ECONOMIC OVERVIEW

- A busy week in the Latam region stands as a big hurdle for markets and economists hoping to cruise into the Holidays Season.

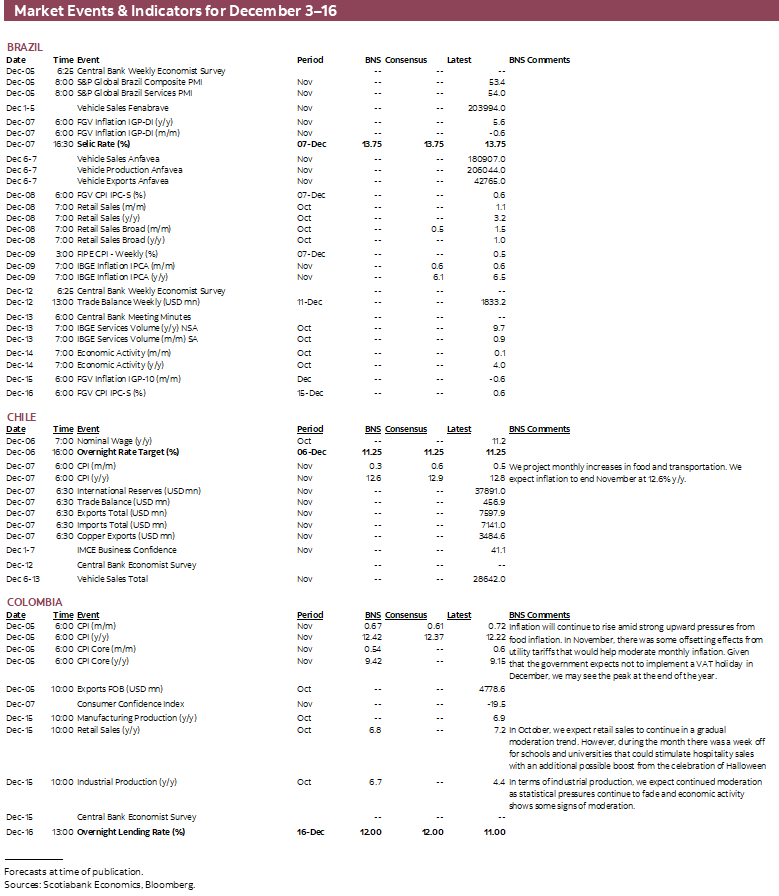

- The week begins with Colombian inflation that we expect will maintain an elevated pace, challenging BanRep to another sizable rate increase at its mid-December meeting.

- Chilean inflation may take a bit of a breather in data out on Wednesday and the BCCh is widely expected to leave its policy rate unchanged at its decision the prior afternoon, but may open the door to a reduction in rates in Q1.

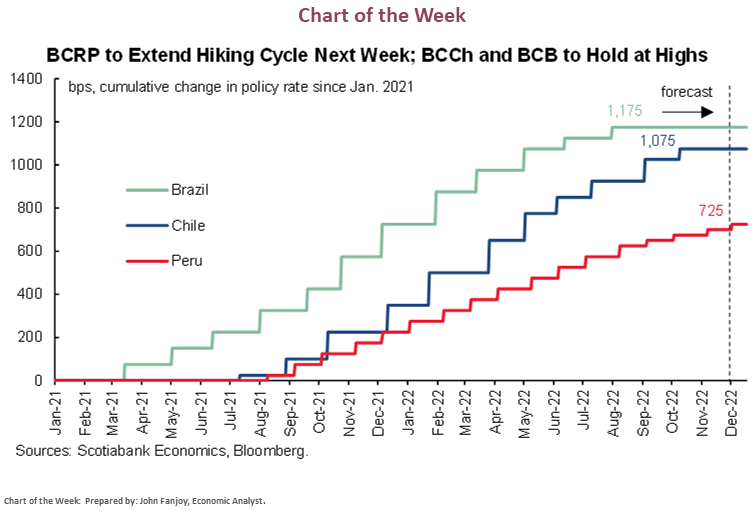

- Another 25bps hike by the BCRP is the consensus’ and our call for its announcement on Wednesday—but this may be a secondary development to Castillo’s impeachment trial and vote scheduled for December 7.

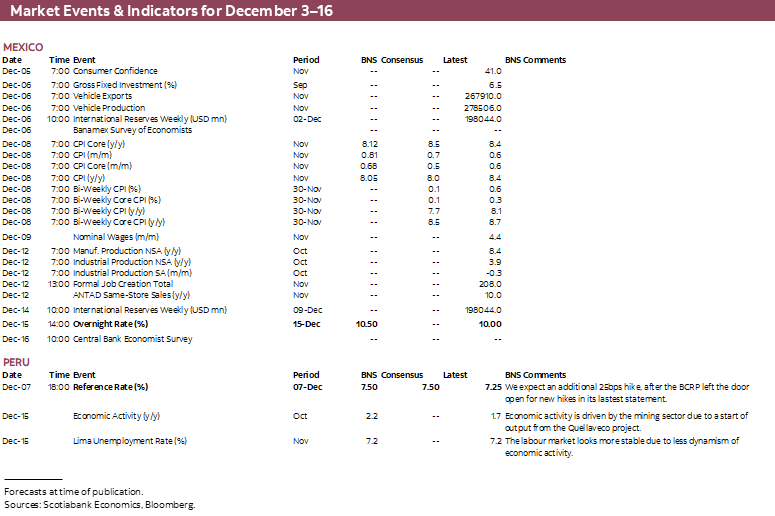

- Mexico publishes H2-Nov inflation data on Thursday to present the full-month picture as uncertainty grows over whether Banxico will soon diverge from the Fed.

- The BCB will decide on rates policy on Wednesday, ahead of November CPI data out on Friday, where it will likely keep its Selic rate at a very high level of 13.75%. Lula’s possible pick of Fin Min as well as decisions/goals on spending/budget and other cabinet names will catch the market’s eye.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Chile, Colombia, Mexico, and Peru.

MARKET EVENTS & INDICATORS

- A comprehensive risk calendar with selected highlights for the period December 3–16 across the Pacific Alliance countries and Brazil.

Economic Overview: Busy Central Banking, Inflation and Political Week in Latam

Juan Manuel Herrera, Senior Economist/Strategist

+44.207.826.5654

Scotiabank GBM

juanmanuel.herrera@scotiabank.com

- A busy week in the Latam region stands as a big hurdle for markets and economists hoping to cruise into the Holidays Season.

- The week begins with Colombian inflation that we expect will maintain an elevated pace, challenging BanRep to another sizable rate increase at its mid-December meeting.

- Chilean inflation may take a bit of a breather in data out on Wednesday and the BCCh is widely expected to leave its policy rate unchanged at its decision the prior afternoon, but may open the door to a reduction in rates in Q1.

- Another 25bps hike by the BCRP is the consensus’ and our call for its announcement on Wednesday—but this may be a secondary development to Castillo’s impeachment trial and vote scheduled for December 7.

- Mexico publishes H2-Nov inflation data on Thursday to present the full-month picture as uncertainty grows over whether Banxico will soon diverge from the Fed.

- The BCB will decide on rates policy on Wednesday, ahead of November CPI data out on Friday, where it will likely keep its Selic rate at a very high level of 13.75%. Lula’s possible pick of Fin Min as well as decisions/goals on spending/budget and other cabinet names will catch the market’s eye.

A busy week in the Latam region stands as a big hurdle for markets and economists hoping to cruise into the Holidays Season—no dice, the Fed policy decision is the following week, as well. The week’s data and rate meetings will nevertheless punctuate the 2022 calendar for some of the countries in the region while ‘off-calendar’ and largely political developments may still keep some up at night for the foreseeable future.

The week begins with Colombian inflation that we expect will maintain an elevated pace, challenging BanRep to another sizable rate increase at its mid-December meeting. Our Bogota economists (see Colombia section) project that prices growth in November will roughly match the prior monthly increase of 0.7%—too high a rate for the central bank to hold its fire. The BanRep board (with a new member in Acosta, replacing Carrasquilla) looks set to lift its policy rate by 100bps on December 16.

Chilean inflation may take a bit of a breather in data out on Wednesday. While the rate of year-on-year prices growth will remain in the upper-12s, this is significantly lower than the 14.1% peak recorded in August and all signs point to a continued decline in headline inflation. The team also believes that core inflation will extend its deceleration on the back of softer services prices growth amid a sharp deceleration economic activity (see Chile section).

The BCCh is widely expected to leave its policy rate unchanged at its decision the prior afternoon, but may open the door to reduction in rates in Q1. Revised forecasts in its MPR should show a weak economic outlook that motivates our call for a sizable cut of between 100-200bps at the bank’s only meeting of Q1. This may be an outlier forecast, but we believe the obvious and hastening contraction that the country currently finds itself in will be difficult to ignore—and slowing inflation will help the BCCh in its decision.

Another 25bps hike by the BCRP is the consensus’ and our call for its announcement on Wednesday—but this may be a secondary development to Castillo’s impeachment trial and vote scheduled for December 7. We don’t think legislators have the required two-thirds votes to dethrone the President (see Peru section), but the Congress-Castillo showdown continues to dominate the scene in the country with multiple fights running in parallel between the Legislative and Executive branches. The proceedings will kick off at 15ET, three hours before the BCRP’s decision.

Mexico publishes H2-Nov inflation data on Thursday to present the full-month picture as uncertainty grows over whether Banxico will soon diverge from the Fed. Recent comments from Banxico officials as well as the bank’s most recent projections (in the quarterly report published earlier this week) and the accompanying press conference suggest that Banxico may be looking to decouple from the Fed sooner than we had expected. For now, we see the bank tracking the Fed’s 50bps increase in December, but subsequent meetings seem less clear with even hawk Heath softening his tone; he also noted some distortion in H1-Nov CPI data owing to the “Good Monday” discounts that will bite back in next week’s bi-weekly reading. We also await a decision by President AMLO on who will replace outgoing Dep Gov Esquivel, Heath’s opposite in the hawk-dove spectrum, whose term ends this month.

The BCB will decide on rates policy on Wednesday, ahead of November CPI data out on Friday, where it will likely keep its Selic rate at a very high level of 13.75%. Amidst the market tumult around the second-round presidential elections (as well as Fed hawkishness at the time), markets briefly positioned for a considerable resumption of the bank’s hiking cycle. Market bets are still reflecting an expectation that the BCB will hike again—by about half a point more, at peak—but this may merely reflect a near-term risk premium rather than a clear justification for renewed hikes in Brazil. Weakening prices data, with inflation seen slowing to 6.1% in November from 6.5% y/y in October, is, in fact, making real policy rates exceedingly restrictive. With this in mind, the bank is unlikely to aim for a higher terminal rate. What’s more, Lula’s spending plans will likely be watered down by an opposition Congress although there remains the latent risk of a ‘looser’ Minister of Finance that may put up a bigger fight against moderating social spending aspirations. Lula’s possible pick of Fin Min as well as decisions/goals on spending/budget and other cabinet names will catch the market’s eye.

Chile—BCCh May Pave the Way for a Rate Cut at the January Meeting

Anibal Alarcón, Senior Economist

+56.2.2619.5465 (Chile)

anibal.alarcon@scotiabank.cl

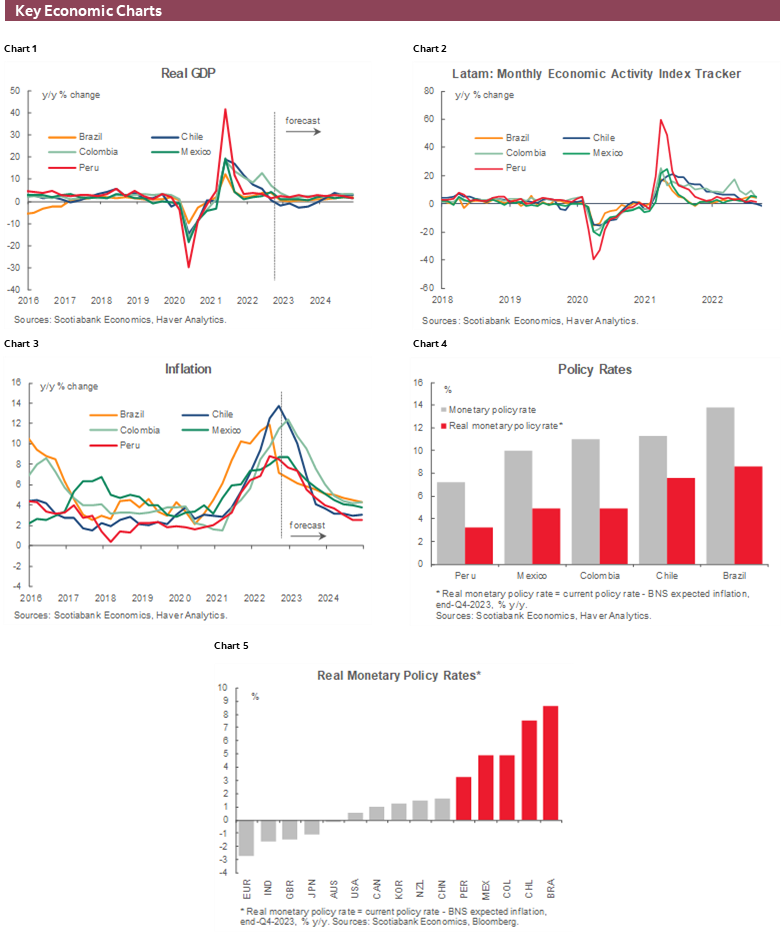

Chilean inflation could take a break in November. We project inflation of 0.3% m/m for November, for a 12.6% y/y rate (from 0.6% and 12.8%) driven by food and transportation prices. Overall, we see a decline in core inflation, mainly in services. Food would contribute 0.22ppts to the headline reading, mainly due to increases in fruit prices (bananas), non-perishable foods, and vegetables. We estimate a combined contribution of 0.13ppts from gasoline and diesel for November, which would be its last increase of the year. Services will continue to add to inflation, although less and less, while goods inflation is already showing signs of exhaustion.

We anticipate that the BCCh will pave the way for a big cut at the January meeting. No changes are expected to the nominal level of the reference rate at the December 6 meeting. However, the Monetary Policy Report should revise the GDP growth forecast weaker for 2023, acknowledging a worse performance of overall economic activity next year and a deterioration in the labour market. In terms of inflation, the BCCh will likely note reduced pressure from main price determinants, notably a 6% appreciation of the CLP since its previous meeting and a drop in international food and energy prices. Taking all of the above into account, in the context of the sharp drop in inflation expectations implicit in both asset prices and surveys, we reiterate our call for a rate cut between 100 and 200bps at the January meeting.

Colombia—November Inflation Ahead of 100bps Hike from BanRep

Sergio Olarte, Head Economist, Colombia

+57.1.745.6300 Ext. 9166 (Colombia)

sergio.olarte@scotiabankcolpatria.com

María Mejía, Economist

+57.1.745.6300 (Colombia)

maria1.mejia@scotiabankcolpatria.com

Jackeline Piraján, Senior Economist

+57.1.745.6300 Ext. 9400 (Colombia)

jackeline.pirajan@scotiabankcolpatria.com

Next week’s inflation print for November will be key. We expect a monthly increase of 0.67% alongside a year-on-year gain of 12.42%, reflecting our upside bias with respect to BanRep’s latest survey (0. 54% median). Price changes across the usual suspects are behind our forecast: food given weather impacting some crops, in contrast to some stabilization in input costs and a moderation in international commodity prices. As for the other items we spot mixed results with less strong accelerations.

The data will be an important input for BanRep’s final meeting of the year on December 16. According to our calculations, y/y inflation won’t show a peak yet which, combined with the fact that the performance of the economy in Q3 was stronger than expected, leads us to anticipate an increase of 100bps taking the policy rate to 12% to close out the year while we cannot rule out an additional 50bps hike in January. During the first quarter of 2023 is when we may see greater price pressures due to the indexation effects though these will, in turn, contribute to a slowing economy that could also allow for a faster adjustment in external accounts.

Finally, since some Board members have referred to the possibility of using some FX intervention mechanisms, it is likely that the discussion will continue if policymakers detect lower liquidity, which could be partially improved with NDF intervention or simple volatility options. Having said that, given the exchange rate has had a slightly more positive performance in recent weeks, it is difficult to envisage an intervention announcement during the final month of the year when liquidity is limited due seasonality rather than market sentiment.

On a related note, Olga Lucía Acosta was appointed as the BanRep board member, replacing Alberto Carrasquilla who was removed from office as his assignment (during Duque’s presidency) broke with rules on female representation in top government boards (one-third share minimum). Prior to this role, Acosta worked as the UN ECLAC’s Director for Colombia, though she was also part of the country’s Autonomous Fiscal Rule Committee.

We see this appointment as positive as Petro has chosen someone with a highly technical profile that will contribute to the board discussion. Acosta is experienced in economic policy and regulation, which suggests to us that she will kick-start her appointment with a focus on growth issues though, due to her technical profile, we can be confident that she will pursue the bank’s price stability mandate.

The other thing that we expect from Acosta is probably more public speaking engagements and as such the volume of communications that we had been accustomed to under Carrasquilla is expected to increase. Our call and outlook for BanRep is unchanged with Acosta’s appointment.

Mexico—December Kicks Off with Focus on Banxico

Eduardo Suárez, VP, Latin America Economics

+52.55.9179.5174 (Mexico)

esuarezm@scotiabank.com.mx

As we kick-off the month of December, we still don’t have confirmation on whether Deputy Governor Esquivel will be re-appointed, or if somebody else will take his place. In his morning conference on November 30th, President Lopez Obrador said the decision on who will take the board seat could take as long as two more weeks (Esquivel’s mandate ends on December 31st).

The president suggested that the choice could fall on FinMin Ramirez de la O. In recent weeks, media have speculated on who could replace Esquivel if he is indeed not re-appointed, with potential replacements including Deputy FinMin Gabriel Yorio, Undersecretary of Expenditures Juan Pablo de Botton, Banxico Chief Economist Alejandrina Salcedo, VP of Regulatory Policy at the CNBV (the bank and securities regulator) Lucia Buenrostro, or former Head of INEGI (the national statistics institute) Julio Santaella.

Within the current board, Deputy Governor Esquivel has been the most dovish in his monetary policy views and has also been a fierce defendant of Banxico’s independence (including on the direct purchase of USD by Banxico, and on the use of FX reserves to pay public debt). We anticipate that markets will careful monitor whoever is selected for the post on both fronts: dovishness/hawkishness and Banxico’s independence.

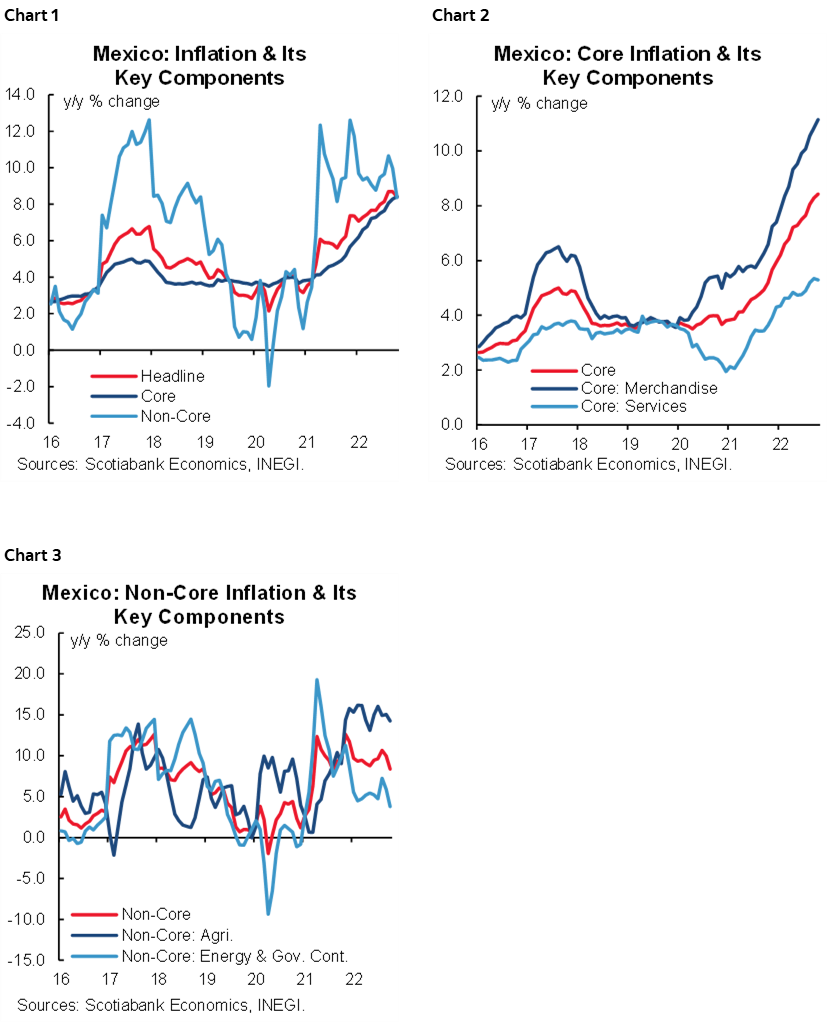

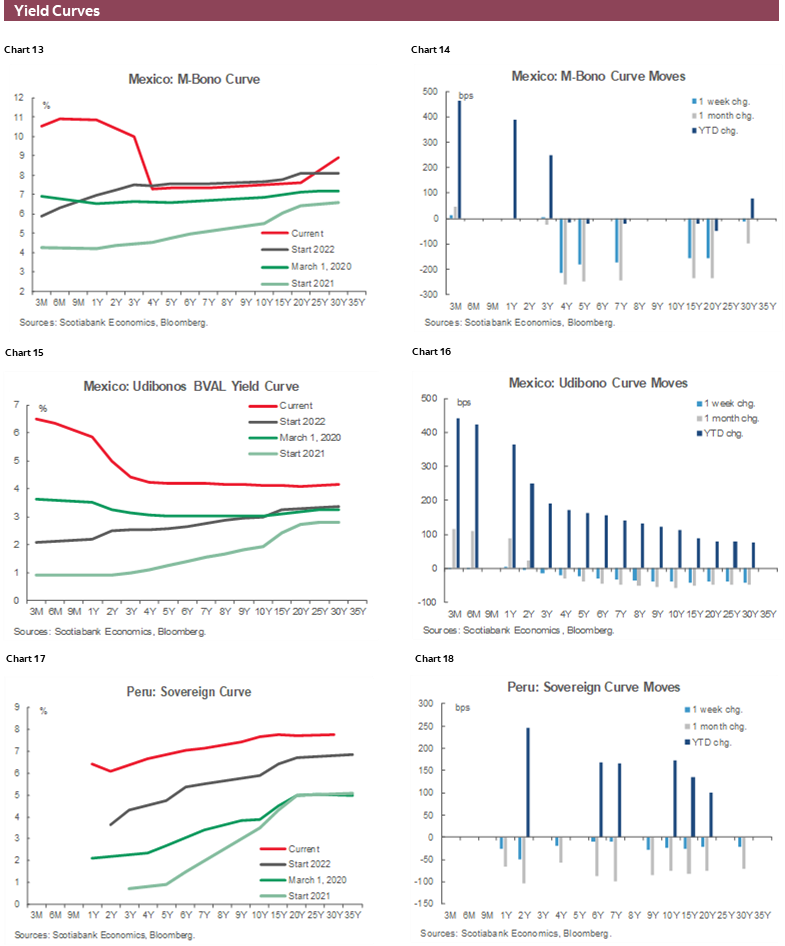

On November 30th, Banxico presented its Quarterly Inflation Report, and in its presentation, Governor Rodriguez said inflation likely peaked in Q3-2022 (table 1). Data suggest that this view is correct but, at the same time, the decline in headline CPI is due to non-core inflation—particularly energy prices and agricultural products. However, core CPI maintains an upward trajectory, including both the merchandise and services components, which Governor Rodriguez acknowledged as more important than headline inflation (charts 1, 2, and 3).

That same day, Deputy Governor Heath, who has been among the more hawkish members of the board, said Banxico could be approaching its terminal rate, and that core CPI could have peaked in the second half of November—both are views that we agree with. Heath highlighted that it is important to consider that Banxico started its tightening cycle ahead of the Fed, which appears to be preparation for an eventual decoupling of Banxico relative from the Fed. Similar guidance to Heath’s was provided by Deputy Governors Borja and Espinosa. It is noteworthy that it has been some time since we’ve had presentations by all members of the board, and hence we take this barrage of Banxico-speak as a strong signal that the board is preparing markets for an important change in policy direction, pointing to the risk that Banxico could decouple from the Fed as soon as the upcoming MPC meeting in December.

In his speech at Brookings on November 30th, Governor Powell suggested that the Fed could moderate its tightening pace as soon as the upcoming meeting, but that the terminal rate would likely be somewhat higher than what was suggested in the Fed’s September meeting. This implies imply that the Fed will hike 50bps in December.

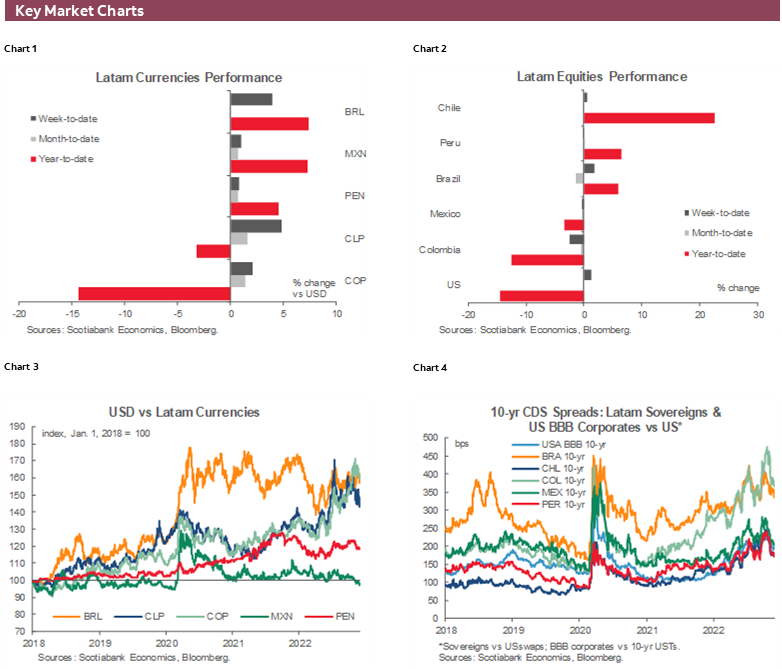

Our base case is that Banxico will match the Fed in December, then decouple afterwards, but Banxico—speak from November 30th suggests Banxico could decouple as soon as December (which we consider to still be somewhat of a gamble on inflation, more so than the market front, as core inflation has not yet moderated). Part of the reason why Banxico could decide to decouple from the Fed in the next couple of meetings is the strength in the MXN, which has outperformed most global currencies (4th best performer on a total returns basis among the 32 most liquid FX on a YTD basis). We believe that Banxico will have the opportunity to decouple from the Fed, as markets are already discounting such a move, and domestic markets have not been destabilized by a prospective interest rate decoupling.

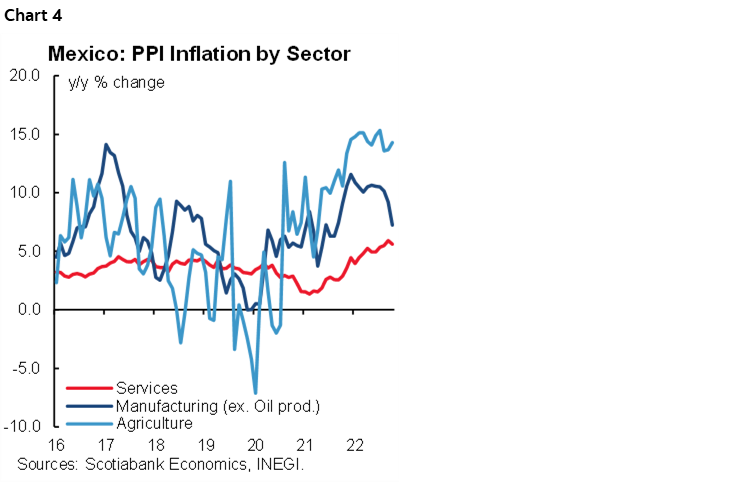

However, it’s also worth bearing in mind that US core CPI already appears to be on a downward trend, while the latest data in Mexico still showed upward momentum. Within core, services CPI may have peaked, but it’s still too soon to tell. Meanwhile, broad core inflation and core-merchandise inflation continued to climb in the latest prints. So far, most of the disinflation has come from the decline in non-core items, such as food and energy. If we look at PPI (chart 4), price momentum seemed to turn around in August 2022, but most of the improvement came from manufacturing prices, as services producer prices have continued to climb (albeit much more moderately than the rest), and primary sector inflation has stabilized, but at a high level.

Producer prices in Mexico may have to contend with a series of shocks in 2023, which includes the 20% increase in minimum wages that President Lopez Obrador has announced, the negotiation of union-level wage agreements under the new USMCA framework (which is expected to put upward pressure on wages), as well as the gradual increase of social security contributions by employers (from 6.5% of wages to 15%) under the 2021 Pension Reform, which will take place between 2023–2030.

We think the ideal moment for Banxico to decouple from the Fed will come after a couple of prints that show core CPI has clearly peaked, which we believe will come around the end of Q1-2023 (we anticipate that by then core CPI will have printed two or three sequential declines). How much room does Banxico have in terms of rate cuts? Our take is that the prudent path for Banxico would be to mind the spread that markets are demanding of Mexican rates, which has recently hovered in the 500–600bps range. To us, when it arrives, Banxico’s easing cycle could prudently accommodate 300–400bps of cuts (assuming inflation is clearly converging to target and with expectations anchored, and the economy is back at its potential which we expect in the first half of 2023).

In terms of forecasts, Banxico increased its 2022 growth forecast to 2.8–3.2% y/y (3.0% base case, up from a previous estimate of 2.2% y/y), and for 2023 to 1.0-2.6% (1.8% base case, up from a previous forecast of 1.6%). Banxico left its inflation forecasts unchanged.

Peru—One Last Increase (Again) in the Reference Rate, but the Congress-Executive Showdown Dominates the Scene

Guillermo Arbe, Head Economist, Peru

+51.1.211.6052 (Peru)

guillermo.arbe@scotiabank.com.pe

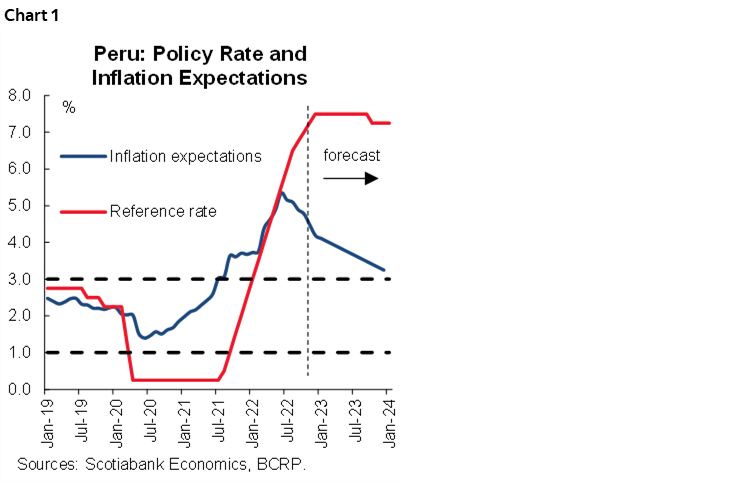

We are changing our view on the BCRP terminal reference policy rate. We had expected the BCRP to raise the reference rate to 7.25% in November, as has occurred, and then leave the rate stable at this level into Q4 2023. We now expect one more 25bps increase in December, to 7.50% (chart 1). We believe this is what the BCRP signaled when it produced a policy statement in November that showed no change in wording compared to the previous decision.

Furthermore, inflation appears seems stuck at about 8.0%. Although it is no longer accelerating, as the BCRP had been hoping would occur by this time, it is also not declining considerably. We do expect it to decline from its current year-on-year rate of 8.4% in November, possibly as soon as December, and with a higher likelihood in Q1 -2023, as the decline in global oil and soft commodity prices filter through. Still, the process is taking quite a bit longer than originally hoped for.

When one looks at BCRP monetary policy, and then looks at political developments in Peru, it’s hard to believe that these correspond to the same country. Monetary policy is reasonable, predictable and sophisticated. Politics is anything but. There are plenty of political issues that are in flux currently.

At the top of the list, Congress must ratify the new Cabinet, sworn in on November 25, with a vote of confidence. Or not. Whatever the decision, it must take place by Christmas.

The decision may be preempted by a new, third, motion to impeach President Castillo. The motion has been signed by 67 members of Congress, which is still well below the 87 needed to be approved, making its approval unlikely. What triggered this new motion was the decision by Congress to refuse to conduct a vote of confidence when requested to do so by the Executive, which then chose to interpret this refusal to a vote as a de facto negative vote of confidence. This interpretation, the legality of which is highly questionable, would mean that, by law, the Executive could choose to ‘close’ Congress if a “second” negative vote occurs.

Some have interpreted the designation as the new Head of Cabinet of the controversial Betssy Chávez, who Congress already impeached in May, as part of a plan to provoke this “second” negative vote. What is probably more likely, however, is that President Castillo may be acting with a view towards survival until 2026 and is using the threat to close Congress as an attempt to counter the threat of impeachment. However this may be, there is plenty of room for miscalculations and events overtaking intentions.

Aside from impeaching President Castillo, Congress is also trying other options. It submitted the Executive’s interpretation of the negative vote to the Constitutional Court early this week. The Court is likely to vote in favour of Congress. The problem is that the Court could take as much as two months to reach a verdict, and in today’s Peru, a lot can happen in two months. Other options being studied include suspending President Castillo for a period of time, although this option seems to have lost some backing in Congress. Unlike an impeachment, which requires 87 votes, a presidential suspension only requires 66. Early “general” elections could also be called, for both Congress and the Presidency, but this does not seem likely for the moment.

Markets have reacted to this new wave of turbulence with surprising calm. One gets the impression that over the past year and a half so many dire political situations have emerged only to be defused, that it would take a verifiable act actually occurring, whether it be the closure of Congress or a change in economic management, and not just the risk of some dramatic event, to shake the markets. The fact that, throughout all of this time of turbulence, there has been continuity and competence in economic management has been beneficial for the markets.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Click here to be redirected |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.