ECONOMIC OVERVIEW

- CPI releases from Mexico, Chile, and Colombia and a 25bps rate cut announcement by Banxico are next week’s Latam highlights, coming off a busy week into another busy week in the region and the G10.

- In today’s report, our team in Mexico updates its projection for GDP growth in 2025, from a 0.5% contraction to a slight 0.1% decline for the year based on recent data and a less bad tariffs outlook.

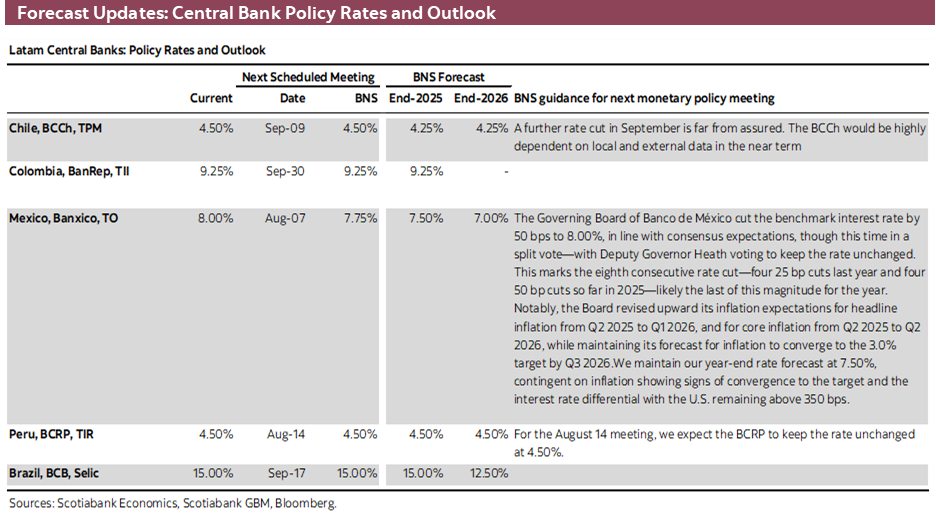

- Thursday’s July CPI data are unlikely to pull Banxico away from a 25bps rate cut that same day before a probable pause at its September meeting. Fixed investment figures should remain weak amid domestic and external risks.

- Chile and Colombia publish July inflation figures at the close of the week, coming off an expected rate cut and an unexpected rate hold, respectively, in recent days.

- Chilean data may increase the odds of another 25bps rate cut in September (as is our local team’s call) while Colombia’s should have little influence on BanRep, which is now in wait-and-see mode until next year’s minimum wage hike is decided.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in Mexico.

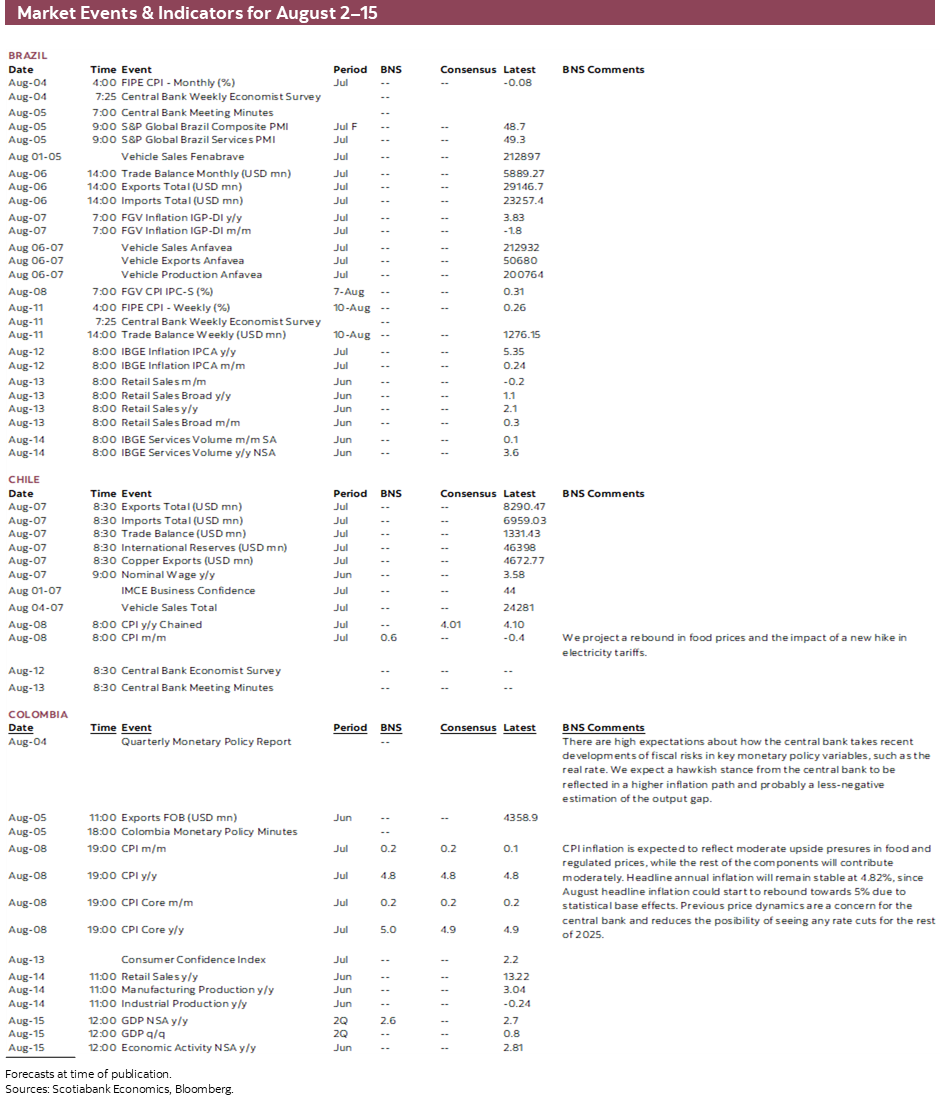

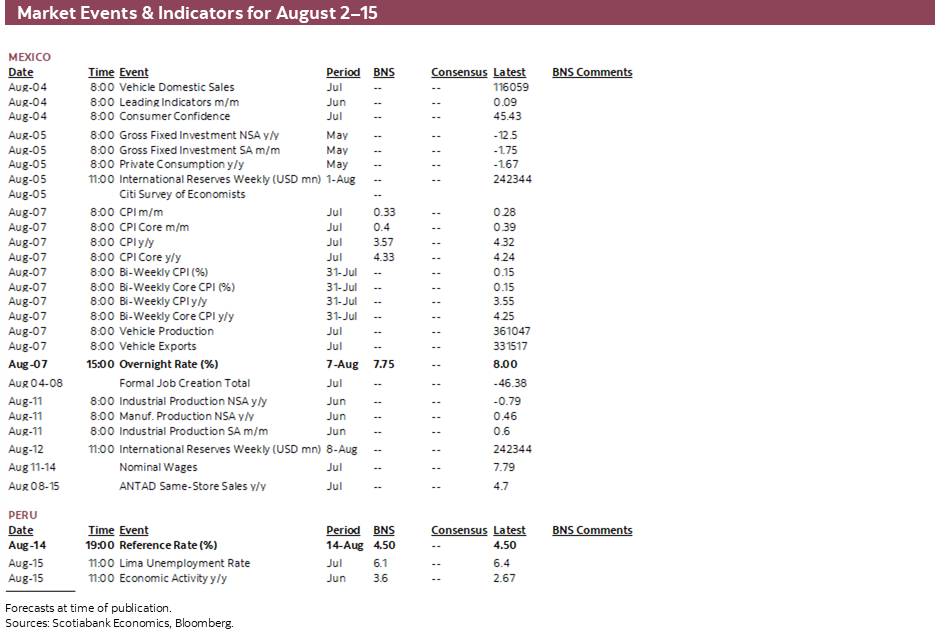

MARKET EVENTS & INDICATORS

- A comprehensive risk calendar with selected highlights for the period August 2–15 across the Pacific Alliance countries and Brazil.

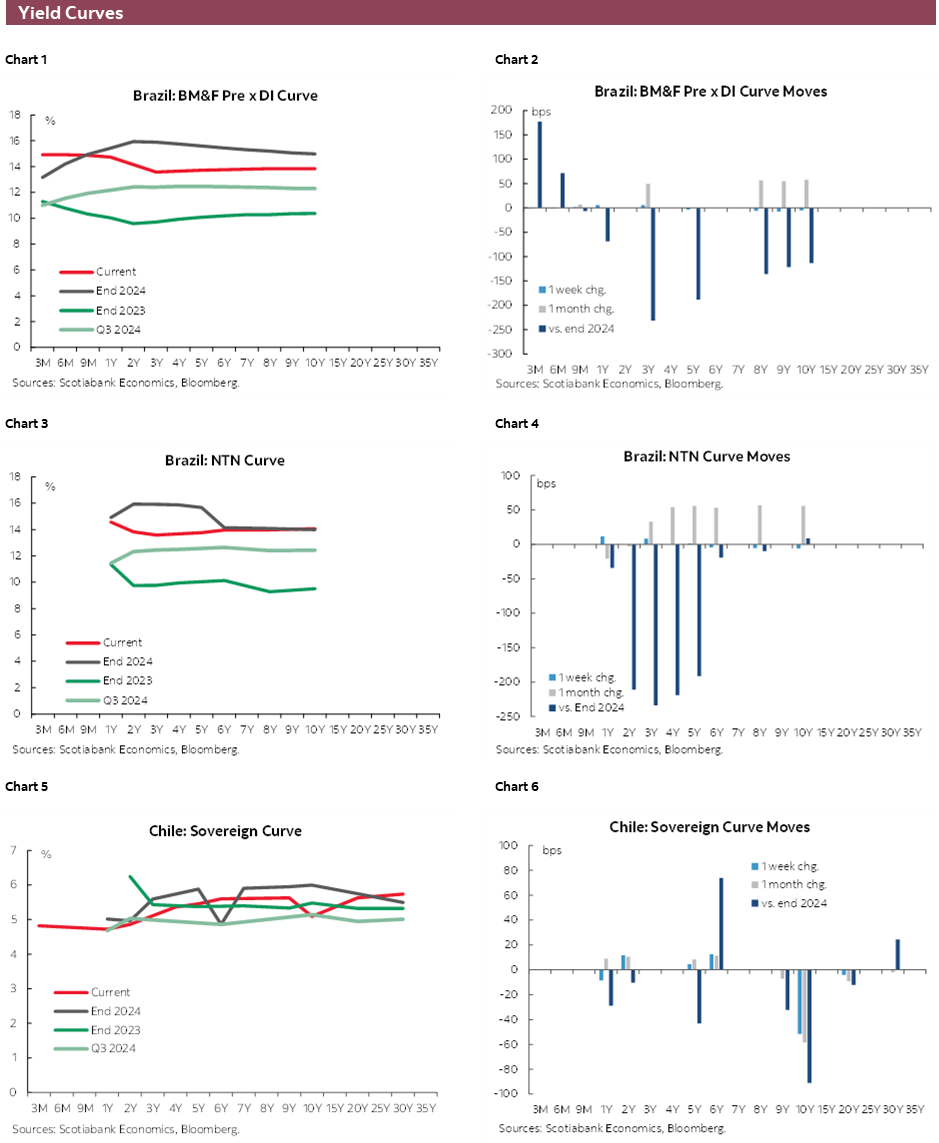

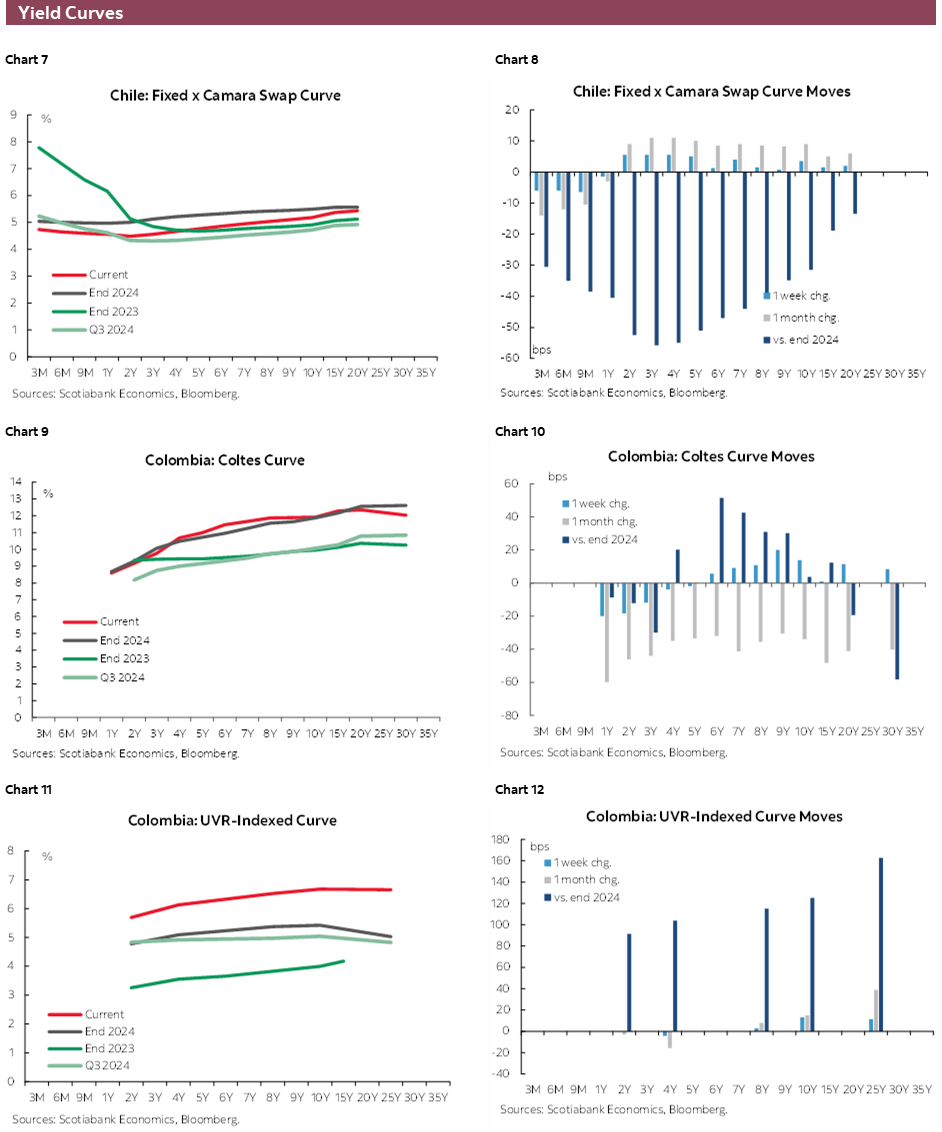

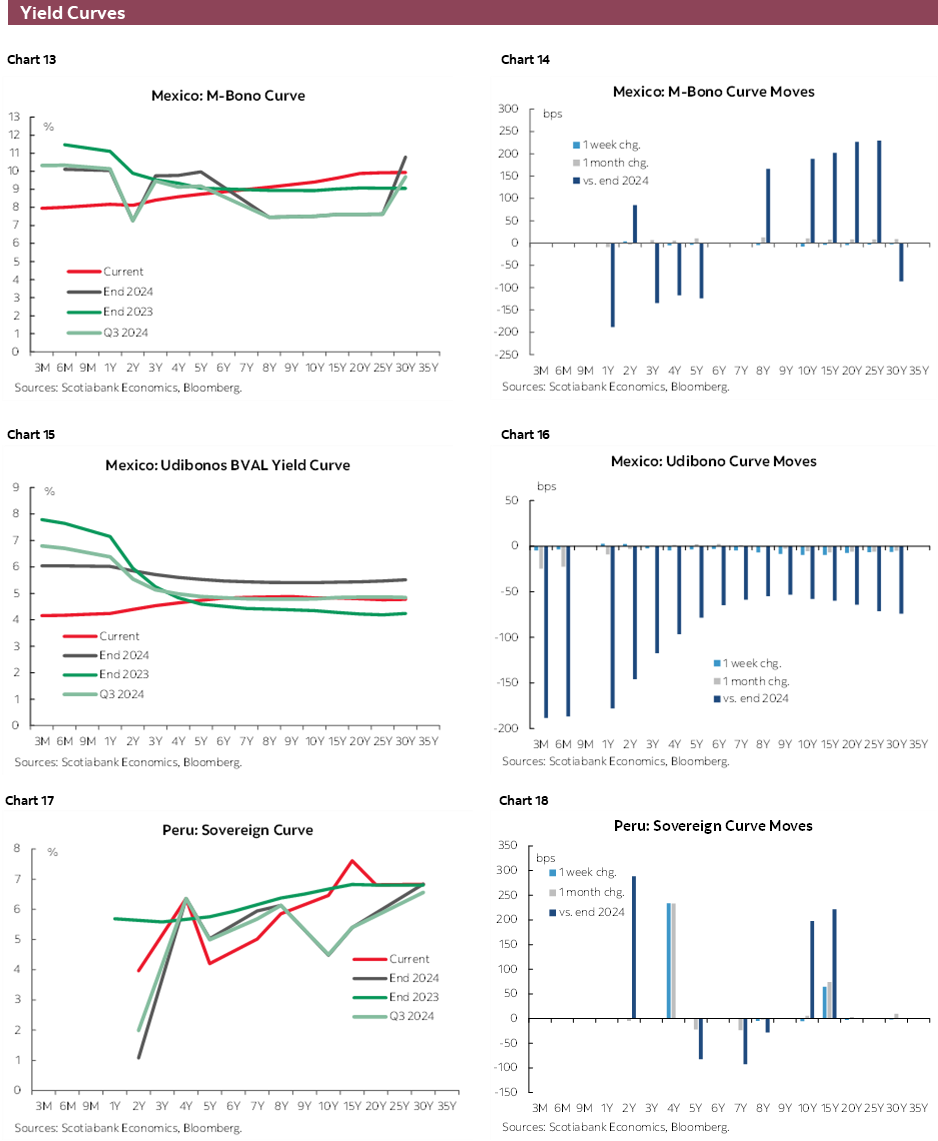

Chart of the Week

ECONOMIC OVERVIEW: REGIONAL CPIs AND BANXICO DECISION

Juan Manuel Herrera, Senior Economist

+52.55.2299.6675

juanmanuel.herrera@scotiabank.com

- CPI releases from Mexico, Chile, and Colombia and a 25bps rate cut announcement by Banxico are next week’s Latam highlights, coming off a busy week into another busy week in the region and the G10.

- In today’s report, our team in Mexico updates its projection for GDP growth in 2025, from a 0.5% contraction to a slight 0.1% decline for the year based on recent data and a less bad tariffs outlook.

- Thursday’s July CPI data are unlikely to pull Banxico away from a 25bps rate cut that same day before a probable pause at its September meeting. Fixed investment figures should remain weak amid domestic and external risks.

- Chile and Colombia publish July inflation figures at the close of the week, coming off an expected rate cut and an unexpected rate hold, respectively, in recent days.

- Chilean data may increase the odds of another 25bps rate cut in September (as is our local team’s call) while Colombia’s should have little influence on BanRep, which is now in wait-and-see mode until next year’s minimum wage hike is decided.

After a big week of key data and central bank decisions in Latam and the G10 awaits a big week of key data and central bank decisions in Latam and the G10. From key U.S. GDP and labour market figures, Mexican and Chilean GDP, and BCCh, BanRep, Fed, BoC, and BoJ meetings (and tariff announcements) we now turn to CPI releases from Mexico, Chile, and Colombia, Canadian employment data (local markets are closed on Monday for Civic holiday) and US ISM services and productivity prints, as well as 25bps rate cut announcements by Banxico and the BoE.

Peru is again taking it easy with a quiet calendar and taking Tuesday off, while Brazil has the minutes to the latest BCB decision as next week’s highlight. On Sunday, OPEC+ is expected to announce another 548k barrels/day output hike that would fully undo its supply reductions launched in 2023 that totalled 2.2mmbpd. Chinese international trade data for July on Thursday will be watched for the effect of scaled back (still-high) U.S. tariffs.

In today’s report, our team in Mexico updates its projection for GDP growth in 2025, from a 0.5% contraction to a slight 0.1% decline for the year, following better-than-expected (albeit still-soft) 2Q GDP data released earlier this week. The U.S.’s 90-day delay to its planned 5ppts tariff hike on Mexican imports (to 30%) has also taken some of the edge off for Mexico’s unimpressive economic outlook. Concerns around Mexican growth partly centre on political and fiscal risks at home.

Markets should get additional clarity on fiscal risks next Tuesday, when the Sheinbaum government is due to unveil a comprehensive plan for Pemex aimed at turning around the fortunes of the troubled state-owned oil company. That same day, investment data will be closely monitored for ongoing signs of depressed sentiment in the private sector in the face of important domestic and external headwinds that have resulted in consistent y/y declines in private capital expenditures for the better part of a year.

The focus for economists and markets alike will be Thursday’s July CPI data followed by Banxico’s rate decision later that day. With H1-Jul CPI data already at hand, there is limited room for surprise in next week’s inflation figures. The release is forecast to show a significant decline in headline inflation due to base effects (from 4.3% to 3.5%) while core inflation remains elevated around 4.2% due to upside pressures in merchandise prices and still-high services inflation.

Nearly all economists anticipate that Banxico will lower its overnight rate to 7.75% from 8.00% (with one likely dissenter preferring a rate hold again). Data since the bank’s latest decision have been mostly as expected (notwithstanding the small GDP overshoot) while market volatility or risks have been generally acceptable, opening the door to another rate cut aimed at supporting soft economic conditions. That said, we think Banxico will choose to stay put for at least one meeting before cutting rates again. Our attention will therefore be on the language in the statement codifying the possibility of another rate cut at the September decision.

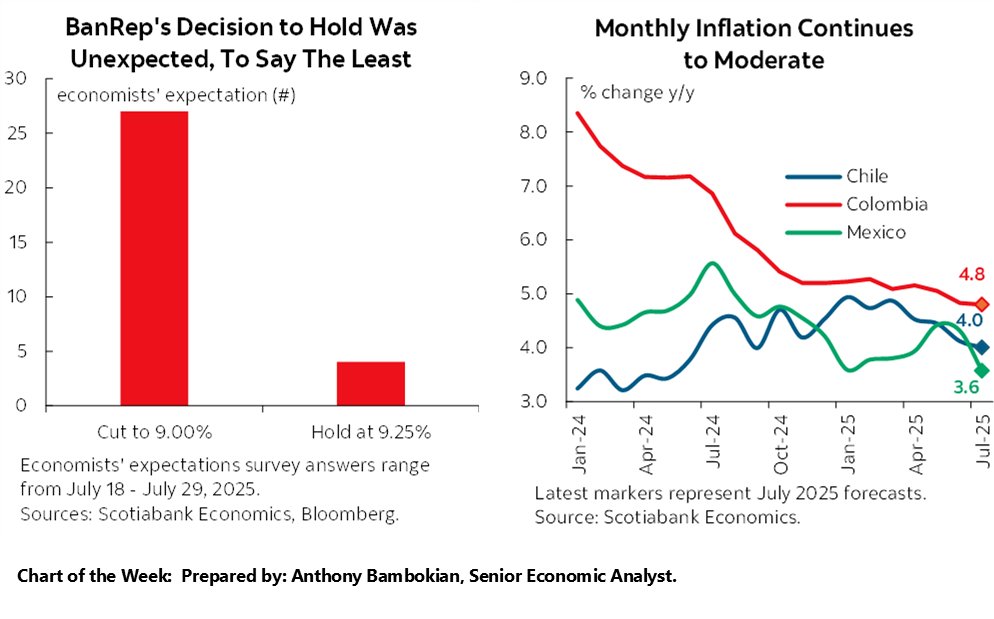

Chile and Colombia publish July inflation figures at the close of the week, coming off an expected rate cut and an unexpected rate hold, respectively, in recent days. Our team’s projection is for the BCCh to roll out another 25bps rate reduction at its September meeting, provided there are no important inflationary surprises nor an important worsening of international (i.e., the CLP) conditions that may motivate a more cautious stance as was the case at its June decision when Iran-Israel risks kept it from easing policy.

Next week’s data are expected to show a slight decline in Chilean headline inflation from 4.1% to 4.0%. It may end up being the case that a 3-handled reading brings forward the market’s next priced in rate cut, which as of Friday’s close was still only fully priced in for the October meeting, though with about 40% implied odds of a September move.

As for Colombia’s prices print, it’s tough to see how it may change the view of the central bank towards a rate cut after yesterday’s surprise hold. The median economist expects practically no change in headline or core inflation, leaving both sitting only a few decimal points shy of the 5% level and expected to remain this way for the balance of the year—with our team expecting inflation to rebound to this mark from August.

Now, BanRep has clearly highlighted the risks that next year’s minimum wage hike poses for their inflation goal, and it will not be until late-2025 that we’ll get a better sense of how large this increase may be. We get to pick BanRep’s brain next week with Monday’s Monetary Policy Report (with updated projections) and the minutes to the latest decision on Tuesday.

PACIFIC ALLIANCE COUNTRY UPDATES

Mexico—Upward Revisions to Growth Expectations Following a Stronger Q2 Reading and a New Tariff Pause

Rodolfo Mitchell, Director of Economic and Sectoral Analysis

+52.55.3977.4556 (Mexico)

mitchell.cervera@scotiabank.com.mx

Miguel Saldaña, Economist

+52.55.5123.1718 (Mexico)

msaldanab@scotiabank.com.mx

The first estimate of Mexico’s GDP for the second quarter of 2025 exceeded expectations, although it still reflected a certain sluggishness in economic activity. Annual real growth was just 0.1%, while seasonally adjusted quarterly growth reached 0.7%. Since late 2024, growth prospects have deteriorated, driven primarily by rising uncertainty both globally and domestically. The most affected sectors have been those tied to investment decisions, such as construction and wholesale trade. Other industrial sectors, including electricity and water generation, as well as mineral extraction, have remained weak for several years. More recently, consumption-related sectors have shown signs of stagnation, in line with a halt in formal job creation and a moderation in remittances, which have now posted three consecutive months of annual declines.

In this context, the IMF revised upward its global growth forecasts for 2025 and 2026, including an improved outlook for Mexico. Back in April, the institution anticipated a more adverse trade environment between Mexico and the United States. Now, the IMF projects a slightly better estimate for the US, from 1.8% to 1.9% in 2025, but it is more optimistic for 2026 (2.0%). Mexico received a higher positive adjustment: the IMF now expects modest growth of 0.2%, in contrast to the previously anticipated contraction. However, the outlook for 2026 remains unchanged at 1.4%, below the historical average. Across most countries, the projections point to a deceleration compared to 2024, with no major shifts in the underlying narrative. Elevated uncertainty and the anticipated impact of tariff impositions continue to weigh on expectations. The IMF also highlighted that high fiscal deficits and the potential for inflationary pressures could tighten financial conditions across economies.

Considering the Q2 reading and the recently announced pause in generalized tariffs on Mexican imports to the U.S., we have revised our GDP forecast for 2025 upward, but are still expecting a contraction, now of -0.1% (-0.5%), below the +0.3% consensus. While the tariff pause is a positive impression, other protectionist measures remain in place, such as the 25% tariff on products that do not meet USMCA requirements. As such, this measure does not fundamentally resolve the sources of heightened international uncertainty.

Domestically, uncertainty also persists. In terms of public finances, questions remain about the sustainability of spending cuts aimed at reducing debt, despite efforts by the Ministry of Finance to extend the maturity profile of debt instruments. Additionally, the implementation of constitutional reforms—such as those affecting the judiciary power—remains pending, with new judges set to take office in September. It is still unclear how long it will take businesses to adapt to the legal changes. Finally, security continues to be a key factor in assessing business risks and costs.

Thus, despite Mexico’s economy performing slightly better than expected in the second quarter, structural risks continue to weigh on the growth outlook. The IMF’s upward revision reflects a less adverse global environment, supported by recent tariff pauses since April. However, it does not eliminate the challenges facing economies in a context less conducive to cooperation and trade. Investment is likely to remain constrained by institutional uncertainty, while consumption slows amid a stagnant labour market. Going forward, revisions to growth expectations will largely depend on the implementation of agreements that foster greater confidence in the business environment.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Click here to be redirected |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.