ECONOMIC OVERVIEW

- A busy period awaits Latam markets, continuing the trend of the past few weeks with global financial turmoil and central bank decisions in the major economies.

- Between now and Good Friday on April 7, central banks in Colombia, Mexico, and Chile will deliver policy decisions while all four countries in the Pacific Alliance will publish March inflation data in the first week of April.

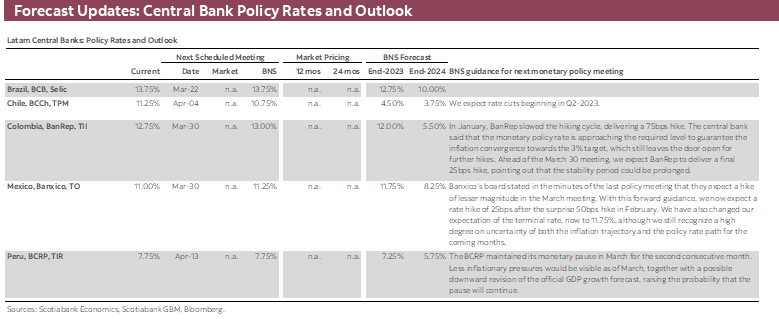

- BanRep and Banxico are set to hike 25bps next week, while the BCCh will likely move in the opposite direction, starting its cutting cycle in early-April. The BCRP can’t rest on its laurels as it hopes that inflation trends towards sub-8% levels. Meanwhile, the BCB’s meeting minutes and its quarterly inflation report will likely push back on rate cuts pressure from Lula and company.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Chile, Colombia, Mexico, and Peru.

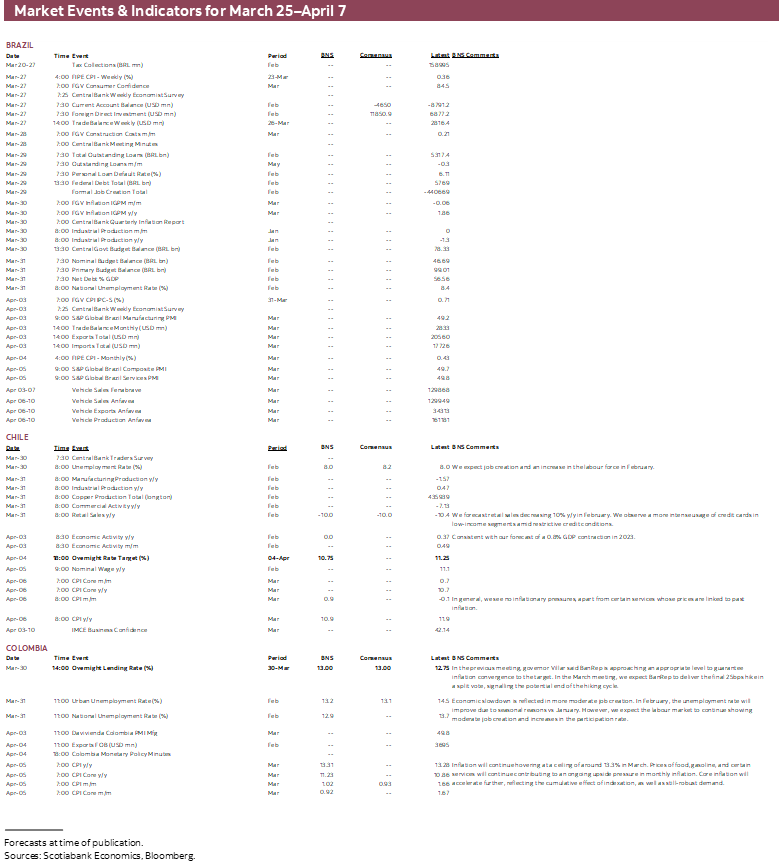

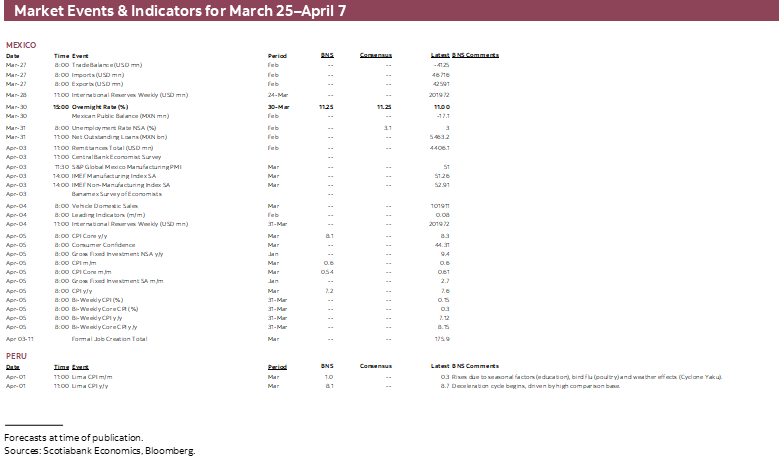

MARKET EVENTS & INDICATORS

- A comprehensive risk calendar with selected highlights for the period March 25–April 7 across the Pacific Alliance countries and Brazil.

Chart of the Week

ECONOMIC OVERVIEW: A FORTNIGHT OF CENTRAL BANK DECISIONS AND INFLATION DATA

Juan Manuel Herrera, Senior Economist/Strategist

Scotiabank GBM

+44.207.826.5654

juanmanuel.herrera@scotiabank.com

- A busy period awaits Latam markets, continuing the trend of the past few weeks with global financial turmoil and central bank decisions in the major economies.

- Between now and Good Friday on April 7, central banks in Colombia, Mexico, and Chile will deliver policy decisions while all four countries in the Pacific Alliance will publish March inflation data in the first week of April.

- BanRep and Banxico are set to hike 25bps next week, while the BCCh will likely move in the opposite direction, starting its cutting cycle in early-April. The BCRP can’t rest on its laurels as it hopes that inflation trends towards sub-8% levels. Meanwhile, the BCB’s meeting minutes and its quarterly inflation report will likely push back on rate cuts pressure from Lula and company.

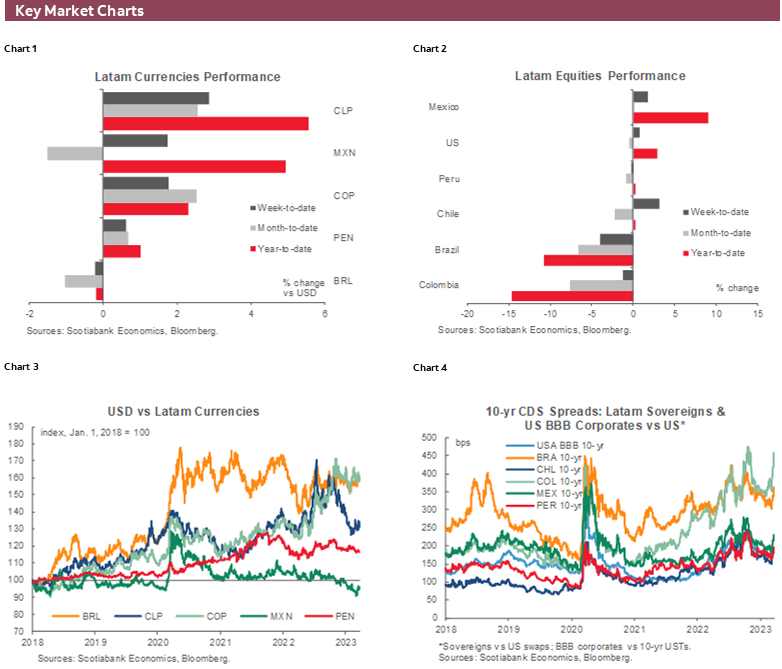

A busy period awaits Latam markets, continuing the trend of the past few weeks with global financial turmoil and central bank decisions in the major economies. Local developments have certainly had a say in the relative performance of the region’s assets, this is particularly true in Brazil with Lula and his team pressuring the BCB to cut (unsuccessfully), but the overarching story of lower global yields and cautious equity markets have strong-armed domestic storylines out of the spotlight.

The Mexican peso went from trading at a four-year high below the 18 pesos level a couple of weeks ago to trade above the 19 pesos level within a week, and remaining near the mark earlier today, with the most obvious trigger for this weakness being the steep fall in US yields that took Mexican rates along for the ride, as well as risk-off sentiment (which has also impacted its Latam FX peers). A global growth slowdown resulting from banking failures is bound to see Fed policy easing, and with it Banxico.

Weak output could translate into declines in commodity prices that act against the likes of the CLP, PEN, and COP; copper prices have held up relatively well, all things considered, but crude oil has fallen to its lowest point since late-2021. These months were supposed to see strength in commodity prices thanks to China’s reopening. That has not been the case.

How the banking sector situation evolves remains anyone’s guess, though one could speculate that markets have delivered their opinion via a sharp steepening of yield curves and rates markets pricing in Fed cuts as soon as the summer months. We think panic has taken over markets, and overextended positioning may have exacerbated moves (and with it led to an overinterpretation of what central banks may do). Traders went from speculating on a half-point hike in the US to witnessing a major bank failure (SVB) in a short period of time, and were caught offside and had to move quickly to cover shorts.

A normalisation of the risk backdrop could see some of the recent moves reverse, providing a risk-on tailwind for Latam currencies and equities, with firmer commodities alongside them. Still, there’s limited appetite to jump back in given the recent volatility in markets.

Between now and Good Friday on April 7, central banks in Colombia, Mexico, and Chile will deliver policy decisions while all four countries in the Pacific Alliance will publish March inflation data in the first week of April. With global risks top of mind for officials and markets, deciding on the need for additional hikes, or even cuts, has become a more difficult task when the most recent macroeconomic data do not clearly suggest a sharp slowdown is in the works.

Persistently elevated inflation (particularly in core services) is pointing to the need for additional tightening of monetary policy but, if all goes as planned, base effects and declines in international commodity prices are teeing up sizable declines in inflation in the months ahead; and central bankers are optimistic that rate hikes to date will act against services inflation continuing its ascent much more.

Unfortunately, BanRep, Banxico, and the BCCh will not have March CPI data at hand when they decide on rates over the next two weeks, but our economists expect that headline inflation in Mexico and Chile will decelerate; in the case of Mexico, H1-March data reinforces this view. The BCRP, who chose a few weeks ago to leave its reference rate unchanged, as was widely expected, has three weeks until its next decision (another hold is expected), but it will watch next week’s March print with the hope that headline inflation heads towards sub 8% levels. We think it’ll come in just a bit above the figure.

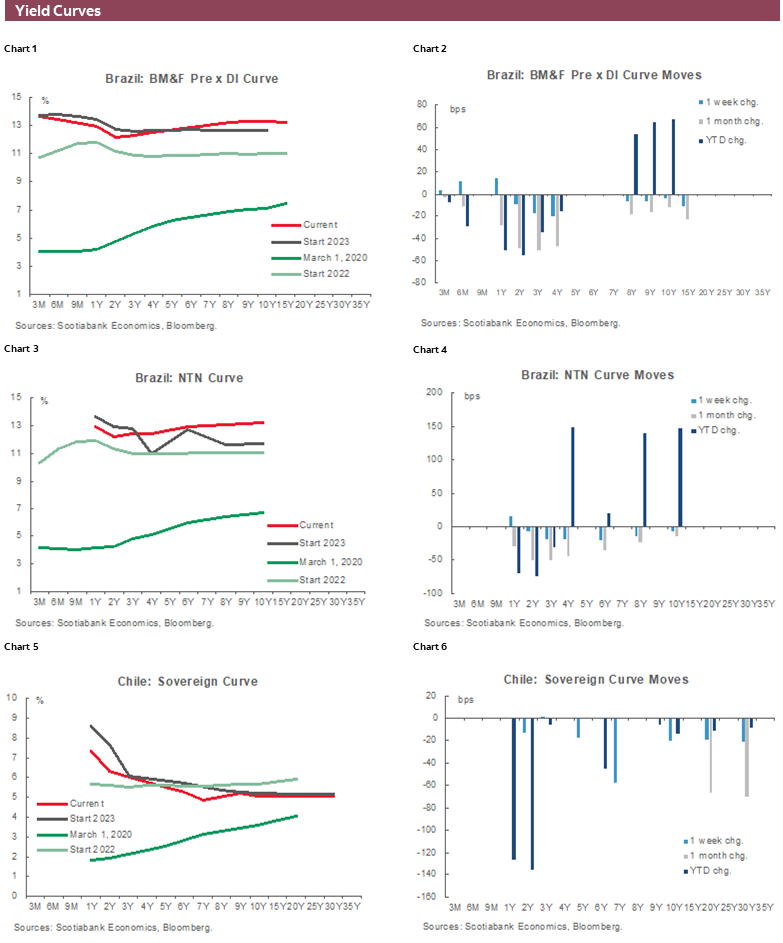

BanRep, however, will still be faced with inflation around a cycle high (the team expects a practically unchanged pace) and a steep path in core inflation that has the tailwind of indexation practices. This is motivation enough to see BanRep hike by 25bps next week according to our economists in Colombia. Banxico is still troubled by high core inflation and officials have expressed no signs of stepping back next week, so we anticipate a rate hike there too. The situation is different in Chile, with the team expecting the BCCh to begin its rate-cutting cycle on April 4, with a 50bps reduction to its highly restrictive policy rate of 11.25%.

And, last but not least, Brazil’s BCB just had a rate decision earlier this week (a hold) with the minutes to this meeting due for release next week and set to be closely monitored for signs that it could soon consider a cut. Based on the latest decision, it seems unlikely. And the bank may even use the opportunity to reaffirm to its critics that it will not yield to pressure. The BCB’s quarterly inflation report (the first of Lula’s current term) and accompanying presser will also likely be used as a tool for Campos Neto’s insistence on an unchanged rate.

Alongside central bank decisions and inflation and other regional economic data releases, the global and Latam market pulse will continue to fluctuate on financial sector risks while the release of US PCE inflation and nonfarm employment data (as well as ISM, JOLTS, and ADP figures) could be of great importance for policy expectations—that’s if the current situation unfolds without significant economic damage. As always, keep an eye on political developments in Latam with reform processes in Colombia and Chile, and Brazil’s fiscal framework plans worth monitoring.

PACIFIC ALLIANCE COUNTRY UPDATES

Chile—Busy Economic Agenda Ahead of Central Bank Meeting

Anibal Alarcón, Senior Economist

+56.2.2619.5465 (Chile)

anibal.alarcon@scotiabank.cl

The statistical agency (INE) will publish on Friday, March 31, data by economic sector, which are used as an input for the monthly GDP growth estimates. For February, we expect a further decline in retail sales, around 10% y/y, mainly due to lower levels of purchases in supermarkets, department stores and electronics. In contrast, our short-term indicators for debit card purchases showed high dynamism in services, especially in restaurants and the tourism sector. With this, we project GDP growth of around 0% y/y in February. As we mentioned in our Latam Daily, the negative surprise in services in Q4-2022, due to a one-off effect in transportation services, would not have a negative impact on 2023 GDP. In line with this, we maintain our forecast of a 0.8% GDP contraction for the current year.

In this context, the labour market has surprised positively in recent months, mainly thanks to the contribution of the public sector to monthly job creation. For the quarter ending February (data to be published on Thursday, March 30), we project an unchanged unemployment rate of 8.0%, mainly due to our expectation of high employment dynamism that would be similar to that observed in the labour force. In our view, the rapid fiscal budget execution observed in December 2022 and January 2023 would continue to provide support for the labour market during Q1-2023.

On the other hand, the Financial Traders’ Survey (also to be published on March 30), should show a drop in 1 and 2-year inflation expectations after the surprise in February’s CPI figures, in line with what was observed in the Economic Expectations Survey published in early-March. At the same time, and taking into account recent developments in financial markets, we are likely to see an increase in the probability of a rate cut at the upcoming meetings. In this regard, the central bank will go into its monetary policy meeting on April 4 without the March CPI data in hand, when we expect a 50bps rate cut to 10.75% and a dovish tone for the coming meetings.

Finally, we expect CPI inflation around 0.8–0.9% m/m in March (below market expectations), mainly due to the positive contribution of educational services. In general, we see no inflationary pressures coming from the rest of the basket, except for some services whose prices are linked to past inflation. Looking ahead, we continue to expect annual inflation to converge rapidly to the central bank’s target, ending this year at 3.7% y/y. March CPI inflation figures will be released by INE on Thursday, April 6.

Colombia—Idiosyncratic Volatility is Easing; BanRep is Approaching the End of the Hiking Cycle

Sergio Olarte, Head Economist, Colombia

+57.1.745.6300 Ext. 9166 (Colombia)

sergio.olarte@scotiabankcolpatria.com

Jackeline Piraján, Senior Economist

+57.1.745.6300 Ext. 9400 (Colombia)

jackeline.pirajan@scotiabankcolpatria.com

During the last year, Colombian assets have overreacted to any international shock due to lower liquidity and especially higher domestic uncertainty around structural reforms and a more disruptive than expected communication strategy from Petro’s Government that has been not taken well by markets. However, recent worldwide banking system distress did not make Colombian assets deteriorate further than peers, which is at least interesting to analyze.

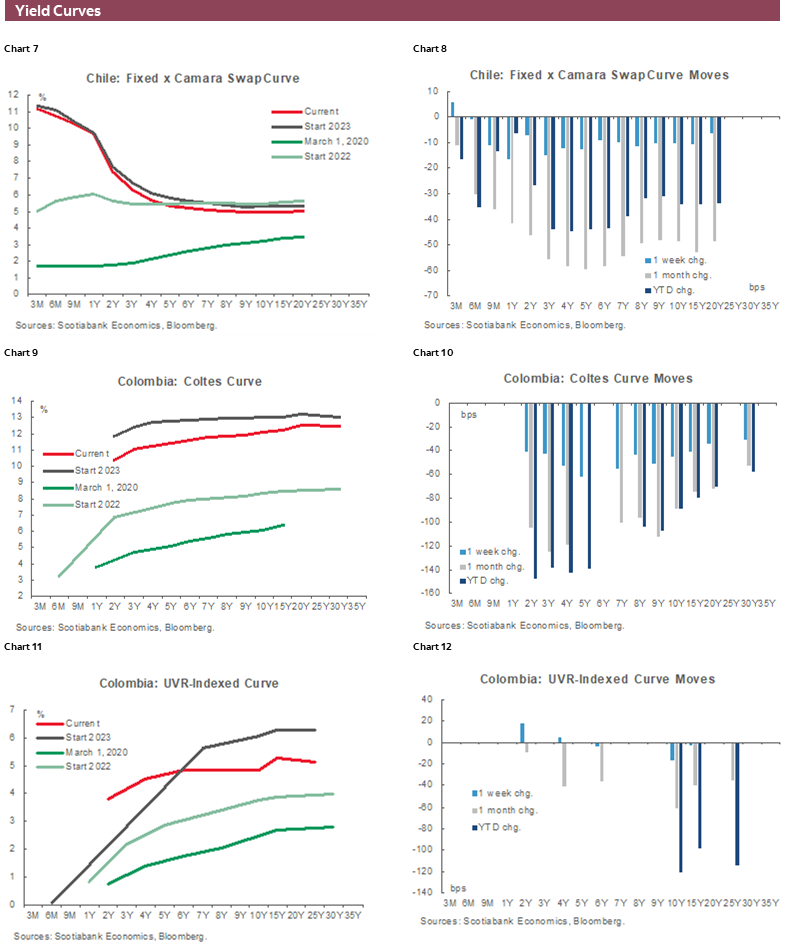

The initial hypothesis is that markets already priced in the additional risk premium that the new Colombian administration’s communication strategy has produced, therefore new pricing volatility should be around external turmoil instead of additional domestic uncertainty. In fact, recent developments around labour and pension reform haven’t been real news for markets. Even President Petro deciding to fire Alejandro Gaviria as Minister of Education did not really move markets. Our calculations say that in the exchange rate, idiosyncratic risk already priced in is around COP750, while it could be around 100 to 150bps in the yield curve. Therefore, if markets see Petro’s announcements and reforms as initially expected, which incorporate the negative bias to market liquidity and some nonstructural rule changing, it should not further affect market pricing. On the contrary, if, for instance, the pension reform guarantees that liquidity and the TES market framework will continue, market participants (particularly offshore) can increase their appetite and help TES and the FX rate to reduce a bit the risk premium in the markets.

Further to the political noise already priced in, we see that some domestic agents have started to add more TES risk to their portfolios. In fact, some trust and insurance companies are buying TES due to lower corporate (financial) debt issued at the margin, higher liquidity in the financial system on the back of TES UVR 2023 maturity that brought COP8tr to the banks, and a slower pace of expansion in consumer credit. In fact, during February offshore investors sold COP4.2tn in TES without a real hit to the market since they found demand from domestic agents.

Turning to the traditional macro equation, economic activity continued showing a decent performance, however some signals are pointing to a deceleration in the formal sector, reaffirming our hypothesis of a gradual slowdown. Core inflation remains high, but headline seems to have peaked which has helped 1-yr and 2-yr inflation expectations stabilize—albeit, above target.

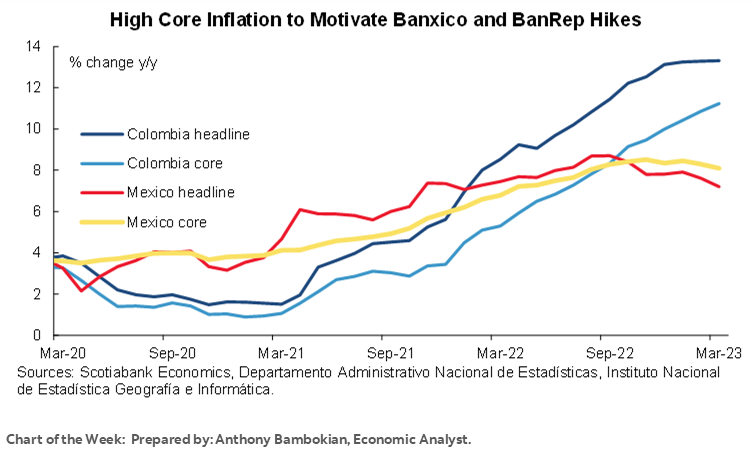

Either way, the macro backdrop regarding inflation and growth is aligned with our call of a final 25bps hike from BanRep to 13% on March 30 to ensure inflation expectations converge in the long run. We also get CPI data for March on April 5, where we expect inflation to continue hovering at the ceiling of around 13.3%. Food, gasoline, and some services prices will continue contributing to upside pressure in monthly inflation. Core inflation will accelerate further reflecting the cumulative effects of indexation but also still robust demand.

Mexico—Banxico Unlikely to Decouple from the Fed Yet

Eduardo Suárez, VP, Latin America Economics

+52.55.9179.5174 (Mexico)

esuarezm@scotiabank.com.mx

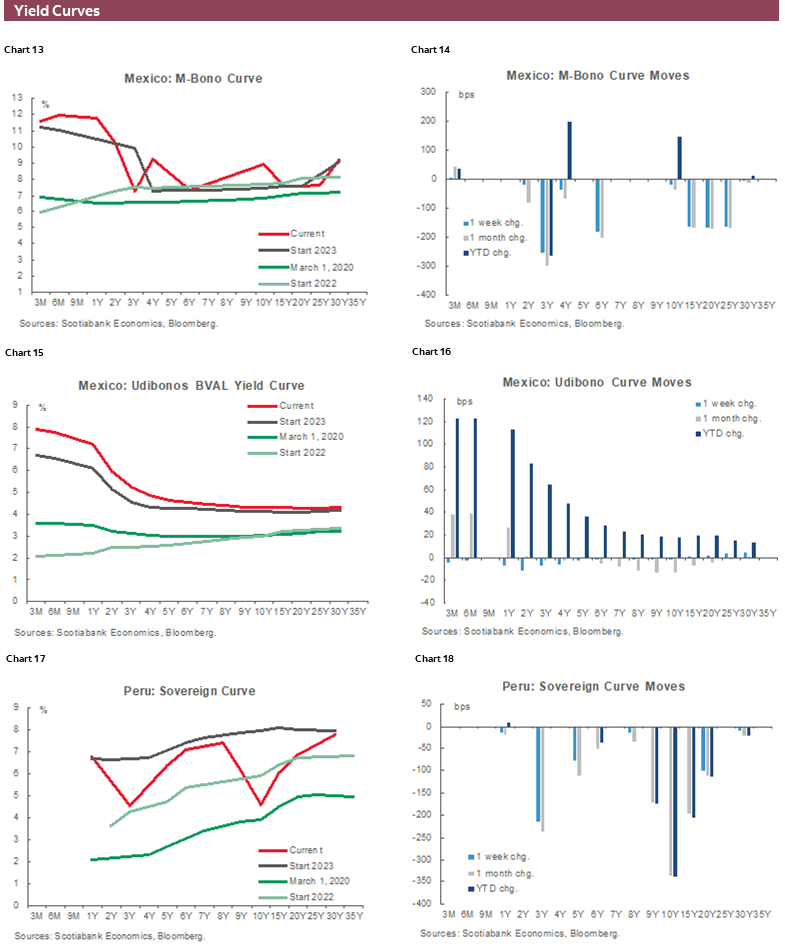

The FOMC revised its dots for 2023 and 2024 upwards in its March 22 decision, yet markets still saw the overall message as a justification to push US yields mostly lower. US OIS implied rate moves now only price about toss-up odds of an additional 25bps hike (in volatile pricing), after which they are discounting over 50bps in cuts by July. This view does not seem consistent with the Fed’s guidance and seems more like another case of “fighting the Fed”. The other big development of the week was Mexico’s CPI release. Headline inflation for the first half of March provided a positive surprise, not only dropping 0.36ppts to 7.12% y/y, but also came in 0.12ppts below consensus. However, the main concern for Banxico’s board now is core, not headline inflation—and the former has been much stickier and misbehaved. Core inflation came in right on consensus, printing at 8.15%, still over twice the top of Banxico’s target range.

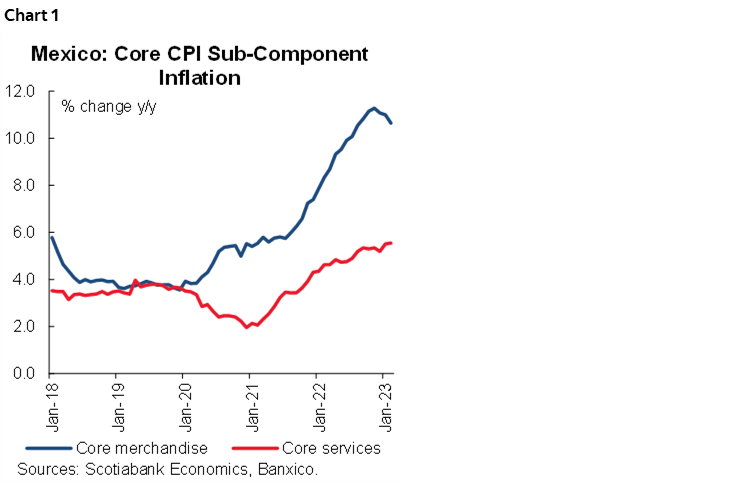

- Within core, merchandise prices had a much higher peak than services, but they started to decline around the end of 2022, as we had anticipated (chart 1). Historically, Mexican CPI highs have occurred six months after those in PPI, and secondary sector PPI inflation reached its maximum of the cycle in July 2022. Similarly, in Banxico’s price-setters survey, by the end of 2022 the majority of goods producers envisioned smaller increases or declines in their own prices. Hence, although core merchandise inflation remains extremely high (over 10%), it’s now on a clear downtrend.

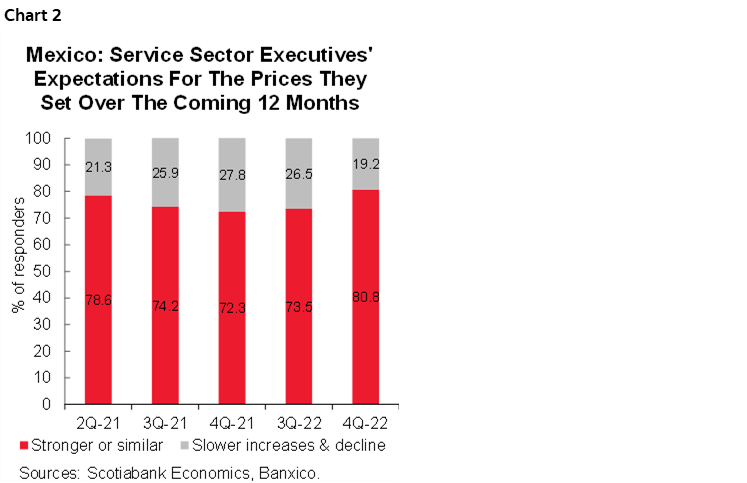

- The same positive dynamic is not yet true in core services inflation. Although the high in the tertiary sector PPI inflation was in October 2022, which would be consistent with a peak on the CPI side around March–April of 2023, the latest survey of service-sector price setters from Banxico actually saw a deterioration, with 81% of respondents anticipating to increase their prices at a similar or faster pace (chart 2). Although core services inflation remains materially lower than its merchandise counterpart (it’s still under 6%), it retains an upward trajectory. We anticipated we would see a peak in core services inflation around this time, but it so far remains elusive.

What does all this mean for Banxico? For starters, we don’t expect the board will fight the Fed—at least not yet. We expect the board to support at least one more 25bps hike on March 30 (matching the FOMC’s), with additional hikes dependent on core services inflation becoming re-anchored, as well as Fed moves. Under the current environment of global uncertainty, as well as resilient Mexican core inflation, we don’t expect Banxico to decouple from the Fed for the time being. Can Banxico deliver another 50bps hike on March 30? It’s possible, but not our base case.

There are starting to be some indications that the MXN may be slightly on the overvalued side, including a rising trade deficit (over USD30bn on a 12month rolling basis), a moderate over-valuation from a real effective exchange rate perspective, but also relative to other manufacturing economies, particularly in Asia and South America, Mexico’s currency looks even stronger. However, the drivers of a strong MXN that we wrote about a couple of weeks ago remain in place. Without the inflationary pressures Mexico is currently going through, we would have anticipated Banxico to stop rolling its FX swaps, to then follow up with a process of reserve accumulation—potentially by resorting to the options mechanism. However, we don’t expect Banxico to take actions on MXN, at least until inflationary pressures abate.

Peru—Under the Weather

Guillermo Arbe, Head Economist, Peru

+51.1.211.6052 (Peru)

guillermo.arbe@scotiabank.com.pe

March may be the month in which inflation in Peru finally breaks to the downside. The key price indicators that we follow are pointing to monthly inflation of just over 1% for March. Given that monthly inflation was 1.5% in March 2022, and we see a 1.0% m/m increase in March 2023, this difference in base effects (if it holds up in prices for the remainder of the month) would imply a drop in yearly inflation for March to 8.1%, from 8.7% in February. Let’s hope so.

More important than base effects, which will be strongest in March and April, the short-term reasons that have been buoying inflation since December, namely the impact of protests/roadblocks and severe weather events on perishable products, and the impact of the bird flu on poultry prices, are starting to dissipate. Protests may recur but are pretty much over and done with for the time being. The severe weather season is not quite over, but we are near the end. That would only leave the bird flu, which appears to be a bit more persistent.

With short-term inflationary events weakening, yearly inflation in April should ease even more, falling (finally!) below the 8.0% threshold that has held it up since June 2022. Market expectations are saying the same thing. Inflation expectations twelve-months out fell from 4.6% in February to 4.3% in March. This provides the BCRP with some relief, although it may only really feel comfortable once headline inflation begins to decline in earnest.

We still believe that inflation will correct very slowly this year, and maintain our forecast of 5.0% inflation for full-year 2023. Global concern regarding failing banks has changed the mood regarding monetary policy in Peru as well. It is not clear how responsive the BCRP will be to this environment, and until we get further guidance from the BCRP we are maintaining our reference rate forecasts at the current rate of 7.75% until October, then two 25bps rate cuts in November and December.

We are starting to take a closer look at 2024. The newly emerging risk to look out for is the possibility of an El Niño event. The local weather authorities are beginning to alert to this, while at the same time stressing that it is too early to be able to determine its magnitude. El Niño tends to have a material impact, albeit temporary, on inflation. As a result, we are raising our 2024 inflation forecast to 3.5% to take into consideration a moderate El Niño in 2024. We are not changing our reference rate forecasts, and continue to expect the reference rate to decline from 7.25% at the beginning of 2024, to 5.75% by year-end.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Click here to be redirected |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.