- Short-term gains and long-term risks in Colombia’s fiscal strategy without the rule

On Friday, June 13th, the Ministry of Finance (MoF) released the Medium-Term Fiscal Framework (MTFF), Colombia’s most important fiscal policy publication. It provides the most precise insights into the Government’s thinking about the country’s economic outlook in the long run, as well as current fiscal results. In fact, it gives a general perspective on the most important factors influencing the main fiscal goals and their sustainability over a ten-year framework.

Fiscal uncertainty has been one of the key factors behind Colombia’s underperformance relative to its credit rating peers. Thus, the release of the 2025 Medium-Term Fiscal Framework (MTFF) was highly anticipated, amid MoF’s announcements of greater transparency.

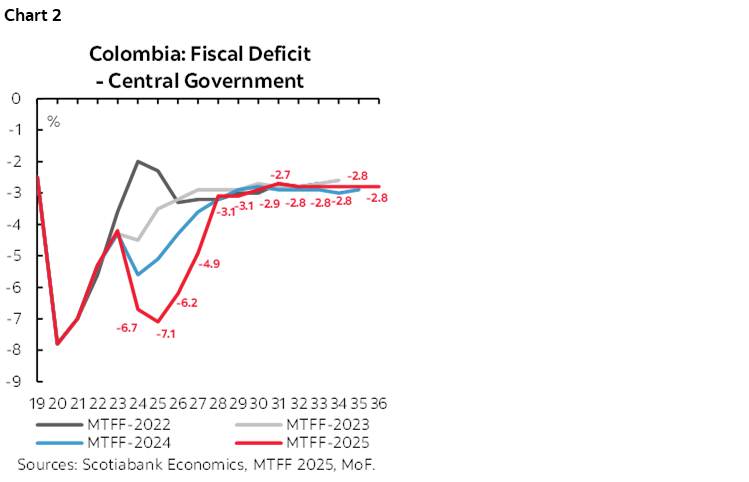

The accounts clean-up meant the suspension of the fiscal rule for up to three years. During this period, the fiscal deficit is expected to remain elevated: the 2025 deficit was revised from 5.1% to 7.1% of GDP—within our projected range (see here)—while the 2026 projection is 6.2% of GDP, above the 4.3% projected last year (chart 1). The path back to compliance with the fiscal rule is expected to include a set of reforms on both the revenue and expenditure sides, as well as the creation of a liquidity reserve starting July 2025.

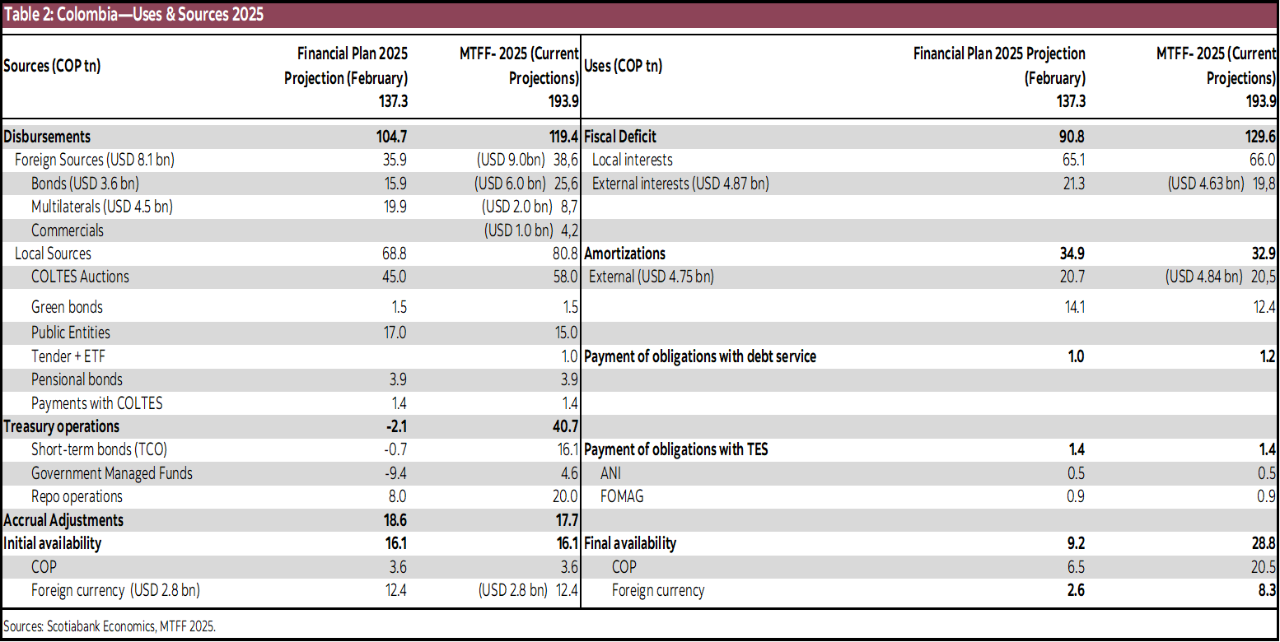

In terms of financing, the 2025 MTFF revealed a significant increase in funding needs, with a clear emphasis on reducing borrowing costs rather than mitigating refinancing risks. For 2025, additional financing needs are projected at COP 56 tn, covered through an increase in local issuance by COP 12 tn, and treasury operations (short-term debt, managed funds, and repos) by COP 43 tn. For 2026, government intends to maintain this strategy, with local issuance up to COP 60 tn (COP +1 tn green bonds), and treasury operations up to COP 13 tn. On the external front, the government aims to diversify its financing sources by increasing exposure to non-dollar currencies and credit lines with offshore banks. In our view, the proposed financing strategy helps to reduce short-term servicing costs by easing pressure on primary bond auctions—where we have anticipated at least an additional COP 20 tn. However, this approach increases refinancing risk.

MACRO ASSUMPTIONS

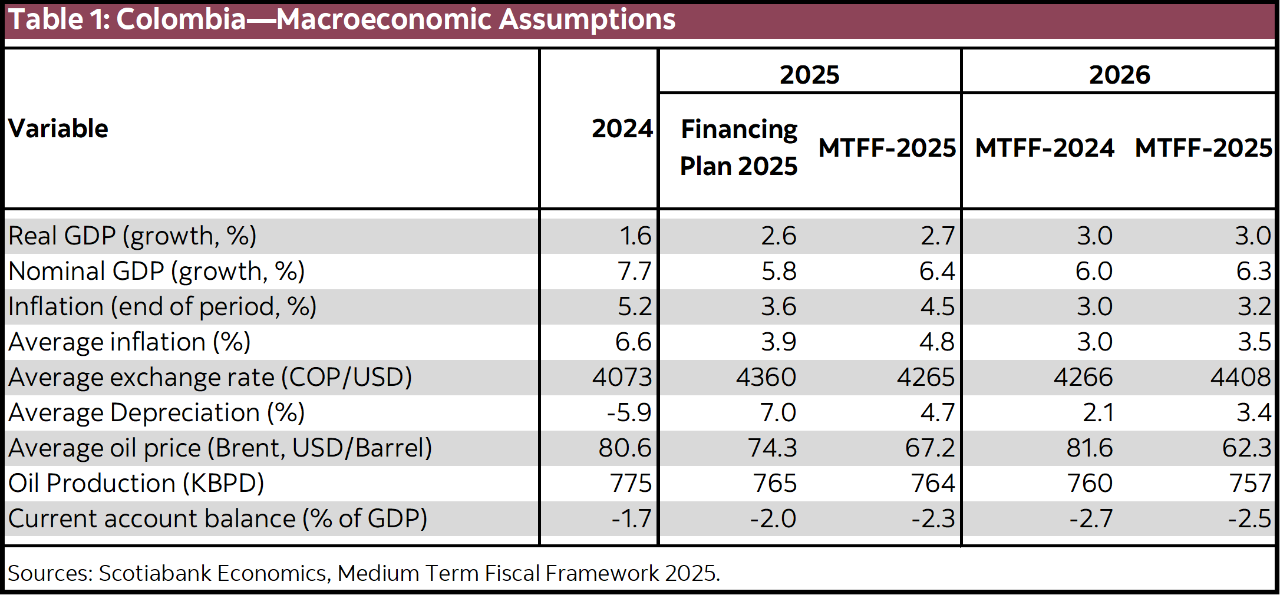

Overall, the macroeconomic assumptions appear reasonable. For 2025, the GDP forecast was revised upward, in line with economic growth of 2.7% y/y in Q1-2025. However, the MoF projects 3% growth in 2026 and the next few years, which may be optimistic given lags in investment and the probability that BanRep will maintain contractionary real interest rates. Also, the inflation projection for 2026 assumes a return to BanRep’s target range, which, in our view, seems unlikely. That said, the remaining variables are broadly in line with market consensus (table 1).

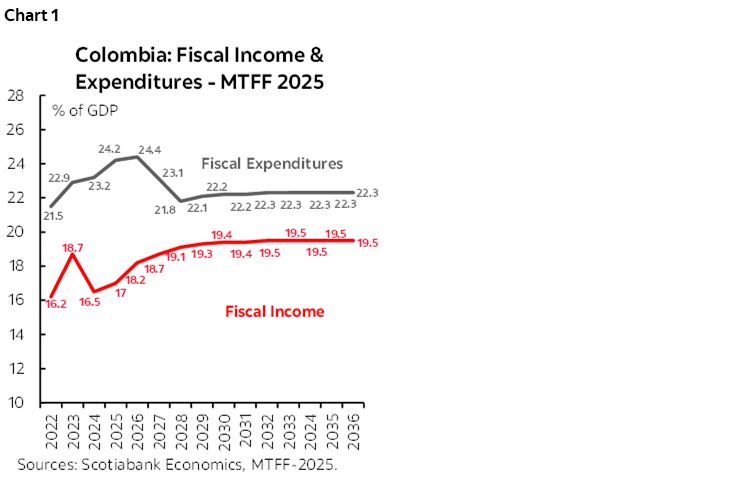

FISCAL INCOME AND SPENDING

The MoF overestimation of tax revenues has led to significant budget adjustments. Compared to the 2025 Financial Plan released in February, projected fiscal revenues were revised down from COP 327.9 tn to COP 309.27 tn—a reduction of COP 18 tn (~1.0% of GDP). Much of this update was due to the adjustment in tax revenues expected, and a decrease of management efforts that will not be offset even by the resources projected by the self-retention decree, which is expected to collect COP 7.2 tn during the second half of the year. Despite this, total expenditures increased from COP 418.7 tn to COP 438.89 tn, reflecting a COP 20 tn rise (~1.1% of GDP). This increase stems mainly from higher primary spending and the backlog execution which would have already paid 65% (~COP 41 tn) of the total. Currently, the MoF is deferring COP 12 tn in investment projects related to infrastructure and defense. However, this has not been officially recognized as a budget cut, even though the revenue shortfall exceeds the deferral amount.

The MoF justifies this stance by highlighting the inflexibility of 87% of public spending. Under the current scenario, the government plans to increase revenue through tax reform and an adjustment in inflexible spending, including an increase in diesel prices to offset the increase in the Fuel Price Stabilization Fund (FEPC) deficit, of which COP 7.2 tn was paid in 2025 (through increased debt issuance) and which is expected to pay 0.2% of GDP (~COP 3.8 tn) in 2026.

In our view, given the limited short-term prospects for increasing tax revenues, the currently planned deferral for 2025 should be formalized as a permanent cut by the year-end. However, the suspension of the fiscal rule (which we discuss later), provides the government with greater flexibility, as its fiscal strategy is no longer constrained by the rule’s deficit and debt targets. In fact, one of the key strategies announced involved prioritizing non-discretionary spending in 2025, while deferring discretionary commitments into a growing budgetary backlog. This approach would allow the government to postpone certain payments and shift them into the next year, thereby easing near-term financing pressures.

FISCAL DEFICIT

The projected fiscal deficit for 2025 was revised up from 5.1%, published in the 2025 Financial Plan, to 7.1% of GDP (chart 2). This is the largest fiscal deficit since comparable data has been available (1994), excluding the pandemic. Much of the deterioration is explained by the 0.8 ppts of GDP increase in primary spending, which pushed the primary deficit from 0.2% of GDP (as projected in the 2025 Financial Plan) to 2.4% of GDP. This scenario represents a 2.1 ppts (~ COP 39 tn) deviation from the fiscal deficit allowed by the fiscal rule (5.0% of GDP). For 2026, the deficit estimate rose from 4.3% of GDP (according to the 2024 MTFF) to 6.2% of GDP. This increase is due to higher primary spending (+0.2% of GDP), which widened the projected primary deficit to 1.4% of GDP. Notably, much of the anticipated fiscal adjustment between 2025 and 2026, relies on an expected COP 41 tn (2.1% of GDP) increase in revenues, which will depend on the approval of a tax reform later this year.

TEMPORARY SUSPENSION OF FISCAL RULE

The government confirmed the activation of an escape clause allowing for the suspension of the fiscal rule. This mechanism can be triggered with a prior (non-binding) opinion from the Autonomous Committee of the Fiscal Rule (CARF) and formal approval by CONFIS, Colombia’s highest fiscal policy authority. Once activated, it permits suspension of the rule for up to three consecutive years. This clause was previously used during the pandemic, suspending the rule from 2020 to 2021, followed by a transition period from 2022 to 2025. The current activation is justified by the government’s claim that 87% of public spending is inflexible, posing a risk to macroeconomic stability. For now, the government has outlined a return path to fiscal rule: i) In 2025, a tax reform is expected to be introduced aiming to raise COP 19 tn (1.1% of GDP) in which an increase in VAT is not ruled out, alongside a proposed “Fiscal Pact” to initiate structural reforms to public spending, ii) In 2026, the tax reform would take effect and the spending reform would be presented, and iii) by 2027, an adjustment is expected, allowing the government to return to compliance with the fiscal rule by 2028.

For now, the CARF announced an unfavourable opinion on the activation of the escape clause (see here). The report highlights that the spending inflexibility alone does not constitute sufficient justification for invoking the clause. Moreover, it warns that the measures approved by CONFIS are inadequate to ensure medium-term debt sustainability. In our view—and consistent with CARF’s position—the law lacks clear criteria for determining non-compliance with the fiscal rule on an ex ante basis. This legal ambiguity could delay the necessary fiscal adjustment that, under such circumstances, should be implemented without hesitation to preserve macroeconomic stability.

DEBT BURDEN AND THE NEW DEBT STRATEGY

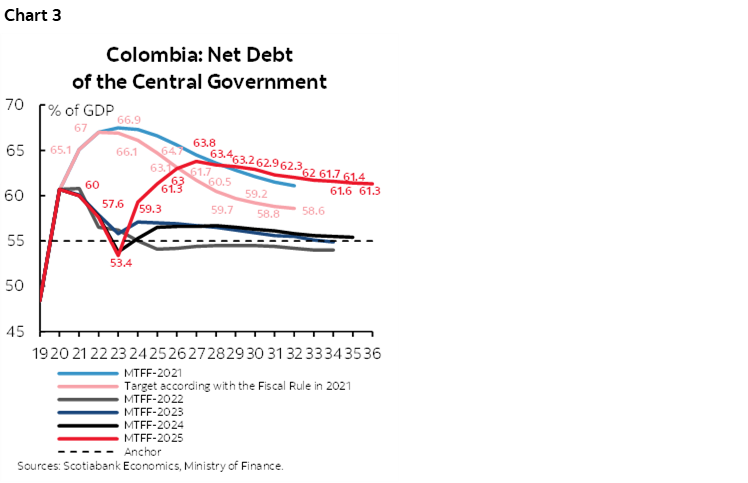

The MoF now projects a significant increase in the central government’s net debt compared to expectations from a year ago. For 2025, the estimate stands at 61.3% of GDP—up from 60.6% in the 2025 Financial Plan—and interest payments are 4.8% of GDP. Furthermore, debt is projected to exceed 63% of GDP by 2029 (chart 3). This trajectory is primarily driven by domestic debt growing faster than nominal GDP, as elevated financing needs persist due to rigid public expenditures. The revised financing strategy seeks to mitigate the adverse implications of this imbalance. What is particularly concerning is that, with the fiscal rule suspended, the government faces no binding constraints on public debt levels between 2025 and 2027. As a result, debt could continue rising, potentially approaching the 70% of GDP ceiling established under the fiscal rule, even in the absence of a clearly defined path toward fiscal consolidation.

The expected debt levels may not be in line with Colombia’s current credit rating. Credit rating agencies have often warned that the country is moving toward an unsustainable level of debt. With this new fiscal scenario, we cannot rule out the possibility of a downgrade in the near future. Unlike other countries in the region, the Colombian government does not seem to be prioritizing a plan to improve its public finances, which could worry investors.

FINANCING

In the absence of proposals to expedite a fiscal consolidation process, the government would be looking for strategies to mitigate exposure to risks resulting from increased financing needs. In this regard, the following is highlighted:

- By 2025, the government’s financing needs would increase by COP 56 tn (3% of GDP) compared to the estimate in the 2025 Financial Plan (table 2). Local debt sources will rise by COP 12 tn. Specifically: i) COP 13 tn will be raised through COLTES, supported by higher auction volumes in both COP and UVR bonds, and ii) COP 2 tn will no longer be issued to public entities, to avoid additional pressure on interest rates.

- One of the main changes in the strategy is the use of an additional COP 42.7 tn in treasury operations, which includes: i) Short-term debt (TCO) worth COP 16.8 tn, ii) COP 14 tn from government-managed funds (such as FONPET and the General Royalty System, and others), where the government compensates the fund managers, and iii) Repo operations involving Total Return Swaps (TRS) with offshore banks, conducted on an unhedged basis—as Treasury Head explained—using COLTES as collateral.

- Regarding repo operations, they estimate a cost of 7.95% in COP terms, and plan to use these funds to buy back TES in the secondary market, for a total of COP 20 tn. These purchases are expected to create a COP 20 tn liquidity buffer. We believe this setup could lead to a significant flattening of the yield curve between the long end and the belly. On the one hand, the COP 20 tn from TRS operations will likely go to buy long-term bonds, which could lower yields at the long end. On the other hand, the new COLTES issuance will focus on the belly, increasing supply there and keeping upward pressure on yields.

- From external sources, the government is considering issuing an additional USD 2.4 bn in global bonds, with the goal of diversifying the currencies in its funding mix. In addition, part of the external financing—about USD 1.0 bn—will shift from multilateral organizations to offshore banks. In our opinion, a higher external debt burden increases the exposure of the budget to exchange rate changes and increases the volatility in fiscal projections.

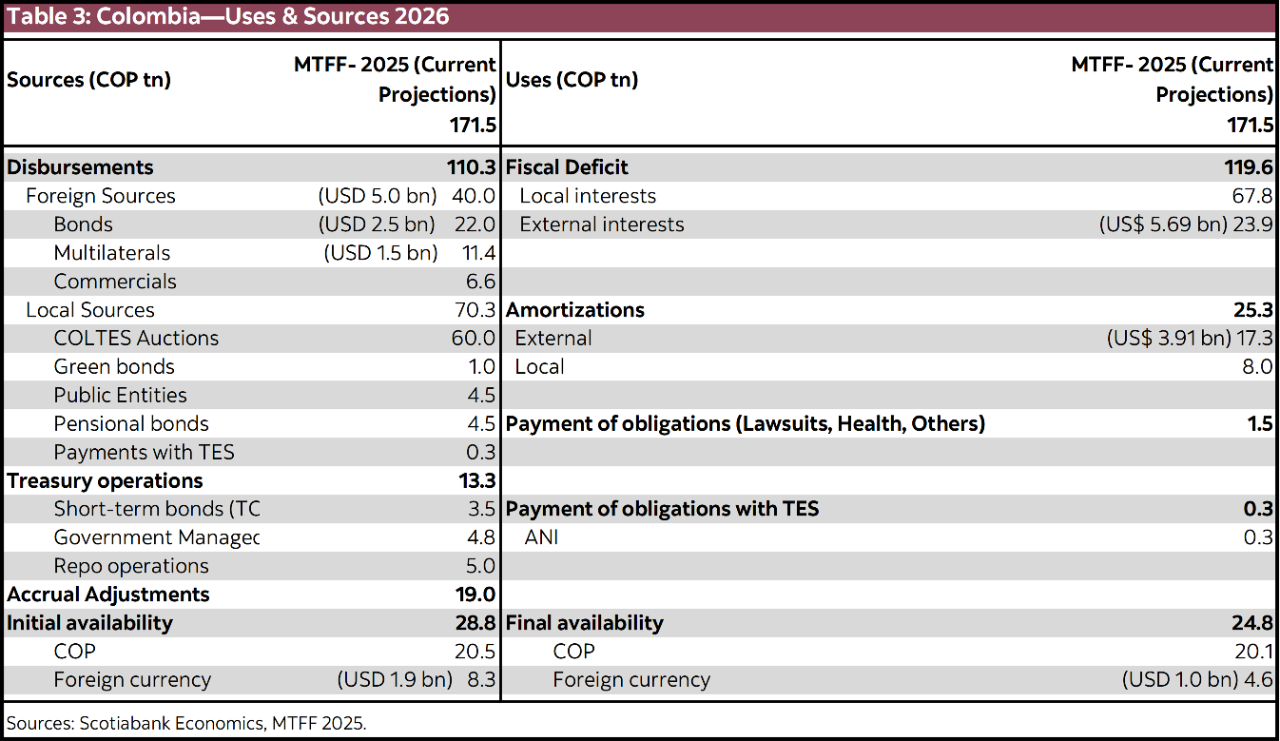

- For 2026, the total deficit to be financed is expected to reach COP 119.6 tn (table 3). Of this, local sources would provide COP 70.3 tn, including COP 60.0 tn in COLTES issuance. According to Cuellar, local debt management operations will help reduce amortizations to around COP 8 tn, easing some of the pressure on bond issuance in 2026—though financing needs will remain high. On the external side, the government plans to reduce global bond issuance and increase borrowing from offshore banks, aiming to secure guarantees—possibly from multilateral institutions—to lower borrowing costs. However, the suspension of the fiscal rule may increase uncertainty and make it harder for Colombia to access international markets under favourable conditions.

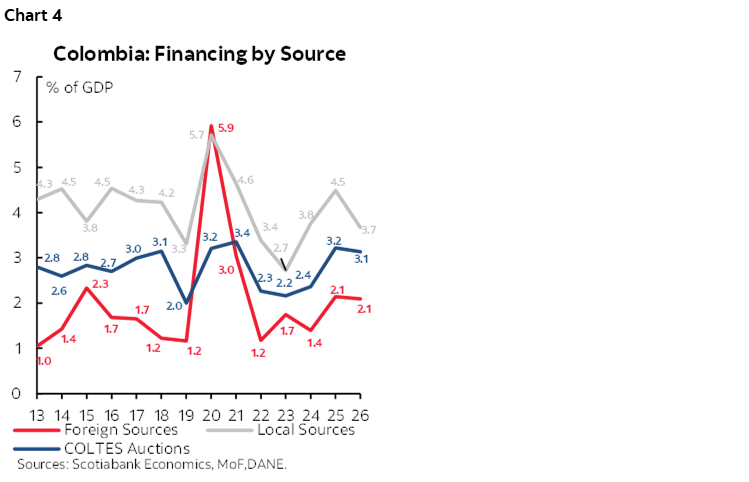

- In our view, COLTES issuance will remain at a manageable level as a percentage of GDP (chart 4). However, the government’s focus on reducing borrowing costs by increasing short-term debt may bring short-term benefits, but it also increases refinancing risk. This risk would likely fall on the next administration—at a time when uncertainty around the upcoming elections could further complicate the outlook.

- The MoF plans to continue its current debt management strategy in coordination with the Market Maker scheme. According to Cuellar, this will involve one liability management operation per month for both the COP and UVR bond curves, with amounts similar to recent operations—around COP 3 tn for the COP curve.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.