ECONOMIC OVERVIEW

- No U.S. data and a limited G20 release slate means there may be little for global markets to trade on next week, leaving traders to sit on their anxiety over AI-related gains in equities, with no end in sight to the longest-ever U.S. government shutdown.

- In Latam, Colombia and Brazil publish inflation data that will be key for minimum wage hike expectations for the former, and with read-throughs to the timing of the next BanRep (maybe even up?) and BCB (when are cuts coming back?) moves.

- We think the BCRP will keep policy steady with real rates sitting practically at their neutral level, but who here hasn’t been surprised by Peru’s central bank.

- Friday’s inflation undershoot may see more economists calling for a BCCh rate cut next month with the results of the central bank’s survey on tap alongside the minutes to its latest meeting, just a few days before next Sunday’s elections.

- Mexican industrial production is the only noteworthy domestic item on tap next week. In today’s report, our team in Mexico discusses recent international trade developments.

PACIFIC ALLIANCE COUNTRY UPDATES

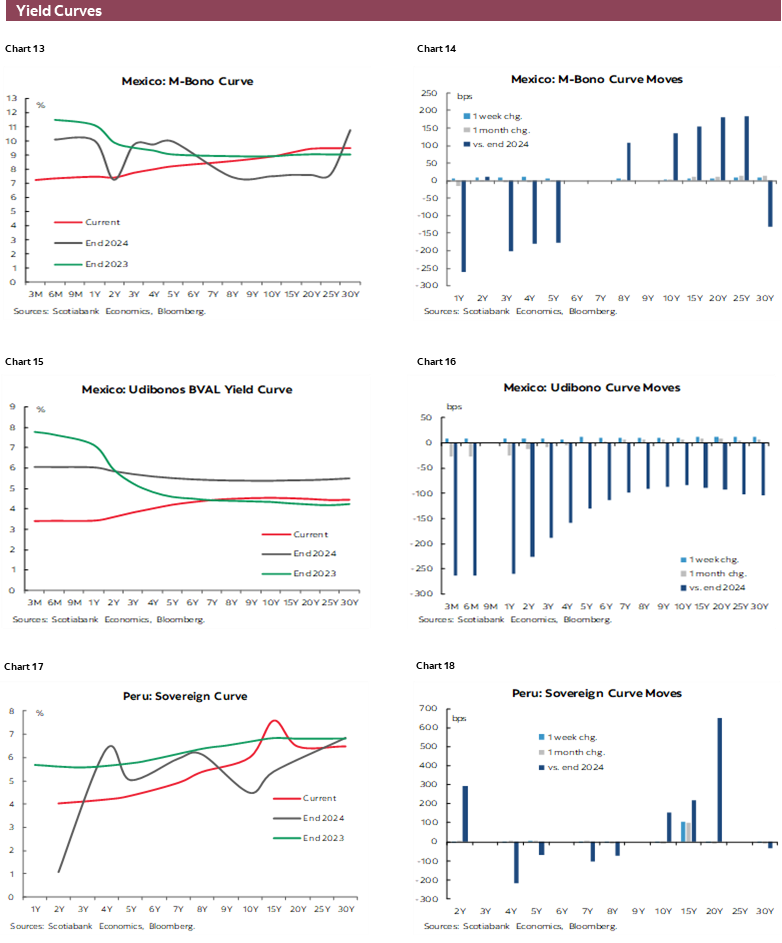

- We assess key insights from the last week, with highlights on the main issues to watch in Mexico.

MARKET EVENTS & INDICATORS

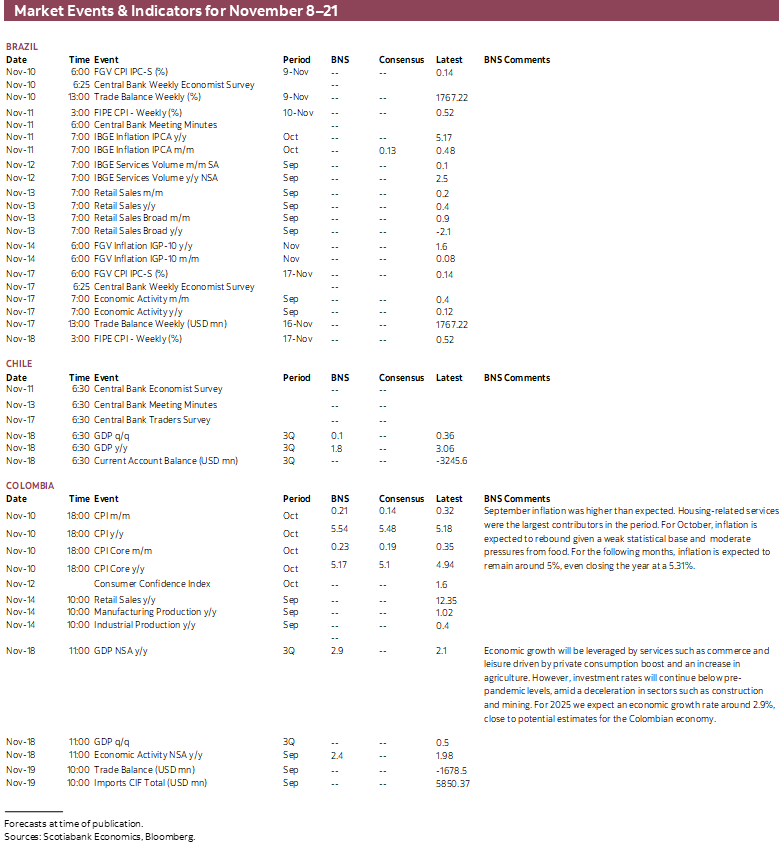

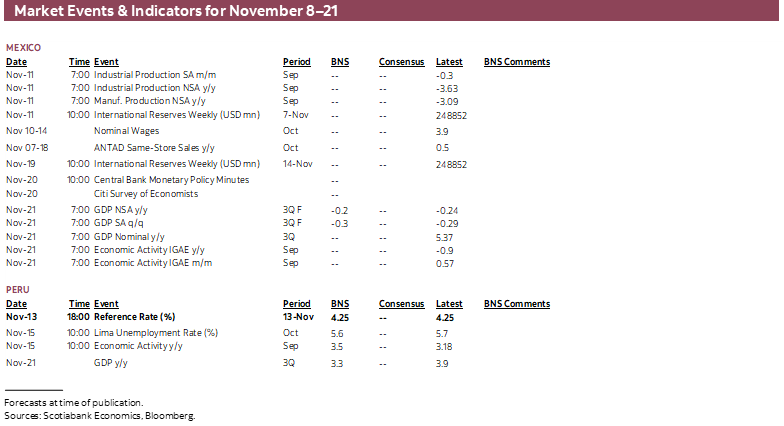

- A comprehensive risk calendar with selected highlights for the period November 8–21 across the Pacific Alliance countries and Brazil.

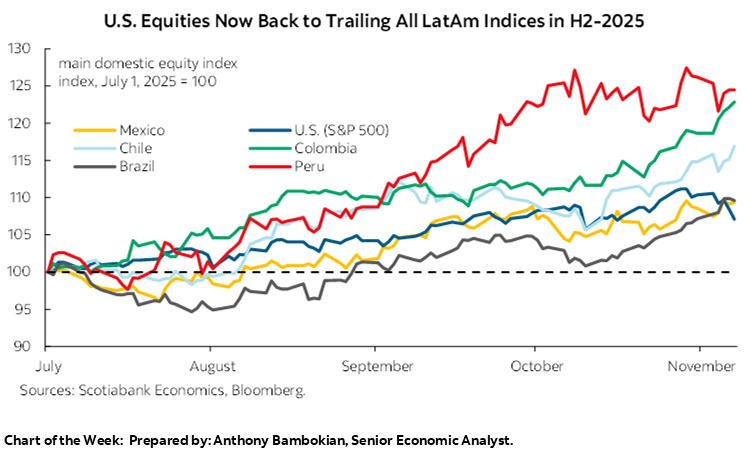

Chart of the Week

ECONOMIC OVERVIEW: COLOMBIA & BRAZIL CPI, BCRP TO HOLD (?)

Juan Manuel Herrera, Senior Economist

+52.55.2299.6675

juanmanuel.herrera@scotiabank.com

- No U.S. data and a limited G20 release slate means there may be little for global markets to trade on next week, leaving traders to sit on their anxiety over AI-related gains in equities, with no end in sight to the longest-ever U.S. government shutdown.

- In Latam, Colombia and Brazil publish inflation data that will be key for minimum wage hike expectations for the former, and with read-throughs to the timing of the next BanRep (maybe even up?) and BCB (when are cuts coming back?) moves.

- We think the BCRP will keep policy steady with real rates sitting practically at their neutral level, but who here hasn’t been surprised by Peru’s central bank.

- Friday’s inflation undershoot may see more economists calling for a BCCh rate cut next month with the results of the central bank’s survey on tap alongside the minutes to its latest meeting, just a few days before next Sunday’s elections.

- Mexican industrial production is the only noteworthy domestic item on tap next week. In today’s report, our team in Mexico discusses recent international trade developments.

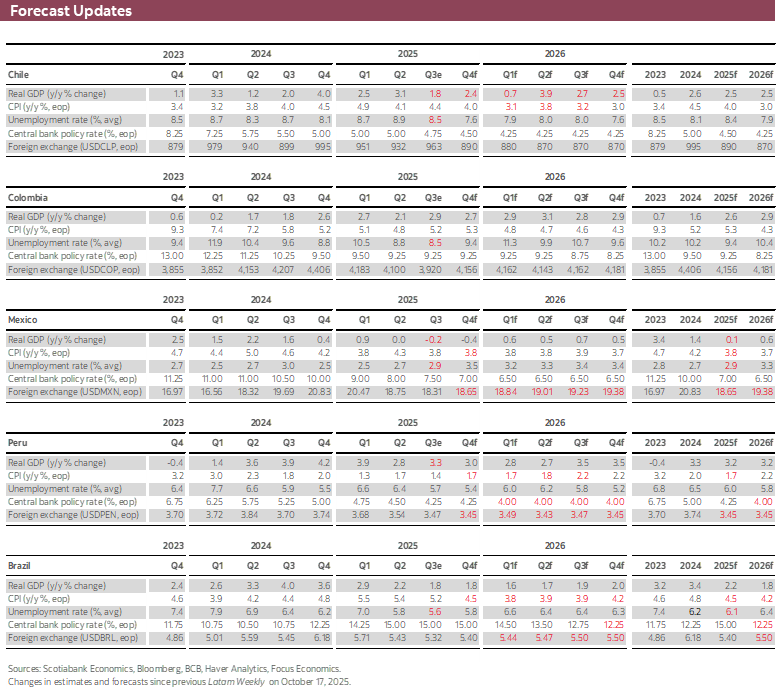

The absence of official U.S. data amid the longest-ever government shutdown (with no end date seemingly in sight) leaves global markets with another relatively quiet release calendar for the days ahead (U.K. GDP and Chinese CPI and retail sales, among others), all while hesitation about rich AI-related valuations brews and unofficial U.S. economic indicators paint an underwhelming picture of domestic conditions. We’ll have a bit more on our plate in Latin America, with Colombia and Brazil publishing inflation data and sectoral activity readings, the BCRP’s rate decision, and a few bits and pieces out of Mexico and Chile, with the latter also holding general elections next Sunday.

In today’s report, our team in Mexico discusses recent trade developments, following Wednesday’s oral arguments in the U.S. Supreme Court over President Trump’s authority to use emergency powers to levy exceptional duties, and as USMCA consultations near a close in Mexico after their conclusion in the U.S. last Monday, with all three parties working on their case for next year’s treaty review.

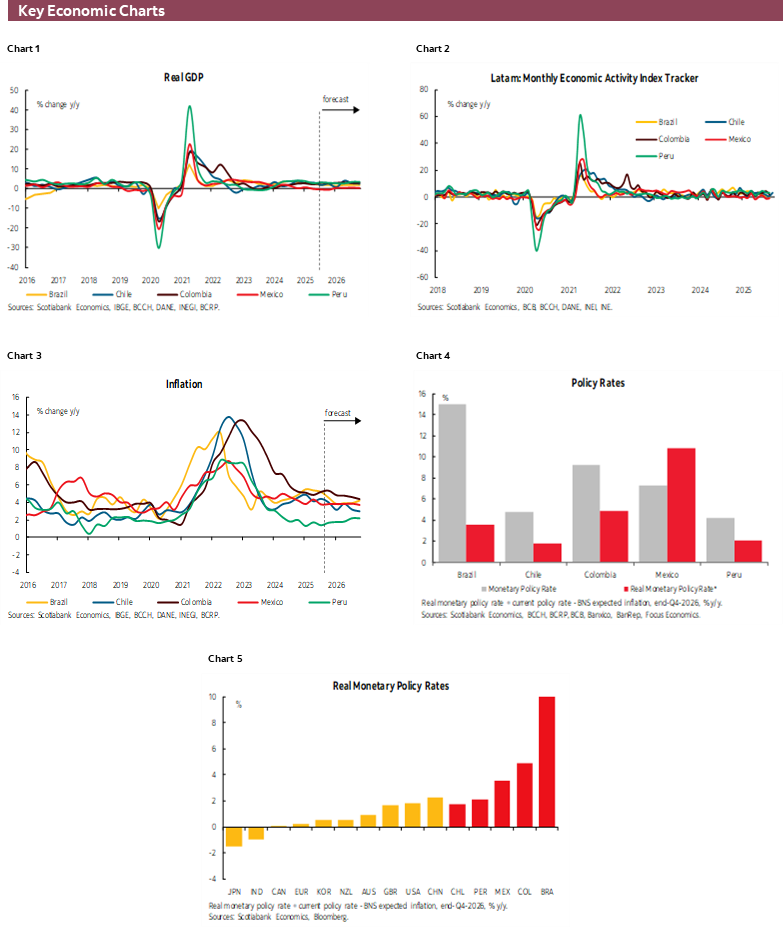

Colombian CPI out on Monday will be key for economist and market expectations for BanRep policy. The minutes to the bank’s latest rate-setting meeting published earlier this week revealed that some policymakers may consider rate hikes were upside inflationary risks to materialize, particularly on the back of another large minimum wage hike for 2026. Petro’s government is eyeing a decent double-digit hike for next year, towards the generous side of things ahead of 2026 elections, in turn stoking important upside price pressures compounded by indexation practices impacting a large share of the CPI basket.

Next week, our economists expect that Colombian CPI inflation will accelerate from 5.2% to 5.5% in headline terms while core inflation (ex. food) goes from 4.9% to 5.2% after four months of sitting just below the 5% mark. The rebound in inflation will owe to a relatively low year-ago base of comparison, but the expected ~0.2% m/m rise in headline and core prices in October is also around double its pre-pandemic decade average increase for October months (while, in October 2024, headline and core CPI marginally rose 0.01% and fell 0.13%, respectively). The team’s forecasted 5.5% increase would be the highest inflation reading since September 2024, falling on the lap of Petro’s administration as discussions on next year’s increase get going over the next few weeks.

Also, does Colombian economic data scream for support from BanRep? Not really, and retail sales and manufacturing/industrial production figures—particularly the former—should show this remains the case. Retail sales are expected to record another double-digit year-on-year gain for September after August’s 12.4% rise, backed by Colombian peso strength that is mirrored in elevated imports, remittances strength, and firmer labour markets. Manufacturing output has been a bit soft, with August’s 1% y/y (its weakest since April) likely to be followed by a stronger reading for September as fewer working days impacted the previous month’s print.

On Tuesday, Brazil’s headline inflation is seen falling below 5% in October, to 4.7–4.8% off a 5.2% y/y rise in September, possibly adding to speculation that the BCB may soon reconsider policy easing. The minutes to the BCB’s latest rate hold decision come out the same day, to be monitored for signs that some within the council are comforted by slowing inflation to back a rate cut, possibly as soon as the December gathering (although short of a majority). At writing, markets are assigning negligible odds to a cut in December, but see about a 60% chance that the BCB lowers the Selic rate in January and are certain that at least one cut will come in 1Q26. Services activity and retail sales data for September out on Wednesday and Thursday, respectively, are expected to show an acceleration from August in year-on-year terms.

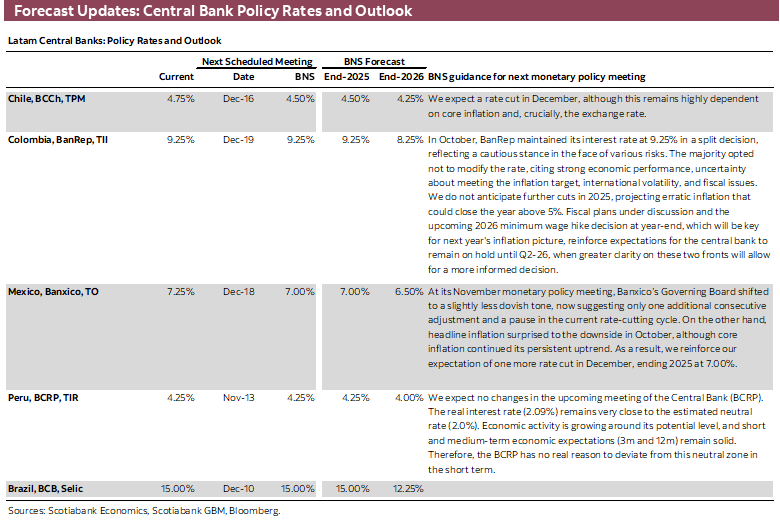

While Colombia and Brazil are stressing out over CPI prints in the 5% zone, Peru’s central bank is kicking back, staring at its 1.35% y/y inflation rate for October and thinking maybe I will just announce another reference rate cut. We still think that the BCRP will opt for a rate hold at its Thursday announcement, with the country’s real interest rate at 2.09% sitting pretty close to the estimated 2% neutral rate, all the while firm economic conditions reflect little need for the BCRP to loosen policy further (at least for the time being). Still, it wouldn’t be unlike the BCRP to surprise some economists by opting for another rate cut—although we don’t think one is justified at the moment.

Mexico’s and Chile’s calendars have little on tap, with the former only publishing industrial production data (another contraction awaits) while Chile’s central bank releases the results to its economists survey on Tuesday and the minutes to its latest decision on Thursday. Chile’s large downside surprise in October inflation out this morning, coming in at 3.4% y/y vs the 3.7% y/y median forecast, will likely see a greater share of economists polled by the BCCh anticipating a rate cut at the December meeting. Markets have drastically revisited their bets on next month’s decision, with 17bps priced in at writing compared to only 9bps at yesterday’s close.

The BCCh’s minutes may shed some light on the bias of officials going into the final meeting of the year and how an encouraging inflation reading, like today’s, could tilt them in favour of a rate cut. However, they may need confirmation from another soft CPI record in December data to opt for a cut, and may also be influenced by the results of elections with votes cast for Congress and the first round presidential election next Sunday, with the second-round presidential vote scheduled for December 14th, two days before the BCCh’s announcement.

PACIFIC ALLIANCE COUNTRY UPDATES

Mexico—Key Week for Mexico’s International Trade: Progress in USMCA Public Consultations and Tariff Review in the U.S.

Rodolfo Mitchell, Director of Economic and Sectoral Analysis

+52.55.3977.4556 (Mexico)

mitchell.cervera@scotiabank.com.mx

Miguel Saldaña, Economist

+52.55.5123.1718 (Mexico)

msaldanab@scotiabank.com.mx

Martha Cordova, Economic Research Specialist

+52.55.5435.4824 (Mexico)

martha.cordovamendez@scotiabank.com.mx

This week marked a significant moment for Mexico’s international trade within the framework of the United States-Mexico-Canada Agreement (USMCA). On November 3rd, public consultations concluded in the United States and Canada, while on November 5th, the U.S. Supreme Court held oral arguments to assess the legality of certain tariffs imposed. These public participation exercises are essential in preparing for the treaty’s six-year review, scheduled for July 2026, in accordance with the agreement.

The USMCA public consultations are an open dialogue mechanism that allows governments, businesses, civil society organizations, and citizens to submit comments, proposals, and concerns regarding the treaty’s implementation. Their goal is to gather input to shape each country’s negotiating stance for the joint review. In Mexico, the process began on September 17th, 2025, lasting 60 calendar days. It was organized by the Ministry of Economy and carried out through sectoral and state-level roundtables across all 32 federal entities, covering more than 30 productive sectors such as agribusiness, automotive, textiles, and information technologies. For the first time, labour unions were formally included, marking progress in the inclusion of key social actors.

Key topics discussed include U.S. tariffs imposed under Section 232, comparative agricultural subsidies between Mexico and the U.S., the Rapid Response Labour Mechanism—applicable only to Mexico—as well as market access, rules of origin, and digital trade. In the United States, the call for public input was issued by the Office of the U.S. Trade Representative (USTR), also beginning on September 17th. Although the consultations ended on November 3rd, a public hearing is scheduled for November 17th to gather additional comments and define the U.S. negotiating position ahead of the 2026 review.

Looking ahead, Mexico is expected to consolidate the proposals received into a document reflecting it’s priorities, although no publication date has been announced yet. Subsequently, formal evaluation among the three countries will begin in January of that year. Finally, in July 2026, the three partners must decide whether to extend the agreement for another 16 years or renegotiate its content.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Click here to be redirected |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.