ECONOMIC OVERVIEW

- More tariff threats are sending us into the weekend ahead of what should have been a relatively calm week—with the U.S. and the U.K. out for holidays on Monday. The Fed’s meeting minutes, CPI readings out of the Europe, and Canadian GDP are the G10 highlights.

- In Latam, the minutes to Banxico’s dovish June decision and updated forecasts in its quarterly report are in focus, as discussed by our Mexico economists, accompanied by a trove of Chilean macro readings on Friday for April that are the data highlight.

- Quiet Colombian and Peruvian calendars notwithstanding, the local teams discuss in today’s report disappointing investment results in the former and bumpy economic developments for the latter.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Colombia, Mexico and Peru.

MARKET EVENTS & INDICATORS

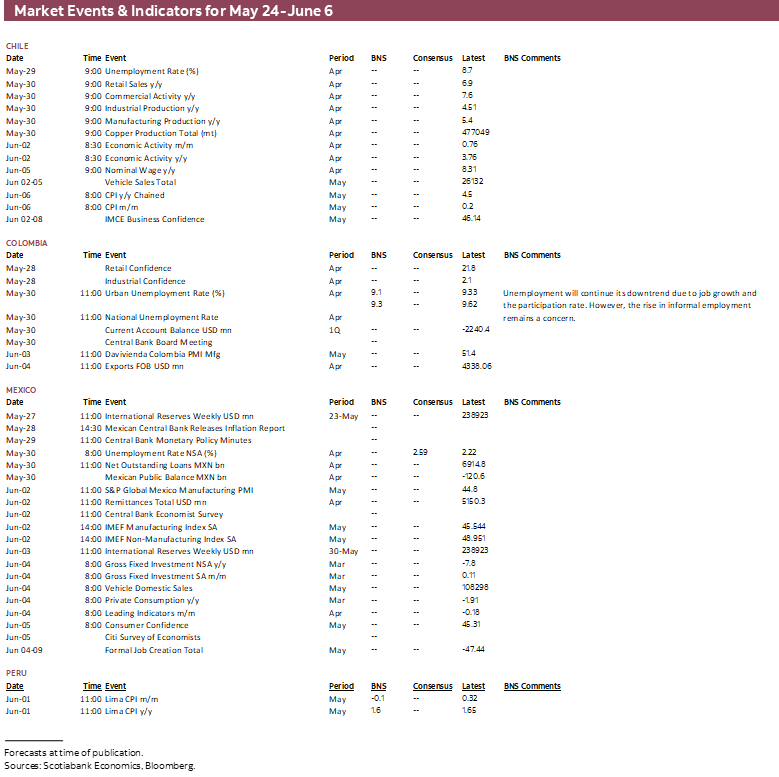

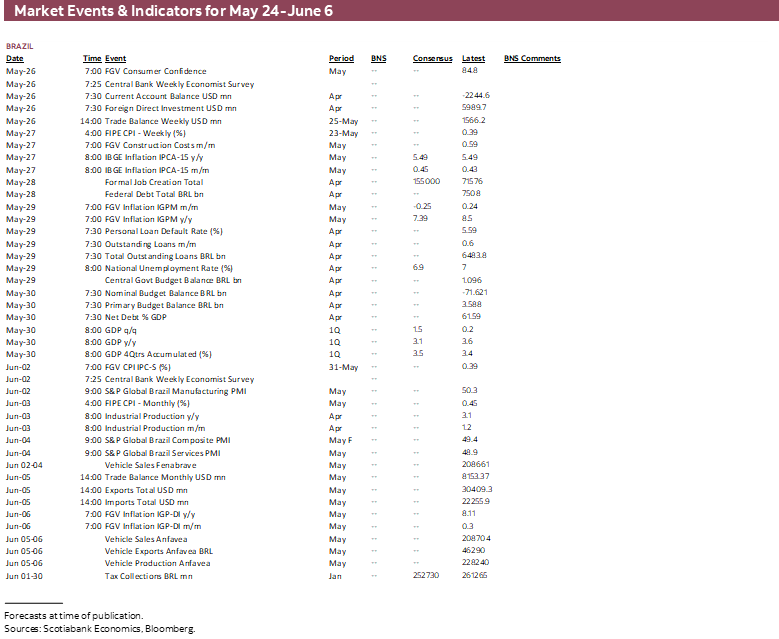

- A comprehensive risk calendar with selected highlights for the period May 24–June 6 across the Pacific Alliance countries and Brazil.

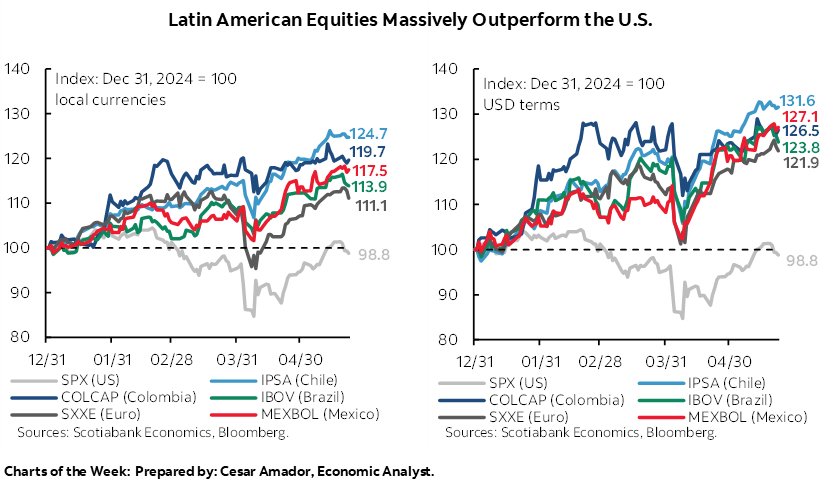

Chart of the Week

ECONOMIC OVERVIEW: BANXICO MINUTES AND FORECASTS, CHILE MACRO FLOOD...MAYBE TARIFFS?

Juan Manuel Herrera, Senior Economist

+52.55.2299.6675

juanmanuel.herrera@scotiabank.com

- More tariff threats are sending us into the weekend ahead of what should have been a relatively calm week—with the U.S. and the U.K. out for holidays on Monday. The Fed’s meeting minutes, CPI readings out of the Europe, and Canadian GDP are the G10 highlights.

- In Latam, the minutes to Banxico’s dovish June decision and updated forecasts in its quarterly report are in focus, as discussed by our Mexico economists, accompanied by a trove of Chilean macro readings on Friday for April that are the data highlight.

- Quiet Colombian and Peruvian calendars notwithstanding, the local teams discuss in today’s report disappointing investment results in the former and bumpy economic developments for the latter.

It could really have been a quiet week next week, with the U.S. and the U.K. closed for holidays on Monday and a relatively light global calendar. We’re at the whim of off-the-cuff comments and social media posts, however. Trump’s threats of 50% tariffs on the E.U. and 25% duties on Apple and Samsung unless they build smartphones in the U.S. have injected a key source of headline risk for trading, and markets are unlikely to trade quietly into next weekend as month-end flows and the possible imposition of additional tariffs on June 1st shake Friday trading. OPEC+ rumours ahead of their meeting that same day will also hang over markets.

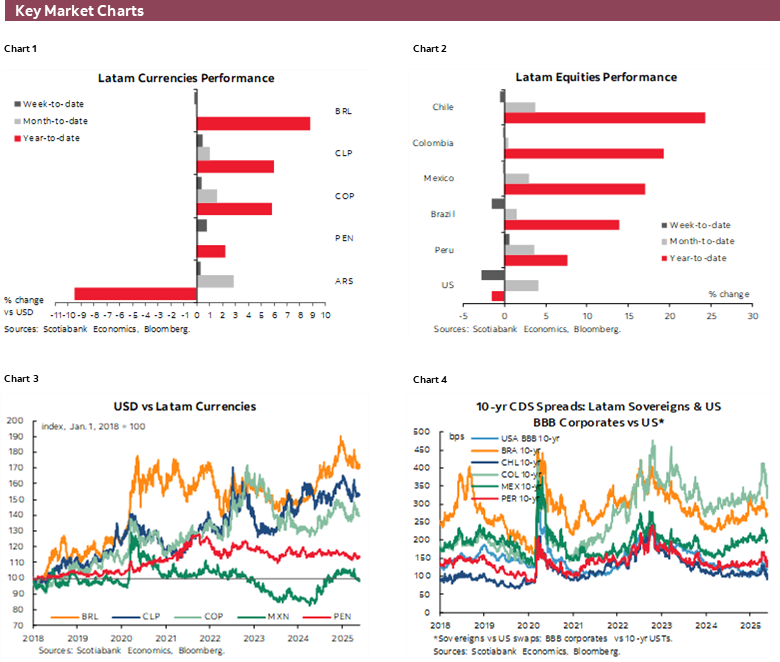

In Latin America, where local assets have more than held up this year, with strong gains in domestic equities and resilience in currencies and sovereign debt (Colombia excluded), the week ahead focus will be on Banxico’s quarterly report and meeting minutes in Mexico, a flood of April macro readings out of Chile, and mid-month CPI and Q1 GDP figures out of Brazil.

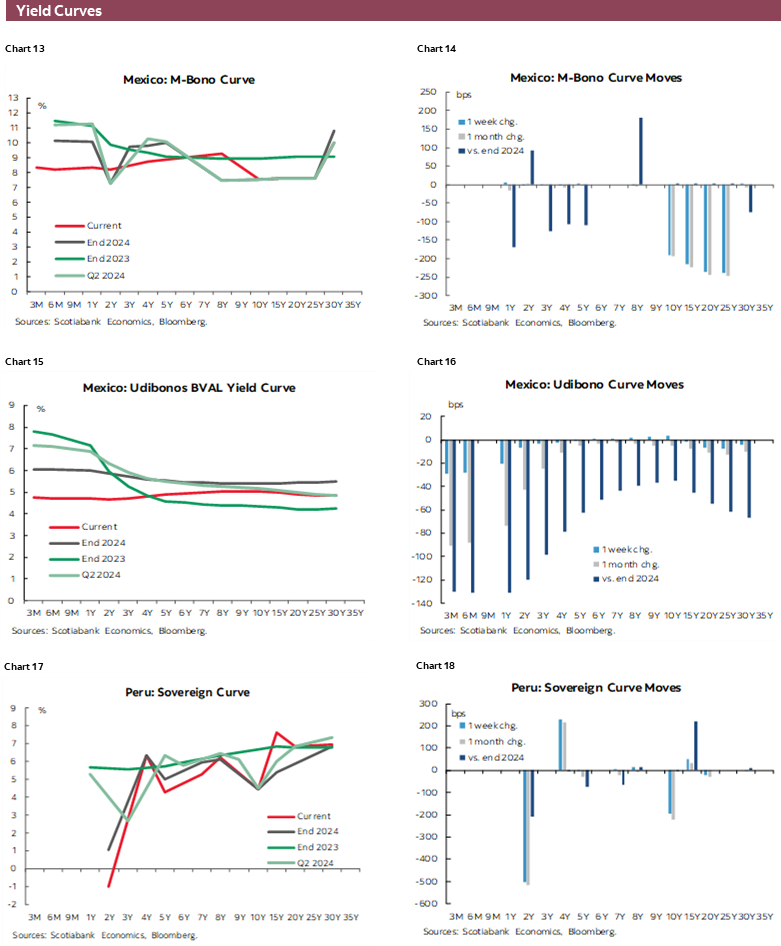

As our team discusses in today’s report, we’ll monitor possible changes to Banxico’s macroeconomic projections and the message of all five Banxico officials in the minutes to their May meeting when a relatively dovish rate cut was announced.

A lot has changed since the bank last updated its forecasts in February. From a domestic standpoint, economic data for the first third of the year have generally surprised to the upside, both in growth terms and inflation terms. Yet, growth data may be somewhat misleading, which brings us to the biggest shock to Banxico’s projections. Trump’s on and off tariffs on Mexico and the world are due to depress domestic growth, notwithstanding a temporary boost to exports that has overstated the strength of Mexico’s economy this year.

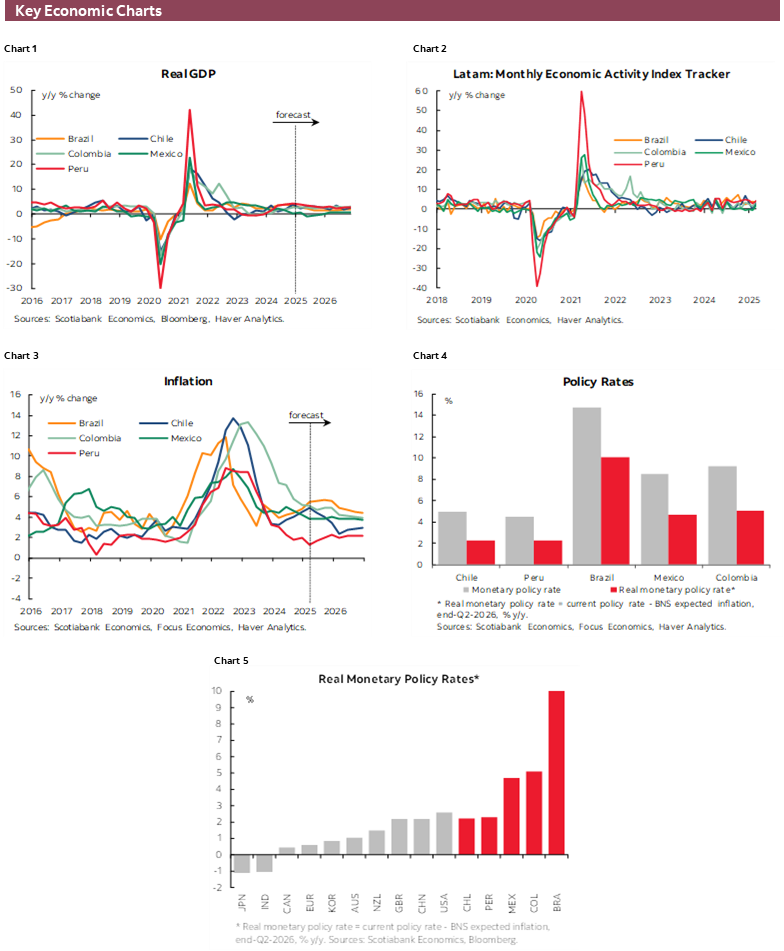

Chilean data out on Friday will offer a good look into how seasonal factors related to the timing of Easter may have overstated economic strength at the end of the first quarter. Massive gains of 6.9% and 5.4% y/y in retail sales and manufacturing production, respectively, in March were helped by a lower base of comparison, which will now hit in the other direction in April. That aside, Chile’s economy looks in good shape, but it may be that large data misses next week prompt markets and economists start to weigh more heavily an earlier restart of BCCh rate cuts, particularly after a nice downside surprise in April inflation.

Despite strong Q1 growth expected in Brazil (1.5% q/q) and headline inflation expected to stick around the mid-5s next week, the BCB seems to suggest it has hiked enough with trends turning more constructive over the second half of the year. So, it could be a few more months of data before we think about when the BCB will take its first step in the other direction; markets are mulling the possibility of a cut in Q4-25.

Colombia’s and Peru’s calendars have relatively little on offer over the next few days—though Colombian balance of payments data out on Friday may be worth a look. That does not mean there is nothing to update from these countries. In today’s Weekly, the team in Colombia discuss the damage that depressed confidence (be it from domestic or external factors) have had on investment trends in the country—which materially lag its regional peers. In Peru, we discuss the bumpiness in economic data in the year-to-date, as certain calendar and one-off factors may complicate the interpretation of monthly data. Volatility notwithstanding, Peru’s economy remains solid, but watch out for risks.

Abroad, excluding geopolitical and tariff dangers, the release of CPI figures from key Eurozone countries for May, and U.S. PCE data and the Fed’s minutes are the highlights. U.S. durable goods orders, U Mich revisions, and the Conference Board survey will also be worth a look, as will Canadian GDP, Australian and Tokyo CPI, and rate decisions in New Zealand and Korea (25bps cuts from both). On the equities front, Nvidia’s results due on the 28th are in focus (in a context of a ~40% rise in its share price since the April lows).

PACIFIC ALLIANCE COUNTRY UPDATES

Colombia—Shock to Economic Confidence Has a Negative Impact on Investment Results

Valentina Guio, Senior Economist

+57.601.745.6300 Ext. 9166 (Colombia)

daniela.guio@scotiabank.com

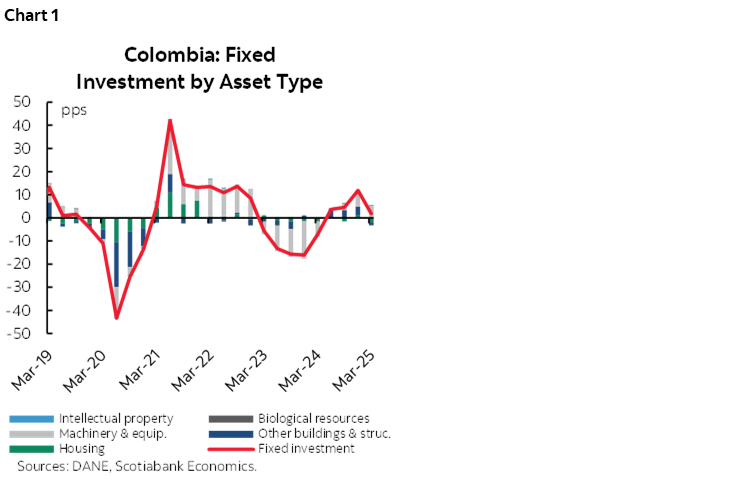

Economic growth in 1Q-2025 showed a mixed picture. According to our latest Colombian GDP report, private consumption accelerated, but fixed investment remained lagging. Indeed, total gross investment registered growth of 8.3% y/y, while fixed investment posted a slight increase of 1.8%, despite having declined by -7.2% y/y last year. Therefore, the increase in investment had been explained by inventory buildup in sectors such as mining, construction and manufacturing.

By asset type (chart 1), the lag in investment has been mainly in housing (-8.6% y/y) and other buildings (-4.5% y/y), offset by investment in machinery and equipment which increased 12.5% y/y (with large imports of capital goods) on the back of the recovery of the industrial sector which expanded 7.2% in 2024.

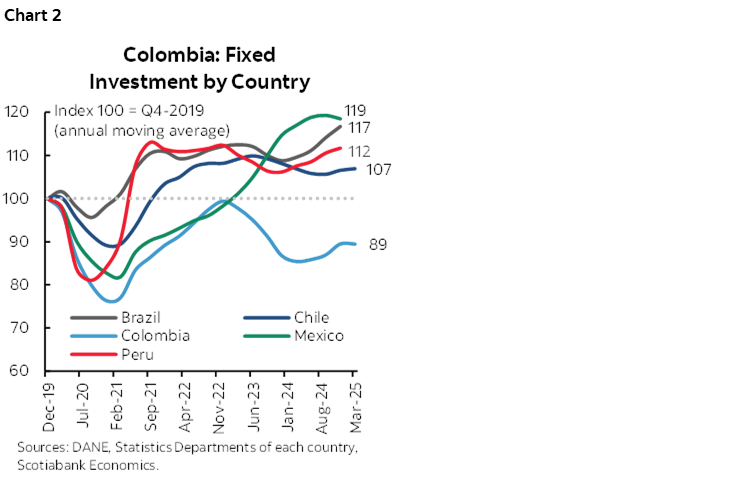

With data to Q1-2025, Colombian fixed investment remains about 10% lower vs pre-pandemic levels (chart 2), significantly lagging trends for regional peers where, despite multiple headwinds and current uncertainty have managed to recover to and then exceed pre-pandemic investment levels.

Currently, investment represents 16% of Colombian GDP, lower than the historical 21% and even the lowest in the last 20 years. Regardless of the fundamental and economic reasons behind the drop in investment (higher interest rates and global economic uncertainty), the severe impact on investor confidence following the loss of the sovereign’s investment grade status in May 2021, volatile political announcements, and the lack of public projects in collaboration with the private sector, also contribute to depressed investment activity.

Following the Colombian credit rating downgrade, the 5-year CDS increased 250 bps in 2022, and the exchange rate depreciation approached 20%, which, while in line with the regional trend, was greater than in other countries in the region. Moody’s is the only credit rating agency to maintain Colombia’s investment grade rating, but it recently announced that fiscal issues, budget inflexibility, rising government interest payments, and declining investor confidence, could deteriorate the country's credit profile.

For now, there is not a clear path towards an investment rebound. The monetary policy rate is expected to remain in contractionary levels, but also issues around public finances have increased uncertainty about fiscal sustainability. For now, the Ministry of Finance has announced to Congress that it expects an increase in primary public spending of around 8% (COP 29 tn) compared to last year, and an increase in tax revenues 8 ppts below what was projected in the 2025 Financing Plan, published in February 2025. In this context, given the structural decline in investment, the publication of the 2025 Medium-Term Fiscal Framework in mid-June will be crucial to demonstrate the public finance adjustment plan and whether it will be sufficient (as announced by the MoF) to regain investor confidence during the last year of the current administration.

Mexico—Banxico Minutes and Quarterly Report

Rodolfo Mitchell, Director of Economic and Sectoral Analysis

+52.55.3977.4556 (Mexico)

mitchell.cervera@scotiabank.com.mx

Brian Pérez, Quant Analyst

+52.55.5123.1221 (Mexico)

bperezgu@scotiabank.com.mx

Miguel Saldaña, Economist

+52.55.5123.1718 (Mexico)

msaldanab@scotiabank.com.mx

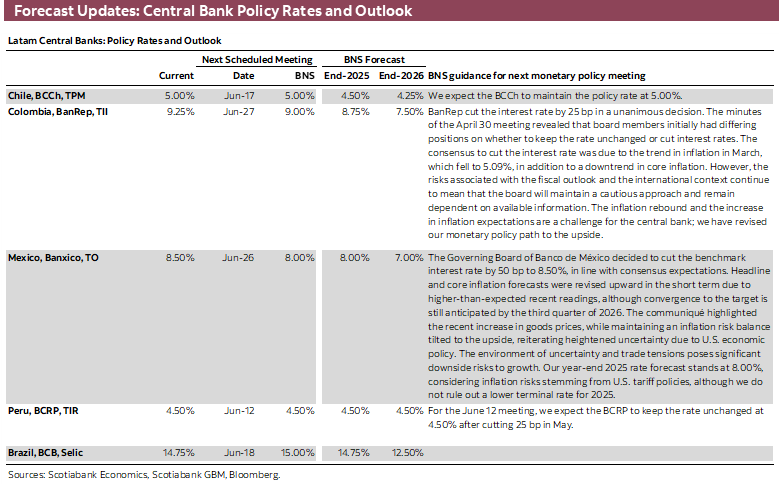

Next week, Banco de México will take centre stage in the national economic landscape with the release of key information. On Wednesday, May 28th, the central bank will publish its Quarterly Report for the first quarter of 2025, which will detail global economic conditions as well as inflation trends in major developed and emerging economies.

Regarding Mexico, the report will include a thorough analysis of the domestic economy’s performance, along with an in-depth review of both headline and core inflation. It will also explain the rationale behind recent monetary policy decisions. As usual, the report will present updated forecasts for economic growth and inflation, along with associated upside and downside risks.

In this context, special attention should be paid to the new economic growth projections. In its previous report, published on February 19th, 2025, Banco de México revised its 2025 growth forecast downward from 1.2% to 0.6%. However, that revision did not yet account for the implementation of U.S. tariffs on imports, making another downward adjustment likely.

This comes even though Mexico’s GDP data for Q1 2025, released earlier this month, surprised to the upside with a 0.2% quarter-over-quarter increase, thereby avoiding a technical recession by not posting two consecutive quarters of contraction.

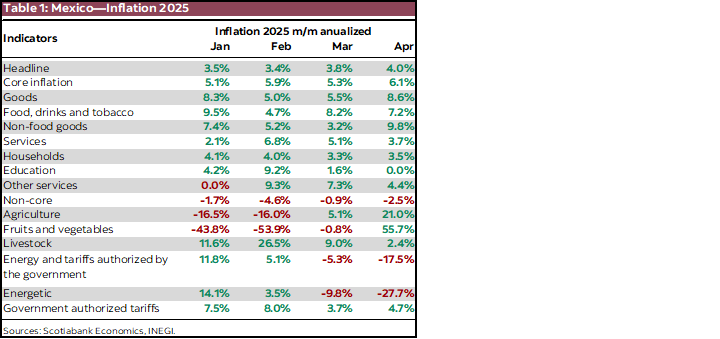

On the inflation front, no major changes are expected in the projections, as the central bank already revised its estimates upward during the May 15th monetary policy decision—raising forecasts for headline inflation in Q2 and Q3 2025, and for core inflation from Q2 through Q4 2025.

Separately, on Thursday, May 29th, the minutes from the May 15th monetary policy meeting will be released. In that meeting, the Governing Board unanimously decided to cut the benchmark interest rate by 50 basis points to 8.50% and signaled the possibility of maintaining the magnitude of cuts at the next meeting scheduled for June 26th. The minutes will be crucial for understanding the Board members’ reasoning behind continuing the rate-cutting cycle and for assessing forward-looking risks. This comes in a context where economic activity has shown resilience, while inflationary pressures persist.

Notably, headline inflation in April exceeded the upper bound of the 4% target range (table 1), driven by inflationary pressures in the goods component, which has been impacted by the exchange rate adjustment—the peso has depreciated by approximately 14% year-over-year.

Given this backdrop, we anticipate that at least two of the five Board members may adopt a more cautious stance, potentially favouring a smaller rate cut at the next monetary policy meeting.

Peru—GDP Growth is Turning Bumpy, but Exports Are Helping

Guillermo Arbe, Head Economist, Peru

+51.1.211.6052 (Peru)

guillermo.arbe@scotiabank.com.pe

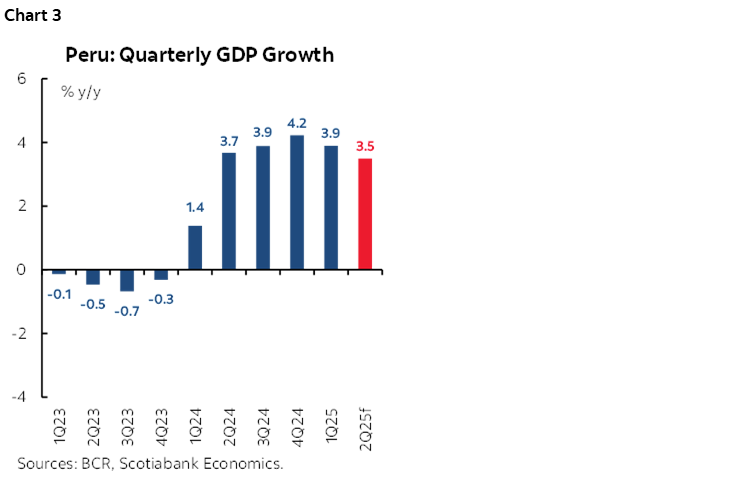

Peruvian GDP growth of 4.7% y/y for March was enough for Q1 2025 GDP to reach 3.9% (chart 3), broadly in line with our forecast of 4.0% growth. April should be substantially weaker than March, however. We are penciling in a forecast of 3.0% for April, but would not be surprised to see it mildly lower. The distance between March and April GDP growth figures reflect the calendar shift in Easter from March in 2024 to April in 2025. As a result, March 2025 had two additional working days, and April two days less.

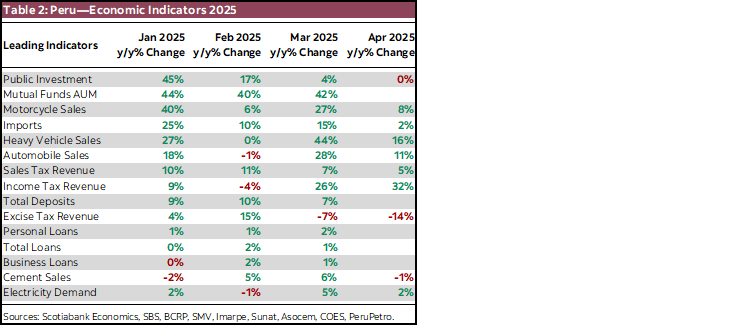

Early indicators reflect this (table 2). Outside of the seasonally-sensitive income tax revenue, every economic indicator that has been released so far for April is lower than it was in March. April’s calendar effect does not affect all indicators or industries equally, although here are two indicators which are, perhaps, more representative. One of them is public investment growth, which has, in truth, been slowing month by month throughout the year. However, to be slightly negative in April, as opposed to simply low, is clearly a reflection of two less working days. Something similar can be said for cement sales, which would have shown mildly positive growth if averaged out by the number of working days in April.

April will be the first month in Q2, and the low growth we expect for the month is one of the reasons that we forecast GDP growth in Q2 to come in at 3.5%, y/y, lower than in Q1 or for the last two quarters of 2024. The other reason for lower growth in Q2 is that it is off of a higher y/y comparison base. Prior to Q1, GDP growth had been rebounding off negative growth numbers the previous year. In Q1, growth was off a positive, but still-low base. From Q2 to Q4, the comparison base is high, which is part of the reason for slower growth in this period.

Recently there has been news that affect mining and give a bit of a downside to our 3.5% Q2 growth forecast. Shougang, Peru’s largest iron ore producer, has announced a four-to-five month interruption in production, from mid-May to approximately July–August, due to problems with its ship loader at the company-owned port of San Nicolás. At the same time, in early March, the government ordered a 30-day suspension in gold production in the gold-rich district of Pataz in the northern Andes, in an attempt to stem a surge in violence there. At first this suspension was interpreted to include legal mining activities, but was later clarified to include only illegal and semi-legal mining. Both events together have a temporary, but material, impact on GDP growth, and represent a mild downside risk to our Q2 forecast.

April GDP figures will not be released until June 15th, but we shall have the figures for a couple sectors, including mining, on June 1st, which should give us a better idea for the month. In the end, upside and downside risks balance out, and we remain comfortable with our full-year 2025 forecast of 3.3%.

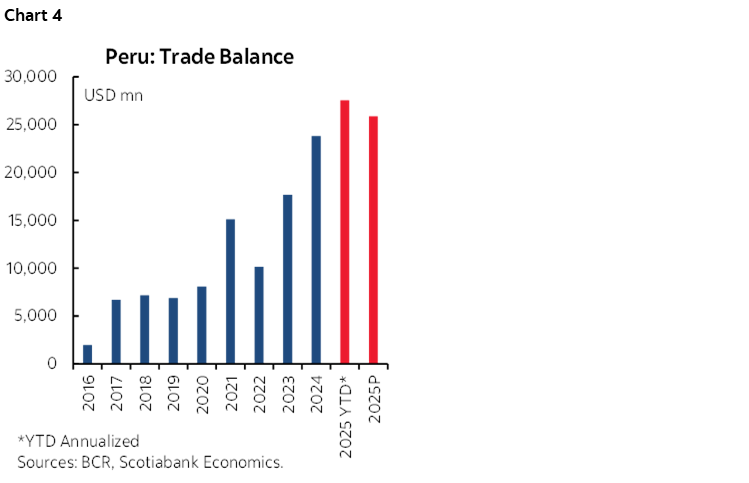

What is not showing up at all in Peru’s economic data, at least not yet, is any significant impact from global events, and more specifically, from U.S. and global tariff policies. Rather the reverse, Peru continues to enjoy extremely positive terms of trade (chart 4), with high key export prices (copper and gold) and low-key import prices (oil and soft commodities).

As long as terms of trade continue to be favourable, this will help underpin growth. The proof of the pudding is in the trade balance info, which was recently released for Q1. Exports were up 25% y/y in Q1, which is huge. The export price index rose 13.8% in the quarter, led by coffee, gold, natural gas, zinc and copper. But it wasn’t all price effect, as the export volume index rose 10% in Q1 as well. The increase in export prices was mostly in metals, while the increase in volume was mostly in agro-industrial goods and textiles, as well as in fishmeal, given a strong, but temporary, seasonal production. For Peru’s agro-industrial products, export volumes were up 38% in Q1, while prices were down 8%. Textiles volume exports increased 11%. Interestingly, exports to the U.S. rose 31% in Q1, while exports to China were up only 0.2%. The U.S. is a major market for Peru’s agro-industrial and textile exports. China is a major market for Peru’s base metals exports (gold is more diversified).

To round out the story, imports were up 14.6%, y/y, in value, mostly on greater volume, which rose 19%. Import prices were down nearly 4% in Q1, in clear contrast to the sharp increase in export prices. Peru’s trade surplus in Q1 (USD6.9bn), when annualized (US27.5bn, chart 4 again), suggests that it will easily break last year’s record surplus (USD23.8bn), and is on trend to surpass our own current forecast of USD25.9bn.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Click here to be redirected |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.