- The Latam region continues on the path of economic recovery. But recent developments underscore that uncertainty remains with respect to near-term economic prospects.

- There is less uncertainty regarding the direction of prices. Higher inflation has elicited policy rate hikes across the region.

- And with uncertainty about the persistence of inflation and the underlying resilience of the recovery, things are getting interesting for central bankers.

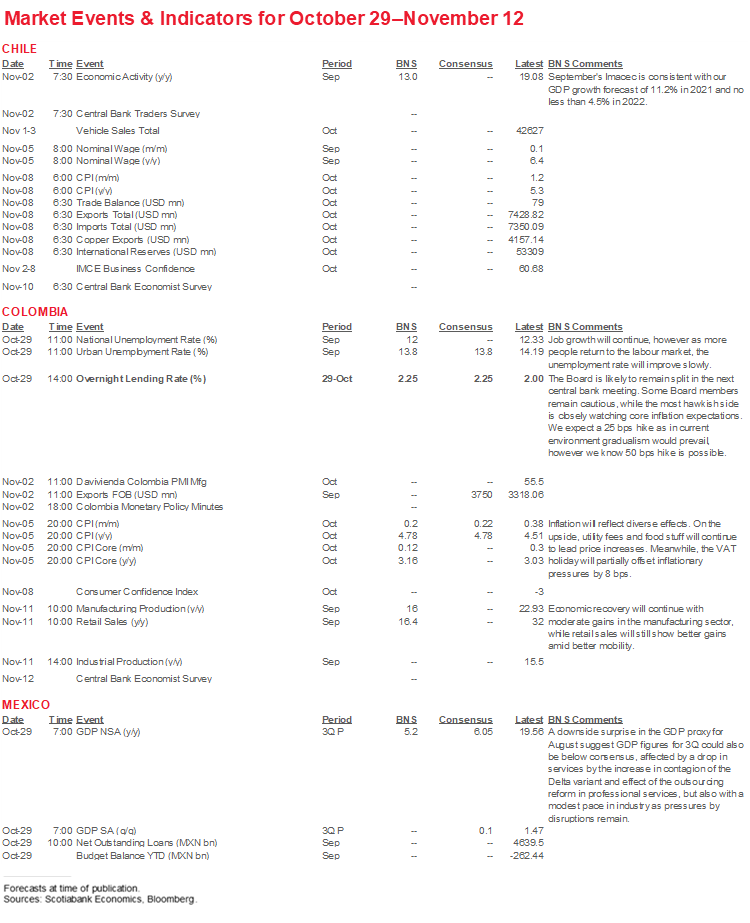

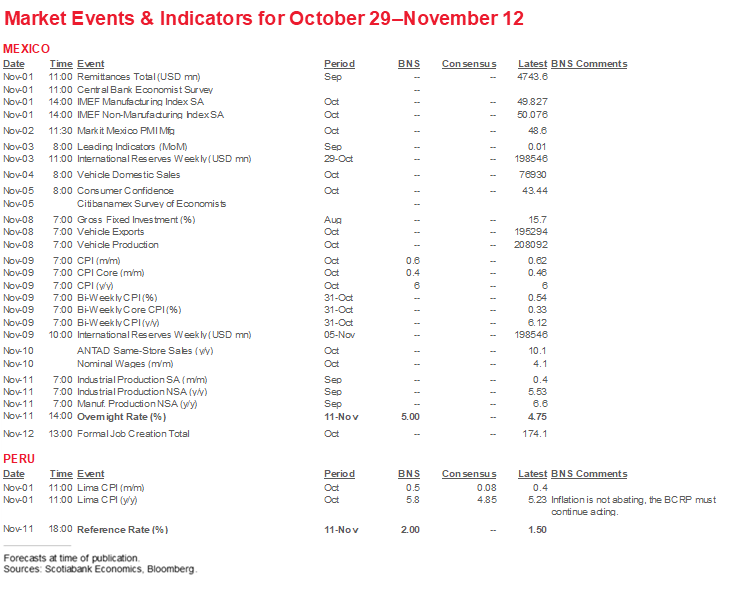

KEY ECONOMIC CHARTS

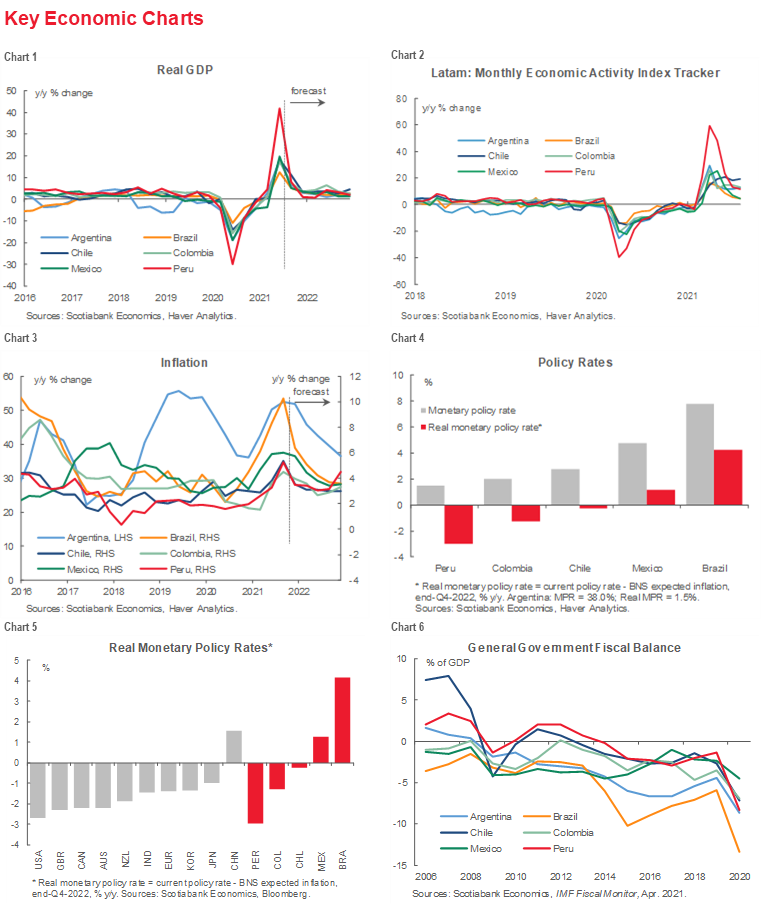

While the economic recovery remains on track across the Latam region, recent developments underscore the uncertainty that clouds the near-term outlook. The bounce back in real GDP that marked the first half of 2020 is expected to moderate over the near term, converging on pre-pandemic growth rates (chart 1). This pattern reflects the return of economic activity to pre-pandemic levels and the waning of base effects on year over year growth rates. Monthly leading indicators provide a preview of this process, with a deceleration evident across most of the region (chart 2). Chile, where the monthly activity index remains elevated, is the exception.

Recent developments complicate the narrative. For example, in Colombia, data on August economic activity, which fell -1.9% m/m on a seasonally-adjusted basis, suggests the recovery still faces challenges, even as the Citi survey of expected growth improved again, increasing to 8.71% y/y, up from 8.26 % y/y. Meanwhile, in Chile, the municipality of Santiago walked back its full re-opening under the “Paso a Paso” plan in the wake of a rise in COVID-19 cases and test positivity rates, despite a truly impressive vaccine rollout. And in Mexico economic activity surprised on the downside in August, with the seasonally adjusted economic activity index declining -1.6% m/m (versus 0.2% m/m consensus). The upshot here is that there is increased uncertainty about near-term growth prospects.

In contrast, there is far less uncertainty about the short-term outlook for inflation, which has risen sharply across the region (chart 3). That increase has elicited Latam central banks to tighten policy. Unwinding the extraordinarily expansionary monetary conditions introduced to combat the economic and financial effects of the pandemic will take time. And while policy rates across the region have moved higher, apart from those in Brazil and Mexico, they remain negative in real (adjusted for inflation) terms (chart 4).

On this basis, central banks are not out of sync with central banks around the globe (chart 5). Indeed, Brazil and Mexico stand out in terms of proactive rate hikes; other Latam central banks will have to follow their lead once advanced economies’ central banks move towards a rebalancing of monetary conditions.

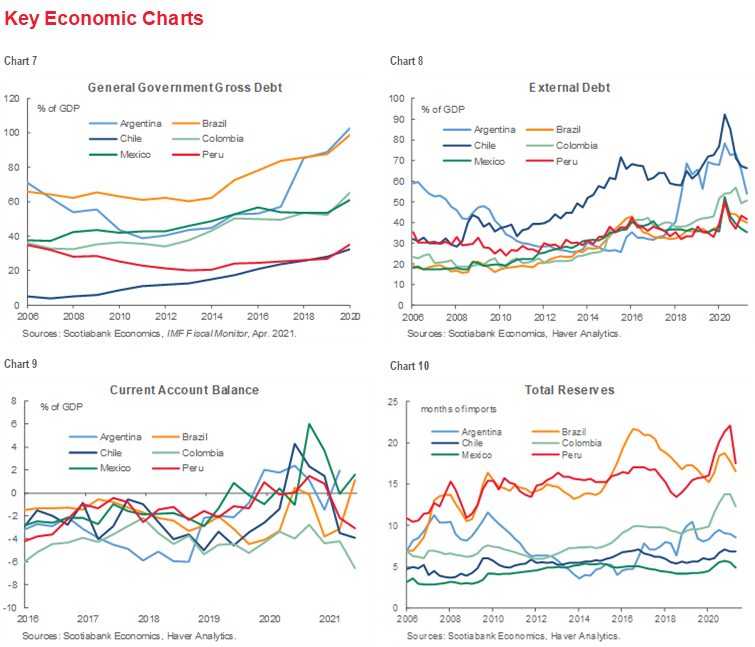

Fiscal policy has also been used aggressively throughout the pandemic, generating large fiscal deficits (chart 6). Markets have thus far readily digested the resulting increase in gross debt (chart 7). However, in the absence of clear, credible plans to preserve fiscal sustainability investors could begin to price in higher risk premiums, leading to an increase in borrowing costs.

Such concerns could become elevated should indicators of external sustainability also deteriorate. For now, external debt (chart 8), current account balances (chart 9), and total reserves (chart 10) do not point to specific risks. External debt burdens have come down from pandemic peaks. And current account balances have improved in Argentina, Brazil and Mexico. That being said, the continued widening of current account deficits (and how they are financed) in Chile, Colombia and Peru may garner closer attention by investors. In contrast, total reserves have either increased or have been flat.

KEY MARKET CHARTS

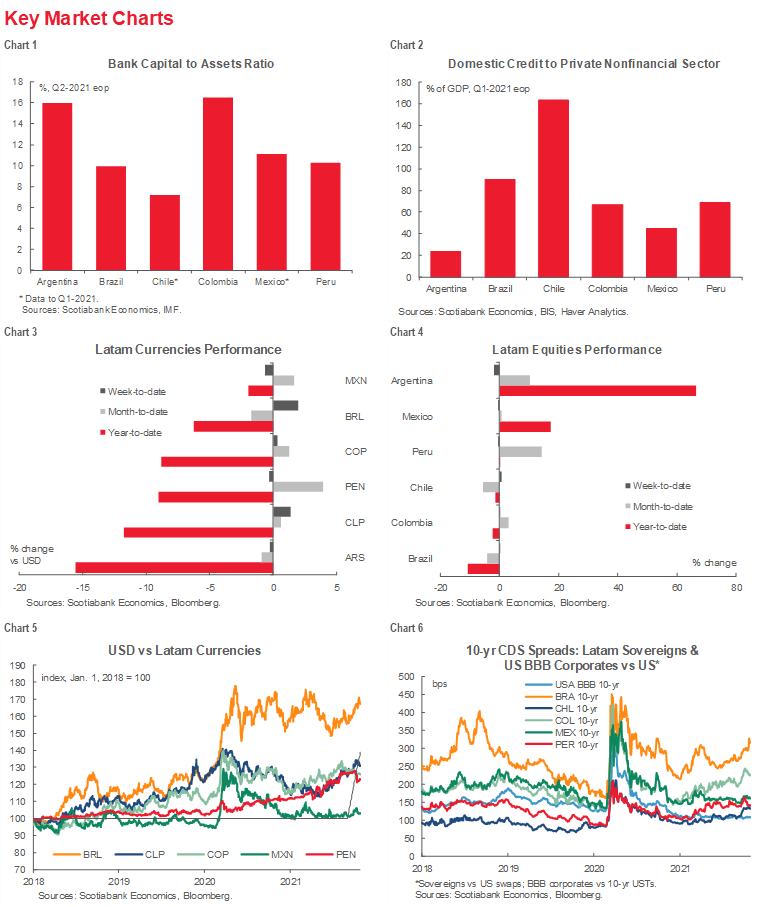

Financial markets have been broadly stable in recent weeks. Latam currencies, which have generally depreciated against the US dollar over the year, have been relatively flat in recent days (chart 3). That being said, the Peruvian currency has appreciated over the past month, reversing some of the losses sustained in the run up to, and the period of political uncertainty that followed, the presidential elections. The reduction in political uncertainty that has strengthened the PEN is also reflected the rebound in the equity market in the past few weeks, which has recouped earlier losses (chart 4). The Mexican peso stands out when viewed in a longer time horizon—it has traded within a comparatively narrow range (chart 5).

Political factors may likewise help explain spreads on Latam sovereign over US Treasuries (chart 6). Spreads widened in Peru, but also in Colombia (as nation-wide strikes earlier in the year disrupted production) and Brazil, where opposition to the president has led to increased political uncertainty. More recently, Chilean sovereign spreads have widened as accusations of impropriety have been leveled against the president. In contrast, spreads have narrowed on Colombian and Peruvian sovereigns in recent days.

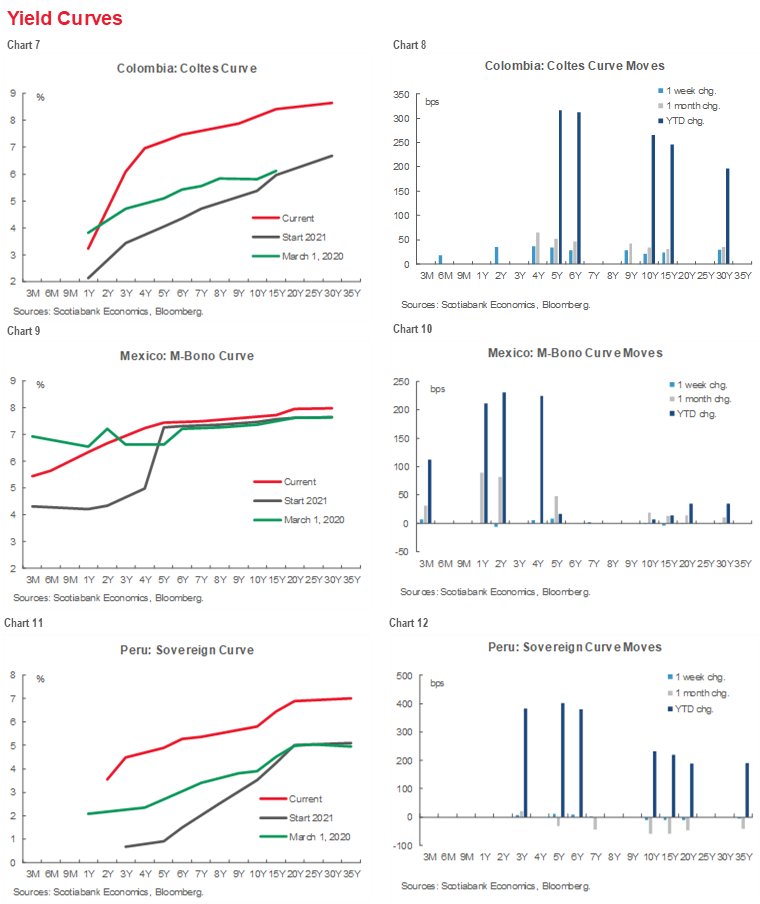

YIELD CURVE CHARTS

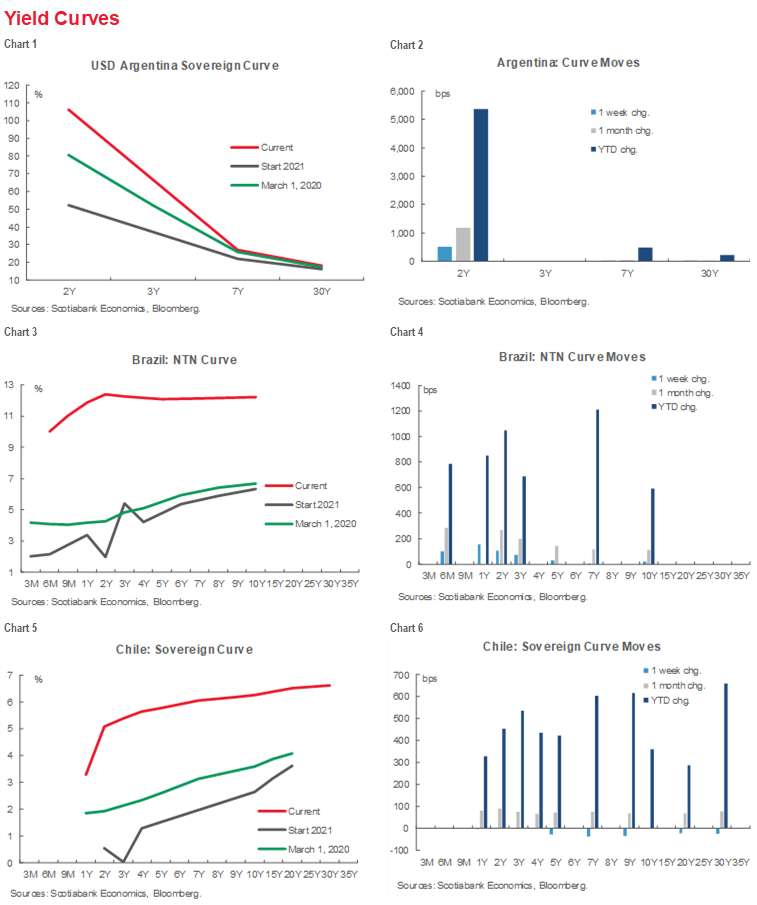

Sovereign yield curves across the Latam region have priced in the progressive rise of inflation and expectations of higher inflation since the start of the year (charts 1–12). For the most part, curves have shifted up across the maturity spectrum. Argentina (chart 1) and Mexico (chart 9), where the Mexico M-Bono curve remains firmly anchored at medium- and long-term maturities, are exceptions. In Brazil, where the BCB raised the Selic rate 150 bps October 28, yields at the short-end of the market have shifted up between 600 and 1,000 bps since the start of the year.

KEY COVID-19 CHARTS

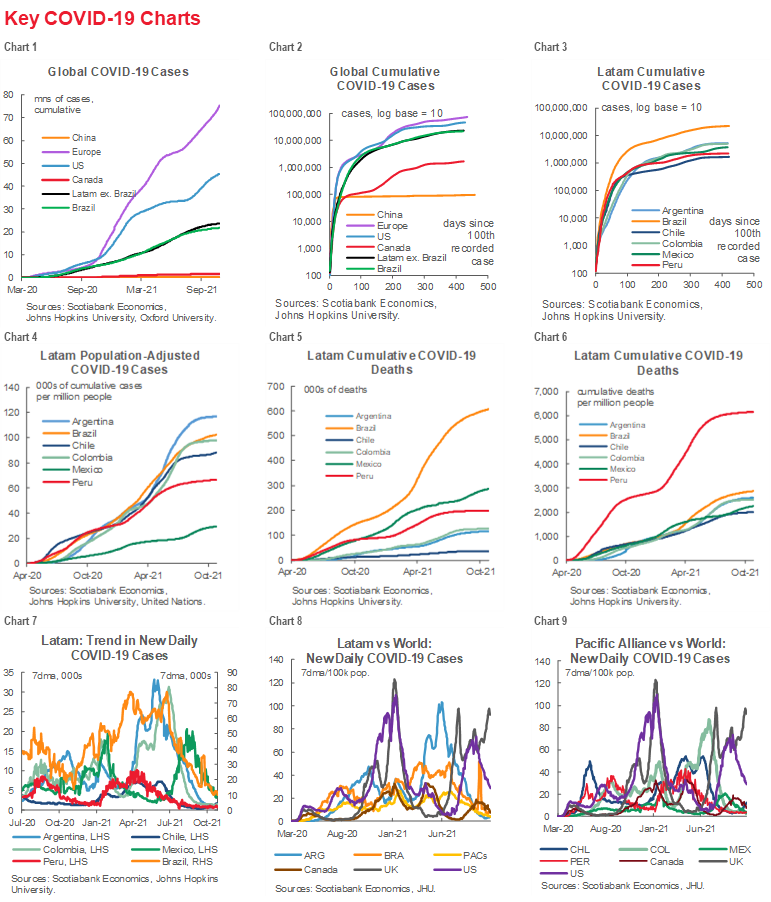

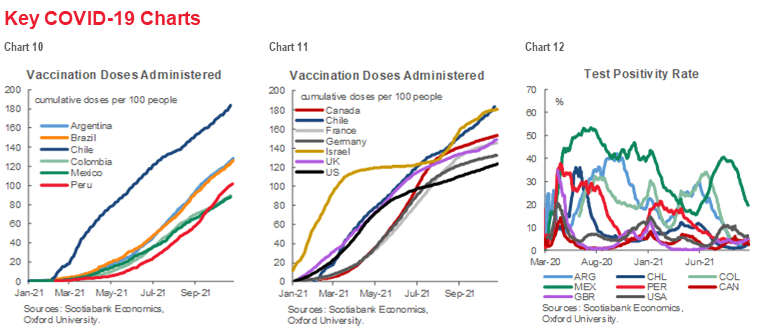

As the reversal of opening initiatives in Chile underscore, the pandemic remains a key driver of economic prospects. Charts 1–12 provide critical information for monitoring COVID-19 developments. In this regard, declines in new daily case counts (chart 7) and test positivity rate (chart 12) are encouraging, notwithstanding the uptick in Chile. So too is the progress made in terms of vaccine rollouts across the Latam region (chart 10). At the same time, the increase in cases in the UK (chart 8), which has a high vaccination rate, clearly demonstrates that the virus continues to pose a threat to recovery.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Forthcoming |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

| COSTA RICA | |

| Website: | Click here to be redirected |

| Subscribe: | estudios.economicos@scotiabank.com |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.