ECONOMIC OVERVIEW

- A quieter week awaits in most of Latam, with Chilean, Peruvian, and Colombian release calendars bare of key data, in contrast to Mexico’s where H1-May CPI data and Q1 GDP details are in focus. Brazil also publishes March economic activity data.

- In today’s report, the team in Mexico outlines their expectation for next week’s releases, on the heels of a dovish Banxico decision, while our colleagues in Chile highlight an increased chance that the BCCh brings forward the timing of their next rate cut.

- Global PMIs out on Thursday are the main event for markets alongside whatever news emerge on trade and geopolitics over the week. Canadian and Chilean markets are closed on Monday and Wednesday, respectively.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Chile and Mexico.

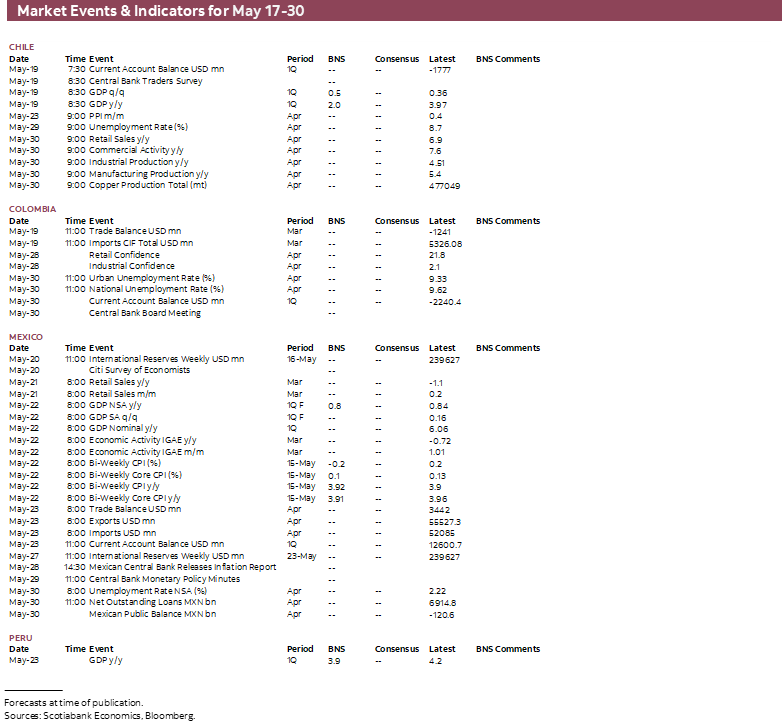

MARKET EVENTS & INDICATORS

- A comprehensive risk calendar with selected highlights for the period May 17–30 across the Pacific Alliance countries and Brazil.

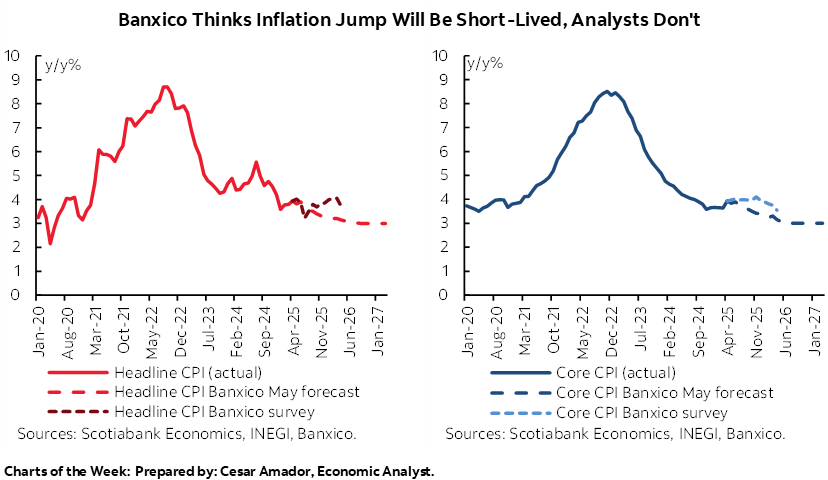

Chart of the Week

ECONOMIC OVERVIEW: GLOBAL PMIs, MEXICO BI-WEEKLY CPI

Juan Manuel Herrera, Senior Economist

+52.55.2299.6675

juanmanuel.herrera@scotiabank.com

- A quieter week awaits in most of Latam, with Chilean, Peruvian, and Colombian release calendars bare of key data, in contrast to Mexico’s where H1-May CPI data and Q1 GDP details are in focus. Brazil also publishes March economic activity data.

- In today’s report, the team in Mexico outlines their expectation for next week’s releases, on the heels of a dovish Banxico decision, while our colleagues in Chile highlight an increased chance that the BCCh brings forward the timing of their next rate cut.

- Global PMIs out on Thursday are the main event for markets alongside whatever news emerge on trade and geopolitics over the week. Canadian and Chilean markets are closed on Monday and Wednesday, respectively.

A quieter week awaits in most of Latam following a past few days when GDP readings out of Colombia and Peru exceeded estimates, Banxico delivered a more dovish decision than expected, and the BCCh’s meeting minutes indicated that Chilean officials considered a rate cut at their April decision. It was also an eventful week outside of the region, with a surprising scaling back of U.S.-China tariffs (lower rates looked possible but not this ‘low’) that juiced market sentiment, while U.S. data, from CPI to retail sales to industrial production, broadly undershot estimates slightly.

Beyond the usual monitoring of trade news and some anxiety around U.S. fiscal policy, global markets will centre their attention on Thursday’s May PMI releases around the world that may capture a slight improvement in trade sentiment (data are collected over the second half of the month). Chinese macro releases over the weekend will also be in focus as it will be interesting to see whether ‘hard’ domestic data are worsening quickly, resulting in a ‘friendlier’ stance in Beijing vis-à-vis a U.S. trade deal. Disappointing figures could also make the case for greater public stimulus. The RBA’s rate decision (25bps cut), U.K. and Canadian CPI, and the ECB’s minutes round out the macro calendar, and Target and Home Depot earnings will be watched for tariff reactions and implications. Note that Canadian and Chilean markets are closed on Monday and Wednesday, respectively.

In Latam, Colombia’s and Peru’s calendars are relatively bare, so political headlines will likely dictate idiosyncratic moves in local markets. Chile’s schedule also has little on offer, but we discuss the rising odds of an earlier resumption of rate cuts in the country. On the flip side, Mexico has the fullest calendar of all as covered by our team in today’s report.

Mexico’s releases start on Tuesday with the Citi economists survey results, followed by Wednesday’s March retail sales, Thursday’s H1-May CPI, Q1 GDP revision, and March economic activity, to then close the week with April international trade data. We already know that Mexico’s economy, with a 0.2% q/q rise in Q1, regained a small part of the ground lost after Q4’s 0.6% contraction, but we also know that this was to a large extent thanks to a surge in agricultural output. What we’re still unclear on, and that next week’s data will expand on, is what drove the weakness in the secondary sector (manufacturing, construction, and utilities) which fell 0.3% q/q and the stalling of the tertiary sector (services).

Banxico’s rate decision on the 15th showed relatively rosy inflation forecasts as, despite near-term upside surprises, the Board left its year-end projections virtually intact—and, in turn, the expected date of convergence to target in 3Q26. Citi’s survey results should stand in stark contrast to the bank’s outlook and will also likely show that most economists anticipate another 50bps cut in June after Thursday’s dovish decision. CPI data will likely show both headline and core inflation remaining very near 4%, and exports may have posted a sharp drop in April as tariffs took a bite and tariffs front-running cooled.

On Monday, Chile and Brazil kick off the data week with Q1 GDP and March economic activity, respectively. Chile’s release is of generally limited relevance as monthly economic activity data for Jan-Mar already tee up a 2% y/y increase in GDP from the 4% expansion in Q4, with weakness early in the year resulting from the brief February blackout. But next week’s release will present an expenditure breakdown of how the Chilean economy fared during the quarter. In today’s report, our economists in Santiago zero in on the increased chance that the BCCh opts to resume rate cuts at its July meeting (still skipping June), with dovish minutes, inflation undershoots, and simmering global risks. We’ll see what those in markets think in the results to the BCCh’s survey out on Monday.

After strong gains of 3.6% y/y in January and 4.1% y/y in February, Brazil’s economy is expected to decelerate to a respectable 2.5-3.0% rise in output in March, supported by a good month for industrial output and retail sales. Overall, Brazil’s economy is expanding at a solid pace, and while the BCB may have thought it was closing in on dialling up its restrictiveness, rumblings that Lula’s government could be considering extra spending to shore up his popularity may end up motivating more BCB hikes. At writing, only a cumulative ~20bps are priced in for additional BCB tightening, but markets will keep a close eye on government stimulus risks.

PACIFIC ALLIANCE COUNTRY UPDATES

Chile—The Probability of a Policy Rate Cut in July Increases

Anibal Alarcón, Senior Economist

+56.2.2619.5465 (Chile)

anibal.alarcon@scotiabank.cl

The Central Bank Board considered cutting the policy rate in April, amid a scenario of more moderate core inflation than expected. According to the minutes of the April monetary policy meeting, the Board assessed that one of the potential impacts of the deteriorating external environment would be lower inflationary pressures than anticipated in the March Monetary Policy Report (IPoM), which could require the rate to move closer to the neutral range sooner than anticipated. On the one hand, the Board notes that the risks to persistent inflation were not under control and that the possibility of an additional cost shock remains open, likely in anticipation of the new electricity rate hike that will take effect in the second half of this year. On the other hand, several Board Members assess that the deteriorating external environment suggests lower inflationary pressures going forward, adding to the downward surprise in core inflation that the Board encountered at the time of the April meeting. In this scenario, the Board considered a 25 bps cut in the policy rate, but it was ruled out as it could generate erroneous readings or undesirable market volatility, given a context where all expectations pointed to a 5% rate hold.

Implications for the June meeting. Since the April 29th meeting, the external environment has become less negative, showing progress in negotiations between the United States and some trading partners, especially China. Domestically, the April CPI would have again surprised the March IPoM’s baseline scenario on the downside in terms of core inflation, although a new increase in electricity rates is beginning to take hold in the short term (impact of 0.2 ppts), and international fuel prices are showing a slight rebound (in USD), with no major developments in the exchange rate. In this scenario, if there is an early convergence of the policy rate to its neutral level, we believe a cut is unlikely to materialize at the June 17th meeting. However, such a scenario would not be ruled out if the external environment worsens—which could be due to a setback in trade negotiations between the United States and China—a drop in oil prices, an appreciation of the Chilean peso, or a new downward inflationary surprise in the May CPI (to be announced on June 6th by the INE).

The probability of a rate cut at the July meeting increases. The March IPoM scenario contemplates two rate cuts this year (third and fourth quarters) and two next year, reaching a 4% policy rate in the third quarter of 2026 (the neutral level estimated by the Central Bank). Based on the new data, the June report could bring forward the convergence of the rate to its neutral level (we estimate to the first half of 2026), which increases the likelihood of bringing forward the cut initially planned for September to the July 29th meeting. This would provide a clearer picture of the external environment and concrete information on inflation and its determinants at the local level. This would also include a probable rate cut by the Fed (July 30th), a condition we consider key for the Central Bank in the current scenario.

For now, our scenario still considers two policy rate cuts this year and one next year, reaching 4.25% during the first quarter of 2026.

Mexico—Q1 GDP Breakdown, H1-May CPI

Rodolfo Mitchell, Director of Economic and Sectoral Analysis

+52.55.3977.4556 (Mexico)

mitchell.cervera@scotiabank.com.mx

Brian Pérez, Quant Analyst

+52.55.5123.1221 (Mexico)

bperezgu@scotiabank.com.mx

Miguel Saldaña, Economist

+52.55.5123.1718 (Mexico)

msaldanab@scotiabank.com.mx

Next week, several economic indicators will be released that will help assess whether the national economy continues to experience a slowdown or contraction. In particular, the detailed GDP figures for the first quarter of 2025 will be published. It will be crucial to analyze the factors that contributed to the decline in the industrial sector, such as the possibility that manufacturing was boosted by an unusual increase in demand for exported goods in anticipation of tariff impositions. Also, regarding quarterly data, the balance of payments numbers for Q1 will be released, where analysts would be especially interested in the FDI composition amid the increase in uncertainty.

Additionally, inflation data for the first half of May will be released, which is expected to remain close to the 3.9% level observed in April. Inflationary pressures are likely to persist in the goods category, driven by the depreciation of the exchange rate. Retail sales figures for March will also be published, along with the Global Indicator of Economic Activity (IGAE) for the same month, the trade balance for April, and Citi’s analyst expectations survey. Most likely, downward revisions will continue in economic growth forecasts (0.1% for 2025), and some analysts could change downwards their year-end forecast for Bank of Mexico’s benchmark interest rate, which currently stand at 7.75% and the dovish guidance of this month’s meeting.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Click here to be redirected |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.