ECONOMIC OVERVIEW

- Developments in Israel have prompted sharp moves in markets in recent days, and may remain the main driver of global price action over the weekend and through next week. The US data calendar is relatively light, so UK and Canadian CPI prints are the G-10 highlights and Chinese Q3 GDP figures will likely be an important influence on the global risk mood.

- In Latam, Peru, Colombia, and Brazil publish economic activity data for August, with none of these countries expected to show a remarkable economic performance for the month—in the case of Peru, another year-on-year contraction is also possible.

- In today’s report, our economics teams in the Pacific Alliance preview Peru’s upcoming GDP print and discuss their early tracking of October CPI, detail the next few steps of Chile’s constitutional process and the INE’s upcoming changes to the CPI basket, analyse Banxico’s September meeting minutes and the influence of procyclical stimulus on their hawkish stance, and break down the drivers of the performance of Colombian government debt in the year to-date.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Chile, Colombia, Mexico and Peru.

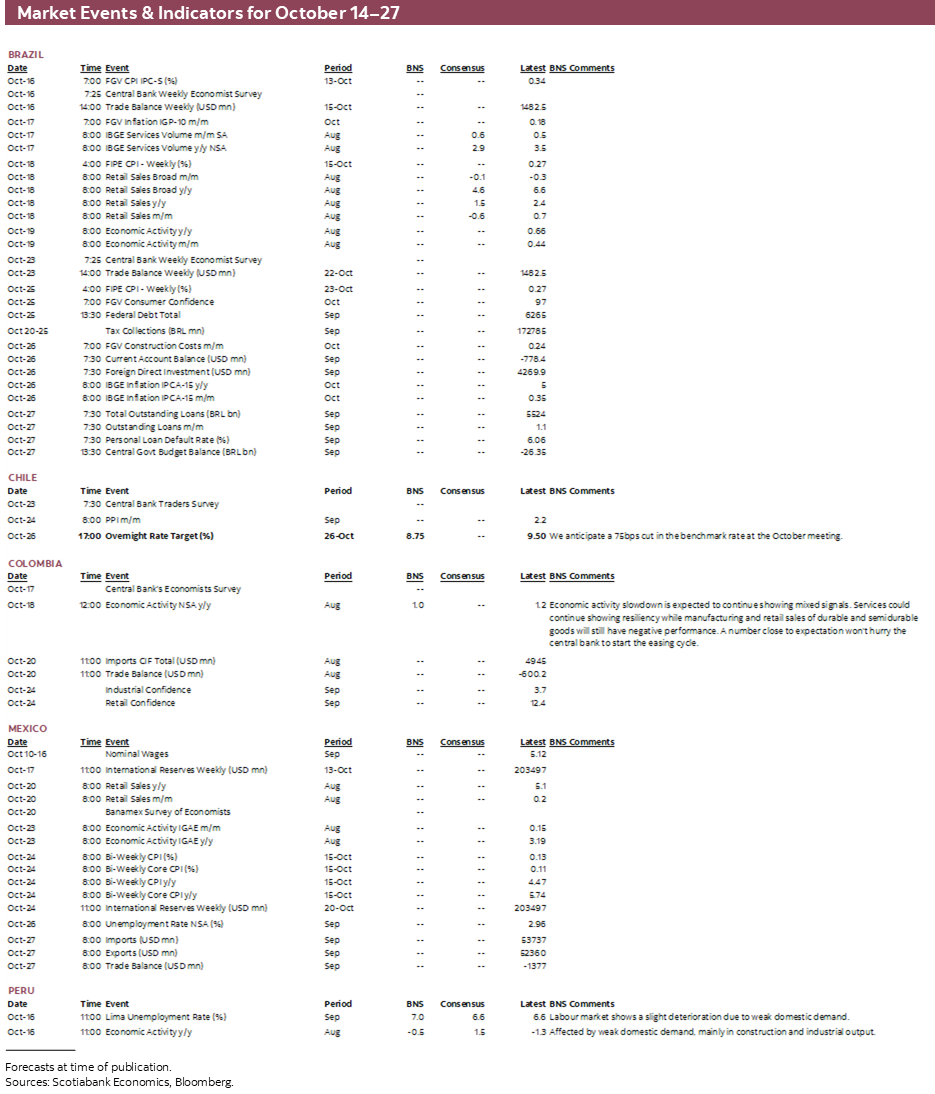

MARKET EVENTS & INDICATORS

- A comprehensive risk calendar with selected highlights for the period October 14–27 across the Pacific Alliance countries and Brazil.

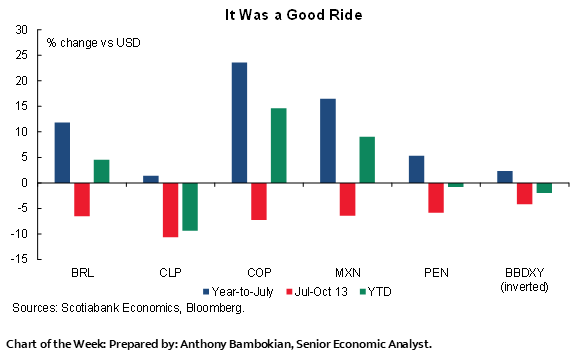

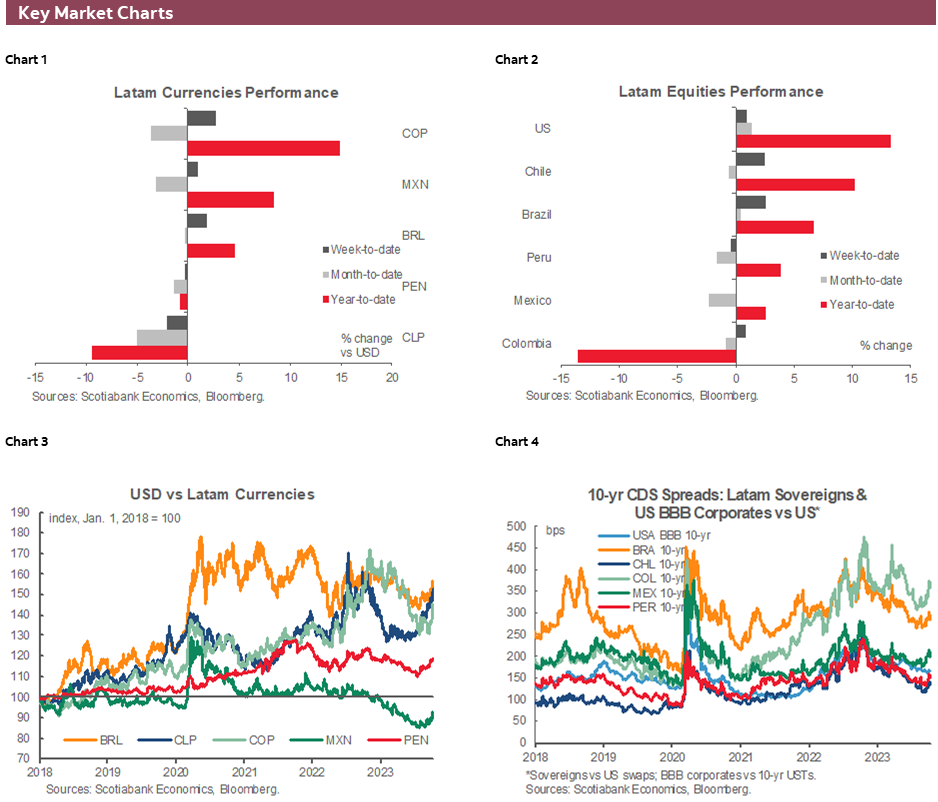

Chart of the Week

ECONOMIC OVERVIEW: PERU, COLOMBIA, AND BRAZIL ECON ACTIVITY ON TAP

Juan Manuel Herrera, Senior Economist/Strategist

Scotiabank GBM

+44.207.826.5654

juanmanuel.herrera@scotiabank.com

- Developments in Israel have prompted sharp moves in markets in recent days, and may remain the main driver of global price action over the weekend and through next week. The US data calendar is relatively light, so UK and Canadian CPI prints are the G-10 highlights and Chinese Q3 GDP figures will likely be an important influence on the global risk mood.

- In Latam, Peru, Colombia, and Brazil publish economic activity data for August, with none of these countries expected to show a remarkable economic performance for the month—in the case of Peru, another year-on-year contraction is also possible.

- In today’s report, our economics teams in the Pacific Alliance preview Peru’s upcoming GDP print and discuss their early tracking of October CPI, detail the next few steps of Chile’s constitutional process and the INE’s upcoming changes to the CPI basket, analyse Banxico’s September meeting minutes and the influence of procyclical stimulus on their hawkish stance, and break down the drivers of the performance of Colombian government debt in the year to-date.

An eventful and volatile week in markets is coming to an end with traders remaining on edge due to the conflict in Israel and the aftermath of stronger-than-expected US CPI data (core services, especially). Markets may break for the weekend, but developments in the Middle East between now and Monday could prompt sharp moves when trading resumes next week. On the ex-Latam data and events front, the US calendar is relatively quiet outside of retail sales figures but other key G-10, Canada and the UK, have key releases that will shape expectations ahead of their respective central bank decisions. Chinese Q3 GDP data are also in focus.

Peru’s monthly GDP and unemployment data out on Sunday are the Latam standout as far as implications for monetary policy go, playing an important role ahead of the BCRP’s November 9th rate decision. The other piece of the puzzle, October inflation data, comes out in early-November.

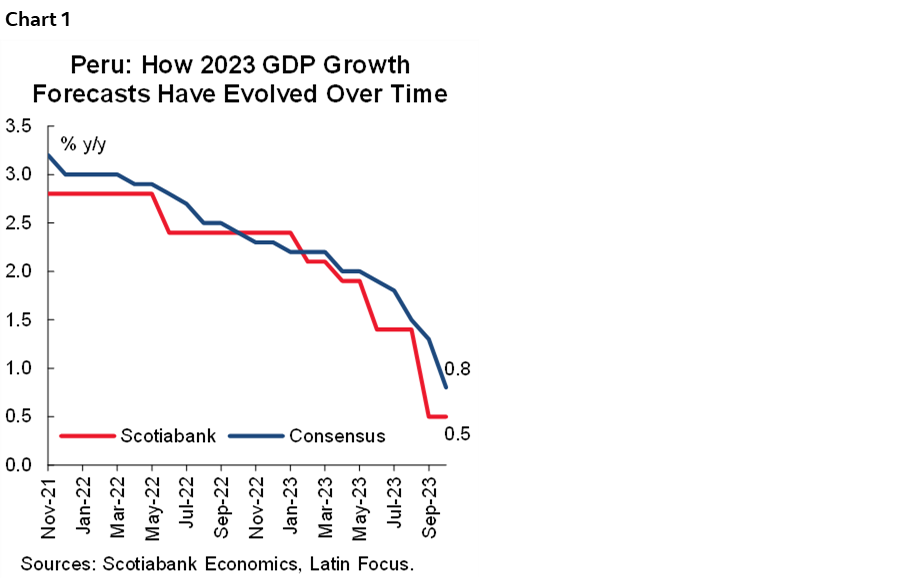

In August, the Peruvian economy likely posted no growth or contracted again according to our economists in Lima who preview the data in today’s report and also discuss their early tracking of October inflation. With the exception of marginal year-on-year gains in GDP in each of March and April (0.3% and 0.4%, respectively), Peru’s economy will have contracted in six out of eight months this year with the 0.5% y/y decline that we have penciled in for next week’s print.

Economic activity growth in Colombia should hold to a relatively soft pace in August data out mid-week. Our team projects that July’s expansion of 1.2% y/y was followed by an even weaker 1% increase; note that this forecast does not incorporate retail sales and industrial/manufacturing production figures out today (Friday).

On Tuesday, BanRep releases the results to its latest survey of economists which we’ll monitor for the split between economists expecting rate cuts to start in October versus those expecting a December start (like us). Trade balance and imports data for August close out the week. We’ll also keep an eye on voting intention polls in Colombia ahead of regional elections on the 29th, which will likely show widespread defeats for Petro’s allies. In today’s weekly, the team analyses the performance and drivers of Colombian government debt through 2023.

Mexico’s schedule has only retail sales data and the bi-weekly Citibanamex survey of economists on tap next week. It’s a bit of a quiet period ahead of the following week’s releases of H1-Oct CPI, and August economic activity, international trade, and unemployment rate figures. Off-calendar developments may be the main influence on local markets that have been sensitive to recent news on surprise changes to airport operators fees schedules and investigations of market power abuse into a major retailer. Banxico’s September meeting minutes released on the 12th of October had an unmistakably hawkish tone that we believe was warranted, as covered by the Mexico economics team in today’s report.

Brazil joins Peru and Colombia in publishing economic activity data (IBC) next week. Thursday’s August figures are expected to show a slight acceleration in output growth, following a soft 0.7% print the previous month. After a strong first half of 2023 supported by the agricultural sector, the underlying weakening trend in Brazil’s economy has become clearer in recent months, which should be reflected in services volume and retail sales readings for August scheduled for release ahead of IBC on Tuesday and Wednesday, respectively.

There’s nothing major to look forward to next week in Chile as far as data is concerned, but the constitutional process is continuing with a vote scheduled in the next few days on the latest observations provided by the Expert Commission. The Santiago team outlines the next few steps in today’s weekly and also breaks down the changes that the INE has announced to the CPI basket beginning with January 2024 data.

Elsewhere around the globe, the UK and Canadian calendars present key releases to gauge whether the BoE or BoC may hike again. Both release CPI and retail sales data, accompanied by the BoC’s consumer and business surveys and UK jobs and wages. US retail sales and industrial production could be market movers in a week that has little else of note out of the country, but comments by Fed officials will be closely watched ahead of the pre-decision (November 1st) communications blackout that begins next Saturday. Japanese CPI and Australian employment are also on tap, and we’ll open on Monday to the results of Poland’s general election over the weekend.

Perhaps more relevant for Latam markets and the broad global mood—and aside from developments in Israel—will be a collection of Chinese data on Wednesday that includes Q3 GDP which, somewhat counterintuitively, would support risk sentiment if it comes in weaker than expected (prompting greater stimulus speculation) or stronger than expected (the Chinese economy is actually doing pretty well). An as-expected expansion of 4.5% y/y may be the least encouraging result for markets. China’s PBoC also sets its medium-term lending facility rate on Monday but the vast majority of economists expect no change.

PACIFIC ALLIANCE COUNTRY UPDATES

Chile—Key Events in Coming Weeks

Anibal Alarcón, Senior Economist

+56.2.2619.5465 (Chile)

anibal.alarcon@scotiabank.cl

Constitutional process in final stages: experts submitted observations prior to delivery of final text.

On Thursday, October 12th, the Expert Commission submitted its observations on the text prepared by the Constitutional Council, which must be voted on by the latter during the week beginning Monday, October 16th. Each observation must be approved (three-fifths, 30 members) or rejected (two-thirds, 32 members). A mixed commission, composed of six experts and six counselors, will analyze observations that are neither approved nor rejected. Once this process is completed, the Constitutional Council must approve the entire text with three-fifths (30) of the members in office (50), with a deadline of November 7th. With this approval, the Constitutional Council will deliver the text to President Boric, who will call for a plebiscite on December 17th.

In our view, the Republican Party (extreme right) will be forced to make its ideas more flexible vis-à-vis the center-right, since it will need their votes to give final approval to the text. This is because the Republican Party has 22 members, which although they have the power of veto (more than two-fifths) do not reach the three-fifths majority necessary to approve. In this line, some of the norms supported by the center-right parties but which did not reach approval in the Constitutional Council were resubmitted by the experts and will probably be part of the negotiation between the extreme and center-right.

New 2023 CPI basket base: higher food weights and updated basket without volatiles.

In February 2024, the statistical agency (INE) will publish January CPI data using the new price basket with base 2023=100, which is updated every five years in line with international recommendations, although less frequently than in OECD countries (between one and two years). Based on information from INE, the new basket will contain 13 divisions, one additional division compared to the current price basket. This will be achieved by separating the current “miscellaneous goods and services” division into two: “personal care, miscellaneous goods and services” and “insurance and financial services”. Regarding the weights, the INE anticipated that education will lose relative importance (today with a 6.6% participation) due to the educational reform that led to a reduction in education spending. On the contrary, the “food and non-alcoholic beverages” division will have an increase in participation (today at 19.3%), also incorporating some services that today are in the “restaurants and hotels” division. As is the trend, the number of products within the basket will be reduced from 303 to approximately 286.

Another relevant change will be the update of the basket of CPI “without volatiles”, a statistical construction made by the central bank in collaboration with INE and which has been used as the main core measure by the central bank board. This “without volatiles” basket corresponds to a fixed basket of 204 products and comes from the analysis of volatility (among other criteria) with information from 2002 to October 2019, so a review and a criterion that allows establishing a frequency for updating this basket is urgently needed.

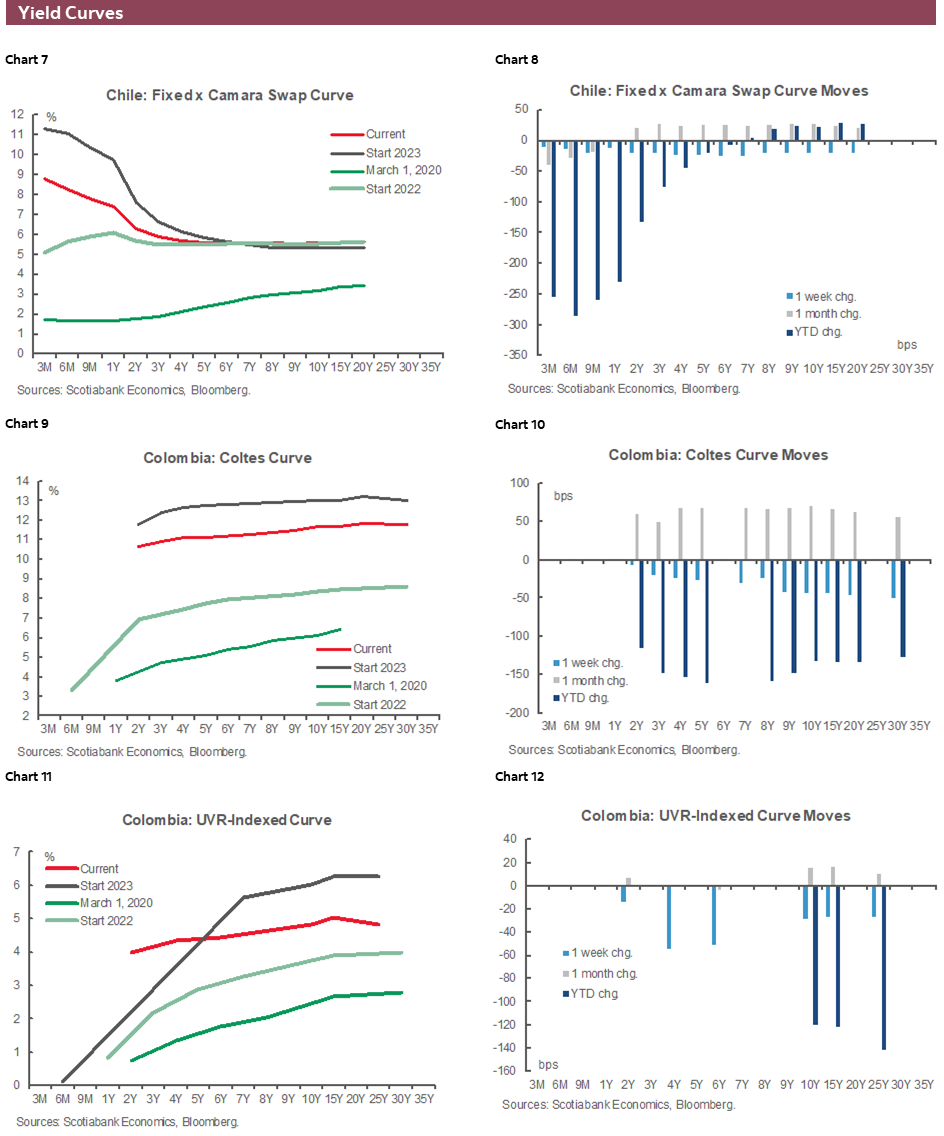

Colombia—What Has Driven Colombian Fixed Income Moves in 2023?

Sergio Olarte, Head Economist, Colombia

+57.601.745.6300 Ext. 9166 (Colombia)

sergio.olarte@scotiabankcolpatria.com

Jackeline Piraján, Senior Economist

+57.601.745.6300 Ext. 9400 (Colombia)

jackeline.pirajan@scotiabankcolpatria.com

Santiago Moreno, Economist

+57.601.745.6300 Ext. 1875 (Colombia)

santiago1.moreno@scotiabankcolpatria.com

The current year remains a challenging one during which many central banks worldwide have struggled to find the end of their hiking cycles in the context of still-high inflation and resilient economy. Uncertainty remains elevated, bringing substantial volatility to financial markets. In Colombia, the COLTES market has been influenced by several shocks; not only does the international scenario matter, but rates also reflect domestic events that must be dissected. That said, it is also relevant to analyze if those shocks are temporary or structural, which could help us assess if current policy rate levels are compatible with macro fundamentals.

1) Macro fundamentals

At the start of 2023, the market consensus saw inflation peaking early in the year, which was compatible with rate stability from BanRep in Q1-2023 and a potential rate cut arriving in H2-2023. However, inflation peaked later than expected in Colombia and, in turn, BanRep’s rate reached a higher-than-expected level. During this back and forth in expectations, markets, especially the yield curve, began to reflect in prices the possibility of an early start to the easing cycle which we believe is what triggered the COLTES nominals curve to trade below the repo rate since early-2023. However, as expectations for a rate cut have been delayed, the COLTES curve lost momentum, and even some of those gains were partially reversed in recent volatility episodes.

2) Flows

As the international context remains challenging due the Fed’s “higher rates for longer” view, investment inflows from offshore investors are no longer a tailwind in Colombia. In 2022, offshore inflows totaled more than COP19tn, even becoming the main COLTES holder with 26.2% of the outstanding total. In contrast, during 2023, offshore agents have sold up to September 2023 COP10.9tn, diminishing their ownership share to 21.8%. One hypothesis about this reduced appetite for local debt could be partly due to a strategy of reducing exposure to Latam, but also trying to balance exposure across countries due to differences in the monetary policy cycle timings across the region.

Local liquidity helped offset reduced offshore participation. We found two events that helped COLTES to more than offset the 2023 offshore mood: one related to domestic investors and the second with economic authorities.

- In the last quarter of 2022, pension funds (AFP) sold COP4tn of COLTES due to the uncertainty around pension reform and sharp COP depreciation that made them reshape the portfolio towards foreign investments, which in the volatile international context produced also demands liquidity to comply with margin calls due to hedge operations in part of the international positioning. In 2023, after a strong COP appreciation in January and easing pressures from previous margin calls, AFPs decided to return to the TES market and began buying significantly. In fact, in the year to September, AFPs have bought COP27.4tn in COLTES that not only helped to counteract offshore selling but also saw them bid on additional issuance by Colombia’s Treasury.

- In 2023, Government budget execution has undershot plans, resulting in the Treasury increasing deposits in their BanRep account by more than COP20tn (above the historical mean) and created a liquidity shortage. This meant BanRep had to buy COP8tn in TES this year to partially resolve liquidity issues in the market, helping COLTES to rally due to the unconventional bid on screens.

Seemingly, these two shocks vanished recently as the Government is speeding up budget execution. At the same time, AFPs already finished their portfolio adjustment. Therefore, we think the recent COLTES sell-off was more on the back of liquidity normalization and a reversal of stretched positioning that had anticipated rate cuts too soon. COLTES spreads vs international references haven’t widened significantly, which suggests that Colombia’s risk perception hasn’t changed substantially.

That said, from the macroeconomic perspective, despite the recent negative episode in rates, the COLTES curve could reflect some positive fundamental value in the future if inflation falls further enough, motivating BanRep to start a decisive easing cycle, which could trigger a better appetite in offshore investors.

In the meantime, volatility episodes may occur more frequently. In fact, in the year-to-July, the whole yield curve had shifted lower by over 170bps on average, while in September it shifter higher by 100 bps, reflecting elevated uncertainty, especially in international markets. However, in the medium-term, inflation and domestic monetary policy fundamentals matter more for the overall trend, namely for the short-end and belly, pointing to a bull steepening of the curve.

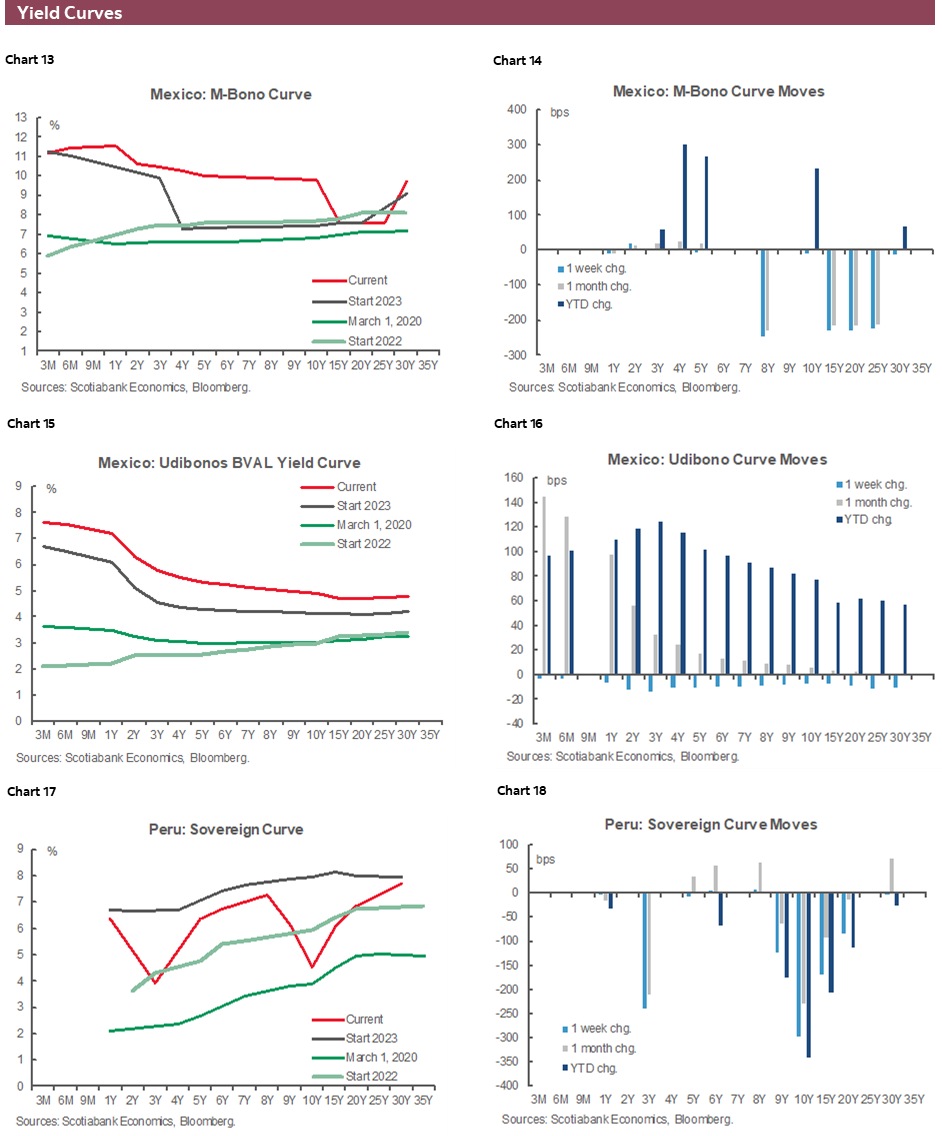

Mexico—Banxico Reinforced Message of Rates Staying Put For Longer

Eduardo Suárez, VP, Latin America Economics

+52.55.9179.5174 (Mexico)

esuarezm@scotiabank.com.mx

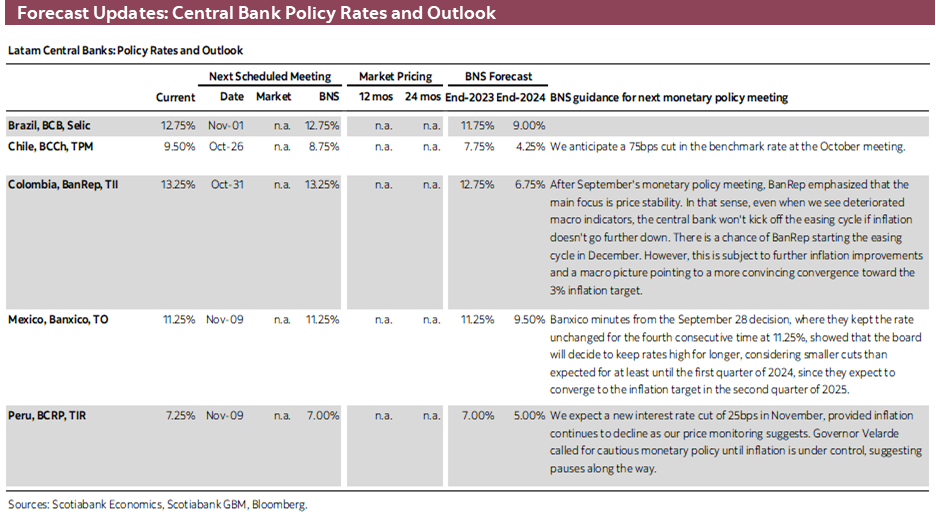

On October 12th, Banxico published the minutes from its September 28th meeting, where we believe the most relevant portions of the statement are: a) the message that the board now expects inflation to get back to target in 2025 Q2, b) the board’s view that risks to inflation remain skewed to the upside, c) and that the board members expect rates to remain on hold for longer than previously expected. The economy will likely remain red hot in 2024, particularly on the consumption front:

- The government’s budget for 2024 is projecting a widening of the fiscal deficit (the PSBR definition) from 3.9% of GDP to 5.4%.

- The bulk of the wider deficit is likely to fall on social spending (the budget has physical investment falling from 2.8% of GDP to 2.6%).

- This fiscal stimulus adds to already strong tailwinds from the roughly 1 percentage point of GDP in consumption boost that the remittance boost is providing. The historic trend in remittances would suggest levels just under US$50bn, yet they are likely to print close to US$65bn. This strength in remittances is in a large part due to the strength of the low income services sector of the US, where most Mexicans work according to the New American Economy studies.

Consumption in Mexico is likely to have very strong tailwinds coming from both continued remittance flows and social transfers from the government, on top of a strong labour market. An economy with a tight labour market and very strong demand will likely keep inflationary pressures in place, which Banxico’s board correctly signaled in their statement that the balance of inflation risks remain stilted to the upside. The latest survey of economists published by Banamex, shows consensus looks for 4.7% inflation in 2023, and 4.0% for 2024. However, there is a moderate upward trend in expectations for 2024, which could be aggravated following the surprise widening of the planned budget deficit that was made public on September 8th.

The concluding statement of the IMF’s 2023 Article IV consultation (published October 3rd), flagged some of the fiscal risks, as well as the implications for interest rates and inflation, with the statement flagging the following: “The planned fiscal path for 2024 is unduly procyclical. Budgetary pressures from lower revenues are compounded by a targeted increase in current spending (i.e., wages, pensions, and social spending) and higher front-loaded spending to complete flagship investment projects. The expected increase in the deficit to 5.4 percent of GDP—a fiscal impulse of 2.4 percent of potential GDP—will boost demand at a time when the economy is operating above potential and inflation is not yet back to the central bank’s target. This is likely to lead to a higher path for interest rates, a stronger currency, higher debt-to-GDP ratio, and a slower decline in inflation than would otherwise be the case. As such, a tighter fiscal stance would be more consistent with Banxico’s efforts to bring inflation back to target.”

“The next administration will face stark choices to adhere to the targeted medium-term fiscal path. A large fiscal consolidation is forecast for 2025 which will exert a significant drag on growth, reversing the expected 2024 boost. Meeting these targets would require substantive fiscal measures of around 2½ percent of GDP, mostly incident on boosting non-oil revenue (which is significantly below Latin American and OECD peers). These could include (i) eliminating the zero-rating for VAT and rationalizing exemptions; (ii) broadening the personal income tax; and (iii) increasing property taxes.” We tend to agree with the IMF’s assessment and believe the procyclical stimulus is likely to keep pressure on Banxico to keep monetary conditions tight.

Peru is in Need of Fiscal Stimulus

Guillermo Arbe, Head Economist, Peru

+51.1.211.6052 (Peru)

guillermo.arbe@scotiabank.com.pe

We’re all bracing ourselves for August GDP data that is to be released by Monday, October 16th. Yet another negative GDP growth number would be disheartening, and yet it is within the realm of possibility. Growth has been nefarious (to put it mildly) throughout 2023, and the Minister of Finance, Contreras, appears quite anxious to see the economy improve before the second El Niño severe climate wave hits in December–April. Of course the government could, and should, do more to stimulate the economy, but the Ministry of Finance appears to fear that providing more stimulus risks not complying with the fiscal rule of a GDP deficit of no more than 2.4% of GDP this year. That is likely to be the case, but, at the same time, this might be a moment when it may make sense to be more Keynesian than that.

We expect August GDP growth to be very low, if not negative. The positive indicators (49% y/y fishing GDP growth albeit with low weight in GDP, 3.7% electricity growth, 2.2% growth in formal jobs) do not seem to compensate the negative (17% decline in sales tax revenue suggest much subdued consumption, as does a 9.4% decline in cement sales, not to mention the impact of El Niño on agriculture). The balance will be determined by industrial manufacturing (officially termed “manufactura no primaria”), which has been performing extremely poorly, and by services, which has been showing mild but stable growth (chart 1).

The paucity of economic growth that we expect to be reiterated in August data should heighten the BCRP’s resolve to lower interest rates. Well, if only there were no El Niño on the horizon.

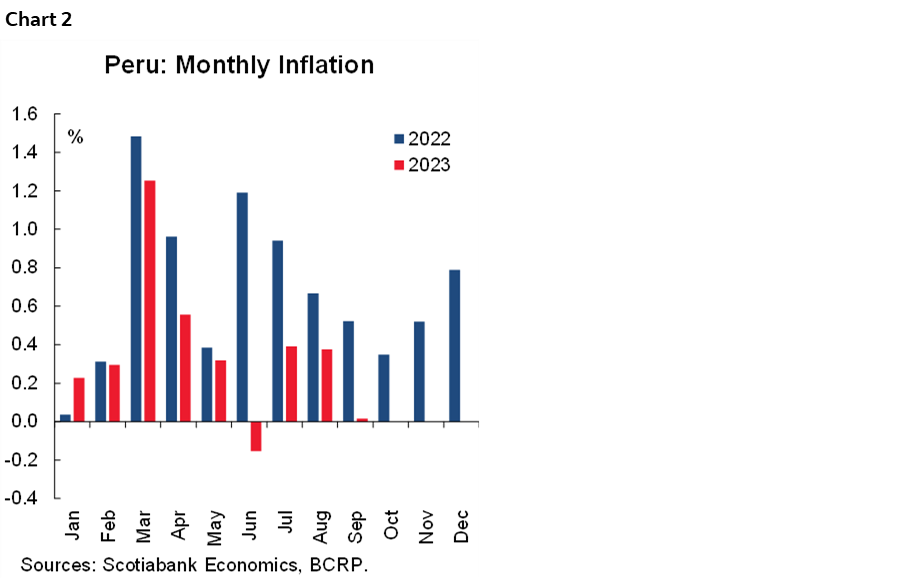

According to the key prices that we follow, inflation for the month of October is tracking at 0.11%. This is, however, before the still moderate increase in global oil prices following the events in the Middle East. If the current trend continues, this month’s inflation would be below 0.3% in October 2022 (see chart 2) and, so, 12-month inflation would continue declining, mildly, from 5.0% to 4.8%. This is our base case scenario for October, albeit now with upside risk. If inflation falls below 5%, even if barely, it would have a psychological impact. As the graph also shows, inflation was quite high in November–December 2022, so there is a good chance that headline inflation will continue declining in the rest of 2023.

The combination of falling inflation and low GDP growth gives the BCRP room and motivation to continue lowering the reference rate in November, to 7.0%, which is what we expect. At the same time, however, the BCRP has an eye on El Niño. Precedents dictate some magnitude of impact on inflation, albeit only a mild one. Still, a blip in inflation once the rains begin gives the BCRP pause in its policy to lower rates, if not in December, then more certainly in Q1 2024.

Finally, things are moving again regarding the pension fund system. The Executive has submitted to congress an initiative that introduces changes in the pension fund system. These include: a minimum pension fund (proposed at PEN600); universal coverage through the inclusion of all citizens in the pension fund system as soon as they reach 18 years old; and opening up the private system to other competitors, including mutual funds, investment funds, and financial institutions in general. This is an initiative that does not put personal funds under management at risk, but will, affect the market that the current AFPs move in. Equally importantly, the Executive apparently hopes that including a minimum pension fund to be financed by fiscal resources, will satisfy congress enough to stem more aggressive initiatives from emerging there. The risk is that the opposite might occur, and that the debate over the government initiative may tempt congress to introduce more aggressive measures. What does seem more probable is that congress will approve a new pension fund withdrawal scheme, likely to take place over the next six months.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Click here to be redirected |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.