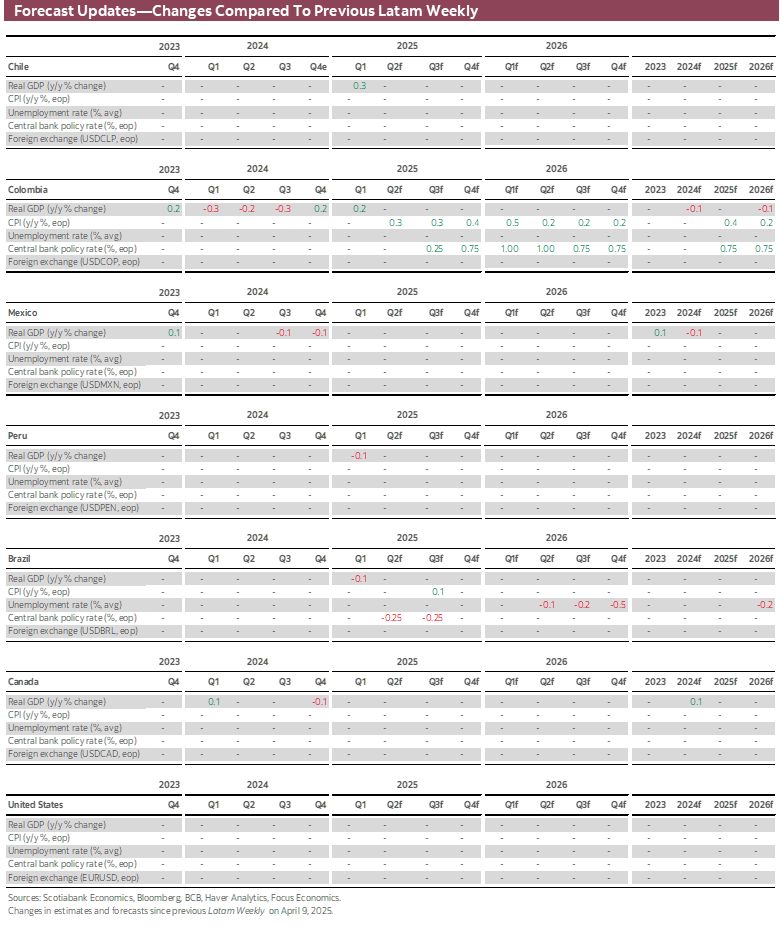

ECONOMIC OVERVIEW

- A relatively quiet Latam week ahead stands in contrast to an eventful week abroad. Chilean and Peruvian CPI releases and Mexico’s Sunday judicial elections are in focus in the region, while global markets eye U.S. and Canadian jobs data, ECB and BoC decisions, and trade news (as always).

- Chilean CPI is expected to only marginally decelerate while Peru’s is seen roughly steady before accelerating over H2. In today’s report, the team in Chile go over their expectations for next week’s CPI and economic activity releases, while our colleagues in Peru highlight the country’s resilience to domestic and external headwinds.

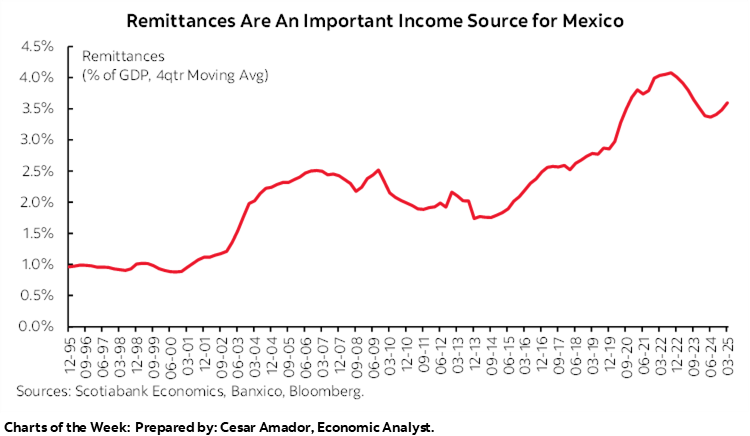

- A low turnout is expected for Sunday’s elections in Mexico, with voters choosing for the first time in history a multitude of judges and magistrates at all levels. Remittances data out on Monday may not show a material hit from U.S. immigration risks.

- Colombia’s calendar is fairly quiet, so in today’s report the team focuses on the status of the Pension Reform that is nearing its scheduled implementation a month away with a handful of obstructions in its way.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Chile, Colombia, Mexico and Peru.

MARKET EVENTS & INDICATORS

- A comprehensive risk calendar with selected highlights for the period May 31–June 13 across the Pacific Alliance countries and Brazil.

Chart of the Week

ECONOMIC OVERVIEW: CHILE AND PERU CPI, MEXICO ELECTIONS, COLOMBIA PENSION REFORM UPDATE

Juan Manuel Herrera, Senior Economist

+52.55.2299.6675

juanmanuel.herrera@scotiabank.com

- A relatively quiet Latam week ahead stands in contrast to an eventful week abroad. Chilean and Peruvian CPI releases and Mexico’s Sunday judicial elections are in focus in the region, while global markets eye U.S. and Canadian jobs data, ECB and BoC decisions, and trade news (as always).

- Chilean CPI is expected to only marginally decelerate while Peru’s is seen roughly steady before accelerating over H2. In today’s report, the team in Chile go over their expectations for next week’s CPI and economic activity releases, while our colleagues in Peru highlight the country’s resilience to domestic and external headwinds.

- A low turnout is expected for Sunday’s elections in Mexico, with voters choosing for the first time in history a multitude of judges and magistrates at all levels. Remittances data out on Monday may not show a material hit from U.S. immigration risks.

- Colombia’s calendar is fairly quiet, so in today’s report the team focuses on the status of the Pension Reform that is nearing its scheduled implementation a month away with a handful of obstructions in its way.

A quiet Latam week ahead stands in contrast to an eventful week abroad. Chile’s calendar includes the region’s headline releases next week, with economic activity and CPI data on tap, to follow Sunday’s release of Peruvian CPI and Mexico’s judicial elections. In contrast, global markets will contend with employment figures from the U.S. and Canada at the close of the week, preceded by U.S. ISM and ADP/JOLTS figures, ECB (25bps cut) and BoC (hold) decisions, and Eurozone CPI. Poland’s runoff presidential vote on Sunday, June 1st also stands as a big risk for Europe on worries that a victory for the nationalist right candidate heightens within the E.U. and NATO.

Just a few hours away from writing, Chinese official PMIs will be monitored for the reaction of local firms to the cooling of U.S.-China tensions. These will also remain in the spotlight next week, as the U.S. claims that China is not holding its end of the bargain, increasing the risk that maybe the U.S. will reconsider the lower 30% tariff rate on Chinese goods. Over the week, we will also monitor the U.S.’s appeal process of a decision that froze their emergency powers tariffs (unfrozen during the appeal), while trade representatives claim that more trade deals are ready to be announced.

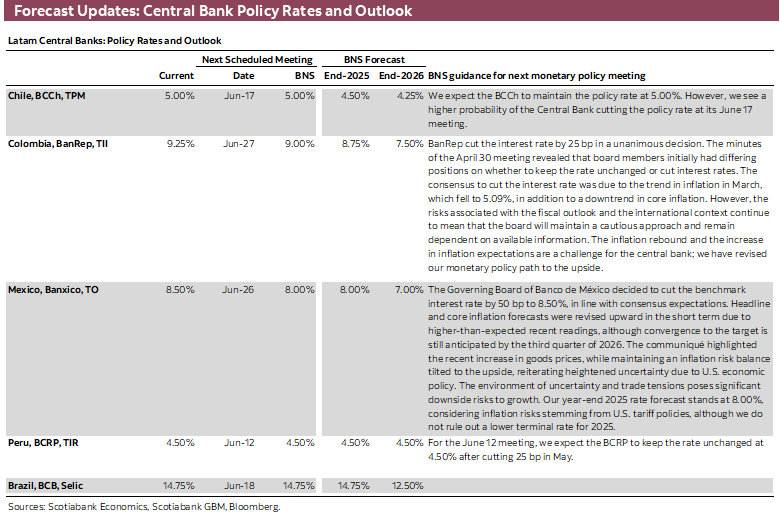

Starting with Chile, our team in Santiago go over their expectations for next week’s data in today’s report. May inflation is estimated to come in at 0.2–0.3% m/m and 4.4–4.5% at its Friday release, with core inflation recording a similar monthly rise but hanging about 1ppt lower at 3.4% y/y. There’s a risk that retailers hiking prices ahead of Cyber Day sales push goods inflation higher. That aside, softening core inflation in line with their projections could increase the odds of a BCCh cut next month. As for economic activity, the timing of Easter this time in April versus in March last year sets up a tough base of comparison for the GDP proxy, but the team projects a respectable 2% y/y expansion that alongside May and June strength should leave 2Q25 growth around the mid-3s in y/y terms.

In Mexico, Sunday’s elections are expected to see a very low turnout for the country’s first ever democratic selection of judges and magistrates in the country. In today’s publication, the local team discusses what’s at stake and expectations and timing of results that are heavily leaning in favour of candidates of the ruling party and independents. On Monday, we will also get remittances data for April, which are expected to remain solid despite U.S. deportation/immigration risks, continuing to provide an important source of income for Mexican households. Investment data, to gauge trade war sentiment, and Citi’s survey of economists results, with a focus on policy and inflation forecasts, on Wednesday and Thursday, respectively, also await.

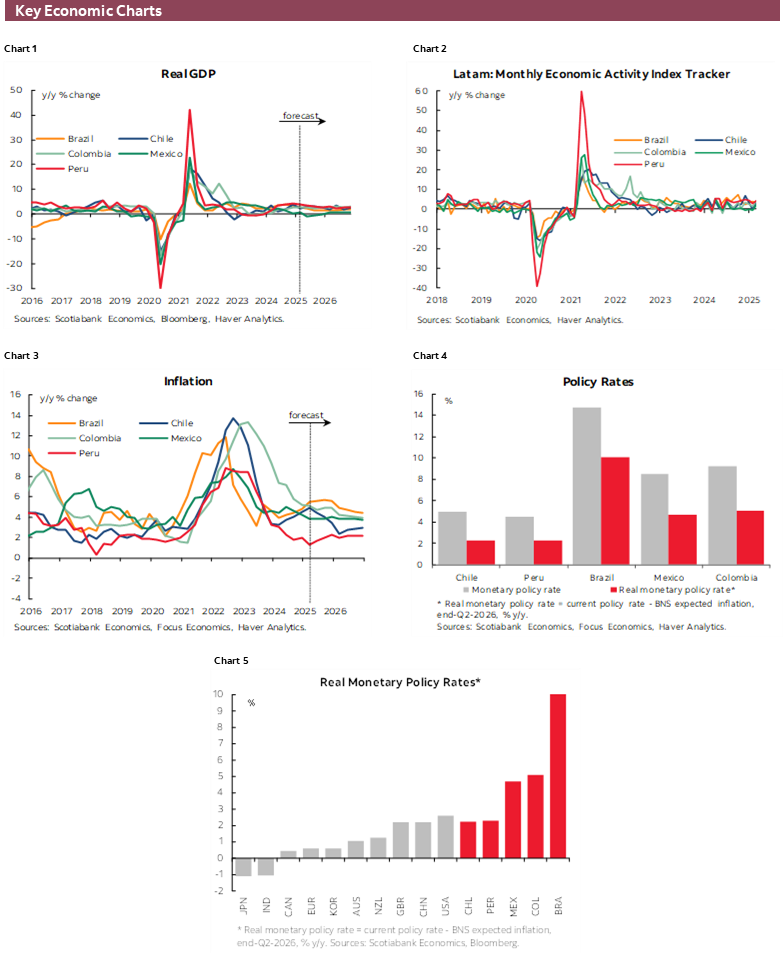

Our team in Lima has a benign view for Peruvian inflation data due over the weekend. Our economists project a 1.6% y/y inflation reading, marking a small deceleration from the 1.7% recorded in April, thanks to a 0.1% m/m drop in prices in May 2025 (alike the decline twelve months prior). Inflation in Peru is generally expected to trend higher over the balance of the year as base effects that had helped inflation reach as low as 1.3% in March are now pulling in the other direction. This is all as expected by economists and the central bank, so it’s no reason to worry. And as the team discuss in today’s note, Peru’s economy seems fairly unbothered by a collection of domestic and political risks. Copper prices, which were/are at risk of global growth weakness and could’ve been a headwind for Peru, are actually doing quite well, while political noise and cabinet shuffles aren’t having a material impact on monitorable data.

Finally, Colombia has a relatively bare releases calendar next week, with only current account readings due on Tuesday worth a look. So, in today’s Weekly the team recaps and looks at the country’s pension reform process which, although very bumpy, has been the only one of president Petro’s social reform pushes that has made it through the legislature and is on track for its implementation. Now, that does remain to be seen, however, as the team in Bogota highlight some of the legal challenges and hiccups that the implementation of the pension reform faces with only about a month to go until it comes into force.

PACIFIC ALLIANCE COUNTRY UPDATES

Chile—May CPI and April Activity Preview, No Electricity Bill Hike (For Now)

Anibal Alarcón, Senior Economist

+56.2.2619.5465 (Chile)

anibal.alarcon@scotiabank.cl

MAY CPI SEEN AT 0.2-0.3% M/M, 4.4-4.5% Y/Y

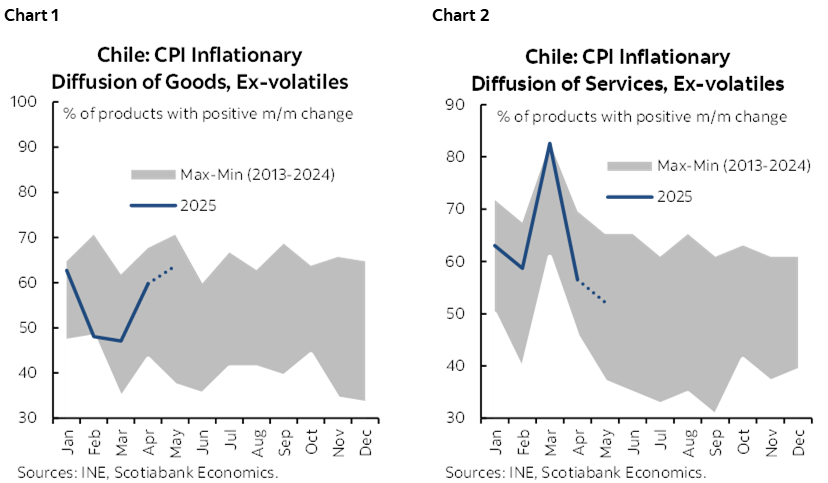

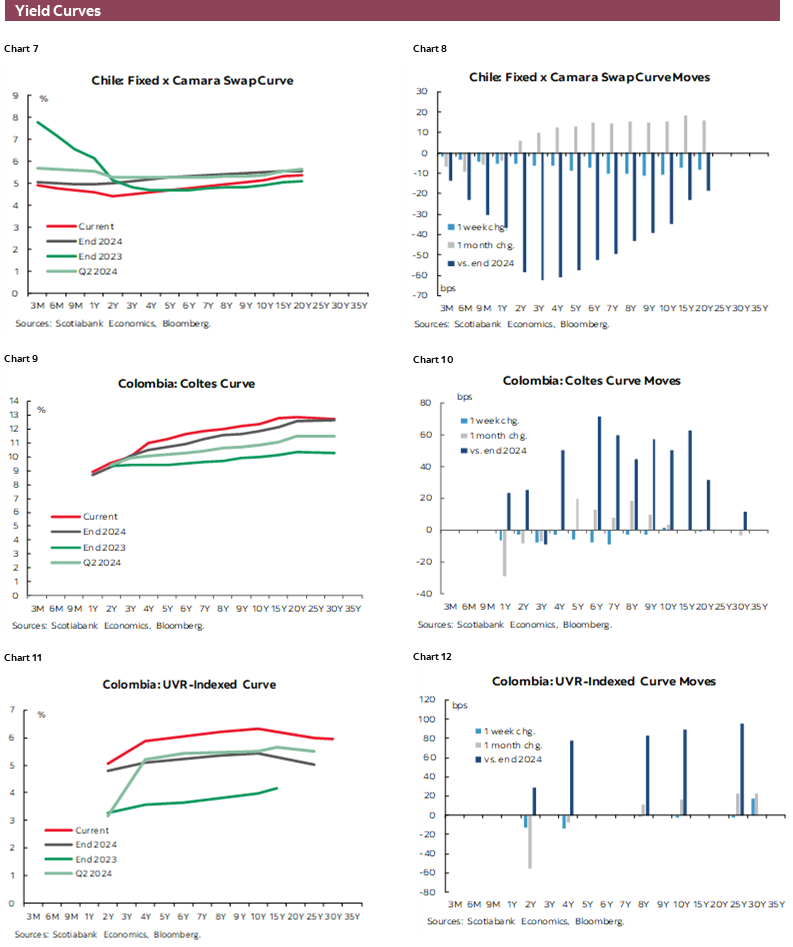

The main positive contributions considered in our projection for a 0.2-0.3% m/m rise in CPI would come from the Food and Housing divisions, while the Transportation division would be the most notable downside. At the core level, we project inflation of around 0.3% m/m (3.4% y/y), with services contributing significantly, although prices for goods are expected to continue to rise, partly due to adjustments to prior prices due to the Cyber Day sales at the beginning of June. Along these lines, we project that the inflationary diffusion of goods would experience an increase compared to that observed in April, while that of services would reach levels closer to their historical average (charts 1 and 2).

If our CPI projection is confirmed, we see a higher probability of the Central Bank cutting the policy rate at its June 18th meeting.

NO NEW ELECTRICITY RATE INCREASES, FOR NOW

Following the publication in the Official Gazette of the Decree readjusting the distribution component of electricity rates, doubts have arisen in the market regarding its potential impact on the next CPI prints. On the one hand, Decree 5T of 2024 set electricity distribution rates for the four years between November 2020 and November 2024, demonstrating a delay of at least two years compared to the original tariff process deadlines. While this would not affect current rates as it is a price setting for a prior period, it could entail additional charges (or discounts) on electricity bills retroactively, a process known as Reliquidation.

While the INE clarified that there is still a lack of information to determine whether or not it is feasible to include this in the CPI calculation, it has been excluded from the CPI calculation for more than 10 years because it affects household income levels and not the rates in effect at the time the service is consumed.

Based on this, at Scotiabank, we are not considering variations in the Electricity CPI for May following the distribution rate adjustment and subsequent recalculation. However, the July CPI could incorporate an increase in the Electricity CPI if the 7% increase announced by the CNE is implemented, which would affect the Transmission component of the electricity rate.

WE ANTICIPATE AN IMACEC OF 2.2% Y/Y FOR APRIL; ACTIVITY COULD ACCELERATE ITS YEAR-ON-YEAR GROWTH RATE IN MAY AND JUNE

As we anticipated several weeks ago, April GDP would grow by over 2% year-on-year, marking a strong start to the second quarter in terms of growth. In terms of speed, non-mining GDP would not show major change, while mining GDP would show clear expansion, recovering part of what was lost last year. While April has a challenging comparison base due to the timing of Easter (April this year, March last year), May and June have more favourable bases, which alone would boost May’s year-on-year growth to figures between 3% and 4% and June’s to values between 4.5% and 5.5%. With this, the second quarter would average a year-on-year growth rate above 3.5%, which continues to support our 2.5% growth projection for the year.

Colombia—Pension Reform One Month Before Implementation

Jackeline Piraján, Head Economist, Colombia

+57.601.745.6300 Ext. 9400 (Colombia)

jackeline.pirajan@scotiabankcolpatria.com

Daniela Silva, Economist

+57.601.745.6300 (Colombia)

daniela1.silva@scotiabankcolpatria.com

The pension reform is the only social reform proposed by the current government that has found its way to be approved in Congress debates. The reform was presented on March 22nd, 2023, aiming to change the current pension scheme, which is composed of two competing sub-systems: the public (pay-as-you-go/defined benefit) and the private (defined contribution scheme) to a pillar scheme of four groups (see below), pursuing universal coverage—while limiting pension subsidies to wealthy people—increasing the scope of the public sector in the management of the pension savings fund and changing the framework for the private actors.

On June 14th, 2023, the reform was approved in the first debate in the Senate Commission VII, where some propositions were approved, such as reducing the number of weeks of contribution to access a pension in the contributory pillar and to whom the transition regime would apply, which means that more people would not be affected by the reform. During the second half of 2023, the project did not make any progress because the government had its eyes set on health reform which eventually failed to be approved.

At the beginning of 2024, opposition parties tried to delay the pension reform discussion, breaking the quorum in the initial sessions. However, the government reached some consensus with the Liberal Party, which helped the project pass the second debate. In the second debate, important agreements were reached, such as reducing the contribution threshold of the contributory pillar from the original proposal of 3.0x to 2.3x minimum wages and ensuring that this fund will be managed by BanRep and not by Colpensiones as originally proposed.

During May and June 2024, the House of Representatives debated on the pension reforms, and despite the seventh commission of the House making some changes, the House Plenary decided to skip the debate on those changes and just approved the same text that was approved by the Senate.

President Petro signed the reform on July 16th, 2024 and the reform is expected to be implemented by July 1st, 2025. However, almost one year after approval, the reform is still pending, awaiting the Constructional Court’s decision on multiple demands that involve procedural defects, as well as a request claiming its unconstitutionality, which could result in the total withdrawal of the reform. In parallel, the regulatory framework has been partially released with little time until the implementation deadline, which is also increasing the uncertainty about how feasible it is to make the transition to the new pension scheme.

While uncertainty is high, we don’t expect the reform to fall completely; in the same way, we see the chance of having a delay in its implementation, resorting to the option of implementing the reform six months after the initial deadline, in January 2026. It is worth noting that short-term uncertainties for capital markets have been contained as the central bank has said the sovereign fund that now will collect ~80% of pension fresh contributions will be managed by professional managers, significantly reducing a potential negative impact.

REFRESHING ONE’S MEMORY. WHAT ARE THE CHANGES THAT THE PENSION REFORM PROMOTES?

The reform changes the current pension scheme, which is composed of two competing sub-systems: the public (pay-as-you-go/defined benefit) and the private (defined contribution scheme) to a pillar scheme of four groups.

- The first group, the solidarity pillar, guarantees a subsidy for those older adults who are in a situation of vulnerability.

- The second is the semi-contributory pillar, which provides a life annuity for those who contributed but did not meet the minimum number of weeks required for a pension.

- The third is the contributory pillar, in which there is a mandatory contribution from all the formal employees in Colombia. The idea is to create a fund that guarantees a high replacement rate; however, limits the benefit up to 2.3 minimum wages (which is currently around USD 770), that means that contribution to this pillar can be over a minimum salary and limited up to 2.3 minimum salaries.

- The fourth pillar is individual savings, which will be managed by existing private pension funds with contributions above the threshold of 2.3 minimum wage threshold.

WHAT IS THE CONTROVERSY AROUND THE PENSION REFORM, AND WHEN MAY COURTS DELIVER A DECISION?

Many political actors consider the pension reform to be a national agreement; however, during its course in Congress, some controversial approaches have now been brought to the attention of the Constitutional Court. The main one is that a few hours before the end of the legislature period in 2024, the Lower House Plenary decided to approve the text approved in the Senate Plenary in the second debate, skipping the changes proposed in the third debate of the seventh commission of the Lower House. Having said that, there are various potential scenarios; the most radical plaintiffs call for the total withdrawal of the reform, while the more moderate part is aiming to resume the debate of the reform.

During the Asofondos Congress in April 2025, some former Constitutional Court members expressed that debate is far from being easy, as the court should analyze all the scenarios that led to the reform being approved in that way. That involves considering that the constant blockage of opposition parties (minorities) to start the debate in 2024 impeded the possibility of Congress majorities to decide with sufficient time. Additionally, the court should also consider various technical and special factors before deciding, such as the fact that some parts of the population have already decided to modify their pension plans in anticipation of the change in pension legislation.

All in all, we have only one month to kick off the implementation of the reform, and despite the courts debating current demands, there is no specific hard deadline for a decision.

WHAT ABOUT THE REGULATORY FRAMEWORK?

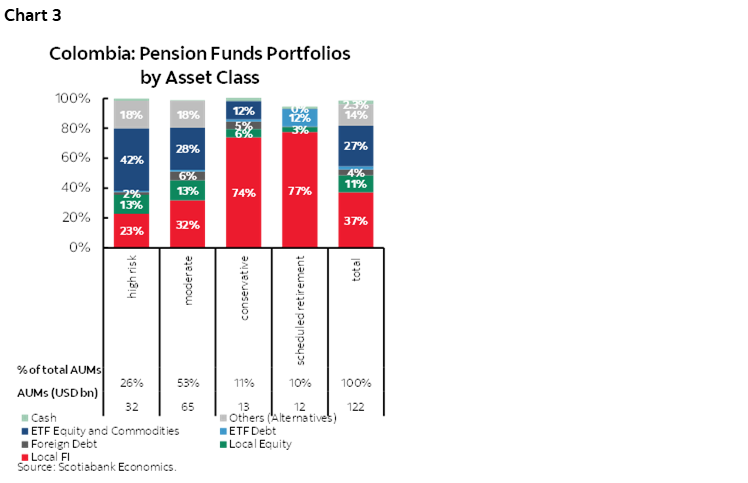

Up to April, the URF (Unidad de Proyección Normativa y Estudios de Regulación Financiera) published 56% of the required regulation. However, by this time, BanRep’s Governor, Leonardo Villar, considered that there were many blanks to be filled, which would impede a smooth transition. Among the central bank’s main concerns were fee schemes, the definition of the decumulation period, and management issues such as the accounting and auditing of the new sovereign fund. Additionally, private actors, the ACAI group (Administradoras del Componente Complementario de Ahorro Individual), former AFPs (pension fund administrators), plus a new company (Positiva Seguros) were expecting the regulation of its investment framework that implied transitioning from the multifunds scheme (Conservative, Moderate, High Risk and Retirement funds, chart 3) to a target date funds scheme, that involves that each entity will have 10 funds in which the investment profile will depend on the proximity of retirement age of its affiliates.

That said, on Thursday, May 22nd, we had the public release of the complementary framework (which remains open to public comments until June 5th), establishing the investment regime for the new managers, ACAI, and the decumulation period. With this release, the government considers that 80% of the regulation is in place. The huge deal that means having ready technological systems and, in general, making the transition to the structure proposed for the government leads us to think that the implementation of the reform will be delayed.

Mexico—June 1st Election Preview

Rodolfo Mitchell, Director of Economic and Sectoral Analysis

+52.55.3977.4556 (Mexico)

mitchell.cervera@scotiabank.com.mx

Brian Pérez, Quant Analyst

+52.55.5123.1221 (Mexico)

bperezgu@scotiabank.com.mx

Miguel Saldaña, Economist

+52.55.5123.1718 (Mexico)

msaldanab@scotiabank.com.mx

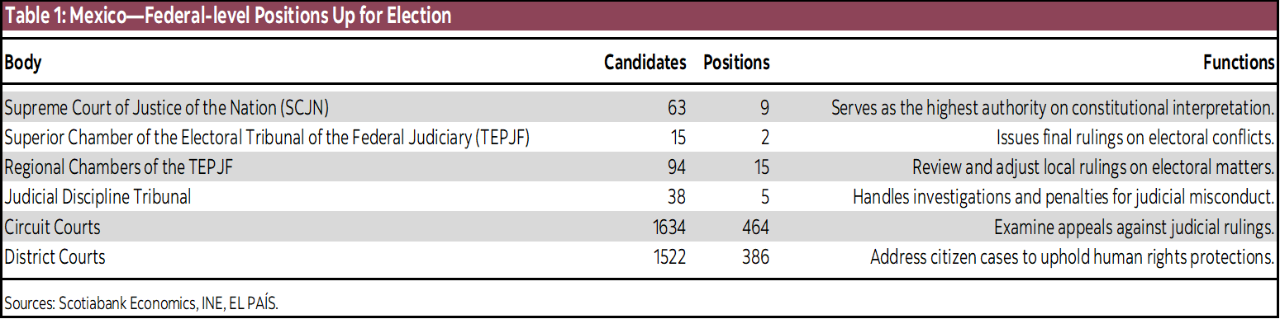

On June 1st, for the first time in history, the election of judges and magistrates will be carried out through citizen voting. This means 881 judicial positions will be renewed as part of the Federal Judiciary (table 1):

- 9 justices of the Supreme Court of Justice of the Nation (SCJN)

- 2 magistrates of the Superior Chamber of the Electoral Tribunal of the Federal Judiciary (TEPJF)

- 15 magistrates of the Regional Chambers of the TEPJF

- 5 magistrates of the Judicial Disciplinary Tribunal

- 464 Circuit magistrates

- 386 District judges

Additionally, 19 states will also hold local judicial elections, with nearly 1,800 local positions to be filled in the following states: Aguascalientes, Baja California, Mexico City, Chihuahua, Coahuila, Colima, Durango, State of Mexico, Michoacán, Nayarit, Quintana Roo, San Luis Potosí, Sonora, Tabasco, Tamaulipas, Tlaxcala, Veracruz, Yucatán, and Zacatecas.

According to the Wilson Center, before the constitutional reform of the Judiciary on September 15, 2024, the process for selecting judges in Mexico’s judicial system consisted of three stages: a general legal knowledge exam, the drafting of a proposed ruling, and an oral exam before a panel of senior judges. The structure of the Judiciary promoted professional progression through civil service positions, starting as auxiliary officers, then as court clerks, agreement secretaries, and finally qualifying for a judge position. This progression was based on gaining significant experience and meeting specific requirements, allowing candidates to apply for a judgeship through a selection process organized by the Federal Judiciary Council (CJF), the governing body of the Judiciary.

Despite this, the system was far from perfect. The Judiciary faced persistent criticism, including the sale of exam answers and widespread nepotism.

The judicial reform in Mexico has radically transformed the judge selection process. One of the main changes is that a career in public service is no longer required, as judges will now be elected through a semi-democratic vote. The three branches of government—Executive, Legislative, and Judicial—will select candidates from among all applicants.

Requirements to Become a Candidate: Mexican nationality by birth and full enjoyment of civil and political rights, a law degree obtained at least 10 years prior. Candidates must also have a good reputation and must not have been convicted of an intentional crime. While professional experience in the legal field is not mandatory, it is considered valuable. Additionally, candidates must submit official documents such as: birth certificate, professional license, résumé, a supporting essay (on their vision of the Judiciary), and letters of recommendation. Finally, candidates must demonstrate that they have not held leadership positions in political parties or been candidates for elected office in recent years.

The New Selection Process consists of a public call and registration of applicants, during which candidates must submit documentation. Evaluation Committees from each branch of government (Executive, Legislative, and Judicial) review the applications, assess the most qualified candidates, and conduct a public lottery to reduce the number of applicants according to the available positions. The lottery results are published, and the final lists are sent to the Executive, Legislative, and Judicial branches for approval. It is worth noting that the members of the Judicial Branch’s Evaluation Committee resigned during the process, so the TEPJF ordered the Senate to conduct a lottery to select the candidates who will appear on the ballots.

Each branch reviewed and validated the candidacies within its jurisdiction and sent the final lists to the National Electoral Institute (INE). The INE manages all election-related activities, from preparing ballots and materials to promoting citizen participation and regulating campaigns.

Candidates:

A study by Viri Ríos found that among the 117 applicants to the three superior courts, 36% are aligned with the ruling party, 9% with the opposition, and 55% are independent candidates. It is also worth noting that 58% had previously served as judges or worked as legal clerks in one of the superior courts.

On the other hand, due to the delimitation of federal-level candidacies, according to the specialized consultancy Integralia, at least 51 positions will be decided by uncontested candidacies due to:

1. the total number of registered candidates equaling the number of positions available,

2. gender parity provisions limiting the number of competitors, and

3. the geographic delimitation of candidacies.

Citizen Participation:

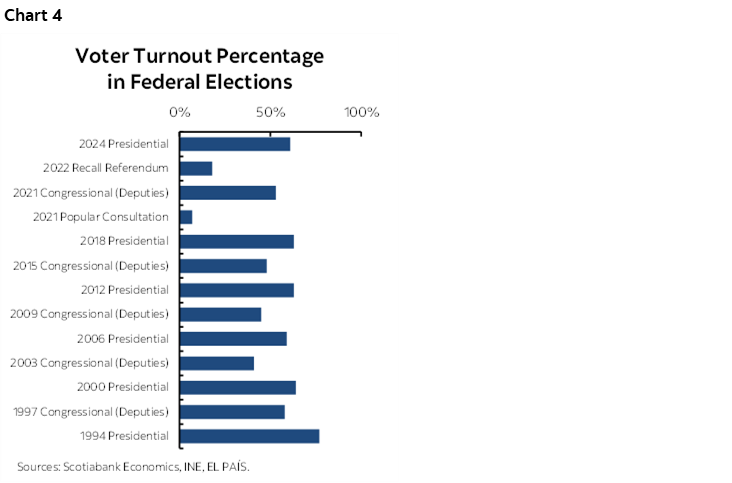

Despite the dissemination of the judicial election through various media outlets and social networks, the president of the National Electoral Institute (INE) announced that the electoral body estimates a voter turnout of between 18% and 20% of the electoral roll.

Despite the authorities’ efforts to promote the election, various polls point to low voter participation (chart 4). According to surveys conducted by Enkoll and Mitofsky, only 34.1% of respondents consider it “very likely” that they will participate in the election. Historically, voter turnout in general presidential elections averages over 60%, but this figure drops to around 45–50% in midterm congressional elections. The two electoral exercises of the previous administration—the public consultation on the airport cancellation and the recall referendum—had participation rates of just 17.8% and 7.1%, respectively.

Budget:

According to Integralia, the total budget approved by Congress for the election was just 4.35 billion pesos, compared to the 8.802 billion pesos approved for the 2024 federal election—less than half the amount allocated for the previous year’s presidential election. This budget constraint will be directly felt at the polling stations, with only 84,000 stations planned, compared to the 170,182 used in previous elections. Additionally, there will be 775,762 polling station officials, compared to 1,531,629 in the previous exercise—again, nearly half the number used in the presidential election.

Results:

The National Electoral Institute (INE) will be responsible for vote counting, tallying, assigning positions based on results, and issuing certificates of majority to the elected federal candidates. Typically, polling stations are staffed by volunteer citizens who conduct the vote count and report results on election day. Based on these, the INE performs quick counts for each election. However, this time, citizen officials will only operate the polling stations, while the counting and presentation of results will be handled by the electoral institute.

On the night of June 1st, the INE is expected to publish an estimate of voter turnout and report on the progress of vote counting for the Supreme Court election. As for results, the deadline for announcing the winners of the 9 Supreme Court justice positions is Tuesday, June 3rd. The elected magistrates of the Disciplinary Tribunal will be announced on Wednesday, June 4th, followed by the winners of the Superior Chamber of the TEPJF on Thursday. By Friday, June 6th, results for the Regional Chambers of the TEPJF should be available. Between Sunday, June 8th, and Tuesday, June 10th, the remaining winners are expected to be announced, with certificates of majority issued by June 15th and the swearing-in of winners scheduled for September 1st.

Upcoming Economic Releases

Next week, several important economic figures will be released. On Monday, Banxico will publish remittances data for April, as well as the analysts’ expectations survey. On Wednesday, we will learn the gross fixed investment figure for March, which has now shown six consecutive months of annual contractions, with February’s figure at -7.8% year-over-year—the lowest since January 2021.

On Thursday, we will see the consumer confidence index for May, which has been significantly slowing down since October of last year. That same day, Citi will also release its expectations survey. Finally, by Friday at the latest, the formal job creation data for May will be published. In April, the economy saw a loss of 47,000 formal jobs.

Peru—Economy Moves On Undaunted by Risks

Guillermo Arbe, Head Economist, Peru

+51.1.211.6052 (Peru)

guillermo.arbe@scotiabank.com.pe

There is so much noise and volatility on both the global economic front and the domestic political front, and yet nothing seems to be impacting actual economic data. Peru faces two sources of risk over the remainder of 2025 and into 2026. One has to do with uncertainty surrounding global events, from swings in tariff policies, to geopolitical tensions. The other has to do with the uncertainty surrounding the 2026 presidential and congressional elections.

Even though the risks are real, neither source of uncertainty is affecting Peru’s economy at this point in time. The main channel through which global economic risks impact Peru is metal prices, especially copper. We are monitoring metal prices closely, but so far, if anything, global events are providing support to high gold and copper prices. As long as these prices, especially copper, remain robust, Peru’s economy should remain resilient to external events.

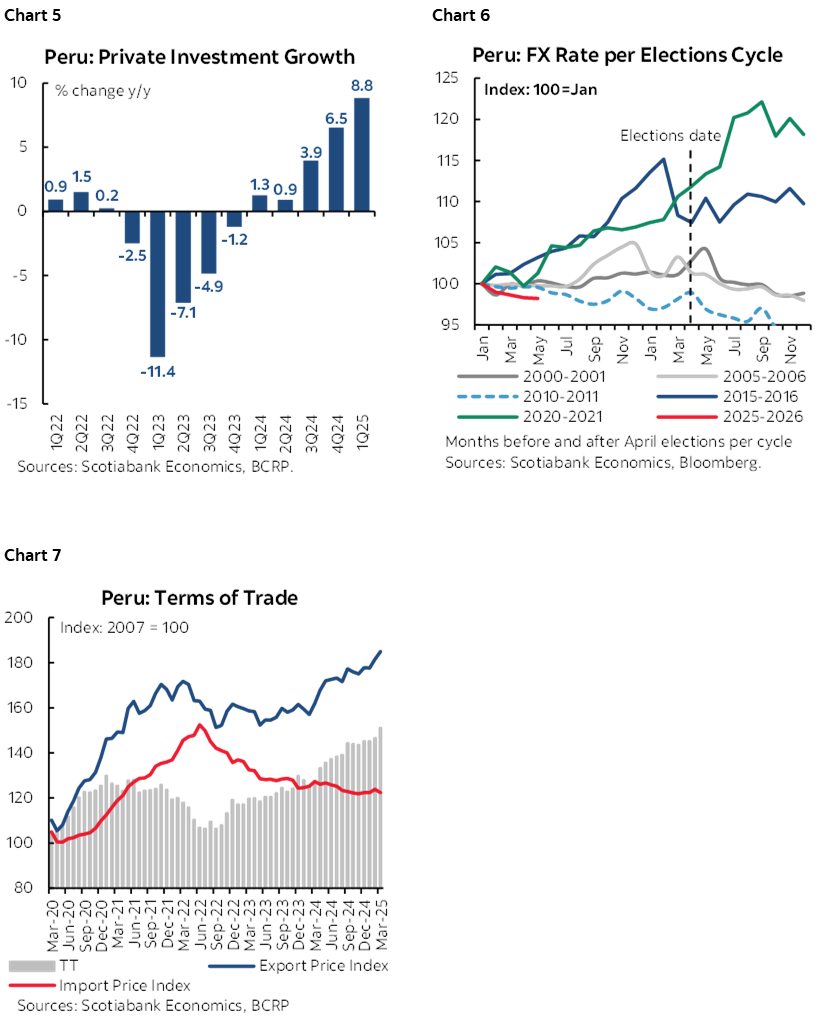

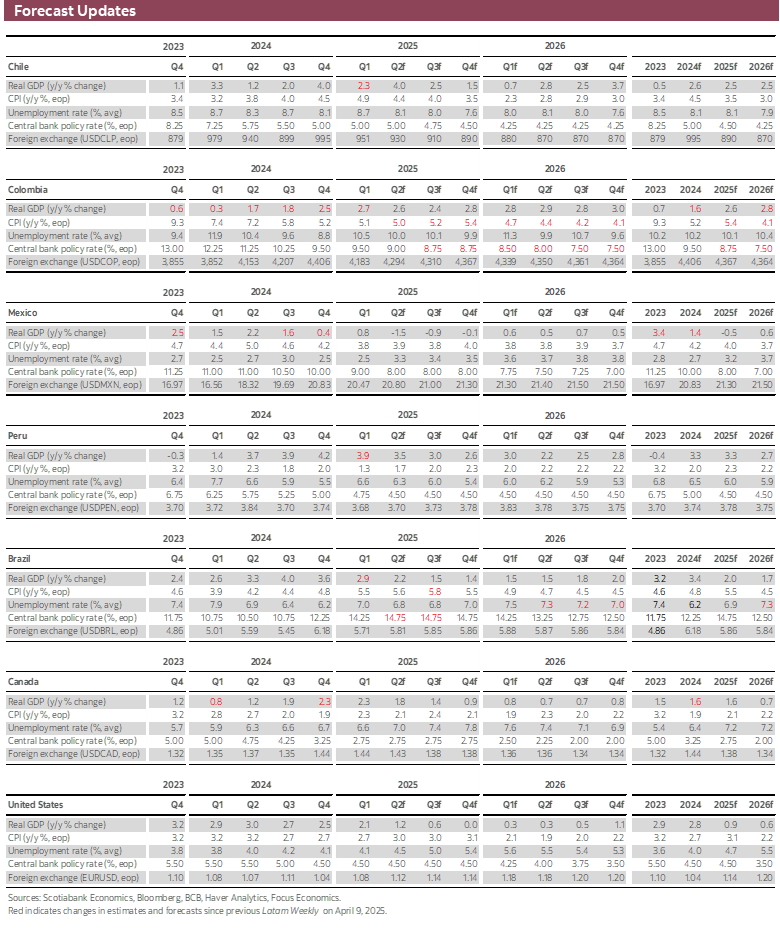

The way political events normally affect the economy is through private investment. Frequently, this impact is preceded by declining business confidence levels, and a rising FX rate. At this point in time, with just over ten months before the April 12th, 2026, elections, none of this is occurring. Private investment during Q1 2025, the latest data available, rose 8.8%, surpassing our expectations of 7.7% (chart 5), business confidence levels continue to improve mildly, and the PEN FX rate continues showing strength (chart 6). This may change as we get closer to the elections. However, note that both business confidence and the PEN have historically shown a degree of correlation with the price of copper (granted, the correlation has weakened since the 2020 Covid pandemic). In a sense, to the extent that global uncertainty is upholding gold and copper prices, it is also helping to override, or at least delay, the impact of political uncertainty (chart 7).

There is one aspect of potential concern regarding private investment and business confidence, however. The removal of José Salardi as Minister of Finance, and his replacement by Raúl Pérez Reyes. Former Minister Salardi had given tremendous momentum to State tendering of infrastructure projects. He had also been working very closely with the business community to resolve obstacles to investment, thereby generating a tremendous amount of good-will. The improvement in business confidence and outperformance of private investment has been largely linked to this environment, in our view. The new Minister Pérez-Reyes has a more political, and congress-appeasing view of things, and is little likely to follow in Salardi’s footsteps in cultivating relations with the private sector.

The bottom line for Peru is this. The country faces two risks, one external, one political. Neither risk has shown any material impact on data released so far. If these risks start to materialize, the most likely first sign shall be falling copper prices on the one hand, and declining business confidence levels and a weakening PEN on the other. Given the lag in the impact of global events on Peru domestic growth, and given precedents in terms of the elections cycle, the impact of either event is likely to be greater in 2026 than in 2025. What will be key in 2026 in terms of external events is where metal prices will be. What will be key in terms of political events is the evolution of voter intention polls before the elections, and who the next Minister of Finance and the next President of the BCRP board will be after the elections.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Click here to be redirected |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.