ECONOMIC OVERVIEW

- Mexican and Brazilian H1-Feb CPI are the highlights of next week’s regional data calendar with only secondary releases elsewhere in Latin America. Recent inflation data in Latam’s largest economies have prompted a re-think of the policy rates outlook by markets, economists, and the local central banks.

- In today’s weekly, our Mexico team analyses the more favourable backdrop for the country’s assets that has developed since late-2022. The MXN has been the best performing major currency for the month, as well, aided in part by Banxico’s surprisingly hawkish decision earlier this month.

- Our economists in Peru discuss the greater-than-expected impact of the protests on the economy, as we near tonight’s deadline for an agreement on an early election—with the risk that lawmakers don’t reach an agreement and protests intensify.

- It’s been a busy week for Colombia after President Petro presented an ambitious health reform. The team in Bogota believe the plan will face tougher opposition in Congress than the tax reform.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Colombia, Mexico, and Peru.

MARKET EVENTS & INDICATORS

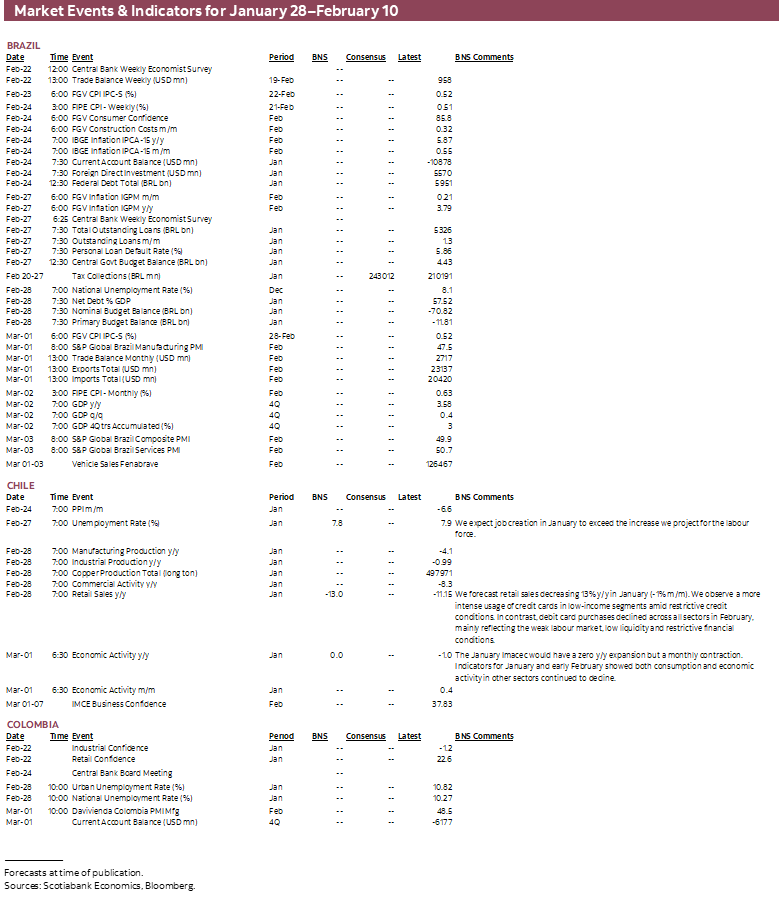

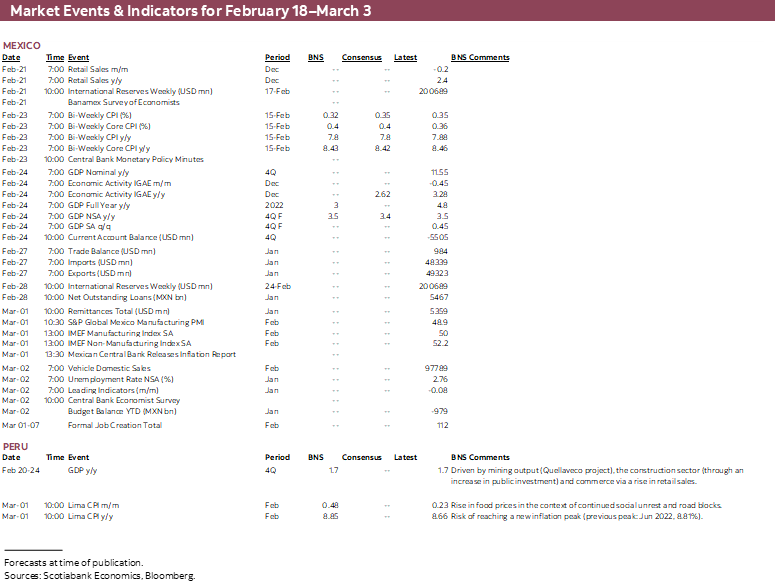

- A comprehensive risk calendar with selected highlights for the period February 18–March 3 across the Pacific Alliance countries and Brazil.

Chart of the Week

ECONOMIC OVERVIEW: MEXICAN AND BRAZILIAN INFLATION AMID REGIONAL POLITICAL RISKS

Juan Manuel Herrera, Senior Economist/Strategist

Scotiabank GBM

+44.207.826.5654

juanmanuel.herrera@scotiabank.com

- Mexican and Brazilian H1-Feb CPI are the highlights of next week’s regional data calendar with only secondary releases elsewhere in Latin America. Recent inflation data in Latam’s largest economies have prompted a re-think of the policy rates outlook by markets, economists, and the local central banks.

- In today’s weekly, our Mexico team analyses the more favourable backdrop for the country’s assets that has developed since late-2022. The MXN has been the best performing major currency for the month, as well, aided in part by Banxico’s surprisingly hawkish decision earlier this month.

- Our economists in Peru discuss the greater-than-expected impact of the protests on the economy, as we near tonight’s deadline for an agreement on an early election—with the risk that lawmakers don’t reach an agreement and protests intensify.

- It’s been a busy week for Colombia after President Petro presented an ambitious health reform. The team in Bogota believe the plan will face tougher opposition in Congress than the tax reform.

Mexican and Brazilian H1-Feb CPI are the highlights of next week’s regional data calendar with only secondary releases elsewhere in Latin America. A few weeks ago, the monetary policy outlook for Banxico and the BCB seemed clearer, with the former previously expected to only hike a couple more times by 25bps while the latter was seen holding rates unchanged for a few months before easing as inflation held its downtrend.

Since then, a strong H1-Jan Mexican inflation print—particularly in core—ultimately prompted Banxico to hike 50bps against a universal expectation of only 25bps. The bank’s decision may have been the right one in reaction to local inflation dynamics, but it was a frustrating turn from a central bank that seemed on track to even consider a pause after its February decision. We hope the bank’s monetary policy meeting minutes due for release on Thursday will clarify why it decided to move in such an unexpected way.

Thursday’s bi-weekly CPI data will be closely watched to determine how many more hikes Banxico roll out, with economists not expecting a sizable deceleration in core inflation. Mexico’s December IGAE out on Friday will provide little additional information after the country’s preliminary Q4 GDP reading of 3.5% y/y (final estimate also out on Friday). INEGI’s IGAE “nowcast” for January showed a 2.8% y/y expansion for the month after 2.6% y/y (a decent start to the year).

The team’s expectation is that the bank will lift the overnight rate by another 50bps at its late-March meeting, with a combined additional 50bps coming in the second quarter. On Tuesday, ahead of the inflation print later in the week, we get the results to the Banamex survey of economists which should show a higher Banxico rate projection than the pre-announcement median of 10.50% at year-end.

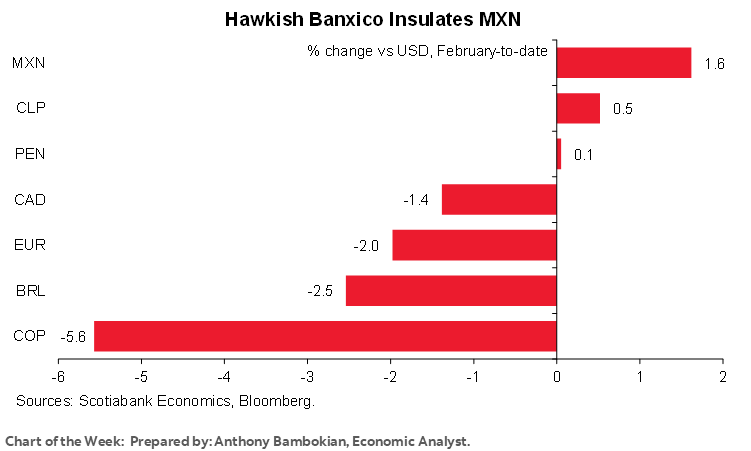

Banxico’s newfound hawkishness has helped the MXN to resist the broad dollar-positive tone that has taken over markets in recent weeks (post nonfarm data). Since the end of January, the MXN has gained roughly 1.5–2% against the USD as the best performing major in the month-to-date against the greenback—it was, in fact, the only currency not in the red for the month before this morning’s slide in the USD. The MXN is the best performing major in the month-to-date against the greenback and is, in fact, the only currency not in the red.

Eduardo Suárez, Scotiabank’s chief economist in Mexico, looks at the improving backdrop for Mexican assets in today’s Weekly. The recent rebound in the share of foreign holdings of the country’s debt—which remains low, however—has been supported, in part, by technical factors.

A similar story to Mexico’s has unfolded in Brazil in regards to rate expectations. However, instead of additional hikes, economists that in November were anticipating 250bps in rate cuts by the end of this year are now projecting half of that. Experts have pushed out the start of the monetary easing and its steepness as the disinflationary path slows at elevated levels around 6% over the past three months. The BCB has also expressed concerns over inflationary pressures from looser fiscal policy alongside an associated pick-up in inflation expectations.

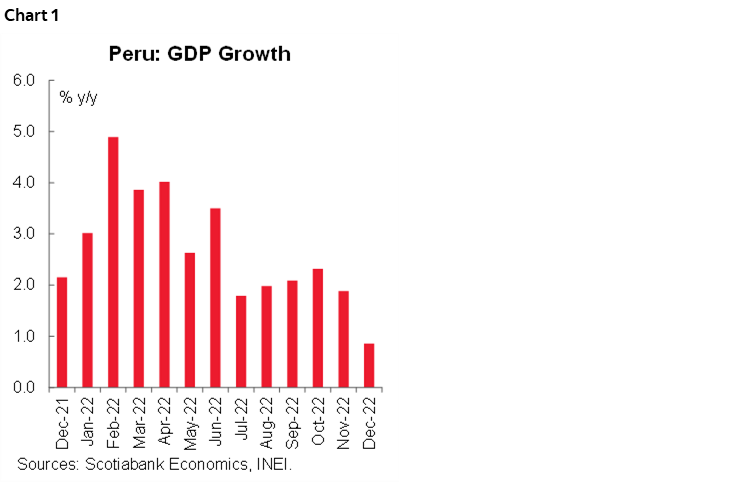

Our attention regarding Peru will squarely remain on protests and their impact and whether Congress reaches an agreement on a new election (deadline today). This looks like a long stretch as President Boluarte has been unable to convince lawmakers to settle on a 2023 date. There’s always a chance that congresspeople kick the can down the road and extend the legislative session another week, as they did last Friday. In today’s report, Mario Guerrero analyses the greater than expected impact of protests on the country's economy, which resulted in the lowest pace of year-on-year growth in Peru since February 2021—and only the beginning of operations at the Quellaveco mine prevented a negative reading. They believe the impact on the economy will be greater in January than in December as protests and disruptions intensified and broadened to other parts of the country.

Also as regards political developments, the Bogota economists discuss an eventful week in Colombia where Petro presented his health reform, a more ambitious plan than anticipated and its progress through Congress will be key to gauge the opposition to the President’s aspirations on multiple fronts—and the team believes this will prove more challenging to him than the tax reform of last year.

As noted previously, data releases elsewhere in the region are limited. Colombia’s industrial and retail confidence surveys (and a non-rate setting meeting) and Chile’s PPI are unlikely to alter our expectations for these economies. Meanwhile, Peruvian Q4 GDP data from the INEI has been front-run by the BCRP’s estimates published on the 15th that showed the country’s economy expanded 1.7% y/y in the quarter. On the international stage, a flood of PMIs will give us an early look into the performance of the major economies in the current month while markets will keep a close eye on the Fed’s Jan 31–Feb 1 meeting minutes in light of the recent hawkish turn from policymakers after strong US data.

PACIFIC ALLIANCE COUNTRY UPDATES

Colombia—Between a Crowded Political Timetable and International Volatility

Sergio Olarte, Head Economist, Colombia

+57.1.745.6300 Ext. 9166 (Colombia)

sergio.olarte@scotiabankcolpatria.com

María Mejía, Economist

+57.1.745.6300 (Colombia)

maria1.mejia@scotiabankcolpatria.com

Jackeline Piraján, Senior Economist

+57.1.745.6300 Ext. 9400 (Colombia)

jackeline.pirajan@scotiabankcolpatria.com

It was an important week for Colombia’s political timetable. On Monday, the government presented its health reform before Congress. The proposal was more ambitious than what was anticipated given past government announcements. As has usually been the case, the “what” is not the problem, the problem is the “how”. In fact, the social purposes of the health reform sound fair, increase and improve medical attention in regions, improve conditions for health sector workers, and increase prevention programs. However, what is worsening uncertainty is the method employed to achieve those targets.

The health reform proposes to centralize the administration of contributions to the health system in a public entity, which will administrate the collection of resources and the payment of health services. This figure reduces the current role of Health Promoting Entities (EPS, private and public), which provide care and insurance for those affiliated with Colombia’s public health system. The current system has been in place for more than 25 years accounting for more than 95% of health coverage in Colombia. The reform proposes a new scheme of regional attention. In the case of EPS, they will see a reduced scope of action to only provide services in limited locations, which increases the uncertainty in the private sector.

The discussion of the health reform in Congress will give us a sense of how strong political support is for the government. For now, the main political parties in Congress haven’t yet given their take on the proposal. We anticipate that negotiations could be harder than what we saw in the case of the tax reform. On the other hand, Minister Ocampo stressed, again, that any reform should be aligned with the fiscal consolidation compromise (fiscal rule and debt reduction). In that regard, preliminary calculations suggest that the implementation cost of the health reform is initially around COP30bn (~2.4 % of GDP), which covers building the initial capacity.

Our opinion of the reform is that it is revealing the guidelines of how the government wants to carry out reform, which is building a bigger State, responsible for administering all social security income and payments.

This week, the government also said that the budget top-up for 2023 will be COP23bn, in line with expectations. The budget addition incorporates around COP20bn financed from additional revenue due to the fiscal reform but also includes the effect of additional tax collection in 2022 due to better economic growth, better than expected oil prices, and under-execution of the 2022 budget. That said, it won’t increase COLTES issuance, it is neutral for debt. On the flip side, it will show how the government wants to spend money. A program that is very intensive in subsidies would make it harder for inflation to slow.

In light of the week’s events, local assets have been under pressure, as domestic investors remain very aware of what happens with this crowded political agenda. Offshore investors seem to be responding more to international drivers around the Fed. All of the above is the perfect mix to keep volatility high.

Mexico—Inflows into Mexican Markets are Recovering Somewhat—Market Technicals are Helping

Eduardo Suárez, VP, Latin America Economics

+52.55.9179.5174 (Mexico)

esuarezm@scotiabank.com.mx

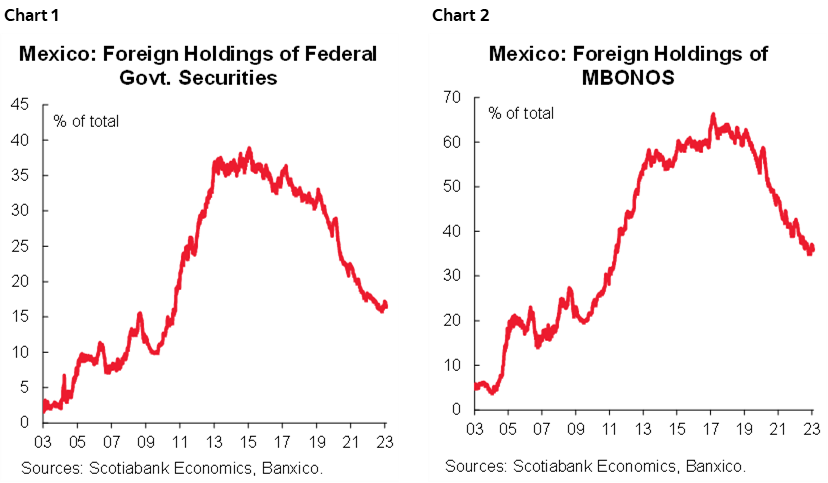

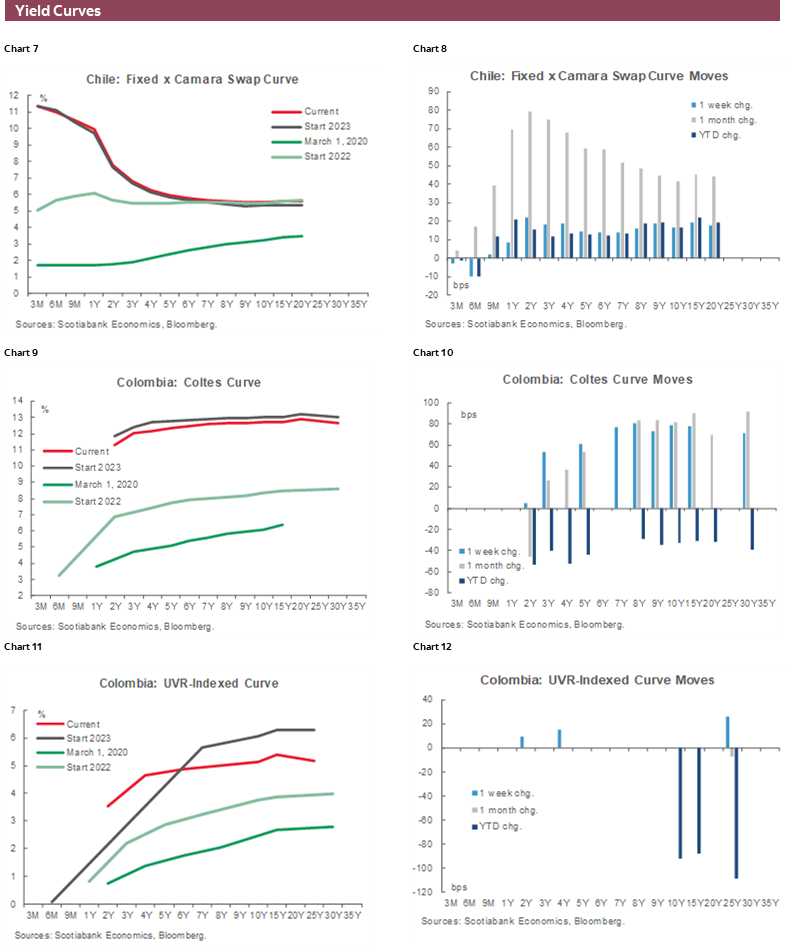

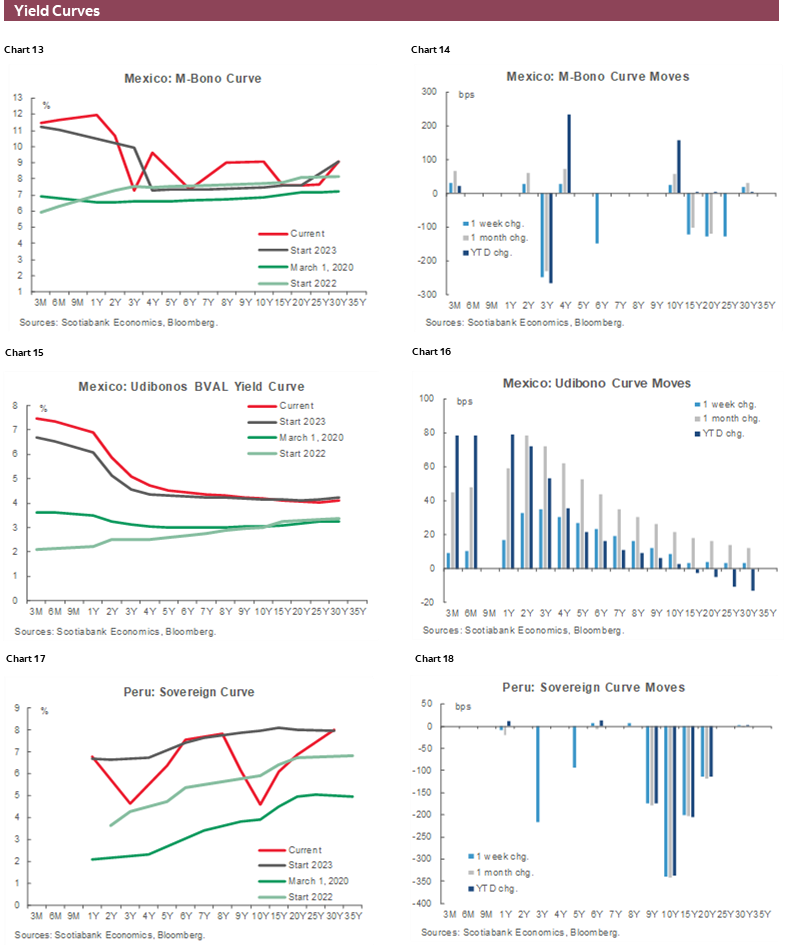

Over the last few weeks, we’ve seen a stabilization / rebound in foreign holdings of Mexican securities—particularly in m-bonos, where foreign holdings bottomed out around November 2022. Foreign holdings are still materially lower than their peak of 66% of the total but have rebounded about 2 percentage points from their minimum of 34.9% in the past four years (charts 1 and 2). We believe several factors explain the recovery in appetite for m-bonos, with several of them being market technicals.

1. We believe that the decline in foreign holdings was driven to a large degree by the exit of crossover investors who did not have m-bonos and MXN risk as part of their benchmark. With that crossover exit, a large share of remaining investors is either passive investors that replicate global benchmarks, such as the WGBI, or EM-dedicated investors that have benchmarks such as the GBI EM or ELMI+. This means that a large share of remaining investors has both m-bono and MXN risk tolerance in their benchmarks and are thus less likely to aggressively buy USD/MXN during periods of uncertainty. This has the impact of reducing MXN volatility—thus improving the carry/vol ratio of Mexican assets.

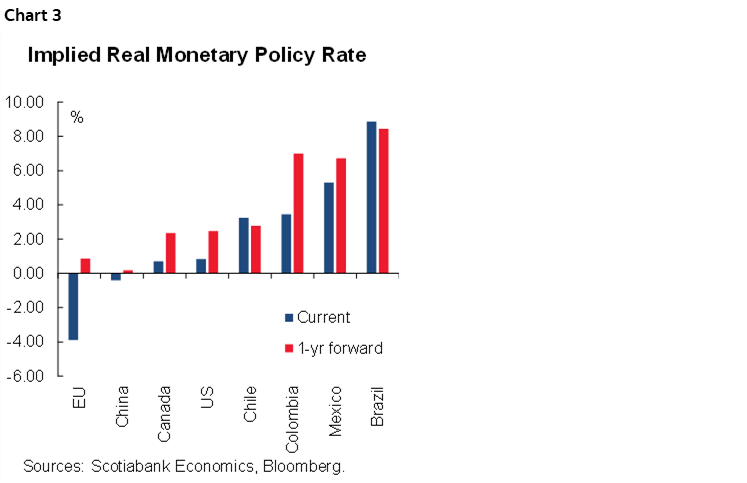

2. Not only is Mexico’s current policy rate among the highest real rates in the world but implied 1-year ahead rates paint a similar story (chart 3). This not only means that from a carry trade perspective Mexico is an attractive market, but it could also be debated that Mexico may have more room for rate compression than other large EMs where more aggressive easing cycles have already been discounted. We stress “may”, as we believe that the prudent course for Banxico will be to remain cautious on its spread over US policy rates, where we think the prudent boundary lies north of 500bps. However, even there, we believe Mexico’s implied spreads over the US still have a larger cushion than elsewhere in the region, and the rest of EM.

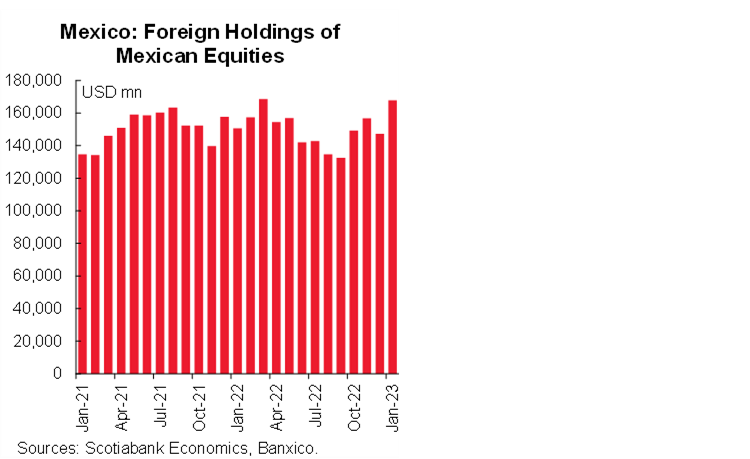

3. The third technical factor which is currently supportive for both Mexican government securities, but also the Bolsa (the Mexican Stock Exchange, chart 4) is convexity. With the relatively rapid increase in global discount rates we’ve seen in the last couple of years, we believe that a lot of the largest global investors were caught with relatively large shares of illiquid assets whose valuations are no longer sustainable at current discount rates. One way of gauging that the mark-to-market adjustment may not have played out yet is that we 1) continue to see declines in real estate prices in major markets, and 2) we continue to see reports of large redemptions in large private equity / real estate funds. One way to reduce the convexity of a portfolio, is to buy low convexity / duration assets, and both m-bonos (with large coupons) and the Bolsa (with a short PE ratio) offer relatively low convexity.

We think these factors will continue to be important supports for Mexican fixed income, FX and equity markets in the coming few months.

Peru—Social Unrest Impacted the Economy More Than Expected

Mario Guerrero, Deputy Head Economist

+51.1.211.6000 Ext. 16557 (Peru)

mario.guerrero@scotiabank.com.pe

The social protests exacerbated by the blockade of roads, damage to public and private property, and partial interruptions in the supply chain showed its impact for the first time in December 2022, with GDP growth of only 0.9% y/y according to official data—the lowest monthly data since February 2021 (chart 1)—well below the rate of close to 2% per month that the economy had been growing by before the political noise, below what was expected by the market consensus (1.2%) and by us (1.3%). Had it not been for the contribution of mining (+1ppt), boosted by the Quellaveco mine project, GDP for December would have been negative. Sectors linked to domestic demand showed a significant slowdown, mainly industrial output, as categories such as agricultural exports, and the dairy and beverage industries were impacted by social protests.

Peru’s economic performance was already weak. GDP fell in October and November, and in December it accumulated its third month of m/m declines, in seasonally adjusted terms, amid tighter monetary conditions, higher inflation, political uncertainty, and a reversal of stimulus implemented during the pandemic. The official 2.7% GDP print for 2022 was below the 2.9% expected by the BCRP (from the 3.0% expected in September) but was in line with our forecast of 2.6%.

The negative shock of unrest continued in January, as the finance minister recently warned. It is possible that the impact in January was greater than that of December, since it was the most critical month when social protests in the southern region became radicalized and the road blockades spread to other parts of the country, so it is likely that growth was zero to start the year. The labour market also reflected this economic shock. The unemployment rate jumped to 8.0% in January, well above what was expected by the market consensus (7.3%) and by our own forecast (7.6%). The BCRP pointed out that the social protests have affected close to 32% of GDP to some degree, making its concern about these macroeconomic effects explicit in its most recent statement. This new economic hit would have been key to the bank’s decision to pause the tightening cycle in February (keeping it at 7.75%). Although the social protests continue, it is evident that they have become less intense. The finance minister pointed out that he expects an economic recovery for February as he considers that the worst of the protests is over, noting that the number of blocked roads is declining. However, the government has extended the state of emergency in various regions for an additional 60 days.

On the political front, Congress extended the legislative session for one more week—until today, Friday the 17th—which preserves the possibility of reaching an agreement regarding earlier elections. So far, there has been no consensus. The outcome is uncertain. President Boluarte has been in favour of Congress approving the early elections. A recent DATUM poll showed that 71% are in favour of Boluarte’s resignation and the renewal of Congress. Boluarte’s disapproval reached 76% in January, according to the poll, while Keiko Fujimori confirmed that she will not be a candidate in the next elections.

If this political solution does not materialize, the intensity of the social protests could rise, with more negative effects for the economy.

So far in February, the prices of perishable food—an indicator sensitive to social protests—have been moderating. However, the rise in prices of poultry products, gasoline, and housing maintenance, would keep the year-on-year inflation rate close to its peak of 8.8%. The BCRP, in its statement, maintained that it expects a visible decline in inflation to begin in March. We share that view, so we believe that the current reference rate level of 7.75% is likely to be the terminal rate. Once inflation starts to ease, there should be no further support for new increases, more so if economic performance is on a downtrend.

The finance minister was also against the bill for a new withdrawal of pension funds, presented last week in Congress. As we know, the precedents in this regard suggest that this bill has a high probability of being approved, despite the opposition of economic authorities.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Click here to be redirected |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.