ECONOMIC OVERVIEW

- Next week’s jam-packed schedule features rate announcements in Colombia and Brazil where we expect a hold and a first rate cut, respectively, alongside decisions in the UK (an uncertain sized hike) and Australia (hike or hold).

- Mexico GDP, Peru CPI, and Chile economic activity are the Latam data highlights, accompanied by Banxico’s economists survey and BanRep’s Monetary Policy Report to round out the Latam week ahead.

- Eurozone GDP/CPI figures, Chinese PMIs, and US and Canadian jobs data are also on tap to drive global markets.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Chile, Colombia and Peru.

MARKET EVENTS & INDICATORS

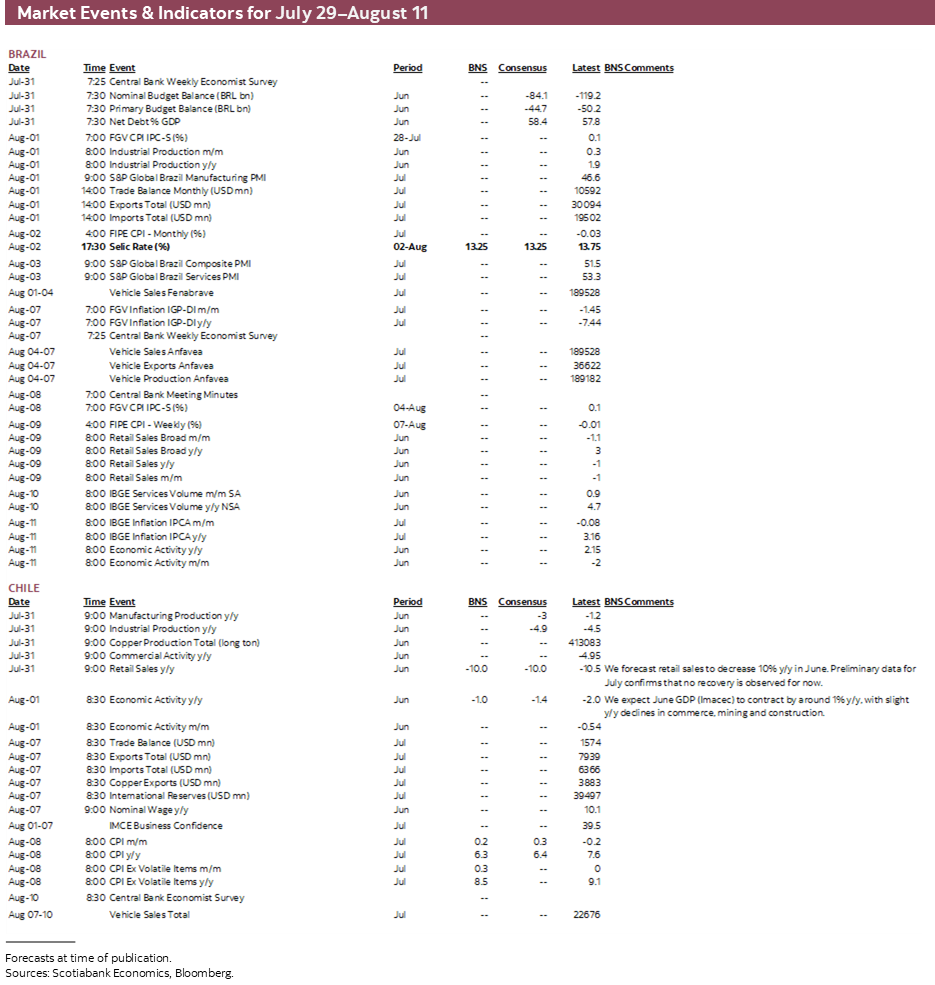

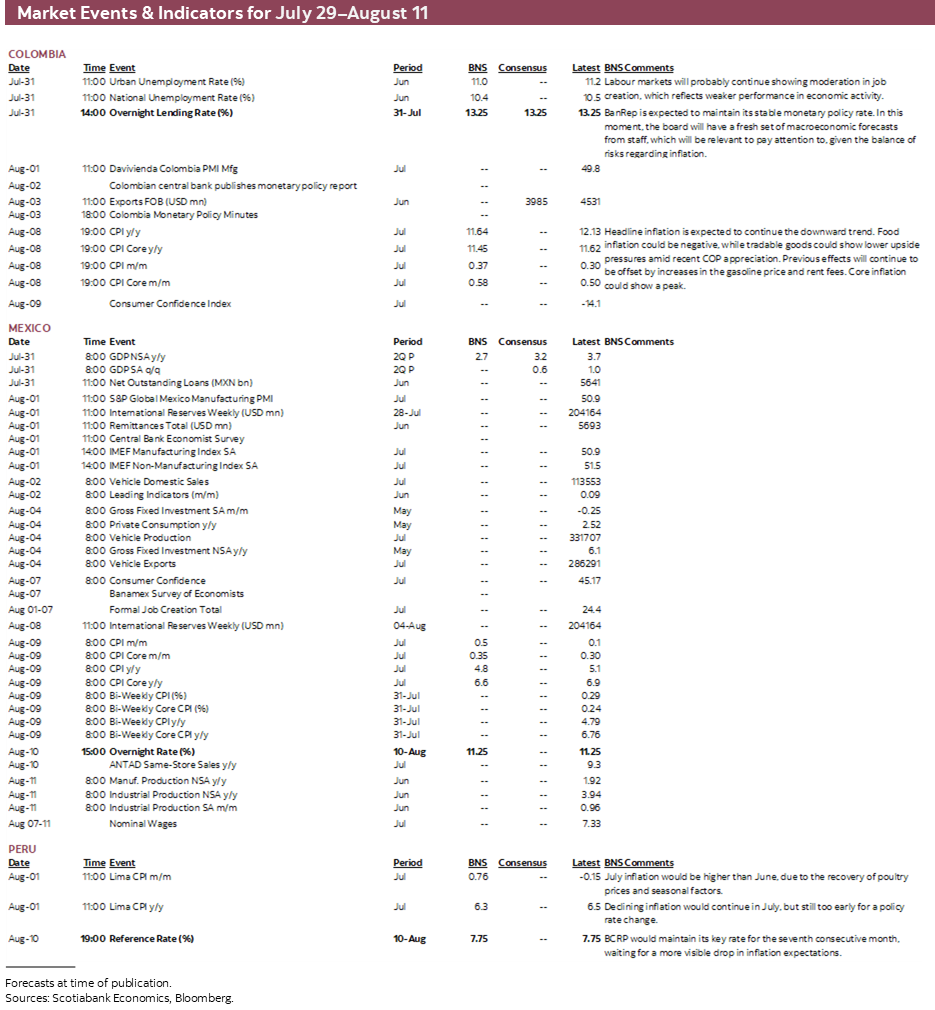

- A comprehensive risk calendar with selected highlights for the period July 29–August 11 across the Pacific Alliance countries and Brazil.

Chart of the Week

ECONOMIC OVERVIEW: BANREP’S HOLD, THE BCB’S FIRST CUT, AND A PACKED WEEK AROUND THE GLOBE

Juan Manuel Herrera, Senior Economist/Strategist

Scotiabank GBM

+44.207.826.5654

juanmanuel.herrera@scotiabank.com

- Next week’s jam-packed schedule features rate announcements in Colombia and Brazil where we expect a hold and a first rate cut, respectively, alongside decisions in the UK (an uncertain sized hike) and Australia (hike or hold).

- Mexico GDP, Peru CPI, and Chile economic activity are the Latam data highlights, accompanied by Banxico’s economists survey and BanRep’s Monetary Policy Report to round out the Latam week ahead.

- Eurozone GDP/CPI figures, Chinese PMIs, and US and Canadian jobs data are also on tap to drive global markets.

Get the popcorn ready for a blockbuster week in Latam and the G-10. Central bank decisions and the release of inflation, jobs, GDP, and survey data have next week’s poster looking like an arthouse film’s after festival season. The Fed, the ECB, the BoJ, and the BCCh will all be in the rear-view mirror, and Oppenheimer and Barbie euphoria has died down, but BanRep, the BCB, the BoE, the RBA, and a collection of data will walk the carpet next week like a bizarro cast from a Wes Anderson premiere.

Latam traders will walk into the office on Monday to the overnight release of official Chinese PMIs shaping the mood in the key commodities, particularly iron ore and copper, as well as Q2 GDP data for Germany, Italy, and the Eurozone and July CPI figures for the latter two.

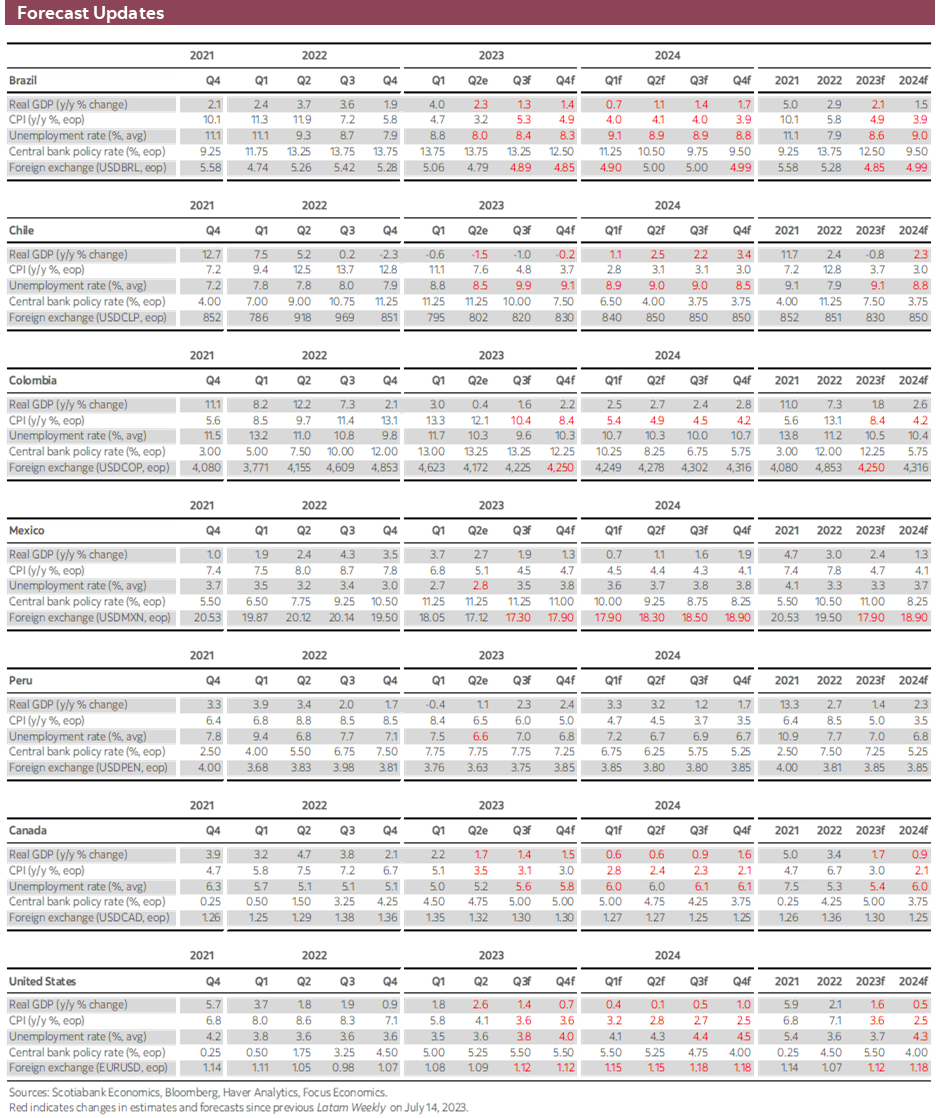

Mexican Q2-GDP out at 7ET on Monday will add to a throve of data to digest at the start of the week. In the latest forecast round, our economists projected that the country’s economy would expand by 2.7% y/y in Q2—a touch above the 2.5% average seen by economists polled by Banxico. This is a decent pace in the face of a 11.25% Banxico rate but would mark a deceleration from 3.7% in Q1-23 and would represent the lowest rate of growth since Q2-22. Monthly economic activity (IGAE) averaged 3.3% y/y in April and May, however, which points to decent odds of a 3-handled Q2 GDP expansion—though these output measures aren’t a one-to-one match.

The remainder of the Mexican week has only second-tier data due for release, but we do get the results of Banxico’s economists survey for a last look into expectations ahead of the bank’s decision on the 10th. In the June edition, end-2023 and end-2024 Banxico rate projections averaged 10.91% and 8.43%, respectively (Scotiabank Economics at 11% and 8.25%, in that order), while year-end inflation was seen at 4.7% and 4.0% (Scotiabank at 4.7% and 4.1%).

Chile’s calendar is also front-loaded to the beginning of the week, with retail sales, manufacturing/industrial production, and copper output data for June all out on Monday. These industry-level figures should give us a decent read of the Chilean economy’s performance to close out Q2, so Tuesday’s June economic activity release should not come as too much of a surprise for markets. The Chilean economy is estimated to have contracted in year-on-year terms in June, as it has in eight of the previous nine months. The economic backdrop is clearly supportive of the BCCh’s sizeable rate cut on Friday (practically a certainty, at writing ahead of the decision).

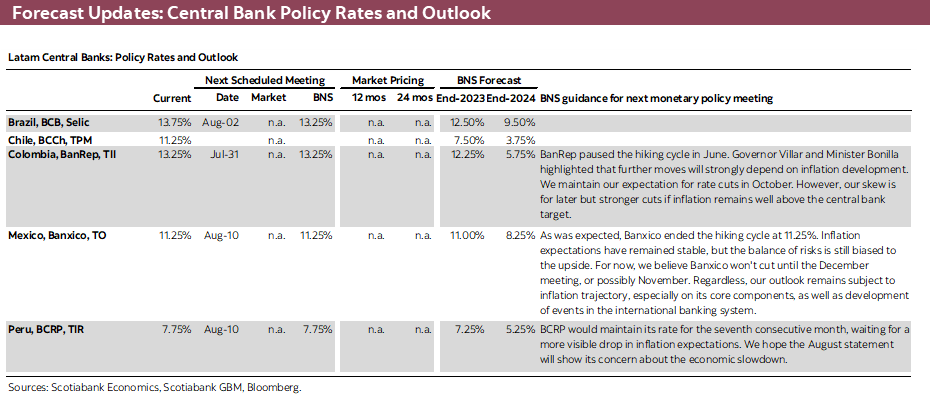

Monday’s top billing in Latam will be BanRep’s rate announcement, where no policy change is expected, and the spotlight will be on guidance and the bank’s assessment of conditions. Some members of the board, like Fin Min Bonilla, will hope that this will be the last policy rate meeting where the overnight rate remains at 13.25% before rate cuts being in September.

In Bogota, our economists believe policymakers will wait until October to start the easing cycle if data cooperate. This timing aligns with the latest BanRep survey median, but our expected cut size of 50bps is below the median’s 75bps reduction. The survey’s year-end target of 11.75% also undershoots our call of 12.25%.

The morning of the decision, June unemployment rate data may slightly move timing and size bets for BanRep policy, but later in the week we’ll get a fuller view of the bank’s outlook for the Colombian economy with the publication of their quarterly Monetary Policy Report on Wednesday and the meeting’s minutes on Thursday that will likely play a bigger role on rate expectations.

Peru July CPI data is Tuesday’s primetime event for us, although global markets will be guided by the RBA’s announcement (likely hold), German unemployment, and the release of US job vacancies and ISM manufacturing survey data. Inflation in Lima broke steeply lower in June, to 6.5% from May’s pace of 7.9%—and significantly missed the 6.9% Bloomberg median. Our Peru colleagues anticipate a smaller deceleration in July, however, to 6.3% as a large decline in poultry prices in June was not repeated. In mid-July, Peru’s Fin Min Contreras revealed that they estimate inflation to print 5.9% y/y, for the first time since January 2022 that inflation would sit in the 5s. Such a result could prompt market bets and economist calls for the BCRP to begin lowering its reference rate in September (we think October).

Things are a bit quieter on Wednesday, but close out with a bang, the BCB’s rate announcement. In the G-10 space, New Zealand Q2 jobs and wages data will be in focus two weeks before the next RBNZ’s decision, while US ADP employment will give us a very rough idea of where Friday’s US nonfarm payrolls may land.

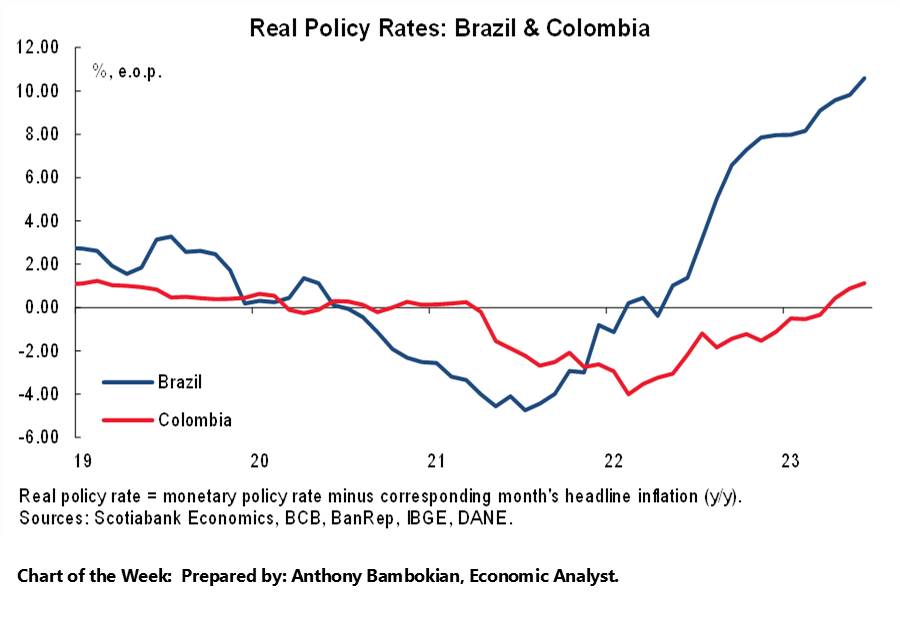

The first BCB rate cut is finally here. Pop the champagne in the Palácio do Planalto, the Selic rate is coming down from 13.75% to 13.25%—or 13.50% and maybe it will only be soft drinks and cold pizza at the President’s office. Inflation (and expectations) has continued to trend in the direction sought by Campos Neto and the rest of the Copom. From the cycle peak of 12.2% in May 2022, headline IPCA-15 inflation has dropped to 3.2% as of July, in data released on the 25th. The latest consumer prices release also show a solid deceleration in services and manufactured goods inflation that show broader-based inflation declines in core categories that had troubled the BCB, delaying the beginning of adjustments.

With the 50bps cut that we expect next week (43bps by the market), the BCB’s real rate would still be at a very restrictive level of around 10%. It’s become safer to assume that another half-point or greater reduction may come at the BCB’s meetings in September, November and December. Markets are currently positioned for a year-end policy rate of 11.50%, or 175bps cuts spread out over the three remaining meetings of 2023 after next week’s. Respondents to the BCB’s weekly survey are more conservative in their expectations, clustered around a 12% target. The most recent IPCA-15 release between weekly surveys could tilt the balance to an 11.75% median in the final pre-decision poll results out on Monday. The size of next week’s cut will certainly be important, but the BCB’s statement and loose guidance around the pace of cuts in coming months will be equally—If not more—relevant for markets.

Some Latam traders may stumble out of the theatre after the BCB’s decision. The movie has been going on forever, it’s already been three days, they’re no longer refilling their popcorn, and the Salma Hayek scene already passed. Their markets will not turn on the theatre lights just yet to roll the credits, because Sweet Caroline just started playing and the BoE’s statement and MPR are coming into focus for Thursday, with markets unsure about whether the bank will hike 25bps or 50bps (38bps priced in, our call is 25bps). Later that day, US ISM services will be the final data point to input into models for the following day’s highlight, the release of US nonfarm payrolls and wages for July that closes out a very busy week accompanied by the random number generator, Canada’s labour force survey.

PACIFIC ALLIANCE COUNTRY UPDATES

Chile—June Economic Activity Figures Continue to Reflect Weakness

Anibal Alarcón, Senior Economist

+56.2.2619.5465 (Chile)

anibal.alarcon@scotiabank.cl

As we mentioned in our last Latam Weekly, our high-frequency data suggest that the slowdown process continued in June, both in goods and in services consumption. Supermarket sales remain weak but stabilizing, at the margin, while restaurant and travel sales showed greater dynamism favoured by CyberDay (transitory effect). In our view, it is not only the weakness of durable goods sales that we observed in Q1, but also that of semi-durable goods more recently. For this reason, we forecast retail sales decreasing 10% y/y in June. Preliminary data for July confirm that no recovery is observed for now.

Taking all of the above into account, we expect June GDP (Imacec) to contract by around 1% y/y, also considering slight y/y declines in other sectors such as mining and construction. With respect to the previous month, we expect no change in the level of non-mining GDP, while mining GDP is expected to increase. Looking ahead, avoiding a technical recession in Q3-23 will require an acceleration of economic activity in the coming months, which will need not only cuts to the BCCh’s policy rate as expected, but also a recovery in public and private investment. In this context, we maintain our GDP growth forecast of -0.8% in 2023, below market expectations in surveys (-0.5%), the Central Bank’s (-0.2%) and the Government’s (+0.2%).

Colombia—Transition Week Between Politics and Light Macro Data Ahead of BanRep’s Meeting

Sergio Olarte, Head Economist, Colombia

+57.601.745.6300 Ext. 9166 (Colombia)

sergio.olarte@scotiabankcolpatria.com

Jackeline Piraján, Senior Economist

+57.601.745.6300 Ext. 9400 (Colombia)

jackeline.pirajan@scotiabankcolpatria.com

Santiago Moreno, Economist

+57.601.745.6300 Ext. 1875 (Colombia)

santiago1.moreno@scotiabankcolpatria.com

The first week of the second legislature of 2023 took place during a week empty of macro indicators. Throughout this first week, Congressional chambers and commissions defined their leaderships and the balance reveals signs of a weakening of the Government party’s influence. In the session’s opening speech, President Petro called for reaching a consensus on key reforms. However, despite current reforms still struggling to find consensus, President Petro is planning to present additional reforms to this legislature in relevant topics such as education, which is for now not supported by key actors, and a reform to mining regulation. At the current point in time, the Government doesn’t have a majority in Congress, though it is important to note that opposition parties also failed to reach a unified block. Broadly, the new legislature starts with a more split balance of power.

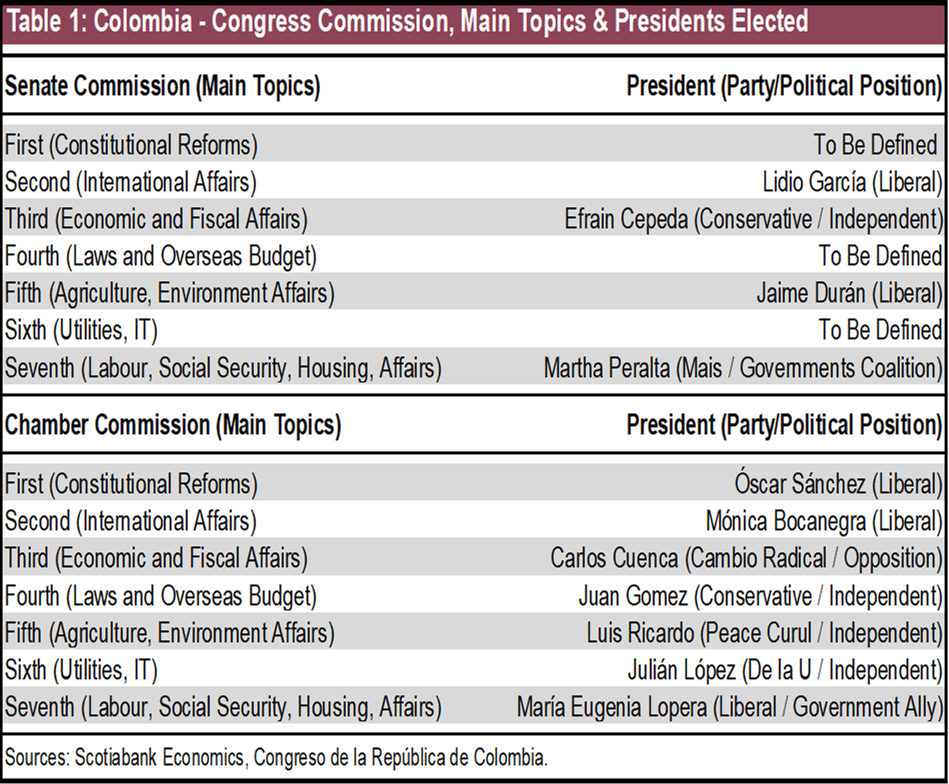

Some interesting facts to highlight are that the Senate leadership was for Ivan Name, who defeated the Government’s candidate, Angélica Lozano. Name reflected the support of traditional parties and is the first signal that this new legislature could pose a greater challenge to the discussion of reforms. Chamber president, Andrés Calle, from the liberal party wasn’t a surprise. The voting process continued with the election of leaders in each congress commission. Among the key commissions, the leadership of the Seventh Commission of the Senate and Chamber, tasked with discussing Health, Pension, and Labour Reforms, went to people close to the Government’s allies, but leadership of the fifth commission, in charge of discussing the potential mining reform, went for a member of the Liberal Party (independent party). All in all, specialized commissions are also showing changes in the balance of power against the Government coalition, which suggests that the reforms under discussion could suffer material changes during debates (see table 1 for a summary of the Commissions composition).

In the second half of the year, the key political milestone is the regional elections, in that regard Saturday, July 29th is the deadline for present candidates. After that, polls will start to take relevance since this will be the main gauge of political strength.

On the economic front, the COP appreciation could offer relief to the imports sector, especially those harder hit by weaker demand, i.e. vehicles and durable goods. However, according to business associations, this impulse still could take longer in being reflected in lower prices since inventories are increasing and consumers remain discouraged by the high cost of credit—meaning reduced purchases by firms from abroad at lower prices given there’s little need to add to inventories.

Fedesarrollo’s confidence data for the business sector showed a contrast between retailers and manufacturers, retail confidence is still weakening, impacted by weaker demand, while on the industrial side, expectations are improving as they anticipate increased production in coming months thanks to lower production costs and the lower USDCOP. Scotiabank Economics projections indicate that the weak period was overcome in the second quarter and that in the near/medium term things could start to show marginal improvements to take the economic growth of all 2023 to 1.8%.

BanRep will have its monetary policy meeting on Monday, July 31st. This meeting will have a fresh set of macroeconomic projections from BanRep’s staff. Our balance ahead of BanRep’s meeting shows that inflation slowed stronger than expected, economic activity maintains decent levels, risk in financial markets has diminished. This support our expectation of rate stability, but during the week it will also be important to see how the balance of risks stand in BanRep’s Monetary Policy Report, which could help us to anticipate the timing for a rate cut.

Peru—New Congress Authorities and Expectations for Presidential Message

Mario Guerrero, Deputy Head Economist

+51.1.211.6000 Ext. 16557 (Peru)

mario.guerrero@scotiabank.com.pe

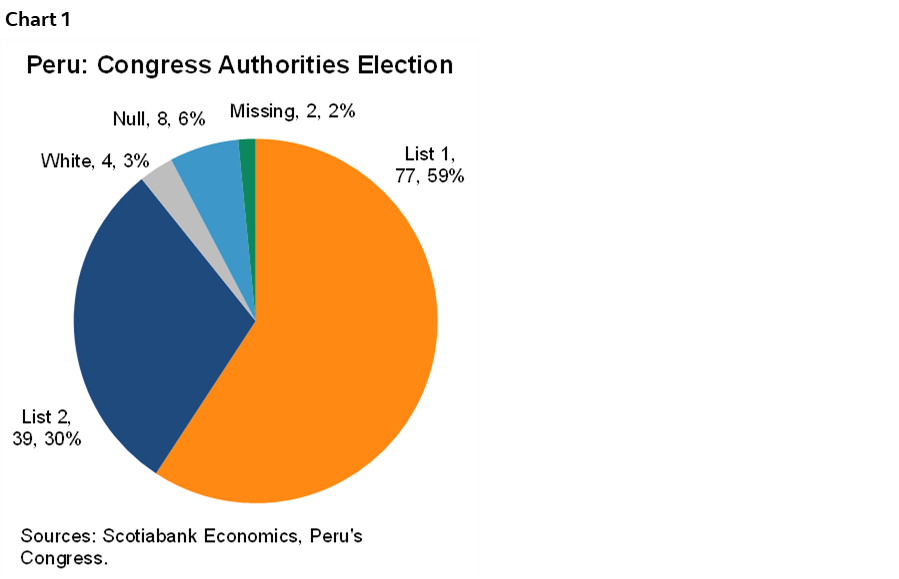

On July 26th, Congress elected its new authorities between two lists. List 1 was the winner with 77 votes out of 130, with surprising members from extreme factions, such as the right-wing Fuerza Popular party and the left-wing Perú Libre party, and centrist parties such as Avanza País and Alianza para el Progreso, which represents a political coalition that could add to the precarious governance of the Boluarte regime. The president of Cabinet welcomed the election and urged working on a joint agenda, a task that has not been easy so far. Even though the list was not ideal, it was the one that best represented the current composition of Congress, so it was not necessary to go to a second round. With 59% of the votes, it prevailed over List 2, made up of members who have been questioned for corruption and who could have brought populist surprises in the economic sphere (chart 1).

The new president of Congress, Alejandro Soto, is a lawyer from Cusco who has been a member of the Alianza para el Progreso (APP), a movement chaired by Cesar Acuña, since 2008 and he has been the host of political programs on television in southern parts of the country. He has held the presidency of the Transportation Commission in the 2021–2022 period and is a spokesman for APP party. In February 2023, he voted in favour of an initiative of the Peru Libre party that proposed early elections and a referendum for a Constitutional Assembly. It is not known if he will now maintain that position.

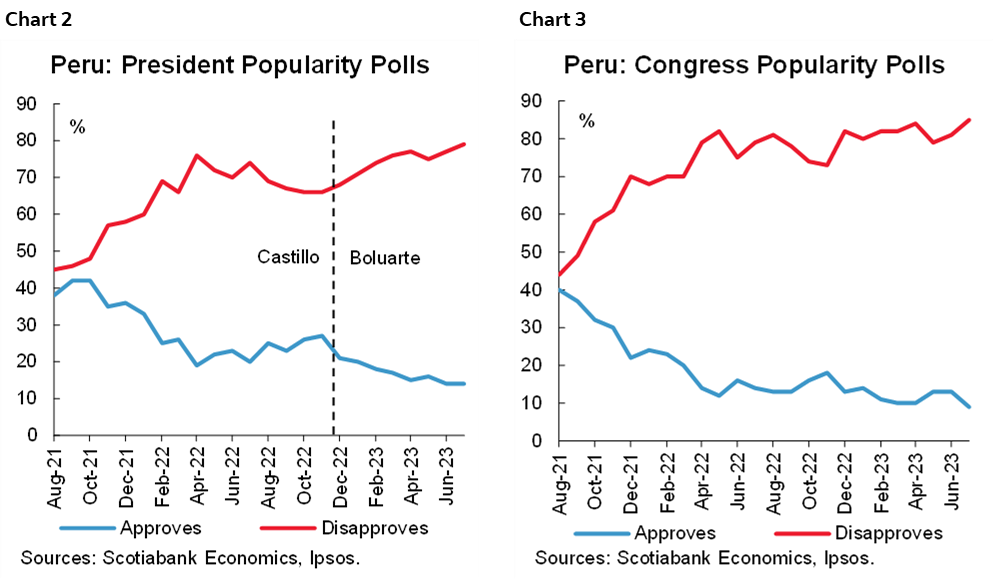

It is not yet clear what the agenda of the new authorities in Congress will be, but the low level of approval (only 9% according to the Ipsos poll, see charts 2 and 3) leaves no room for error. The Peru Libre party would seek to retake its flag to convince Congress to hold a Constitutional Assembly. Although it is unlikely that this type of initiative will prosper, the formation of the Constitutional Commission will be key to determining the intensity of the political noise around this issue.

On Friday, July 28th, President Dina Boluarte will deliver a presidential message for the National Holidays. There were no expectations regarding it, although given the results of the formation of the new authorities in Congress, the meetings that the governor of the BCRP, Julio Velarde, has held in recent days with high government authorities (including President Boluarte) and the recent statements by the Minister of Finance, Alex Contreras, regarding the announcement of specific measures, we hope this will be an opportunity to consolidate messages that contribute to improving business confidence and promoting investment.

In recent announcements, the Minister of Finance has been optimistic, insisting that Peru is not in recession—despite the most recent weak economic indicators—and that he expects inflation to continue to fall below 6% in July. Our July inflation forecast is 6.3%.

Among other announcements, the minister also highlighted that: i) measures have been approved against the El Niño phenomenon (Plan “Con Punche Emergencia”) for PEN 3.5Bn (0.4% GDP), ii) an execution level of 50% was reached in the economic reactivation plan "Con Punche Perú" (0.8% GDP), iii) PEN 0.4Bn of a total of PEN 3Bn (0.3% GDP) have been disbursed from the "Impulso MyPerú" plan that provides financing to SMEs, iv) public investment has been growing at the national government level (+12%) but not at the subnational government level (-15% in the case of regional governments and -33% in the case of local governments). These efforts have been providing some support to the economy, although so far not to a sufficient degree to move the needle on economic indicators.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Click here to be redirected |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.