- Last week, Mexico’s government presented its 2026 Economic Package that covers economic and fiscal policy guidelines, as well as proposed revenue and spending plans.

- The forecasts for key economic variables in the 2026 Economic Package are more optimistic than current estimates from private-sector analysts for both 2025 and 2026, posing a significant risk that the Finance Ministry misses its projections.

- The government predicts a 5.7% increase in tax revenues compared to the 2025 estimate, on greater collection efficiency and an expansion of the tax base (including a jump in import tariff revenues). The package also estimates a nominal increase in oil revenues of 20.3% in 2026, banking on a significant rise in PEMEX output.

- The proposed net government spending for 2026 amounts to MXN 10,114.8 billion pesos, representing a 5.9% increase compared to the estimated amount for 2025. The package pencils in investment of MXN 536.8 billion pesos allocated to 13 priority projects, equivalent to 5.3% of total spending, with ~60% of this in energy projects (PEMEX included) and the bulk of the remainder in transportation infrastructure projects.

Budget Approval Dynamics

On Monday, September 8th, the Secretary of Finance, Edgar Amador, submitted the 2026 Economic Package to the Chamber of Deputies. The package consists of the following documents:

1. General Criteria of Economic Policy

2. Federal Revenue Law Initiative

3. Proposed Federal Expenditure Budget

After the documents are submitted, the Chamber of Deputies must discuss and approve the Revenue Law no later than October 20th, and the Senate must ratify it by October 31st. Meanwhile, the Chamber of Deputies must approve the Expenditure Budget no later than November 15th.

The details of each document are presented below:

1. General Economic and Fiscal Policy Guidelines (CGPE):

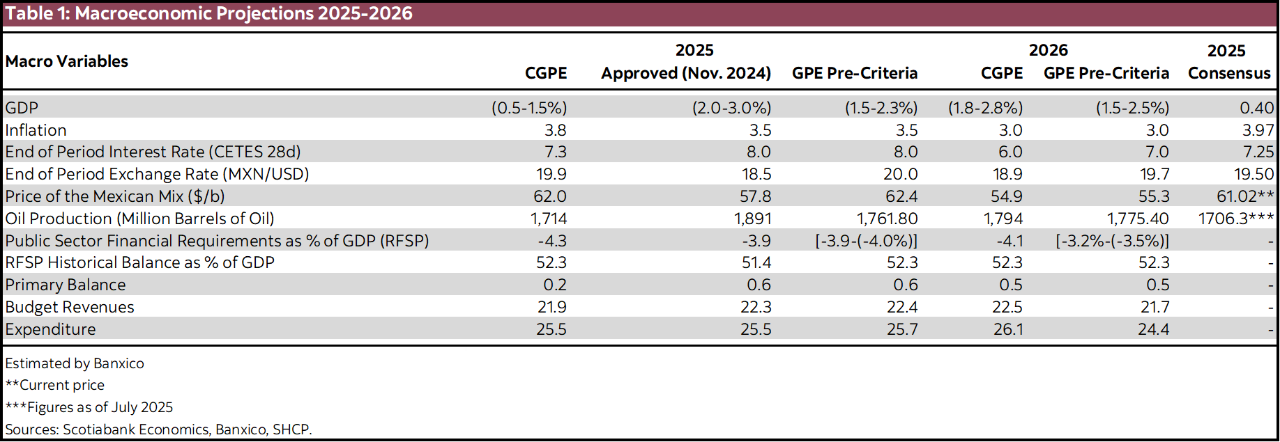

It presents the economic and fiscal policy guidelines for 2026 (click here1 to view the document), whose macroeconomic projections serve as the basis for estimating government revenues and expenditures. Notably, these projections are more optimistic than market consensus. Table 1 provides a summary of the main variables.

The forecasts for key economic variables in the 2026 Economic Package are more optimistic than current estimates from private-sector analysts for both 2025 and 2026, posing a significant risk of underperformance. For GDP in 2025, the projected range of 0.5%–1.5% exceeds the current consensus forecast of 0.4%. Achieving the midpoint (1.0%) would require growth above 1.5% in the second half of 2025, which appears unlikely given persistent downside risks such as weak investment amid domestic and global uncertainty, deficient infrastructure, security concerns, and labour market fragility. For 2026, the Finance Ministry’s (SHCP) forecast also exceeds historical averages and projections from private analysts, which currently stand at 1.4% (i.e., about 1ppt below the SHCP’s forecast midpoint).

Inflation and interest rate projections also carry upward risks. The SHCP estimates year-end inflation at 3.8% for 2025 and 3.0% for 2026, compared to the 4.0% and 3.7% consensus. Analysts have noted upside risks, including persistent core inflation and potential rebounds in non-core components like agricultural prices. New taxes and tariffs in 2026 could further pressure prices, widening the gap between SHCP and market expectations.

Interest rate forecasts of 7.25% for 2025 and 6.0% for 2026 are below the consensus estimates of 7.50% and 6.50%, respectively, and may also be subject to upward revisions.

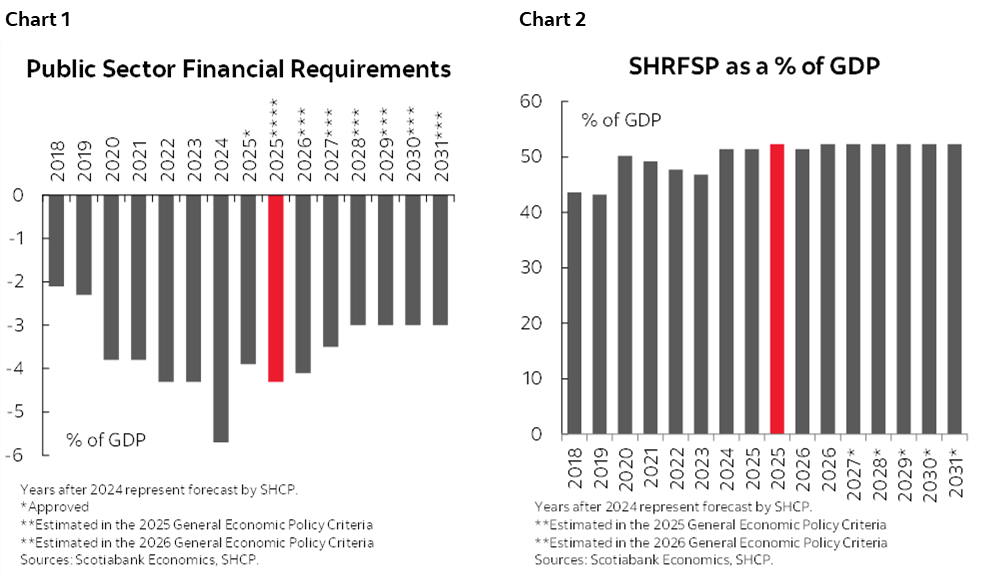

On public debt, while efforts to reduce the Public Sector Borrowing Requirements (RFSP) are noted, fiscal consolidation appears delayed. The 2025 RFSP deficit is projected at 4.3% of GDP (chart 1)—lower than 2024’s 5.7% but higher than the 3.9% approved by Congress and the 4.0% estimated in April’s Pre-Criteria. For 2026, the deficit is expected at 4.1%, nearly one percentage point above previous estimates. The Historical Balance of RFSP (SHRFSP), the broadest measure of public debt, is projected at 52.3% of GDP for 2025, up from the previously approved 51.4%, and is expected to remain at that level through 2031 (chart 2).

2. Federal Revenue Law Initiative (ILIF)

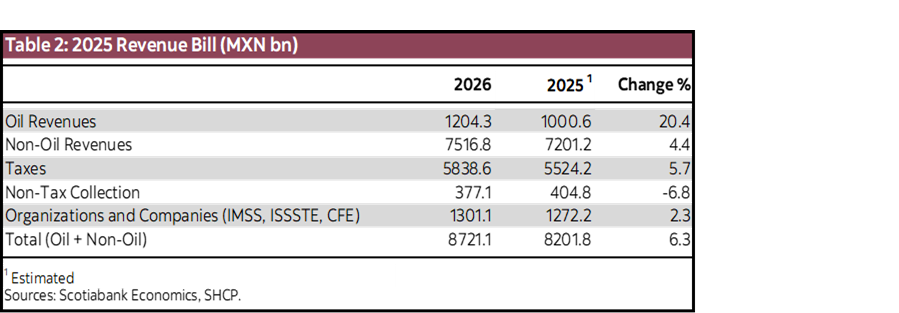

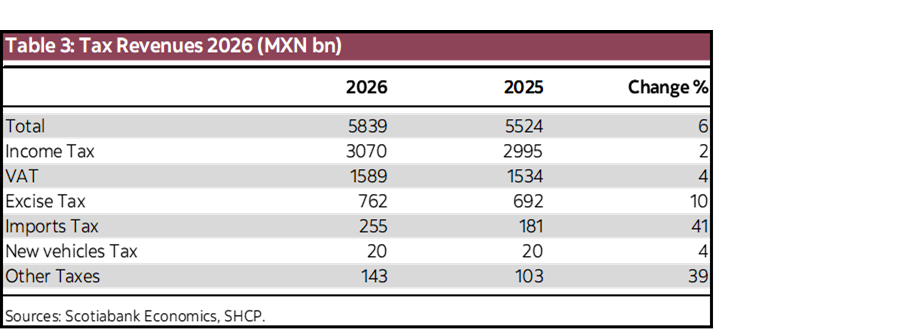

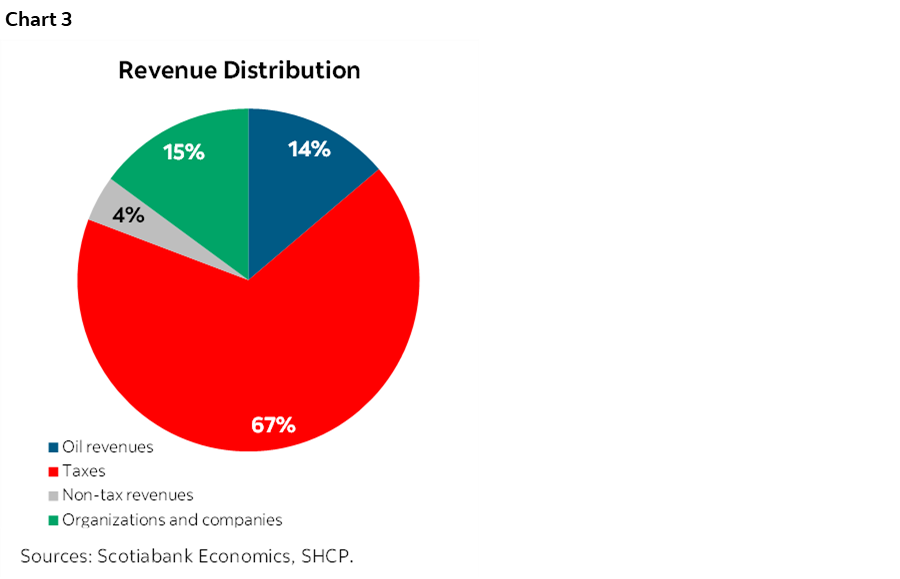

It presents the expected government revenues for 2026 (click here1 to view the document). According to the document, total budgetary revenues are estimated at 8,721 billion pesos (bn MXN), of which 1,204 bn MXN correspond to oil revenues and 5,839 bn MXN to tax revenues (tables 2 and 3, and chart 3). This implies a projected 5.7% increase in tax revenues compared to the 2025 estimate, driven mainly by the government’s efforts to improve collection efficiency and expand the tax base.

In this context, the 2026 Revenue Law initiative estimates a nominal increase in oil revenues of 20.3% compared to 2025 forecasts, based on expectations of an 80.1 thousand barrels per day increase in oil production. This projection appears highly optimistic, given the limited capacity of Pemex and the Federal Government to invest in improving operations (extraction and production).

Regarding tax revenues, nominal growth of 5.7% is anticipated compared to the 2025 estimate (table 3 again). This increase is mainly attributed to:

- A 40.7% increase in the import revenues component, resulting from the rise in the General Import Tax. Under the Plan México, the government aims to impose tariffs on more than 1,400 products to consolidate a sovereign economic model that promotes productive development and competitiveness in strategic sectors. This tax could lead to inflationary pressures.

- Additionally, the government plans to increase IEPS (Special Tax on Production and Services) revenues by 10% through measures aimed at reducing the consumption of goods and products that have adverse health effects. These measures include:

- An increase of $3.0818 per litre for flavoured beverages.

- For manufactured tobacco products, the tax rate is proposed to rise from 160% to 200%, and for handmade tobacco, the rate would increase to 32%.

- A special 8% tax is proposed on digital video game services that contain violent content.

- The tax on gambling is proposed to increase from 30% to 50% on the total amount wagered.

- The government also aims to increase VAT and income tax (ISR) revenues by 3.6% and 2.5%, respectively, through measures such as:

- Disallowing the deductibility of three-fourths of the fees paid to IPAB by multiple banking institutions.

- Standardizing the deduction treatment for credit institutions, eliminating the special regime established in Article 27 of the Income Tax Law (LISR).

- Introducing a unified withholding rate for digital intermediation platforms: 2.5% for individuals under the simplified RESICO regime, 4.0% for legal entities with a tax ID (RFC), and 20.0% for those who do not provide one.

- Applying VAT withholding rates of 8% for entities with an RFC and 16% for those without or located abroad.

- Requiring crowdfunding institutions (FinTech) to withhold and remit both ISR and VAT on transactions where they act as intermediaries.

However, the package also includes measures that could have adverse effects on tax revenue, notably:

- Tax exemptions related to the FIFA World Cup 2026, which would relieve individuals and entities involved in organizing, developing, and executing activities related to the event from tax and administrative burdens—potentially reducing public revenues.

- Changes in the securities lending market, where provisional interest withholding would be applied to the premium paid to the lender rather than the original capital amount, potentially lowering effective tax collection.

- Facilitation of foreign investment in private equity, by easing tax requirements to grant transparency benefits to foreign legal entities managing private equity funds in Mexico—raising concerns about aggressive tax planning if not properly regulated.

- Capital repatriation, offering tax benefits to individuals and entities returning lawful funds to Mexico, provided the funds remained abroad until September 8th, 2025. The applicable income tax rate would be 15%, with no deductions allowed, and conditioned on investing the funds in productive activities for at least three years. While this measure aims to encourage investment, it also implies a lower tax burden compared to the regular regime (table 3 again).

Finally, the 2026 Revenue Law estimates non-tax revenues from fees, duties, and products at 377.1 billion pesos, representing a nominal decrease of 6.8% compared to the projected year-end figure. This decline is mainly due to the exclusion of extraordinary revenues recorded in 2025, particularly non-recurring duties. Meanwhile, revenues from agencies and state-owned enterprises other than Pemex are projected to grow by 2.3% in nominal terms compared to the estimated 2025 year-end, in line with the GDP growth forecast for 2026.

3. Federal Expenditure Budget Proposal (PPEF)

It presents the expected government expenditures for 2026 (click here1 to view the document).

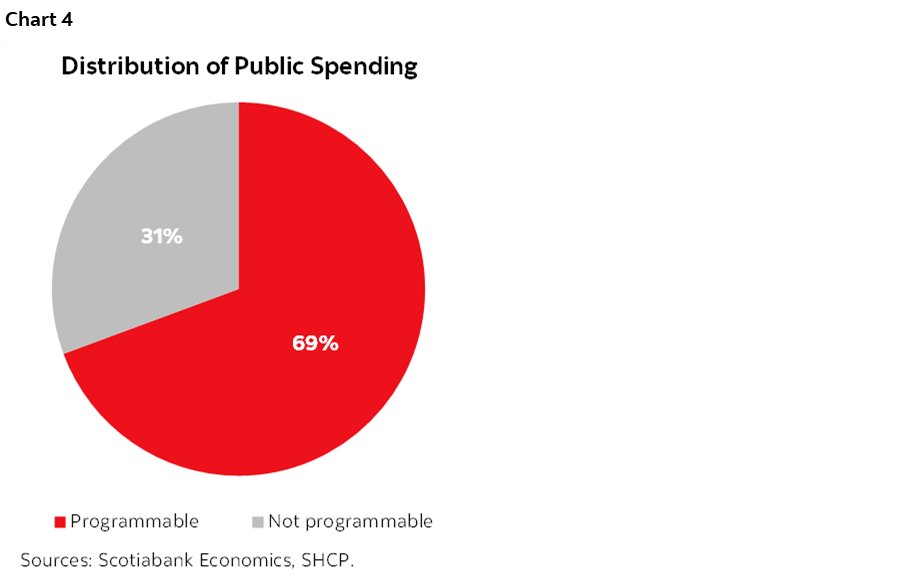

The proposed net government spending for 2026 amounts to 10,114.8 billion pesos, representing a 5.9% increase compared to the estimated amount for 2025. Of this total, 69% is classified as programmable spending and the remaining 31% as non-programmable (chart 4).

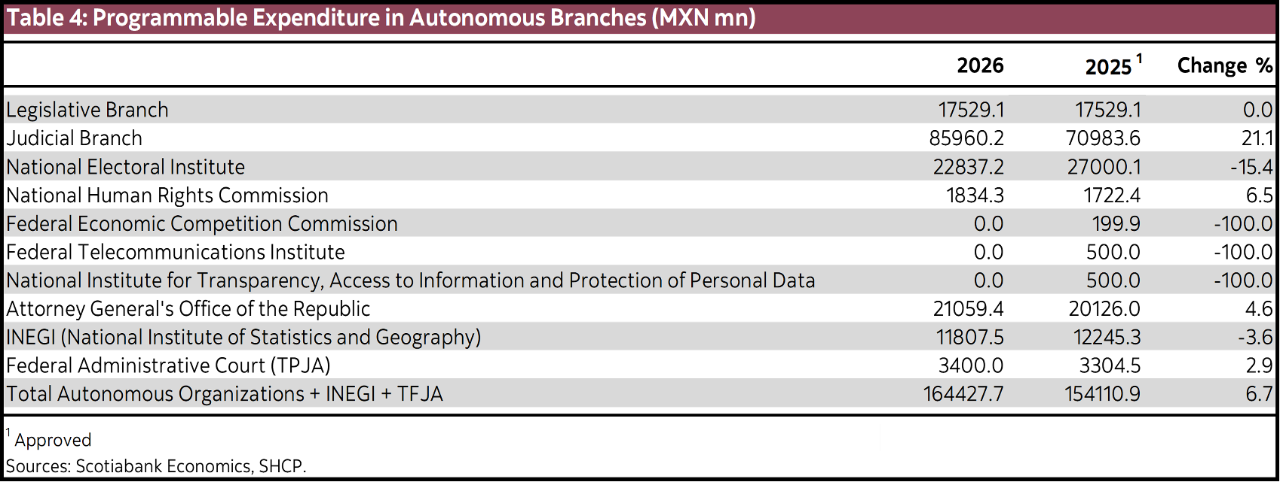

Regarding the reallocation of spending in autonomous branches, as shown in table 4, the structure of the public sector was modified following the dissolution of seven autonomous bodies in December 2024, which impacted budget allocations. In 2025, additional changes were approved, including the elimination of the National Institute for Transparency, Access to Information and Personal Data Protection (INAI) and the creation of a new decentralized body, Transparency for the People, under the Secretariat for Anti-Corruption and Good Governance. Key variations include a 15.4% cut to the budget of the National Electoral Institute (INE), which now stands at 22.837 billion pesos, in line with reduced electoral activity expected in 2026; a 21.1% increase for the Judiciary, with a budget of 85.960 billion pesos; and a 3.6% reduction for the National Institute of Statistics and Geography (INEGI), which will receive 11.807 billion pesos, marking its second consecutive budget cut.

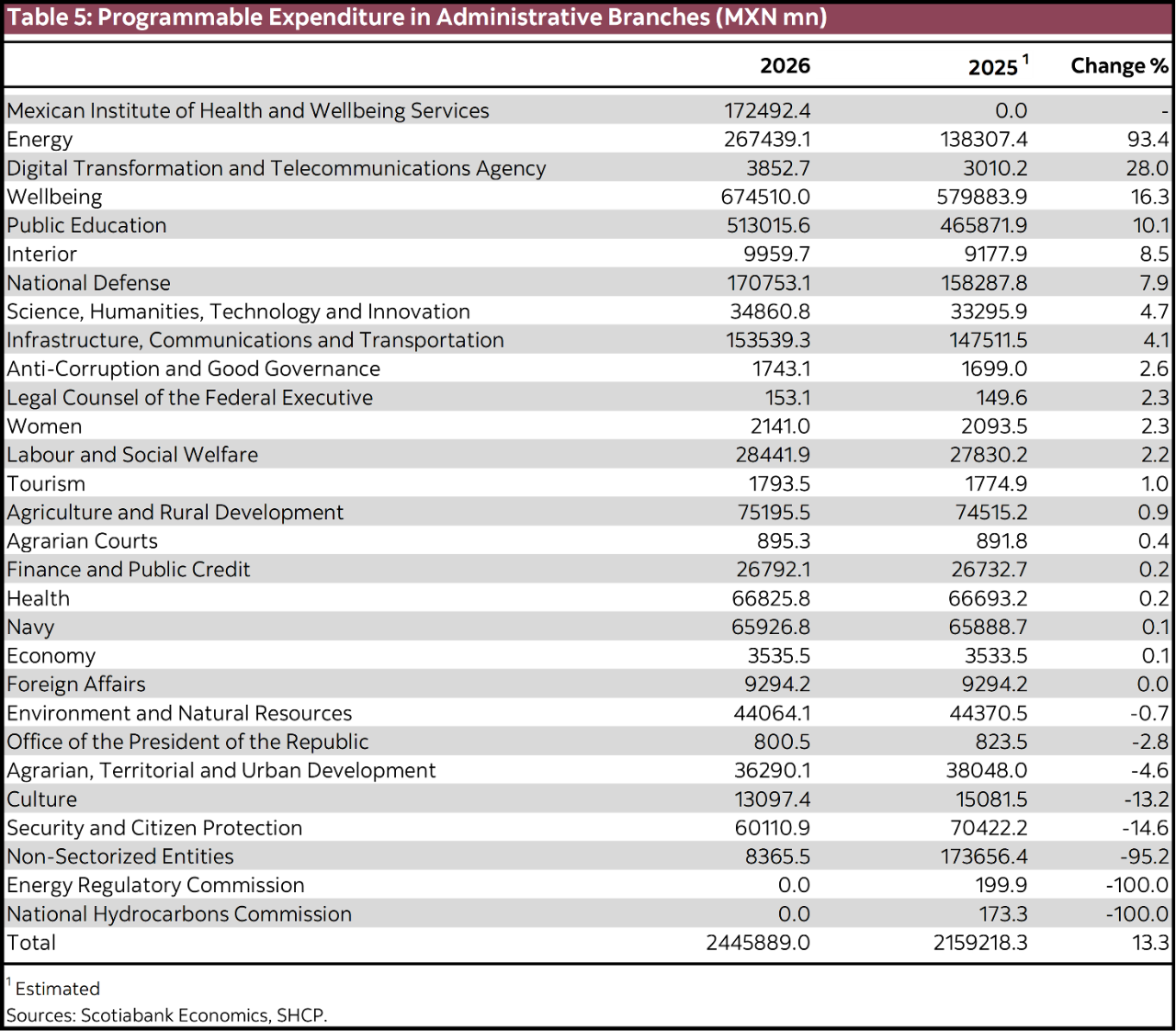

The 2026 Federal Expenditure Budget Proposal (PPEF) allocates 2.45 trillion pesos to 29 administrative branches, representing a 13.28% increase compared to 2025 (table 5). Of these, 18 branches show increases, 8 show reductions, and 3 remain virtually unchanged. Notable increases include the Secretariat of Energy, due to capital transfers to Pemex and the absorption of functions from the Energy Regulatory Commission (CRE) and the National Hydrocarbons Commission (CNH); the Digital Transformation and Telecommunications Agency; and the Secretariat of Wellbeing, driven by administrative adjustments and fiscal commitments. In contrast, the Secretariat of Infrastructure, Communications and Transportation grows only 4.09%, maintaining a low share of GDP. The most significant cuts are observed in the Secretariat of Security and Citizen Protection, the Secretariat of Culture, and the Secretariat of Agrarian, Territorial and Urban Development.

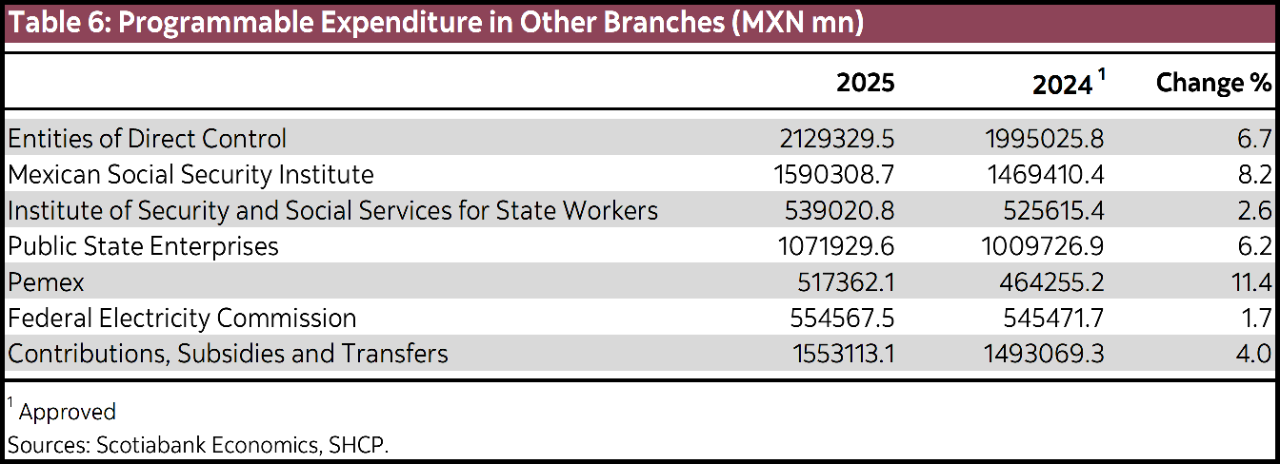

Regarding programmable spending in other branches, a 6.73% increase is observed in the budget allocated to directly controlled entities such as IMSS and ISSSTE (table 6). However, the total health sector budget—equivalent to 2.6% of GDP—remains well below the minimum standard recommended by the WHO, which is at least 6%. Despite efforts to strengthen functional and infrastructure-related spending, structural challenges persist, including timely supply of medical inputs, hiring and training of personnel, and coordination between federal and state governments. On the other hand, Pemex is expected to receive an 11.44% increase in spending, although much of these resources will be used to service financial obligations, limiting its operational investment capacity and raising doubts about the viability of the 2025–2035 Strategic Plan, which aims to increase production to 1.8 million barrels per day. In the case of CFE, the projected budget increases by only 1.7%, which appears insufficient to meet the goals of the 2025–2030 National Electric System Strengthening Plan.

Additionally, the 2026 Economic Package anticipates that the government’s physical investment will remain at a modest 2.4% of GDP, with a projected reduction to 2.3% in the following years. This level of public investment is limited given the infrastructure challenges the country faces and may not align with the objectives of the Mexico Plan, which aims to raise total investment (public and private) to 26% of GDP in the short term and up to 28% in the medium term. The gap between projected public investment and the plan’s targets suggests that a more favourable environment for private investment will be essential, as well as a reassessment of budgetary priorities if the goal is to move toward sustained and competitive growth.

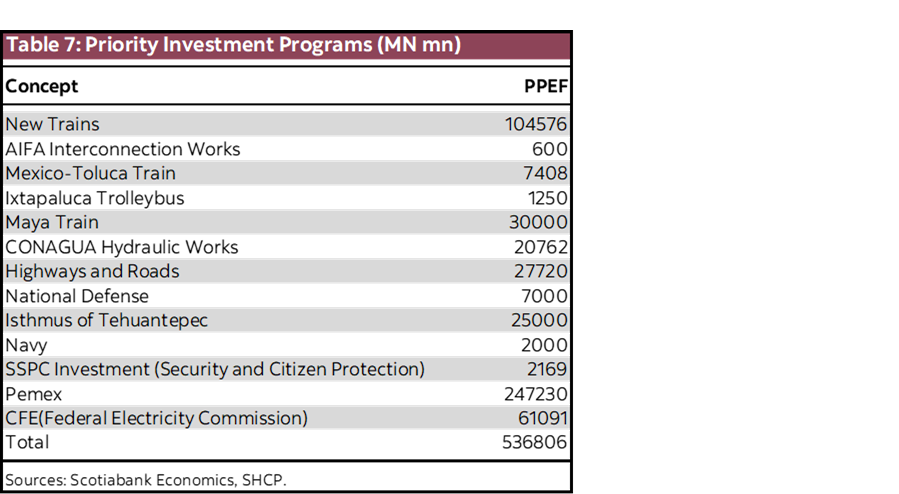

The 2026 Economic Package includes an investment of 536.8 billion pesos allocated to 13 priority projects, equivalent to 5.3% of total spending (table 7). In addition to energy projects (327.6 billion pesos), the “New Trains” initiative stands out with 104.6 billion pesos assigned, covering routes such as Mexico City–Querétaro, AIFA–Pachuca, and Saltillo–Nuevo Laredo, among others. Resources are also allocated to the Maya Train (30 billion pesos), the Mexico–Toluca Interurban Train (7.4 billion pesos), and the AIFA–Lechería connection (600 million pesos). While these projects generate employment and demand for inputs, they do not necessarily enhance the country’s capacity to attract investment. In this context, the challenge of fiscal consolidation requires boosting freight logistics infrastructure and ensuring access to energy and water. However, investment in hydrocarbons, electricity, and water infrastructure (20.7 billion pesos, similar to the previous year) remains insufficient to meet the country’s structural needs.

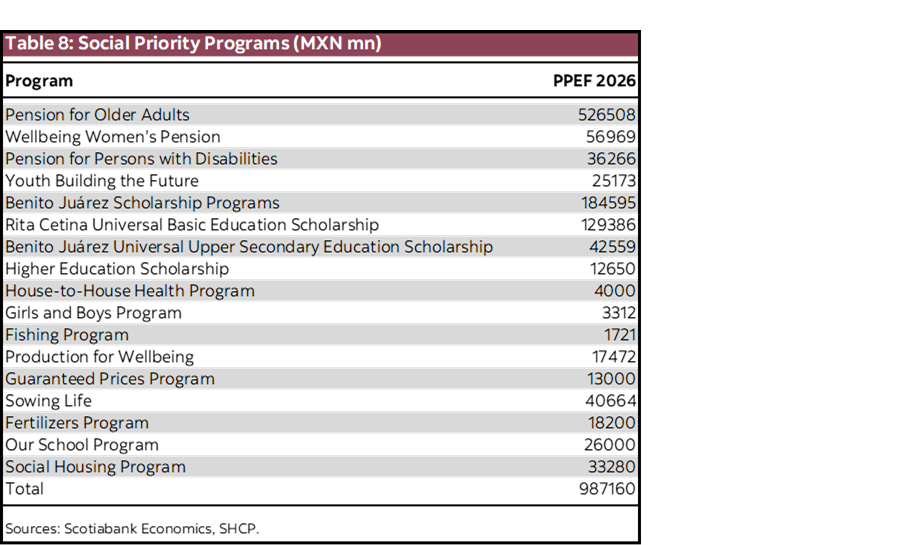

Meanwhile, the 16 priority social programs account for nearly 10% of total spending, with none facing budget cuts (table 8). The expansion of the “Wellbeing Women’s Pension” stands out, as it now includes women aged 60 to 64. Also notable are the “House-to-House Health” program, which has incorporated new home care protocols, and the “Rita Cetina Scholarship,” which has expanded its coverage. On the other hand, the “Wellbeing High Schools and Universities” program is no longer considered a priority program for 2026.

In summary, the 2026 Economic Package raises some concerns regarding its macroeconomic assumptions, as well as the consequences of significant spending cuts in key sectors. It seems unlikely that the Public Sector Borrowing Requirements will close the year with a deficit of 4.1% of GDP, given a slowdown in consumption, lower remittances, and reduced investment, all of which will likely result in lower growth than projected by the Ministry of Finance. This, in turn, will negatively impact the debt-to-GDP ratio, putting pressure on its sustainability, which could be reflected in a downgrade of the sovereign credit rating, thereby increasing borrowing costs. In this context, it will be crucial to closely monitor the evolution of the economic program and pay attention to potential revisions in the 2027 General Economic Policy Pre-Criteria, scheduled for release in April 2026.

1 Referenced on pages 1, 2, 4: Some readers may encounter issues in accessing the Finance Ministry’s documents. Unfortunately, as of writing, there are no other publicly accessible sources for these documents.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.