USD 3 bn (1.4% of GDP), mainly from the IADB and the World Bank. Given the amount of bonds already issued (USD 3 bn, or 1.4% of GDP of global bonds issued In April), another USD 3 bn, or 1.4% of GDP would still be pending. More significantly, most of 6.2% of GDP in sovereign bonds are still to be issued. These figures should be taken as the current government intention, as much is likely to change over the next 18 months.

The MEF expects public sector debt to rise to 38% of GDP in 2021, and peak at 39.1% of GDP in 2023 before tapering off, as the fiscal deficit slides progressively toward 1.0% by 2026. In our view, the crucial aspect in the trend of public finances will not be government and/or Congressional spending initiatives, but how quickly fiscal revenue recovers. Peru’s credit rating going forward may also hinge most critically on this.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | carlos.munoz@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Forthcoming |

| Subscribe: | pirajaj@colptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

| COSTA RICA | |

| Website: | Click here to be redirected |

| Subscribe: | estudios.economicos@scotiabank.com |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including, Scotiabanc Inc.; Citadel Hill Advisors L.L.C.; The Bank of Nova Scotia Trust Company of New York; Scotiabank Europe plc; Scotiabank (Ireland) Limited; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Scotia Inverlat Casa de Bolsa S.A. de C.V., Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorised by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorised by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V., and Scotia Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.