ECONOMIC OVERVIEW

- The week ahead presents a series of key CPI releases in the Latam region and in the US, as well as rate decisions in Peru and Chile where another pause is expected.

- Chile kicks off the week with inflation data for April that may hold to a thirteenth consecutive month in double-digits.

- Mexican and Brazilian prices data follows, with Banxico’s decision next week (hike or pause?) hinging on Tuesday’s release while the BCB faces a long campaign of pressure until its next announcement in June.

- Colombia’s calendar is quiet, in what is a welcome break by markets that have been troubled by another episode of political risks. The team discusses how markets may have learned to worry less about the tape bomb, but fiscal developments remain a must-watch.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Chile, Colombia, and Peru.

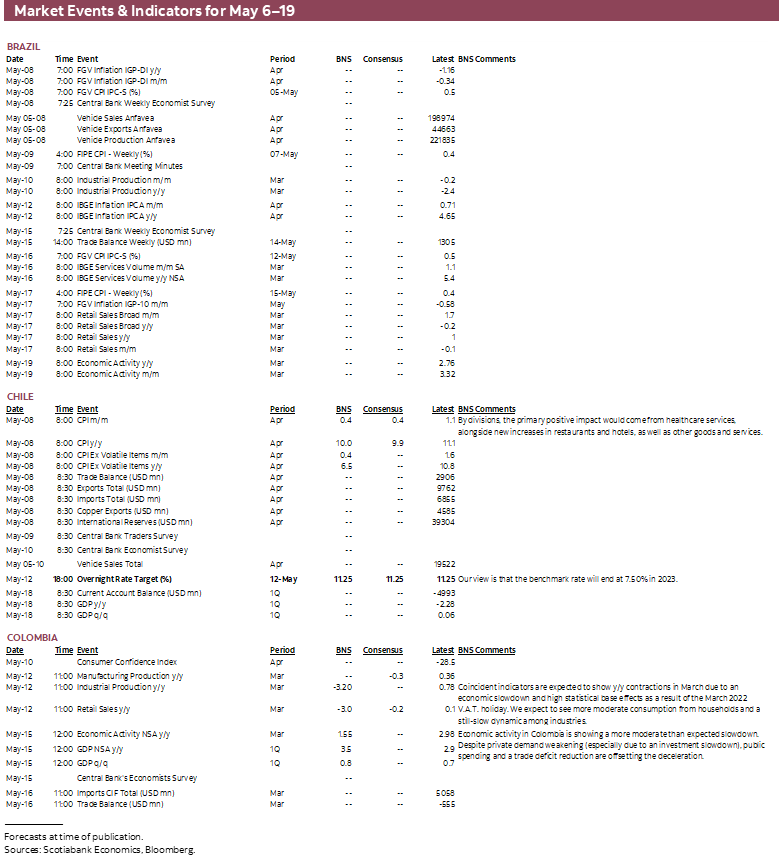

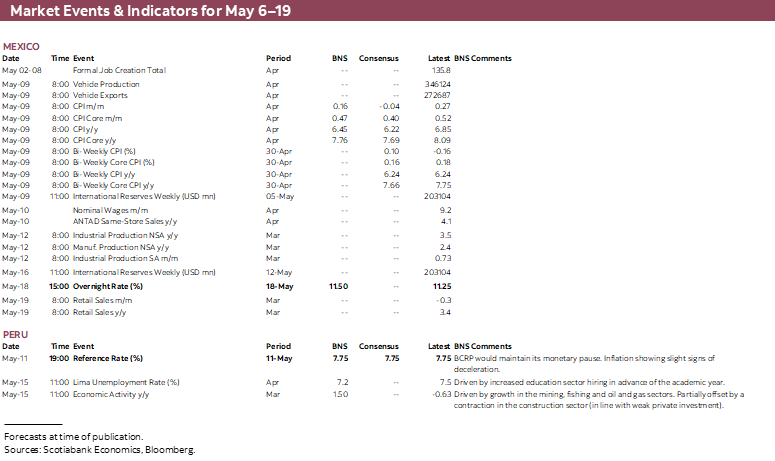

MARKET EVENTS & INDICATORS

- A comprehensive risk calendar with selected highlights for the period May 6–19 across the Pacific Alliance countries and Brazil.

ECONOMIC OVERVIEW: KEY LATAM AND US CPIs; PERU AND CHILE RATE DECISIONS

Juan Manuel Herrera, Senior Economist/Strategist

Scotiabank GBM

+44.207.826.5654

juanmanuel.herrera@scotiabank.com

- The week ahead presents a series of key CPI releases in the Latam region and in the US, as well as rate decisions in Peru and Chile where another pause is expected.

- Chile kicks off the week with inflation data for April that may hold to a thirteenth consecutive month in double-digits.

- Mexican and Brazilian prices data follows, with Banxico’s decision next week (hike or pause?) hinging on Tuesday’s release while the BCB faces a long campaign of pressure until its next announcement in June.

- Colombia’s calendar is quiet, in what is a welcome break by markets that have been troubled by another episode of political risks. The team discusses how markets may have learned to worry less about the tape bomb, but fiscal developments remain a must-watch.

The week ahead presents a series of key CPI releases in the Latam region and in the US, as well as important rate decisions in Peru and Chile—with their respective central banks set to once again leave their policy rates unchanged. While the broad global market mood will likely remain bound by developments in US markets around banking sector and debt ceiling risks, as well as the country’s inflation data on Wednesday, the weekly Latam calendar will also be key in shaping local yield curves and other markets as traders adjust their expectations for when the first rate cut may come in each of the key countries that we cover.

Chile kicks us off on Monday with April inflation data, seen at 10% y/y and, therefore, marking thirteen consecutive months in double-digits (just about). The headline figure is important to follow, but the BCCh may pay closer attention to the underlying baskets of the index; notably, the excl. volatile items gauge has show no clear signs of easing materially in the same way that headline has (with indexation practices partly to blame). The team in Santiago believes that the BCCh will stick to its guns at its policy announcement on Friday, leaving the overnight rate target at 11.25% but also leaving cut discussions until the June meeting—as they have guided. We’ll get a final look at the expectations of market participants ahead of the decision with the release of the BCCh’s Traders’ Survey on Tuesday.

With mid-April data already at hand, Mexico and Brazil publish full-month figures on Tuesday and Thursday, respectively. Economists project that Mexican core inflation decelerated once again in April, this time below 8% in line with the bi-weekly release, (7.75%) and with this confirmed in the full-month reading Banxico could build a case in favour of pausing next week (May 18). We think that the Fed’s 25bps hike as well as continued pressure in services prices tilt the balance of risks in favour of another increase—but a softer-than-expected April inflation figure would increase odds of a pause. Markets are well-convinced that Banxico is done hiking. Industrial production data out on Friday rounds out the local data calendar.

The BCB made a call last week to only slightly change its decision statement with a bit less hawkishness alongside an unchanged (and quite restrictive) policy rate of 13.75%. This was met with accusations by Pres Lula over the weekend that BCB president Campos Neto “is committed to the previous administration and those who benefit from high interest rates.” Reports that Lula is looking to slowly build in a dovish (and more open to rate-cutting) set of policymakers at the BCB will likely add to caution in Brazilian markets around the bank’s independence; the BCB looks set to provide limited heads-up before its first rate reduction. Headline inflation is expected to fall to the low-4s in this week’s IPCA release, placing additional pressure on the central bank to cut rates given a nearly double-digits real policy rate (using y/y inflation). But it will be a long wait with pressure from government, and maybe even markets and economic data, before the BCB’s next rate decision on June 21.

Peru’s data and events calendar presents little of note before closing with a bang on Thursday with the BCRP’s decision. It’s very much consensus that the central bank will pause once again, at 7.75%, but some slight optimism around the trend in inflation is building, though very slowly, and were this to continue, the BCRP would be looking to reduce rates in the final quarter of the year, as we anticipate. It’s too soon, still, for officials to sound the all-clear on inflation and message to markets that rate reductions could come soon. Our Lima team discusses the outlook for inflation in their BCRP’s preview in today’s Weekly.

Amid rate decisions and key data elsewhere in the region, Colombia stands out with a relatively quiet week ahead (though retail sales data on Friday are worth a look). It’s a welcome break for those in Colombian markets that have had to wrestle with political risks in the country owing to Petro’s cabinet shake-up as well as a rate hike in late-April that caught some by surprise. Our economists in Bogota discuss recent political and macro developments in the country in today’s report, with somewhat conflicting signals from recently-appointed FinMin Bonilla muddying fiscal expectations—though, on the whole, markets seem to be better equipped for dealing with political curveballs.

PACIFIC ALLIANCE COUNTRY UPDATES

Chile—Benchmark Rate Cuts Would be Assessed No Earlier Than June

Anibal Alarcón, Senior Economist

+56.2.2619.5465 (Chile)

anibal.alarcon@scotiabank.cl

On Monday, May 8, the INE will release April CPI data, for which we project an increase of 0.4% m/m (10% y/y), above the BCCh’s Financial Traders' Survey (0.3%), but in line with the BCCh’s Economic Expectations Survey and forward markets. By divisions, the main positive impact would come from healthcare services, to which would be added new increases in restaurants and hotels and other goods and services, all of them with relevant second round effects. Other divisions, such as transportation and food, would have a limited impact on the m/m CPI print.

On Friday, May 12, the Central Bank (BCCh) will hold its monetary policy meeting, with no changes expected in the reference rate, currently at 11.25%. In recent days, some members of the Board expressed that it will be necessary to cut the reference rate "as soon as possible", stating that the cuts will probably be assessed no earlier than the June meeting, conditional on an easing of annual inflation. Our view is that the benchmark rate will end 2023 at 7.5%.

Colombia—Fundamentals vs Bias: Has Something Changed in Colombia After the Political and Economic Surprises of the Past Few Weeks?

Sergio Olarte, Head Economist, Colombia

+57.601.745.6300 Ext. 9166 (Colombia)

sergio.olarte@scotiabankcolpatria.com

Jackeline Piraján, Senior Economist

+57.601.745.6300 Ext. 9400 (Colombia)

jackeline.pirajan@scotiabankcolpatria.com

Santiago Moreno, Economist

+57.601.745.6300 Ext. 1875 (Colombia)

santiago1.moreno@scotiabankcolpatria.com

The past few weeks have been full of unexpected events. President Petro reshuffled his cabinet, which included a change of finance minister. Additionally, the central bank delivered one more rate hike of 25 bps to 13.25%. In this context, markets faced a high volatility episode that interrupted the calm observed since April. Still, we think this period was different compared to prior episodes of volatility seen last year, and we think that it is associated with a learning process that we had in terms of how large the Colombian risk premium is, and after learning that the institutional framework of the country is solid and works.

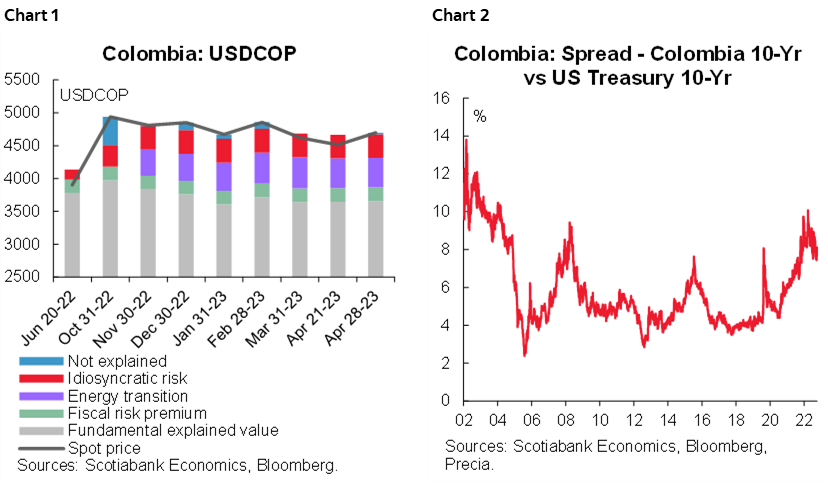

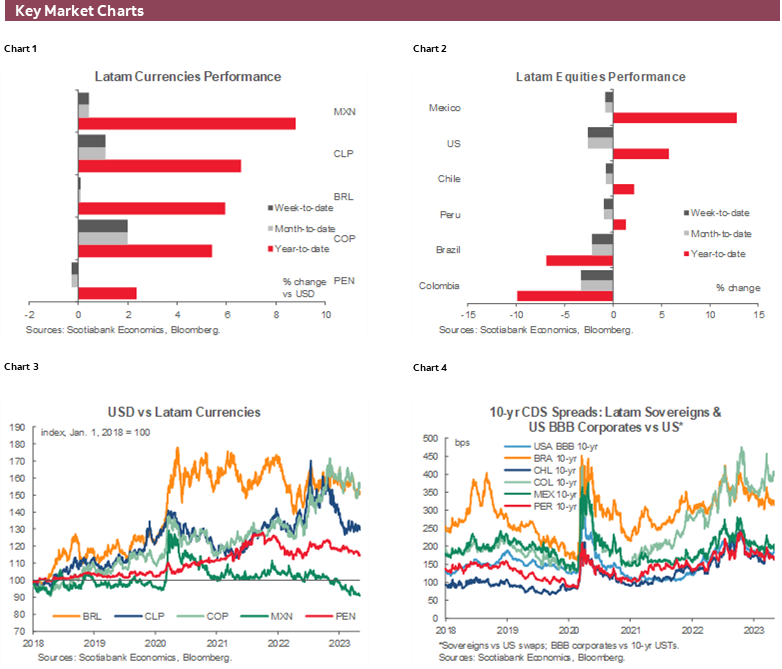

After the announcement of the cabinet changes, the USDCOP jumped from 4,526 to hover between 4600–4700 pesos, which according to our fundamental macro model, is more aligned with the traditional risk premium that Colombia has faced since the end of 2022 (chart 1). In the case of the COLTES market, the nominal curve cheapened by 30 bps. However, the risk premium vs. what happened in the volatility episode of October/November last year is lower (chart 2). We think there are two reasons behind this contained shock: i) we think markets realized that the institutional framework works and that the government is acting under appropriate rules; and ii) we are closer to the end of the hiking cycle in Colombia and the US, which signals that the economic cycle is in a different stage vs. October 2022.

On the political front, Minister Bonilla emphasized that the change in the leadership of the Ministry does not mean a change in its policy; in fact, he started his administration by increasing gasoline prices by 600 pesos, 200 pesos more than what had been usual with Ocampo (+400 pesos), sending a message of strong commitment to the fiscal rule and with the task of reducing the deficit in the oil prices stabilization fund. On the other hand, preliminary information suggests that the MinFin plans to increase the expected fiscal deficit for 2023 from 3.8% of GDP to 4.2% of GDP, which is still aligned with the fiscal rule but is open to weaker-than-expected oil prices that reduce the revenues expected from this sector. In that sense, the Director of Public Credit, Jose Roberto Acosta, said the nation will try to prefinance 2024. For now, Minister Bonilla has remarked that macroeconomic stability is a must in his administration. We think that the Medium-Term Fiscal Framework is now, more than ever, an essential publication. In fact, it will show the medium-term strategy of the current government, including more clarity about social policies since the National Development Plan is expected to be fully approved by this time.

In the macro world, the central bank delivered a new 25bps hike, unexpected in our case, but showing that the board is waiting for the right signal to pause; the right signal is the peak of inflation and at least the stability in inflation expectations by the end of 2023. Having said that, that Colombia’s policy rate is closer to the end of the hiking cycle remains our base case. The next meeting is June 30th, and we think by this time the board will have more information to start the pause with more confidence.

Peru—The BCRP to Keep Policy Rate Steady as it Awaits Downward Momentum on Prices

Guillermo Arbe, Head Economist, Peru

+51.1.211.6052 (Peru)

guillermo.arbe@scotiabank.com.pe

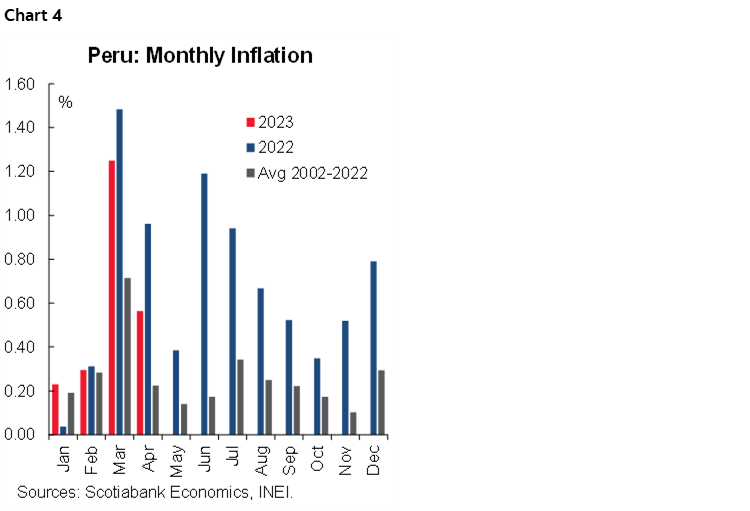

We are not especially unique in expecting the BCRP to hold the reference rate steady at 7.75% at its policy meeting next Thursday, May 11. The rate has been unchanged since January, and the mild decline in yearly inflation to just below 8.0% in April was not nearly enough to justify a reversal of policy. Not yet anyway. But trends are changing. All important inflation indicators are now clearly trending lower (chart 3). Wholesale inflation continues to plummet, and is now at 4.2%, the same level it was in early 2021 when the Producer Price Index first began alerting us that inflation would be rising. It has now come full circle and has been telling us for some time that headline inflation should begin declining.

Inflation expectations (12 months out) have been creeping lower for some time, and this broadly coincides with wholesale inflation pointing to the low 4% area as the zone where inflation appears to be heading. Core inflation has been much stickier, at 5.7%. Importantly, however, core inflation fell for the first time this year in April, joining other inflation indicators in starting to head in the right direction.

There is the feeling that the worst has passed, but that doesn’t mean that the future will necessarily be quick in coming. Inflation is still in the vicinity of 8.0% (7.97% to April, to be exact), very close to where it has been stuck over the past twelve months. The mild decline in inflation that has been taking place so far requires much more conviction before the BCRP will be moved to lower rates.

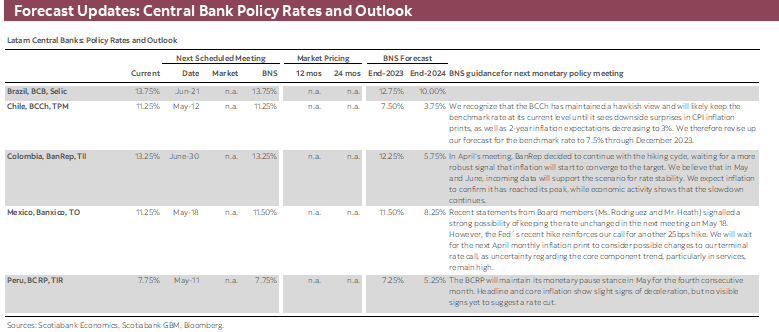

However, in terms of conviction, the next three months (May to July), are likely to prove very interesting, given base comparisons with 2022. Inflation in May is not likely to come in much lower than the 0.38% monthly inflation reading that took place in May 2022. The outlook is much more positive for June and July, however, as inflation was very high in these months in 2022 (chart 4). Inflation does not need to be near historical levels (as portrayed by the avg 2002–2022 figures) for inflation to plummet in the June–August period. Given our initial forecast of 0.38% monthly inflation for May, it will be more than enough for inflation to repeat the year-to-date monthly average of 0.58% in June–August, for yearly inflation to drop to a 6.6%–7.0% range by August. This is conservative, as we actually expect monthly inflation to be quite a bit lower going forward than it has been so far in the year. We maintain our forecast of 5.0% inflation for full-year 2023, which would require monthly inflation to be a feasible 0.33% from May through the end of the year.

We also maintain our expectation that the BCRP will maintain the reference rate at 7.75% through Q3, lower to 7.25% in Q4, and continue to do so until a level near 5.25% by the end of 2024. One issue that may make the BCRP be cautious about hurrying to begin lowering the reference rate is the growing expectation of an El Niño event in 2024, and the uncertainty it brings on prices.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Click here to be redirected |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.