- Residents shift from net buyers to net sellers of USD, led by firms and mutual funds

The relevant multilateral nominal appreciation of the Chilean peso (CLP), stronger since last September's plebiscite, can be understood as an adjustment of expectations that does not necessarily have to coincide with a relevant flow of US dollar sales in the spot/forward market. The change in expectations can move the demand for US dollars without an aggressive shift in flows. In this Latam Insights, we try to see which spot flows—broken down by agent type—have accompanied this change in expectations.

The adjustment in expectations could be explained by lower political uncertainty and/or a lower probability of aggressive structural reforms. The outcome regarding the makeup of the new constitutional council would also support arguments in favour of political moderation, although for several political analysts it raises the need for agreements to achieve the approval of the constitutional draft on December 17. On the whole, what seems quite clear is that, despite the announcement of a reduction of FX forward sales by the Central Bank (BCCh), the null sale of US dollars in the spot market by the Treasury during May, and declines in copper prices, the CLP has continued to show strength in relation to comparable currencies (not exempt from high volatility).

We have analyzed the dollar purchase and sale flows in the spot FX market for various resident and non-resident agents. It is worth noting that in the derivatives/non-deliverable forward (NDF) area, we had relevant movements by non-residents, but not coincident with the appreciation of the CLP (chart 1). Indeed, foreigners reduced their positions in favour of CLP by nearly USD 4 bn from the beginning of the year to the second half of May, while the currency has appreciated against the US dollar and in multilateral terms by 7.5% in the same period.

Analysis of US dollar buying and selling flows in the spot FX market helps to understand the CLP's resilience in a context of an unwind in NDF positions by non-residents and copper price declines from year-ago levels. We detected:

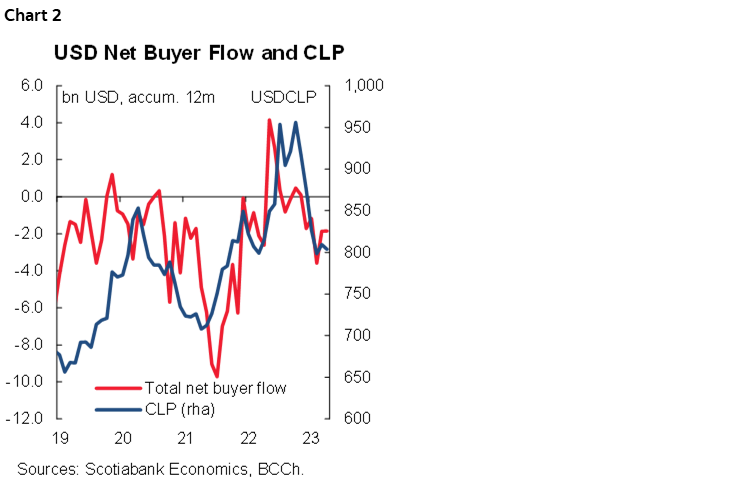

- As expected, net purchases flows in the FX spot market co-move significantly with the exchange rate (chart 2).

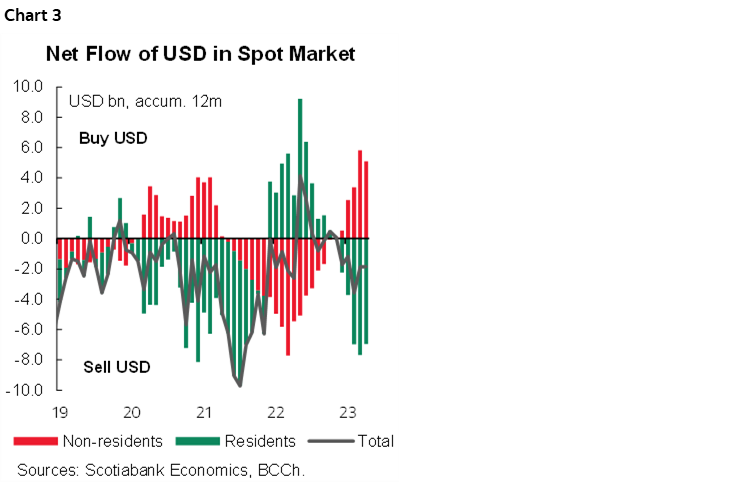

- Before the third withdrawal of pension funds—in May 2021—residents were net sellers of USD (appreciation pressure on the CLP), with net sales at their highest level in the first half of 2021. After the third withdrawal, residents shifted sharply to net buyers of USD, a situation that continues until the third quarter of 2022 (chart 3).

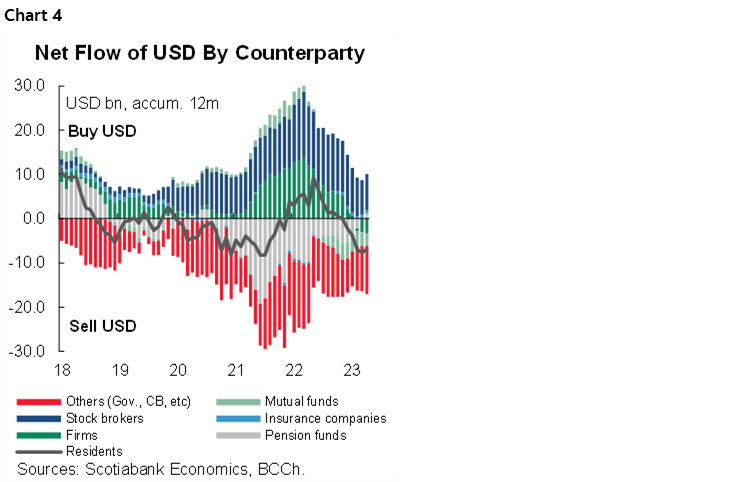

- However, not all residents were net buyers after the third pension fund withdrawal (chart 4). In particular, firms and stock brokers—as tasked by clients—were net buyers. In contrast, pension funds (PFs) were net sellers of US dollars in the FX spot market due to the repatriation of capital required to pay for PF withdrawals.

- In line with this, and as expected given the announcements of USD sales by the Treasury, the government has shown relatively persistent USD sales flows in the last two years.

- In a marked and, for now, persistent manner throughout 2023, residents have shifted from USD buyers to net sellers since Q4-22, coinciding with CLP resilience (chart 3 again). Analysis at counterparty level would show that USD selling by residents observed since late-2022 is led by mutual funds and firms (chart 4 again). Mutual fund sales are likely due to the adjustment of their clients' portfolios towards CLP and Unidad de Fomento denominated funds, while for companies, it would be as part of the unwind of usual hedges, dividend distributions, among others.

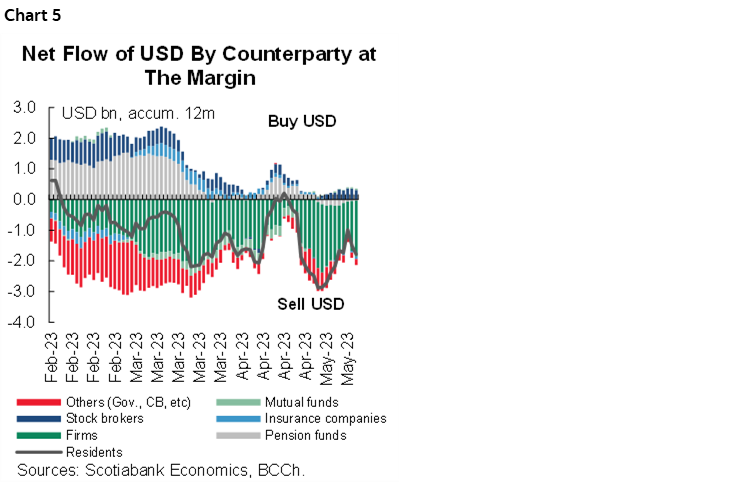

- For their part, stock brokers—by client requests—have been net buyers since social unrest picked up, which has eased during the early months of 2023 and especially during May (chart 4 again and chart 5). Spot USD buying by stock brokers could be symptomatic of a more structural monetary denomination adjustment process in the wealth of high net worth residents, since, although USD buying has declined, it has not been reversed—at the margin. In other words, they are still buying USD, but at a significantly slower pace. We continue to see no flow of sales by stock brokers, which would be a symptom of asset repatriation by individuals.

- In the first two months of 2023, Pension Funds (PF) started to buy US dollars in the spot market, contrary to firms, mutual funds and the government (chart 5 again). However, since the end of March, these agents have been less active in the FX spot market, probably explained by the higher volatility of foreign assets, which has led to a lower appetite of the PF contributors towards risk funds more exposed to foreign currencies.

- In a clear and relevant way, companies in the real sector started USD sales in the spot market at the end of 2022 that have since continued (firms, in chart 5 again), and stand as one of the factors that have supported the CLP's resilience.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.