FORECAST UPDATES

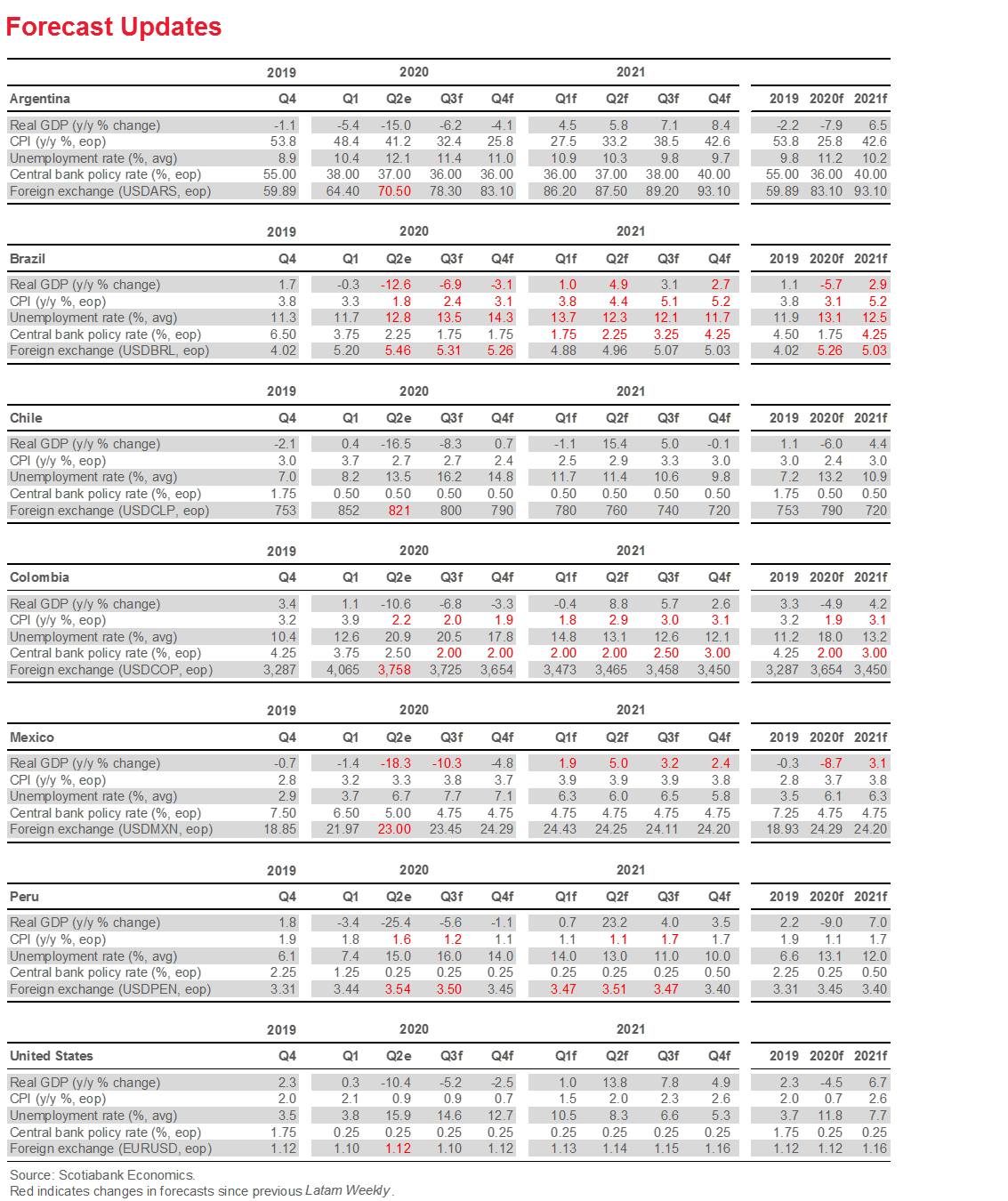

The depth and breadth of the ongoing COVID-19 pandemic in Brazil, the uneven policy response, and recent data have prompted a major overhaul of our forecasts, which now feature lower growth, weaker inflation, and higher unemployment. Softer inflation in Colombia and the latest communications from the BanRep have moved our team in Bogota to cut its forecast for the terminal monetary policy rate by -50 bps from 2.50% to 2.00%. Growth in Mexico is now expected to be a touch weaker in 2020, followed by a stronger rebound in 2021.

ECONOMIC OVERVIEW

As the COVID-19 pandemic remains entrenched, economic conditions are shifting in Latam. Activity is rising as quarantines ease, but tight lockdown conditions have been re-imposed where COVID-19 cases have surged. Stop-start, step-wise recoveries lie ahead for the Latam-6.

MARKETS REPORT

Our teams in Santiago and New York look at the possible market implications of proposed reforms to Chile’s private pension funds.

COUNTRY UPDATES

Concise analysis of recent developments and guides to the fortnight ahead in the Latam-6: Argentina, Brazil, Chile, Colombia, Mexico, and Peru.

MARKET EVENTS & INDICATORS

Risk calendar with selected highlights for the period July 11–July 24 across our six major Latam economies.

Economic Overview: Coping with a Chronic Condition

Brett House, VP & Deputy Chief Economist

416.863.7463

Scotiabank Economics

brett.house@scotiabank.com

COVID-19 is becoming a chronic condition in Latam, with little prospect that the pandemic will be imminently brought under control.

Our country teams continue to incorporate a bit more softness into their forecasts for the Latam-6 economies in 2020, with revisions this week in Brazil, Colombia, and Mexico.

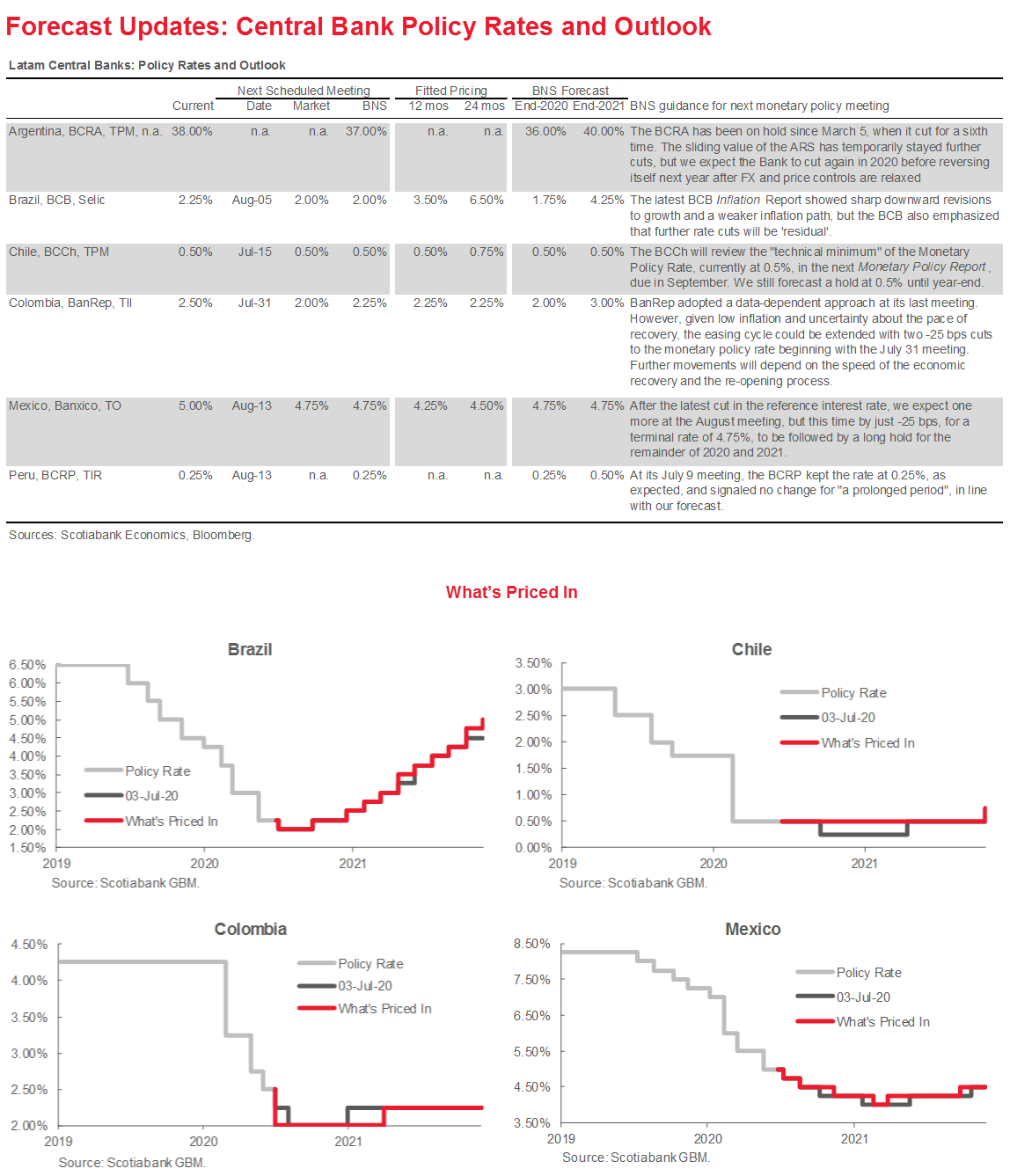

Monetary policy is set to continue easing across the region, but Chile’s BCCh is expected to keep rates on hold at its July 15 meeting and maintain the option of invoking unconventional measures, if needed.

MARKETS PRICING MORE MONETARY EASING

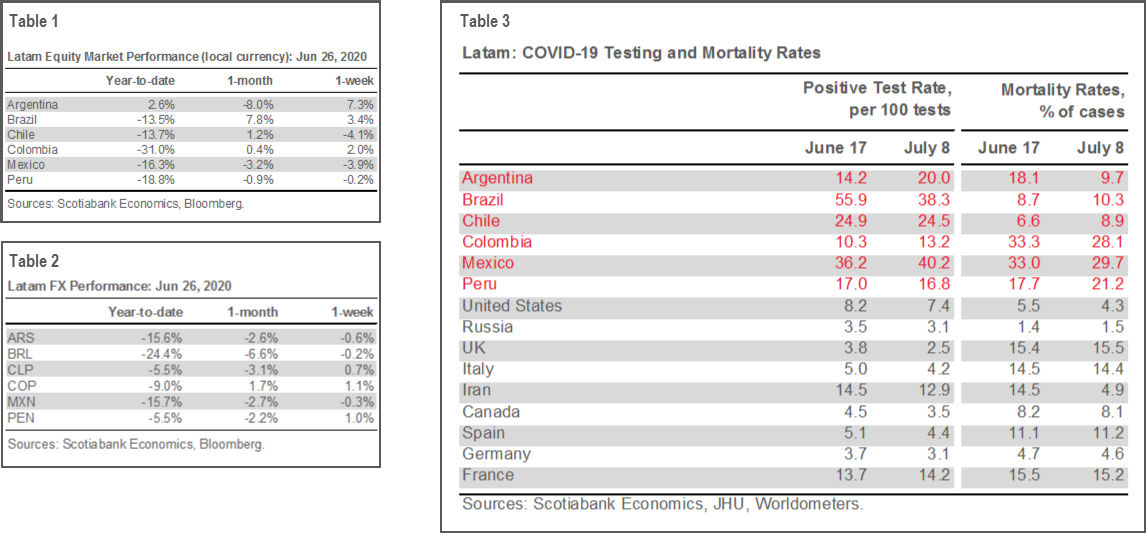

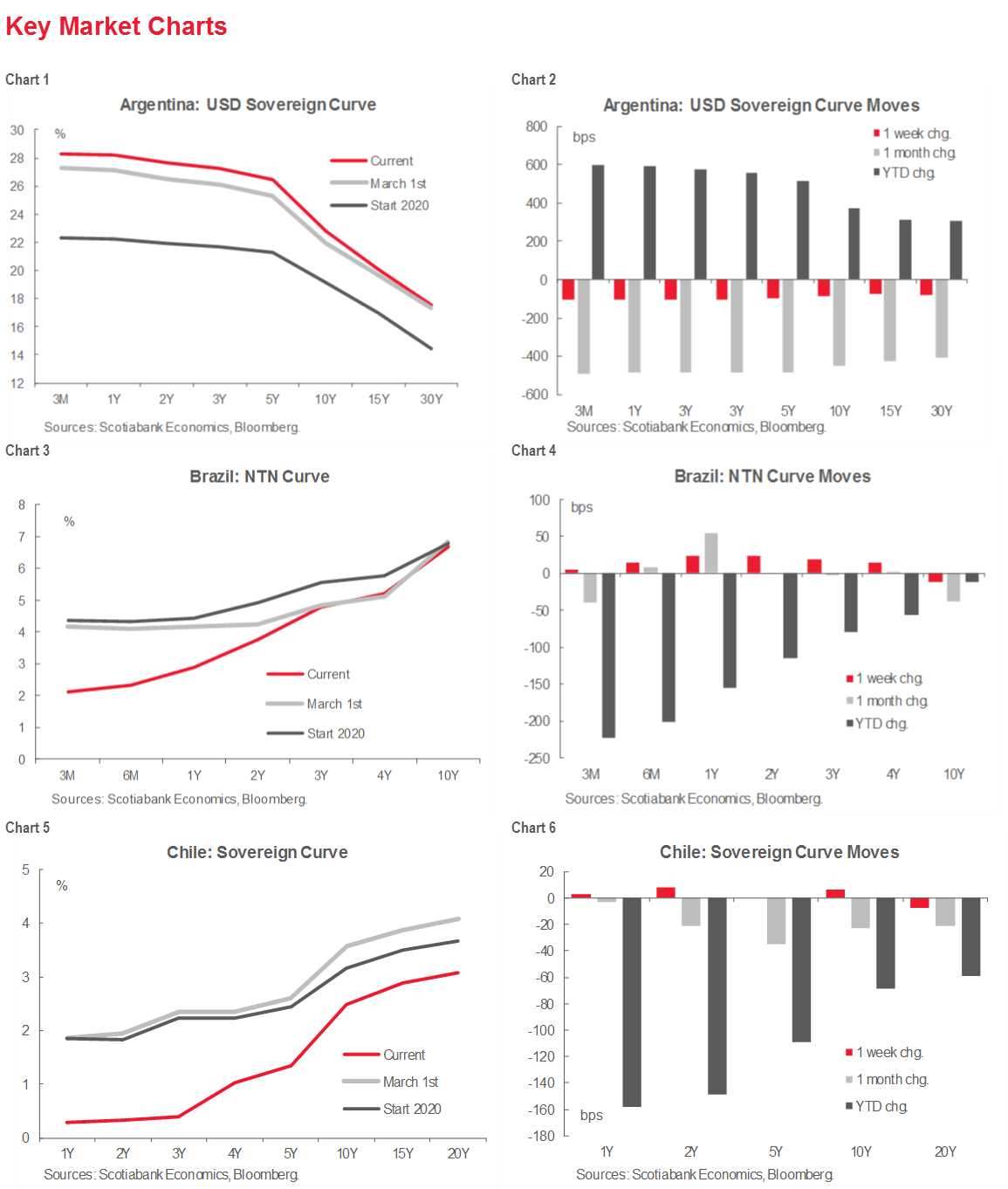

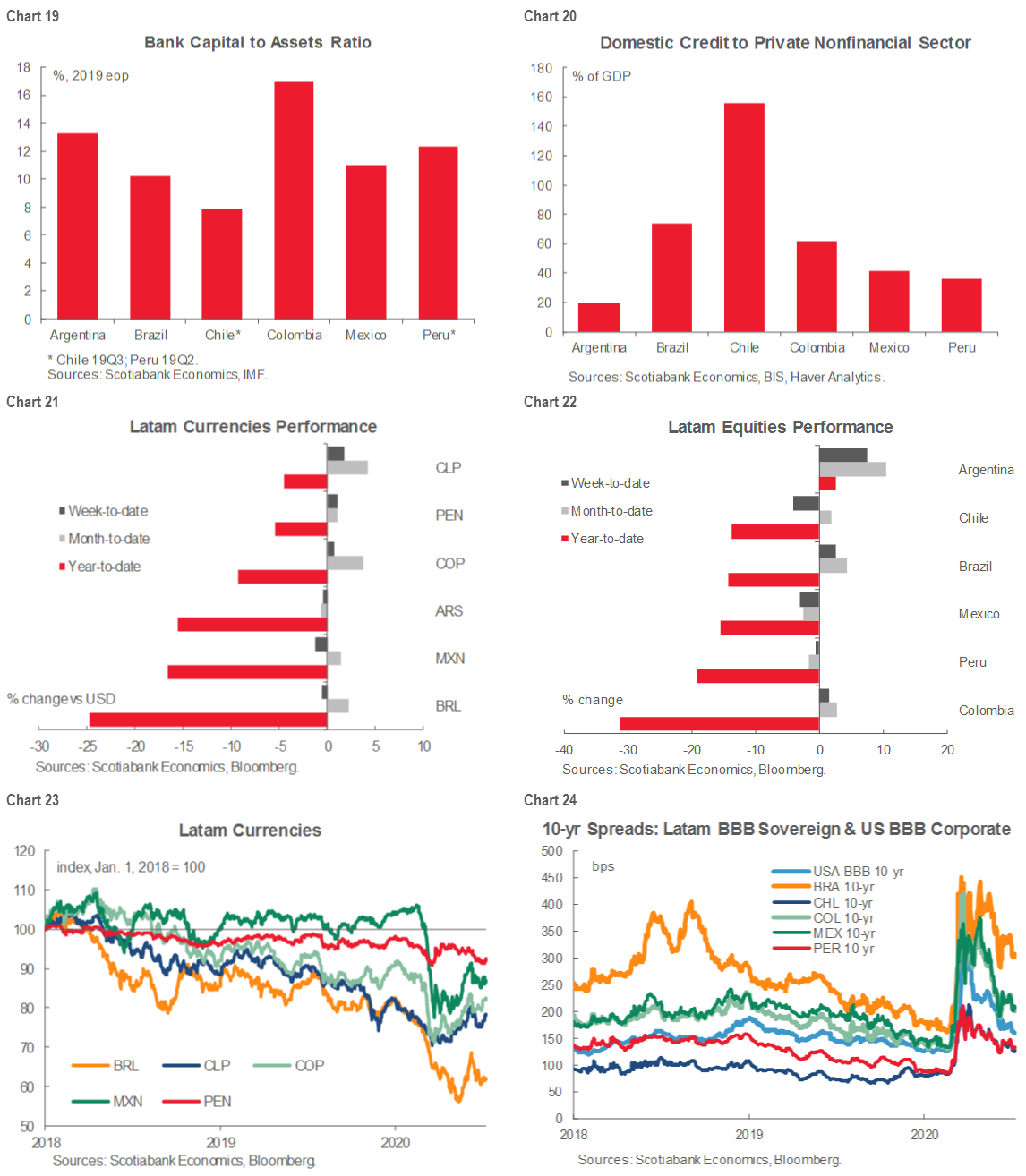

In a week of mixed international risk sentiment all three major US equity indices managed to post net gains, but Latam markets tended to reflect country-specific developments. Traders shook off Pres. Trump’s announcement that a Phase 2 trade deal with China is now unlikely. Equities ended the week up in Argentina (table 1)on the release of a richer debt restructuring offer from its authorities, while Chile saw the biggest week-on-week losses in response to the increase in COVID-19 cases in greater Santiago and the extension of lockdown measures in the capital region. Mexican equities also suffered as June inflation surprised again on the upside while May industrial production came in weaker than expected. FX markets were quieter (table 2), with commodity prices providing a small lift to the COP and PEN.

In rates, markets priced out another cut from Chile’s BCCh, but stuck to their expectations of more monetary policy easing from the central banks in Brazil, Colombia, and Mexico (see What’s Priced In, p. 4).

Brazil. Markets still expect the easing cycle to reach its bottom with a -25 bps cut in the Selic to 2.00% at the next Copom meeting in August, but our Brazil economist sees the BCB going one -25 bps cut further to 1.75% in September.

Chile. In June, markets began pricing a further -25 bps cut from Chile’s BCCh that would take its monetary policy rate below its so-called “technical minimum” of 0.5% to 0.25% in September. The move followed an announcement that the central bank would be reassessing whether 0.5% truly is the policy rate’s lower bound. This analysis is still due to be published in the BCCh’s September Monetary Policy Report, but markets have reverted to expecting the policy rate to stay on hold at 0.5% until end-2021 as Congress advances toward enabling the BCCh to purchase an expanded range of assets.

Colombia. In Colombia, the swap curve continues to price a terminal level for the intervention rate at 2.00%. While the market has moved over the past week to pricing a -50 bps cut at the next meeting on July 31, our team in Bogota believes the split decision at the most recent meeting implies “gradualism” remains the name of BanRep’s game and the move to 2.00% will be implemented through two -25 bps cuts, one at each of the next two meetings.

Mexico. Swap markets continue to price a terminal rate of 4.00% for Banxico’s easing cycle, to be delivered through 4 x -25 bps cuts. But compared with last week, markets now expect the last two cuts to be delivered slightly more gradually. In contrast, our team in CDMX expects Banxico to hold its target rate at 4.75% for the remainder of 2020 and all of 2021 following a last -25 bps cut at its next meeting in August. Mexico’s recent inflation surprises tilt toward their view.

INFLECTION MOMENT: WHEN COVID-19 BECOMES CHRONIC

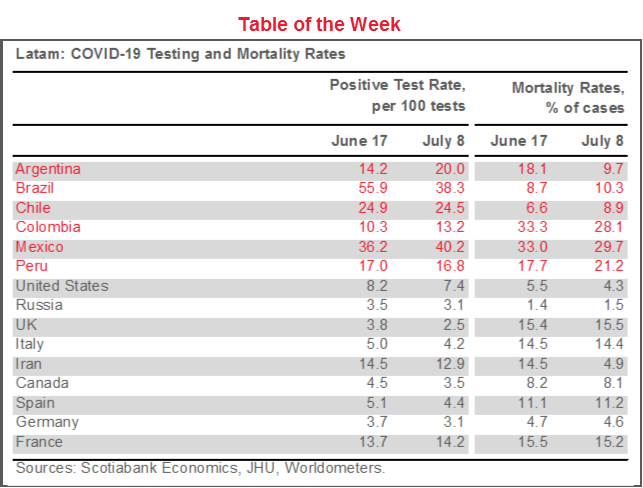

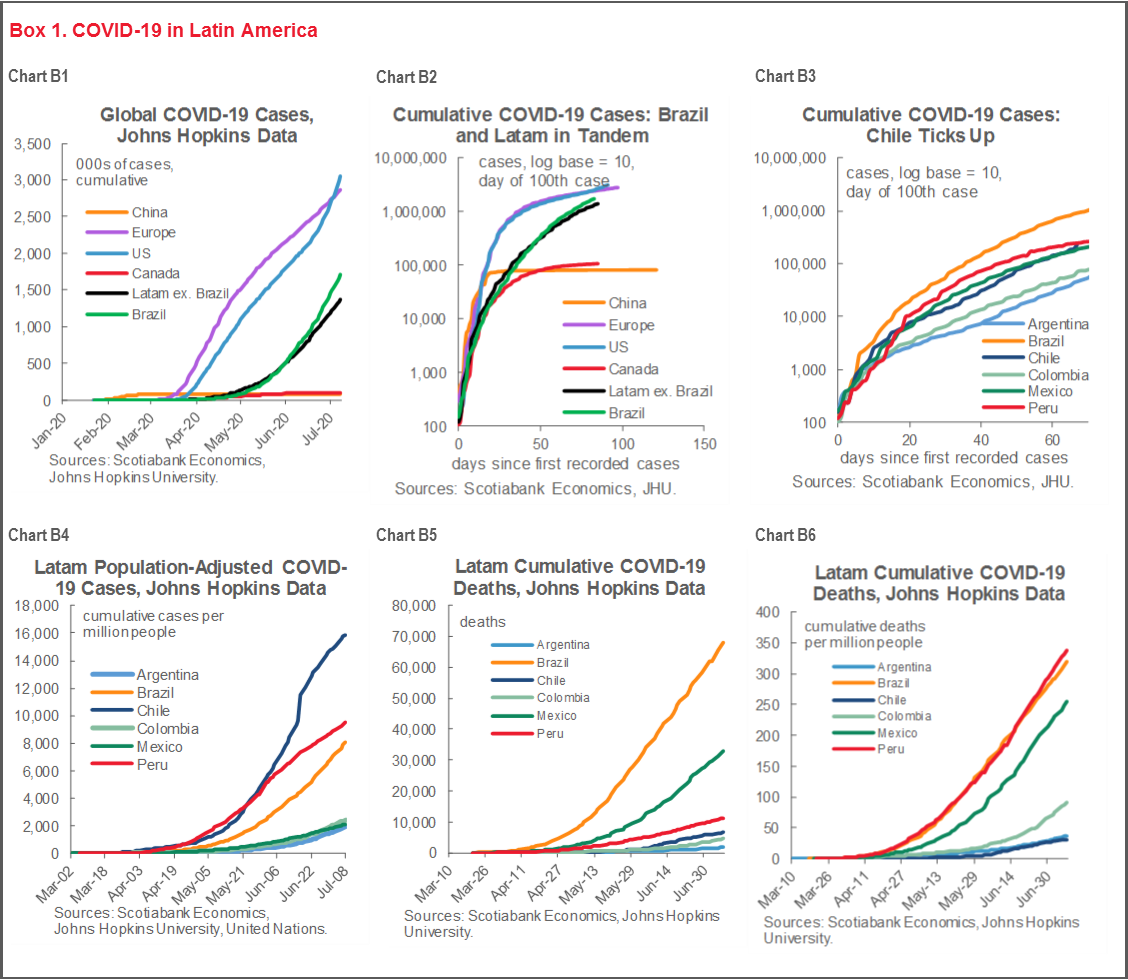

The COVID-19 storm remains stalled in the Americas, with eyes in both the United States and across Latin America. After weeks in which we hoped that small changes in big numbers might herald a turning point in the course of the novel coronavirus’ spread in the region, it now appears that COVID-19 is set to become a chronic condition for the near term in the Americas. Positive test rates remain far higher across the Latam-6 than in any other area that has been an epicentre of contagion (table 3). Latam’s positive test rates imply that community transmission remains rampant, testing is not yet adequate, and the region’s major countries are still far from the point where concerted contact tracing could support the identification and containment of localized outbreaks. As a result, re-opening is likely to proceed in a stop-start fashion in most of the Latam-6 countries. While Peru’s accelerated unlocking is unlikely to be rolled back, re-opening is equally unlikely to speed up in its Latam peers.

At the country level, new COVID-19 case numbers continue to make notable rises in Argentina and Chile. This past week Argentina recorded its first instance of more than 3k new cases in a single day. Both countries have intensified and extended lockdown measures in their capital regions until at least mid-July, with a strong likelihood that the expiry dates on these measures will be pushed out even further. That said, both countries also continue to ease restrictions in more remote regions where new case numbers are much lower. Our standard panel of COVID-19 charts in box 1 at the end of this section underscores that Brazil’s curve remains relatively steep compared with that for the rest of Latam, and that both Argentina and Chile have fared relatively poorly in recent weeks.

FORECAST UPDATES

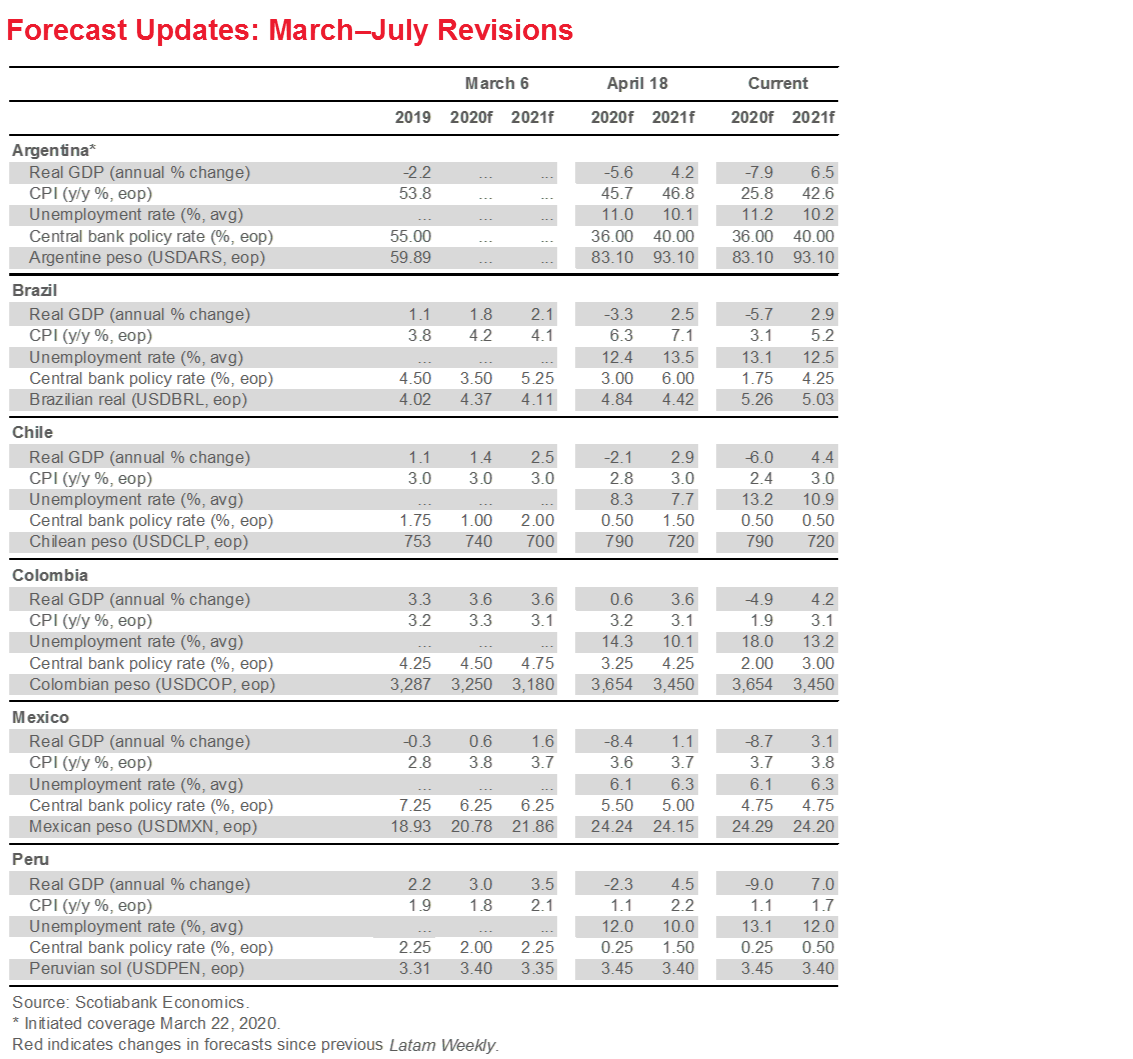

Although an accumulating set of data imply that the peak of lockdown measures in April was also the bottom for economic activity, our country teams continue to incorporate a bit more softness into their forecasts for the Latam-6 economies in 2020 (see Forecast Tables, pp. 2 and 3).

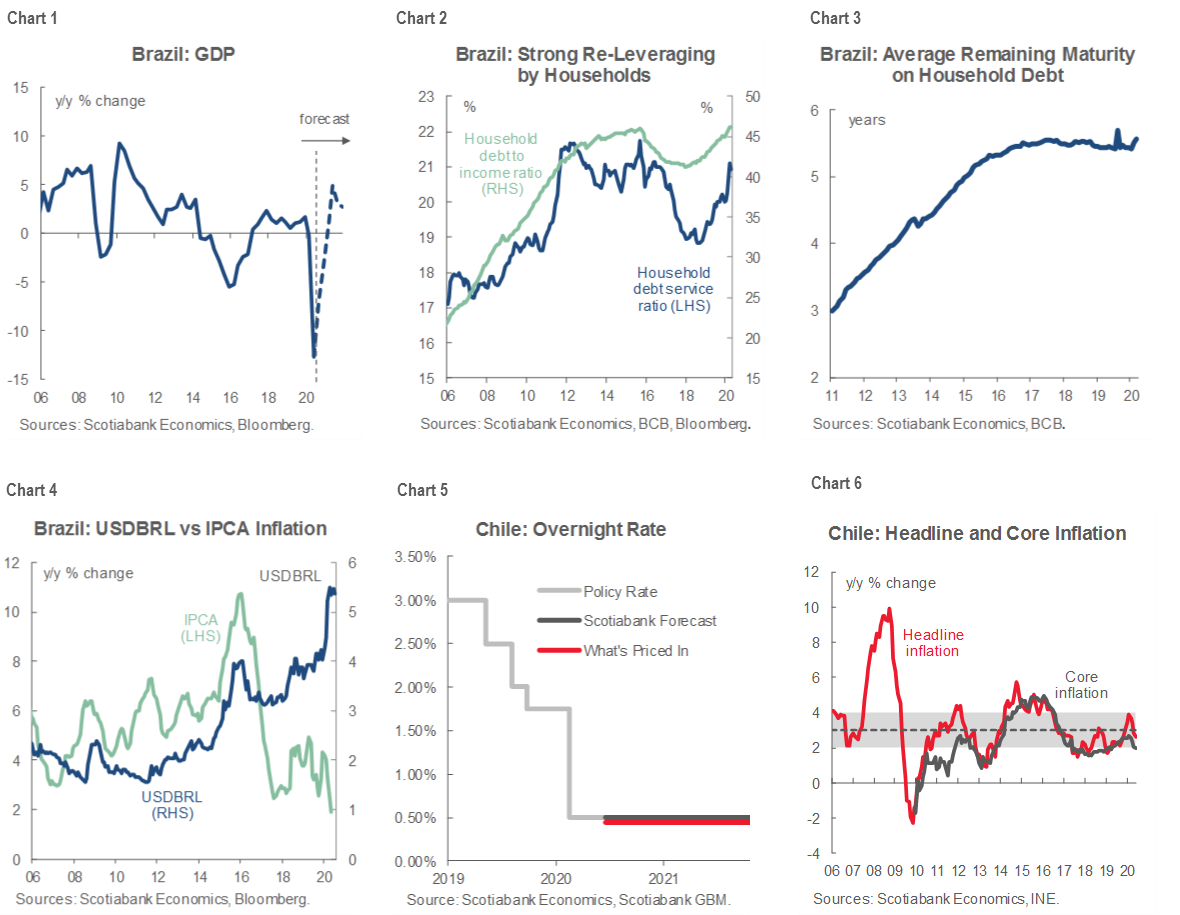

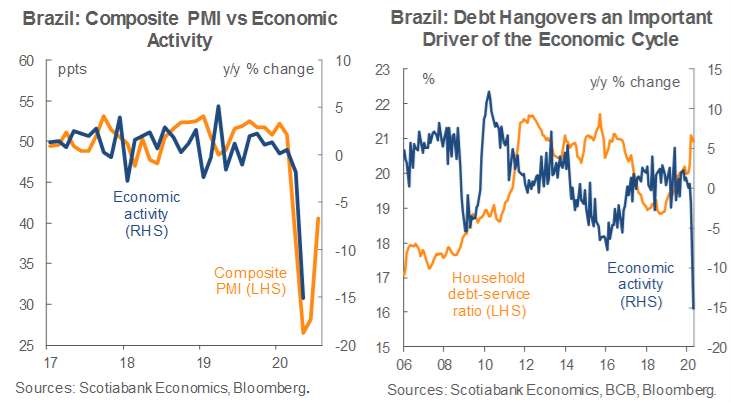

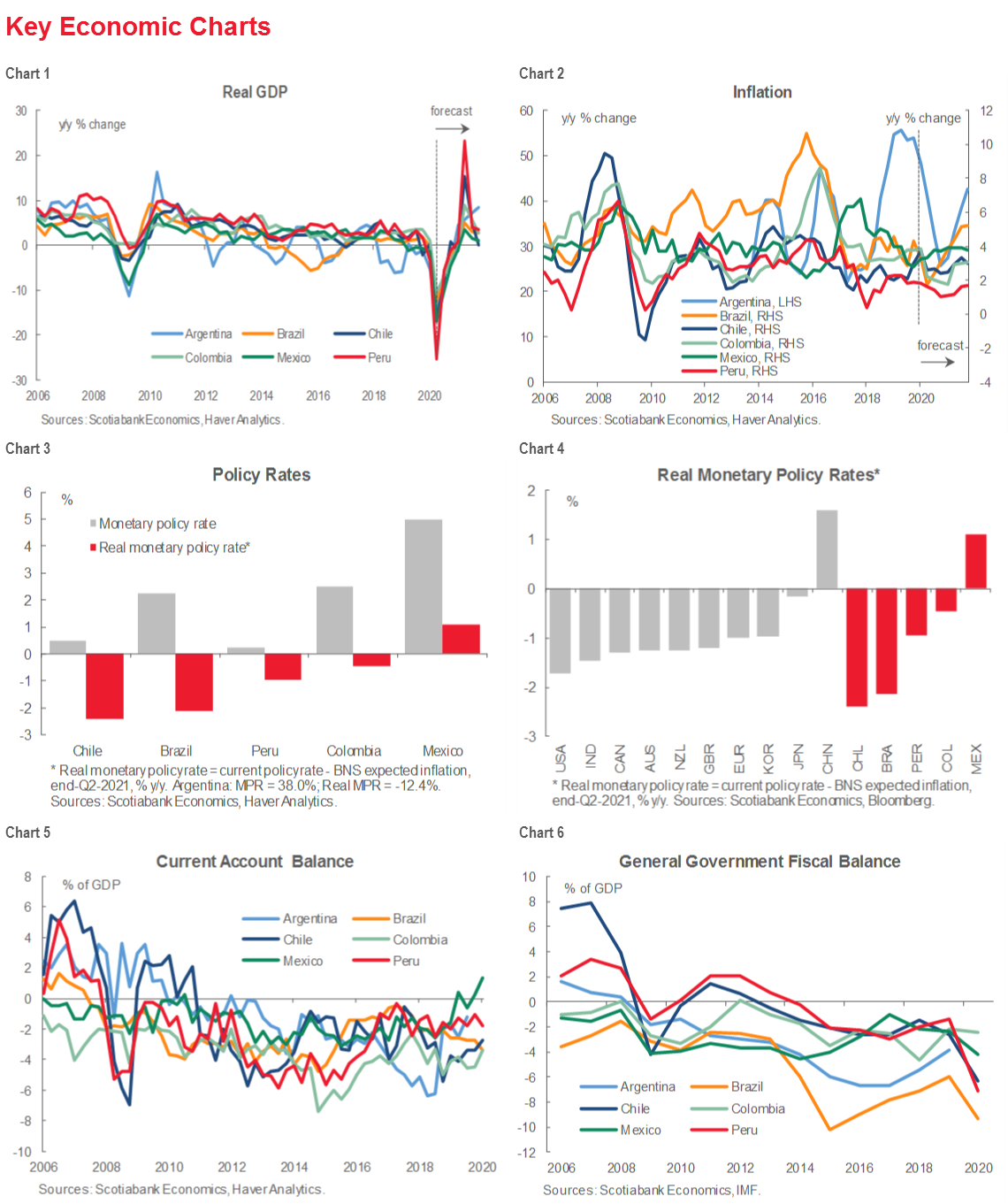

Brazil. The depth and breadth of the ongoing COVID-19 pandemic in Brazil, the uneven domestic policy response, and the continuing deterioration in macroeconomic indicators has prompted a major overhaul of our forecasts for the country’s economy, which now feature lower growth, weaker inflation, and higher unemployment. The contraction in economic activity in 2020 has been moved from -4.3% to -5.7% y/y (chart 1), while the rebound in 2021 appears a touch stronger at 2.9% y/y (previously 2.0% y/y) only because it’s coming from a lower base. Year-end headline inflation has been shaved by about half a point for both 2020 and 2021, to 3.1% y/y and 5.2% y/y, respectively, while the average unemployment rate projected for 2020 has been pushed up from 12.5% to 13.1%. Our Brazil economist believes households’ high debt burdens (chart 2) will provide a drag on growth that will be made worse as the relatively short average maturity of Brazilian household debt (chart 3) implies that expected policy rate increases in 2021 will have an immediate impact on Brazilians’ purchasing power. Although pass-through from exchange rate depreciation to domestic prices appears to be limited so far this year, the decoupling between the BRL and headline inflation (chart 4) is unlikely to continue for long.

Colombia. A softer inflation outlook in Colombia, where headline CPI is now expected hit 1.9% y/y at end-2020 compared with 2.7% y/y in our previous forecasts, underpins our Bogota team’s view that BanRep will deliver two more -25 bps cuts, one at each of its next two meetings.

Mexico. Growth in Mexico is now expected to be a touch weaker in 2020, at -8.7% y/y versus 8.4% in our previous forecast, followed by a stronger rebound in 2021, up from our previous projection of 1.1% y/y growth to 3.1%. It’s worth recalling that our team in CDMX was far ahead of the curve in calling the depth of the 2020 downturn, so these changes are on the order of fine tuning. As in Brazil, the forecast for faster growth in 2021 comes off a weaker base.

FORTNIGHT AHEAD: CHILE’S CENTRAL BANK EXPECTED TO HOLD

The next two weeks sees only one policy rate decision in the Latam-6 in Chile. Our team in Santiago and the market expect the BCCh’s Monetary Policy Committee (MPC) to keep its policy rate on hold at 0.5% at its next meeting on Wednesday, July 15 (chart 5). At the BCCh’s most recent MPC meeting on June 16, the Committee voted unanimously to keep the monetary policy rate at the central bank’s lower bound at 0.5% in a dovish hold. The MPC’s statement noted that the Committee “estimates that it will keep the MPR at its technical minimum over the entire projection horizon.” At two years, the “projection horizon” was by nearly all interpretations longer than the “extended period of time” in previous statements and double the 12 months that the BCCh kept the monetary policy rate at 0.5% in response to the 2008 global financial crisis.

Although inflation is now below target (chart 6), the MPC observed that it will look to rely on asset purchases rather than further rate cuts to support the economy: “in addition, if economic developments so require, it will continue to explore options to intensify the impulse and support financial stability, using unconventional instruments.” Similarly, the BCCh’s Q2 Monetary Policy Report, released on June 17 following the last MPC meeting, emphasized that in a downside scenario the Bank ”may have to make extreme use of its available policy instruments” and that it “especially appreciates the support that Congressmen from the Finance Committee of the Senate have expressed for a constitutional and legal reform that would expand the Bank’s power to act in exceptional situations where the preservation of financial stability especially requires it.” These reforms remain under discussion by Congress, but are expected to be implemented.

In major data prints, May economic activity index readings are due in Brazil (July 14), Peru (July 15), and Argentina (July 22). They will likely confirm the beginning of rebounds from the worst of the COVID-19-induced shutdowns in April, but will also point to long recoveries ahead.

ARGENTINA’S DEBT NEGOTIATIONS NEAR AN END, BUT AT A COST

With the delivery on July 5 of a fourth set of new and improved offer terms, we believe Argentina’s government will reach an agreement over the next few weeks on an exchange of at least two-thirds of its USD 65 bn in external-law bonds that are currently in default. Argentina has significantly enriched its offer compared with its initial negotiating position (see Argentina’s Country Update below and our Latam Daily reports from this past week for details).

The current proposal, however, implies the possibility of some collateral implications for the international financial system. In response to creditor demands, the new offer terms would allow holders of bonds from Argentina’s 2005 exchange to maintain indentures that make these bonds relatively difficult to restructure. Since 2014, model contractual language agreed through ICMA has been the basis for new bond issues across emerging and frontier markets. In the event of payment difficulties, this language makes newer bonds easier to restructure and less likely to provide the basis for a drawn out, damaging legal struggle like the one Argentina engaged in with some creditors from 2005 to 2016. Balancing debtor and creditor interests in a debt restructuring always requires careful calibration: contracts entered in good faith should be respected. But Argentina’s proposed retreat from the 2014 ICMA language would make future restructurings harder and this could set a damaging precedent for emerging markets as a whole.

USEFUL REFERENCES

J. Jacobs, “Trump Says Phase 2 China Trade Deal Unlikely at This Point”, Bloomberg, July 10, 2020: https://www.bloomberg.com/news/articles/2020-07-10/trump-says-phase-2-china-trade-deal-unlikely-at-this-point?sref=GlimkFcY

Stiglitz, Howse, and Slaughter, “Sovereign Creditors Must Not Rewrite the Rules During the Pandemic”, Project Syndicate, July 9, 2020: https://www.project-syndicate.org/commentary/argentina-sovereign-debt-rules-creditors-by-joseph-e-stiglitz-et-al-2020-07

Markets Report: Implications of Proposed Reform to Chile’s Private Pension Plans

Jorge Selaive, Chief Economist, Chile

56.2.2939.1092 (Chile)

jorge.selaive@scotiabank.cl

Tania Escobedo Jacob, Associate Director

212.225.6256 (New York)

Latam Macro Strategy

tania.escobedojacob@scotiabank.com

Carlos Muñoz, Senior Economist

56.2.2619.6848 (Chile)

carlos.munoz@scotiabank.cl

The Lower House of Chile’s Congress has advanced a bill that allows participants in the country’s private pension plans (AFPs) to withdraw up to 10% of their savings. The government remains resolutely opposed to the initiative.

We estimate that total withdrawals from the AFPs could be between USD 3.5 bn and USD 17 bn. This range would imply sales of around USD 600 mn to USD 3 bn in sovereign bonds.

The Chilean yield curve widened by about 20 bps in the aftermath of the news, but we think it will stabilize at current levels with limited space to move out further.

In the FX market, we have seen USD sales in anticipation of the liquidation of foreign assets currently held by the AFPs, but we still think that levels around USDCLP 780 are adequate to build USD longs.

POLITICAL DIVIDE ON POSSIBLE PENSION WITHDRAWALS

On the evening of July 8, the Lower House in Chile advanced a bill that would allow members of the private pension system to withdraw up to 10% of accumulated funds in their individual capitalization accounts into which their mandatory contributions are directed. The bill needed 93 votes (out of 155, i.e., 60%) for further discussion and got 95; it will now be discussed in the Constitutional Committee of the Lower House and then in the Senate in a process that might take a few weeks.

The government, through its finance and labour ministers, had earlier expressed its refusal to approve the proposal. It argued that other relief measures have been proposed for the middle class that do not harm future pensions. But despite tough negotiations, even some members of the government’s coalition (13) voted in favour of the bill.

Besides authorizing a voluntary, one-time withdrawal of 10% of the funds accumulated in the individual capitalization accounts, the bill also establishes a maximum withdrawal equivalent to about USD 5,000 with a minimum withdrawal amount of about USD 1,250. The money would be delivered either in one payment ten days after an application for withdrawal or in a maximum of five monthly disbursements. Under the current bill, the government would be expected to create a fund, in conjunction with employers, to make up for both the outflows and the minimum interest those funds would earn over time, but there is still a lot of space for changes to the bill.

It is difficult at this point to estimate how much money would be withdrawn from the AFPs as a result of this measure. The willingness of individuals to make a withdrawal from their retirement accounts varies a lot depending on their age group, income bracket, and overall financial situation. We could argue, however, that in general terms, people who are closer to their retirement ages should be more likely to tap into these funds. But we must also consider that the effects of the crisis have been disproportionately heavy on youth employment and this cohort could be more inclined to use these resources during the current difficult financial conditions.

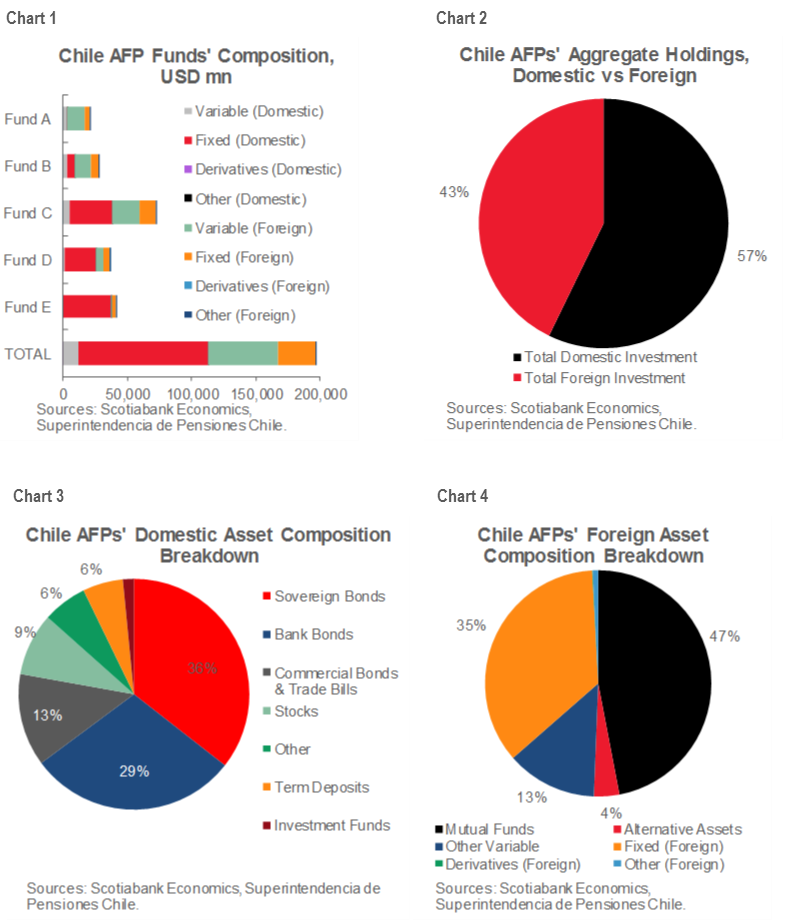

The Chilean pension system has a total of 5.7 million contributors and assets under management of about USD 200 bn. By looking at the composition of the different investment portfolios of the AFPs and at the information contained in the most recent labour statistics, we estimate that the minimum amount that could be withdrawn as a result of the measures under discussion is around USD 3.5 bn and the maximum might reach USD 17 bn.

According to our calculations, about 40% of the total would be withdrawn from the “most risky” portfolios (Funds A and B), 35% from the “balanced risk” portfolio (Fund C), and 25% from the “conservative” portfolios (Funds D and E).

MARKET IMPACT

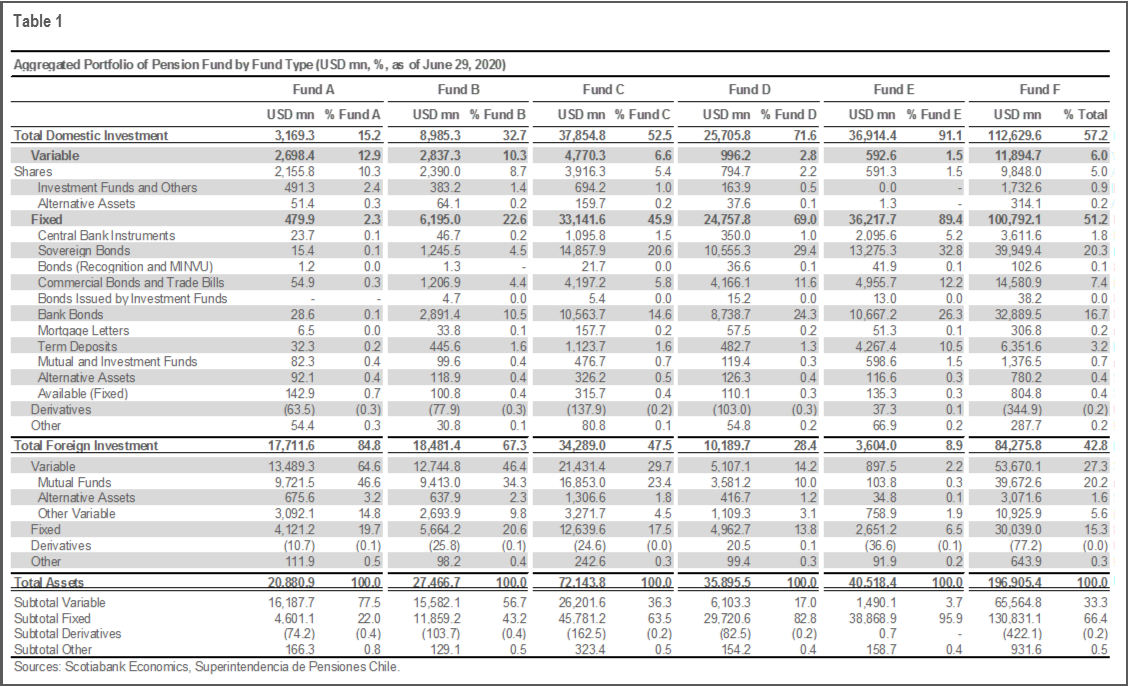

The AFPs in Chile own about 75% of Chile’s local government debt, and 6% of local equities. The broad composition of their portfolios is in charts 1–4 and further detail is provided in table1.

If one assumes that the current composition of the portfolios is optimal and that the pension funds would like to maintain the same or very similar exposures, the AFPs would have to sell about USD 600 mn of sovereign bonds in our optimistic, low-withdrawal scenario (i.e, USD 3.5 bn in total asset sales). In contrast, the AFPs would have to sell close to USD 3 bn of sovereign bonds if withdrawals are at the upper limit of our estimates (i.e., USD 17 bn). To put these numbers in context, the average daily volume in the Chilean local sovereign bond market in 2020 has been CLP 170 bn in nominal bonds and CLP 160 bn in linkers.

As the bill has begun its advanced through Congress’ legislative path, the yield curve in Chile has widened up to 20 bps in a very illiquid market. But we must consider two things. First, there is still a long way to go for the bill to become a law and there is a good chance that it will be stopped at some point in the process. Second, there is a separate discussion in Congress to pass a bill to allow the BCCh, the central bank, to buy government bonds on the secondary market, which might mitigate some of the effects of the AFP sales. For now, we think that the curve will stabilize at current levels, and that there is limited space for additional widening.

Meanwhile, in the FX market, we have seen sales of USD in anticipation of the possible liquidation of foreign assets currently held by AFPs. These flows, along with the constant presence of the Ministry of Finance selling USD in the spot market, might continue to put a lid on USDCLP rallies, but we still think that levels around USDCLP 780 are good entry points for long USD positions.

WILL THE LAW PASS?

We believe the probability of some version of this law being approved is still below 50%. Congress’ full Lower House must vote on the bill one more time after the discussion in its Constitutional Committee and some of the members that voted in favour the first time, particularly in the right-wing parties, might change their minds after encountering strong resistance within their coalitions. Only three deputies would have to change their votes to stop the bill from advancing since it was approved by 95 votes and 93 is the minimum needed to pass.

Even if the bill makes it to the Senate, a good number of opposition lawmakers could reject the bill if the government presents a new fiscal package specifically designed to protect the middle class—an alternative we would not rule out. All in all, we would expect the Senate to hold a more technical rather than political discussion on the bill compared to what we have seen in the Lower House and, hence, we should see at least some important tweaks to the current bill. Options such as narrowing the scope of eligible participants to those who have lost their jobs, or other similar revisions, might help to soften the effects of the bill on financial markets. If, however, any version of the bill passes, we think political uncertainty will remain high as the precedent set would be unambiguously negative.

The President could veto the bill if it is sent to him for final approval into law, but we think Piñera will prefer not to do so as this would carry a high political cost, particularly as we get closer to the constitutional referendum that will be held in October. The timing of the next votes is not fixed yet so we might see this issue on the Congressional agenda for the next few weeks.

COUNTRY UPDATES

Argentina—Coming Up from the Bottom

Brett House, VP & Deputy Chief Economist

416.863.7463

brett.house@scotiabank.com

With its fourth set of proposed debt restructuring terms that were delivered on July 5 and the fifth extension of its offer period to August 4, the government is nearing an end to its drawn-out back and forth with creditors on one of the largest emerging-market bond swaps in history. Although the Ad Hoc Bondholders Group, which controls what could be blocking positions in some bond series, has rejected the offer, we believe Argentina and the holders of its impaired foreign-law bonds will move ahead on a swap on terms quite close to those now on offer. The exchange is due to be executed on September 3.

The current proposal represents a substantial movement toward bondholders’ demands. It would provide creditors with about 54 cents on the dollar under the assumption of a 10% exit yield; it would also see interest accrued during the period of default capitalized and paid; and, in a major concession, the 2005 exchange bondholders would also see their vintage indentures maintained despite the evolution in model bond contracts since then. The authorities’ SEC filing makes it plain, via relatively low participation thresholds, that they are prepared to move ahead even if some creditors remain on the sidelines.

At this stage, we’re more concerned with what comes after the debt swap. The current offer terms deliver only about USD 31 bn in debt relief compared with the nearly USD 45 bn sought under the government’s original offer. In principle, conclusion of the debt exchange should allow the IMF and Argentina to move forward on a new lending arrangement and policy program this autumn. In practice, weaker growth than anticipated in the IMF’s most recent debt sustainability analysis and more limited debt relief could make negotiations on fiscal targets for an eventual program quite challenging.

Recent economic data point to some gains in May, which reflect the first loosening of the country’s strict lockdown in the latter third of the month. According to government data released on July 9, diesel demand rose from a 10-year low in April to 94% of pre-pandemic levels in May. Gasoline demand rose to 46% of pre-virus levels. Demand for jet fuel, however, remained at just 8.9% of pre-lockdown sales.

The coming fortnight will see the release of two major macro indicators in Argentina:

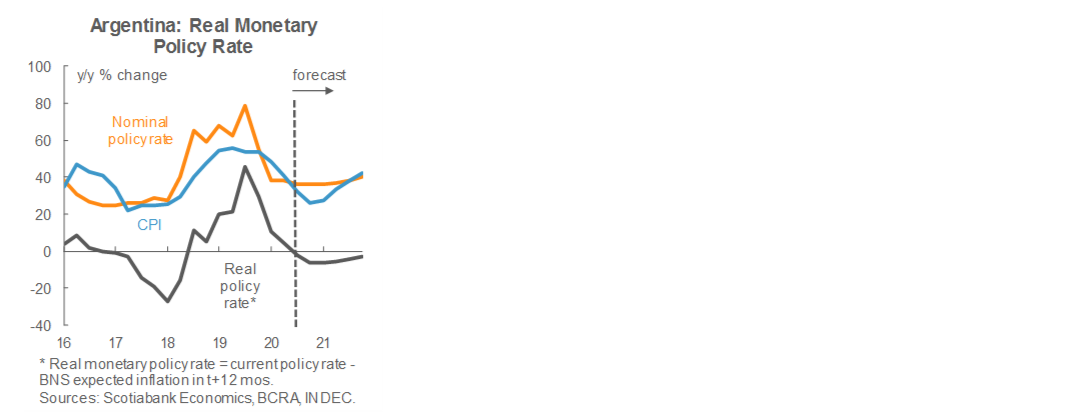

With its fourth set of proposed debt restructuring terms that were delivered on July 5 June inflation numbers come out on Wednesday, July 15. Official inflation readings continue to be artificially suppressed by (1) capital controls that are propping up the official value of the ARS and (2) domestic price controls on the utility sector along with official monitoring of thousands of additional items to discourage price increases. As a result, our inflation outlook is grounded more in a political view that these measures will remain in place late into 2020 rather than a clean reflection of fundamental macroeconomic dynamics. We expect June to record a third month in a row with headline inflation held around 1.5% m/m, which would bring annual inflation down to around 42% y/y owing to base effects from last year’s spike in prices. We expect the authorities to loosen FX controls in the autumn and allow prices to begin to move slightly more freely, which would see month-on-month inflation rise to around 2% even as base effects bring annual inflation down to a temporary low at 25.7% y/y by end-2020, its lowest rate since April 2018. Even with artificially low official inflation numbers, real monetary policy rates have moved back into negative territory and are set to stay there over our forecast horizon (chart); and

May’s EMAE monthly economic activity indicator follows on Wednesday, July 22. May industrial production and construction activity, which together account for about a quarter of GDP, imply that April, the month with the most intense quarantine measures, was likely the bottom for Argentina’s pandemic-induced shutdown. We anticipate a 13.7% m/m gain in total economic activity in May, which would still leave economic activity down -22.9% y/y for the month.

Despite these emerging bright spots, Argentina’s economic landscape otherwise remains bleak. GDP remains on track for a -15% y/y contraction in Q2 and 2020 is still set to see an annual decline of around -8% y/y or worse. A successful conclusion to the proposed debt exchange would be welcome, but can do little to boost growth this year.

We expect the intensification of lockdown measures in greater Buenos Aires that were imposed at end-June to be extended beyond their current July 17 expiry date. The ongoing spike in COVID-19 cases in the capital region will make it difficult for the authorities to relax these measures even if the lockdown continues to be loosened in the rest of the country. About one third of the country lives in BsAs.

Brazil—A Lackluster Recovery Weighed Down by Debt and Uncertainty

Eduardo Suárez, VP, Latin America Economics

52.55.9179.5174 (Mexico)

esuarezm@scotiabank.com.mx

Our revised forecasts for weaker Brazilian growth are still a bit more optimistic than consensus for 2020, but less constructive for 2021. Our flatter growth pattern is to a large degree based on the recent “upward surprises” we have had with respect to Brazilian PMIs. In addition, we think the loosely enforced lockdowns the Brazilian government has implemented will mean some sporadic boosts to activity, but a longer pandemic, and a more lackluster recovery in 2021. We see two factors weighing on growth next year: (1) a consumer debt hangover; and (2) shaken confidence due to political uncertainty, which would present significant headwinds for investment. Rising rates could also suppress next year’s bounce. The combination of these factors explains our flatter-than-consensus anticipated rebound in 2021.

PMIs suggest that by the end of Q2 the effects of the COVID-19 quarantine on the economy were starting to fade, although overall activity remained fairly deeply in contraction territory. We think the recovery will not be a straight line, as the severity of the pandemic’s expansion in Brazil will likely lead to a stop-and-go reopening of the economy, whether it is mandated by the government or not. The absence of a V-shaped recovery is consistent with the central bank’s (BCB) view, described by Director Kanczuk on July 2.

Up to now, Brazilian consumers have remained the main support for the country’s growth, boosted by a re-leveraging process and falling yields. Although the average maturity of Brazilian household debt rose materially at the beginning of the decade, it stagnated and remains relatively short (around 5 years), suggesting about 1/5 of debt rolls over every year. This has been supportive for growth during the period of BCB easing, but we expect it to provide some headwinds starting next year as the central bank moves into a tightening cycle. We anticipate a consumer debt hangover to be triggered by three factors: (1) the recession will hit aggregate income, making the already-high leverage ratio climb further; (2) we expect rising yields to lead to additional increases in the household debt-service ratio (the share of disposable income eaten up by debt payments); and (3) rising yields and uncertainty should make consumers averse to increasing their debt levels.

For 2020, we anticipate all quarters to show negative prints, followed by a gradual bounce at the beginning of 2021, with peak-growth achieved in Q2, boosted by very favourable base effects. However, we anticipate the overall rebound will be disappointing, weighed down by the factors we outlined above. On the inflation front, we have been wrong in anticipating the BRL’s decline would trigger an early bounce in inflation, which speaks to both the improvement in the BCB’s credibility over recent years—partly due to the improvements in the inflation targeting regime and the tightening of tolerance bands—as well as very weak growth. However, we still anticipate inflation will ultimately rise, as: (1) FX-inflation pass-through arrives, 2) an increase in the pace of fiscal deterioration stokes inflation, and 3) the now multi-year period of very low investment weighs on potential output, reducing the inflation-dampening impact that a larger output gap would have had. On the currency front, we think the BRL has now found somewhat of a new equilibrium, and see it trading somewhat range bound for the next 18 months. Part of the absence of a bounce can be attributable to the absence of any positive news to serve as a rebound catalyst.

Chile—May GDP Falls -15.3% y/y; Bill to Allow Withdrawals from Pension Funds Under Discussion by Congress

Jorge Selaive, Chief Economist, Chile

56.2.2939.1092 (Chile)

jorge.selaive@scotiabank.cl

Carlos Muñoz, Senior Economist

56.2.2619.6848 (Chile)

carlos.munoz@scotiabank.cl

Several key data releases have been received over the past two weeks. On June 30, sectoral and employment data were released. Retail sales showed a contraction of -28.7% y/y in May. Declines in automobiles, clothing, footwear and durable consumer goods in general were mainly responsible for this major fall. On the other hand, and as we have been pointing out for some time, supermarket sales grew by 2.3% y/y—which closely reflects what we have seen in credit and debit card transactions data. The unemployment rate reached 11.2% in the March–May period (2 ppts higher than the previous quarter), revealing a sharp drop in employment (-16.5% y/y), although the estimate of the unemployment rate continues to be attenuated by the significant contraction in the labour force (-12.8% y/y), a phenomenon we have observed since the pandemic began and quarantine measures were imposed. This labour force dynamic is making it difficult for the market to correctly anticipate the evolution of the unemployment rate.

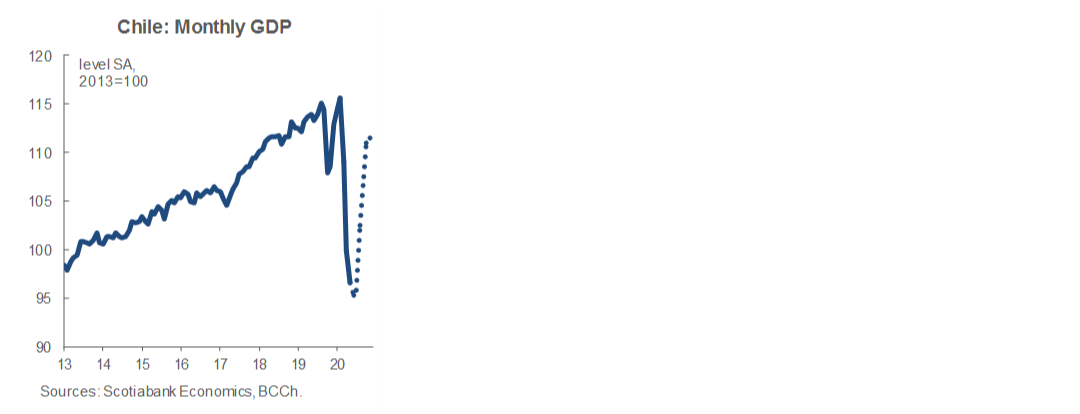

On July 1, we learned that the year-over-year contraction for monthly GDP in May reached -15.3%. It is expected that this decline will be followed by a similar one in June, after the fall of -14.1% y/y in April. May’s drop in activity would be compatible with the “optimistic” end of the central bank’s 2020 GDP growth range (-5.5 to -7.5% y/y). Non-mining activity contracted -3.7% m/m (seasonally adjusted), considerably less than what was seen in April, reaching a year-over-year contraction of -17%. Much of the negative effect was generated after the initial shutdown of the economy, leaving little room for further deterioration in the coming months. For this reason, despite the new quarantine measures applied in June, economic activity should be less negative and less volatile than that registered until May. On the other hand, mining activity remained without major distortions in its production, as revealed by the 1.2% y/y growth in May.

This past week, on Wednesday, July 8, we received the inflation data for June. June headline inflation came in at -0.1% m/m, which put annual inflation at 2.6% y/y. The dynamics of headline inflation continue to be dominated by the most volatile products, with increases in food prices and drops in fuel costs, while core inflation remains fairly stable—all of which is still conditioned on the ongoing difficulties in collecting prices and imputing missing prices during the pandemic. Core inflation decreased -0.1% m/m (2% y/y) in June, with a change of -0.3% m/m in goods (2.1% y/y) and 0% m/m in services (1.9% y/y).

A hot topic this week has been the bill under discussion by Congress to allow withdrawals from pension funds. On July 8, the process to move forward on the bill was approved by the Chamber of Deputies, and it will be discussed by the Senate in the coming weeks. The bill specifically proposes to authorize members of the private pension system to withdraw, voluntarily and only once, 10% of the funds accumulated in their individual capitalization account which is built on mandatory contributions. The bill would also establish a maximum withdrawal equivalent to about USD 5,000 with a minimum withdrawal of about USD 1,250. This proposal has much more worrisome implications for financial markets and for eventual actions by the central bank (see our Markets Report section).

On Monday, Gran Santiago area will enter its ninth consecutive week in total confinement, as re-opening measures start to gradually materialize in very specific areas in the south of Chile, where there has been improvement in COVID-19 caseloads. With no tier-1 indicators coming out in the next two weeks, we will continue monitoring the discussion of the pension bill in Congress, as well as high-frequency indicators.

Colombia—Low Inflation and Uncertainty Regarding the Demand Recovery Open the Door for Two More 25 bps Rate Cuts by BanRep

Sergio Olarte, Head Economist, Colombia

57.1.745.6300 (Colombia)

sergio.olarte@co.scotiabank.com

Jackeline Piraján, Economist

57.1.745.6300 (Colombia)

jackeline.pirajan@co.scotiabank.com

The COVID-19 / oil price shock has brought unprecedented uncertainty to the global economy. Colombia has not been spared. The depth of the recession, the speed of recovery, the reaction of prices to demand and supply disruptions, financial system sustainability, fiscal needs, additional exigencies due to the pandemic, and long-run financial sustainability concerns raise more questions than answers, not to mention the possibility of a structural change in consumers' behaviour and worries regarding the global trade recovery.

In this context, the strategy of Colombia's central bank has been to provide ample liquidity to markets to avoid a financial crisis in a "whatever it takes" approach. In contrast, in terms of conventional monetary policy, BanRep has decided to take a more gradual line and has cut policy rates initially at a -50 bps pace (in March, April, and May) and has more recently reduced the speed to a -25 bps cut in June, which brought the monetary policy rate to 2.50% as BanRep entered a very data-dependent phase for the coming months.

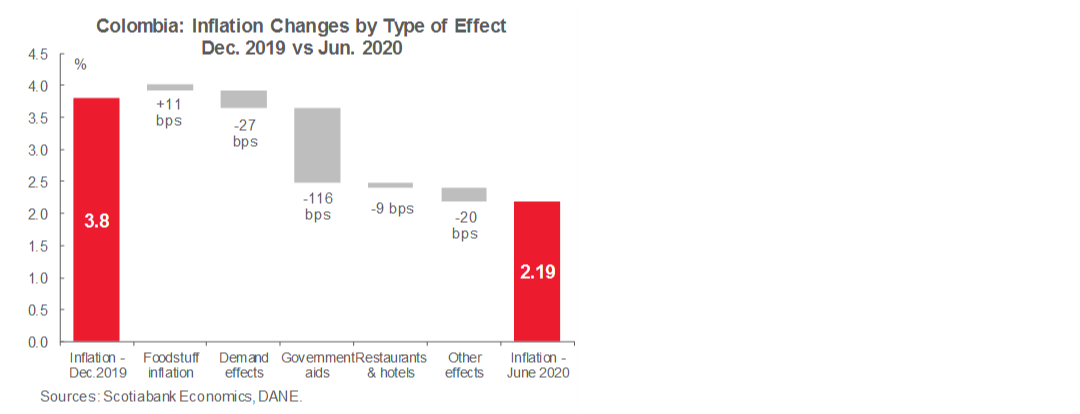

CPI inflation contracted by -0.38% m/m in June, well below market expectations and the strongest pullback in at least ten years. Although temporary government aid on utility fees and a VAT holiday accounted for most of this deflation (around 70%), and eventually these factors will reverse, the June print gives some additional room for BanRep to cut at least an additional -25 bps in July to 2.25%. Consumer confidence and credit and debit card expenditures have improved slightly, but point to a much slower recovery on the demand side of the economy. Therefore, we now expect another -25 bps cut at the August meeting to take the monetary policy rate to 2.00%.

However, the question that arises is why BanRep continues to be so cautious in terms of the easing cycle. Our answer to that question has three parts:

1. According to some BanRep communications, a very negative real interest rate could bring more risks to financial stability and could help to trigger a financial crisis, which BanRep wants to avoid at all cost;

2. There is uncertainty in terms of inflation being too high. In fact, long-run inflation expectations and some core inflation measures are still close to 3%. A major part of the reduction in inflation has been due to administered prices, which points to future, undesirable volatility in CPI inflation due to potential reversal effects in 2021.

3. According to recent BanRep Board statements, in the short-run, interest rates will do very little to help the economy, while fiscal policy is the one to step in and give some traction to economic activity, although it will bring significant risks in terms of long-run fiscal sustainability.

To sum up, recent inflation data and gradualism in the demand-side recovery path will open the door to the delivery of two more -25 bps cuts in the July and August BanRep meetings. However, we still do not expect BanRep to either speed up the easing cycle or take a more aggressive approach in the near term. Additionally, further central bank movements will depend on the pace of economic recovery. Therefore, we think the next coincident indicator releases will be vital, since they could confirm that the worst for economic activity passed in April. Although in May we expect economic activity to show contractions in y/y terms, there should be an improvement with respect to April´s results due to the reopening process that started in May after 33 days of strict lockdown.

Mexico—Economic Indicators Reflect the Severe Disruption Caused by the Pandemic

Mario Correa, Economic Research Director

52.55.5123.2683 (Mexico)

mcorrea@scotiacb.com.mx

The second half of a complicated year is starting, and the Mexican economy, as well as many others around the world, is in a delicate situation. COVID-19 contagion keeps not only rising, but even accelerating in the world, and the ugly possibility of new isolation measures or a longer period of restricted economic activity is increasing. If this is the case, then the contraction of economic activity in Mexico will be even deeper than we currently forecast. Recent economic indicators have presented unprecedented and dramatic readings that depict the magnitude of the disruption produced by the pandemic. Real private domestic consumption fell -22.3% y/y in April, the deepest contraction on record for the main aggregate demand component. Total investment plummeted -36.9% y/y in real terms in the same month, also an unwanted record. Auto industry figures for the month of June were released and show that activity is resuming, but remains far away from previous levels: domestic sales contracted -41.1% y/y, production was -29.3% lower than a year ago, and exports fell -38.8% y/y. To have a better idea of where we are on the path to recovery, domestic sales were 60% of the average level registered in January–February; production was 74%, and exports were 79%, so there is still a good stretch to cover.

One of the recurring themes of these unusual times has been the frequent surprises in economic indicators, as was the case with the inflation figures for the month of June. General inflation came in higher than expected at 0.51% m/m versus the consensus’ 0.43% m/m projection, making it the highest reading for a month of June since the year 2000. Year-over-year inflation reached 3.33%, once again above the 3.0% target. Most of the increase was produced by energy (5.98% y/y); meat, dairy and poultry (1.02% y/y); and non-food merchandise (0.86% y/y). Core inflation was 0.37% m/m and 3.71% y/y, showing once again a surprising stubbornness even when there is a huge slack in economic activity and demand has plummeted. This could be a key issue for Banco de México in the handling of monetary policy. We are currently expecting one more cut in the monetary reference interest rate in August, but this time of only -25 bps, followed by a long pause to navigate the complex second part of the year. Further reductions will need to be preceded by more benign behaviour from core inflation.

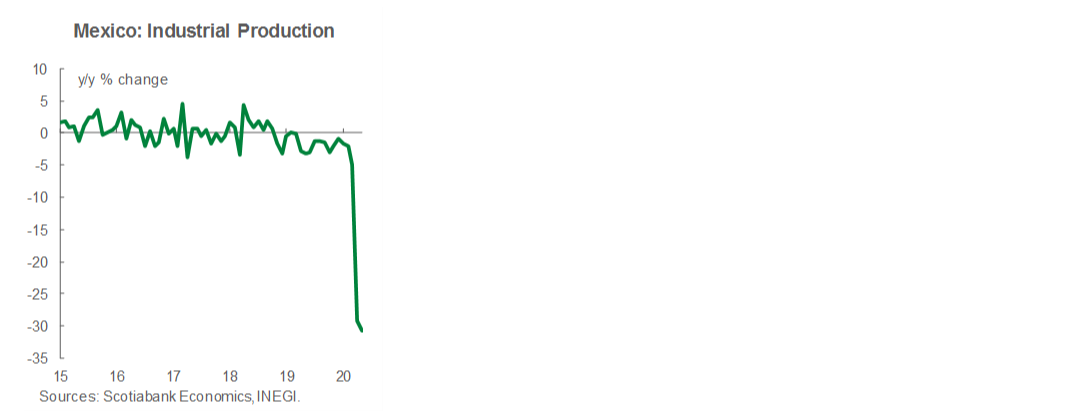

Real industrial activity plummeted -30.7% y/y in May, coming in well below the already dramatic market forecast of -25.6% y/y. Manufacturing activity—representing more than half of total industry production—was the hardest-hit, falling -37.1% y/y, closely followed by the -36.3% y/y drop in construction. Utilities fell -13.1% y/y and mining posted a -5.9% y/y drop. As the numbers revealed, the disruptive effect of the pandemic on industrial activity has been severe and unprecedented.

Finally, we made some adjustments to our forecasts that we will be commenting on next week. Most notably, our GDP forecast for 2020 is a bit lower, down from -8.4% to -8.7% y/y; while the 2021 forecast is stronger, up from the previous gain of 1.1% to 3.1% y/y.

The weeks ahead will be basically empty of relevant economic indicators in Mexico. Perhaps the job creation (loss) figures will be released by the IMSS, but the main issue to monitor will be the evolution of COVID-19 and the reopening of economic activity. If contagion continues to grow at a fast pace, a new postponement of the re-opening in many states could be necessary, which would impose a higher toll on economic activity.

Peru—Confusing Signals…from the Economy to COVID to Politics

Guillermo Arbe, Head of Economic Research

51.1.211.6052 (Peru)

guillermo.arbe@scotiabank.com.pe

COVID-19 may be stabilizing, but it is not abating…at least not convincingly. While both active cases and the daily death rate are down 10% from their peak highs, hospitalizations are at record levels. Contagion seems to be moving out of previous hot spots—including Lima, the northern coast and the northern rainforest—and into relatively new areas: the central highlands and the southern coast. Some of the new areas of concern have important mining operations, especially Arequipa, raising the risk that some mining operations may once again be curtailed, although this is not a sure thing. For the time being, mining operations continue to move toward complete recovery by the end of July.

On July 16, the BCRP is scheduled to release May GDP data. Initial information released by the National Statistics Institute has been discouraging—in May, mining GDP fell nearly -50%, y/y, and fishing was down -47%, y/y. In addition, cement consumption fell -65% y/y, and public investment declined a whopping -72% y/y. These figures point to a GDP decline closer to -30% y/y, rather than the -25% we had been expecting.

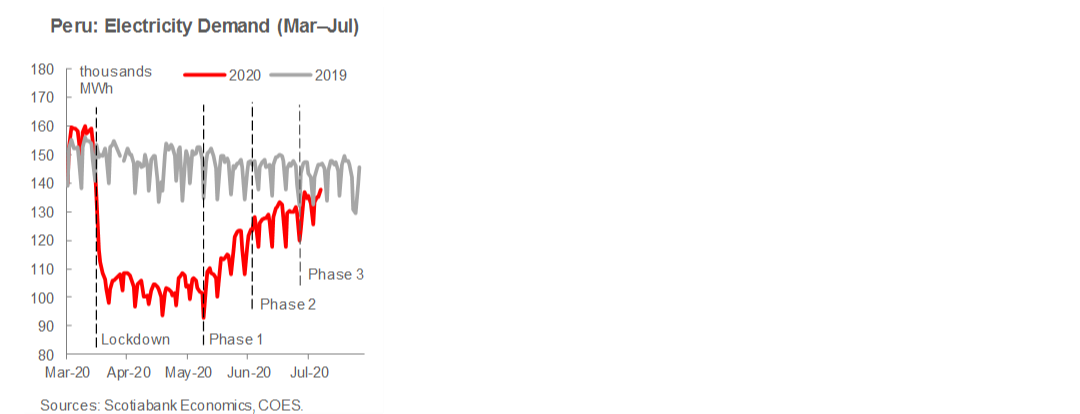

This data is, however, backward-looking and there are more positives looking forward. Formal employment actually rose in the first half of June. True, the increase was a paltry 60,000 jobs, but this was the first increase this year. Also, Peru’s external terms of trade are improving. Gold prices have surpassed USD 1,800/oz, just a short hop from the all-time high of USD 1,900/oz; while copper prices surged to a very decent USD 2.85, much higher than we were expecting for this year. Finally, electricity demand is just 6% under pre-COVID levels in July, a significant improvement from the 30% decline during most of the lockdown period (see chart).

The central bank maintained its reference rate at 0.25% on July 9, as expected. There was one interesting change in the text of the policy statement—the BCRP expects inflation to come in below the 1% floor not only in 2020, but also in 2021. Given this, and with inflation expectations (currently at 1.4%) declining, we ratify our expectation that the BCRP will not change its policy rate until Q4-2021 at the earliest.

The past week was fraught with political events. On July 8, President Vizcarra officially established April 11, 2021 as the date for the next Presidential and Congressional elections, thereby dispelling rumours that he would use the COVID-19 emergency to delay elections and stay in power longer. Meanwhile, Congress approved a new law that would eliminate legal immunity for the presidency and for high court officials. Although the law, if enacted (a second vote is required), is likely to be struck down by the courts as unconstitutional, it has been widely seen by political analysts as a deliberately hostile act against President Vizcarra, thereby escalating the political tensions in the country.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | carlos.munoz@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Forthcoming |

| Subscribe: | pirajaj@colptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

| COSTA RICA | |

| Website: | Click here to be redirected |

| Subscribe: | estudios.economicos@scotiabank.com |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including, Scotiabanc Inc.; Citadel Hill Advisors L.L.C.; The Bank of Nova Scotia Trust Company of New York; Scotiabank Europe plc; Scotiabank (Ireland) Limited; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Scotia Inverlat Casa de Bolsa S.A. de C.V., Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorised by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorised by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V., and Scotia Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.