- The monetary policy report showed a complicated balance between still upside risks on inflation and an economic downturn.

On Monday, the central bank staff released the Monetary Policy Report (MPR), updating their assessment of the current macroeconomic scenario and the balance of risks for the monetary policy horizon.

Regarding the international backdrop, the staff highlighted that inflation pressures had eased. However, inflation is expected to remain above central banks’ targets, resulting in an upward revision to the staff’s international rates forecasts. On the other hand, staff remarked that global financial conditions have improved, contributing to a reduction in Colombia’s risk premium—though they also said uncertainty remains high.

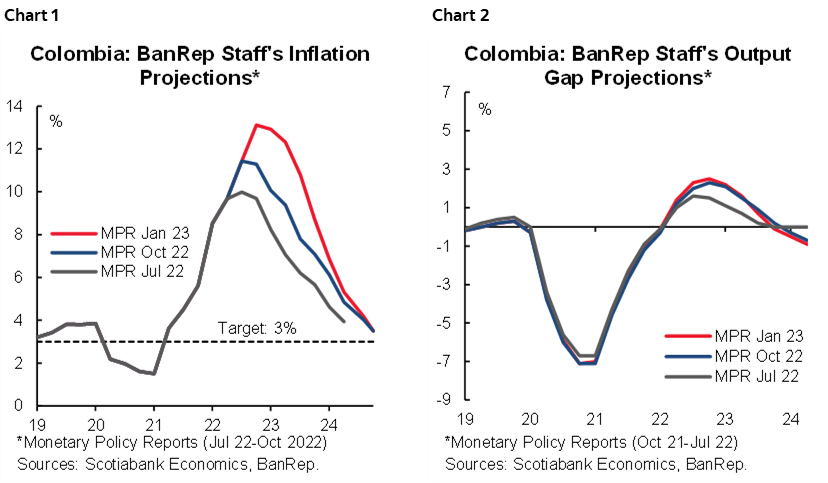

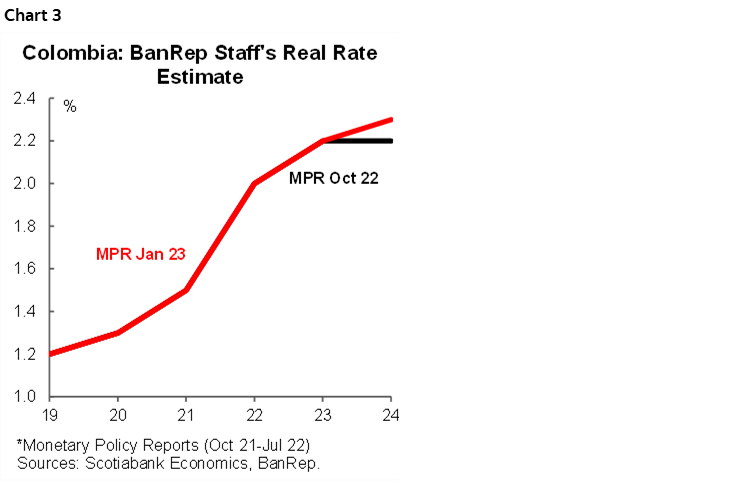

As for the domestic picture, higher-than-expected inflation by the end of 2022 saw staff revise their inflation forecast path higher. They now expect inflation to close 2023 at 8.7% and between 3.5% and 3.8% at end-2024 (chart 1). On the activity front, Colombia’s GDP expansion in 2022 was revised from 7.9% to 8.0%. However, the outlook for 2023 is more pessimistic, as the latest MPR projects 0.2% growth vs the previous expectation of 0.50%. The negative revision reflects the effect of tighter financial conditions, which are expected to significantly mute domestic demand. With this weaker growth profile, the output gap should have closed by end-2023 (chart 2). BanRep’s staff reiterated that uncertainty is very high, however, risks are tilted to the upside on inflation and to the downside in economic activity.

All in all, BanRep said that the monetary policy rate path to achieve the inflation target by the end of 2024 is on average higher than currently expected by the economist consensus, which points to a monetary policy rate reaching 13%, and closing 2023 around 10.5%. This highlights that the staff recommendation is probably more hawkishly tilted than what was finally delivered by the board in last Friday’s announcement.

Our take on the Monetary Policy Report is that the central bank staff is more willing to recommend higher rates that would produce a strong economic deceleration—resulting in a faster convergence of inflation towards target. However, we feel that the staff’s projection of a strong deceleration is one key piece of information that prevented the board from being more aggressive with its rate hike last week.

In any case, Governor Villar said explicitly that the board is in a data-dependent mode and that they leave the door open to further rate hikes, if needed. We expect a final move of 25bps in the March meeting. At Scotiabank Economics, we have a more constructive view about economic activity in relation to the central bank but believe that it won’t be possible to reach the inflation target—even in 2024.

The main highlights of the MPR include the following:

- International context: BanRep’s staff highlighted that external financial conditions for Colombia have eased at the margin, which led to a downside revision of the country’s risk premium versus the previous report (CDS hovering around 281 ppts in 2023 and 2024), however, it will remain at high levels.

- On the flip side, the staff revised to the upside their assumption about the Federal Reserve’s policy rate for 2023. However, it is interesting to note that the real neutral rate remained stable at 2.2% for 2023, while for 2024, it is now estimated at 2.4% (chart 3).

- The expected inflation path was revised significantly to the upside. The staff stressed that the FX depreciation and indexation effects led to the upward revision. By the end of 2023, inflation is expected at 8.71%. However, it is worth noting that the staff expects inflation to peak in Q1-2023 due to the high statistical base effects of food inflation. By the end of 2024, inflation is expected to close a 3.5%, within the 2–4% target range, which is compatible with the reduction of the positive output gap. We affirm our expectation of a peak in inflation in Q1-2023, and our inflation forecast of 8.8% by the end of 2023; however, we believe that indexation effects will make it difficult for inflation to reach the target by the end of 2024 and our projection points to 5.03% inflation in December 2024.

- Economic activity: BanRep staff anticipate GDP growth of 8.0% for 2022 (slightly above the previous forecast of 7.9%). The staff highlighted that Colombia started a phase of slower economic growth. Consumption is expected to increase mildly in Q4-2022, which signals a reduction in savings. On a negative note, imports suggest weaker investment activity. That said, in parallel with moderating activity, a reduction in the external deficit is also expected. Ahead of 2023, the staff projects a 0.2% expansion amid high financing costs in the context of a global slowdown. Private demand is expected to continue moderating domestically, while investment will also lose momentum. In 2024, growth is expected to accelerate to a 1% expansion, which is still very low compared to the long-term growth rate of ~3–3.5%.

- The 2022 current account deficit is estimated at 6.3% of GDP (higher than the previous estimate of 5.7% of GDP), but is expected to narrow to 3.9% of GDP in 2023 because of a strong economic deceleration which would be reflected in lower imports. The main risk for this scenario is lower than expected commodity prices. Still, BanRep’s staff said that Colombia would maintain enough access to international finance.

- All in all, the staff estimate that the economy shows a positive output gap, which would become negative in 2023. However, as the inflation gap will still be high, there is room for taking the rate to a more contractive stance and maintaining this for a longer time.

Key points about the press conference (Wednesday, February 1)

- During the press conference on Wednesday, February 1, BanRep’s Chief Economist, Hernando Vargas, said that downside revision in the GDP growth expectation for 2023 involves: statistical base effect as in 2022 GDP growth was revised to the upside, further moderation in the private consumption and investments, and a more challenging economic environment. Additionally, despite the MPR, they said that risks are tilted to the downside; in the press conference, he also recognized that estimations about the output gap have shown by the time that excess of capacities has not been as high as previously estimated.

- Chief Econ Vargas also said that although a GDP expansion of 0.2% in 2023 could imply some q/q GDP contractions it should not be qualified as a recession. Instead, it should be considered as a healthy deceleration in which households are reducing their financial burden, maintaining still a high level of economic activity.

- During the press conference, Chief Vargas also said that the household savings had decreased significantly in the previous year, while the financial burden was high. That said, he highlighted is contributing to incentivizing a deleveraging in the economy. He also remarked that the financial system is robust and has strong liquidity and solvency indicators.

- Regarding inflation, Chief Vargas said that inflation projection in the policy horizon (for 2024 at 3.5%) assumes that inflation above the target is not altering the credibility of the inflation target or the degree of indexation in prices. Our interpretation of this line is that probably the staff is assuming weaker indexation effects in the medium term, which poses a significant upside risk in the staff’s projection. Either way, as inflation is reaching a ceiling, we don’t think this potential upside risk to conduct to a higher terminal rate. Instead, it would lead to a long period of stability with higher rates.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.