- Chile: Healthy GDP adjustment next year, after a better-than-expected 2022

- Colombia: Inflation to remain elevated in 2023, with restrictive rates throughout the year

- Mexico: Shadow of potential US recession clouds Mexican outlook, but hope remains

- Peru: Unlike politics, the economy is poised to stabilize in 2023, albeit at levels that combine low growth and high reference rate levels

- Brazil: Year-ahead filled with challenges, but rate cuts will eventually provide the economy with important relief

In this report, our local economists present their views for 2023 as well as recapping the drivers of growth in 2022 that, in some cases, are quickly fading and leaving the strong COVID-19 recovery behind for a period of slow growth in the best of cases to a recession at worst.

Economic adjustments are expected in coming quarters. This expectation is also a hope. The threat of runaway inflation has not fully faded and a scenario where inflation does not sufficiently converge to central banks’ targets will keep rates higher than we may have anticipated in the past—possibly worsening the medium/long-term prices outlook as investment plans suffer and production capabilities fall behind. Early signs that inflation has clearly crested can be observed in some countries, however.

We see regional policy rates eventually falling later this year as inflation eases with some banks facing more pronounced economic malaise and cutting sooner and faster(Chile) while others are faced with robust growth and country-specific factors that complicate their goals and see them keep policy rates in double digits by year-end (Colombia).

Political risks may limit investment in some of the countries that we study with Peru currently mired in a particularly unstable political moment that may see early elections next year (though the new government wants these in April 2024); mining policy will be key. Brazil’s Lula will take another crack at the presidency with markets hoping that he will moderate his leftist goals (or Congress will force him too) once inaugurated, while Mexico’s policies deterring foreign investment in specific sectors or clashes with trade-deal partners could continue to broadly limit capital spending in the country—despite ‘nearshoring’ opportunities.

Throughout all of these local developments, the global outlook with a possibly faster Chinese reopening, decisions from the globe’s top central banks (namely the Fed and the ECB), and the energy and food prices backdrop are additional factors contributing to Latam economic uncertainty ahead.

—Juan Manuel Herrera

CHILE: HEALTHY GDP ADJUSTMENT NEXT YEAR, AFTER A BETTER-THAN-EXPECTED 2022

The economy should end 2022 better than expected a few months ago, mainly thanks to a good performance in private investment, set to grow in the current year. However, a healthy contraction of GDP is expected for 2023. Inflation has slowed, driven by a stabilization of the Chilean peso (CLP) and reduced domestic demand activity in the face of a very restrictive monetary policy rate, which has reached 11.25%. In light of this, the central bank will begin rate reductions in 2023.

We project GDP growth of 2.7% in 2022, higher than previously seen, namely due to a better performance of investment-related services in recent months. The adjustment in private consumption continues, while investment has surprised positively thanks to greater dynamism both in machinery and equipment, and in construction. At the same time, fiscal spending is estimated to decline by around 24% this year.

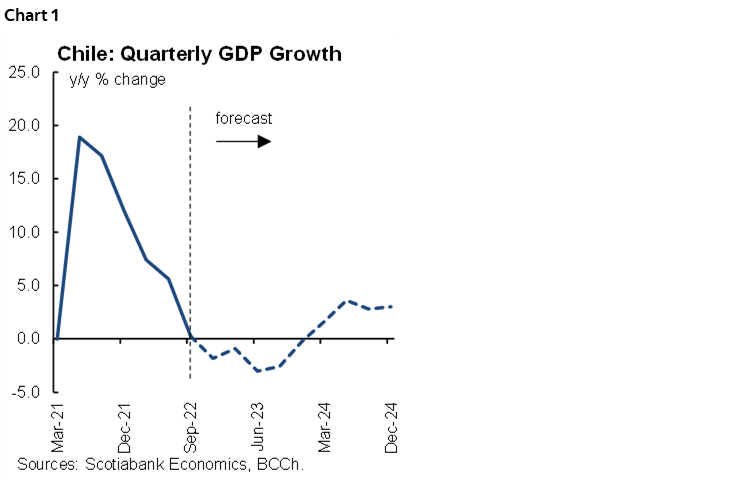

In line with a necessary adjustment towards trend, we project a contraction in GDP of 1.7% in 2023 (chart 1), in large degree owing to high comparison bases (following the pension-withdrawals sugar-rush) alongside weaker demand in consumption and investment. On the other hand, the trade balance should contribute positively to GDP growth next year, while fiscal spending should climb by a sustainable rate of around 4%. In 2024, GDP is forecast to expand by 2.8%, close to its long-term rate of growth.

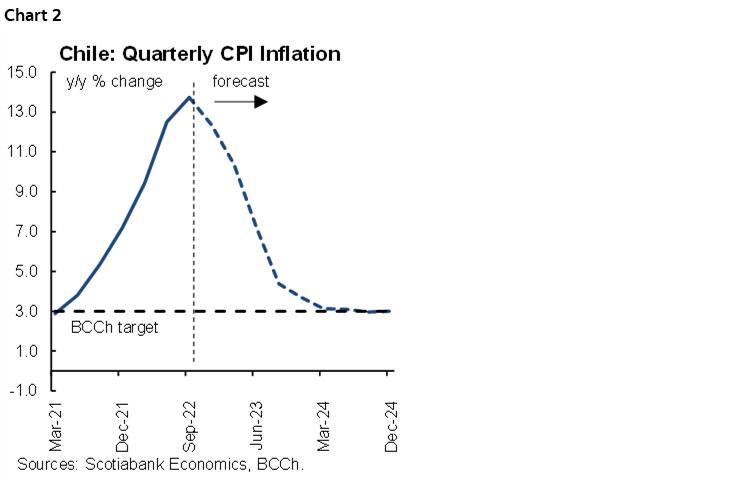

We expect a sharp slowdown in inflation to 3.7% y/y by the end of 2023 (chart 2). Inflation has been slowing in recent months, after reaching 14.1% y/y in August. In tandem with prices volatility, core inflation has slowed down in goods and services, reflecting a stabilization of the CLP (and marginal gains), flat-lining domestic demand growth and job destruction (mainly formal) in the past two months. Taking the above into account, inflation expectations are falling, both those implicit in asset prices and those reflected in surveys.

In our view, the main determinants of headline inflation point to a sharp slowdown in price increases in coming months to close 2022 at 12.4% y/y to then slow considerably, to 3.7% y/y in December 2023. Our scenario assumes no new supply interruptions that would impact commodity prices—mainly those of food and energy—and the absence of new pension fund withdrawals. At the same time, it is consistent with an appreciation of the CLP towards 850 at the end of 2023 and 750 at the end of 2024. Regarding the CLP, our scenario assumes that structural reforms sought by Boric’s government (tax and pensions) will be moderated (i.e. watered-down) by Chile’s and the new constitutional process will be devoid of extreme proposals, which should reduce the risk ‘discount’ that markets have imposed on the currency.

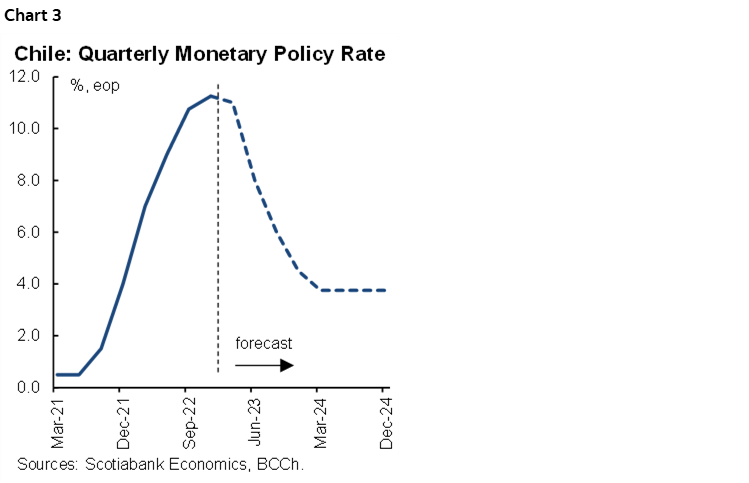

The central bank will begin reference rate cuts in the first quarter of 2023. We reaffirm our view of a cut in the reference rate in January, although to a lesser extent than we had previously expected, both due to the greater volatility that we have observed in recent inflation data and a greater sense of persistent or sticky inflation. In addition, the central bank revised upwards its level of the neutral monetary policy rate, from 3.50% to 3.75%. Thus, we expect a 25bps rate cut at the January meeting and more cuts over the course of the year, to bring the policy rate to 4.50% by the end of 2023 (chart 3). Note that we continue to see an easing path that is significantly more aggressive than the one implied by swap rates, surveys, and the one expected in the center of the central bank’s projection corridor in its latest Monetary Policy Report (around 9% at end-2023).

—Aníbal Alarcón

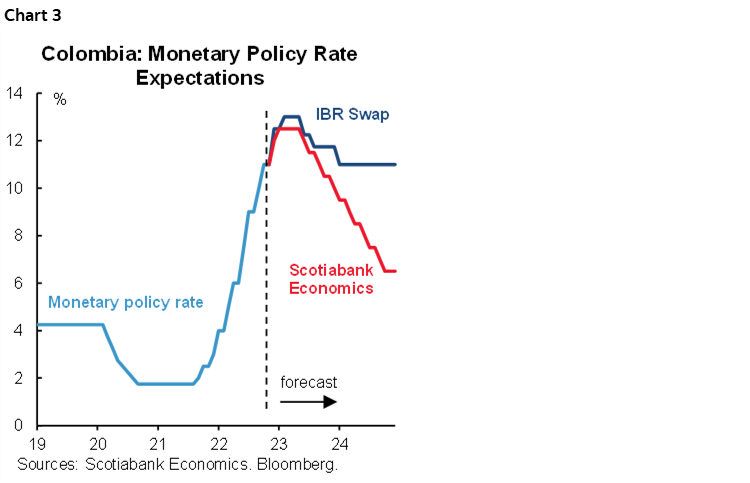

COLOMBIA: INFLATION TO REMAIN ELEVATED IN 2023, WITH RESTRICTIVE RATES THROUGHOUT THE YEAR

Despite markets and economic agents thinking that risks for 2022 were relatively muted in comparison to the pandemic shock, the world, in fact, faced significant disruptions. The base case scenario for 2022 pointed to a normalization in economic policies in combination with the consolidation of economic reopenings around the globe and inflation was expected to normalize as supply chain issues corrected. However, Russia’s invasion of Ukraine and the still-strict lockdown measures to contain COVID-19 in China worsened price shocks, lifting global inflation close to a thirty-year high.

Colombia started 2022 with a full reopening of the economy, allowing in-person activities in schools and offices early in the year. Economic activity indicators showed a strong recovery, demonstrating the resilience and adaptability of the private sector. Services sectors continued outpacing the economy’s overall performance, while mining and construction lagged. From a demand perspective, private consumption has led the recovery. In fact, according to the latest GDP statistics, private consumption is 8.9% above its long-term trend, which would reflect a reduction in household savings but also a positive shock from record-high remittances, which currently represent around ~2.8% of GDP. Meanwhile, investment as of September 2022 remained 12% below pre-pandemic levels, reflecting soft construction sector activity.

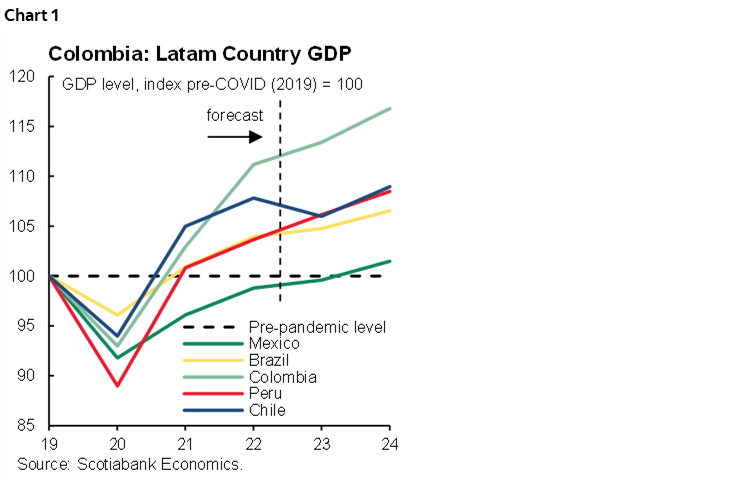

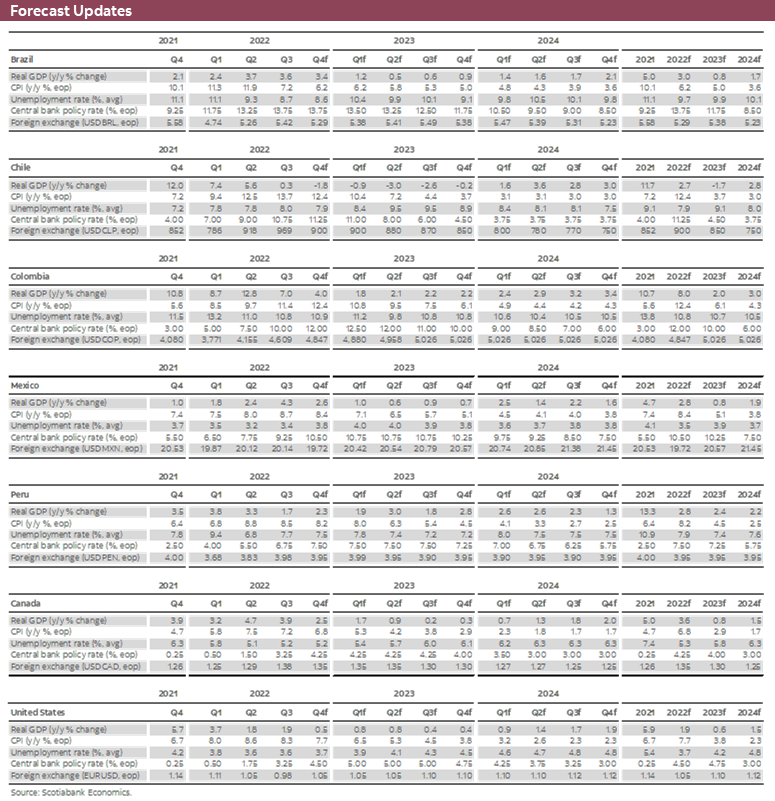

In any case, Colombia is the year’s best performer in terms of growth in the PAC + Brazil group (chart 1). In 2022, economic growth is expected at 8.0%, with a strong positive bias. In 2023, economic growth is expected to hover around 2% pointing to a healthy moderation in private demand combined with more modest investment growth. Our projection assumes that households will cool consumption increases in response to the cumulative effect of rate increases and tighter personal budgets due to the impact of inflation on disposable incomes. Overall, the output gap should remain positive over the coming months but is expected to close by the end of 2023.

Inflation increased from 5.62% at end-2021 to 12.53% in November 2022, reaching its highest level since 1999. In the YTD, 21% of the inflation increase is explained by food inflation, which reflects the impact of higher input costs due to the Russia-Ukraine conflict. Around 15% is accounted for by housing-related prices, mainly those that are regulated but also rent fees given indexation effects. The remainder was the result of a combination of strong demand which led to higher services inflation (i.e., restaurants and hotels), but also due to FX depreciation and global bottlenecks—which impacted prices in tradeable goods such as vehicles. All in all, accelerating inflation is not only a result of external shocks but also of robust domestic demand that has allowed the pass through of those supply shocks to prices to be strong.

At Scotiabank Economics, we anticipate that inflation peaked in December at 12.66% (chart 2). In 2023, strong statistical bases will allow a pivot in inflation. At the start of 2022, food inflation of 3.79% m/m and 3.26% m/m in January and February, respectively, and core inflation was atypically high: 1.21% m/m in January and 1.28% y/y in February, due to reversal effect in VAT holidays. This provides a high base off which early-2023 numbers will not look as high. Nevertheless, although headline inflation is seen closing 2023 at 7.51%, average inflation in 2023 will be 10%. Core inflation is expected to close at 6.64% y/y, more than twice the central bank target of 3%. In 2023, indexation effects and FX passthrough will be the main contributors to inflation. Meanwhile, food inflation is set to decelerate from the current 27.08% towards 11% y/y inflation by the end of 2023.

The inflation backdrop leads us to think that BanRep must continue to tighten monetary policy, delivering a 100bps hike in December and a final move of 50bps in January to reach 12.50% as a terminal rate. The rate must remain restrictive until no sooner than mid-2024. That said, gradual rate cuts are not anticipated before H2-2023. By the end of 2023, we expect a 10% monetary policy rate (chart 3), translating into a restrictive 3.7% real rate (using an ex-ante and ex-post average approach) vs the ~2% rate that is considered neutral.

Finally, our outlook for the COP exchange rate involves broad stability from current levels, showing that Colombia is paying a risk premium due to idiosyncratic issues. This involves not only erratic communications from government and the expectation of a less dynamic oil sector but also the fact that the central bank will continue to be perceived as behind the curve and reluctant to intervene in the FX market. A USDCOP level between 4,700 and 4,900 by the end of 2023 is our base case scenario.

—Sergio Olarte, María (Tatiana) Mejía & Jackeline Piraján

MEXICO: SHADOW OF POTENTIAL US RECESSION CLOUDS MEXICAN 2023 OUTLOOK, BUT HOPE REMAINS

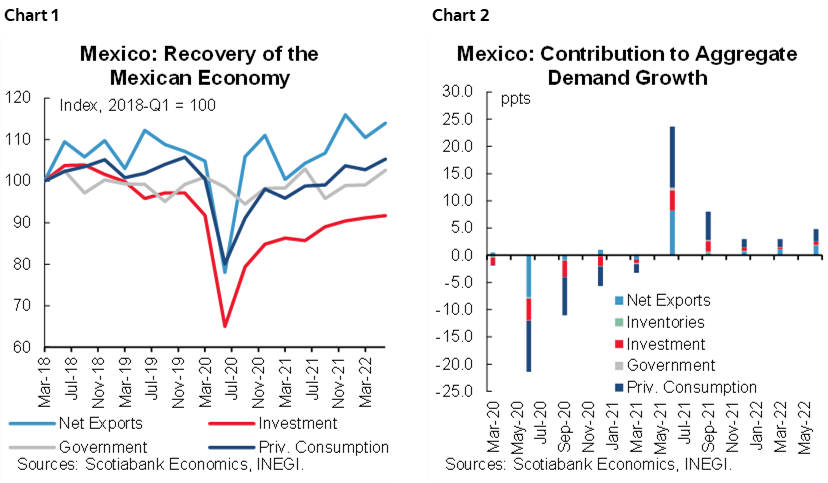

The median forecast for 2023 GDP growth in Mexico is still around twice the rate seen for the US (at just under 1.0% for Mexico compared to 0.4% in the US, from Bloomberg). If Mexico indeed manages to expand materially faster than the US, it will mark an important break from what has been the norm over the past 5 years, where net exports have proven to be the most dynamic engine for the Mexican economic recovery. This time around, it has been net exports with the help of private consumption that have powered the rebound (charts 1 and 2). Note, however, that private consumption has benefited from consistently record-breaking remittances that have acted as a strong tailwind. We estimate that the windfall from ‘excess’ remittances has explained about 1 percentage point per year of the contribution of consumption over the past 3 years. Thus, it can be argued that the major driver of Mexico’s recovery from the COVID-19 economic shock has come from abroad. Jointly, net exports and consumption have explained about ⅔ of the post COVID-19 rebound, while investment, which currently sits at around 2013 levels in real terms remains the main drag.

With investment remaining one of the key headwinds for the Mexican rebound, the opportunities presented from near-shoring are could contribute to Mexico outperforming the US on growth (although the US itself is also “capturing” part of these flows). Can Mexico capitalize on these? The answer is very complex, but the first thing to consider is that FDI does not drive growth. FDI is a balance of payments concept which, even when it rises, does not necessarily mean growth will accelerate. The acquisition of Banamex by Citibank twenty years ago, or the acquisition of Modelo by ABInbev were both FDI flows of over USD10bn, but neither one of these represented investments which would be added into GDP. The investment that matters is that which installs new productive capacity. In Mexico that number is reported in the gross fixed investment data, which currently sits at 2013 levels in volume terms. It is possible that with near-shoring that number accelerates, and could explain why Mexico may outperform the US, but there are a number of factors that will be key to boost fixed investment:

- Confidence: Many sectors in the Mexican economy continue to run very smoothly, and free of any direct interference by the government—manufacturing and agro-industry are both in this group and have been among the most dynamic of the post-COVID-19 recovery. Investment in these sectors where confidence has not been shaken could be one of the drivers of a resurgence in investment. However, each of these two sectors faces an important challenge. For manufacturing, this is access to power, and for agro-industry access to water is increasingly ’flashing red’ (it’s still not a ‘macro level’ risk, but we saw a water conflict at the centre of the cancellation of the USD1.5bn Constellation brands plant in Mexicali, and earlier this summer for Casa Madero—the oldest vineyard in the Americas, among others).

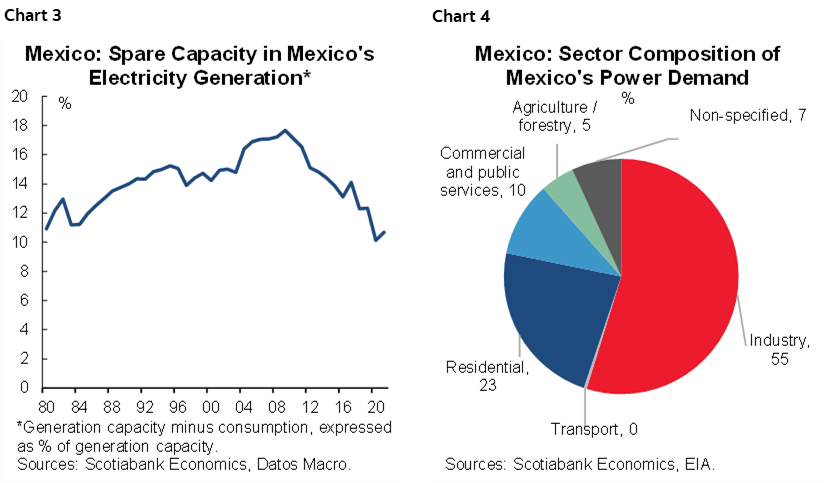

- Energy policy: The conflict between the government and private energy generators is well documented and is now at the heart of an early-stage ‘state-state’ dispute between Mexico vs Canada and the US under USMCA. With uncertainty facing the sector, investment has been stagnant and today spare power generation capacity in Mexico sits at a four-decade low. Industry consumes 55% of Mexico’s power, so this is clearly a risk (charts 3 and 4).

We continue to see Mexico’s 2023 growth at just under 1.0%, but the balance of risks is currently skewed to the downside. However, there are also a few bright spots. Markets are anticipating that Banxico will start cutting rates around mid-2023, cutting 150bps over the next 12 months. The easing of monetary conditions will provide some relief to growth. Another potential positive could be the elimination of uncertainty in the energy sector—this would come if an agreement is reached and regulations around investment in the sector are clarified in a way that is appealing to capital.

—Eduardo Suárez

PERU: UNLIKE POLITICS, THE ECONOMY IS POISED TO STABILIZE IN 2023, ALBEIT AT LEVELS THAT COMBINE LOW GROWTH AND HIGH REFERENCE RATE LEVELS

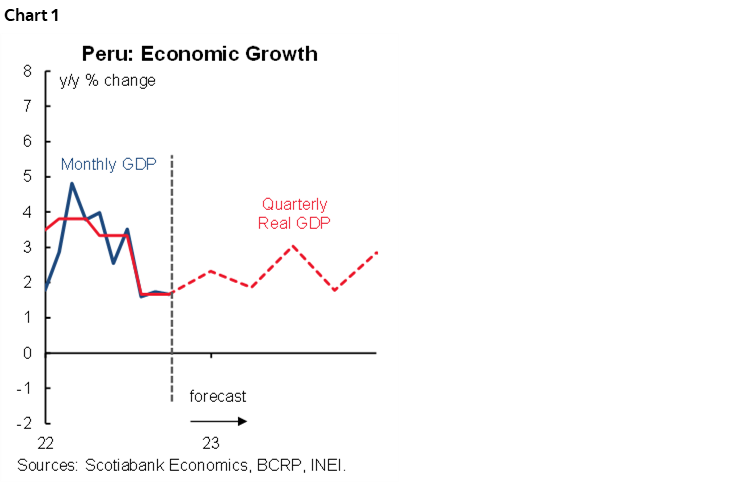

We expect GDP growth of 2.4% in 2023 (chart 1). On the face of it, this does not seem all that bad. Note, however, that we expect domestic demand growth to be a paltry 1.3%. Growth will be led by exports, up 7.6%, and to a lesser extent by consumption, 2.5%. The increase in exports is due mainly to greater copper output as the new Quellaveco copper operation comes fully on stream. Agro-industrial exports growth will help somewhat as well. Quellaveco’s economic contribution is huge, however. Without it, GDP growth would be somewhat below 2.0%.

Our concern, as always, is private investment, which we expect to decline by 3.6%. Political turbulence will prevent new mining investment in particular, despite a host of potential projects. We also expect public investment to decline, falling 1.5%. Once again, political turbulence does not make for a smooth spending agenda. Moreover, newly elected regional and local authorities will take office in January, which in the past has been a harbinger for a decline in public investment.

Consumption just might hang in there, as the labour market has been performing moderately well. However, consumption will begin to depend only on the jobs market as there have been no indication by authorities of possible new access to pension fund resources or large transfers which drove strong consumption growth in the past.

Note that these forecasts were made when Castillo was still President and before the latest round of political instability, so the level of uncertainty regarding our forecasts are higher than usual.

Fairly contractionary monetary policy will not help (chart 2). Inflation seems stuck above 8% and although we do expect inflation to decline progressively to 4.5% in 2023 (chart 3), this is still high enough to warrant the BCRP keeping rates high for most of the year. We believe the BCRP may keep the reference rate at its current 7.50% in January, although an increase to 7.75% is conceivable, to then leave the rate at this terminal level until late-2023.

The PEN has shown remarkable resilience to political events recently, although one must credit BCRP intervention to calm down the volatility in the market. It’s not easy to judge the PEN’s performance in 2023. Fundamentals point to a stronger PEN. But, if political turbulence increases, fundamentals could take a back seat to political risk. Our forecast of USDPEN3.95 at year-end 2023 tries to balance the two.

Macro balances will remain Peru’s strong point. Even if the fiscal deficit rises, as we expect, to 2.4% of GDP, this is still manageable. External accounts, especially the trade balance, will also be very positive in 2023. Less so than in 2022, but with a surplus that will still be one of the highest ever. Metal prices appear to no longer be falling. And then there is the added copper output thanks to Quellaveco.

A final word on politics: anything can happen. There is a good chance that Peru will have early elections, with a new president and Congress, as soon as 2023, or possibly in 2024. The path forward will be an unstable one, whatever the final outcome.

—Guillermo Arbe

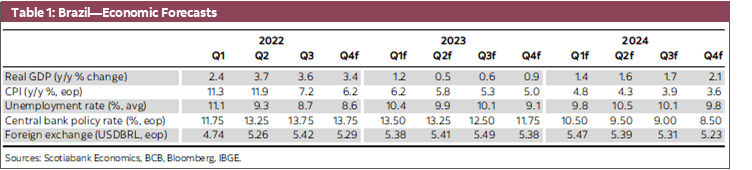

BRAZIL: YEAR AHEAD FILLED WITH CHALLENGES, BUT RATE CUTS WILL PROVIDE THE ECONOMY WITH IMPORTANT RELIEF

The Lula Administration 2.0 kicks off facing a series of uncertainties that need to be resolved in a challenging environment. Chief among them is tacking the country’s fiscal challenges, which can be summarized as the country has a 100% gross public debt/GDP ratio, of which close to ¼ needs to be rolled over on an annual basis. The importance of tackling this fiscal risk is exacerbated by a global environment of much higher interest rates which, barring some sort of solution, will mean that over one fifth of Brazil’s GDP could be put towards paying interest rates and pensions—neither of which add to future growth in the country. Besides this fiscal obstacle, Lula will find a very polarized country with a fragmented legislative, with which he will have to create a consensus to move through his agenda. Our take is that tacking to the centre could be a way to selectively secure issue-specific support from centrist parties (MDB, and potentially even the PSDB, PSB, and MDB).

The good news is that outside of fiscal challenges, and dealing with a very polarized country, some of the macro data suggest the shocks faced by the economy in 2022 are starting to improve, including inflation which now sits just under 6.5% y/y, after peaking at 12%. This could allow the BCB to start easing monetary conditions as soon as the first quarter of 2023. In a country with a low average debt maturity (around 4 years) and high credit penetration (domestic credit to the private sector of around 70%), this will be good news on the growth front. It’s worth bearing in mind that with the rapid spike in interest rates, the private non-financial sector’s debt service ratio in Brazil has risen from around 17% in 2020, to over 22% in 2022. This rapid spike in interest costs will erode both investment and consumption, and its looming decline will provide important relief. We still expect a bit of a ‘growth hangover’ in 2023, partly driven by political uncertainty stalling investment. However, as we near the end 2023 and into 2024 the growth outlook will look sunnier (table 1).

—Eduardo Suárez

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.