- This year will be an exciting one for Mexico, filled with both challenges and opportunities. In this report, we look closely at the main issues that the country will face over the coming quarters from a macroeconomic and political perspective.

- The US’ economic performance will play a key role on Mexican growth at a time when Mexico is seen as an important beneficiary of nearshoring plans. The link between the countries’ economies will also be top of mind for investors anticipating a narrow window for when Banxico could ’decouple’ from the Fed.

- From a more domestic standpoint, state elections in Edomex and Coahuila, as well as public finances and risks surrounding state-owned enteprises are additional considerations for the Mexican economic and financial outlook.

This year will be an exciting one for Mexico, filled with both challenges and opportunities. In this report, we look closely at the main issues that the country will face over the coming quarters from a macroeconomic and political perspective.

The US’ economic performance will play a key role on Mexican growth and we’re keeping a close eye on whether clearer nearshoring green shoots will emerge that could give the Mexican economy a welcome push against a broad global slowdown. Challenges to the domestic environment for investment remain, although we expect that the Mexico vs US & Canada dispute over energy sector rules under the USMCA treaty is expected to find a resolution.

Inflation likely peaked at the end of 2022 and hence the next key debate will be when Banxico begins its easing cycle. We anticipate Banxico will decouple from the Fed in early-2023, but we still expect the bank’s overnight rate will rise to 11%, which means that the policy rate spread between the two countries will only slightly narrow. Next year we will see three factors combine to put upward pressure on employer costs: 1) another 20% increase in minimum wages which has already been approved, 2) the pension reform’s gradual increase from 6.25% to 15% in employer contributions to employee pensions will start in 2023, and 3) the negotiation of union wage contracts under the new USMCA framework needs to be completed by summer 2023. These wage pressures could make inflation ‘stickier’ in 2023.

In politics, the State of Mexico governorship election is seen as an important preamble to the 2024 presidential election. Edomex is the PRI’s only remaining major bastion, the country’s largest economy after Mexico City, and the most populous state. In addition, the government’s political reform will remain on track, and its ratification will be important for shaping the 2024 election.

As for public finances, the budget is again a prudent one, although it is once more built on what look like somewhat optimistic budget assumptions, with growth likely being the budget’s Achilles’ heel.

I. CAN NEARSHORING SAVE THE DAY IN 2023, DRIVING A STRONGER INCREASE IN INVESTMENT?

The US is now broadly expected to fall into technical recession in 2023. This is likely to prove a challenge for the Mexican economy, since about ⅔ of the recovery from the 2020 pandemic low is accounted for by exports to the US and strong remittance flows accounted.

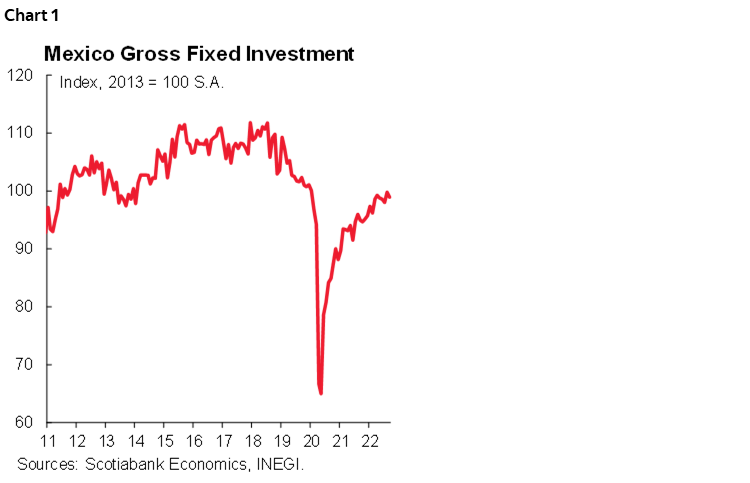

One of the great questions heading into 2023 is how much could investment contribute to Mexico’s economic rebound. Could this offset US-led weakness? The latest reading for total gross fixed investment in Mexico in Q3-2022 stood slightly below the 2013 average (chart 1), as weak capital formation acts as a primary drag on Mexican growth.

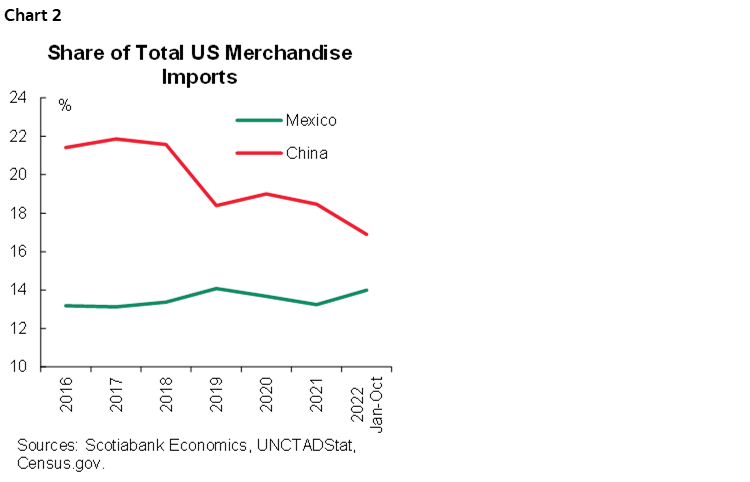

Can the nearshoring story lead to a stronger bounce in investment? We think the answer is complex. On the one hand, the opportunity for attracting investment is there as production targeting US consumers migrates from China. Goods from China have lost market shares as a total of US imports since 2017, sitting at 17% currently from 22% five years ago (chart 2). However, Mexico’s share of US imports is essentially flat, hovering in a 13–14% range over this period. So far, Mexico has not seen an increase in its US market share nor in domestic investment. Will that change?

As our equity research team has argued, there’s evidence that certain regions and sectors of the Mexican economy are seeing positive results from nearshoring, particularly sectors linked to logistics and manufacturing. Certain regions in Mexico (Torreon, Monterrey, etc.) are seeing rising investment related to nearshoring. However, the macro level impact of nearshoring remains elusive. What can trigger a rebound in investment?

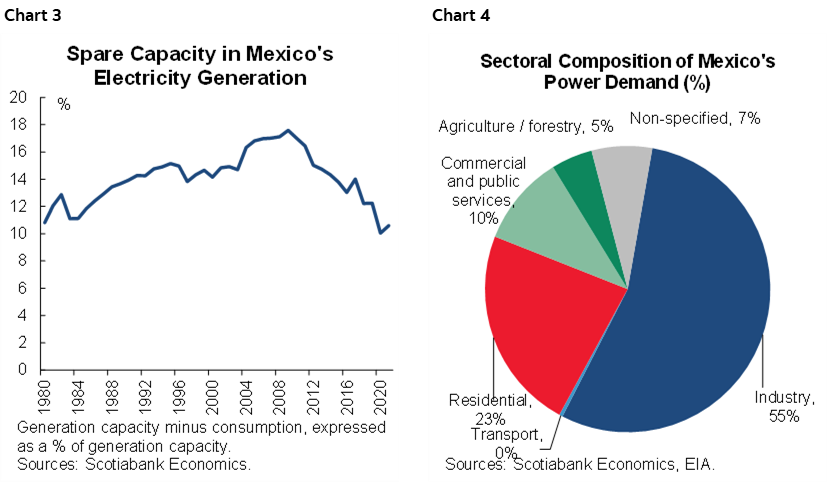

- Power: With the private sector’s role in power generation facing important uncertainty around fair competition between private and public players—including an ongoing dispute between Mexico vs US & Canada under USMCA—investment in the energy sector has been stagnant in recent years. This has resulted in concerns over whether electricity supply will be sufficient to power manufacturing in the country. Currently, excess energy capacity is close to its lowest level of the past 40 years (chart 3) and Mexico’s industry is very energy intensive—accounting for over half of the country’s power demand (chart 4).

- Valuations: Over the past 20-years, episodes of sharp real depreciation in the MXN have been followed by large increases in investment flows. Several metrics such as the real-effective exchange rate are beginning to suggest that the Mexican peso is becoming relatively expensive. We believe that an exchange rate move could be the catalyst for a rebound in investment as global bargain hunters swoop in.

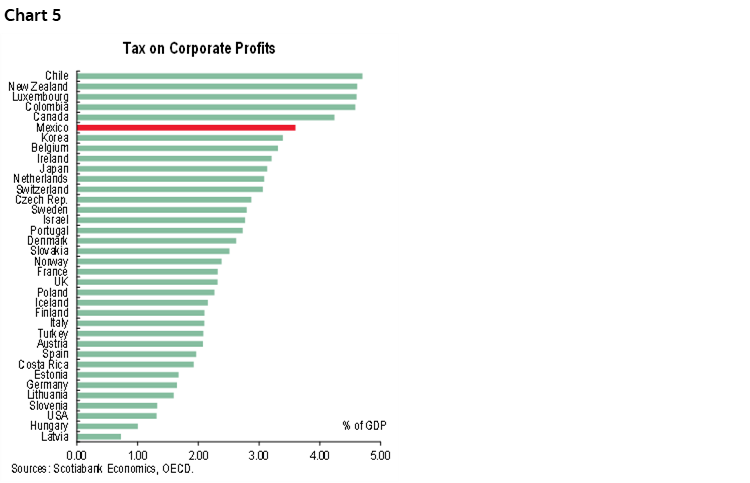

- Policy stimulus / tax reform: Mexico’s collection of corporate profit taxes as a share of GDP is relatively high (3.6%, vs 1.3% in the US, chart 5), which combined with other “high costs” such as security, electricity, and cost of capital, erode Mexico’s competitiveness—somewhat offsetting the attractiveness of cheap labour and land. Mexico’s “expensive corporate taxes” are even worse, if we consider that close to 50% of the economy lives in informality, meaning formal contributors face an even higher burden to reach a high collection share of GDP. At this point in time, tax reform looks “off the table”.

- Broader Structural Reforms: There have been many attempts to boost Mexico’s attractiveness to investment over the past 40 years, ranging from the steps taken in the 1980s (price stability pacts, financial liberalization, entering the GATT, and privatizing state owned enterprises), to those that followed in the 1990s (establishing the domestic pension system to boost savings rates, entering NAFTA, granting Banxico formal independence to stabilize prices and interest rates), as well as those undertaken in the 2010s (opening the energy sector to private investment, strengthening anti competition authorities, attempts to strengthen education institutions). At this stage, many of the pending challenges to investment in the country relate to previous attempts, and include:

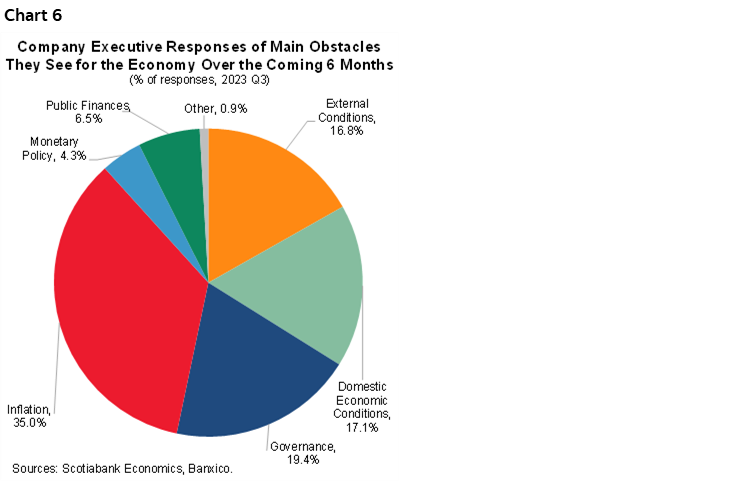

1) deepening financial intermediation (credit / GDP in Mexico is between ½ to ⅓ of that in Chile and Brazil), 2) improving the education system (similarly to elsewhere in LATAM, Mexico scores at the very lowest level in the PISA tests), 3) strengthening the judicial system to tackle corruption and insecurity (more on this below), as well as 4) fiscal, social security and energy reforms. Most of these topics are off the political agenda, and hence we will address them closer to the 2023 Presidential election. - As noted above, another hurdle to capitalizing on the opportunity presented by nearshoring are crime and governance shortfalls. In a survey of firm executives carried out by Banxico (chart 6), those polled were asked what the main obstacles to the recovery were, with a combination of short-term issues (inflation, monetary policy) and longer-term factors mentioned. It’s noteworthy that among longer-term issues, around a fifth of respondents said ‘governance’ represents a key structural factor hindering economic growth. Within governance, the main obstacles cited are insecurity (40%), political uncertainty (31%), and corruption (19%). It’s difficult to quantify how much insecurity truly subtracts from Mexican growth and investment, but estimates range widely from around 1.0% to 5.5% of GDP (and an outlier estimate of as high as 20%).

- The National Statistic’s Institute (INEGI) survey on the cost of crime shows that in 2021, 1.5% of GDP was the cost of what was directly lost by citizens to crime and what was spent in crime prevention. INEGI’s figures show there were at least 28 million crimes committed in Mexico in 2021, of which robbery represented 21.4%, extortion 17.5%, fraud 19.2%, and automobile theft 10.8%.

- A study by the Mexican Institute for Competitiveness (IMCO) in 2022 said a full 25% of firms were victims of crime, and 53% see insecurity as their main problem to its operations. The direct impact of crime on companies (extortions, robberies, fraud, etc.) is estimated to cost 0.67% of GDP. This does not include the costs of private and public security measures, adjustments in business strategies, etc. On top of that, the IMCO report shows that only 1 in 10 crimes on firms were reported.

- Estimates by the Mexican Employer Organization Coparmex (an association of SMEs) put the direct costs at 1% of GDP.

- An estimate by an academic from the University of Guadalajara put the cost borne by companies at around 5% of GDP (the estimate was made by Roberto Soria Romo in 2018, based on “accounting costs” from companies).

- A more extreme estimate, by the Institute for the Economy and Peace, put the cost of insecurity and violence at 20% of GDP—but this estimate includes items such as defense spending, etc.

At this point in time, data suggest that nearshoring is a macro-opportunity, which is yielding sectoral and regional results—although it’s likely helping balance out other drags on broader growth. Security, access to utilities, and access to transportation infrastructure are very uneven across states. This helps explain why some states are tapping nearshoring more than others—as we argued in a past report. Indicators on US market share gains, economic growth, and economy-wide investment rates have been weak-to-flat by historical Mexican standards. However, steps can be taken to broaden the benefits enjoyed by the Mexican economy.

—Eduardo Suárez

II. BANXICO DECOUPLING FROM THE FED

History has taught us that preventing an inflationary spiral by front loading monetary policy actions is better for long-term growth, despite the short-term costs (BIS Annual Economic Report 2022). Both in the US and Mexico, inflation has been stubbornly high (charts 7 and 8), consistently beating forecasts and increasing the risk of de-anchoring expectations.

After showing up a little late to the hiking party, the Federal Reserve firmed up its hawkish guidance with phrases like “ongoing increases”, “restrictive policy stance for some time”, “[our] priority is price stability” in almost every communication. Of course, they needed to do this, as not doing it would have jeopardized their credibility. However, as central banks struggle with balancing rising inflation against deteriorating growth prospects, ‘fear-trading’ in markets over the Fed guiding higher-for-longer stance seems to have eased, particularly following its December 2022 decision (chart 9).

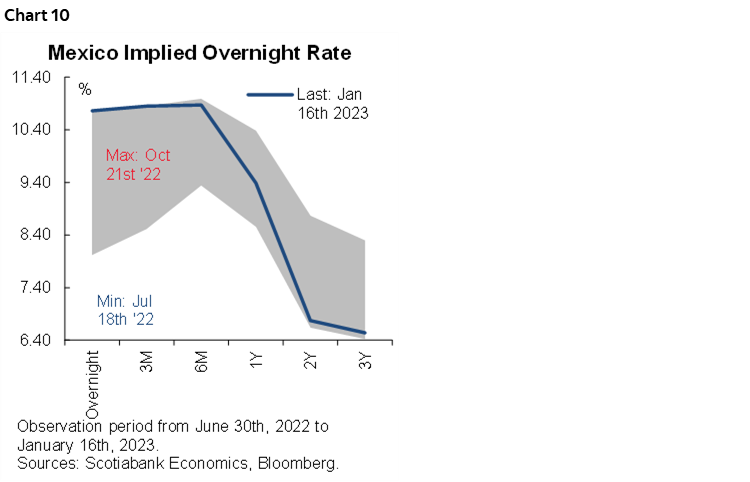

But, what about Mexico? The Mexican economy is highly integrated to the US’: according to Banxico’s latest Regional Economic Report, the economic phases of both countries coincide in 80% of the time (on a quarterly basis). Additionally, members of Banxico’s board have repeatedly acknowledged the importance of the relative monetary policy stance with the Fed and, as such, the fact that Banxico has followed the Fed’s steps in the last six decisions is no surprise (chart 10). Both countries face similar external inflationary pressures such as the conflict in Europe and its impact on energy prices, broadly stronger commodity prices, and logistical bottlenecks (whose effects are fading). However, Banxico might be closer to reaching its terminal rate than the Fed.

Headline inflation in Mexico declined to 7.82% y/y in November (from 8.41% in October), but pressures in merchandises and services have seen core inflation leapfrog headline. Although some board members have highlighted in the past that reducing the hiking pace will happen only once the “inflationary outlook improves, especially in its core component”, we think that core inflation will have peaked prior to Banxico’s February meeting, its first of 2023. Also, in the latest Quarterly Inflation Report Presentation, even the most hawkish members of the board signaled that they would support slowing the hiking pace, building on speculation over a decoupling from the Fed in the near term. That said, we still expect Banxico to hike at least one more time, in line with the latest communiqué stating: “it will still be necessary to raise the reference rate at the next monetary policy meeting”. Additionally, the minutes from December’s meeting confirm our expectation that Banxico will further reduce the hiking pace to 25bps and deviate from the Fed.

Going forward, our baseline scenario has Banxico keeping the hawkish tone and delivering one last hike in March, leaving the rate at 11.00% throughout most of 2023. The timing for Banxico to begin with its easing cycle is still uncertain. There’s a considerable divergence between markets and economists' expectations, with the market implied policy rate for the end of 2023 standing at around 9.50%, while Bloomberg’s economic forecast consensus is 10.50%. In our view, there are still important pressures to inflation that might push the easing cycle further in to the future, potentially to 2024, but at this point, we expect the rate to close the year at 10.50%.

III: WHAT ABOUT MEXICAN FINANCIAL MARKETS?

Despite political uncertainty, the MXN was resilient through 2022, appreciating 5.3%, and only behind the BRL in terms of annual performance among the major currencies (chart 11). Of course, we cannot ignore the 600bps Banxico-Fed spread (charts 12 and 13). Even considering a very likely decoupling soon, the median economist in Bloomberg’s surveys sees a 20 pesos per USD exchange rate level at end-2023. This is in line with 1-yr FX swaps (chart 14), which nevertheless diverge by around two pesos higher in their view for the USDMXN exchange rate at end-2024 (21 pesos) when compared to the economist median (~19 pesos).

Another, although bittersweet reason, for the MXN’s stability is the fact that non-resident holdings of Mexican public debt have practically halved and stalled in the last 3 years (charts 15 and 16). An upside to this? Most of these remaining holders are passive investors such as pension funds, meaning lower speculative flows and reduced MXN volatility.

Regarding money markets, we expect Banxico to stop its hiking cycle in Q1-2023, but now a long wait begins, with rate cuts likely beginning around year-end or even early-2024.

Growth prospects in 2023, as everywhere else, will be hindered by the effects of high inflation and synchronized restrictive financial conditions. Locally, investment is far from pre-COVID-19 levels, not because of monetary policy but rather owing to political uncertainty (see Section IV). As a result, as we enter the easing cycle in late-2023, we expect a bull steepening curve (chart 17).

Mexican assets may face some headwinds in the form of : a) a higher minimum wage starting in 2023 that will increase firms’ costs, and without more (or better) qualified workers and/or more investment in fixed capital, productivity may not improve; b) the pension reform’s increase in employers’ contributions; and c) the negotiation of union wage contracts under the new USMCA framework will worsen the profit outlook of firms.

On the flip side, we believe that strength in certain industries such as manufacturing, tourism, agriculture, and e-commerce, could prove supportive. Furthermore, nearshoring activity may have some positive (though perhaps limited) spillovers on the broader economy that could buoy Mexican financial markets (see Section I).

—Luisa Valle

IV: PUBLIC FINANCES AND POLITICAL OUTLOOK

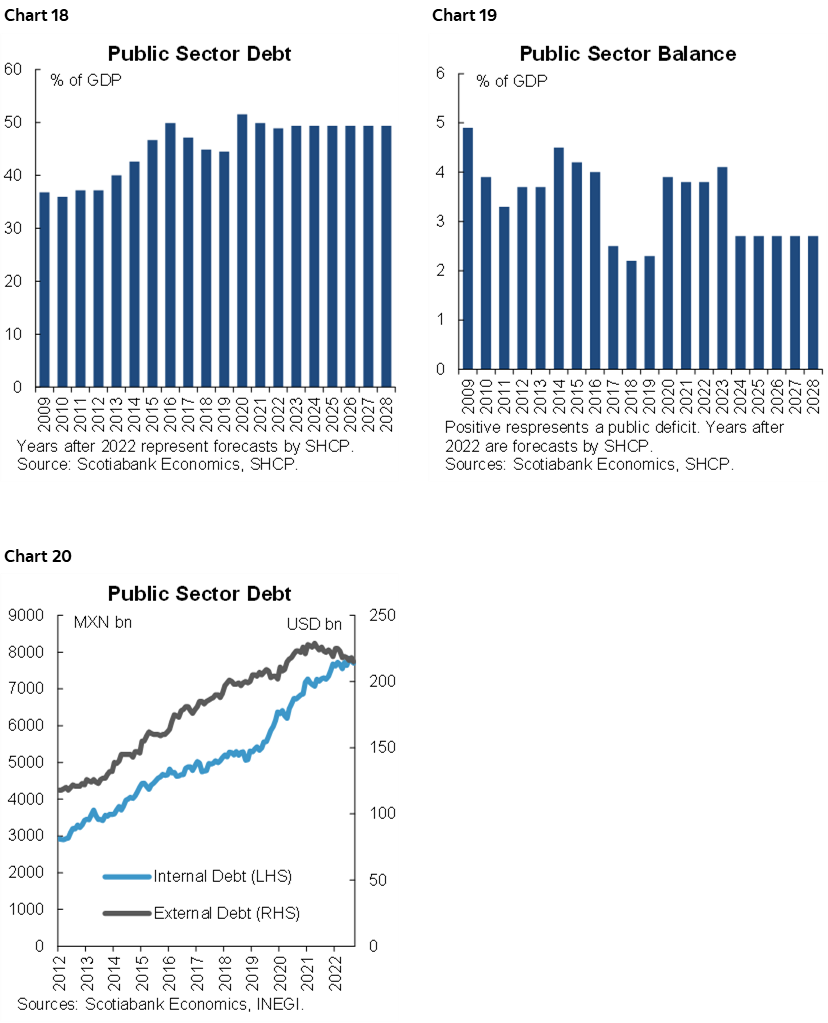

In contrast to most countries, Mexico’s response to the COVID-19 pandemic didn’t include material fiscal stimulus (only about 0.7% of GDP). This placed Mexico’s public finances in a relatively robust position. While as a percentage of GDP public debt rose to a fresh high in 2020, the deterioration in public finances was mostly the result of a decline in GDP. Notwithstanding Mexico’s relatively solid fiscal position post-pandemic, the Ministry of Finance (SHCP) is planning to steady the trajectory of public debt in relation to GDP (charts 18, 19, and 20).

However, the government’s estimates for growth in 2023 still look too optimistic in relation to economists’ forecasts (2023 growth: 3.0% vs 0.9% consensus, and end-2023 inflation: 3.2% vs 5.07% consensus). In addition to the growth estimate, the SHCP’s outlook is also optimistic regarding the level of Banxico’s policy rate for the end of the year, as their 8.50% projection is significantly lower than the 10.25% median analyst estimate. Thus, their projected deficit of 4.1% of GDP for 2023 may end up being too optimistic considering weak growth, which in turn will result in lower revenues relative to spending plans, despite the austerity strategy in key areas of government.

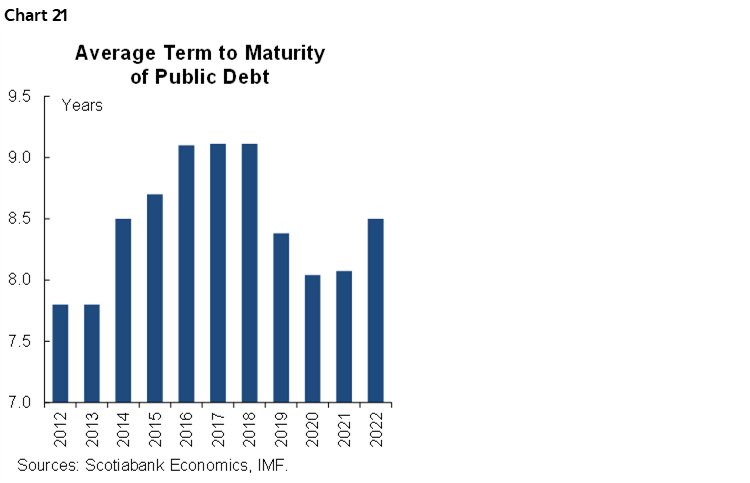

Additionally, we highlight the government’s efforts to extend the average maturity of debt (chart 21). In this regard, the composition of debt has benefited from a lower share of external debt denominated in dollars, reducing the impact of external volatility on Mexico’s public sector balance.

Among the risks to sovereign debt, the breakdown of outlays will be decisive in maintaining Mexico’s credit rating at acceptable levels. In particular, the state’s creditworthiness will remain linked to that of Pemex and CFE (the state-owned electricity company, charts 22 and 23). Rating agencies have highlighted Pemex’s dependence on the federal government as the company’s increased revenues from higher oil prices fall short of increases in spending, which has led to liquidity problems, higher financial losses, and therefore a strong dependence on federal government support.

On the political front, the next presidential election is coming more into focus, despite June 2024 still being some time away. Two state elections will take place in 2023, Coahuila and the State of Mexico, states that historically have been PRI strongholds where the party will face opposition from two strong Morena candidates: former Secretary of Education and close ally of the President, Delfina Gómez, in Edomex, and senator and coal industry businessman, Armando Guaidana, in Coahuila. In particular, the Edomex election will also be relevant due to its proximity to the capital, its share of the country’s population, and its contribution to national economic activity.

In the international arena, negotiations regarding energy, automotive and labour chapters of the USMCA will remain an important item to monitor. Currently, delegates are still in the process of consultations regarding the Mexican government’s energy policy, with recently appointed trade secretary Raquel Buenrostro representing Mexico.

—Miguel Saldaña

V: THE INCREASE IN THE MINIMUM WAGE AND THE IMPACT ON HOUSEHOLDS

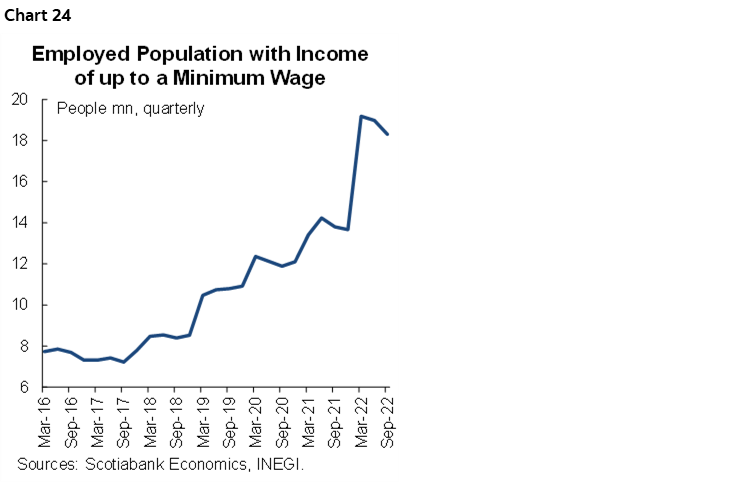

Recently, the government announced a 20% increase in the minimum wage for 2023, reaching MXN312.41 (USD16.10) per day in border states and MXN207.44 (USD10.30) in the rest of the country. With this, the AMLO administration kept its promise to raise standards for workers, with the minimum wage increasing every year by close to 20% on average since taking office. The wage increase will impact as much as 18 million workers (in both formal and informal sectors, chart 24)—about 31% of employed population—who earn the current minimum wage or less. The wage increase could support consumption in 2023 amid higher household incomes complemented by the vigorous trend in remittances during the pandemic—if it holds.

However, there are also some risks associated with the government’s minimum wage increase, particularly in a persistently high inflation environment. For instance, there could be a chain reaction that lift overall wages, which would increase payroll costs, hindering employment, and negatively affecting economic activity. This is particularly relevant as the rise in wages would not reflect higher productivity (chart 25). Spending on other areas such as developing skills, and higher investment and innovation would be a better use of funds than a larger wages bill.

With an expected economic slowdown amid high interest rates, household finances will be strained during 2023. On the positive side, the increase in salaries, accompanied by the record gains in remittances, could increase the financial resilience of Mexicans. Inflation is also expected to decelerate considerably in 2023, and the loss in purchasing power from consumers should not be as pronounced as in 2022. On the financing side, housing loans growth remains on an ascending path (setting aside data ‘kinks’, charts 26 and 27), on the prevailing trend pre-COVID-19. Still, consumption sharply recovered in 2021 and 2022, supported by the reduction in sanitary measures and pent-up demand.

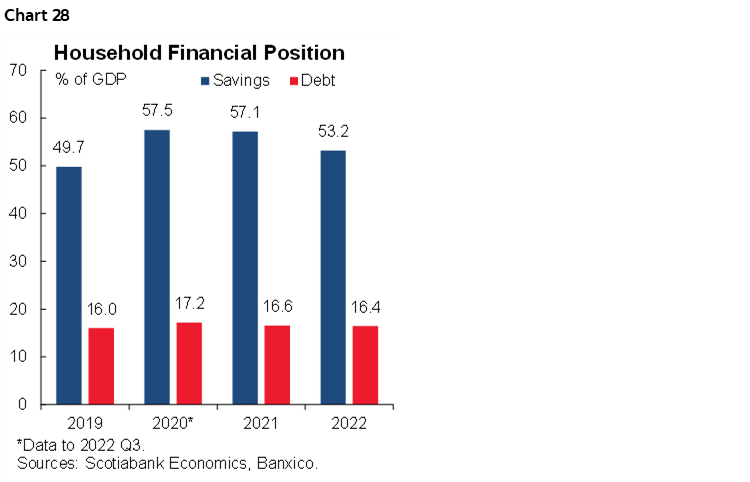

Nonetheless, slower economic activity could also result in higher unemployment, impacting aggregate household income. Also, despite remittances totaling USD53bn in January–November 2022, it will be difficult for these to exceed their maximum share of GDP, which surpassed 4% in 2021. Data up to the third quarter of 2022, shows they barely crossed 3%, meaning we may see a deceleration in remittances in 2023 alongside lower economic activity in the US. Lastly, household savings as percentage of GDP (chart 28) have fallen since the pandemic, and a contributing factor to this are COVID-19-related expenses that have diminished and restrictions have been eliminated, translating into people returning to prior consumption patterns, diminishing savings.

—Brian Pérez

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.