ECONOMIC OVERVIEW

- Next week will gravitate around monetary policy announcements in Chile, Mexico, and Brazil—and in several EM and DM peers—on the heels the Fed and the ECB delivering as-expected rate decisions but hawkish guidance.

- All three of the Latam CBs meeting next week will likely leave policy unchanged, but we believe that the BCCh and the BCB will adjust guidance to tee up the start of their easing cycles in July and August, respectively.

- Banxico officials just started the pause stage of the cycle when they left the overnight rate steady at 11.25% in May and they’ve guided no changes for at least two or three meetings.

- With a quiet week ahead in Peru, our Lima economists analyse the underwhelming April GDP data released earlier this week.

- In Colombia, economic activity and international trade figures are on tap. BanRep is the last of the central banks that we cover to decide on policy this month, on the 30th. In today’s report, the team shares their thoughts on fiscal, reform, and market developments of the past week.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Chile, Colombia, Mexico and Peru.

MARKET EVENTS & INDICATORS

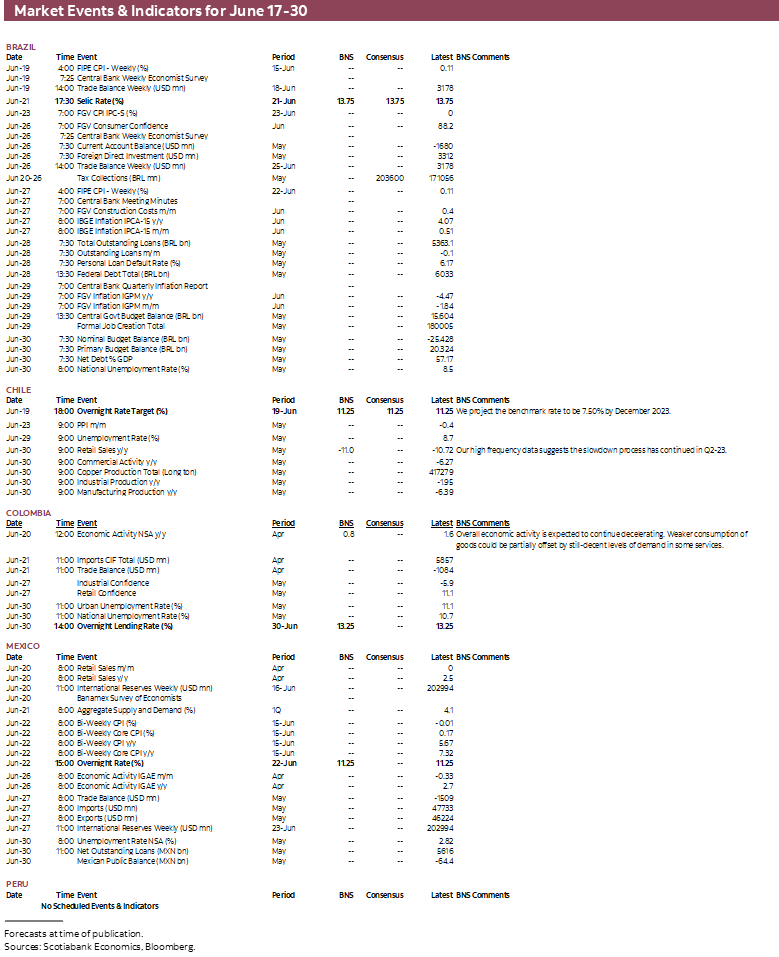

- A comprehensive risk calendar with selected highlights for the period June 17–30 across the Pacific Alliance countries and Brazil.

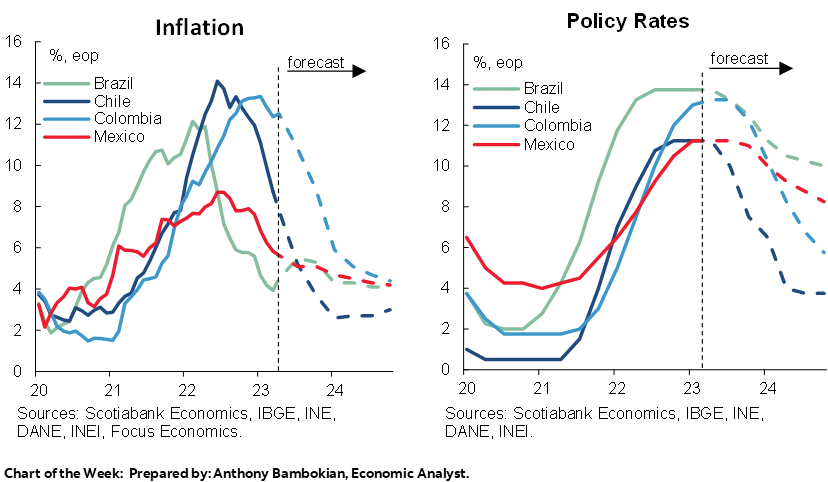

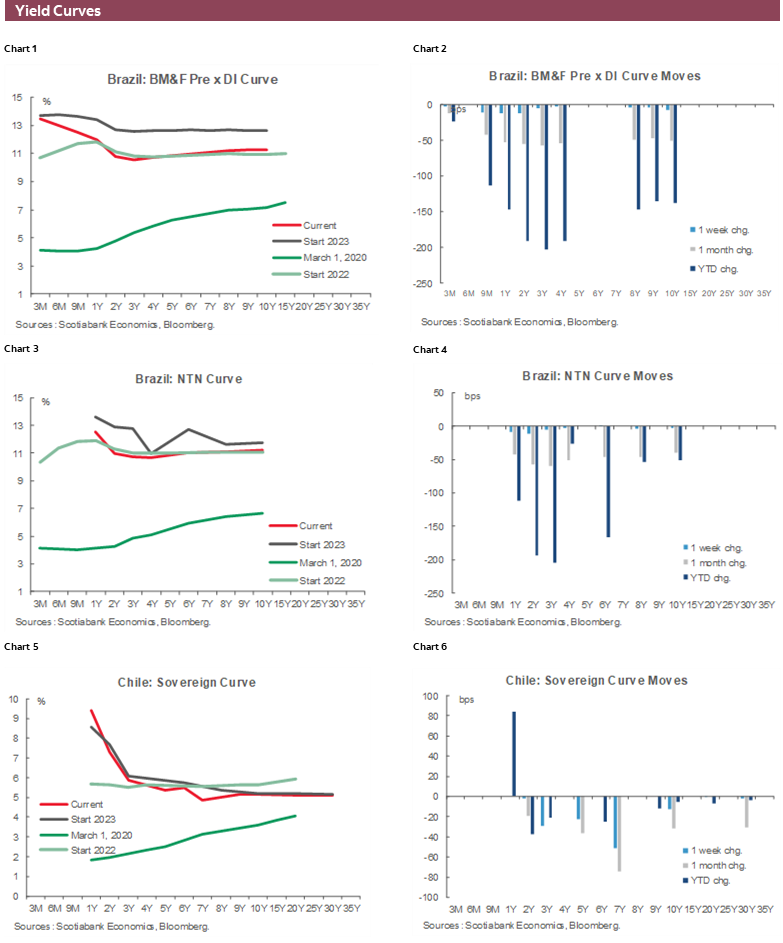

Charts of the Week

ECONOMIC OVERVIEW: DECISIONS, DECISIONS

Juan Manuel Herrera, Senior Economist/Strategist

Scotiabank GBM

+44.207.826.5654

juanmanuel.herrera@scotiabank.com

- Next week will gravitate around monetary policy announcements in Chile, Mexico, and Brazil—and in several EM and DM peers—on the heels the Fed and the ECB delivering as-expected rate decisions but hawkish guidance.

- All three of the Latam CBs meeting next week will likely leave policy unchanged, but we believe that the BCCh and the BCB will adjust guidance to tee up the start of their easing cycles in July and August, respectively.

- Banxico officials just started the pause stage of the cycle when they left the overnight rate steady at 11.25% in May and they’ve guided no changes for at least two or three meetings.

- With a quiet week ahead in Peru, our Lima economists analyse the underwhelming April GDP data released earlier this week.

- In Colombia, economic activity and international trade figures are on tap. BanRep is the last of the central banks that we cover to decide on policy this month, on the 30th. In today’s report, the team shares their thoughts on fiscal, reform, and market developments of the past week.

Next week will gravitate around monetary policy announcements in Latam—and in several EM and DM peers—on the heels of the top global central banks, the Fed and the ECB, delivering as-expected rate decisions but hawkish guidance (pause and +25bps, respectively). Officials in other countries, such as in Japan, stuck to an unchanged dovish message while in China the PBoC rolled out rate reductions to support the weaker-than-expected economic recovery.

Before delving into the week ahead for our core Latam coverage, here are some of the other countries where global central banks will make rate announcements next week: Hungary, Czechia, Philippines, Indonesia, Switzerland, Norway, the UK, Turkey, Egypt, and Paraguay. None of these central banks are seen cutting rates, all are expected to increase or maintain the status quo.

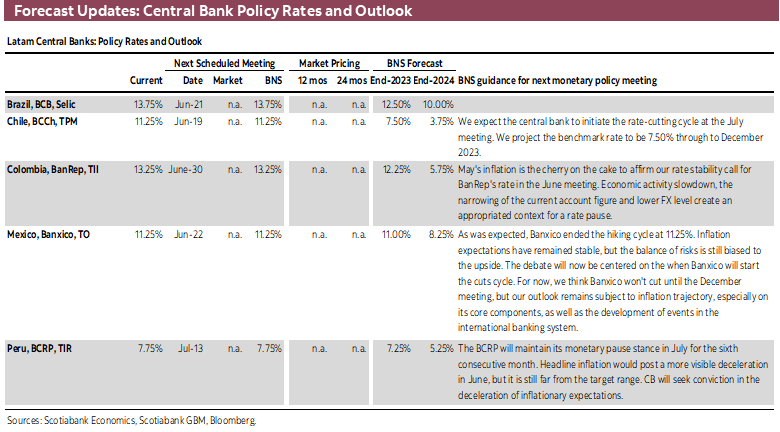

Likewise, the time has not yet come for rate cuts in Chile, Brazil, or Mexico, whose central banks’ decisions are due over the coming week.

Ahead of this, the BCRP left its policy rate unchanged last week while checking its optimism on inflation. But economic data are not looking good, and April GDP figures released yesterday were underwhelming, missing even the weakness that had been teed up by Fin Min Contreras. Our Lima economics team analyses these data in today’s weekly, ahead of a quiet data period in Peru until the release of June CPI data a couple of weeks from now.

Colombia’s BanRep is not scheduled to decide on policy until late June. In the interim, economic activity data for April out on Tuesday will give us a headline read of the country’s performance after industrial/manufacturing production and retail sales figures out on the 15th highlighted an ongoing growth deceleration. With this in mind, our economists anticipate that BanRep will leave its policy rate unchanged on the 30th, thus beginning the on-hold phase of the cycle. Earlier this week, Colombia’s Ministry of Finance presented its Medium Term Fiscal Framework that showed greater expected deficits in 2023 and 2024, with increased COLTES issuance as a result. In today’s weekly, the Bogota team shares their thoughts on fiscal, reform, and market developments of the past week.

The Santiago team argues that the BCCh will go into its rate decision on Monday with well-anchored inflation expectations among economists and traders (surveyed by the bank), and breakeven markets. The bank is not expected to make a rate adjustment, but guidance will likely have clear changes and new projections out on Tuesday that show a lower inflation forecast should reflect a rate path that anticipates over 100bps in cuts in Q3.

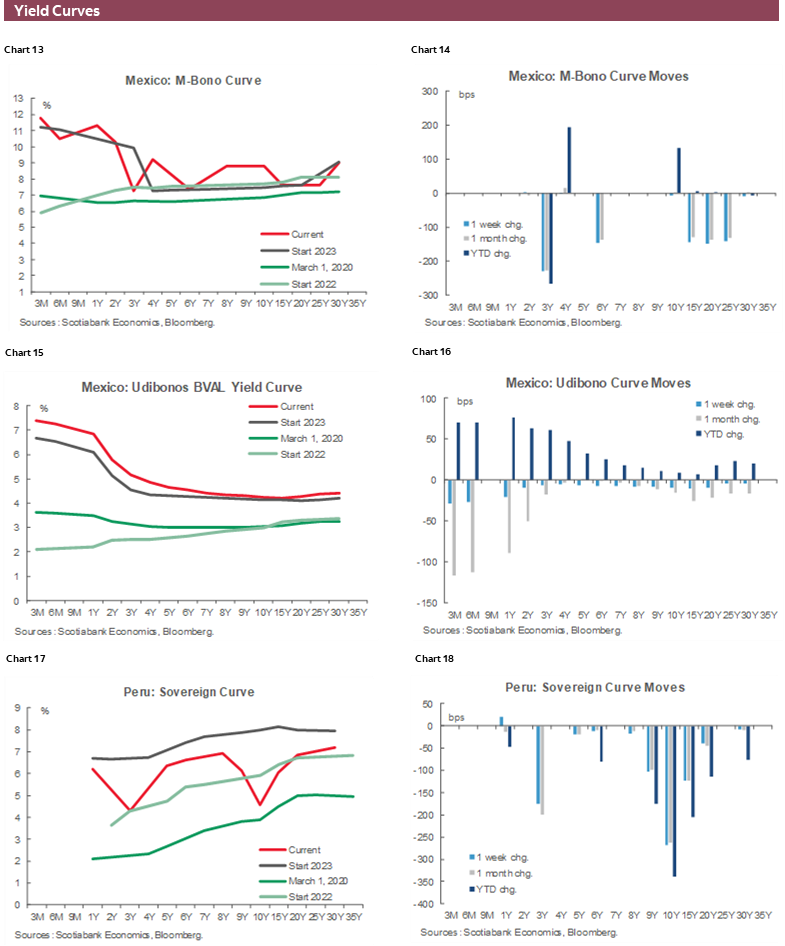

Banxico officials just started the pause stage of the cycle when they left the overnight rate steady at 11.25% in May. Since then, hawkish meeting minutes and officials saying that policy will remain the same for at least two meetings, if not three for some within the board, means next week’s meeting is merely procedural as the bank observes data to pick the best time for the first rate cut (in September, November, or even December). The morning of the decision, H1-June CPI data are seen showing another deceleration in headline and core inflation, but it’s much too early for the central bank to sound optimistic as core prices growth remains above 7% y/y. Retail sales data out on Tuesday should mostly be an afterthought. Ahead of the mostly uneventful announcement, today’s Mexico section of Latam Weekly reviews the state of investment in the country. Though things are looking up, there remains considerable ground to cover to return to where investment stood about five years ago.

Finally, Brazil’s central bank announcement on Wednesday will likely be the last that shows a Selic rate of 13.75%, as the bank looks set to begin the easing cycle as soon as its August decision (we may even get an official voting for a cut next week). The fiscal backdrop is looking better than feared and there is optimism on the path of inflation. Twelve-month ahead inflation expectations in the BCB’s weekly survey have fallen to 4.42%, their lowest point since last August, and down from 5.80% at the start of the year when markets and economists worried about fiscal policy under Lula possibly preventing a greater deceleration. It is also important to note that the BCB’s policy rate is practically in double digits in real terms as well—at some point, this is too much of a drag on the economy and investment. The day after the decision, Brazil’s Senate Economic Affairs Committee may soon vote on the appointment of Galipolo, Lula’s nominee to the BCB board who has shown a clear preference for cuts (the nomination would then go to the Senate floor).

PMI releases around the globe, rate decisions in the UK, Norway, and Switzerland, UK and Japan inflation, and some second-tier US data will drive the global market mood, as could the usual headlines around Chinese stimulus, oil supplies and natural gas demand, and a parade of central bank speakers. For our readers in Canada, retail sales data and the BoC’s June meeting minutes (after a somewhat surprising restart of hikes) on Wednesday are the highlights. Note that US markets are closed on Monday for Juneteenth.

PACIFIC ALLIANCE COUNTRY UPDATES

Chile—Broad Anchoring of 2-Year Inflation Expectations—Benchmark Rate Cut Process in Sight

Anibal Alarcón, Senior Economist

+56.2.2619.5465 (Chile)

anibal.alarcon@scotiabank.cl

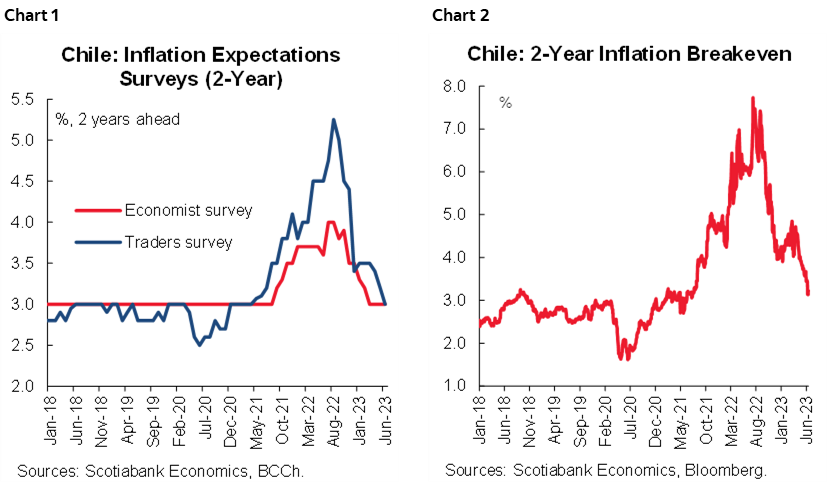

Two-year inflation expectations are anchored at 3%. At its last monetary policy meeting, the Central Bank (BCCh) kept the benchmark rate at 11.25% and maintained a neutral bias. One of the main arguments behind the BCCh’s decision was a de-anchoring of inflation expectations, stating that “most measures of two-year inflation expectations continue to place it above 3%”.

Recently, the Traders Survey showed that 2-year inflation expectations declined to 3%, after having been for more than two years above the BCCh’s target (chart 1). In addition, 2-year inflation breakevens have declined rapidly in recent months and are now very close to 3% (chart 2). Along these lines, 2-year inflation expectations from the Economists Survey have remained at 3% since March, the same as the expectations implicit in forwards, all of which allows us to affirm that inflation expectations—under different measures—are anchored at 3%.

Next week, the BCCh will hold its monetary policy meeting (on June 19), for which we do not see changes in the reference rate, today at 11.25%, but we expect relevant changes to their bias.

On this occasion, the BCCh will present its new macroeconomic scenario through the Monetary Policy Report (IPoM, on June 20), where we expect a downward adjustment to its inflation forecast—currently at 4.6% at the end of 2023—and a lower rate corridor, closer to our projection that considers a reference rate at the end of 2023 at 7.5%.

In our view, although core inflation has evolved in line with the BCCh’s scenario, they should recognize that headline inflation figures in recent months—mainly May—represented a downward surprise in relation to their forecasts. The latter, added to the fact that the real exchange rate depreciation assumed in its scenario never occurred, would be sufficient arguments to justify a lowering of its inflation forecast. Consistent with this new scenario, we believe that the BCCh will incorporate, at least, cuts in the benchmark rate by 125 bps by September 2023 as a working assumption.

Colombia—Fiscal News, Reforms Debates and Calmer Markets

Sergio Olarte, Head Economist, Colombia

+57.601.745.6300 Ext. 9166 (Colombia)

sergio.olarte@scotiabankcolpatria.com

Jackeline Piraján, Senior Economist

+57.601.745.6300 Ext. 9400 (Colombia)

jackeline.pirajan@scotiabankcolpatria.com

Santiago Moreno, Economist

+57.601.745.6300 Ext. 1875 (Colombia)

santiago1.moreno@scotiabankcolpatria.com

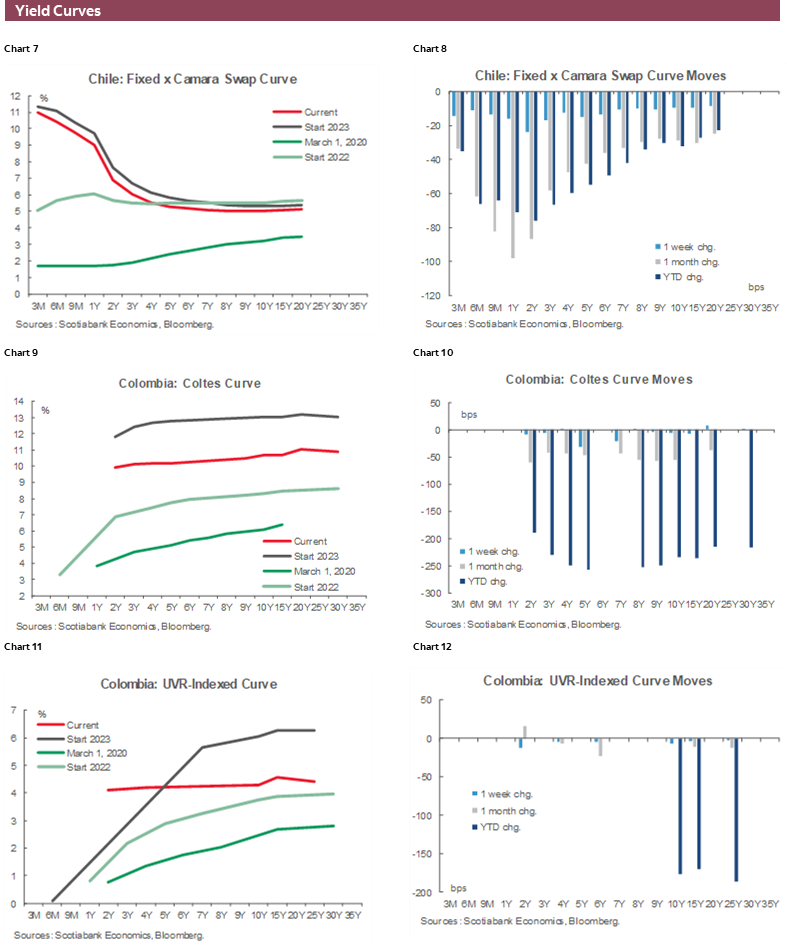

It was a busy week on the fiscal front in Colombia. The Minister of Finance released the Medium-Term Fiscal Framework for 2023. As was anticipated, the fiscal deficit projection increased for 2023, but also for 2024. The Government is expecting lower tax collection amid lower oil prices vs the previous budget, due to lower taxes on imports. On the other side, they anticipated that during the second half of 2023, budget execution will increase with special emphasis on the social agenda aligned with the National Development Plan approved a few weeks ago. Markets will now have an extended issuance calendar. COLTES auctions in 2023 will go from COP27tn to COP34tn as the government seeks to ‘pre-fund’ 2024.

In 2024, a moderate outlook for tax collection and higher interest payments, joined by even greater spending on the social agenda, will lead to a fiscal deficit of 4.5% of GDP, higher than expected in 2023. COLTES issuances will be COP37bn (~2.5% of GDP) still a decent size that the market can absorb. We highlight that these forecasts are more conservative than what we had seen in previous publications, however, as debt to GDP is expected to rise, instead of decrease, which could pose a challenging development towards recovering investment grade status in the medium term.

In the meantime, reforms discussions continued. The regular legislative period ends on June 20; however, this period is expected to be extended. The Pension Reform passed the first of the four required debates to become a Law, with tweaks made in some parameters regarding the transition of people that are closing in on pension age. However, the big topics such as the mandatory contribution to the savings fund and its regulatory framework haven’t changed substantially. The Health Reform process remained stagnant (it has passed only the first debate), while the Budget addition still faces a long road ahead.

On the flip side, the Labour Reform is in danger of being discarded since Congress hasn’t had any debates about it. That said, we probably will continue seeing discussions regarding reforms, but the final word and the most critical part of the negotiations will take place in the second half of the year.

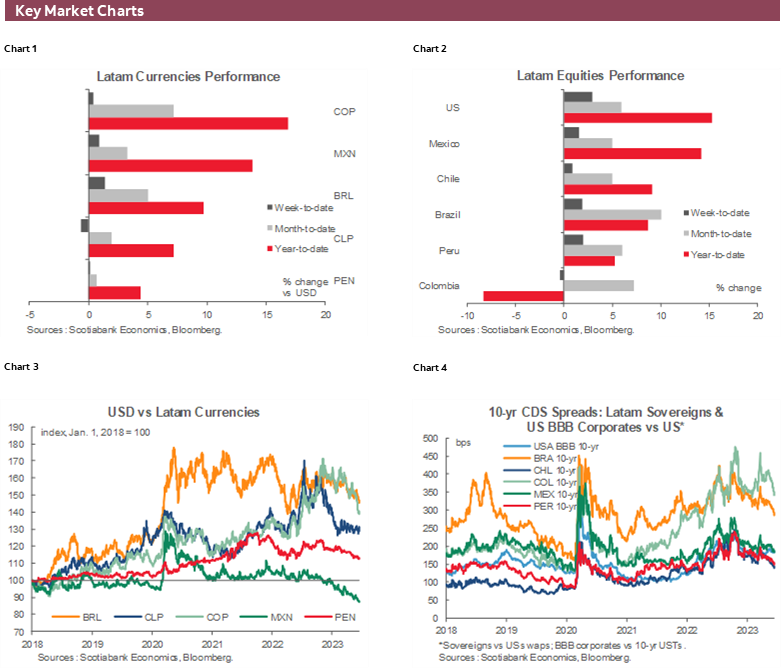

Finally, Colombia’s assets stabilized. The market apparently is taking a breath after the strong appreciation of past weeks. In Scotiabank Economics, the macro fundamental model points to an FX fundamental level of 4200 pesos, while the COLTES market must probably wait for more information before continuing with the downtrend in yields in the medium term.

Mexico—Investment in Mexico Posting Moderate Improvements. What’s Behind It?

Eduardo Suárez, VP, Latin America Economics

+52.55.9179.5174 (Mexico)

esuarezm@scotiabank.com.mx

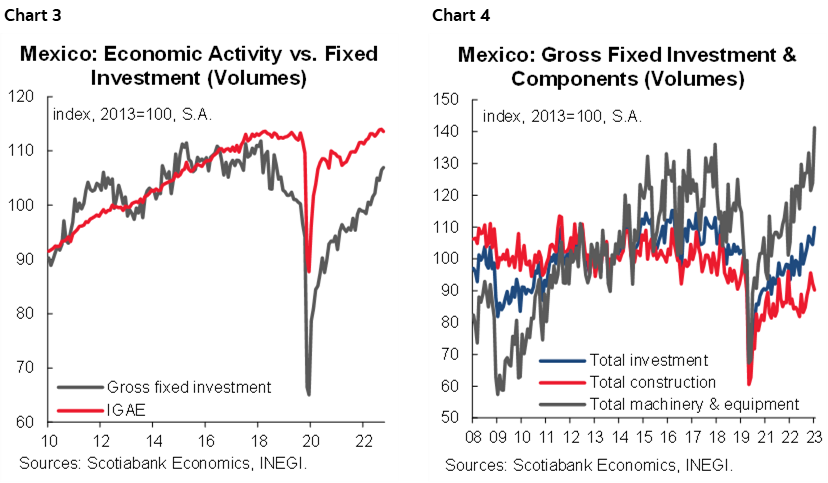

Over the past 5 years, investment has arguably been the weakest link in the Mexican economy, with investment trailing aggregate economic activity by one of the largest gaps in recorded history. Thankfully, recent data show a moderate acceleration in investment which is now outpacing broader growth—however, investment volumes and investment to GDP remain well below pre-2018 levels (charts 3 & 4).

This acceleration in investment is good news, but also needs to be put into context. Some key points to consider include:

- After 5 years of abnormally low investment rates, part of the capital stock—particularly machinery and equipment—has likely depreciated materially. Hence part of the spike in investment is likely a refreshment, replacement, and update of this depleted capital stock.

- It’s also worth noting that with Mexico’s population having expanded almost 5%, and the size of the economy also having expanded in that period, there is some catching up left to do.

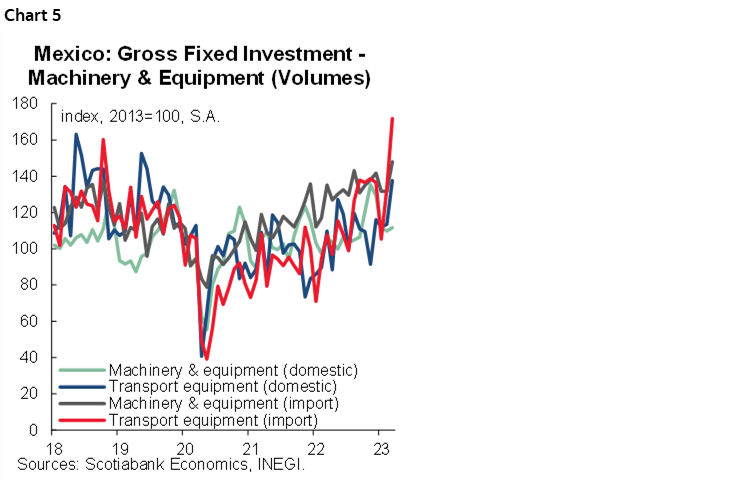

- If we look at investment by component, it is machinery and equipment that has seen a recent acceleration (chart 5). Construction today remains well below 2013 levels in volume terms. Interestingly, if we look at Banxico’s latest Report on Regional Economies (figure 11), it’s noteworthy that within the country, only the South has had any material activity in construction (an index defined as 2019=100 has the South at 140, and the rest of the regions between 65 and 90). The strong construction activity in the region is almost exclusively driven by public sector investment. Also of note is that private construction is below 2019 levels in all regions but the North (where it’s just above 2019 levels). The relatively better data on private construction activity is consistent with our view that the nearshoring/friendshoring story is a regional story.

- The improvement in investment is good news, but after 5 years of historically low investment rates, the capital stock needs to be replenished. This will likely require a period of above-trend investment for that capital stock to be replenished to pre-2018 levels—which in turn presents the risk that potential growth for the country has suffered, which has implications for monetary policy.

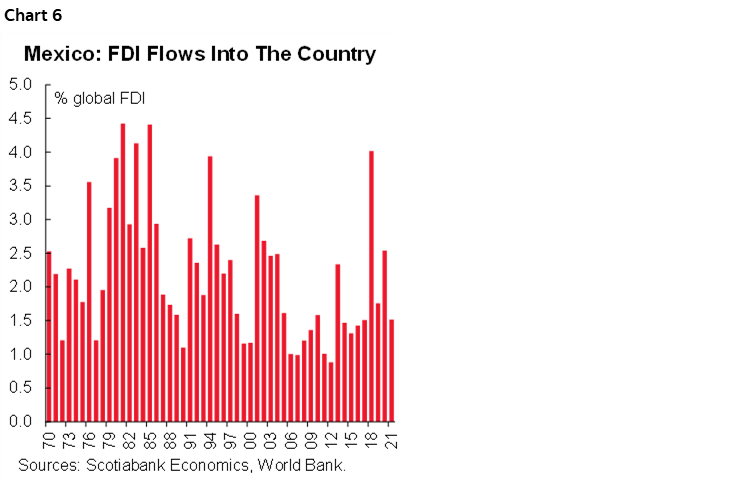

- We don’t yet have aggregate global FDI flows for 2022, but Mexico’s share of global FDI seems to also have fallen (chart 6).

Peru—If Not for Mining… Peru Tiptoeing Around Recession; April GDP Growth was 0.3% y/y and -1.5% Ex-Mining

Guillermo Arbe, Head Economist, Peru

+51.1.211.6052 (Peru)

guillermo.arbe@scotiabank.com.pe

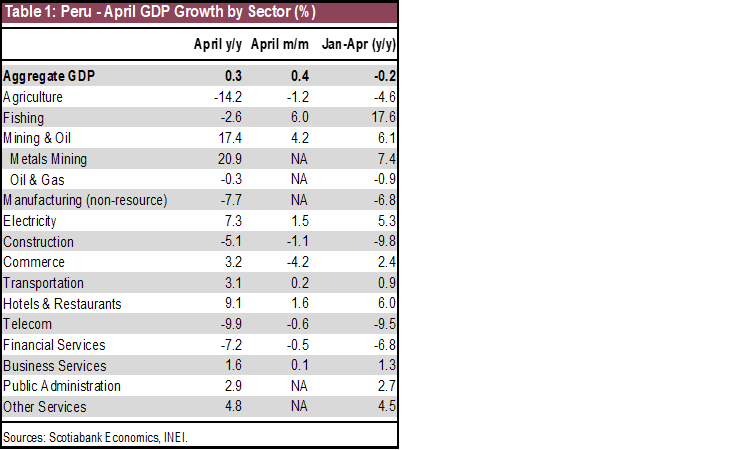

April GDP growth came in at 0.3% y/y, only marginally above negligible, and not only below market expectations of 1.7% y/y, but also below the 0.7% y/y figure suggested last week by Finance Minister Alex Contreras, and which had tinted our own expectations. It’s not much comfort that GDP was up 0.4% m/m, as March was such a weak month.

One could say that April GDP growth continued to be hampered by extraordinary events, as in previous months. But poor weather, which did have a stronger-than-expected impact on sectors such as agriculture GDP, which plunged 14.2% y/y and 1.2% m/m—was only part of the problem. It’s time to recognize two issues. One of major concern, is that the economy is quite simply running cold. Domestic demand is nil or worse. Manufacturing (non-processing) was negative in April, down 7.7%, for the seventh consecutive month.

Most domestic demand-related services did poorly in April (table 1). But some did not. Electricity growth of 7.3% y/y was particularly shocking, until one realizes it is probably linked to the growth of mining activities, which are energy-intensive. Growth in hospitality sectors and in transportation was robust, but these are sectors that are still rebounding, and have yet to reach their pre-COVID levels.

Comatose domestic demand is our main concern, but not the only one. The El Niño weather event is having greater impact than we had envisioned (e.g. agriculture), and we now also fear that this impact may be longer lasting than we previously thought. These two factors, one on the demand side and the other on supply, put our 1.9% GDP forecast for full-year 2023 at risk. Growth in the January–April period was -0.2%. The 2.8% average monthly growth needed henceforth to meet our 1.9% GDP forecast for the full year no longer seems tenable. As a result, we are placing our 2023 GDP forecast under revision.

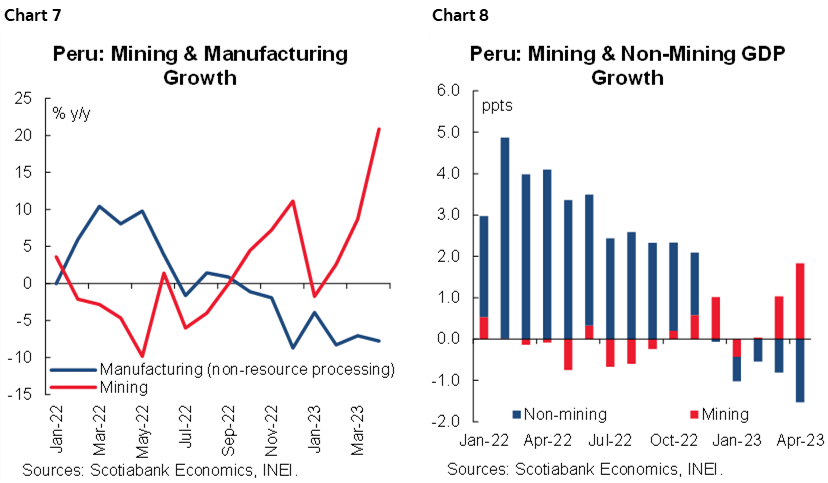

In terms of GDP growth, Peru has become a divergent economy. Exports sectors, especially metals and agroindustry, are outperforming not only the economy but expectations. Metals mining soared 20.9% y/y in April. But if you take out mining, the rest of the economy would have declined 1.5%. Negative non-mining GDP growth has been ongoing since December. Outside of mining, it would not be difficult to argue that Peru is in a recession (charts 7 and 8).

The contrast between mining and domestic demand driven sectors is particularly noticeable when one plots mining GDP (including oil & gas) against manufacturing, as we have done. Just like mining has been showing mostly robust positive growth since Q4 -22, manufacturing growth has been negative over the same time period.

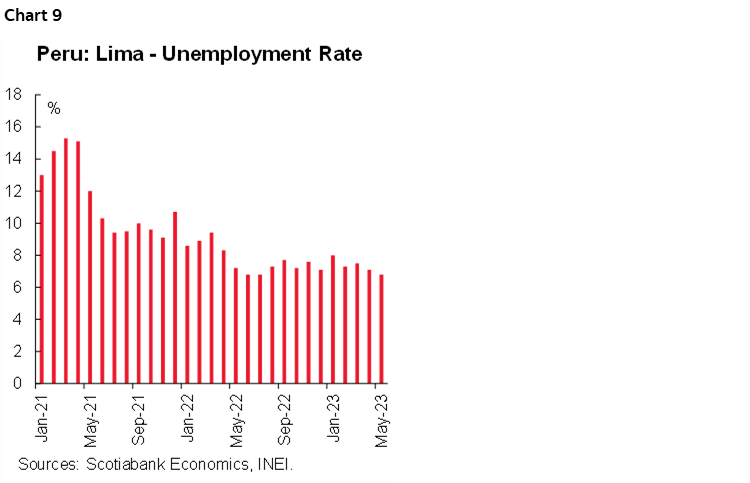

Maybe May will be a bit better. At least employment data for Lima is hopeful in this regard. Unemployment for Lima came in at 6.8% in the quarter to May (chart 9). This was down from 7.1% for April. It was also the lowest level since June 2022. And yet, one feels like there is a disconnect between the labour market and domestic demand. Part of the difference is that within domestic demand, it is investment that is declining sharply, while consumption has weakened but remains positive, and more in line with the 1.0% jobs growth reading.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Click here to be redirected |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.