This is our last Latam Weekly of 2022; the next edition is scheduled to be released on January 13, 2023.

Best wishes for very happy and safe holidays from all of us at Scotiabank Economics!

ECONOMIC OVERVIEW

- Following a busy week on the regional and global stage, with major central banks announcing their latest policy decisions, we head into to the final trading days of the year with little to wake us up from our overfed slumber.

- The social and political situation in Peru remains an important risk that needs to be monitored 24/7.

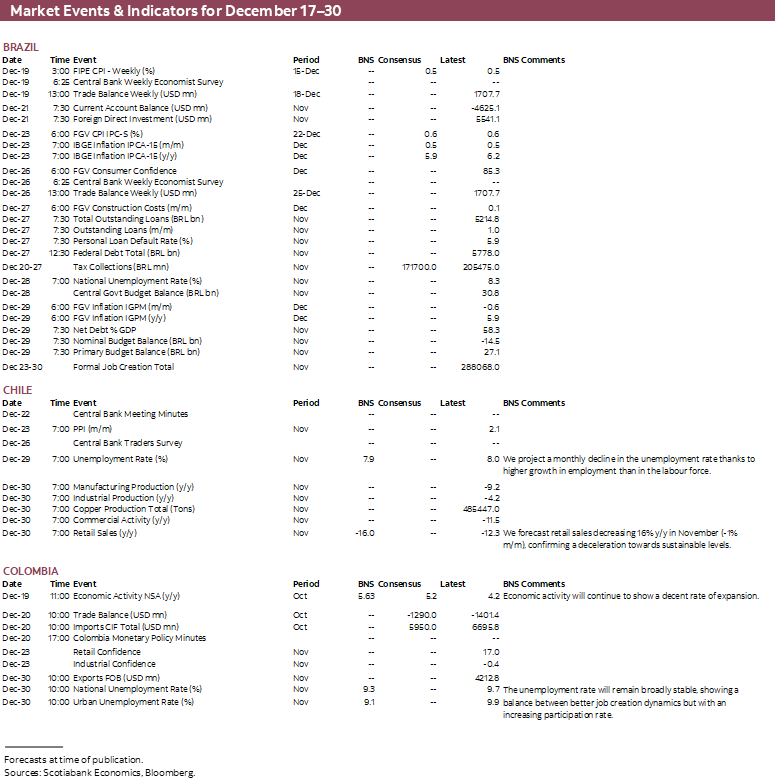

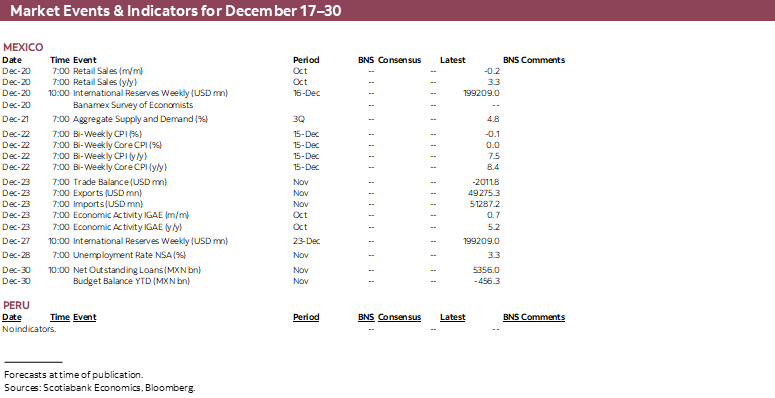

- Inflation data out next week for the first half of December in Brazil and Mexico will provide a first, and important, guide for the full month.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Colombia and Peru.

MARKET EVENTS & INDICATORS

- A comprehensive risk calendar with selected highlights for the period December 17–30 across the Pacific Alliance countries and Brazil.

Economic Overview: Peru Unrest the Highlight Ahead of the Holidays

Juan Manuel Herrera, Senior Economist/Strategist

+44.207.826.5654

Scotiabank GBM

juanmanuel.herrera@scotiabank.com

- Following a busy week on the regional and global stage, with major central banks announcing their latest policy decisions, we head into to the final trading days of the year with little to wake us up from our overfed slumber.

- The social and political situation in Peru remains an important risk that needs to be monitored 24/7.

- Inflation data out next week for the first half of December in Brazil and Mexico will provide a first, and important, guide for the full month.

Following a busy week on the regional and global stage, with major central banks announcing their latest policy decisions, we head into to the final trading days of the year with little to wake us up from our overfed slumber.

This may only be true from an on-calendar perspective, however, as the social and political situation in Peru remains an important risk that needs to be monitored 24/7. Announcements, decisions, and incidents that disturb economic activity could occur at any moment.

Those involved in local markets will hope for clarity on an early-election date and/or diminishing social unrest. Holiday celebrations may bring a temporary period of relative quiet and hopefully a reset of emotions in government and among protesters. On the other hand, the detainment of former Pres Castillo and decisions related to his imprisonment over the next few days could inflame unrest.

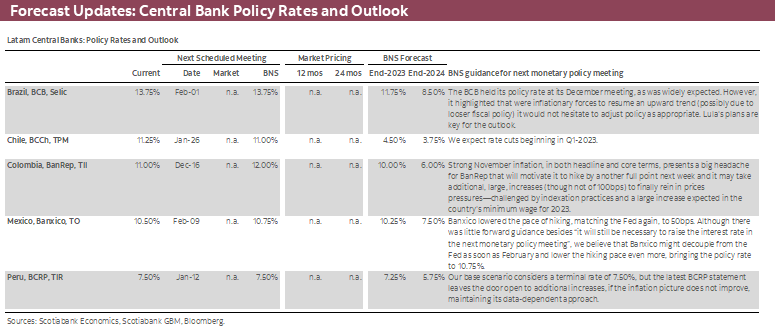

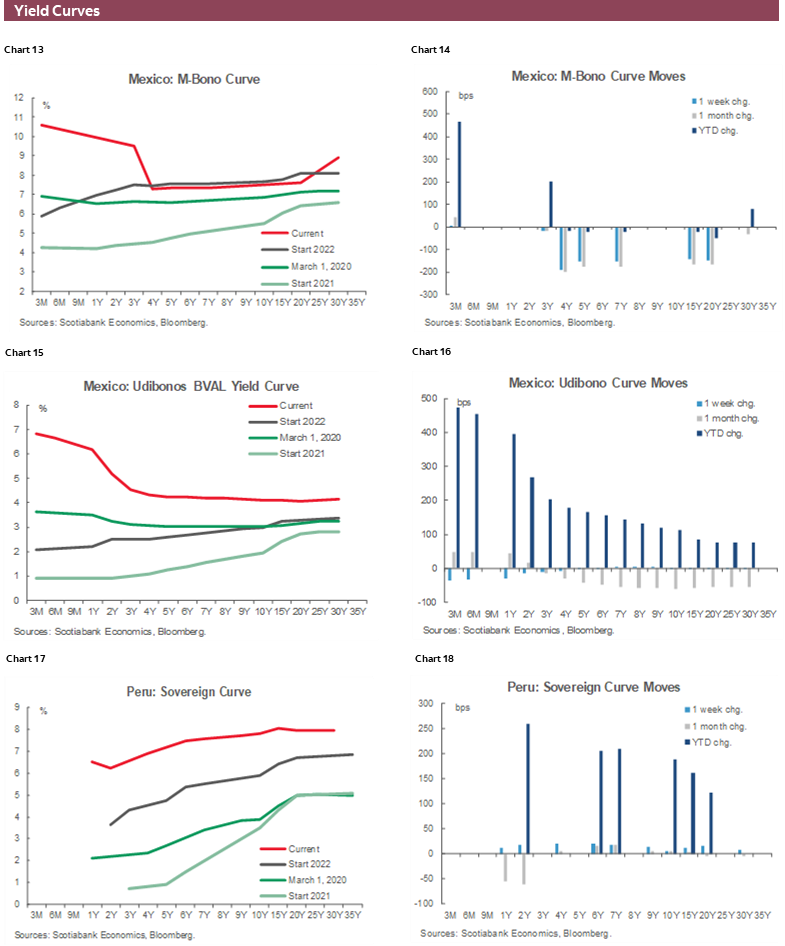

Inflation data out next week for the first half of December in Brazil and Mexico will provide a first, and important, guide for the full month. Banxico’s decision on December 15 suggested the bank could even decouple from the Fed at its February decision. A soft inflation reading would increase speculation that this will be the case, although markets may be in for a surprise if price gyrations around Mexico’s Black Friday sales equivalent (Buen Fin) triggers a sharp jump in core prices that keeps inflation upside risks alive.

In the case of Brazil, economists are seeing another deceleration in prices growth that should provide the BCB with some relief in contrast to its concerns about the incoming government’s fiscal plans.

On that note, Lula’s transition bill and its spending-cap exclusion plan are reportedly facing fierce opposition in the Lower House and it now looks likely to be watered down further from his team’s original asks. The opposition is seeking a BRL80bn cap increase and only for one year compared to the Senate-approved BRL145bn social aid bump for two years. Lawmakers will vote on the bill on December 20 a day after the Supreme Court passes judgment on whether it’s unconstitutional that lawmakers can have hand on the country’s budget.

Economic activity and international trade figures for Colombia and Mexico are also worth a watch. Mexico also publishes retail sales data.

PACIFIC ALLIANCE COUNTRY UPDATES

Colombia—Key Points for Year-End

Sergio Olarte, Head Economist, Colombia

+57.1.745.6300 Ext. 9166 (Colombia)

sergio.olarte@scotiabankcolpatria.com

María Mejía, Economist

+57.1.745.6300 (Colombia)

maria1.mejia@scotiabankcolpatria.com

Jackeline Piraján, Senior Economist

+57.1.745.6300 Ext. 9400 (Colombia)

jackeline.pirajan@scotiabankcolpatria.com

Despite recent leading indicators showing that economic activity is on a decelerating path, private consumption is still significantly above the long-run trend, while headline inflation has not peaked yet. Additionally, the weaker COP continues to pressure inflation expectations for next year and recent external balance data showed a still too-wide current account deficit that needs portfolio investment to help finance it. Therefore, we do not see much flexibility for BanRep in the short run. Furthermore, we anticipate a 100bps hike at the December monetary policy meeting and a final 50bps hike in January to 12.50%.

The next question is how long BanRep will need to keep the policy rate at 12.50%. We think that until core inflation shows a clear path of deceleration, it is not possible to start the gradual easing cycle. Our calculations are such that only after July inflation data, BanRep will be less concerned about inflation and start to gradual policy rate cuts to end 2023 at 10%.

After the central bank’s decision today, the main focus for the rest of the year will be on macroeconomic indicators. The economic activity indicator ISE is expected to show a moderate deceleration, showing muted industrial and retail activity but a still-strong performance in services-related sectors.

Labor unions and business associations reached an agreement on a 16% minimum wage increase for 2023. Our current inflation forecast had assumed ~14% increase. That said, the final decision will not significantly change our projection. We still see the peak of inflation in December 2022, which will be confirmed in February when we will have January prices data at hand showing the first moderation in 21 months. The min wage agreement is positive news since the increase didn’t significantly deviate from the traditional rule (inflation + productivity), but also was well below the labor unions’ proposal of 20%.

Colombia’s Min Fin is expected to release the Financing Plan before the end of the year (we do not have a specific date yet). From this publication, it is important to understand not only how consistent the macroeconomic scenario is, but also the information regarding issuance, the domestic/foreign debt split, plans for social and green bonds, and plans for the COLTES ETF, among other issues that the new administration has not yet addressed.

Peru—A Slowing Economy, Resistant Inflation, and a State of Emergency: Not the Best Ending for 2022

Guillermo Arbe, Head Economist, Peru

+51.1.211.6052 (Peru)

guillermo.arbe@scotiabank.com.pe

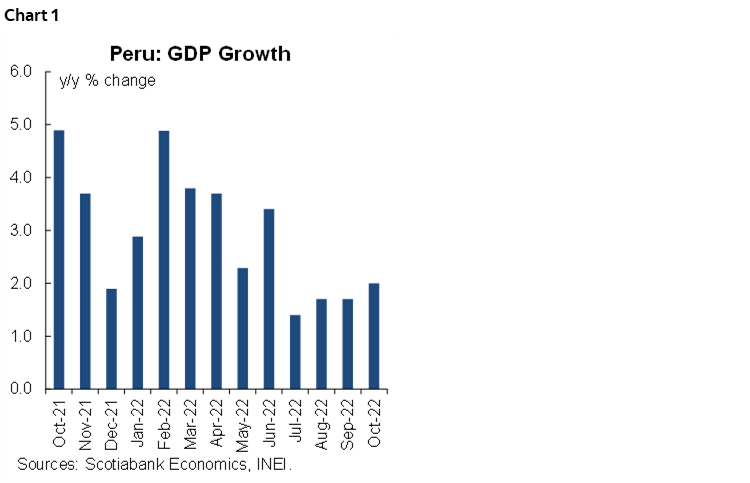

Peru’s GDP grew 2.0% y/y in October (chart 1). The data is in line with our forecast of 2.8% growth for full-year 2022. In fact, 12-month GDP growth (November 2021 to October 2022) is currently at 2.8%. However, given the level of political turbulence in December, October’s GDP has lost significance as an indicator of future growth.

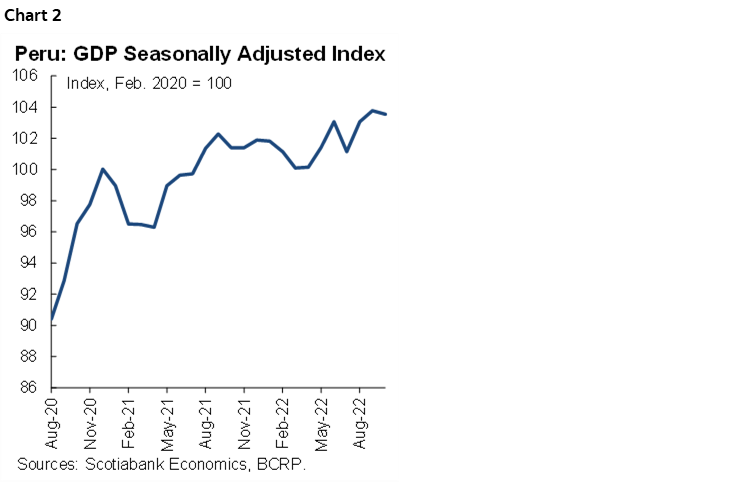

There are a couple of things to note concerning October’s GDP. The first is that m/m growth was negative (chart 2). Perhaps the most worrisome aspect was that manufacturing (non-primary processing) fell in both y/y and m/m terms (table 1). The one positive is that metals mining was up 3.5%, suggesting that production from the Quellaveco copper operation was beginning to have an impact.

Although November GDP growth is likely to be more or less in line with October, December GDP should be materially impacted by the ongoing political and social turbulence. Since December 7, former President Castillo tried and failed to close Congress and was impeached and detaind, sparking a wave of violence that was followed by a declaration of a State of Emergency on December 14. In addition, Congress began debating early elections, which could conceivably take place late in 2023. We expect political turbulence to negatively impact mining, agriculture, commerce, tourism, and, no doubt, public investment. Note that December is a key month in which public investment is normally at its highest, and Christmas sales and travel stimulate sales overall, thus contributing significantly to demand growth. Since developments are still ongoing, it is hard to gauge the level of impact, but it is fair to say that our full-year 2.8% forecast has downside risk.

We expect the interruption in transportation/distribution that occurred in December to have an impact on inflation as well. While the impact is likely to be temporary, it comes at a terrible moment, just when there were incipient hopes that the BCRP would pause in its policy of increasing the reference rate. We had been expecting inflation to decline from 8.4% yearly in November to 8.1% yearly in December. Our hopes for a reduction in inflation haven’t been quite dashed yet. Key price indicators to mid-December point to 8.2%-8.3%, but the month is not over, and the full effects of the disturbances may not have fully sunk in yet. This scenario puts our scenario of a BCRP pause in its reference rate policy in January at risk.

Throughout all of this, the PEN has been notoriously stable, and financial assets have moved more or less in line with the region. At least so far. This is a testament, most likely, to two things: confidence in the BCRP, and continuity in economic policy over the past years, if not decades, despite extreme political events. Meanwhile, several political decisions need to be taken, most importantly whether and when early elections will be held.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Click here to be redirected |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.