- Ministry of Finance bets to support the economic recovery, and it means acting within the limit of fiscal rule compliance

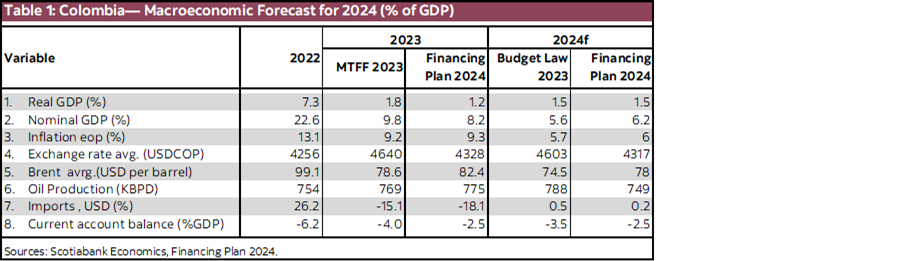

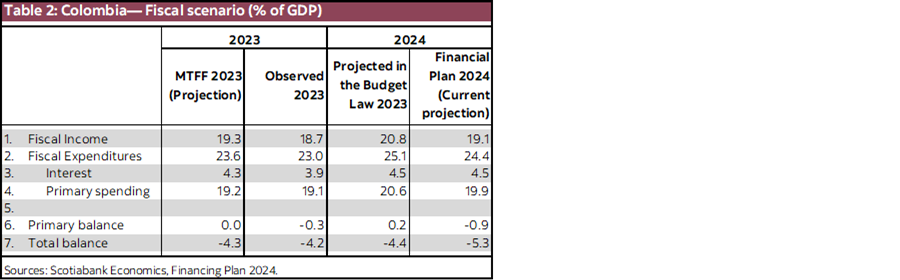

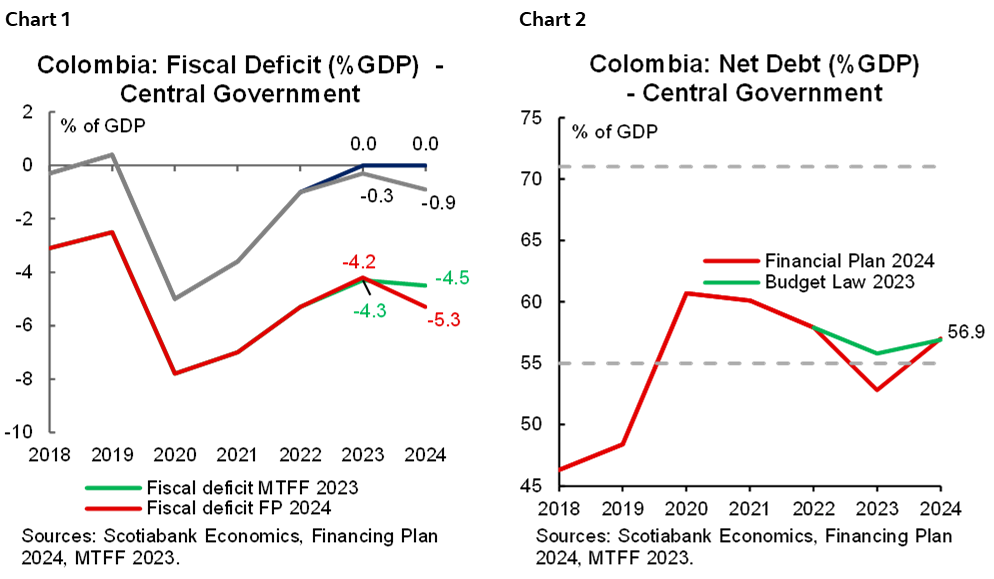

On February 1st, the Ministry of Finance (MoF) released the Financing Plan for 2024 and preliminary financial results for 2023. It was a bittersweet balance. Despite the Government announcing over-compliance in fiscal metrics in 2023, posting a fiscal deficit of 4.2% of GDP, with a primary deficit reduction from 1% of GDP in 2022 to 0.3% in 2023, the MoF projects a higher fiscal deficit of 5.3% of GDP, which also implies push back in the primary balance progress with a 0.9% deficit for 2024.

Minister Bonilla explained that in 2024, the fiscal revenue will be lower by 1.7% of GDP. Although they will make a reduction in expenditures, the government plan involves maintaining a higher level of spending as a percentage of GDP compared to 2023, aiming to support the economic activity recovery. One part of this spending also involves debt interest payments, which in 2024 will reflect the payment of the Flexible Credit Line with the IMF. The cost of this strategy ends up with the Government abandoning the possibility of having a primary surplus, which also means the increase of the total debt from 52.8% of GDP in 2023 to 57% of GDP in 2024, still below the debt recorded in 2022 but showing that the Government will use a fiscal buffer that could reduce maneuverability in 2025 and 2026.

The good news is that the Government is committed to the fiscal rule; they reduced expenditures given the expected shortfall in revenues, which could suggest that a potential response for a future shock will take the compliance of the fiscal rule as a hard constraint. That said, macroeconomic assumptions for 2024 are apparently conservative. However, we still see some uncertainty around income projected from lawsuits. Another key point to keep an eye on is the fund for stabilization of gasoline prices (FEPC). Increases in gasoline prices already ended, but diesel price increases are under negotiations, and the spending derived from the deficit of FEPC could also impact in either direction depending on the advance in the negotiation with truckers associations.

Given the previous context, the Government is also trying to act at the limit of the fiscal rule as a commitment to improve the budget implementation in 2024. That said, we don’t expect the Government to deliver a lower fiscal deficit if there is additional fiscal revenues.

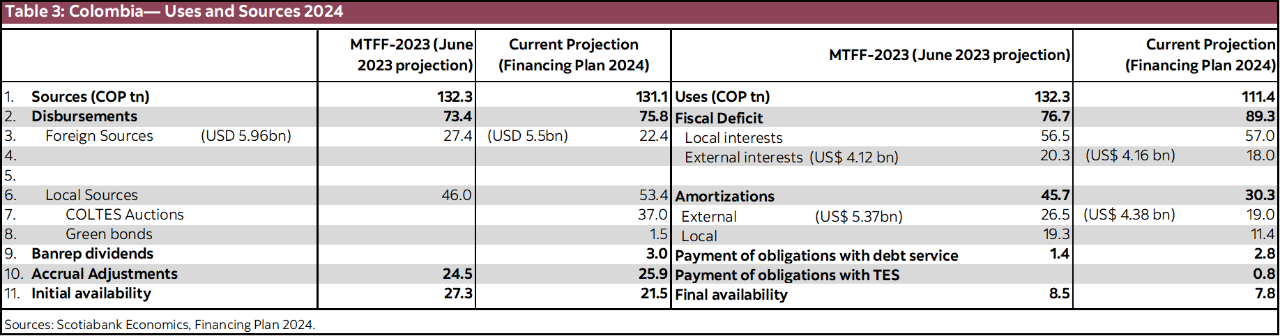

Coltes issuances will be higher COP 37 tn vs COP 34 tn. However, the supply impact would not be a big issue in the context of an ongoing easing cycle in the monetary policy. However, in the medium term, high debt burden and ongoing debt swaps could lead to a structurally more steep yield curve. Some preliminary information from the market makers meeting suggests that the issuance scheme will remain the same during February with on-the-run references in the nominals space COLTES 2023, COLTES 2042, and COLTES 2050, and in linkers COLTES UVR 2029, COLTES UVR 2037 and COLTES UVR 2049, however, the MoF is considering making some tweaks.

In the context of international markets, the MoF showed the willingness to issue around USD 2.5 bn in external debt; the timing for this operation will depend on the market’s environment. However, the Government is also trying to diminish the reliance on external debt to contain potential impacts from FX volatility in their accounts.

Further details about the Financing Plan of 2024

- Macroeconomic assumptions: The 2023 economic performance was weaker than expected, which produced a lower tax collection and is generating a lower base for an increase of tax revenues in 2024.

That said, 2024 macroeconomic forecasts are conservative (table 1), and FX projection is apparently high; however, it could not represent a game changer for 2024 projections. We must keep an eye on the evolution of tax collection from DIAN, especially in April, when businesses have a significant season of tax payments, and between August and September, when individuals pay taxes.

During the press conference, Minister Bonilla said inflation is expected to go down from the current 9.28% to 6% in December 2024, which, in his opinion, supports a reduction in the monetary policy rate to around 8% at the end of the year, above our forecast of 7%.

- Preliminary Fiscal Results in 2023:

Colombia complied with the fiscal rule in 2023. Despite the challenging context in the economic activity and having fallen short in GDP projections, the negative effect of having a lower tax collection was compensated by lower spending. Most of this lower spending was due to a reduction of 0.5% of GDP in interest payments due to the COP appreciation and liability management operations made by the treasury. In addition, Minister Bonilla confirmed that there was an implementation of the budget of COP 17 tn (~1.1% of GDP) in the National Government Accounts, while for the Central Government, the under execution was of COP 8 bn (0.5% of GDP).

In 2024, the Government wants to improve budget implementation. It probably means pursuing an active spending policy in which this positive surprise of a lower deficit in 2023 won’t be repeated in 2024. The fiscal deficit stood at 4.2% of GDP, below the previous projection of 4.3% of GDP, which was compatible with a primary deficit of 0.3% of GDP, above the previous projection of a neutral balance of 0% of GDP, but lower than the deficit recorded during 2022 of 1% of GDP. That said, the debt-to-GDP ratio for the central Government stood at 52.8% of GDP, below the 55% long-term anchor established in the Fiscal Rule. All of the above suggest an over-compliance with fiscal targets.

- Fiscal Plan for 2024:

The deficit will increase amid a weaker economic and oil price cycle.

The MoF expects a still challenging macroeconomic environment in 2024. Fiscal income and expenditures were revised to the downside this year. Tax collection will reflect the impact of lower economic growth and lower income from lawsuits; meanwhile, expenditure reduction is a response to lower-than-expected tax collection amid the court’s decision about the deductibility of royalties from income taxes of oil and mining companies. The previous adjustment demonstrates that the Government is willing to adjust its plans to comply with the fiscal rule if circumstances change (table 2)

An additional ingredient in this publication was that given an expected weak economic activity and a weak cycle in oil prices, the fiscal rule allows the space for a higher fiscal deficit. Having said that, the fiscal deficit will increase from 4.2% of GDP in 2023 to 5.3% of GDP (chart 1), which involves having a 0.9% primary deficit. Our take on that is that the Government will act within the limit of the fiscal rule, and in that sense, if fiscal revenue doesn’t evolve as expected, fine-tuning is critical. The main concerns in terms of revenues are around tax collection amid weaker economic growth in 2023. Companies could give a sense of that in April, while individuals could still contribute positively between August and September since tax payments in 2024 will start to reflect the effect of the fiscal reform of 2022. In terms of net debt, net debt will jump again during 2024 to 56.9% of GDP (chart 2).

- Financing Plan 2024:

According to the Head of Colombia’s Treasury and Public Credit, José Roberto Acosta, higher local debt issuance will mostly support the increase in financing needs. COLTES auctions will increase from COP 34 tn in 2023 to COP 37 tn in 2024 (table 3), which includes green references. Total COLTES auctions will represent 22.05% of GDP in 2024, which is 0.59% higher versus 2023, which suggests that it is a decent amount. However, the supply effect at the long end of the curve, assuming that the MoF will continue doing liability management operations (debt swaps), leads us to think that the curve should remain steep even after the end of the easing cycle in the monetary policy.

Regarding external markets, issuances will be relatively moderate, with a total of USD 5.5 bn and around USD 2.5 bn in external debt issuances. The Government said it will continue studying the possibility of having thematic bonds (green and social). However, further details still need to be provided.

During February, auctions will remain as announced at the beginning of the year; however, the MoF is considering changing medium-term references in the nominals’ curve.

A final interesting point is that Final cash availability is expected to close 2024 in COP 7.8 tn, which is compatible with an expectation of having a very active government pursuing budget implementation.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.