ECONOMIC OVERVIEW

- Next week’s Latam schedule is relatively empty, with 2Q GDP details out of Mexico, Peru, and Chile in focus alongside Brazilian June activity figures. Mexico’s busy release calendar also includes the release of retail sales, H1-Aug CPI, and Banxico’s meeting minutes.

- In today’s report, the team in Mexico writes on their expectations for next week’s releases while the team in Peru updates us on the country’s positive terms of trade developments, covers the latest fiscal figures, and outlines their expectations for inflation and the BCRP.

- Abroad, markets will pay close attention to comments by Fed speakers at the Jackson Hole Symposium and we’ll also get the first look at economic conditions in August with global PMIs for the month due on Thursday. Canada, the U.K., and Japan also publish July inflation data.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Mexico and Peru.

MARKET EVENTS & INDICATORS

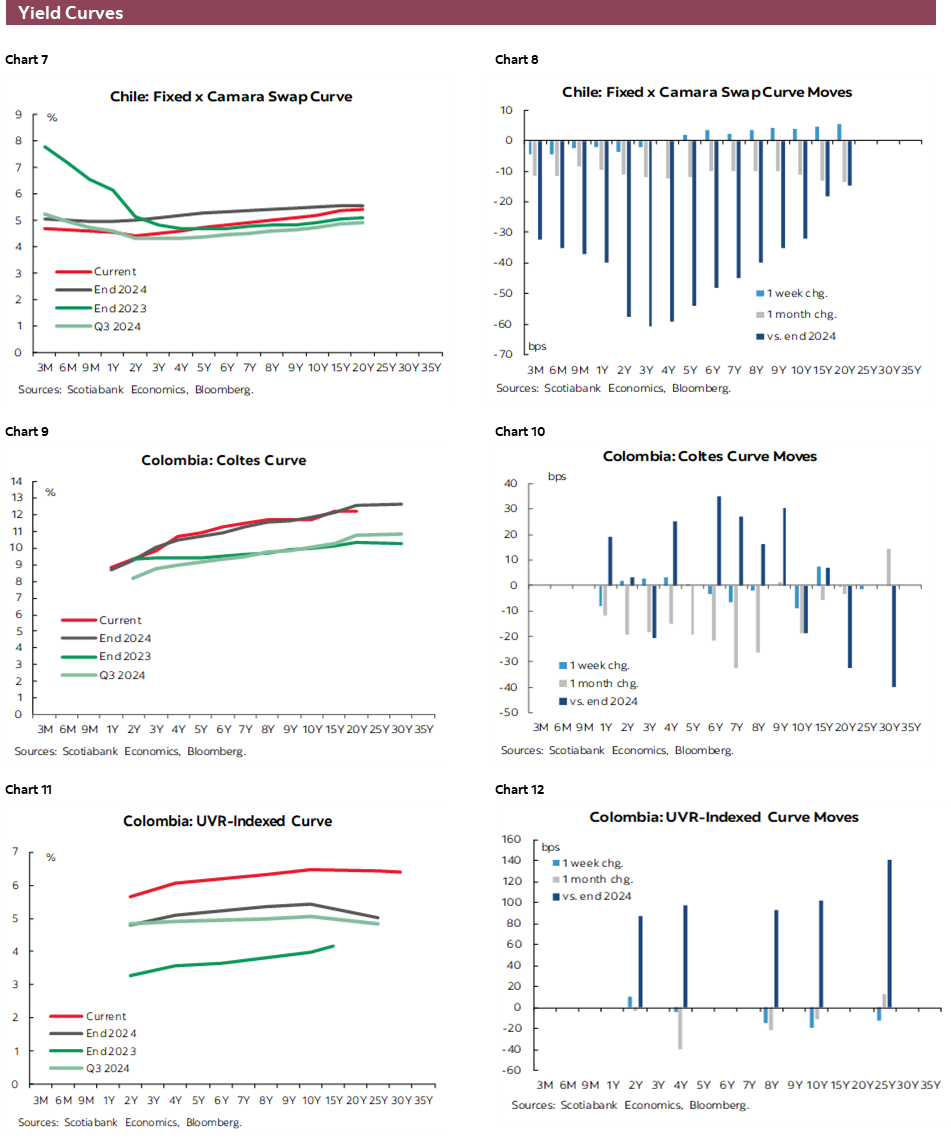

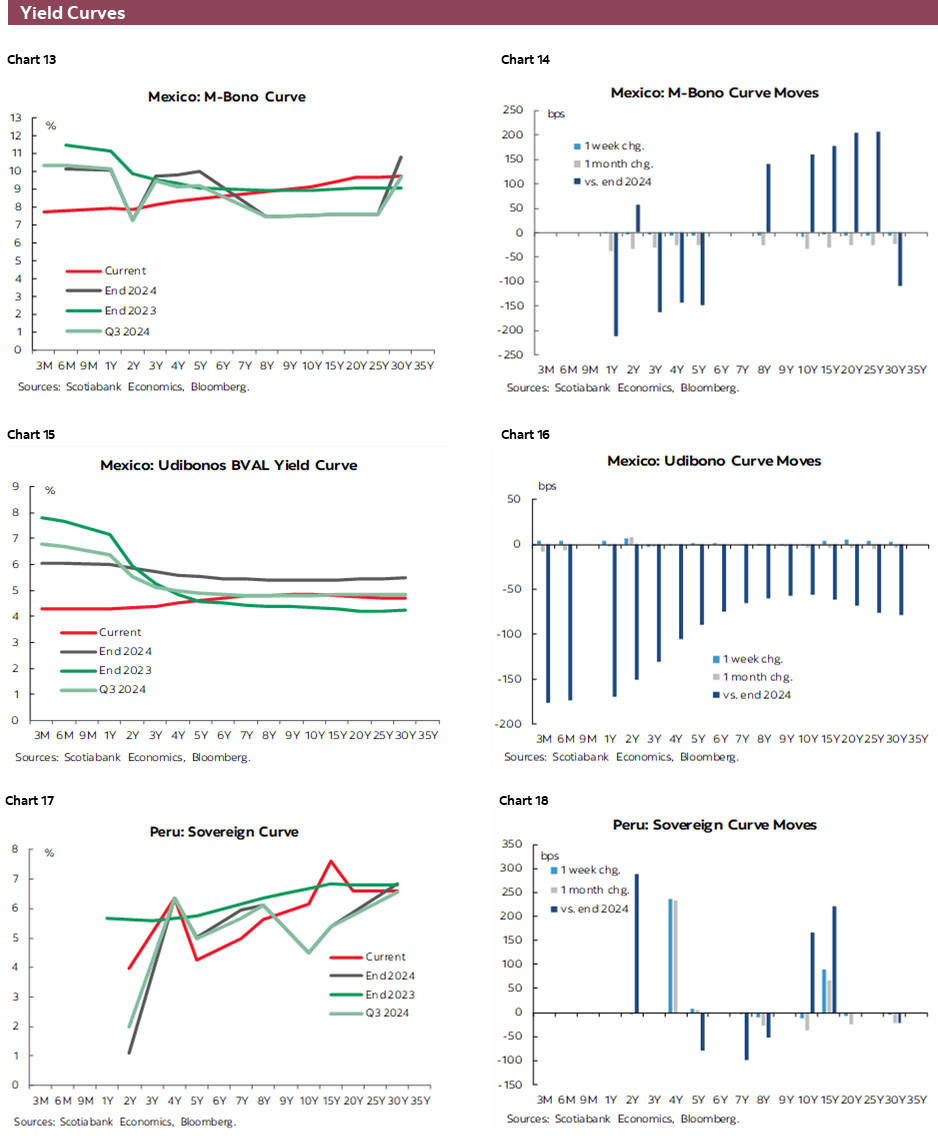

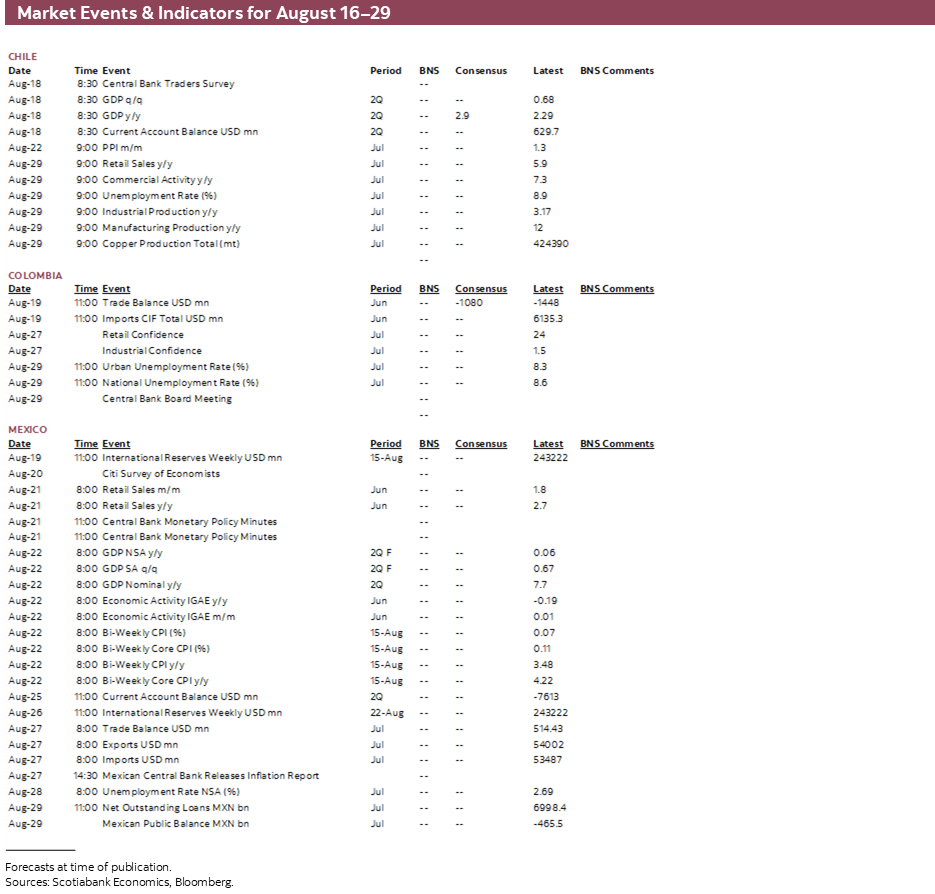

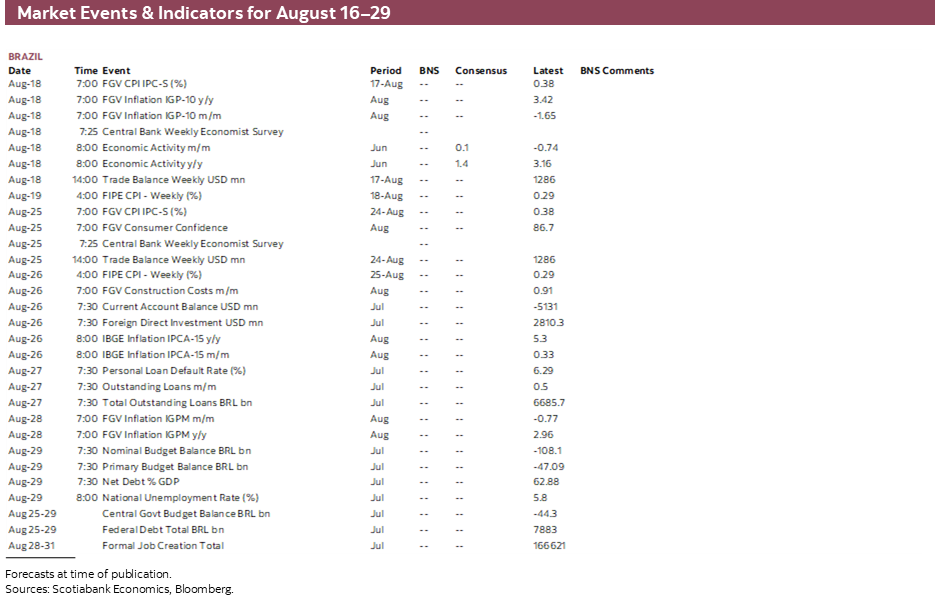

- A comprehensive risk calendar with selected highlights for the period August 16–29 across the Pacific Alliance countries and Brazil.

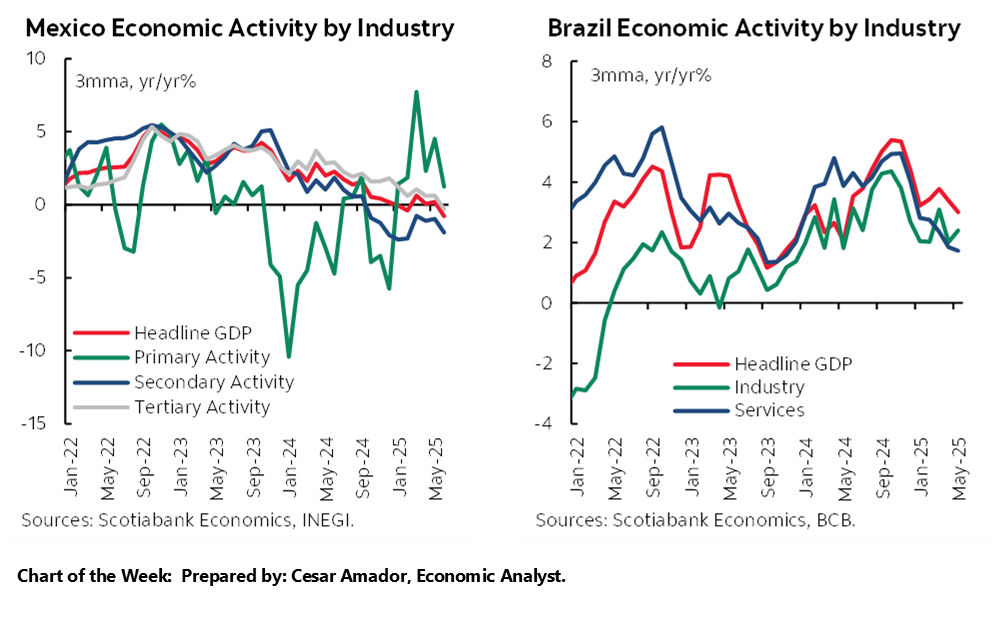

Chart of the Week

ECONOMIC OVERVIEW: REFINING 2Q LATAM GDP, GLOBAL PMIs AND JACKSON HOLE

Juan Manuel Herrera, Senior Economist

+52.55.2299.6675

juanmanuel.herrera@scotiabank.com

- Next week’s Latam schedule is relatively empty, with 2Q GDP details out of Mexico, Peru, and Chile in focus alongside Brazilian June activity figures. Mexico’s busy release calendar also includes the release of retail sales, H1-Aug CPI, and Banxico’s meeting minutes.

- In today’s report, the team in Mexico writes on their expectations for next week’s releases while the team in Peru updates us on the country’s positive terms of trade developments, covers the latest fiscal figures, and outlines their expectations for inflation and the BCRP.

- Abroad, markets will pay close attention to comments by Fed speakers at the Jackson Hole Symposium and we’ll also get the first look at economic conditions in August with global PMIs for the month due on Thursday. Canada, the U.K., and Japan also publish July inflation data.

There’s not a ton to be excited about next week in Latam, with the region having a relatively empty calendar with a focus on expenditure or sectoral details for 2Q GDP out of Mexico, Peru, and Chile to give us a better sense of the balance of growth, and also rounding out Brazil’s 2Q data with June economic activity figures. Mexico has the busiest calendar of all, with H1-Aug CPI, June retail sales, Banxico’s meeting minutes, and the results of the Citi survey also on tap. Chilean PPI and Colombian international trade figures should be of limited influence on markets.

Abroad, markets will pay close attention to comments by Fed speakers at the Jackson Hole Symposium and we’ll also get the first look at economic conditions in August with global PMIs for the month due on Thursday. The Fed’s meeting minutes will also be parsed for confirmation or refutation of the market’s near-full expectation that the bank will cut rates next month (~80–90% priced-in). Canadian CPI on Tuesday, a 25bps rate cut by the RBNZ and U.K. CPI on Wednesday, and Japanese CPI and U.K. retail sales on Friday fill up the G10 schedule. At writing, we’re also keeping an eye on what comes out from Friday’s Trump-Putin summit in relation to the Russia-Ukraine war.

In today’s report, the team in Mexico go over their expectations for next week’s releases. The first release of 2Q GDP showed that Mexico’s economy managed a modest 0.7% q/q expansion on the back of the secondary and tertiary sectors. We’ll get detailed colour on what subsectors were behind this improvement alongside the release of June economic activity (IGAE) data. In May, the IGAE readings suggest that a firmer manufacturing industry helped secondary sector growth, while tertiary sector drivers were more broad-based.

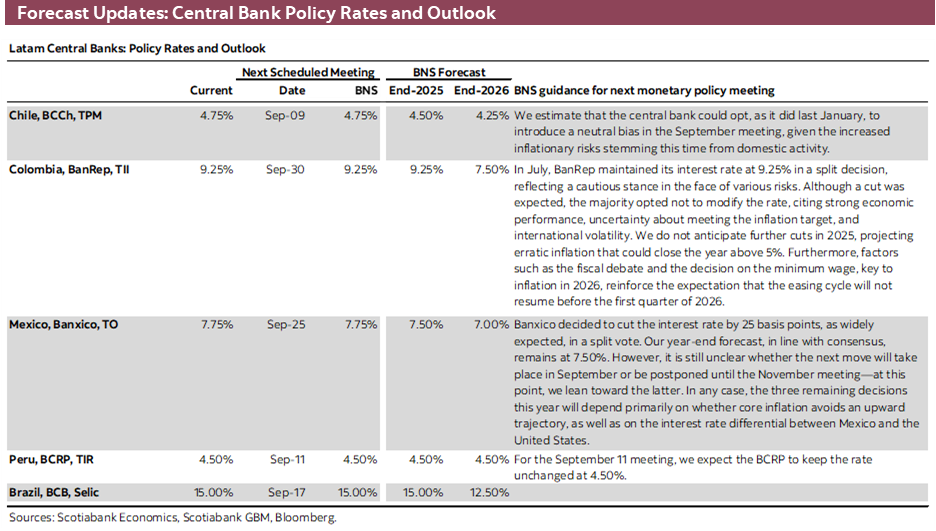

As for CPI, inflation is estimated to have rebounded in August from a temporary lull in July when base effects were key in pulling headline inflation to the mid-3s from 4.3% in June. Meanwhile, core inflation is expected to remain practically unchanged at 4.2–4.3% as merchandise prices pressure it higher. Banxico’s 25bps rate cut decision on the 7th pointed to greater concerns around core inflation, but markets are still placing about 80% odds of a repeat 25bps at the September announcement. The meeting minutes out on Thursday may shed some light on which members of the board may join Heath in voting for a rate hold.

Based on monthly data released this morning, Peru’s economy expanded by 2.9% y/y in 2Q, slowing from the 3.9% of 1Q, though maintaining a nevertheless solid pace where the timing of Easter in April instead of March as in 2024 played an important role in this deceleration. As the team highlights in today’s Weekly, terms of trade have unexpectedly been a strong positive for Peru’s economy in 2025, despite the threat and application of tariffs and a broad sense of a global economic deceleration. With data to date, the team maintains its forecast for 3.3% growth in 2025, but we’ll look at the expenditure details of 2Q GDP data out on Friday. Aside from their analysis of trade and economic dynamics in Peru, our economists provide an update on fiscal developments, inflation expectations, and the outlook for the BCRP.

PACIFIC ALLIANCE COUNTRY UPDATES

Mexico—GDP Details and H1-Aug CPI

Rodolfo Mitchell, Director of Economic and Sectoral Analysis

+52.55.3977.4556 (Mexico)

mitchell.cervera@scotiabank.com.mx

Miguel Saldaña, Economist

+52.55.5123.1718 (Mexico)

msaldanab@scotiabank.com.mx

Next week, two particularly relevant economic indicators will be released in Mexico: the final estimate of GDP for the second quarter and inflation for the first half of August.

The final GDP reading will be key to assessing sectoral dynamics during the second quarter, complemented by monthly IGAE data, which will allow us to track sectoral performance through June. We do not anticipate significant revisions from the initial estimate.

As we’ve recently highlighted, sectors most closely tied to investment—such as construction, mining, and wholesale trade—have been the most affected by a highly uncertain environment. This uncertainty stems from both international factors and domestic developments, including the implementation of constitutional reforms approved last year, particularly the reform of the judiciary, as well as concerns about security conditions for doing business in the country.

Meanwhile, sectors linked to private consumption and household income continue to show weak momentum, impacted by a stagnant labour market and declining remittances. In contrast, export-oriented sectors such as manufacturing have performed relatively well. However, they remain vulnerable to uncertainty surrounding potential changes in trade policy between Mexico and the United States.

For the second half of the year, we expect these conditions to remain relatively unchanged and therefore continue to forecast an economic contraction in 2025—albeit less pronounced than in previous estimates.

Regarding inflation, following a moderation to 3.51% y/y in July, we expect a rebound in headline inflation in August, although likely remaining below 4.0%, with pressures concentrated in the core component.

July’s print was positively influenced by falling prices of fruits and vegetables, driven by excess supply. Additionally, the base effect contributed to the moderation, as inflation in July 2024 was particularly high (5.57%) due to climate-related disruptions in agricultural production, which pushed prices up by 13.7% in July 2024. While the base effect may still play a role in August, its impact is expected to be smaller this time.

On the other hand, pressures in core components remain a key concern. At its latest monetary policy meeting, the Bank of Mexico’s Governing Board highlighted the persistence of core inflation as a significant upside risk.

As such, this upcoming reading will be crucial for adjusting expectations regarding both inflation and interest rates in the coming months.

Peru—Enjoying the Fruits of Strong Terms of Trade

Guillermo Arbe, Head Economist, Peru

+51.1.211.6052 (Peru)

guillermo.arbe@scotiabank.com.pe

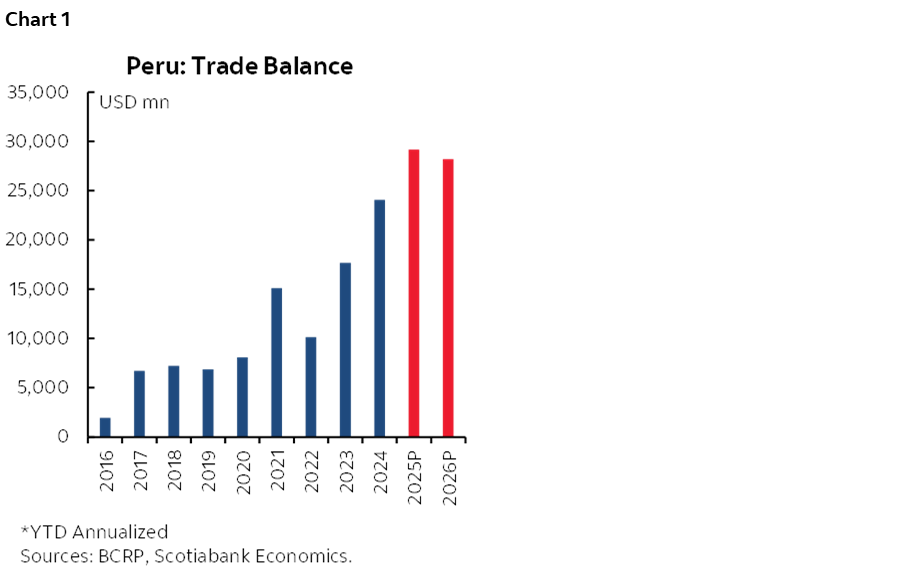

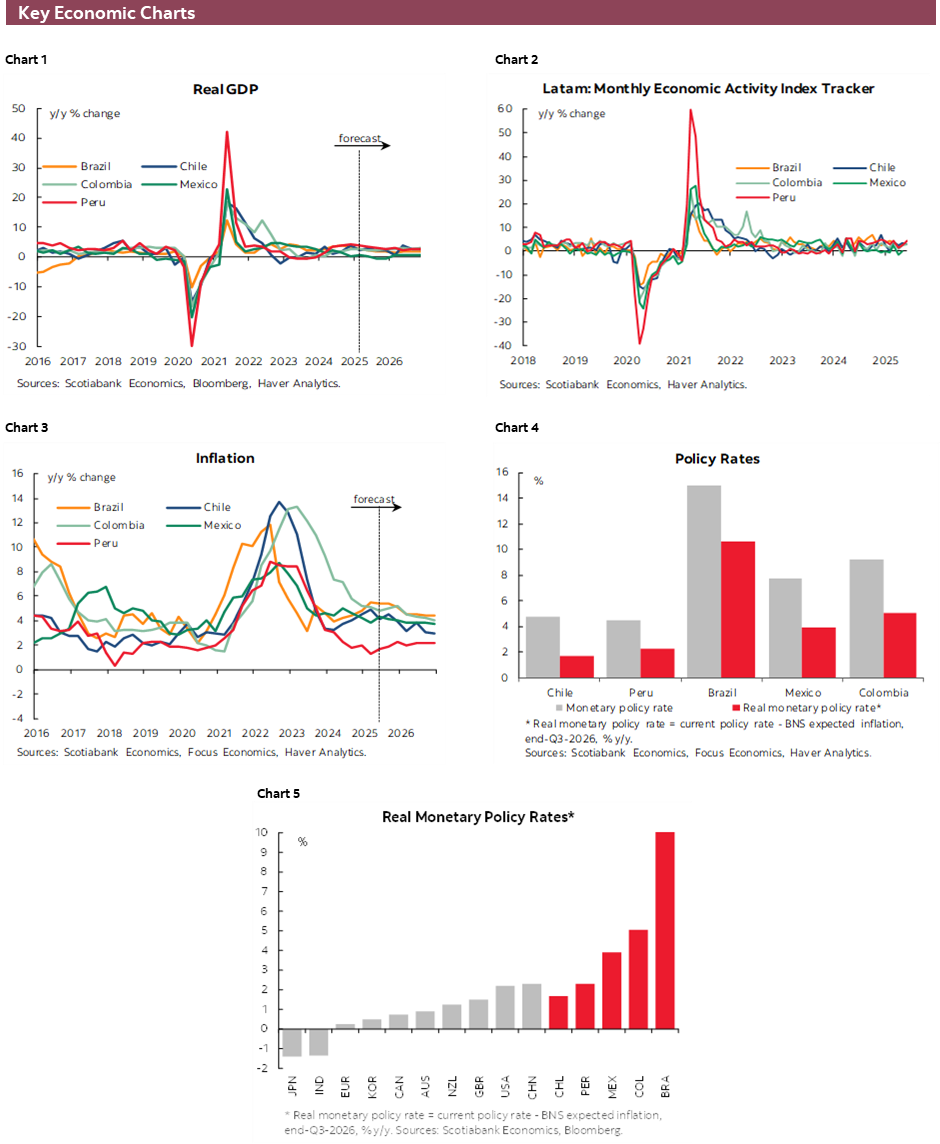

Peru’s economy has been extraordinarily stable throughout 2025. We have needed to make only minor changes in our forecasts so far this year, and we see nothing indicating an increase in volatility in economic trends. What’s more, as unlikely as it sounds, with terms of trade at all-time highs, the global environment continues to be favourable for Peru (chart 1). Metal export prices continue outperforming our expectations, led by gold, while copper remains robust even after a 50% tariff was announced by the U.S. government for certain copper products. Equally important, prices for many of Peru’s imports, especially those linked to the production of staple goods, have declined this year, namely oil, wheat (used in bread), maize (for chicken feed), and soy (cooking oil). One can argue, then, that the tariff issues and global uncertainty have influenced these price dynamics in a positive way for Peru. This has implications for GDP growth, macro accounts, and price stability.

We maintain our 3.3% GDP growth forecast for full-year 2025. At least for now. The fact is GDP growth is actually trending mildly below this level. At the same time, however, the jobs market is robust and could well provide enough support going forward to maintain our 3.3% forecast. We’ll have a better feel for this when we revise the Q2 private consumption and private investment growth figures to be released on August 22nd. This release, regarding private investment growth in particular, will be key for our growth outlook going forward. The higher private investment comes in for Q2, the more likely it will be that we will not need to revise our GDP growth figure for 2025.

On the downside, high gold prices are also driving an expansion in illegal gold mining. This expansion is adding to GDP growth, but, of course, also imply multiple negative impacts on welfare in a broader sense.

Meanwhile, high metal prices are also contributing to strengthening Peru’s macro accounts. External accounts are extremely positive, and we expect another consecutive record trade surplus in 2025, at US$29.2b, a sharp 21% increase from another record US$24.1b in 2024.

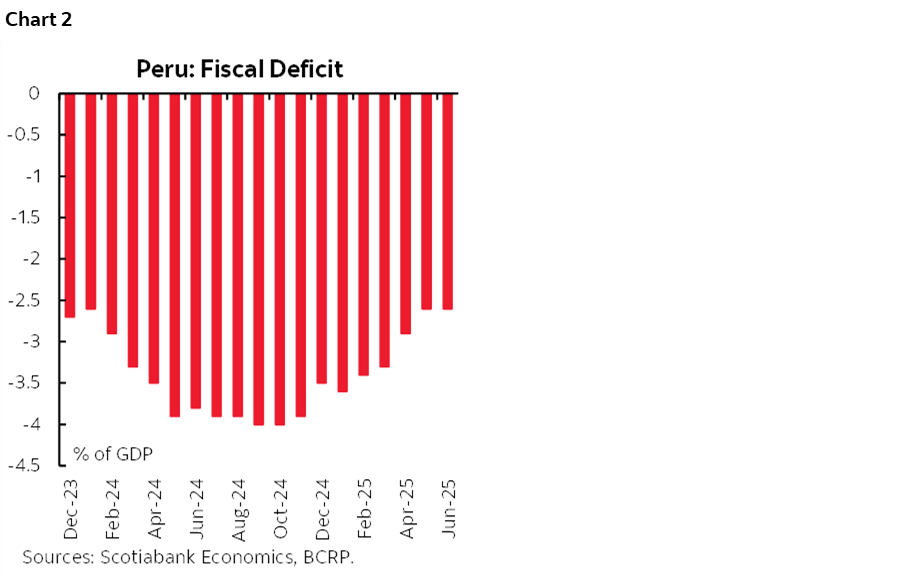

We already have fiscal deficit figures for Q2. Over the four-quarter period to Q2 2025, the fiscal deficit was 2.6% of GDP (chart 2). This is a sharp improvement from the near-term high of 4.0% of GDP in October 2024, less than a year ago. The main driver behind this improvement was not a slowdown in government spending (which did occur to some extent), but, rather, an increase in fiscal revenue, with mining companies contributing significantly on the back of high metal prices. Once again, global events are proving, so far at least, to be more of a blessing than a curse for Peru. This has been true to such an extent that the government, which at one point had been contemplating raising the fiscal deficit target for 2025 from 2.2% of GDP to 2.8%, has canceled these intentions, and is maintaining the 2.2% target. Basically, the government has found that fiscal revenue is strong enough to uphold this target without sacrificing spending.

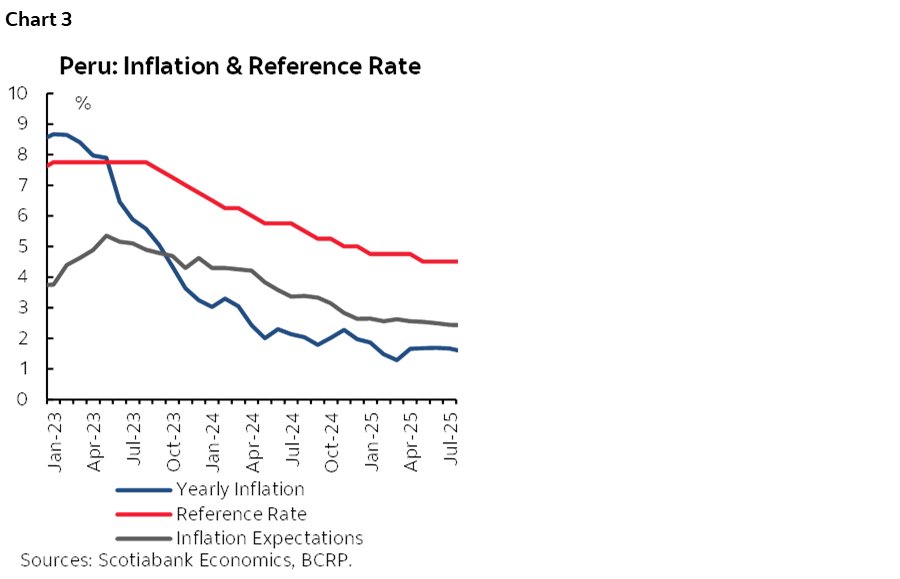

Finally, price stability. We won’t get new inflation data for another two weeks, when inflation for August is released on September 1st. However, the trend for inflation to date is encouraging. Yearly inflation has been stable for the last few months, at 1.7%, including July. For August, the key prices we follow are trending at nil or lower for the month. If such low monthly inflation is confirmed, this would lead to a decline in yearly inflation for August (monthly inflation in August 2024 was +0.28%). The soft inflation print for August is, no doubt, in part driven by currency appreciation, in addition to declining import prices for oil and for soft commodities that are used to produce staples. Thus, low inflation also reflects in part Peru’s strong terms of trade. If yearly inflation does decline in August, we would need to take a close look at our forecast of 2.3% inflation for full-year 2025. The risk is to the downside (chart 3).

One has to wonder what the BCRP will do with inflation trending lower than expected, and with inflation expectations declining. This scenario certainly gives the BCRP more room to consider at least one further 25bps decrease in the reference rate. Take note, however, that whatever decision the BCRP takes, it is likely to do so with an eye on the Fed. Should the Fed lower its reference rate, this would increase the likelihood that the BCRP will do as well, without inverting interest rate differentials.

Note that throughout this discussion, we have not mentioned the 2026 elections. This continues to be a risk, but it is a risk that has had no visible bearing on Peru’s economic data so far in 2025. If anything, judging by business confidence levels which have stabilized in positive territory, the business community does not seem overly concerned about the 2026 elections. This may change, but for the time being, the 2026 elections do not appear to be on the economics radar screen.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Click here to be redirected |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.