ECONOMIC OVERVIEW

- A busy month-end (and start) awaits, chock full of central bank decisions in Latam and the G10 accompanied by key data around the globe and a flood of U.S. tariff announcements and possible last-minute deals.

- Rate cuts are expected only by the BCCh and BanRep while the BCB, BoC, Fed, and BoJ stay put. Chile will also publish several key sector readings over the week ahead of Friday’s monthly economic activity print.

- Mexico will join the U.S. in publishing 2Q GDP figures that should show the inverse effect of tariffs front-running during 1Q, which weighed on U.S. GDP yet support Mexican data—Eurozone data will likely show the same reversal, with Germany’s economy likely contracting during the quarter.

- In today’s report, the teams in Chile and Colombia provide updates on their respective countries’ fiscal developments, while the economists in Mexico discuss their latest forecast change for the MXN, outlining some structural shifts that have possibly weakened some long-held views.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Chile, Colombia and Mexico.

MARKET EVENTS & INDICATORS

- A comprehensive risk calendar with selected highlights for the period July 26–August 8 across the Pacific Alliance countries and Brazil.

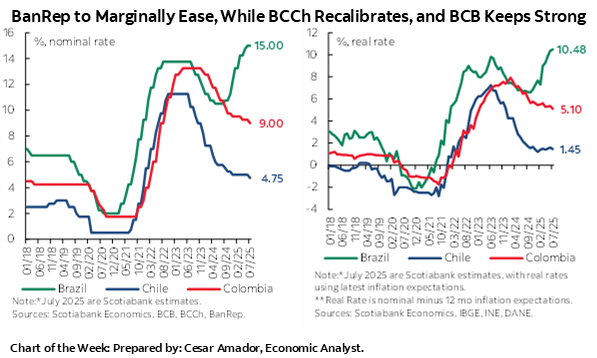

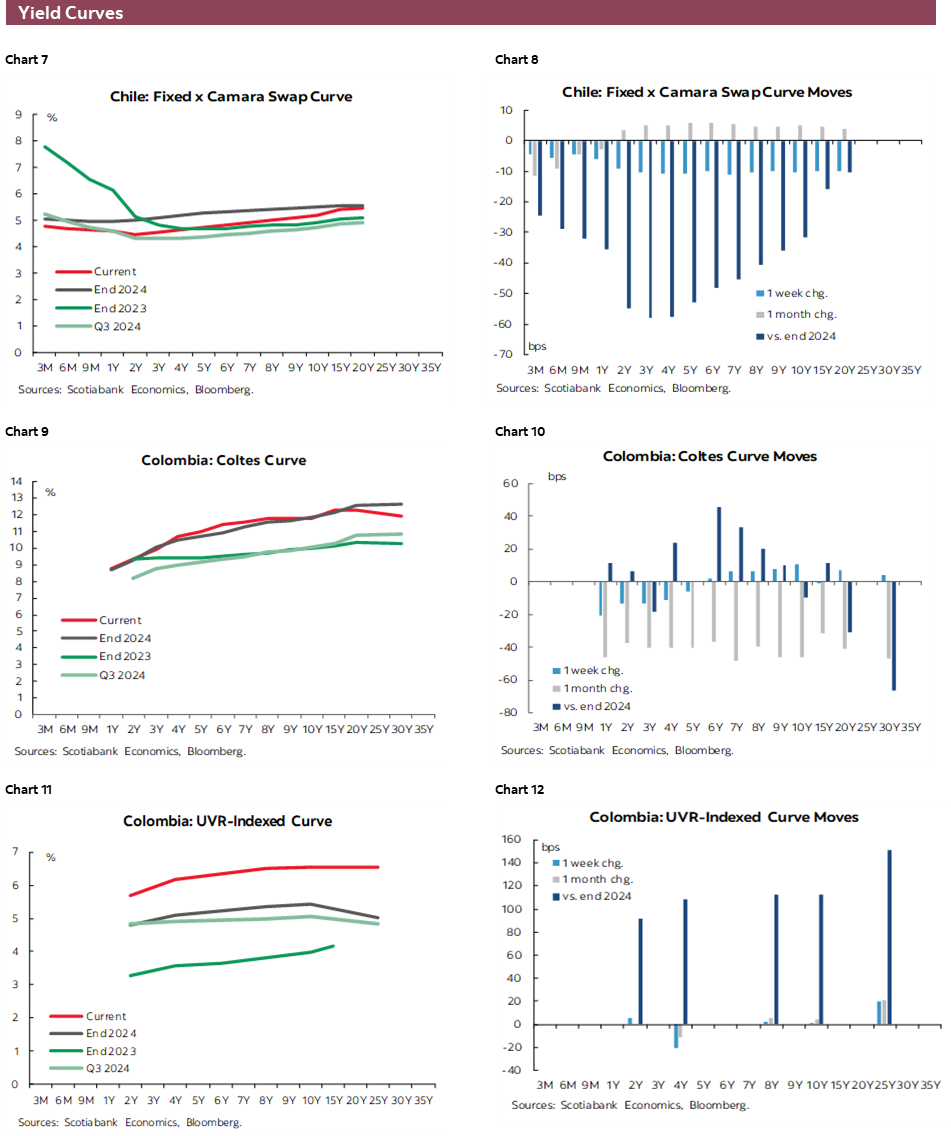

Chart of the Week

ECONOMIC OVERVIEW: POLICY RATES AND TARIFFS DECISIONS

Juan Manuel Herrera, Senior Economist

+52.55.2299.6675

juanmanuel.herrera@scotiabank.com

- A busy month-end (and start) awaits, chock full of central bank decisions in Latam and the G10 accompanied by key data around the globe and a flood of U.S. tariff announcements and possible last-minute deals.

- Rate cuts are expected only by the BCCh and BanRep while the BCB, BoC, Fed, and BoJ stay put. Chile will also publish several key sector readings over the week ahead of Friday’s monthly economic activity print.

- Mexico will join the U.S. in publishing 2Q GDP figures that should show the inverse effect of tariffs front-running during 1Q, which weighed on U.S. GDP yet support Mexican data—Eurozone data will likely show the same reversal, with Germany’s economy likely contracting during the quarter.

- In today’s report, the teams in Chile and Colombia provide updates on their respective countries’ fiscal developments, while the economists in Mexico discuss their latest forecast change for the MXN, outlining some structural shifts that have possibly weakened some long-held views.

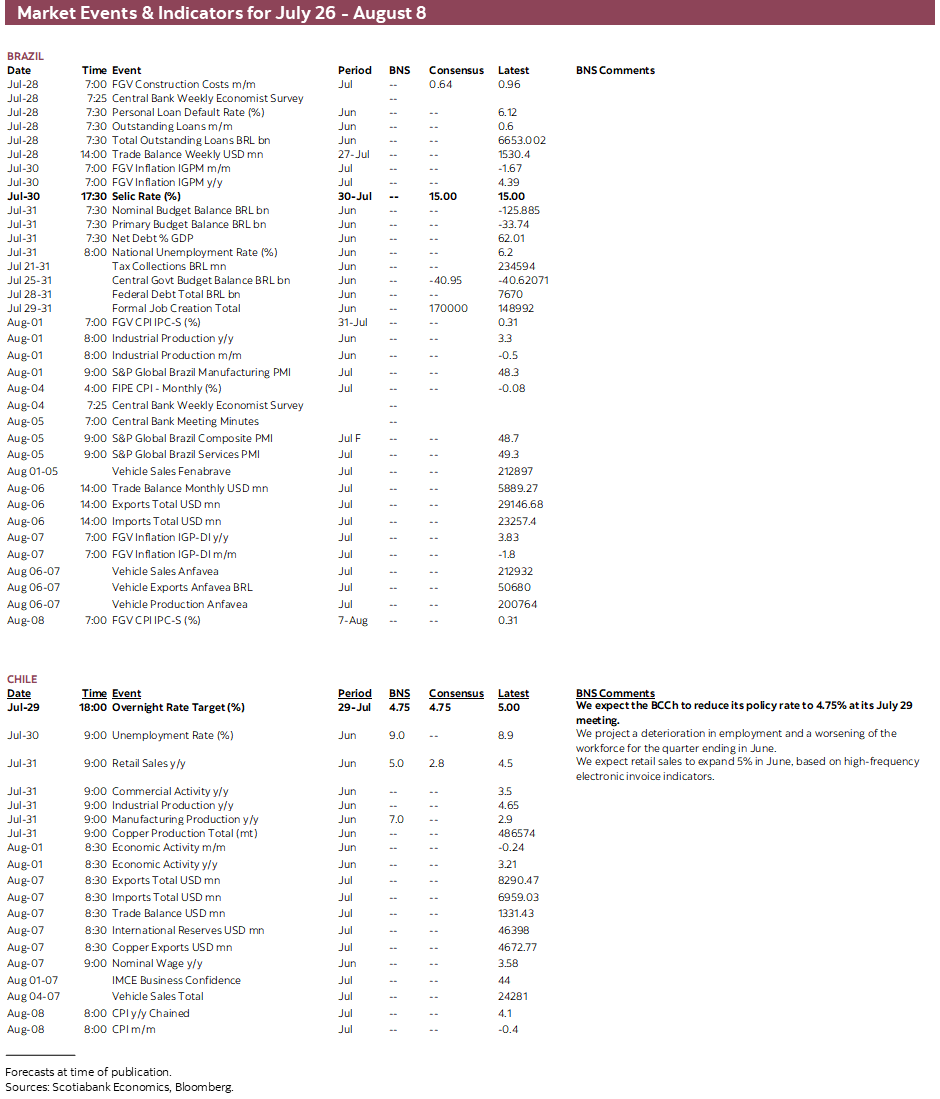

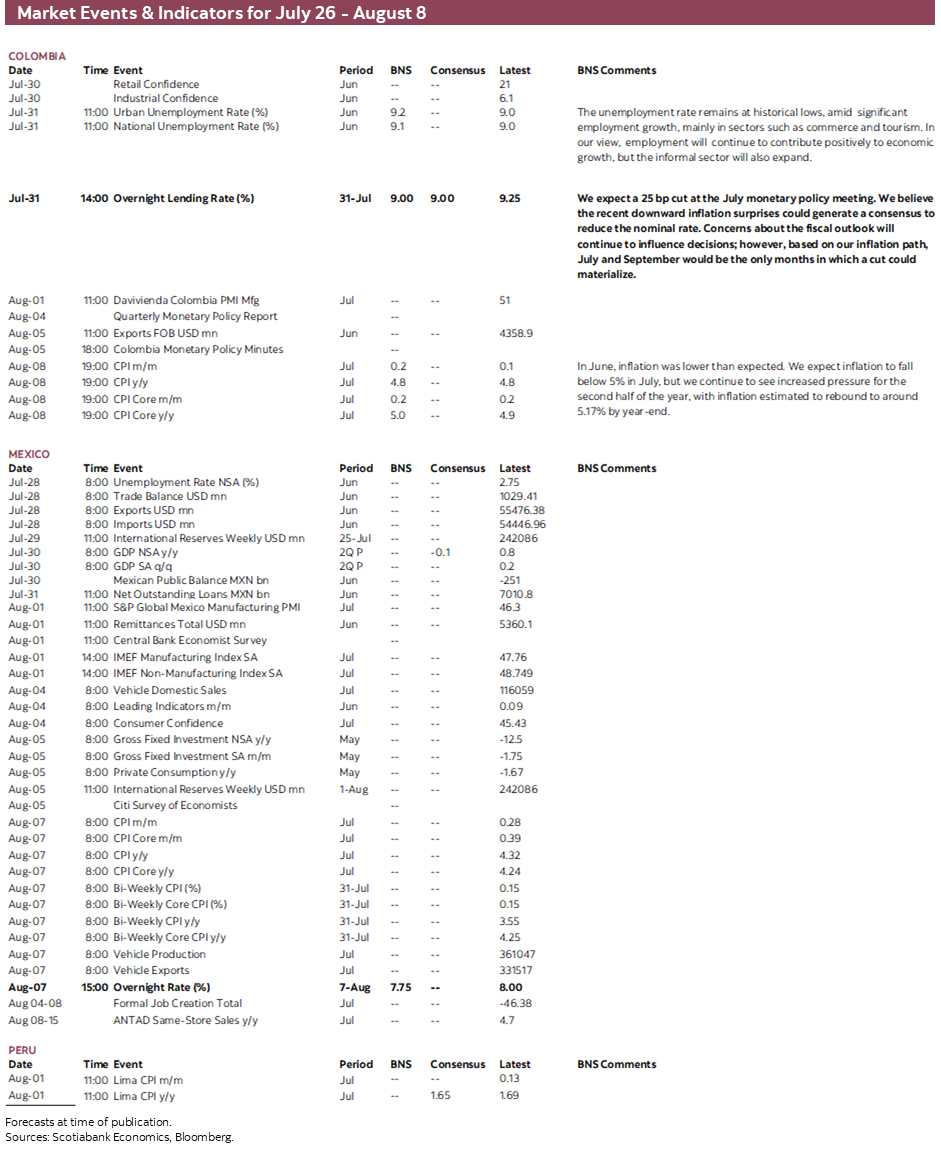

A busy month-end (and start) awaits, chock full of central bank decisions in Latam and the G10 accompanied by key data around the globe and a flood of U.S. tariff announcements and possible last-minute deals ahead of the scheduled August 1st duty hike. Most countries in Latam will have a busy few days ahead, while they look at Peru with envy as the country is closed for holidays on Monday and Tuesday. Peru does close the week with the release of July CPI, with another soft one in store based on our team’s tracking of prices that point to a monthly reading below historical averages.

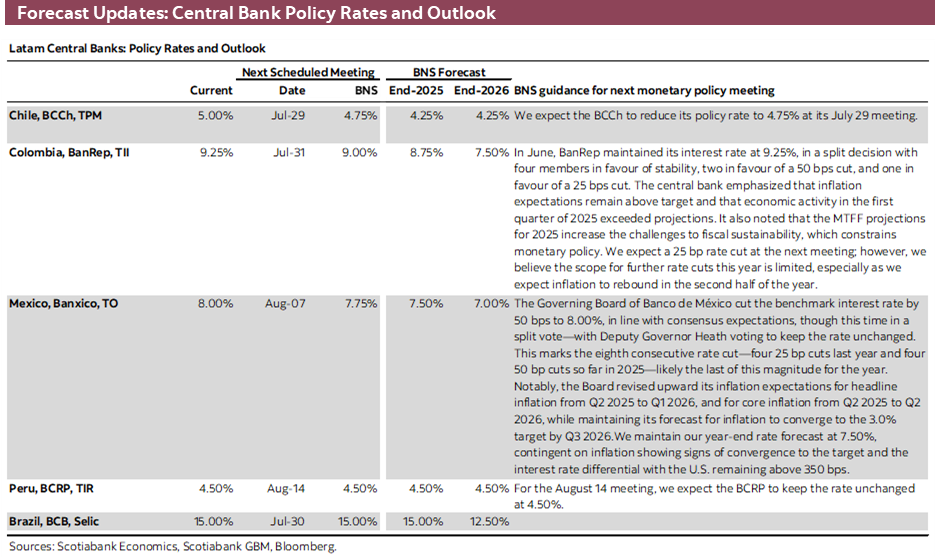

The BCCh kicks things off on Tuesday with a likely 25bps cut, returning to slight policy easing for the first time this year, followed by the BCB, Fed, and BoC who are all expected to leave their policy rates steady on Wednesday, as is the BoJ at its Thursday announcement with BanRep later that day expected to resume cuts with a 25bps move.

A busy Latam week ahead coincides with packed calendars abroad (more later) while global markets will also be on the edge of their seats regarding U.S. tariff decisions vis-à-vis Mexico, Canada, and the E.U. With only a week to go until the U.S. hikes tariffs on E.U. and Mexican goods to 30% (from 10% and 25%, with exemptions, currently) and to 35% on imports from Canada (from 25%, with exemptions), there are tentative signs that the White House may reach an agreement with the E.U. to only increase these duties to 15%.

However, U.S. trade discussions with Mexico and Canada seem to be going nowhere, likely resulting in these tariff hikes taking effect. Yet, note that USMCA exemptions have significantly lowered the effective duty rate on these countries compared to the headline 25%, with U.S. imports data as of May showing that Mexico ‘only’ faced a 4.3% effective duty rate while Canadian goods were only levied a 1.9% tariff. The tariff hikes would only lift these effective rates by a few decimal points. The biggest risk next week is not that higher rates kick in, but that the U.S. decides to narrow or remove exemptions for USMCA-compliant goods (85–90% of imports from the countries) or for the U.S.-share in Mexican/Canadian vehicles and key auto parts.

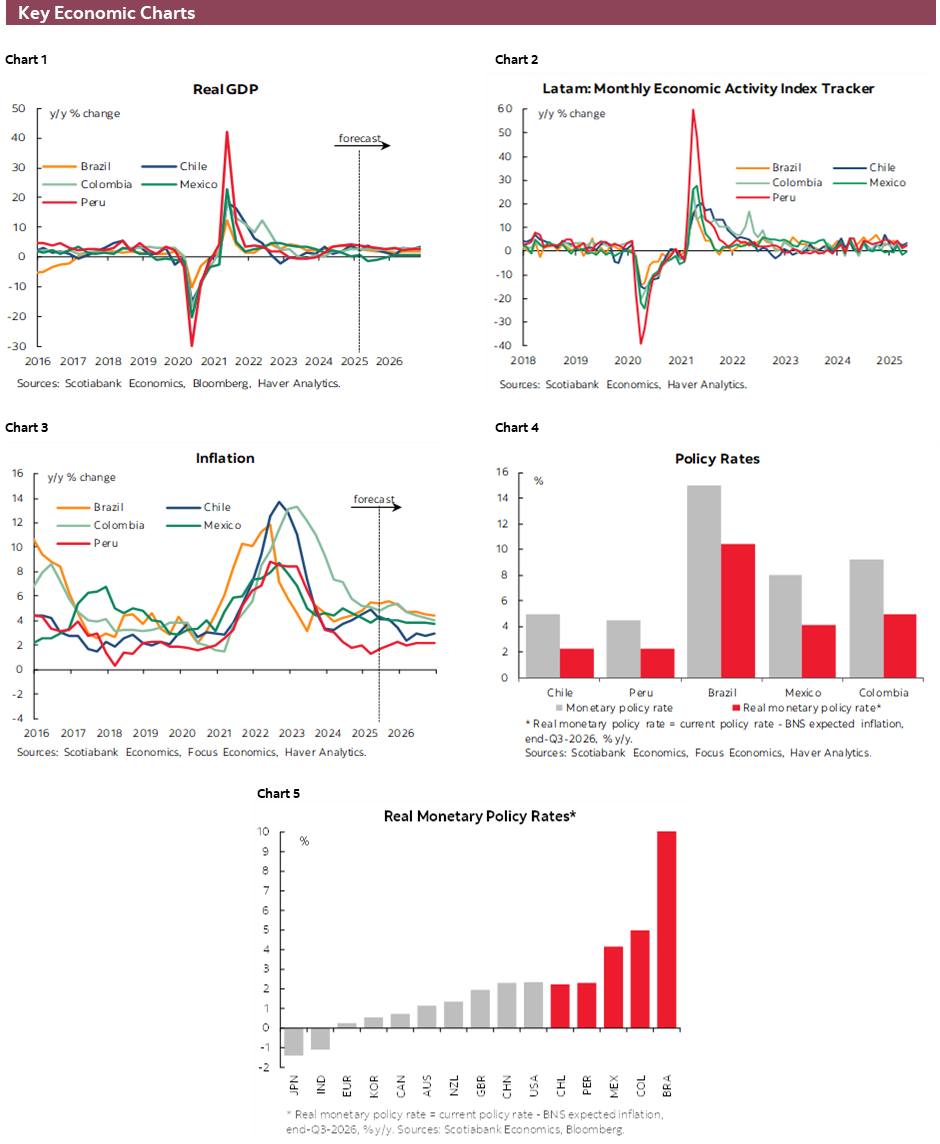

Turning to the broader Latam region, Chile has the busiest calendar of all, with the BCCh’s Tuesday announcement followed by unemployment rate figures on Wednesday, retail sales, industrial/copper production, and commercial activity readings on Thursday, and closing the week with June economic activity data to round it all up. Labour market data are expected to show another increase in the unemployment rate to hit the 9% level, but retail sales are estimated to have posted strong growth in June based on high-frequency payment indicators.

Chile’s central bank was looking on track to resume cuts at its June decision, yet heightened geopolitical risks on Israel-Iran’s conflict (and the U.S.) around the time of the meeting pushed the BCCh to err on the side of caution and instead hold. June’s inflation undershoot (see here), mostly as-expected economic data, and a retreat in international risks have clearly placed a rate cut back on the table next week. In today’s Weekly, the local team looks at the Ministry of Finance’s slight upward revision to its deficit projection for the year, despite lowering its outlook for public expenditures this year.

Staying on fiscal developments, our economists in Colombia include in today’s report an in-depth look at the government’s actions to turn around the worsening fiscal picture with a flurry of announcement of late perhaps taking away from structural issues in the country’s fiscal trends. The Ministry of Finance may be running out of room to manoeuvre given structural limits on tax revenues growth, paired with unwillingness to materially cut spending. Fiscal risks aside, Colombia’s central bank is due to announce a 25bps rate cut at its Thursday decision, according to the vast majority of economists, with an eye on recalibrating significantly restrictive monetary policy from the current target rate level of 9.25%. It is but a minor adjustment, and we’ll keep a close eye on the vote split as well as Gov Villar’s guidance as we think this will be the last (and only second) cut of 2025 with inflation expected to rebound slightly over the second half of 2025—then pushing into next year via indexation effects on prices and the minimum wage hike.

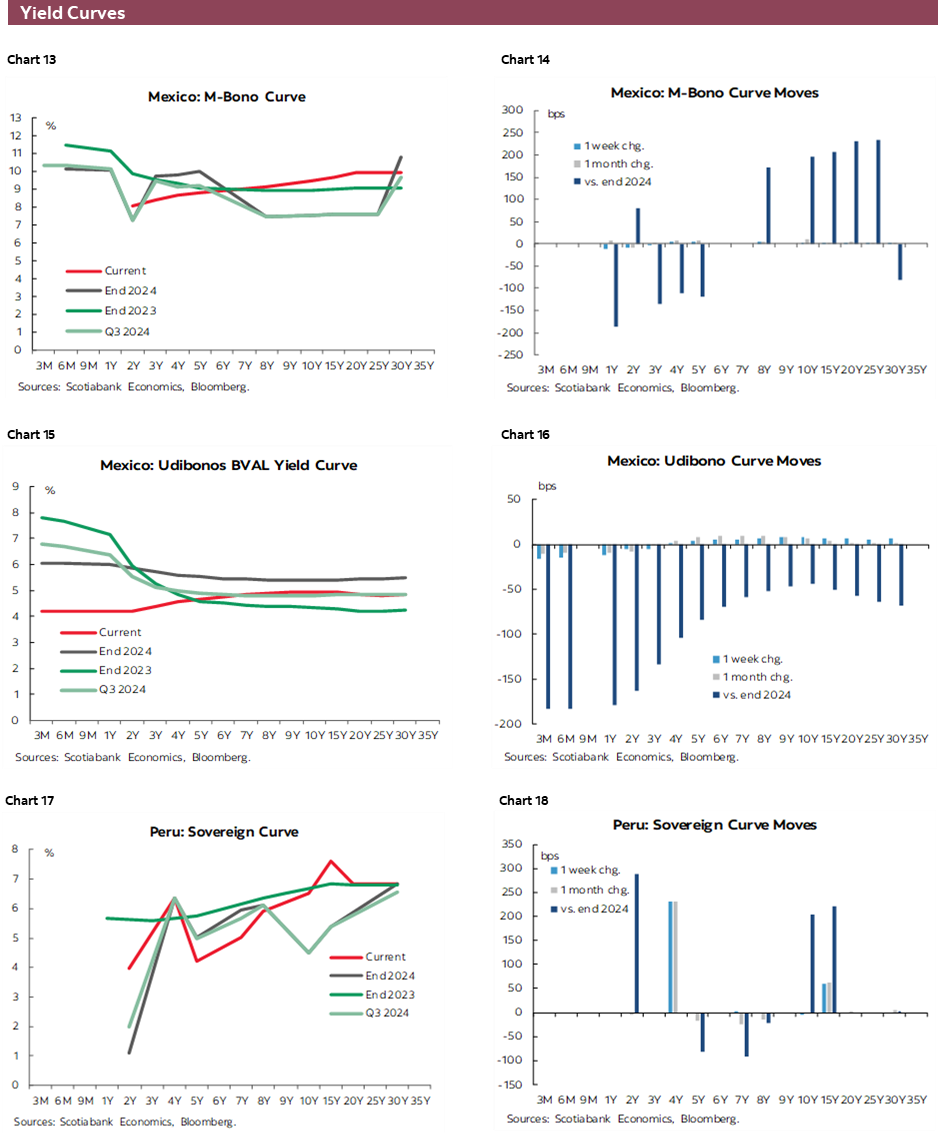

Mexico’s economy likely contracted in year-on-year terms in 2Q, following soft sub-1% growth in 1Q thanks to a rebound in the primary sector as well as the temporary support of tariffs front-running that masked muted underlying economic momentum that is seemingly worsening. Monthly economic activity figures showed that Mexican GDP contracted y/y in each of April and May by about 1% on average in non-seasonally adjusted terms, setting up a contraction for the quarter. The timing of Easter was a bit of a drag on industry-GDP given fewer working days in April 2025 vs April 2024, which one should be careful about when interpreting next week’s y/y NSA reading.

Still, the economy likely posted little to no growth in 2Q on a q/q seasonally-adjusted basis as guided by monthly data, and while next week’s figures only indicate activity at the three headline industries level, one can infer that seasonally adjusted m/m declines in exports in April and May will translate into a net trade drag on 2Q GDP from an expenditures standpoint. Monday’s international trade data for June will help refine expectations for the magnitude of this drag. Friday’s remittances data will be closely watched for a continued (possible) headwind of strict U.S. immigration policy, with foreign inflows coming off two months of large y/y declines of 12.1% and 4.6% in April and May, respectively. On the topic of Mexico’s external sector, our local economists discuss their latest revision to their USDMXN forecasts, digging into possible structural shifts for the MXN that have built some resilience into the peso throughout recent periods of USD strength or global uncertainty.

In the U.S. the Fed’s Wednesday statement will be important for traders, but with no cut expected and already plenty of guidance by officials pre-blackout the market will likely pay closer attention to Wednesday’s 2Q GDP release where a strong net trade rebound is expected. JOLTS vacancies Tuesday, Thursday PCE, and Friday’s nonfarm payrolls and unemployment figures will be key for shaping cuts pricing that is sticking to 40–45bps in implied reductions by year-end.

Elsewhere in the key economies, the Eurozone, Germany, France, Spain, and Italy all release 2Q GDP figures on Tuesday and Wednesday that are expected to show the inverse of the U.S.’s net trade rebound, with the currency bloc estimated to record zero growth for the quarter, with Germany forecast to have slightly contracted. On the heels of this week’s ECB decision, CPI data over Thursday and Friday at a country level and for the bloc as a whole will likely reinforce the bank’s steady stance with little change expected in headline and core inflation.

Canada also releases GDP data on Thursday, but only for May with loose industry-based guidance for June, to come after the BoC’s expected rate hold with new forecasts on Wednesday. Greater clarity on the tariff front thanks to a 15% tariff agreement with the U.S. has given the BoJ a better sense of what to expect for the months ahead, and in turn may help it bias its updated forecasts published alongside its Thursday rate announcement. It’s steady as she goes for now, and while a rate hike may come in 4Q, the BoJ remains sensitive to political anxiety, angsty domestic bond markets, and the possibility of fiscal stimulus, all making it difficult to pin down the timing of the next rate move.

PACIFIC ALLIANCE COUNTRY UPDATES

Chile—The MoF Again Raises This Year’s Projected Fiscal Deficit, While Reaffirming Its GDP Growth Projection of 2.5%

Anibal Alarcón, Senior Economist

+56.2.2619.5465 (Chile)

anibal.alarcon@scotiabank.cl

On Wednesday, July 23rd, the Ministry of Finance (MoF) published its quarterly Public Finance Report, corresponding to the second quarter of 2025. A key change from the previous report is the downward revision to fiscal expenditure growth for this year, which reduced from 2.6% in April to 2.2%. Regarding GDP, the main driver of the projected 2.5% economic growth for this year will be the resilience of domestic demand, which is projected to grow by 3.1% in 2025. Also, a strong performance of mining GDP is expected, in line with the positive outlook for investment in the sector. At Scotiabank Economics, we forecast GDP expansion by 2.5% in 2025 and 2026.

Regarding the effective fiscal deficit, the Ministry of Finance projects a deterioration to 1.4%–1.5% of GDP for 2025, compared to the projections in the first quarter Public Finance Report, due to lower-than-expected revenues. The structural fiscal deficit is also projected to widen to 1.8% of GDP (compared to 1.6% of GDP in the April projection), while gross public debt is expected to rise to 42.2% of GDP (Q1 projection: 42.3%). For 2026, the government’s fiscal commitment implies convergence to a structural fiscal deficit of 1.1% of GDP (consistent with an effective fiscal deficit of 0.8% of GDP), assuming a gross public debt level of 43% of GDP, below the prudent level defined by the authorities. The Ministry of Finance also projected negative fiscal slack through the next year.

Colombia—Structural Trends Behind the Financing Strategy

Jackeline Piraján, Head Economist, Colombia

+57.601.745.6300 Ext. 9400 (Colombia)

jackeline.pirajan@scotiabankcolpatria.com

Fiscal policy in Colombia has come under increasing scrutiny in recent years. Post-pandemic spending has become more rigid, while fiscal revenues have not recovered with the same momentum. In fact, during the first half of 2025, uncertainty surged as the fiscal projections presented in the February 2025 Financing Plan proved unreliable. This heightened anticipation around the release of the Medium-Term Fiscal Framework (MTFF) in mid-June.

When the MTFF was finally published, the government presented a more honest—though still-worrisome—view of the fiscal deficit. First, it openly acknowledged non-compliance with the fiscal rule and activated the escape clause for the 2025–2027 period. Second, it outlined an adjustment strategy that hinges on tax and spending reforms—measures that are politically and technically difficult to implement.

Curiously, the market’s main focus wasn’t on the fiscal risks themselves, but rather on the Financing Strategy, which quickly took center stage. The lack of clarity around this strategy has disrupted market pricing and hindered effective decision-making. From our perspective, the core issue remains structural and fiscal in nature—beyond the reach of any short-term financing manoeuvre. This document aims to cut through the noise and identify the underlying structural trends.

Thoughts on the Financing Strategy

Despite the erratic communication around the financing operations, it’s clear that Public Credit Director Javier Cuellar is focused on minimizing financing costs. At the heart of the strategy are conventional elements—such as favouring short- and medium-term issuances—based on the assumption that interest rates will decline in the future, allowing for longer-term debt extensions at lower costs.

However, Cuellar’s approach goes beyond traditional tactics, in which the reduction on the financing cost is a target for new issuances. Additionally, he has introduced an innovative repo operation aimed at reducing the cost of existing floating debt. This could potentially lower the interest burden by up to 0.5% of GDP—a modest impact considering projected interest expenditures of 4.7% of GDP in 2025 and 4.8% in 2026. Unfortunately, inconsistent messaging around the operation’s details has triggered volatility in both the COLTES and FX markets, probably undermining the intended benefits.

From what we understand, the Ministry of Finance (MoF) initiated the repo using disposable cash from its BanRep deposit account (DTN) to build collateral for a loan in Swiss francs. The proceeds are being used to construct a portfolio—potentially of COLTES or Global Bonds—designed to exploit rate differentials, as the Swiss franc loan is unhedged. The stated goal was to build a strategic reserve, though in practice, this reserve is not liquid but rather a managed portfolio.

So far, Cuellar has confirmed the purchase of approximately COP 5 trillion in COLTES, though it’s unclear whether Global Bonds have also been acquired. As market conditions have shifted, the expected payoff from the repo operation may no longer be as attractive, suggesting in our opinion a possible downscaling of the original plan. It’s also now clarified that this repo is not a financing source, as previously implied in the MTFF’s Sources and Uses chart. Instead, it serves liability management purposes, not cash buffer accumulation. Yet, the core issue that prompted the repo—Colombia’s weak cash position—remains unresolved, reinforcing our primary concern: fiscal risk.

Liability Management and Debt Metrics

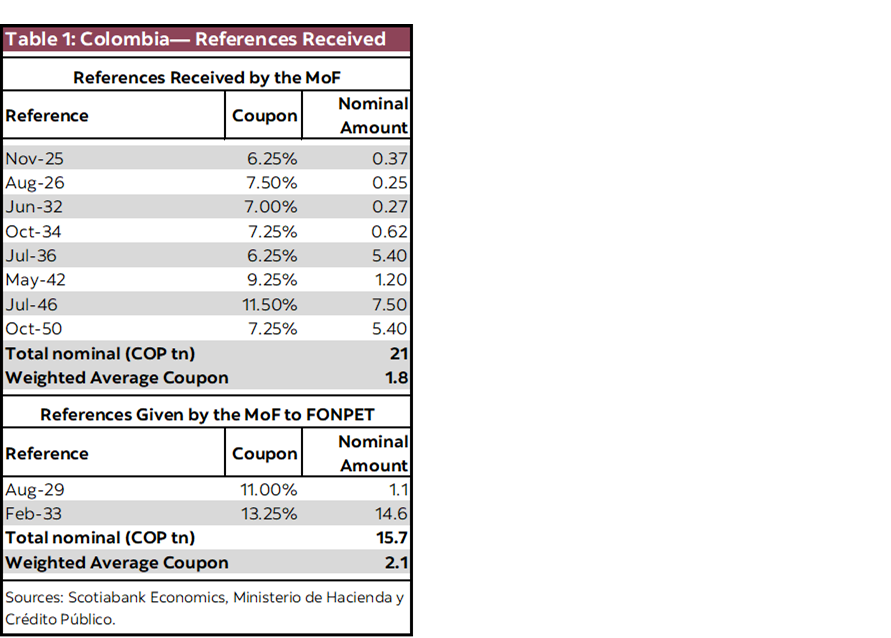

Cuellar’s liability management strategy also appears to be aimed at improving the debt-to-GDP ratio, which is calculated using the nominal value of outstanding debt rather than its cash equivalent. To this end, he has been actively retiring discounted bonds and replacing them with bonds closer to par. While this may improve the debt ratio on paper, it comes at the cost of higher interest payments due to elevated coupons.

This week, the MoF announced the use of funds from the Territorial Pension Fund (FONPET)—which are temporarily under government administration—to retire COP 21 trillion in COLTES (about 1.3% of GDP) with low single-digit coupons (table 1). These were exchanged for COLTES 2029 (11% coupon) and COLTES 2033 (13.25% coupon), totaling COP 15.7 trillion (around 0.85% of GDP). While this manoeuvre reduces the nominal debt-to-GDP ratio by approximately 0.3%, our calculations suggest it slightly increases the interest burden, however we recognize the MoF could see some benefits in terms of their cashflow requirement to pay interests in the short-term.

Returning to the Structural Issue: Colombia’s Fiscal Situation

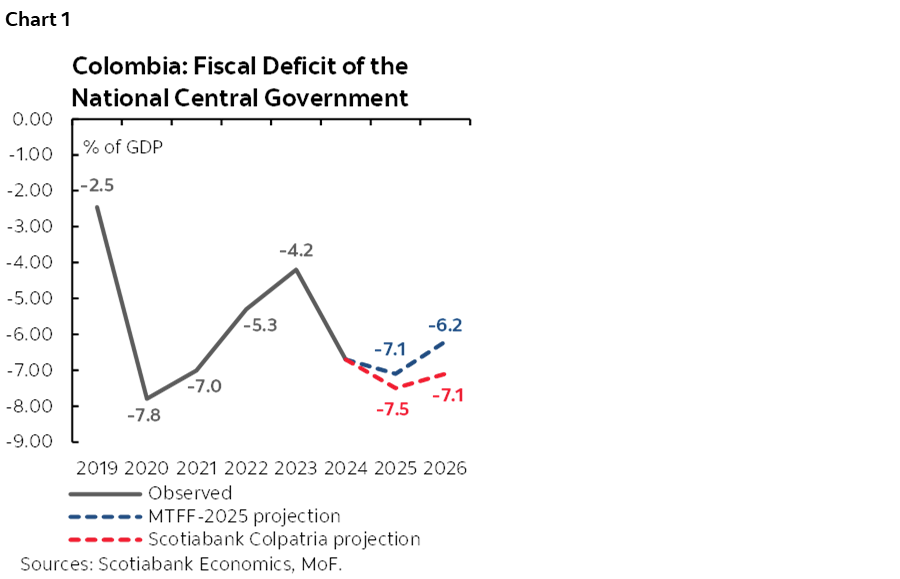

Colombia’s main fiscal challenge continues to be tax revenues falling short of expectations, coupled with a low political willingness to cut spending. Based on current dynamics, we believe that instead of a fiscal deficit of 7.1% of GDP in 2025, the actual figure could be 0.5 to 1 percentage points of GDP wider (chart 1). The likelihood of a tax reform as ambitious as the government envisions is low, which leads us to expect a deficit at least 1 percentage point higher than the 6.2% of GDP projected by the government. Looking ahead to 2027, we also see little chance of a significant correction toward a 4.9% of GDP deficit, as this would require a spending reform—something that has never been seriously discussed in Colombia.

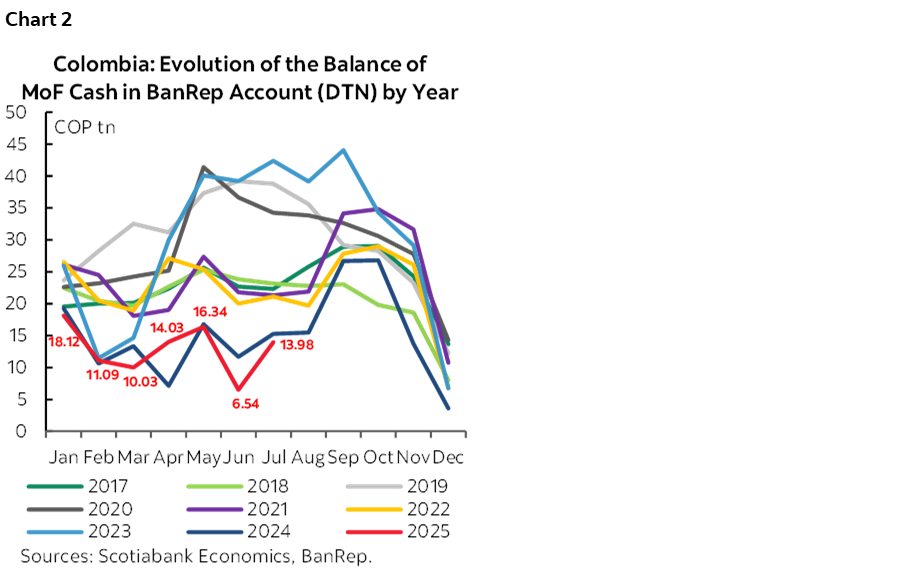

Against this backdrop, we’re seeing signs that the Ministry of Finance (MoF) is reaching the limits of its manoeuvring room, particularly in continuing to act as a net buyer of COLTES. The first sign is the low liquidity in the DTN account (chart 2), and the second is the announcement that FONPET funds have already been used for a major debt swap. The picture became clearer after Cuellar’s announcement on Monday regarding the issuance of two new nominal COLTES references, including one with a 33-year maturity (COLTES 2058). This issuance was not originally part of Cuellar’s plan but is now being considered due to the flattening of the yield curve—a result of the repo operation announcement and the MoF’s strong presence on the bid side.

The decision to return to markets with new references—especially one with such a long tenor—demonstrates that fiscal pressure is a force beyond any liability management strategy. The MoF is shifting its focus back to issuance, and markets are taking notice. As a result, the sharp flattening of the curve is beginning to reverse.

Overall, recent events show that pricing Colombia’s fiscal premium has become more complex, with noise surrounding both issuance decisions and liability management operations. At Scotiabank Colpatria, we believe the fiscal risk premium is currently concentrated in TCOs (Colombia’s equivalent of T-bills), as well as in the short and belly segments of the curve, which have been the MoF’s preferred issuance points. However, with Cuellar now signaling a return to the long end of the curve, we believe the fiscal premium could begin to reappear there as well.

As of Friday, July 25th, we’re seeing a cleaner dynamic in the COLTES market. The MoF appears to be losing its ability to intervene as actively as in previous weeks, and rates are beginning to better reflect the underlying fiscal premium. Looking ahead to next week’s issuance, we estimate that the coupon for the COLTES 2058 could range between 10 to 15 bps above the yield of the COLTES 2050 refence (according with current levels ~12.10%), depending on how markets price in the reality that Colombia’s structural fiscal challenges are constraining the MoF’s flexibility.

Mexico—Revising Our MXN Forecast, and Questioning Widespread Assumptions

Eduardo Suárez, VP, Latin America Economics

+52.55.9179.5174 (Mexico)

esuarezm@scotiabank.com.mx

- Revising our USD/MXN forecasts to 20.30.

- USD/MXN seemed to have a structural shift in its behaviour around the start of the pandemic, with a departure of more aggressive hedgers from the m-bono market.

- Foreign investors departed at a very fortunate time for MXN, with their outflows being offset by a massive and atypical trade surplus being recorded.

- Banxico’s rate hikes, combined with departure of active hedgers to increase MXN’s attractiveness from a carry-vol perspective. Is that changing?

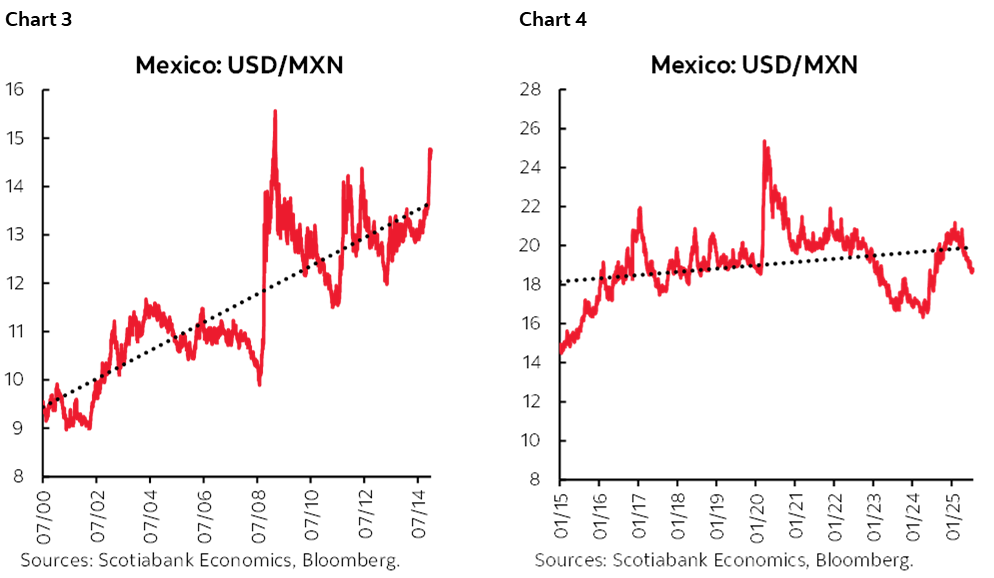

Outside of 3–4 episodes, USD/MXN has been bound by a 17.50–21.50 range since 2015. The slope of simple regression went from roughly 4–5% depreciation per year in 2000–2015, to a roughly flat slope since. Interestingly, the more stable MXN has come in a period where foreign investments in Mexico have not been particularly robust, especially on the portfolio front (charts 3 and 4).

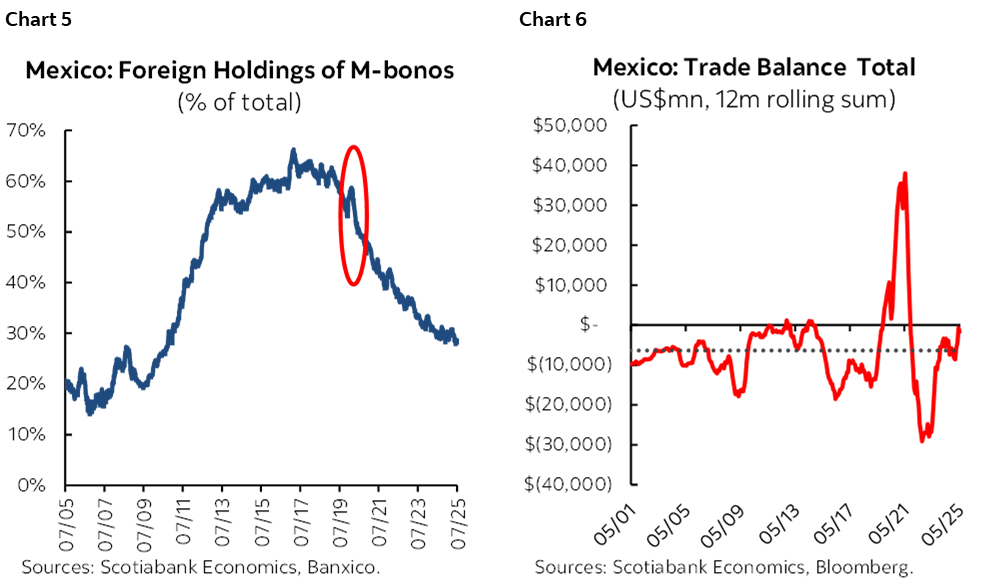

Looking back at the data, it appears that in 2018–2022 the MXN had a structural break in its dynamics. A large share of the “exit of foreign holders” coincided with a very unusual reversal in Mexico’s quasi-permanent trade deficit. Over the past 25 years, Mexico’s trade balance has averaged -US$500mn (a deficit), whereas in June–December of 2020, when the auto sector “re-opened” during the Covid-19 pandemic, and the US introduced aggressive stimulus, whereas Mexico was fiscally austere, the trade balance recorded a monthly average trade balance of US$5.3bn—which essentially absorbed US$37bn of portfolio outflows, negating the adverse impact these would have had on MXN (charts 5 and 6).

To understand the impact of the reduction of foreign holders on MXN’s dynamics it’s relevant to consider the type of investor that left, and that which stayed. At peak, foreigners held about 2/3 of outstanding m-bonos, with those holdings roughly split into 3 equal sized buckets (according to our estimates).

- Crossovers: Un-benchmarked money that has mostly left. Not having MXN as part of their mandate, these investors tended to be strong buyers of USD/MXN when uncertainty rose, which not only hit the peso in these episodes, but also added to the peso’s volatility.

- Local EM FX Benchmarked: roughly 1/3 of foreign investors in m-bonos (about 20% of the total at peak) were benchmarked to EM local currency benchmarks (GBI EM, ELMI+, etc), which mostly have MXN as part of their mandates. Although this tends to be active money, their aggressiveness in hedging tends to be lower due to 2 factors: 1) MXN is part of the benchmark, which gives them tolerance for its moves, 2) “benchmark hugging”. Our estimates suggest about half of this money is gone, but more due to a loss of favour of the broader EM asset class, rather than Mexico specific factors. However, these types of investors tend to generate less volatility than the bucket above.

- DM Index Benchmarked: the last bucket corresponds to investors whose benchmarks are DM indices, which tend to have restrictions on investing in non-investment grade countries. Mexico retains its investment grade, and its weighting in major benchmarks has not changed materially. Our estimates suggest most of this money is still there. A large share of the money behind these indices is passive money, and hence hedging by these investors is not an issue for MXN.

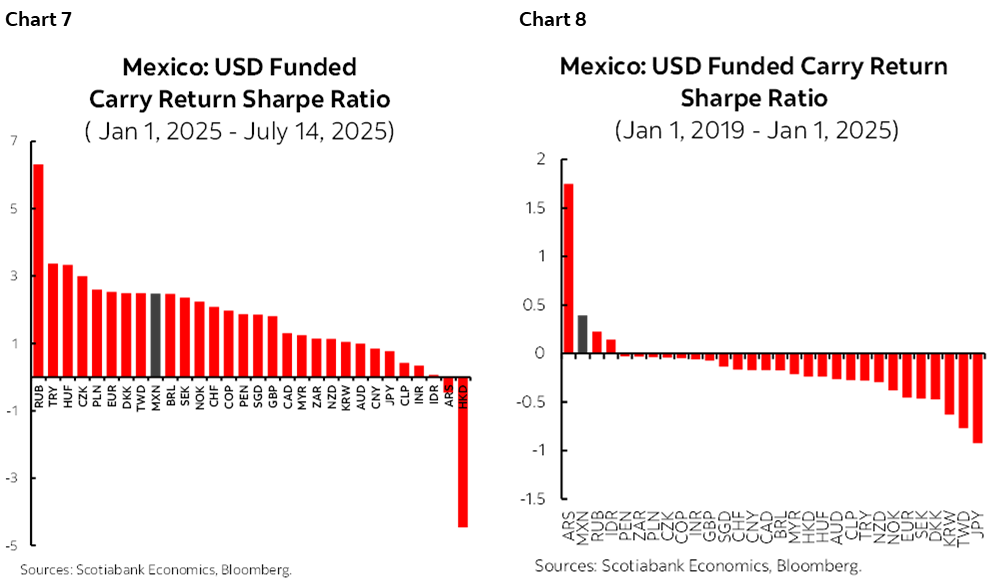

The large reductions in active hedgers in the foreign holders of m-bonos reduced the volatility of the peso. In addition, following the pandemic in 2021, Banxico started an aggressive rate hike cycle that saw the overnight rate rise from 4.00% to 11.25%. As a result, the peso’s carry-to-vol ratio became the second most attractive among the 32 most liquid FX globally. The carry-to-vol ratio is frequently a strong factor explaining FX performance, and in the peso’s case, we argue that it’s among the major drivers of its strong performance and seeming change in traditional behaviour. A key question is whether Banxico’s material cuts this year have eroded the peso’s anchors (charts 7 and 8).

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Click here to be redirected |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.