FORECAST UPDATES

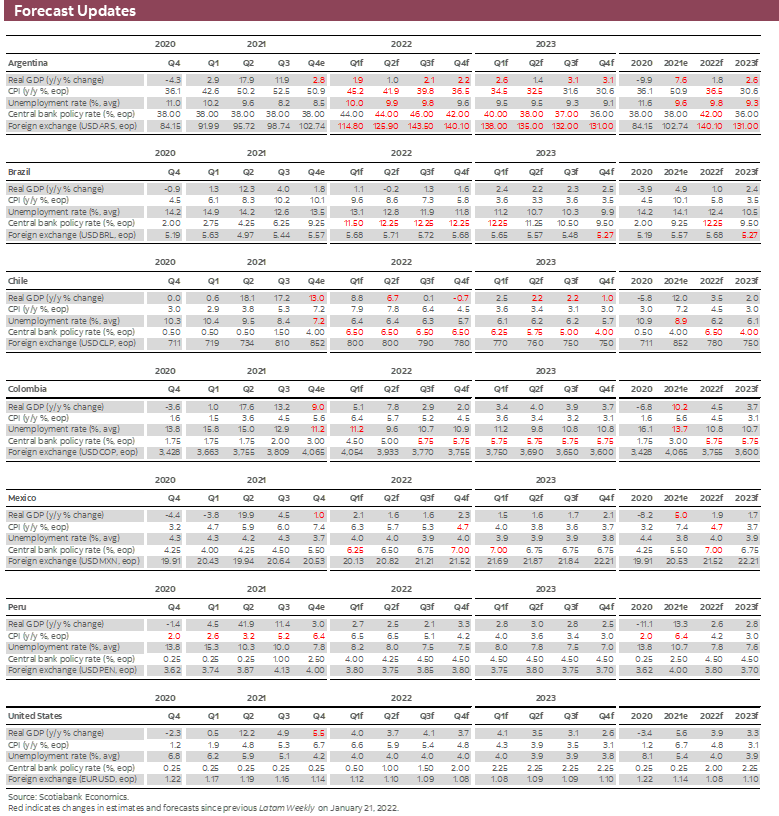

- Recent growth indicators in the Latam region remain strong, though Mexico is teetering on the brink of a technical recession, with advance GDP estimates showing two consecutive quarters of q/q contraction. Price pressures also remain high. Stronger growth and higher inflation continue to drive forecast revisions. See the full set of changes in the forecast update table below.

ECONOMIC OVERVIEW

- Central banks in the Latam region, and around the globe, confront price pressures emanating from supply-side shocks that push prices higher and constrain output. The risk is that higher inflation becomes embedded in inflation expectations in a process that may best be described as “gradually, then suddenly.”

- Latam central banks have already started to tighten policy. Brazil’s BCB and Mexico’s Banxico were early movers; other central banks have joined them in normalizing monetary conditions. In this respect, the region’s central banks, which adopted the inflation-targeting framework developed by their advanced country peers, are leading the way for other central banks.

- Their challenge going forward is to ensure that the pace of tightening is appropriate given the threat to inflation expectations and possible shocks to potential output.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Chile, Colombia, Mexico, and Peru.

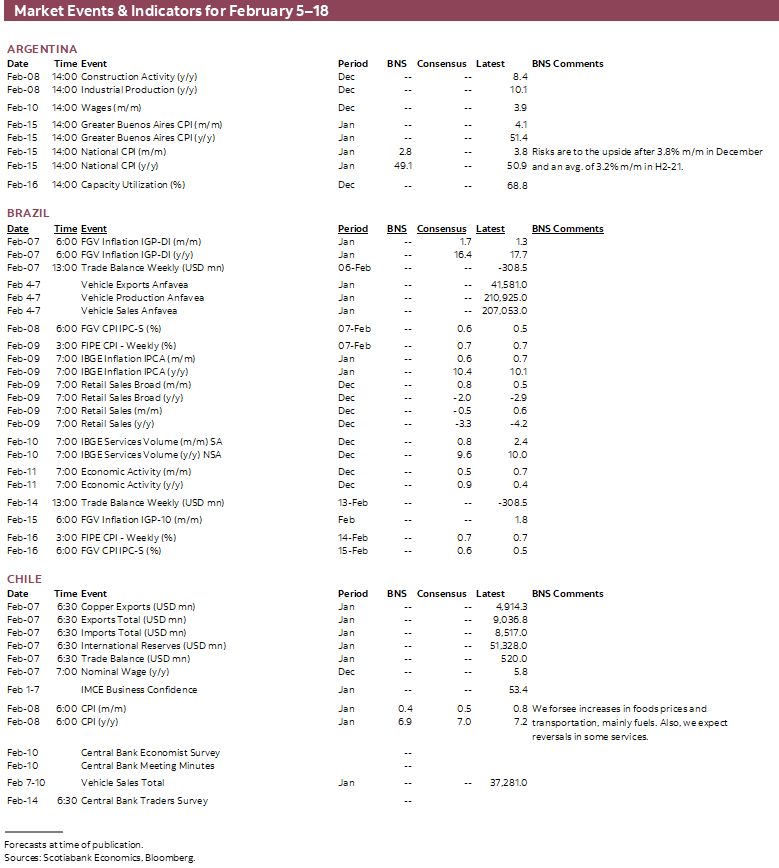

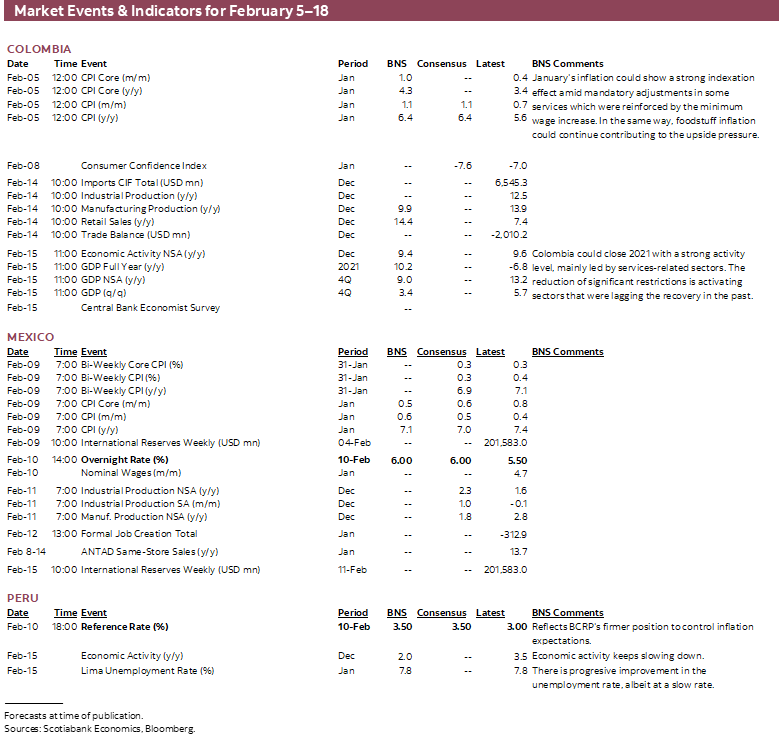

MARKET EVENTS & INDICATORS

- A comprehensive risk calendar with selected highlights for the period February 5–18 across the Pacific Alliance countries, plus their regional neighbours Argentina and Brazil.

Economic Overview: Inflation and the Macroeconomics of Supply Shocks

James Haley, Special Advisor

416.607.0058

Scotiabank Economics

jim.haley@scotiabank.com

- While there is reason to expect that the omicron outbreak will not derail economic recoveries in the Latam region, there is an important unknown clouding the outlook. That unknown is the longer-term impact of the pandemic on aggregate supply.

- Arguably, the last time that global supply shocks featured so prominently in the macroeconomic conjuncture was five decades ago. At the time, central banks viewed the effects of supply-side shocks on prices as temporary and sought to preserve full employment. Over time, inflation expectations were progressively ratcheted upwards in a “gradually, then suddenly” manner.

- Central banks then did not have what Latam central banks have today—a clear framework for decision-making provided by inflation targeting. And while the region’s central banks have already embarked on a tightening cycle to keep expectations firmly anchored to inflation targets, they will have to ensure that the pace of their tightening is appropriately calibrated.

- Understanding the effects of supply shocks on potential output will be critical. Unfortunately, central banks may only learn that their estimates are off, ex post. At that point, potential output estimates may likewise be adjusted in a “gradually, then suddenly” manner.

GRADUALLY, THEN SUDDENLY

As the wave of omicron variant cases starts to recede in countries which were affected the earliest, there is cautious optimism that economic recoveries will remain on track. This holds true in Latam countries that are now seeing caseloads crest. But a key unknown remains—that is whether omicron or some future variant will impart yet more shocks to global supply chains.

For Latam central banks busily ramping up the pace of monetary tightening, the answer to that question is critical to calibrating the appropriate pace of tightening. Across the region, and around the globe, central banks are confronting the discomforting fact that recent inflation has been generated by supply-side shocks that have disrupted global supply chains and created bottlenecks, as much as—or more than —by excess demand.

Over the past fifty years or so, periods of rising inflation were generally cases of excess demand—episodes in which aggregate demand exceeds potential output. More recent inflation, however, has reflected dislocations induced by the pandemic, coupled with abrupt shifts in the pattern of demand away from services, for example, to durable goods. To some extent, none of this should be surprising, given the truly unique nature of the “COVID-19 event”, as the pandemic is euphemistically referred to in official circles. Moreover, shifts in relative prices that push up the price level are not necessarily considered problematic in the macroeconomics literature, provided they do not unleash ongoing price pressures through overlapping contracts or become embedded in expectations.

Supply-side shocks are not necessarily the only source of price pressures, as the Mexico country update (below) makes clear. But there is little debate that they are an exceptionally important driver of the current high levels of inflation. In fact, we must go back to the oil price shocks of the 1970s to find another period in which supply considerations played such an important part in the inflation story.

At the time, central banks viewed price pressures as temporary, and because they viewed full employment as their primary mandate, they temporized with higher inflation. Over time, inflation that was initially perceived as “transitory” become embedded into inflation expectations. The process by which this transpired is akin to F. Scott Fitzgerald’s depiction of bankruptcy—it happened “gradually, then suddenly”. The moral of the story is that the eventual costs (measured in terms of foregone output and employment) increased as inflation—and expectations of future inflation—rose.

The upshot of the current conjuncture is that the current generation of central bankers is facing a fundamentally different challenge—the noxious combination of inflation and supply-constrained growth. It is different because inflation generated by excess demand does not pose the same challenge to central banks for the simple reason that, with output growing at or above potential output growth, there is no conflict in inflation control and full employment objectives. Supply-side shocks introduce the potential for conflicted virtue: the central bank may have to choose between its full employment and price stability commitments.

But while central bankers are facing a challenge not seen in 50 years, their policy frameworks are fundamentally different from those five decades ago. In this respect, the potential dilemma over full employment and inflation control may be less pressing for inflation-targeting central banks in the Latam region with well-defined objectives and a clear framework in which to achieve those objectives. In theory at least, such central banks do not have to balance the competing objectives of a dual mandate, which Paul Volcker—the legendary chairman of the Fed who vanquished the great inflation of the 1970s—once described as “operationally confusing and ultimately illusionary”.

As Scotiabank’s team in Mexico City notes in the country updates below, however, even “pure” inflation-targeting central banks seek to achieve their inflation targets by minimizing potential employment losses through an “efficient: disinflation process. Moreover, while the dilemma may be attenuated by inflation-targeting frameworks, supply shocks introduce additional uncertainty to monetary policy decision-making. This is because such shocks generate price pressures while constraining output, unlike aggregate demand shocks, which push output and prices up.

Central banks ignore this distinction at their peril. A supply-side shock that reduces the economy’s capacity to produce goods and services, or “potential” output in the macroeconomics lexicon, implies that price pressures will be greater for any given level of aggregate demand. In turn, this means that a central bank expecting to “efficiently” contain inflation with a projected path of tightening may be frustrated by inflation that is stubbornly persistent. And this failure could result in a ratcheting up of inflation expectations as workers and firms incorporate higher future inflation into wage demands and pricing decisions. That is the risk central banks run in delaying their responses to rising inflation, even if expectations appear to be well anchored. As noted above, expectations can become untethered “gradually, then suddenly”.

Fortunately, while most advanced economy central banks have thus far hesitated pulling the trigger on rate hikes (the Bank of England being the exception), central banks in the Latam region have been more proactive. All have begun to normalize monetary policy, withdrawing some of the stimulus they provided in the pandemic. And as more data have come in, the region’s central banks are evaluating whether they have the calibration right; that is to say, whether the pace of rate hikes and other measures, such as BCRP’s reserve requirements increases in Peru, is sufficient to keep inflation expectations moored firmly to their inflation targets.

As Scotiabank’s team in Colombia argue in the country update section below, BanRep has conducted such an assessment and has adjusted policy accordingly. Our economists in Bogota note that a decomposition of three critical factors behind the calibration of policy rates points to the need for the central bank’s accelerated pace of rate hikes, which kicked off with a gradual 25 bps increase. The pace of tightening picked up, however, as the estimated neutral real rate—the real interest rate required to keep inflation on target and stabilize output around potential—was raised, inflation expectations rose, and the potential output gap (the difference between actual and potential output) narrowed more quickly than previously expected.

Other central banks in the region are likewise carefully watching these indicators, particularly where growth has rebounded stronger and more quickly than anticipated. In Chile, for example, the MoF’s recent revision to GDP highlights the potential risk of layering strong demand on top of supply-side shocks that could result in a marking down of potential growth estimates. Similarly, as the discussion in the country notes section below makes clear, the robust recovery in Peru—that has pushed growth up despite pervasive political uncertainty that fueled record capital outflows—is the context in which the BCRP has both raised rates and constrained credit growth by raising reserve requirements.

Going forward, the challenge for Latam central banks is to accurately assess the extent to which past COVID-19 waves and future variants impair supply responses in the economy. The task is all the more difficult because potential output is inferred over time, not observed. And central banks will only know if their estimates are off, ex post, once they are proven incorrect. Revisions to potential output may thus also come “gradually, then suddenly”.

PACIFIC ALLIANCE COUNTRY UPDATES

Chile—Positive Year-End Paves Way for 3.5% GDP Growth

Jorge Selaive, Head Economist, Chile

+56.2.2619.5435 (Chile)

jorge.selaive@scotiabank.cl

Anibal Alarcón, Senior Economist

+56.2.2619.5465 (Chile)

anibal.alarcon@scotiabank.cl

Waldo Riveras, Senior Economist

+56.2.2619.5465 (Chile)

waldo.riveras@scotiabank.cl

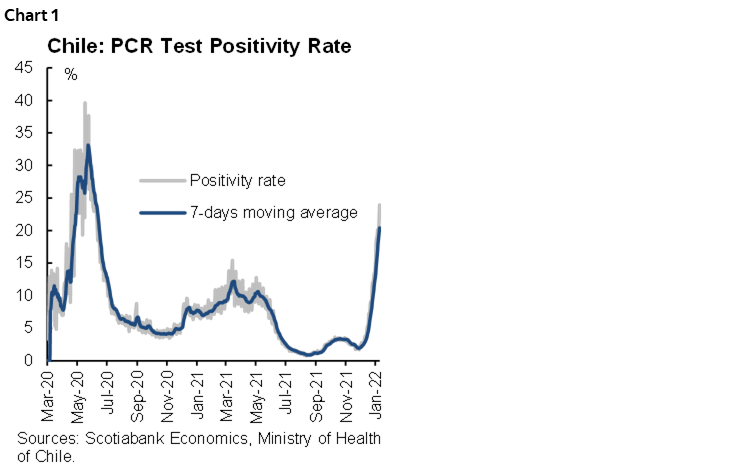

Owing to the advance of the omicron variant, the daily number of confirmed COVID-19 cases increased sharply in recent days, reaching its highest level since the beginning of the pandemic. The positivity rate rose to 24% (chart 1). The occupancy rate of ICU beds is slowly increasing, while the COVID-19-related death rate remains low. Meanwhile, the vaccination campaign reached 92.7% of the eligible population. The rollout of booster (third) doses continues—reaching 11.8 million people—and the new booster dose (fourth) is in progress.

On Wednesday, January 26, the central bank (BCCh) surprised markets and Scotiabank Economics with a 150 basis points (bps) increase in the benchmark Monetary Policy Rate (MPR), to 5.5%. In our view, the BCCh is potentially facing the most worrisome de-anchoring of inflation expectations in the last two decades. While expectations of inflation three years ahead are slightly above 3%, the market now expects the MPR to reach 7.0% in the first half of this year. In such situations, gradual increases in the benchmark rate may prove insufficient to reverse expectations. Three conditions must be satisfied to contain this type of de-anchoring: first, that the MPR move decisively into restrictive territory; second, disinflationary surprises compared to market expectations; and third, an easing of inflationary pressures (slower consumption growth and Chilean peso appreciation).

Meanwhile, recent data point to continued labour market recovery. On Monday, January 31, Chile’s statistical agency (INE) published data on the unemployment rate for the quarter ending in December 2021, which fell to 7.2%. The decrease in the unemployment rate compared to the last quarter was explained by an increase in job creation (+1.4% m/m) that outpaced labour force growth (+1.0% m/m). The unemployment rate fell to 8.9% on average during 2021 compared to 10.8% in 2020. The labour market created 120k new jobs in the final quarter of 2021, resulting in a further narrowing of the employment gap relative to pre-pandemic levels.

Data on economic activity are more mixed. On Tuesday, February 1, the central bank published December’s Imacec index of economic activity, which grew 10.1% y/y. Services (business and health) and trade largely explained the y/y economic growth. Goods production also contributed positively to the y/y increase, highlighting the performance of construction. On a m/m basis, however, goods production and trade showed weakness in December. The Imacec fell 0.4% m/m, which is mainly explained by the negative performance of mining (-6.2% m/m). The Imacec of the manufacturing industry fell -1.4% m/m, registering its second consecutive drop after six months of expansion. Trade also fell -1.4% m/m, continuing the slowdown that has been dragging on for a few months, after the high level it reached in the middle of the year fueled by fiscal transfers and pension fund withdrawals.

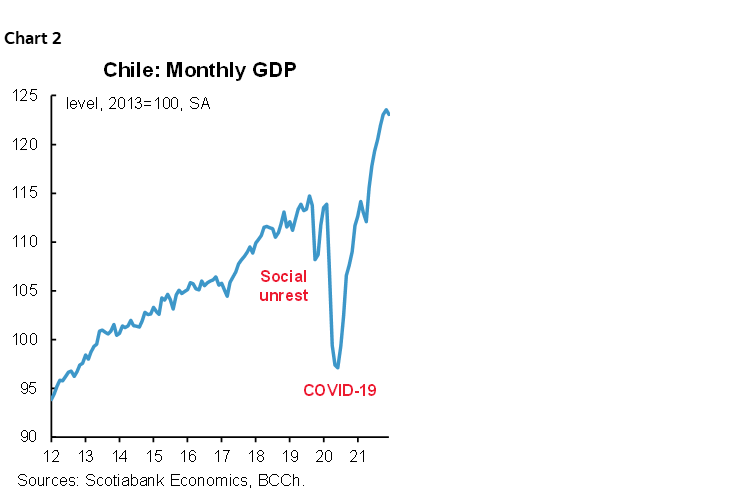

All in all, GDP is likely to have grown 12% in 2021, in the upper part of the range of the central bank’s projection made in December. And while GDP contracted in December in seasonally adjusted terms, we consider that the high level with which it began 2022 provides solid growth support for the year ahead, which is likely to see an expansion of 3.5% (chart 2).

In the political arena, on Wednesday January 26, Congress passed the bill creating the Universal Guaranteed Pension (PGU) and its financing. The initiative will provide a contribution of up to CLP 185,000 (USD 231) on an annual basis for all those over 65 who are in the 90% of the lowest income brackets, whether they are retired or not, benefiting 2.2 million people. According to government estimates, the first stage of benefit payments will begin in the third week of February, targeting around 1.5 million people. According to Scotiabank estimates, the PGU could contribute around 0.2–0.3 percentage points of additional GDP growth in 2022 owing to the positive impact that will have on the private consumption.

On Friday January 28, the Ministry of Finance reported issuing Treasury bonds in international markets totaling USD 4 bn, as part of the government’s 2022 financing plan. For 2022, the government’s plan considers issuing Treasury bonds for a total of USD 20 bn, within the debt limit authorized by the 2022 Budget Law, of which USD 6 bn corresponds to foreign currency offerings. With the current issuance, USD 2 bn remains to be issued in foreign currency.

In the fortnight ahead, on February 8, the INE will release January’s CPI, for which we expect an increase of 0.4% m/m (6.9% y/y), mainly due to a rise in food prices and fuels.

Colombia—Changes in Reaction Function Elements Lead to a Higher Terminal Rate

Sergio Olarte, Head Economist, Colombia

+57.1.745.6300 Ext. 9166 (Colombia)

sergio.olarte@scotiabankcolpatria.com

Jackeline Piraján, Economist

+57.1.745.6300 Ext. 9400 (Colombia)

jackeline.pirajan@scotiabankcolpatria.com

An uneven but faster recovery in economic activity together with much higher-than-expected inflation have posed an unusual significant challenge to central banks in terms of calibrating the appropriate pace of monetary tightening. This task is especially challenging given the pervasive uncertainty that remains regarding pandemic/omicron developments and because bottlenecks in the distribution channels can produce an abrupt deceleration in economic activity along with higher inflation.

Of course, the Colombian central bank (BanRep) is not exempted from this challenge. In fact, BanRep has transitioned from a very dovish and gradual approach to hawkish guidance in just a couple of months. The central bank started its hiking cycle in September’s meeting with a 25 bps increase. BanRep accelerated the pace of tightening to 50 bps hikes in October and December 2021, further increasing that pace with a 100 bps hike in January, which is the highest increase since the inflation-targeting framework started in 2000.

Given this 180-degree shift in policy stance from gradual to hawkish hikes, it is important to analyze the reasons behind the change in BanRep guidance. We examine BanRep’s reaction function to better understand the dynamics of the recent Colombian hiking cycle and to anticipate what may happen under an assumption that, in the base case scenario, the terminal real rate adjusted for expected inflation. It should be noted, however, that if external imbalances remain high, and financing current account deficits proves challenging, the terminal rate could exceed this base case scenario to restore external balance.

A conventional reaction function incorporates three main components: i) an estimate of the neutral rate, typically specified in real terms, that ensures inflation remains “on target” and output growth is consistent with potential growth; ii) a measure of the inflation gap—that is, the difference between actual inflation and targeted inflation; and iii) a projected output gap estimate, or the gap between actual output and (estimated) potential output. So, what has changed to increase the pace and, probably, the expected terminal rate?

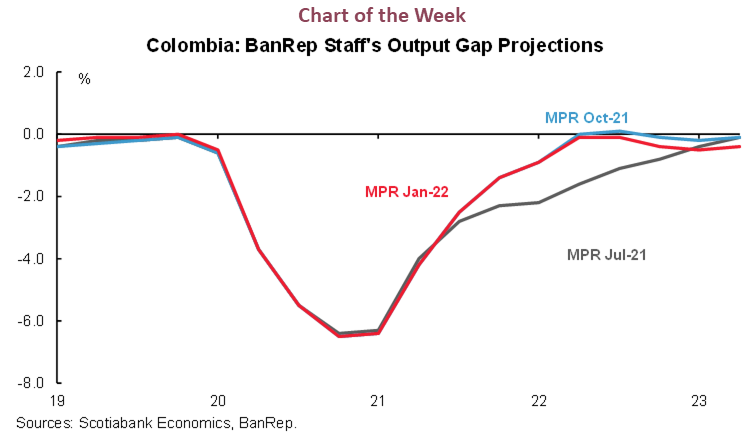

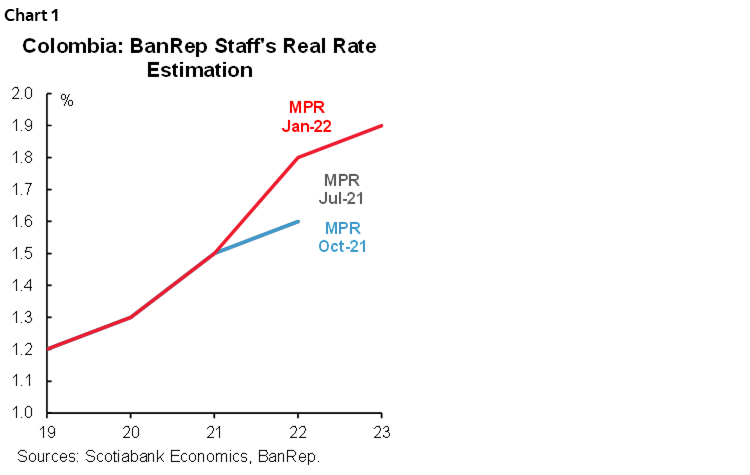

i) First, the neutral rate estimate. According to BanRep’s staff, up to December 2021, the neutral real rate did not change, maintaining a level between 1.5 and 1.6%, despite a more hawkish Federal Reserve and higher interest rates in emerging markets. For January’s forecasts, however, BanRep increased the neutral rate to 1.9% (chart 1), which tells us that the new terminal rate in the base case scenario is around 50 bps higher.

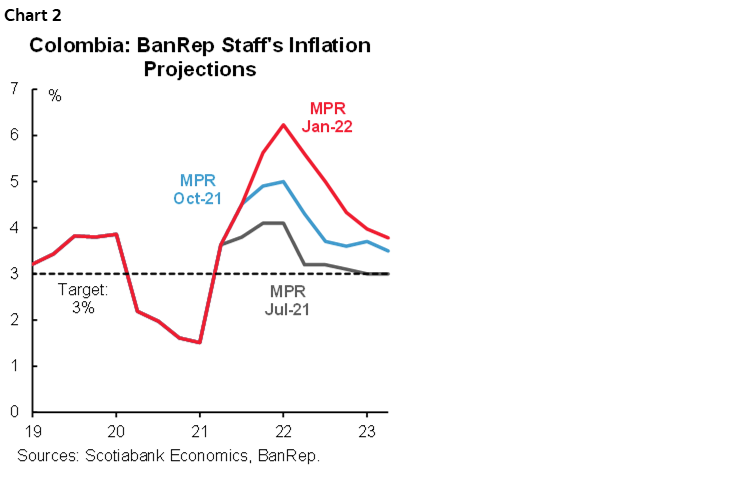

ii) Second, the inflation gap. This indicator has changed significantly since BanRep started to signal that a normalization of monetary policy was needed. In July’s Monetary Policy Report, the staff projected inflation to end 2021 at 4.1%, converging to target in 2022 at 3.1%, while in October they updated inflation forecasts to 4.9% for 2021 and 3.6% to 2022 (chart 2), adding that core inflation could increase more than initially expected. For November’s policy meeting, the staff signaled concerns of higher inflation and inflation expectations, which led the Board to speed up the hiking cycle. By January, however, BanRep was faced with 2021 inflation at 5.6% and 2022 headline inflation expected to again exceed target at 4.3% (4.5% for core inflation). Meanwhile, recent upward surprises in the headline over the past five months have ratcheted up market expectations for year-end inflation above the target range (4.4%) and for year-end 2023 inflation from 3% to 3.5%. And in our opinion, the recent significant increase in spot headline inflation and longer-run inflation expectations is the main reason the Board surprised the market in January and hiked its policy rate by 100 bps to 4%. The threat of inflation expectations becoming unmoored also supports the case for expecting 100 bps increase in March as BanRep moves to reach the neutral rate as quickly as it can.

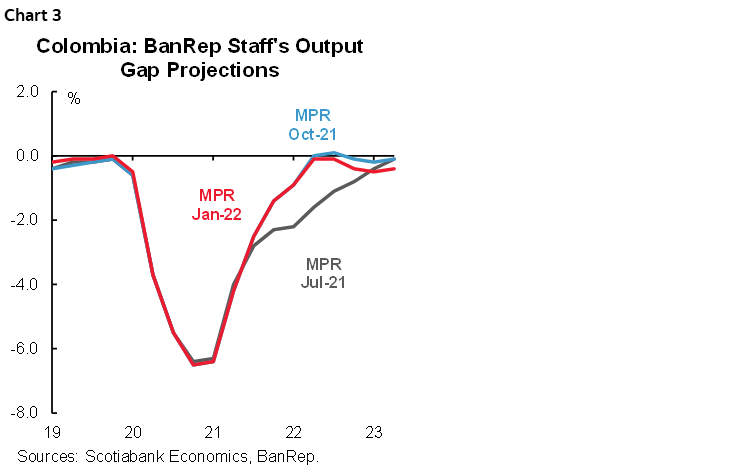

iii) Third, the output gap. Initially, the output gap was the main reason BanRep started the normalization process with a conventional 25 bps pace in September. In July of last year, for example, the central bank expected an output gap of -2.3% in 2021 which narrowed relatively quickly in 2022 to -0.8% (chart 3). By October, however, BanRep staff realized that the economy was growing faster and reduced the negative output gap estimate to -1.4% for 2021 and -0.1% for 2022. Interestingly, the relaxation of mobility restrictions did not produce major changes in the output gap estimates. In fact, in January’s inflation report, staff estimated that in 2021 the output gap remained at -1.4%, and that 2022 will be -0.4%. These projections imply that the economy is no longer in need of monetary stimulus since the pace of recovery could increase as employment returns to pre-pandemic levels.

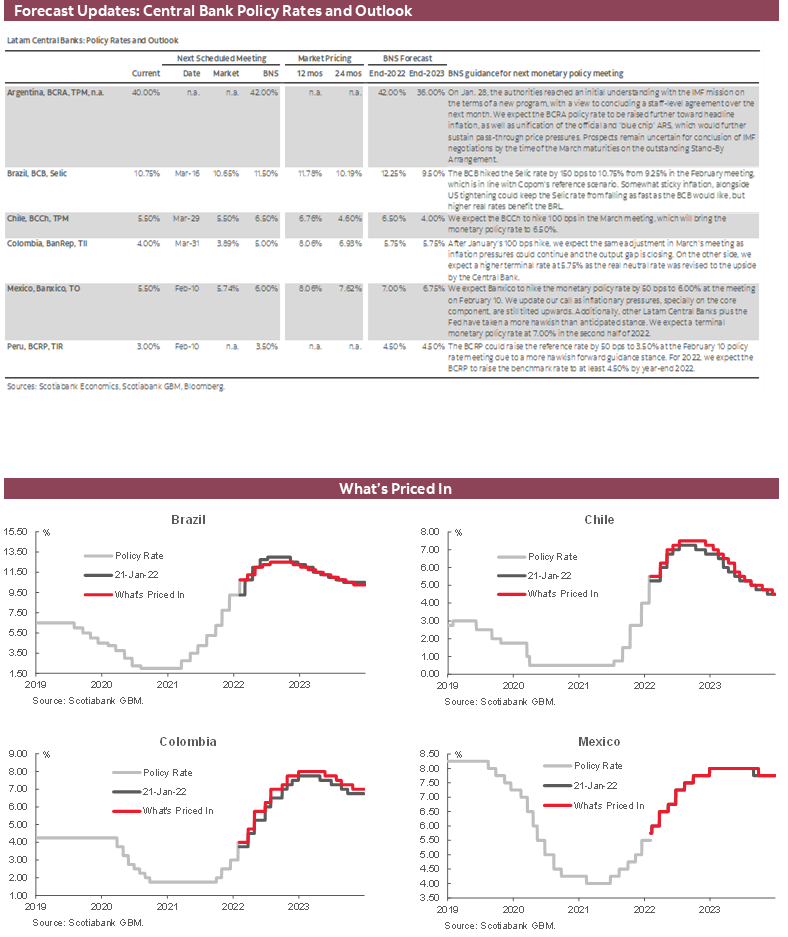

This reaction function perspective illustrates that higher inflation and, more important, higher expected inflation for 2022 and 2023, both by the market and BanRep staff, explain why the central bank has accelerated the pace of its policy rate normalization. At the same time, because the economy has responded positively to reopening strategies and has achieved pre-pandemic levels much faster than initially anticipated, we do not see the pace slowing so that a neutral rate is achieved faster than previously expected. Finally, since the neutral rate estimates have increased, and longer-run inflation expectations also have risen, the terminal rate should be higher. We calculate that the terminal rate should be between 5.5% and 6%, depending on the expected inflation measure used. Taking the average of expected inflation metrics, we have updated our terminal rate to 5.75% by June 2022, with one more hike of 100 bps in March, 50 bps in April and a final 25 bps in June.

Mexico—Banxico, Caught Between Inflation and a Contracting Economy

Eduardo Suárez, VP, Latin America Economics

+52.55.9179.5174 (Mexico)

esuarezm@scotiabank.com.mx

The upcoming Banxico call is difficult for us to predict. But we imagine that it will also be a particularly difficult decision for the Board, which is caught between inflation and contracting economy. And while Banxico is a pure inflation-targeting central bank, it is also true that since Governor Carstens was in command, it has adopted somewhat of an efficient convergence to target mandate (Carstens used the term to define an approach that seeks to control inflation within its relevant time horizon, with the smallest possible cost to growth, as most central banks do today).

At this point in time, the economy is in a difficult spot. Inflation is north of 7% (consensus expects a 7.01% y/y print for January to be published the day before the meeting), and core inflation sits at 6%—over twice the mid-point of the central bank’s target. At the same time, advance Q4 GDP estimates revealed a second consecutive quarter of q/q contraction, putting the economy in a technical recession. (Although two sequential quarters of contraction don’t necessarily mean there is a recession, the fact remains that the economy is currently around 7% smaller than it was in 2018 in real terms.) In short, the economy is stuck in a flat growth, high inflation environment.

In addition, the first few data releases for the start of 2022 have not been particularly rosy, with IMEF’s services PMI at 49.0 (consensus anticipated 51.9) and manufacturing at 48.8 (consensus expected 51.8), both results in contraction territory, below the 50 mark. Meanwhile, the recently published Banxico Survey of Economists’ Expectations showed a decline in the 2022 GDP forecast, which now anticipates an average growth of 2.27%, down from 2.79% in the previous version of the survey, just one month earlier. The same survey showed an increase in inflation expectations to 4.42% y/y for year-end 2022, up from 4.22% y/y the month before. So far, data and expectations for this year are not trending in the right direction.

With respect to the implications for monetary policy, we have argued that the current inflation shock is not only driven by supply chain disruptions. In our view, several other factors are also at play, including: a) strong demand for goods (in sectors where demand is already at pre-crisis levels, and where consumer habit shifts could have an enduring component); b) cumulative producer price inflation (driven in part by policy decisions such as the outsourcing regime restrictions, minimum wage hikes, corporate tax collection increases, etc.); and c) price formation process contamination, as higher expected inflation is embedded in price and wage setting. Regarding this final point, economists’ inflation surveys show that inflation is expected to converge to target at a slower pace than Banxico anticipates, while producers are even looking to further increase their prices. Hence, in our view, a monetary policy response to the inflation shock is clearly warranted.

On the flip side, while the economy has contracted in the last two quarters, it is noteworthy that demand has rebounded strongly, as evidenced by the very large trade deficits recorded in H2-2021, which were partly driven by imports that are now well above pre-pandemic levels. Moreover, even though total private consumption remains about five percentage points off its pre-pandemic peak, demand for goods has basically fully recovered. The notable laggard in the Mexican economy for the past three years has been investment, but weak investment was evident well before the pandemic. And we don’t believe that investment’s underperformance is attributable to high interest rates—or to the pandemic (investment dropped 4.5% in 2019).

With the foregoing in mind, we argue that there is a case to be made to continue reducing monetary policy stimulus to avoid an inflationary spiral (and even to tighten settings a little). In this regard, we are not convinced that loose monetary policy is going to substantially help the lagging growth sectors (low rates, for example, would not produce more microchips or bring back private confidence).

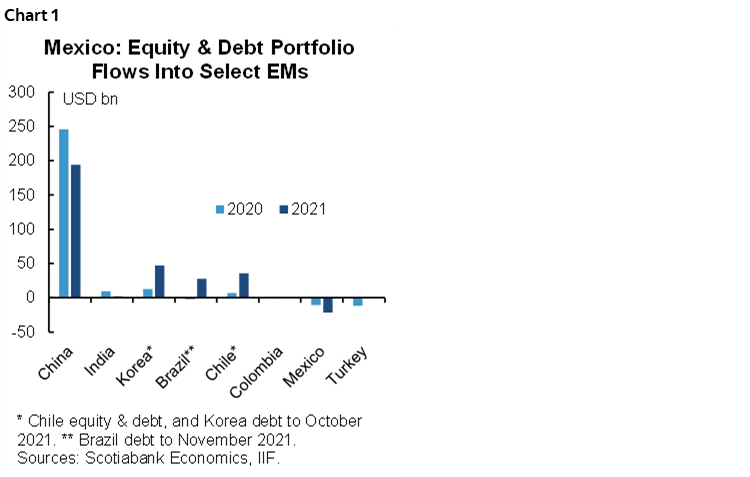

Moreover, recent actions and signals sent by regional central banks could also prompt Banxico to once again hike rates by 50 bps, to help anchor domestic capital markets. It is notable that so far in 2022, four of the six top-performing currencies among the most liquid 32 are in Latam (BRL +7.6%, CLP +4.96%, COP +3.3% and PEN +2.8%), while MXN is in negative territory YTD (-0.2%). Chile, Colombia, and Brazil have all seen triple-digit rate hikes in their latest central bank decisions—even if they did start the cycle with much looser settings. Part of MXN’s underperformance could reflect a catch-up effect, but current negative real policy rates (-150 bps) and an economy in technical recession are likely not helping. According to the IIF’s portfolio flows data, Mexico is one of the rare EMs where portfolio flows were negative in both 2020 and 2021, and which also saw an acceleration of outflows into 2022 (chart 1). Over the past two years, Mexico’s debt and equity markets lost around USD30 bn in foreign portfolio flows.

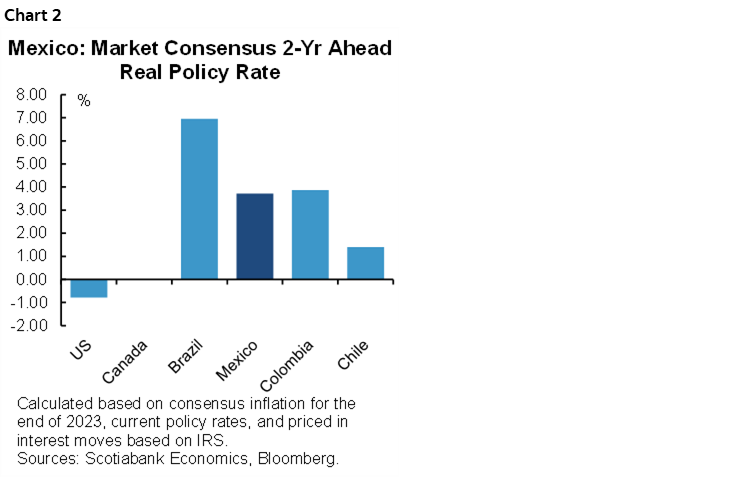

With all this in play, the TIIE curve is pricing in another 190 bps of hikes by Banxico over the next two years, up from the current policy rate of 5.5%. And while we do not anticipate a terminal rate of 7.5%, as the TIIE curve is pricing-in, we are revising our terminal rate call to 7.0%, from 6.75% previously, as we anticipate that inflation will be a bit stickier. For the February 10 meeting, we are revising our call from a low conviction call of a 25 bps hike to a low conviction call for a 50 bps hike. (We think there are arguments for both a 25 bps and 50 bps hike, while the Board is tough to read, with a new governor in place and with Deputy Borja being relatively dovish). Contributing to our more hawkish expectation are more aggressive rate hikes elsewhere in the Latam region (Chile hiked 150 bps on January 26), as well as more hawkish signaling from the Fed, which has continued to drive a more aggressive tightening cycle to be priced into the US yield curve. Markets (local yield curves and consensus inflation expectations) are anticipating that Mexico and Colombia will have similar real policy rates in two years, somewhere in between rates in Brazil and Chile (chart 2). Our call would put Mexico’s real rates in between what markets anticipate for Chile and Colombia.

Peru—Political and Economic Outlook 2022

Mario Guerrero, Deputy Head Economist

+51.1.211.6000 Ext. 16557 (Peru)

mario.guerrero@scotiabank.com.pe

I. Where we come from: A disconnected economy in 2021

2021 was a year of great political uncertainty. And yet, there is not much evidence that political turbulence affected growth. GDP not only grew more than many analysts expected at the beginning of the year—13.3% y/y is our current estimate, while the market consensus at the beginning of 2021 was 9.5% (Latinfocus, January 2021)—but was 0.8% above the 2019. Moreover, by end-2021 most economic activity indicators already exceeded the pre-pandemic levels of 2019, something that was not expected to happen before 2022.

In short, macroeconomic balances show strong results. However, political uncertainty did have an impact, which was particularly evident in the financial and FX markets. The uncertainty and risk perception of a large part of the population triggered an unprecedented capital outflow, exceeding the previous record by seven times.

How do you reconcile an economy that is growing so strongly on the real side with such a high degree of mistrust in financial markets? To start with, the real economy is more resilient than in the past. This probably has to do with factors such as government programs that kept the payment chain intact and provided support to consumption, allowing a quick rebound; a favourable global environment mainly in metal prices; a government transition that did not feature institutional, political, or economic breakdowns; the existence of a middle class that has provided more support to domestic demand; and greater digitization, which has made transactions more fluid and easier. Had it not been for these factors, perhaps the 2020 crisis would have continued in 2021, as would have been the case in times past. At the same time, however, one is left with the feeling that growth could have been considerably higher had there not been so much political uncertainty and turbulence.

II. 2022: Adapting to the circumstances

Owing to the new omicron variant, 2022 has started with a record increase in COVID-19 cases, exceeding 50,000 cases per day at the end of January. But there are differences from past waves: Peru has already vaccinated at least 80% of the population over 12 years of age with two doses and the death rate associated with omicron are lower than past variants. Consequently, the country is moving from policies of immobility to one of living with the virus. The government recently lifted the nationwide curfew restriction, and while the future of the pandemic is not predictable, our assumption is that there will be no significant mobility restrictions in 2022. Whatever restrictions may be imposed in 2022, they will occur in a slowing economy, which is a very different situation from last year.

As of February, the number of cases is starting to decline and there is a feeling that perhaps the worst is over and things will soon return to normal. But then, just when you start to feel relieved, you remember: politics!

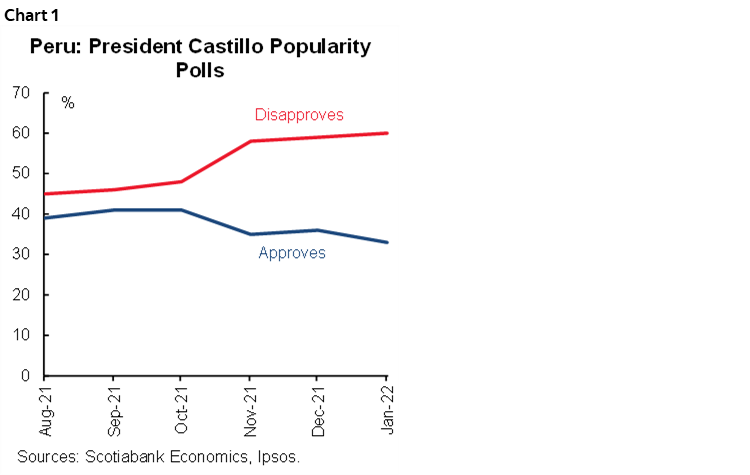

2022 begins with a new episode of political tension that has led to the appointment of a new Cabinet, the third in six months. The previous Cabinet chaired by Mirtha Vasquez lasted only four months, from October 2021 to January 2022. Though it had a moderate profile in general, it did not resolve underlying problems, so the president’s disapproval rating was increasing (64% in January according to an IEP survey). Meanwhile, the change of Cabinet reflects that the frictions within the government continue. The appointment of the Cabinet chaired by Hector Valer has been criticized for supporting the Constituent Assembly, the inclusion of inexperienced ministers, and police complaints regarding some of its members, and for what is perceived as a step backwards in government management. The signal from the Valer Cabinet is that the frictions with Congress, and therefore the political uncertainty, will continue. This leaves us with the feeling that the country is adjusting to a situation of lasting political discomfort. President Castillo’s popularity has been weakening during the first six months of government, reaching a level of disapproval of 62% in January according to an IEP survey (chart 1).

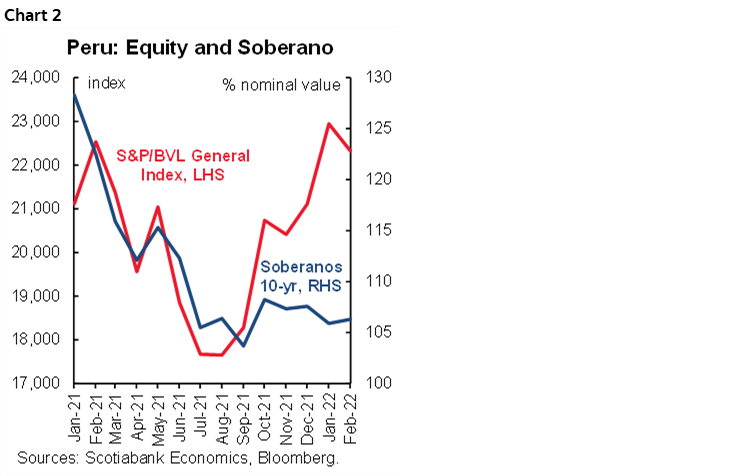

The highlight of the new Cabinet is the appointment to the Ministry of Finance of Oscar Graham, who succeeds Pedro Francke. Graham has a more technical profile and experience at the BCRP and the MoF. This is a powerful signal that economic stability will be maintained, and that Peru will not implement abrupt changes in its economic model. In this respect, the market’s reaction to this episode of political turbulence has been moderate, with a drop of almost 3% in the Lima stock market and a slight improvement in the prices of Peru’s sovereign bonds (chart 2).

Regional and municipal elections to be held on October 2 are also on the political agenda. These elections do not usually generate enough turbulence to affect the economy, though in the past they have not been held in a context as complicated as this year. Given the polarization that exists in the country, and in the political community in particular, Peru will be subject to political risk events in 2022, including the risk of social conflicts such as those that had a temporary but material impact on mining production in 2021.

Against this background, we expect GDP growth of 2.6% in 2022. The political environment makes it difficult for the economy to grow at the rate of its potential. At the same time, the economy may not be subject to situations as unusual as the 2020 economic shutdown, or the 2021 rebound. Admittedly, a growth rate of 2.6% is low. But the problem with projecting stronger growth is finding a motor. The 5.5% growth in volume of exports will contribute, led by agribusiness and the contribution of mining production from new projects such as Mina Justa and, in an incipient form, Quellaveco and the Toromocho Expansion. Public investment will also contribute to growth; based on the public budget for 2022, we expect it to grow 4.4%. There is room for public investment to grow more, especially in terms of the country’s infrastructure, if the national government gave it more priority. That said, the limited capacity of the different levels of government to invest remains a challenging structural problem. Consumption has been somewhat more difficult to estimate. Several factors have distorted consumption in the last two years, including government programs and savings withdrawals. We do not contemplate a new withdrawal of pension funds, although that is not impossible. The government has announced that it is considering an increase in the minimum wage, something that we hope will materialize, though of limited magnitude. In general, the weight of these positive factors from the past will be less in 2022, and consumption should once again be more in line with labour dynamics.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Forthcoming |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

| COSTA RICA | |

| Website: | Click here to be redirected |

| Subscribe: | estudios.economicos@scotiabank.com |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.