ECONOMIC OVERVIEW

- Only Banxico is expected to deliver a rate cut next week among central banks announcing decisions next week, as the BCB, BoE, and RBA all stay put. Fed expectations may be shaped by another round of key private sector data making up for the lack of official figures due to the U.S. government shutdown that, next Wednesday, would be its longest ever.

- Weekend CPI data out of Peru will be nothing to be scared about, as previewed by our local team in today’s Weekly, who also discuss early data teeing up another strong month for growth in November. Our economists in Chile also preview September CPI and August economic activity data that may shape uncertain BCCh expectations in markets.

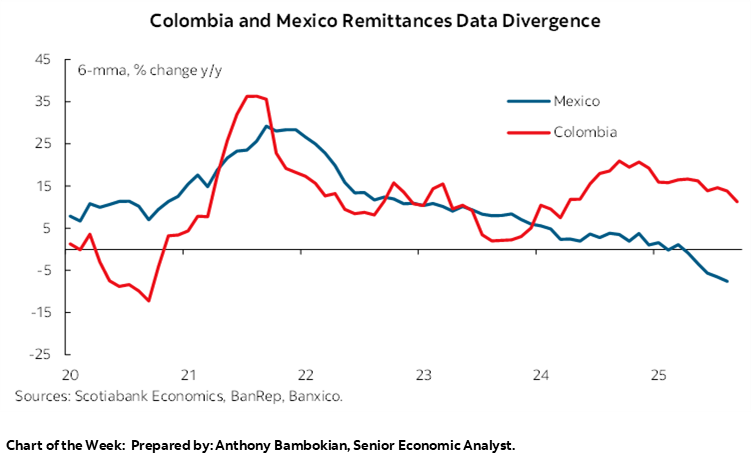

- Mexican investment and remittances data should remain weak, in line with recent GDP data that suggest the country’s economy is broadly stagnating according to our colleagues in Mexico. In Colombia, the team talks about the recent selection of Cepeda to represent the ruling party in next year’s votes, as the local electoral season begins to heat up.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Chile, Colombia, Mexico and Peru.

MARKET EVENTS & INDICATORS

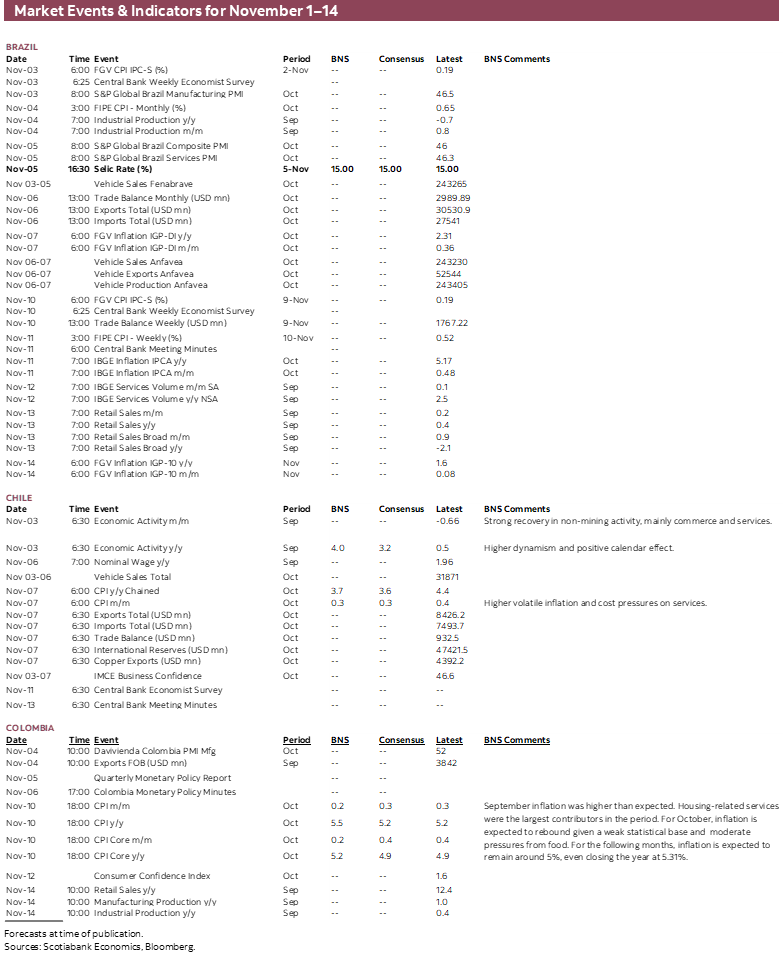

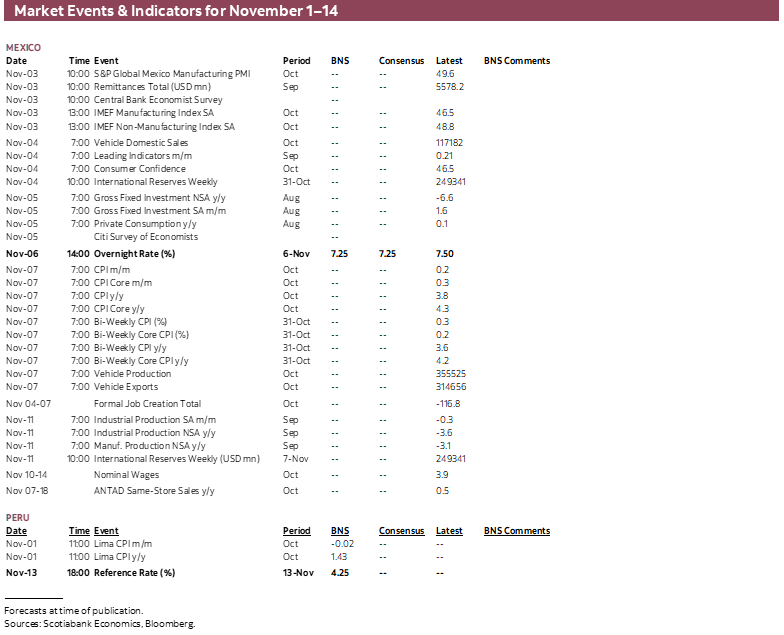

- A comprehensive risk calendar with selected highlights for the period November 1–14 across the Pacific Alliance countries and Brazil.

Chart of the Week

ECONOMIC OVERVIEW: REGIONAL CPIs, ANOTHER BANXICO CUT

Juan Manuel Herrera, Senior Economist

+52.55.2299.6675

juanmanuel.herrera@scotiabank.com

- Only Banxico is expected to deliver a rate cut next week among central banks announcing decisions next week, as the BCB, BoE, and RBA all stay put. Fed expectations may be shaped by another round of key private sector data making up for the lack of official figures due to the U.S. government shutdown that, next Wednesday, would be its longest ever.

- Weekend CPI data out of Peru will be nothing to be scared about, as previewed by our local team in today’s Weekly, who also discuss early data teeing up another strong month for growth in November. Our economists in Chile also preview September CPI and August economic activity data that may shape uncertain BCCh expectations in markets.

- Mexican investment and remittances data should remain weak, in line with recent GDP data that suggest the country’s economy is broadly stagnating according to our colleagues in Mexico. In Colombia, the team talks about the recent selection of Cepeda to represent the ruling party in next year’s votes, as the local electoral season begins to heat up.

More central bank decisions and inflation readings are in store next week, while international trade risks and earnings releases take on reduced importance after the successful Trump-Xi summit and, on average, strong results from tech giants this week. The next few days will be key in shaping Fed cut expectations, with unofficial data (ADP, ISM, and U Mich) on tap, after a hawkish presser by Chairman Powell that slashed cut bets. The U.S. government shutdown continues, with no end in sight. Elsewhere, outside of Latam, the BoE and RBA are widely expected to keep rates steady, while markets will pay attention to Chinese international trade data and Canadian employment figures.

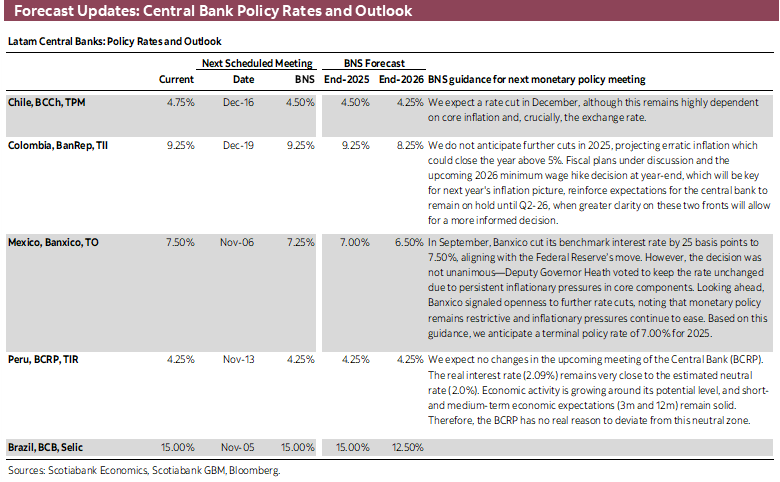

In Latam, we have a couple of rate announcements, with the BCB and Banxico unveiling another rate hold and another 25bps rate cut on Wednesday and Thursday, respectively. On the data front, we’ll have a long gap between regional CPI readings, with Peru releasing October readings over the weekend while Chile and Mexico publish their own figures next Friday. Mexican markets will also parse remittances and investment data, Chile drops economic activity data, and Colombia’s BanRep publishes the meetings to its October 31st meeting as well as a new Monetary Policy Report.

Starting with Banxico, don’t expect anything else than a 25 bps rate cut with a single dissenter in favour of a hold (Heath). Guidance will also likely remain tilted in favour of continued adjustments going forward. However, the case for a Banxico rate cut in December, which remains our call, may have been weakened by lower odds of another Fed reduction at the end of the year—just as Fed dovishness a few months ago helped build up projections fore more easing in Mexico. Slight changes to Banxico’s statement that open the door to ‘skipping’ a meeting may reverberate strongly in markets. Yet, there may already be some apprehension reflected in pricing for the December announcement, with about 16/17bps in market-implied cuts, down from about 20/21 at the start of the week.

On the economic front, expect more weak readings from remittances and investment figures to reinforce calls for looser Banxico rates, keeping in line with underwhelming GDP data released this week that our team in Mexico discuss in today’s weekly. Remittances growth that averaged 2.4% in 2024 has sharply turned in the other direction, averaging a 3.6% y/y decline on a twelve-month rolling basis—or tracking a 5.3% year-to-date y/y drop—that is impacting disposable incomes. Remittances data from Banxico may be failing at capturing money transfers via other means that don’t require or specify that they are remittances flows (possible explaining the divergence with Colombian data, see front page). However, U.S. immigration and employment data would point to a clear impact on the incomes of Mexicans residing in the U.S. and, in turn, on those of domestic recipients of remittances.

Investment figures are some of the worst data out of Mexico these days, reflecting ongoing headwinds to confidence and growth prospects from domestic and external sources. Investment has declined from year-ago levels for since September of last year, when private spending slipped into negative readings, joining public outlays drops as infrastructure investment normalised. In the year-to-July (YTD), machinery investment has fallen by 8% y/y, compared to a 5.7% y/y drop in construction where residential investment has been a decent counterweight, up 7.8% YTD, to a 16% decline in non-residential spending. July figures showed a strong m/m rise of 1.6% (seas.-adj.) on the back of a ~25% rise in imported transport equipment investment that will likely normalise in August figures to show a monthly decline on the aggregate. As for CPI, it’s tough to see markets being surprised by the full-month data as bi-weekly CPI releases already give us a rough, but good, sense of where the monthly print will land—around 3.5–3.6% for headline and 4.2–4.3% for core inflation, both hot but neither troubling Banxico too much.

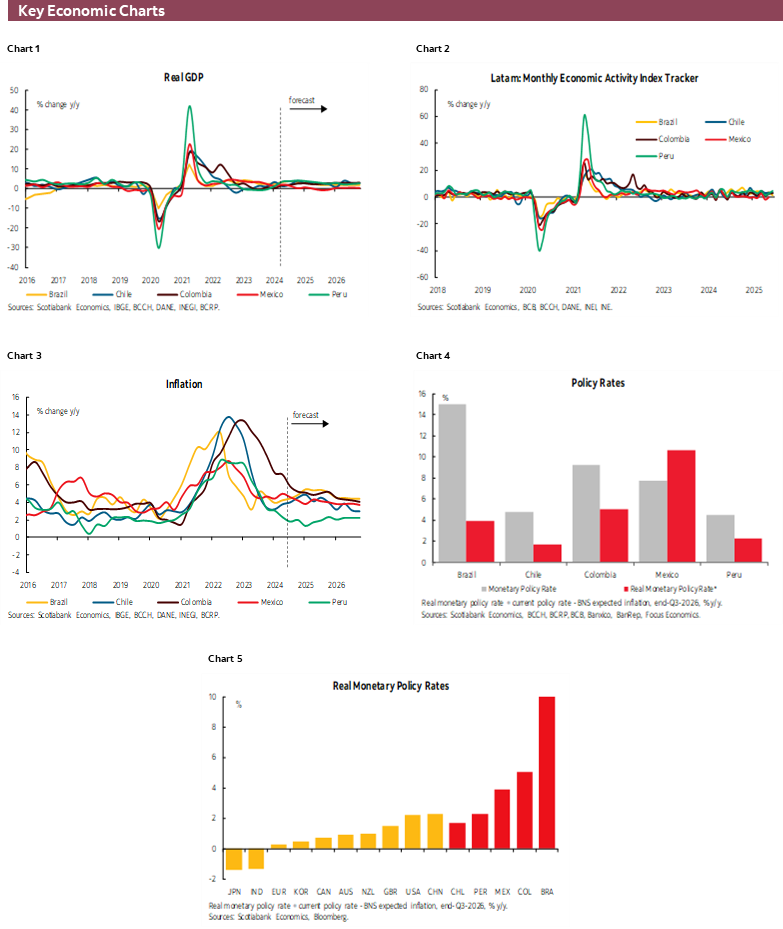

In today’s report, our team in Santiago previews next week’s bookend releases, September economic activity on Monday and CPI on Friday. The team’s models point to GDP gains driven by services, trade, and manufacturing, rebounding from losses in August, that would translate into a 4.4.5% y/y rise in output for the month—decently above the Bloomberg median forecast of 3.2% and the BCCh’s economists survey at 2.5%. For CPI, some price adjustments related to Cyber Day will dampen goods prices, while services prices gains would reflect some seasonal factors as well as labour costs pressures.

Next week’s CPI data will be one of two prices readings that the BCCh will have at hand for their December decision, one that may still be too close to call while our bias remains for a 25bps cut (and markets are pricing in about a 35–40% chance). The BCCh’s next meeting will also take place after the first- and second-round presidential vote in the country, with polls showing the left’s Jara easily heading into a runoff vote against an uncertain opposition, as right-wing candidate Kast has seen his lead over the (more) right-wing Kaiser narrow in recent weeks. Either of the two right-wing candidates would win over Jara according to surveys, though a decent share of ‘unknowns’ among respondents and voters possibly shifting around after the November 16th first round vote leave the final result up in the air.

On a related note, our colleagues in Colombia write on the country’s electoral season starting to heat up. Colombia’s ruling party held a vote last Sunday on who will lead them into the 2026 elections, with Ivan Cepeda coming out victorious. Political observers will now keep a close eye on the forming of coalitions over the next few months, as well as on voting intention polls officially resuming, to help narrow expectations for who will lead the country in 2026–2030. Colombia’s data calendar offers little of note next week, but markets will watch updated projections by BanRep staff in the Monetary Policy Report due on Wednesday as well as the minutes to today’s rate hold scheduled for release on Thursday. News and speculation on next year’s minimum wage hike will also be key to forming BanRep expectations, as the process to decide this increase gets going ahead of formal discussions and consultations in late-November.

According to our economists, Peruvian inflation out on Saturday should be “anything but spooky”, nor should September GDP data based on industry-level indicators. As detailed in today’s note, the team expects a 1.4–1.5% y/y increase in CPI in October, with data trending slightly below our team’s projections which are thus biased downward. In light of muted, below-target, price trends we think the BCRP will have room to lower its reference rate by an additional 25bps at some point in early-2026. This comes despite a strong economic performance, as sectoral data and high-frequency indicators suggest GDP growth may accelerate in September from August’s already-solid 3.2% print. Late-2025 economic data will also have an impact on 2026 forecasts, as the latest withdrawal from pensions funds should begin to show up in spending figures.

PACIFIC ALLIANCE COUNTRY UPDATES

Chile—Inflation Driven by Volatile Items and Cost Pressures in Services

Waldo Riveras, Senior Economist

+56.2.2619.5465 (Chile)

waldo.riveras@scotiabank.cl

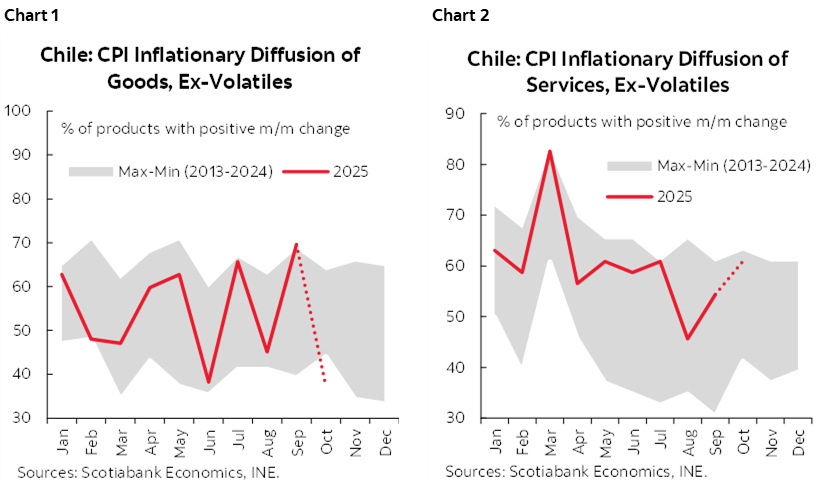

We forecast October CPI at 0.3% m/m, slightly above market pricing but aligned with survey expectations. Core inflation (excluding volatiles) would rise 0.2% m/m, supported by services, while goods remain flat. Volatile items would contribute +0.18 ppts. Food and housing divisions lead the monthly increase due to seasonal price adjustments and higher labour costs.

We assume broad price declines in goods, reflecting Cyber Monday effects (charts 1 and 2). Though not sharp, these declines are widespread across core goods, leading to negative contributions from clothing, household equipment, and miscellaneous goods. In contrast, services inflation diffusion increases, reflecting labour cost pressures.

Fuel prices rose slightly in October, with limited CPI impact. However, a notable drop in gasoline prices is expected next week, implying a negative contribution to November CPI.

Electricity tariffs are projected to fall in January, with a 2% drop in electricity supply contributing –0.07 ppts to CPI. Expected refunds for overcharges will be applied directly to bills and are excluded from CPI calculations, implying no inflation impact.

We anticipate a monthly GDP (Imacec) between 4–4.5% y/y for September (4.5–5% for Non-mining GDP), well above consensus.

Our nowcasting models suggest that services, commerce, and manufacturing posted seasonally adjusted gains in September, fully reversing the decline observed in August and pushing non-mining GDP to a new historical high. Seasonal factors also played a key role in September, with two additional working days compared to the same month last year. At Scotiabank, we reaffirm our full-year GDP growth forecast of 2.5%, which should be seen as a floor.

Colombia’s Electoral Season Gains Momentum

Jackeline Piraján, Head Economist, Colombia

+57.601.745.6300 Ext. 9400 (Colombia)

jackeline.pirajan@scotiabankcolpatria.com

Valentina Guio, Senior Economist

+57.601.745.6300 Ext. 9166 (Colombia)

daniela.guio@scotiabank.com

On Sunday, October 26th, Colombia’s ruling party, Pacto Histórico, held an internal consultation to select its candidate for the 2026 presidential and congressional elections. This event marks the beginning of increased political activity and attention in the country as the electoral cycle approaches.

Key highlights from the consultation include:

- Voter turnout: Approximately 2.7 million people participated. While this figure may seem low compared to the 2022 presidential elections, it is considered significant given the current stage of the electoral calendar. This turnout is comparable to the support Pacto Histórico received in the 2022 congressional elections (~2.8 million votes), where it emerged as the largest individual force in the Senate and the second largest in the House of Representatives.

- Regional strengthening: Support for Pacto Histórico increased in several regions, particularly where governors belong to the ruling party and public spending has risen. However, the party showed signs of weakening in Colombia’s major cities.

- Presidential candidate: Iván Cepeda was elected as the party’s presidential candidate, receiving 1.5 million votes. This provides a solid foundation for positioning himself as the leading figure of the left. There is potential for Cepeda to participate in a broader coalition consultation in March 2026, although this depends on the ruling of the National Electoral Council.

- Coalition talks: The results of the consultation have prompted key political leaders to explore potential alliances. Former President César Gaviria, leader of the Liberal Party (third largest in the Senate and largest in the House), and former President Álvaro Uribe, leader of the Centro Democrático Party (fifth in the Senate and sixth in the House), scheduled a meeting later in the week to discuss possible coalitions. Other prominent candidates have also begun forming alliances.

Although the congressional elections are five months away and the presidential elections are seven months out, the coalitions formed before year-end will be critical. Starting October 31th, voter intention polls may be published again, providing clearer insights into the electoral landscape in the coming weeks.

Centro Democrático will select its presidential candidate on November 28th, and other parties are expected to announce their candidates and coalition intentions before the end of the year, ahead of the March 8th congressional vote.

Market Implications

So far, Colombian financial assets have responded primarily to macroeconomic and market-driven factors. However, structural issues such as fiscal policy will be heavily influenced by the upcoming government transition. In this context, certain fiscal risk premiums, moderately reflected in the exchange rate due to what we consider an overshooting FX of the carry trade and expectations around government monetization of foreign currency debt. In Scotiabank Colpatria we estimate the fiscal risk premium of the FX at approximately COP 200, and we think it could at least start to emerge again as a relevant component of the operation depending on the proximity of the elections and the direction of voter sentiment.

Mexico—Data Point to Stagnation

Rodolfo Mitchell, Director of Economic and Sectoral Analysis

+52.55.3977.4556 (Mexico)

mitchell.cervera@scotiabank.com.mx

Miguel Saldaña, Economist

+52.55.5123.1718 (Mexico)

msaldanab@scotiabank.com.mx

Martha Cordova, Economic Research Specialist

+52.55.5435.4824 (Mexico)

martha.cordovamendez@scotiabank.com.mx

As the year draws to a close, recent economic activity data continues to point to stagnation. This week, two indicators stood out reinforcing this outlook: the flash GDP estimate for the third quarter and labour market figures for September.

In the first case, the data show significant declines in industry and a slowdown in services throughout the year, while labour indicators suggest weaker momentum and, consequently, softer income conditions for households. However, these figures contrast with some expectations from private analysts and international organizations, so we believe downward revisions to those forecasts are likely in the coming weeks.

According to INEGI figures, GDP contracted by -0.2% year-over-year in the third quarter, following stagnation (0.0% y/y) in the previous quarter. This means the Mexican economy has grown only 0.2% YTD in the first three quarters of the year. Most of the decline comes from industrial activities, except for several manufacturing sectors.

As of August, mining (including oil extraction) posted an annual real drop of -8.1%, while electricity, water, and gas supply—public utilities—fell by -2.3%. Construction also shows a cumulative decline of -1.8%, driven by a collapse of nearly one-third during the same period, and has recorded annual decreases since July 2024, affected by the closure of key government projects and heightened domestic uncertainty following the composition of the new legislature and the approval of constitutional reforms that altered the structure of the federal government and the judiciary.

Uncertainty has also impacted some manufacturing sectors, notably transportation equipment (-4.0% annual real decline), which has been particularly affected by uncertainty surrounding U.S. trade policy and the renegotiation of the USMCA. Thus, we believe the combined effect of domestic and international uncertainty is reflected in the contraction of industrial activities, especially those tied to investment prospects.

This negative reading contrasts with recent upward revisions in growth expectations by private analysts and international organizations. According to Banco de México’s Survey of Expectations, private analysts now forecast 0.5% growth for this year, up from the 0.18% low expected in May, followed by 1.35% in 2026. In the same vein, the IMF also revised its forecast in October, now projecting 1.0%.

However, based on this week’s data and assuming no major revisions, achieving the 0.5% consensus would require economic activity to rebound by 1.5% year-over-year in the fourth quarter, while reaching 1.0% would demand a rebound of over 3.0%. This contrasts with the outlook of downside risks, mainly due to weaker-than-expected investment stemming from domestic uncertainty, as well as greater international uncertainty regarding U.S. trade policy.

If the current consensus holds, this year’s growth would be the slowest for any positive year since at least 1985, and including contraction years, the weakest since the 2020 pandemic. Therefore, the outlook for the next quarter remains one of economic weakness, with a risk balance tilted to the downside, driven mainly by industrial setbacks amid high uncertainty, a more aggressive tax policy, subdued public investment spending, and lower household incomes, which will in turn affect service activity.

Peru—Key Upcoming Data is Anything but Spooky

Guillermo Arbe, Head Economist, Peru

+51.1.211.6052 (Peru)

guillermo.arbe@scotiabank.com.pe

The October inflation figure will be released on Saturday, November 1st. In addition, key sector growth data for September will be released either on Saturday or Monday, November 3rd, given that Saturday is a holiday (All Saints Day).

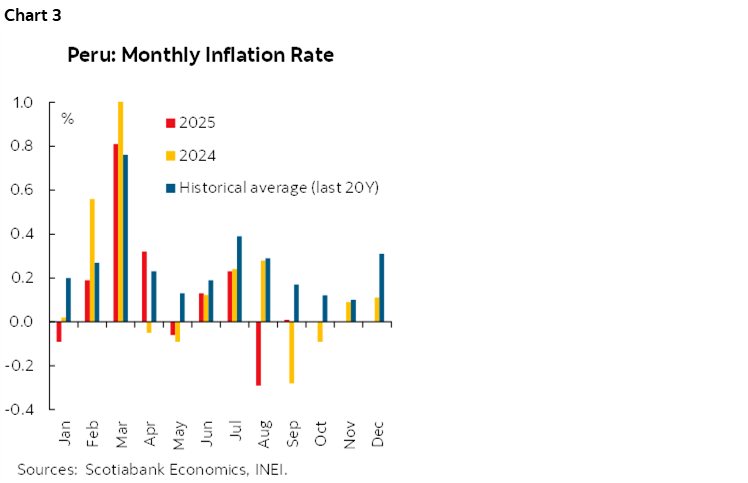

If you are reading this on Monday, you probably know the inflation figure by now. The key price figures that we follow point to a monthly inflation of nil to slightly negative for October. Something similar occurred in October 2024, when inflation came in at -0.1%, MoM (chart 3). As a result, yearly inflation could conceivably stay at 1.4%, or rise slightly to 1.5%. The bottom line is this: inflation is trending mildly below our full-year forecast of 1.9%, which gives our forecast a downward bias.

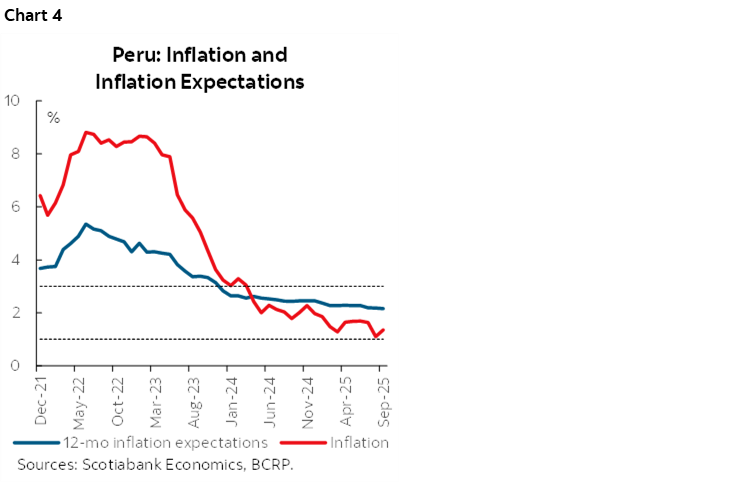

Weak inflation reinforces our expectation that the BCRP will lower the reference rate one more time, to 4.0%, sometime in the first few months of 2026. Inflation expectations, currently at 2.16% (chart 4), are likely to decline closer to 2.0%, putting the neutral reference rate within striking range of 4.0% (given the BCRP determined neutral real rate of 2.0%). And, with inflation so low, there is no reason to keep the reference rate higher than neutral. Note that there is also no reason to lower it below neutral as economic growth is also doing reasonably well.

September GDP still hovering above 3.0%

Fishing GDP rose 6.4%, YoY, in September. This figure, released this week, was the first sector figure for September GDP. Either on Saturday or Monday, Mining GDP figures should be released, and possibly Agriculture GDP as well. Fishing GDP figure is non-material, as September is still the off-season for fishing, but mining and agriculture will be indicative. Mining GDP growth has been rather weak lately, and we do not expect much better for September. Agriculture GDP growth, however, could be more interesting. Agriculture has been very volatile in MoM terms, but robust overall.

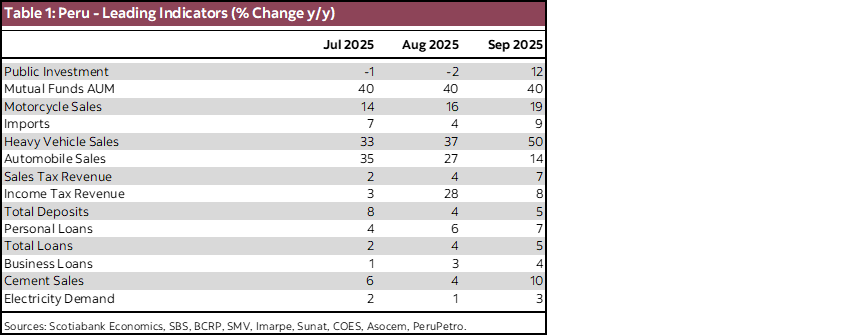

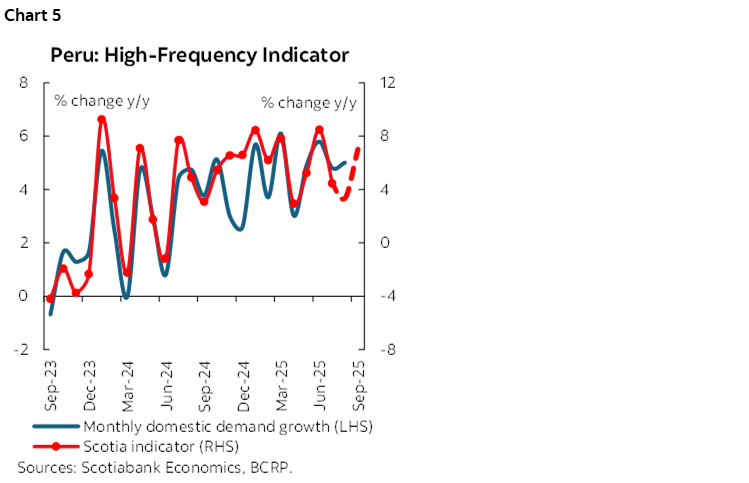

All these resource-related figures will pale in comparison to GDP sectors linked to domestic demand. The high frequency indicator we follow suggests that in September non-resource GDP growth—linked to domestic demand—should surpass the 3.6% registered in August (table 1 and chart 5). Note, however, the comparison base is high. Given this, it will be telling if September GDP growth could surpass 3.2% growth seen in August. If it does, and it’s a fair bet that it will, this would indicate that domestic demand is, indeed, accelerating.

November GDP growth will be even more interesting. Pension fund withdrawals will begin in November, and although most of the impact on consumption is likely to take place in early 2026, there will be at least an incipient effect starting in November.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Click here to be redirected |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.