KEY TAKEAWAYS

- Mexico’s economic growth remains constrained by weak investment, as well as deteriorating economic expectations and broader challenges.

- Exports remain the main driver of the Mexican economy, alongside still somewhat resilient consumption. Despite the noise generated by the USMCA renegotiation, Mexico remains the United States’ main trading partner.

- The USMCA remains a structural advantage for Mexico, although negotiations are entering a new stage as the U.S. midterm elections approach.

- Public finances remain under pressure as weaker revenues, rising spending inertia, particularly in pensions, and Pemex’s financing needs continue to limit fiscal space and increase sovereign risk concerns. Weak growth is a key headwind for public finances.

- Monetary policy is likely to remain cautious as headline inflation has eased, but persistent core and services inflation, upside risks, and a narrower Mexico–U.S. rate differential argue for an extended pause by Banxico.

DOMESTIC SECTOR: WEAKNESS PERSISTS

The Mexican economy ended 2025 stronger than analysts had expected, with annual growth of 0.5% and a particularly resilient final quarter, when it expanded 1.6% year over year. However, this momentum did not carry over into the beginning of 2026. The latest figures continue to point to structural weakness across several areas of the economy, both from the standpoint of economic activity and aggregate demand, particularly consumption and investment.

During the first quarter of the year, GDP performed below expectations. It posted annual growth of just 0.2% and a quarterly decline of -0.6%, with unfavourable movements across its main components. Agricultural activities grew only marginally (0.4% year over year), industrial activities deepened their contraction (-1.2% year over year), and services expanded at a moderate pace (1.0% year over year). In addition, all three major sectors recorded negative quarterly variations.

Consistent with these results, economic activity has shown signs of stagnation for much of the year. The Global Indicator of Economic Activity (IGAE) posted annual changes of -0.3% in January and February before growing to 1.4% in March. A slight improvement followed in April, when the indicator reached growth of 2.3%, its highest reading in the past year.

At the sector level, performance has been mixed. Primary activities grew by an average of 1.43% year over year during the first four months of the year, showing some resilience despite weather-related factors affecting the agricultural sector. Industry, meanwhile, recorded an average contraction of -1.21% year over year between January and March, although it rebounded 2.3% in April, driven mainly by growth in construction (10.6%) and mining (3.2%), partially offset by stagnant manufacturing (0.0%) and a slight decline in utilities (-0.4%). Finally, services have also shown some resilience, with average growth of 1.29% so far this year. While these signals suggest a moderate recovery compared with 2025, more structural improvements will be needed to sustain stronger economic momentum for the remainder of the year and over the medium term.

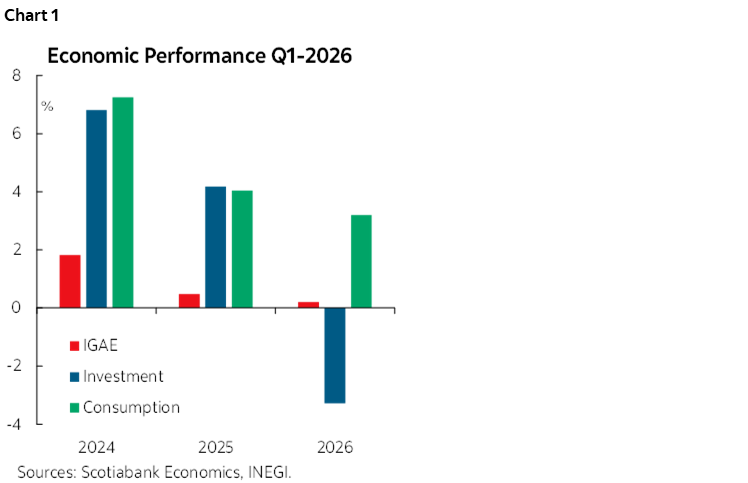

On the aggregate demand side, the performance during the first quarter of 2026 also reflected an economy that continues to face significant challenges. Although private consumption remained the main driver of economic activity (49.5% of GDP; +3.2% year over year, chart 1), signs of fragility persist, linked to the deterioration of the labour market and purchasing power, as reflected in the mixed signals observed in recent months. The external sector also continued to contribute to growth, with exports of goods and services equivalent to 27.5% of GDP; while they declined slightly during the quarter (-0.5%), they grew by nearly 18% year over year. Public spending (7.8% of GDP; +3.4%) also contributed positively to economic activity, albeit in a limited way.

However, investment remains the main area of weakness. Its share fell to 15.2% of GDP, returning to levels last seen in 2021 and recording an annual contraction of -3.3%. The weakness was broad-based, with declines in both construction (-8.5% in March) and machinery and equipment (-1.5%), accumulating 19 months of stagnation or declines. Monthly indicators confirm this trend: during the first quarter of 2026, gross fixed investment accumulated a -3.3% decline compared with the same period last year, with persistent decreases in machinery and equipment (-6.8%), particularly in the domestic component, reflecting private-sector caution amid a highly uncertain environment. That said, the April figure showed a rebound, growing by 5.9%, its strongest increase in two years. Therefore, it will be important to continue assessing the investment outlook in the coming months to determine whether this rebound marks the beginning of a more sustained recovery or reflects transitory factors.

This slowdown has also been reflected in revisions to Mexico’s growth outlook by international organizations, authorities, and market participants. Domestically, the Ministry of Finance lowered its expectation from 3.0% in March to a central estimate of 2.3% —within a range of 1.8% to 2.8%—while Banxico adjusted its forecast from 1.6% to 1.1%, and analyst surveys from both Citi and Banxico also point to a gradual deterioration in expectations. The IMF maintains a growth forecast of 1.6% and the World Bank of 1.3%, while the OECD cut its estimate from 1.3% to 0.8%.

At Scotiabank, we have maintained a more cautious view for several months, with growth below 1%. During 2025, our forecast for 2026 stood at 0.6% and currently stands at 0.7%; although the favourable performance at the end of 2025 temporarily led to an upward revision to 1.0%, the weakness observed in first-quarter GDP prompted a new adjustment.

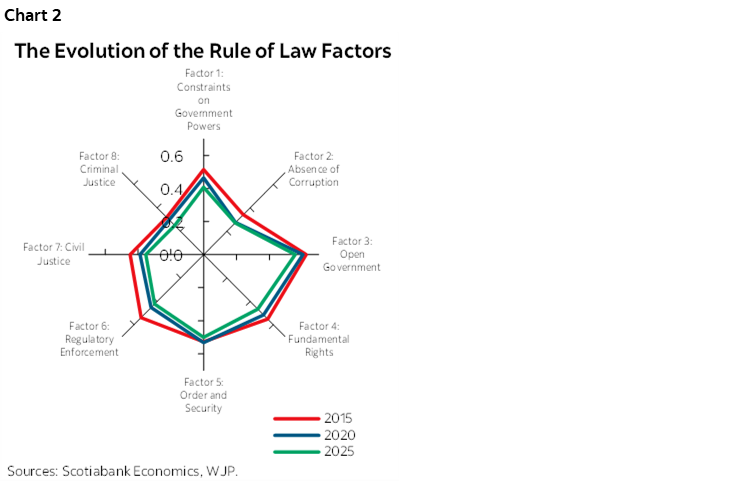

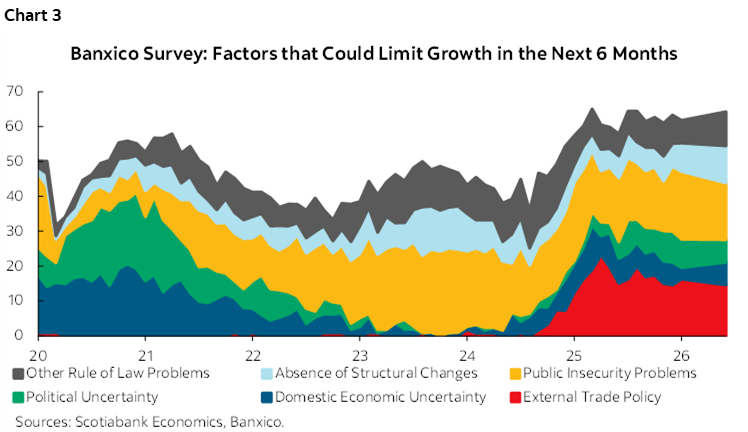

In this context, it is worth highlighting that Mexico continues to have important advantages for attracting foreign investment, including its integration with the United States through the USMCA, its strategic location, and a relatively solid productive base. However, international evidence shows that factors such as the rule of law, institutional quality, judicial independence, regulatory certainty, and contract enforcement are increasingly decisive in investment decisions. Several international indices—including the World Justice Project (WJP), the Democracy Index, the Legatum Prosperity Index, and Infrascope—suggest that Mexico has experienced a sustained deterioration in several of these dimensions over the past decade (chart 2), particularly in constraints on government powers, control of corruption, regulatory enforcement, and the functioning of the justice system. Moreover, in Banxico’s Survey of Private-Sector Economic Specialists’ Expectations, 41% of analysts identify governance as one of the main factors that could hinder growth over the next six months, a share that has remained close to 40% since October of last year (chart 3).

Although Mexico remains an attractive investment destination and continues to hold a relevant position in global foreign direct investment rankings, these institutional weaknesses have increased investors’ perception of risk. While this does not imply an automatic reduction in investment flows, it does alter their characteristics: projects tend to be more cautious, with shorter planning horizons and lower transformative potential for the economy. As a result, strengthening regulatory effectiveness, judicial independence, accountability, and legal certainty will be essential for the country to translate its competitive advantages into stronger, more sustained, and more inclusive growth in the coming years.

EXTERNAL SECTOR: THE STRENGTH OF THE MEXICAN ECONOMY

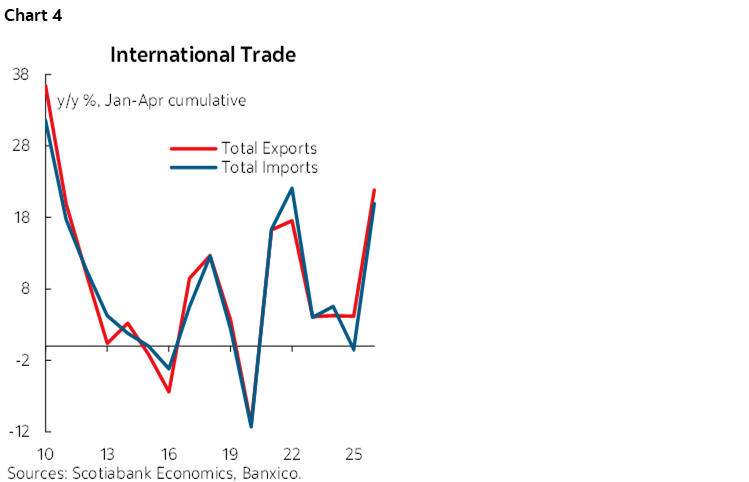

The external sector has consolidated its position as one of the main drivers of the Mexican economy amid a slowdown in domestic demand. This performance has been supported both by the recovery of U.S. consumption and by the deepening of regional value chains. Between January–April 2025 and the same period in 2026, Mexico’s total exports increased from USD 203.2 billion to USD 247.6 billion, representing growth of 21.8% (chart 4).

This momentum was concentrated in non-oil exports, particularly manufacturing exports, which expanded by 23.3% year over year, confirming that the country’s external competitiveness continues to rest on a strong industrial base that is closely integrated with the U.S. economy. Meanwhile, imports grew by 19.9%, driven primarily by intermediate goods, reflecting greater demand for manufacturing inputs and intensified activity within regional supply chains. As a result, Mexico’s trade balance shifted from a deficit of USD 313.7 million during the first four months of 2025 to a surplus of USD 3.5 billion in the same period of 2026, indicating that export growth has outpaced import growth.

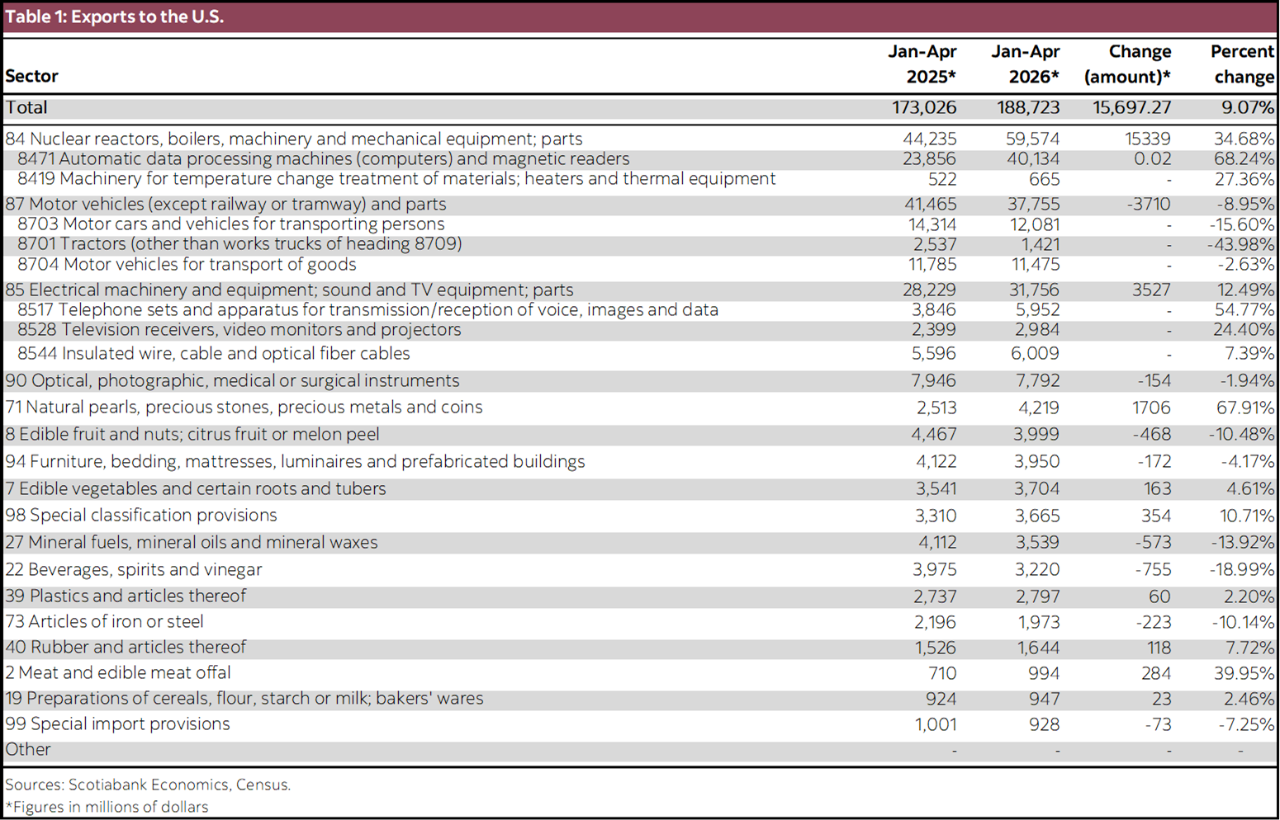

The strengthening of Mexico’s foreign trade is closely tied to the resilience of U.S. demand. According to data from the U.S. Census Bureau, imports of goods from Mexico increased from USD 173 billion between January and April 2025 to USD 188.7 billion during the same period of 2026, equivalent to annual growth of 9.1%. This increase was driven primarily by high value-added manufacturing sectors such as machinery, electrical equipment, and the automotive industry—activities that account for a significant share of the productive integration between the two countries. The evidence suggests that the export momentum is not driven solely by stronger demand for final goods—potentially brought forward amid uncertainty surrounding the upcoming USMCA review—but also by the expansion of intra-industry trade flows that characterize North American value chains.

Within this, machinery and mechanical equipment have emerged as one of the most dynamic segments of Mexican exports to the United States (table 1). U.S. imports of products classified under Chapter 84 increased by 34.7% year over year between January–April 2025 and the same period in 2026, driven by data-processing equipment, specialized industrial machinery, refrigeration systems, and components used in manufacturing processes. Particularly noteworthy was the increase in purchases of computers and data-processing equipment, whose imports nearly doubled during the period under review. This trend reflects both the strengthening of regional supply chains linked to advanced manufacturing and technology and Mexico’s growing role as a production platform for global companies serving the U.S. market.

The electrical and electronics sector also maintained solid performance. U.S. imports of Chapter 85 products from Mexico rose 12.5% year over year, supported by telecommunications equipment, cables, transformers, electrical panels, and a variety of electronic components. This momentum confirms the increasing specialization of Mexican manufacturing in activities linked to digitalization, automation, and the electrification of the economy—trends that are becoming increasingly important globally. It also reflects Mexico’s expanding participation in supply chains associated with information technology, data centres, and energy infrastructure.

The automotive industry remains one of the pillars of economic integration between Mexico and the United States. However, U.S. imports of vehicles, auto parts, and other land transportation equipment from Mexico declined by 9.0% during the first four months of 2026 compared with the same period a year earlier. Despite this moderation, the overall balance of the sector remains favourable, particularly in segments such as commercial vehicles and auto parts, which maintain strong links to regional production chains. The strategic importance of this industry lies in its high degree of integration, as numerous components cross the border multiple times before being incorporated into the final product.

The strength of bilateral trade has enabled Mexico to consolidate its position as the United States’ leading trading partner. Since 2023, Mexico has surpassed China as the largest source of U.S. goods imports, benefiting from structural factors such as the advantages provided by the USMCA, geographic proximity, and the need to diversify global supply chains away from Asia. Between 2018 and 2026, China’s share of U.S. imports fell from 23% to 7.3%, while Mexico’s increased from 13% to 17%, reflecting a significant reconfiguration of international trade and a strengthening of North America’s regional production model.

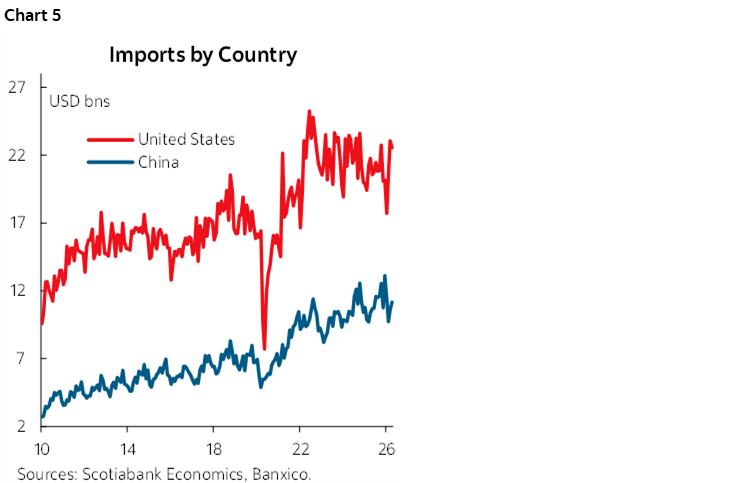

Mexico’s growing share of U.S. imports has also had implications for the country’s own trade structure. While exports to the United States have increased at an extraordinary pace, imports from China have grown more moderately. In 2024, Mexico imported USD 129.5 billion worth of goods from China, rising to USD 133.3 billion in 2025, equivalent to annual growth of 2.9% (chart 5). During the January–April period of 2026, imports from China reached USD 42.9 billion, increasing by approximately 5.2% year over year—a rate lower than that recorded by Mexican exports to the United States. Nonetheless, China has consolidated its position as Mexico’s second-largest supplier. Even so, the United States remains the dominant source of Mexican imports, with exports to Mexico totaling USD 261.5 billion in 2024 and USD 249.8 billion in 2025—nearly double the value of imports from China—underscoring the continued consolidation of supply chains between the two countries. Canada, for its part, recorded exports to Mexico of approximately USD 13.0 billion in 2024 and USD 12.6 billion in 2025, highlighting an area of opportunity between these two markets. Taken together, these figures show that although China has gradually increased its presence in the Mexican market, the United States continues to be, by a wide margin, Mexico’s most important trading partner in terms of external sourcing.

Nevertheless, the outlook for Mexico’s external sector is not without risks. Since 2025, the imposition of tariffs on certain Mexican products by the U.S. administration has increased uncertainty for investment and regional supply chains. These challenges are compounded by persistent structural constraints, including limited logistics infrastructure, insufficient integration of domestic suppliers, and limited technology transfer, all of which have constrained the impact of foreign trade on productivity and investment. These risks have become particularly relevant in a context where the Mexican economy recorded a quarterly contraction at the beginning of 2026 and where market participants have revised growth expectations downward.

Despite these challenges, the structural outlook for the external sector remains favourable. Ongoing trade tensions between the United States and China, the search for more resilient supply chains, and the upcoming review of the USMCA reinforce Mexico’s strategic importance within North America. In this context, the strong performance of manufacturing exports, the dynamism of sectors such as machinery, electronics, and automotive manufacturing, as well as Mexico’s consolidation as the leading supplier of goods to the U.S. market, suggest that the external sector will continue to play a fundamental role as a driver of Mexican economic growth in the years ahead.

USMCA

As had been teed up and expected, on July 1st, the US chose not to renew USMCA for an additional 16 years. This means that under Article 34.7, the USMCA agreement goes into a process of annual reviews that will stretch for the following 10 years (until July 2036)—barring one of two alternatives:

- At a coming date, the agreement gets renegotiated / ratified, which we see as the base case.

- Article 34.6 (withdrawal) is invoked by any of the three leaders, meaning that 6 months afterwards the agreement expires—which we see as extremely unlikely.

We believe the most likely scenario is one where negotiations continue, and an agreement is reached later. The U.S. midterm elections are a key date to follow, as a loss by the GOP could erode President Trump’s strength vis-à-vis key governors—many of which are very heavily invested in USMCA—not least of which is Governor Abbott of Texas—arguably the most powerful governor for the Republican Party, whose state’s economy is boosted by almost US$900bn of trade with Mexico. This could be positive for the agreement.

It is also important to monitor the U.S. midterms as enough change to the agreement would imply that an executive re-ratification is insufficient, but a Congressional vote becomes necessary. Requiring Congressional approval reduces “tail risks” of drastic changes to the agreement’s core, as a worsening of the deal would affect the economies of states dependent on trade with Mexico and Canada, which should help defend North American partner’s interests. At this point in time, it appears that enough will be changed to require Legislative involvement.

According to the latest opinion polls, it appears that the House of Representatives could swing in the Democrat’s power, with many recent polls giving the Democratic party a +3 to +9 edge. The Senate appears less likely to switch hands, but the Democrats also have a chance to take it although that is a much closer call according to polls. A key question is how President Trump would react to a loss in the midterms, and how his influence over his party evolves if this scenario materializes. As we mentioned above, we believe that stronger governors relative to the Presidency would likely help reduce the likelihood of adverse outcomes for the North American partnership. It’s important to bear in mind that executive orders still give President Trump important powers, on trade and other matters.

Time should also be seen as an ally for a USMCA agreement, as the cost of extending uncertainty will likely increase pressure on the parties involved to reach a new deal. However, at this point in time, the biggest potential risk appears to be that some in the U.S. administration are leaning towards reaching two separate deals with Mexico and Canada, rather than a trilateral deal, which we see as negative.

We think the most important points for the negotiation to be a success will include:

- Mexico and Canada likely want assurances that the agreement will shield them from future use of tariffs such as those under sections 232 and 301.

- Negotiating the U.S. objectives for the auto sector which are believed to currently seek 82% North American content in the cars, with 50 percentage points of that produced in the U.S. (similar to the current 40% high-wage labour value cost requirement).

- Determining the various issues that relate to China—including those around national security and investment from the Asian giant. Another China centric concern is that USMCA shuts any potential back doors though which China could push its manufacturing over capacity.

Topics we don’t believe are currently at the core of the negotiations, but we believe should be, include:

- Using USMCA’s update as a mechanism for increasing investor certainty in Mexico—including on key sectors such as infra and power.

- Aligning the posture of the three countries on how strategic sectors such as data storage, power generation, infrastructure and telecommunications will be managed in a way which makes the three North American partners compatible in their views. One of the key elements should be the respective roles and leadership between private and public sectors.

PUBLIC FINANCES

At the beginning of the year, we discussed the three main events that have shaped public finances since 2025: the government’s efforts to increase tax collection efficiency while keeping taxes unchanged, the contraction in public spending, characterized by weak support for public investment and support operations for Pemex, and more optimistic estimates compared with analyst consensus. Fiscal deterioration has become evident through these developments, also leading to changes in credit rating outlooks and ratings, affected by pressures on public finances. As a result, the risk of losing investment-grade status has increased significantly for the outlook over the coming years. One of the main headwinds to Mexico’s public finances remains sub-par growth, which affects the growth path of tax revenue.

According to the latest available data, the public balance during the first five months of the year stood at -391,303.2 million pesos, below the programmed deficit of -684,842.4 million pesos.

Despite this result, budgetary revenues show relevant pressures, falling 1.8% year over year in real terms to 3.554 trillion pesos during January–May, also below the 3.706 trillion approved in the program. Part of this result is explained by the decline in oil revenues of -3.2% year over year in real terms, due to a lower production platform and the effect of a weaker exchange rate, which offset the increase in prices related to the geopolitical conflict in the Middle East.

Likewise, tax revenues declined during the period, by -1.4% year over year in real terms, reflecting weaker economic momentum and the exhaustion of efforts to improve collection efficiency. In contrast, spending grew 2.3% year over year in real terms during the same period, reaching 3.973 trillion pesos, although this amount was below the programmed level, implying under-execution relative to the 4.391 trillion pesos stipulated in the program.

Although the decline in financial costs has provided some relief during the fiscal year, the spending outlook faces significant inertia in the coming years, particularly pension spending, which has grown 6.0% year over year in real terms and in 2025 reached a record high as a share of GDP, at 4.6%. In contrast, physical investment continues to contract (17.3%), after representing only 2.2% of GDP in 2025.

Given spending pressures and limited room to allocate resources to public investment, the federal government has opted to promote greater private-sector participation in strategic infrastructure projects under Plan México and the Portfolio for Shared Prosperity. Within this effort, the energy sector stands out, where the administration has sought to combine the role of the Federal Electricity Commission (CFE) with private capital in power generation, transmission, and distribution projects, as shortages in these areas have become one of the main bottlenecks for the development of productive chains.

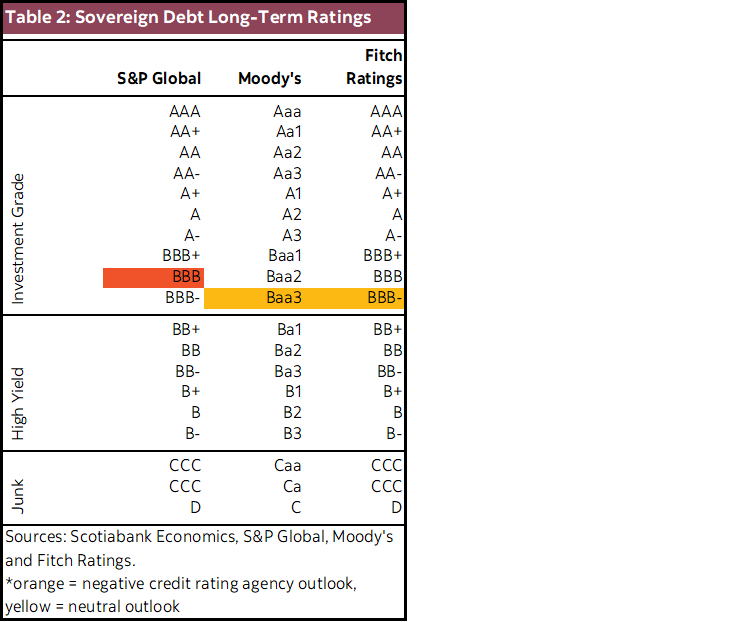

In addition, fiscal space remains constrained by Pemex’s support needs. In recent years, the government has relied on both capital transfers and reductions in the company’s tax burden—strategies that have partially contained short-term liquidity risks but have also transferred part of these pressures to the sovereign balance sheet. Federal government support for Pemex has become one of the main areas of focus for investors and rating agencies. Indeed, although the government has reiterated its financial support for the company, the scale of its debt maturities and persistent operational weakness continue to draw the attention of rating agencies, which have repeatedly noted that any further deterioration in the sovereign’s capacity to provide support or in the fiscal trajectory could lead to new negative actions on Mexico’s credit rating (table 2, S&P has Mexico on ‘negative’ watch).

MONETARY POLICY AND INFLATION

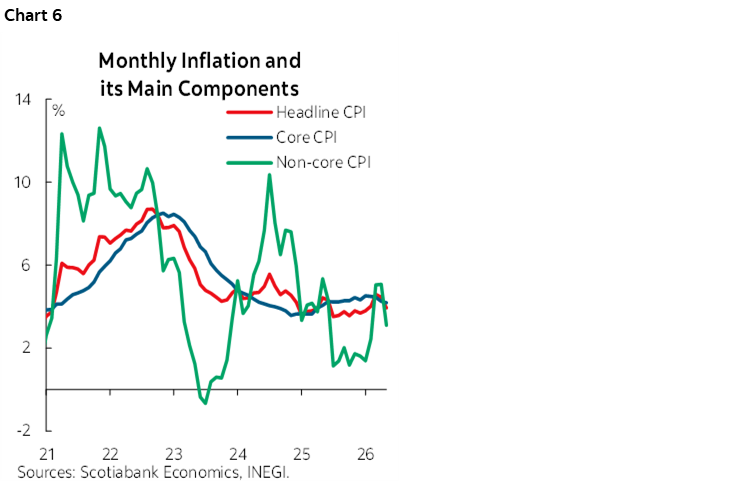

During 2025 and the first half of 2026, the disinflationary trend became more firmly established, though inflation remained above Banco de México’s 3% target (chart 6). In fact, headline inflation spent most of the period near the upper end of the ±1% tolerance range and exceeded 4% on several occasions. Notably, core inflation—a key gauge for monetary policy decisions—remained consistently above 4% from May 2025 onward, despite the low-growth economic environment.

Nevertheless, the recent moderation in prices allowed annual headline inflation to decline to 3.55% in the first half of June 2026, while core inflation eased to 4.12%. This slowdown has been driven mainly by lower pressures in fresh food products and certain energy prices; however, the services component continues to exhibit considerable persistence, with inflation rates above 4.5%. In this context, the main challenge for monetary policy is to ensure that inflation converges toward target in a sustainable manner and that the decline reflects a structural reduction in inflationary pressures, rather than merely temporary or volatile factors.

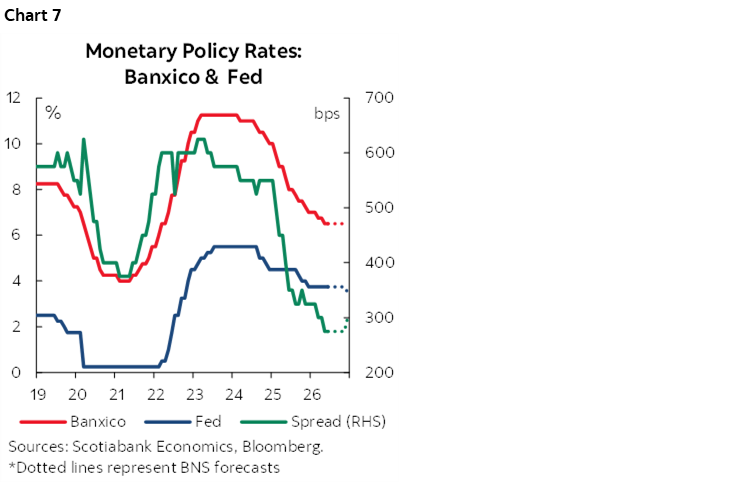

In response to the inflation surge, Banxico reacted early and decisively. Between mid-2021 and early 2024, it implemented one of the most significant monetary tightening cycles among emerging economies, raising the policy rate from 4.00% in June 2021 to a record high of 11.25%. The objective of this strategy was to contain demand-side pressures, prevent second-round effects on wages and prices, and preserve the anchoring of inflation expectations. As a result, Mexico maintained one of the highest ex-ante real interest rates in the emerging-market universe, strengthening the central bank’s credibility and helping stabilize inflation expectations.

Subsequently, as inflation began to follow a more consistent downward path and economic activity showed signs of slowing, Banxico initiated a monetary easing cycle in March 2024 that accumulated 475 basis points in rate cuts. This process concluded—at least temporarily—at the June 25th, 2026 meeting, when the Governing Board decided to keep the policy rate unchanged at 6.50%, arguing that although headline inflation has declined significantly, core inflation remains resilient, however both inflation expectations and the balance of risks continue to be tilted to the upside.

Banxico’s strategy contrasts with that of other central banks, both in advanced and emerging economies. In the United States, for example, the Federal Reserve raised the ceiling of the federal funds rate to 5.50% at the peak of its tightening cycle in 2022–2023. It subsequently began a monetary easing cycle in September 2024 as inflation followed a more favourable trajectory, a process that concluded in December 2025. Since then, the Fed has kept rates in a 3.50% to 3.75% band, reflecting concerns about potential inflationary pressures arising from developments in energy prices linked to the conflict in the Middle East, as well as the continued resilience of the U.S. labour market.

As a result of these policy moves, the interest rate differential between Mexico and the United States has narrowed to 275 basis points, its lowest level since 2015 and well below the historical average of roughly 450 basis points (chart 7). This decline has partly reduced the relative attractiveness of Mexican assets, as the yield differential appears insufficient to fully compensate for the risk premium that investors typically require to hold positions in emerging markets. Consequently, the support that the carry trade has traditionally provided to the exchange rate has weakened considerably in recent months.

Looking ahead, our baseline scenario assumes that Banxico will keep the policy rate unchanged for the remainder of 2026, despite the fact that inflation risks remain tilted to the upside. In this regard, the ex-ante real interest rate currently stands at around 2.7%, virtually at the midpoint of Banco de México’s estimated neutral rate range of 1.8% to 3.6%.

Nevertheless, following the release of the inflation data for the first half of June and recent comments by Governor Victoria Rodríguez Ceja, the debate over the possibility of an additional rate adjustment has resurfaced. Rodríguez emphasized that the current policy rate remains sufficiently restrictive to ensure inflation converges to target and that the pause in rate cuts has no predetermined duration, meaning that future decisions will depend strictly on incoming data. Therefore, while our baseline scenario envisages an extended pause, an additional rate cut cannot be ruled out if headline inflation remains sustainably within the 3% ± 1% variability range and underlying inflationary pressures continue to moderate.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.