ECONOMIC OVERVIEW

- The turmoil in the banking sector of the past week has shaken markets and left analysts and economists uncertain about the path, with the global risk backdrop dominating the performance and trading volumes of markets in the Latam region and may continue to do so over the next five trading days.

- The Colombian and Peruvian weeks are quiet from a data or events perspective, though we’re keeping an eye on Petro’s reform plans. In Chile, somewhat stale Q4 GDP data and PPI figures will allow us to marginally tinker our expectations.

- There’s more that catches the eye in Mexico (CPI, IGAE, retail sales) and in Brazil (BCB decision, hold expected) as far as local markets are concerned, but the main event for global traders will be, by and large, the Fed’s decision on Wednesday.

- In today’s Weekly, the teams on the ground write on their expectations for BanRep’s decision at month-end, Mexican FDI and the recent Tesla announcement, and Peru’s weak (and unfortunate) start to 2023.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Colombia, Mexico, and Peru.

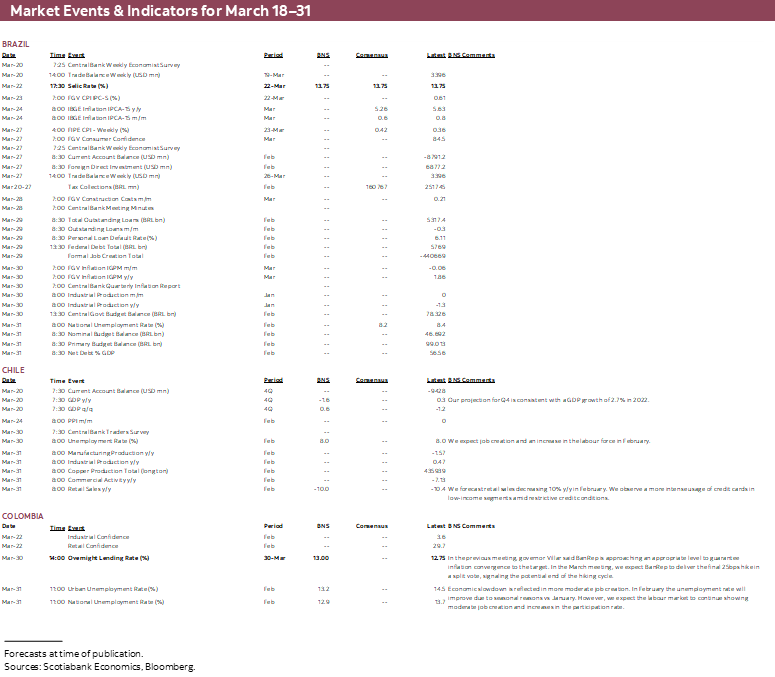

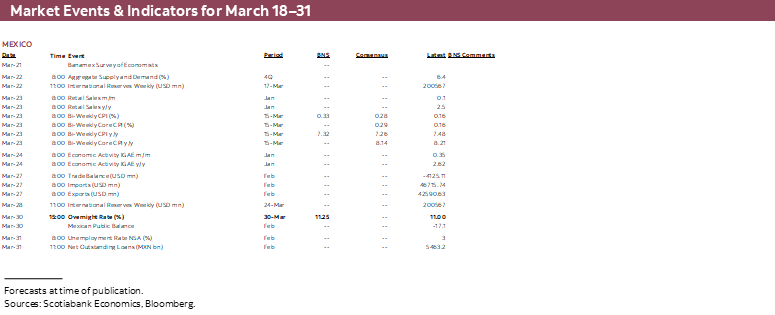

MARKET EVENTS & INDICATORS

- A comprehensive risk calendar with selected highlights for the period March 18–31 across the Pacific Alliance countries and Brazil.

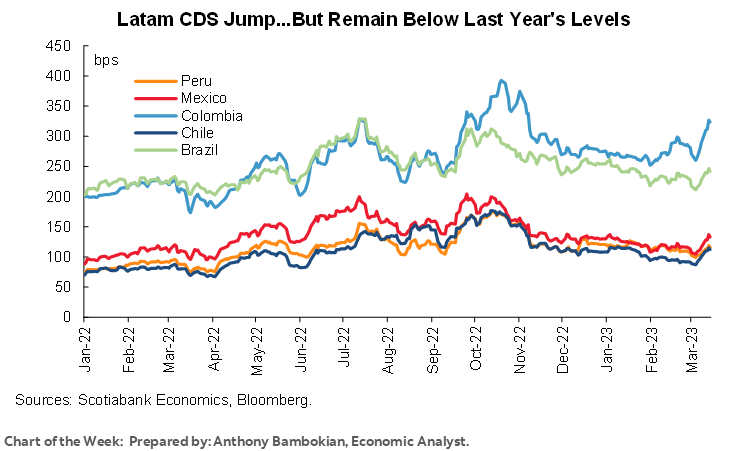

Chart of the Week

ECONOMIC OVERVIEW: KEY MEXICO DATA AND BCB AS GLOBAL MARKETS WATCH FED

Juan Manuel Herrera, Senior Economist/Strategist

Scotiabank GBM

+44.207.826.5654

juanmanuel.herrera@scotiabank.com

- The turmoil in the banking sector of the past week has shaken markets and left analysts and economists uncertain about the path, with the global risk backdrop dominating the performance and trading volumes of markets in the Latam region and may continue to do so over the next five trading days.

- The Colombian and Peruvian weeks are quiet from a data or events perspective, though we’re keeping an eye on Petro’s reform plans. In Chile, somewhat stale Q4 GDP data and PPI figures will allow us to marginally tinker our expectations.

- There’s more that catches the eye in Mexico (CPI, IGAE, retail sales) and in Brazil (BCB decision, hold expected) as far as local markets are concerned, but the main event for global traders will be, by and large, the Fed’s decision on Wednesday.

- In today’s Weekly, the teams on the ground write on their expectations for BanRep’s decision at month-end, Mexican FDI and the recent Tesla announcement, and Peru’s weak (and unfortunate) start to 2023.

The turmoil in the banking sector of the past week has shaken markets and left analysts and economists uncertain about the path ahead for monetary policy (and growth) in the major economies. Although idiosyncratic factors seem (mostly) to blame for the recent bank failures and uncertainty, the repercussions of these on broader market sentiment and consequences in credit creation globally or broader consumer and business sentiment remain to be seen.

This may all seem somewhat detached and beyond this note’s focus on the week ahead in Latam, but the global risk backdrop has dominated the performance of assets in the region and may continue to do so over the next five trading days. This may be particularly true for Colombia and Peru, whose data calendars are relatively bare—though we’re watching developments around reform proposals in Colombia—while Chile’s week kicks off with (somewhat stale) Q4 GDP data on Monday, complemented by PPI on Friday.

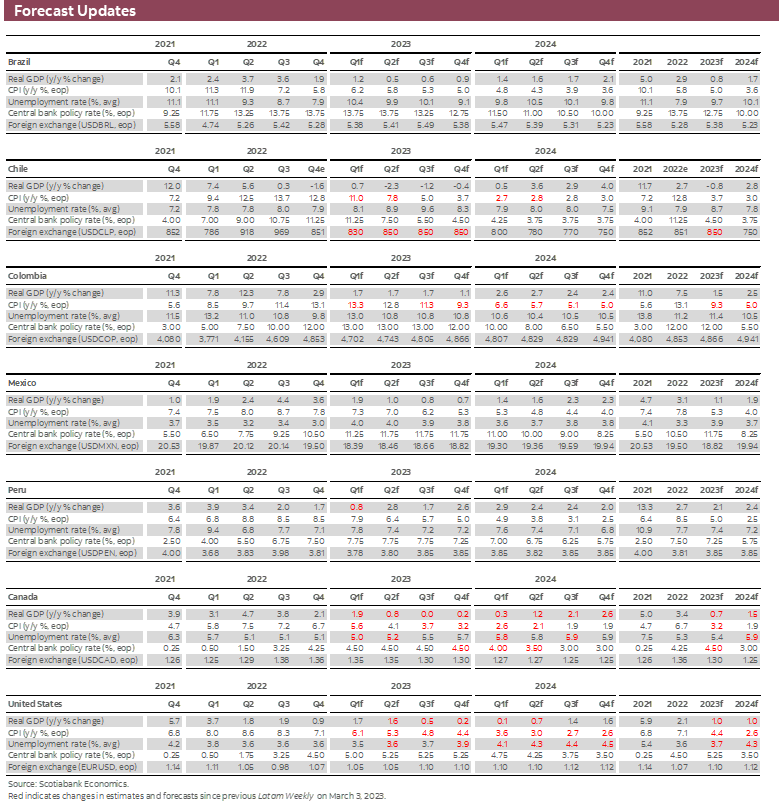

There’s more that catches the eye in Mexico (CPI, IGAE, retail sales) and in Brazil (BCB decision) as far as local markets are concerned, but the main event for global traders will be, by and large, the Fed’s decision on Wednesday. There, market expectations have swung sharply from seeing an elevated chance of a 50bps hike, to now assigning about 25% odds to a rate hold. The evolution of banking sector issues ahead of it is bound to play an important role in the bank’s decision but we think that, ultimately, the Fed will hike.

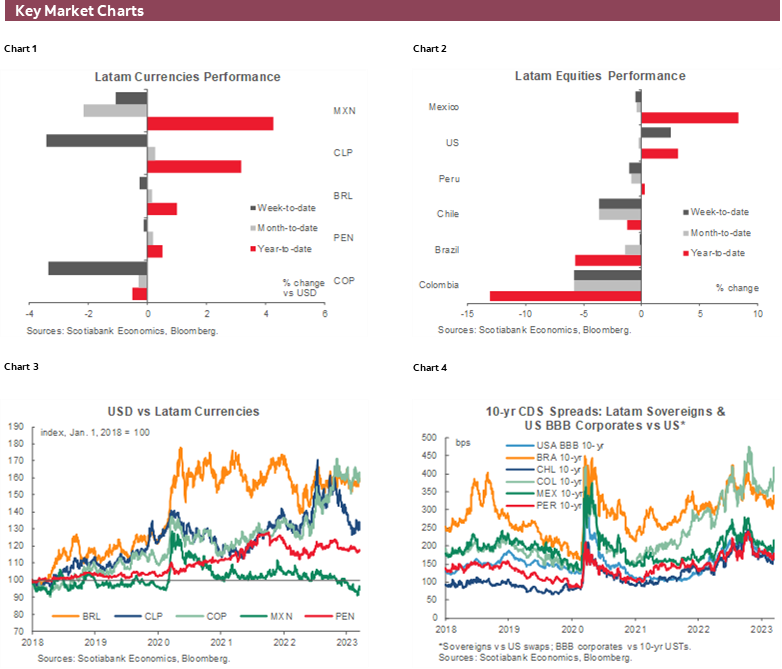

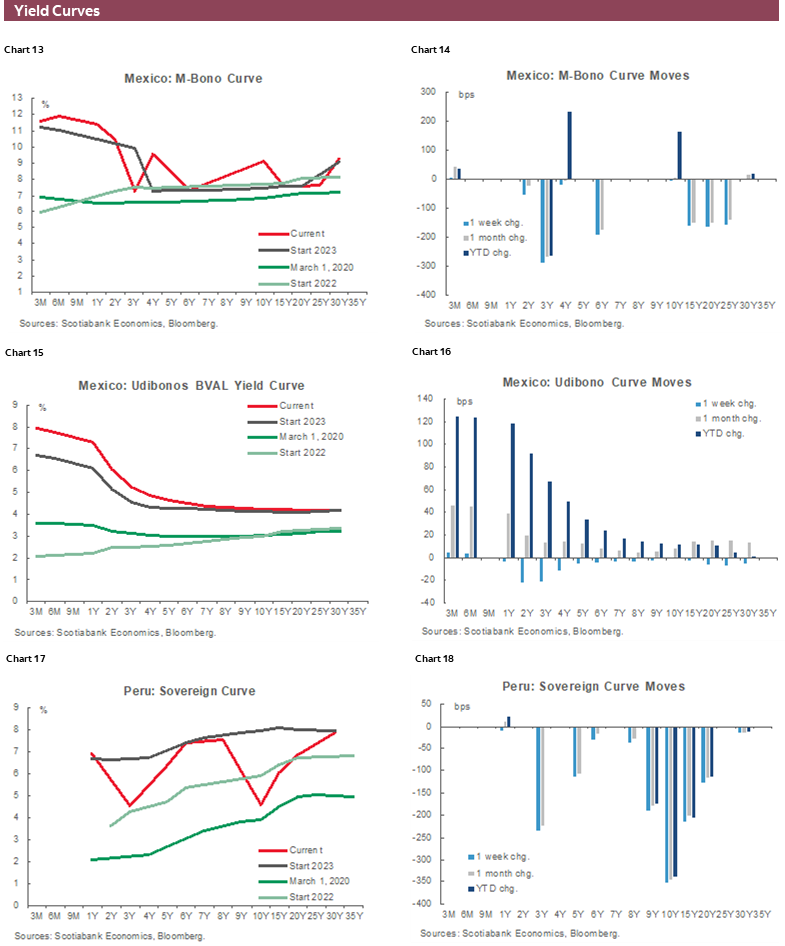

The recent performance in the peso exemplifies the pull of external developments. We saw the MXN weaken sharply from its best levels since 2017, below the 18 pesos level, to trade above the 19 mark on multiple occasions this week, with a double-hit from the risk-off mood as well as the implications for Banxico from a less hawkish Fed and/or a US economic slowdown. Twelve-month implied MXN yields fell from ~12.8% last Wednesday to just under 12% this morning, while year-ahead implied Banxico rate pricing has dropped from 11% to around 9.75%; we see it at 11% in Q1-24. That the peso also looked technically overbought and the market noise came on the heels of a softer-than-expected February CPI print in Mexico also likely didn’t help.

On the inflation front, we get H1-March CPI data in Mexico next Thursday. Our Mexico team and the Bloomberg consensus anticipates a deceleration year-on-year, but an uptick month-on-month, with the data released on the same day as January retail sales, and ahead of January IGAE figures on Friday. According to INEGI’s advance indicator, the Mexican economy expanded 2.83% y/y to start the year, a modest acceleration from the 2.62% that the IGAE showed in February. We got solid early-2023 manufacturing and industrial production data earlier this week, and the investment outlook in Mexico is looking a bit better than we had perhaps thought a few months back (see Mexico section).

Will all of next week’s data matter all that much to Banxico? It may be the case that the central bank was already fairly certain that it would roll out two more 25bps increases, and now the broader Fed and risk backdrop could be what determines whether they actually follow this plan.

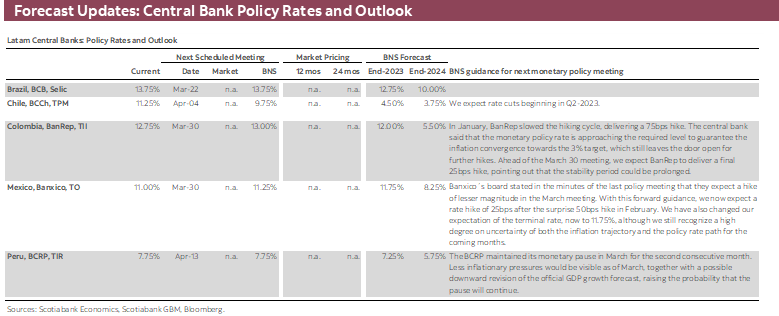

Brazil’s BCB is widely expected to leave its policy rate on hold at 13.75% on Wednesday. The central bank is in the unenviable position of facing pressure from government to lower policy rates while markets would not welcome a rate reduction in the current environment. The BRL lost ground to its weakest level since early-January this week and optics (political pressure) are certainly not favourable to easing policy, despite falling inflation and signs of economic weakness. The country’s new fiscal framework plans is also hanging negatively over Brazilian assets but its presentation and more details to come next week would reduce fiscal upside uncertainty that could comfort the BCB. A countercyclical fiscal rule would (in theory) ease pressure on the BCB when the economy is overheated and inflation is above target. A rate cut may come in the second half of the year.

PACIFIC ALLIANCE COUNTRY UPDATES

Colombia—Economic activity deceleration reaffirms our expectation of a 25bps hike in March

Sergio Olarte, Head Economist, Colombia

+57.1.745.6300 Ext. 9166 (Colombia)

sergio.olarte@scotiabankcolpatria.com

María Mejía, Economist

+57.1.745.6300 (Colombia)

maria1.mejia@scotiabankcolpatria.com

Jackeline Piraján, Senior Economist

+57.1.745.6300 Ext. 9400 (Colombia)

jackeline.pirajan@scotiabankcolpatria.com

The current BanRep hiking cycle aims to make inflation return to more sustainable levels close to the target range (2%–4%) while helping, in the end, long-run growth and more certainty around decision-making in investment and durable consumption. It is therefor optimal for the central bank to see an economic activity deceleration in the short run to ensure higher growth in the future with no excessive noise around prices, especially in an environment of unusually high headline inflation (above 13%), and almost 10% y/y private consumption growth last year.

However, it is tricky for BanRep to finetune how big the pain for the economy should be in the short run, in order to increase long-run growth. Because of this, it is important to keep an eye on how painful high rates are for current economic activity to predict when BanRep can start to think about easing its monetary policy stance.

Recent data show that Colombian domestic demand is in a significant deceleration path since Q4-22. In fact, according to DANE, GDP grew 0.7% q/q (2.9% y/y) in the final quarter of 2022, while private consumption fell by 0.2% q/q (4.3% y/y). Soft data published by RADDAR (an agency that analyses consumer behaviour) point to private consumption falling ~2% y/y in Q1-23.

In fact, new vehicle sales have fallen 19% y/y during the first two months of the year. The question that arises is if these data are in line with BanRep expectations. The best answer to that is the most recent BanRep staff projections which point to a 0.2% GDP expansion for this year in combination with very poor private consumption dynamics, and better investment performance.

Therefore, in our opinion, a soft landing in 2023 is still the base case scenario, which is in line with BanRep hiking once more on March 30, by 25bps to 13% and keeping it at that level at least until Q4-23—when we think core inflation will consolidate its convergence path helping inflation expectations to return in the 1Y tenor to the inflation target range.

Next week’s calendar for Colombia will be light in terms of macro data. In the meantime, the market will continue to focus on international developments and on the presentation of new reforms (pension and labour). We insist that political negotiation on those topics could be harder, and traditional political powers could push to vanish any disruptive proposal. Meanwhile, volatility may continue.

Mexico—Global turbulence clouds the outlook for several variables, but Mexico had a solid start to 2023

Eduardo Suárez, VP, Latin America Economics

+52.55.9179.5174 (Mexico)

esuarezm@scotiabank.com.mx

Miguel Saldaña, Economist

+52.55.5123.1718 (Mexico)

msaldanab@scotiabank.com.mx

January offered fairly good news on the growth front, with firmer than expected manufacturing activity (+4.8% y/y vs consensus +3.0% y/y) and industrial activity (+2.8% y/y vs consensus +2.4% y/y). The robust growth surprise, alongside somewhat bad news on the inflation front (core inflation has continued to rise, with the last print coming in at +8.21% y/y) and on price setter expectations (the latest Regional Economies Report by Banxico showed that more than half of services price setters continue to anticipate similar or larger increases in prices charged) should keep Banxico on a tightening stance. However, global financial sector turbulence decided to add uncertainty to the mix. Consensus anticipates an upswing in next week’s CPI release, and we also have the FOMC set to make its own decision on March 22nd, where both consensus and OIS are favouring a 25bps hike. If those two conditions are met, Banxico will likely follow suit with its own 25bps hike in its March 30th decision—but the outlook has become much cloudier given the ongoing turmoil in global markets.

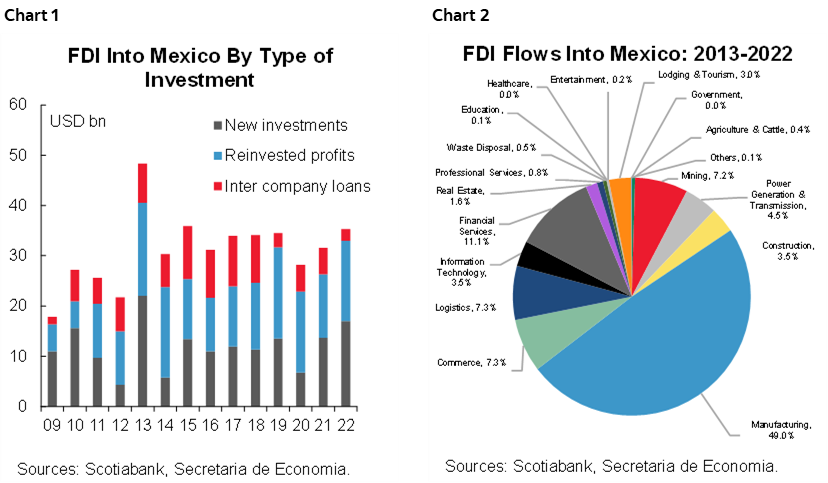

FDI in Mexico has picked up over the past couple of years (chart 1), with the main good news being the new investments category (this includes both the acquisition of existing businesses by foreigners, as well as the establishment of brand-new ventures). Although 2022 FDI didn’t quite reach “Mexico Moment” levels, it was still a strong print in that category. As we have argued in the past, we think that nearshoring will lead to important positive outcomes, but these will be concentrated in the usual regions (the North, Bajio, and Mexico City & Yucatan), as well as the sectors that have traditionally been the biggest and most dynamic investment magnets (manufacturing taking the lion’s share, alongside logistics, financial services, commerce, and tourism, see chart 2).

There are many potential ways to read the recent announcement of the Tesla plant (two weeks ago), which could be worth up to USD10bn over several stages. The unquestionable good news is that it will mean a tailwind for lackluster investment in Mexico, which currently sits at 2013 levels (measured through gross fixed investment). More complex to interpret are the broader implications.

- There are likely few companies with clients as sensitive to carbon footprints as Tesla buyers, and hence the announcement of a plant built by the company in Nuevo Leon could mean AMLO is opening the doors to a cleaner power mix in the country. This would be good news for the country as a whole.

- However, even if this proves true and AMLO indeed decides to open the door for cleaner power for Tesla, it’s hard to tell if this is the start of a trend, or a one-off. It’s important to bear in mind that similar to Trump on the other side of the border a few years ago, AMLO’s approach to negotiations is more transactional than principles-based, and hence one good data point does not necessarily mean the start of a trend.

- There is another angle that has been discussed which is that Tesla is such an important symbol that it can trigger a wave of goodwill and a surge in investment. We are more hesitant to buy into this narrative, given that as we have argued in the past, the limits to Mexico’s capacity to attract investment are driven by scarcity of production factors (spare power generation capacity, skilled labor, water, etc), more than by sentiment.

Overall, the news of the Tesla plant was good. How good, remains to be seen.

Mexican Inflation Seen Lower

Next week, eyes will be on the inflation print for the first half of March. On a yearly basis, we expect headline inflation to decelerate from its last print, (7.48% in H2-Feb). Price dynamics are expected to remain driven by the core component, despite a slow deceleration.

Merchandise items inflation, above 10.0%, is leading the increases, but these have moderated since the beginning of 2023. However, services prices remain on the rise, and our expectation is that they will start a declining trend possibly in the last half of the month, or in April. In this sense, Banxico mentioned in the latest Quarterly Inflation Report that price indexation could be one of the reasons holding core inflation stickiness.

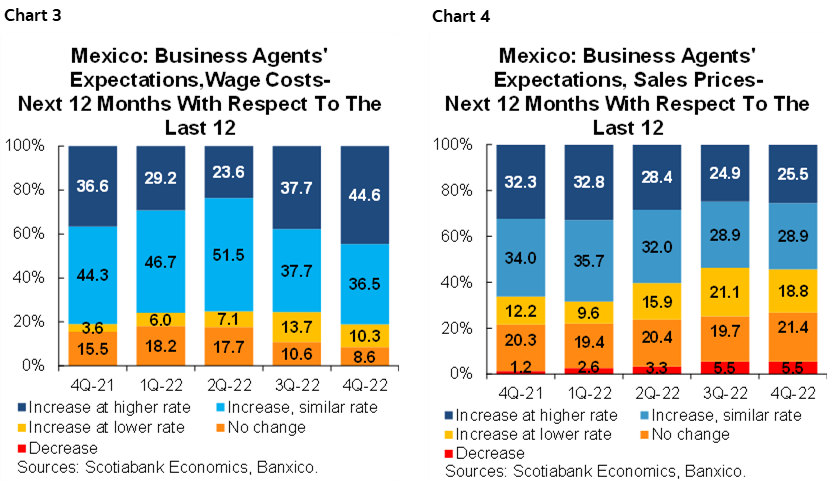

This week, Banxico also noted in the Regional Economic Report that a higher proportion of business agents (44.6% in 2022 Q4 vs. 37.7% in the previous quarter, chart 3) expects wage costs to increase at a higher rate in the next 12 months, placing upward pressure on consumer prices. In line with this, the share of directors that expects sale prices to increase at a similar or higher rate stood almost unchanged at 54.4% (chart 4), suggesting that stickiness, especially in the core component, and still unanchored expectations, remain as key upside risks for the inflation outlook.

It is also worth noting that this will be the last inflation print before Banxico’s monetary policy decision on March 30. Uncertainty regarding the terminal rate and March’s hike decision have remarkably increased in light of recent developments in the international banking system. For now, we stick to our call of a 25bps hike, although at this point everything is on the table; next week’s inflation print, the Fed’s stance, and the development of financial risks will be key to possible changes to our outlook.

Peru—A Hard Rain’s Gonna Fall

Guillermo Arbe, Head Economist, Peru

+51.1.211.6052 (Peru)

guillermo.arbe@scotiabank.com.pe

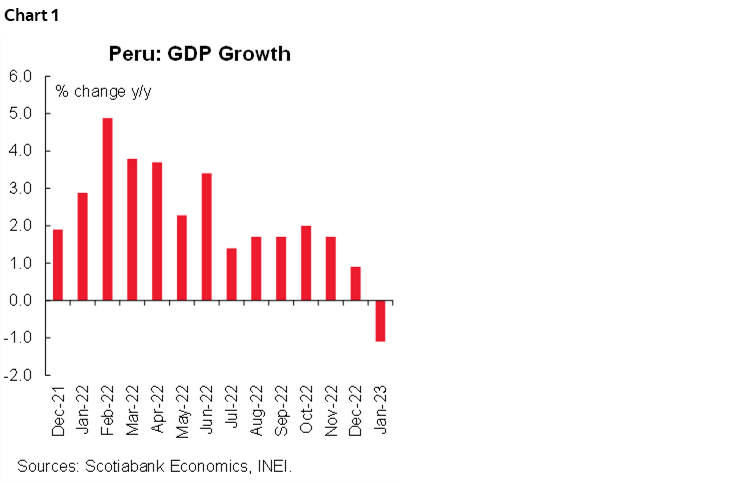

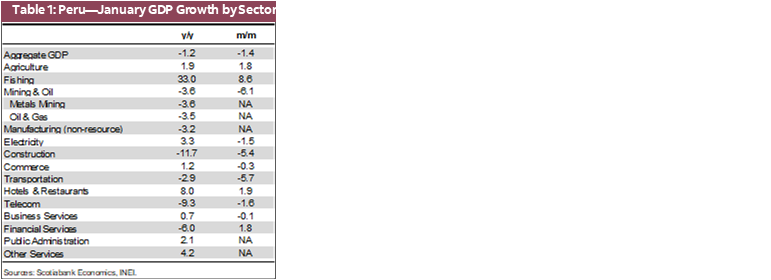

January GDP fell 1.1% y/y and 1.4% m/m (chart 1 and table 1). This was not unexpected, due to the protests that took place during the month.

Of particular concern was the 1.4% m/m decline, as this was the fourth consecutive month-on-month contraction. Given this, a case could be made that Peru is on the verge of a recession. Twelve-month moving GDP growth to January is now trending at 2.4%, after ending 2022 at 2.7%.

February GDP growth should not be much better than January, possibly between nil to slightly negative. We had high hopes that March would perform much better than the previous two or three months… but then the rains came. Even after factoring in the rains, March growth should be positive at least, although not enough to prevent a weak print for the first quarter as a whole.

The breakdown of growth in January was telling. Construction plummeted 11.7% y/y. Construction requires mobilizing not only personnel, but also material and machinery, and doing so on a daily basis, frequently to the city outskirts and non-centric places in general. The protests were not the only factor behind the weak print, however, as higher interest rates and greater constructions costs due to inflation were also a factor in residential building weakness. Furthermore, public investment by regional and local governments plunged after the change in authorities that took place on January 1.

Of these three factors (protests, higher interest rates and costs, and low public spending), the first two will have also impacted construction in February. The one positive is that public investment rose 18% y/y in February. That should help. In March, protests will no longer be a factor for construction, but rains will have inhibited construction instead.

The 2.9% y/y decline in transportation in January can also be attributed to the protests. In previous months, transportation had been growing strongly.

Mining (including oil & gas) fell 3.6% y/y and 6.1% m/m. Much of this was linked to the protests. The 62% y/y decline in tin output certainly was, as Peru’s only prominent tin mine, San Rafael (Minsur) closed temporarily due to the protests. The three largest mining operations that were affected by the protests in January, Las Bambas (copper), Antapaccay (copper) and San Rafael (tin) were also impacted in February, but not in March.

Not everything was terrible. Fishing was up 33% y/y. Too bad that it has such a low weight, at under 1% of GDP. Electricity rose 3.3% y/y, roughly on trend with past months. Commerce rose a modest 1.2% y/y (-0.3% m/m), which was not as bad as one might have expected given the protests and roadblocks. Restaurants and hotels rose a surprising 8.0% y/y and 1.9% m/m, a quite robust result given the way the protests shut down the tourism business in much of the country, including the key region of Cusco.

So, what does this all mean? Mostly, that our forecasts, of 0.8% GDP growth in Q1 2023, and 2.1% for the full year, are at risk and are under revision. Most of the factors that have been impacting Q1 are temporary (the protests have subsided, the rains will end eventually, and even the reference rate has stabilized, with the next move this year likely to be downward), and there seems to be little reason to do more than tweak our remaining quarterly forecasts for the year, but enough damage has been done in Q1 to warrant a new look at our numbers.

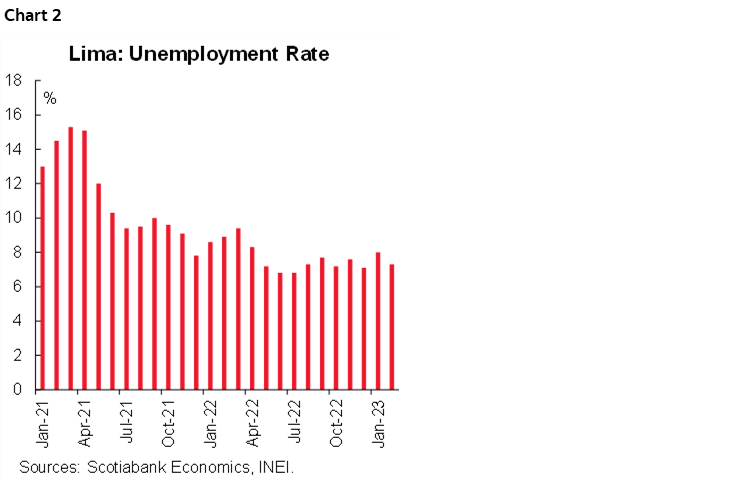

The job scenario in Lima was better than one might expect, given the events so far this year. Unemployment in the three months ending in February was 7.3% (chart 2). This was down from 8.0% in January and from 8.9% a year ago. The figure is for Lima only, as the countrywide figure is released with a delay (the most recent figure was 3.6% for Q4 2022; note that unemployment does not include the underemployed, which is important in Peru). The protests, which mostly took place in the southern part of the country, did not affect the Lima job market all that much.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Click here to be redirected |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.