As the COVID-19 pandemic and Latam’s response to it continue to evolve, we are also shifting our coverage of the region in response to requests from our readers. This report marks the first edition of our new Latam Charts Weekly. This pack of figures formerly appeared as an appendix to our flagship Latam Weekly report; it will henceforth be published as a standalone on a fortnightly basis between editions of the parent publication to provide an interim update to institutional investors and corporate clients. Both Weekly reports will continue to be posted on ScotiaView and on our public website.

We highlight six key things about the Latam-6 economies to keep in mind at the midpoint of Q4 as thoughts start turning toward 2021: (1) new COVID-19 numbers are declining in most of the region; (2) economic activity is set to continue recovering into 2021; (3) inflation should remain muted across the Latam-5 inflation targetters; (4) monetary policy is expected to remain stimulative well into next year; (5) the external balance of payments in most Latam countries has weathered the crisis well; and (6) the region’s rates markets have come through 2020 with admirable resilience.

As we sit at the mid-point of Q4-2020 and begin looking ahead to 2021, our charts highlight six key themes that look set to animate the transition in Latam from this most unusual year to the new one ahead.

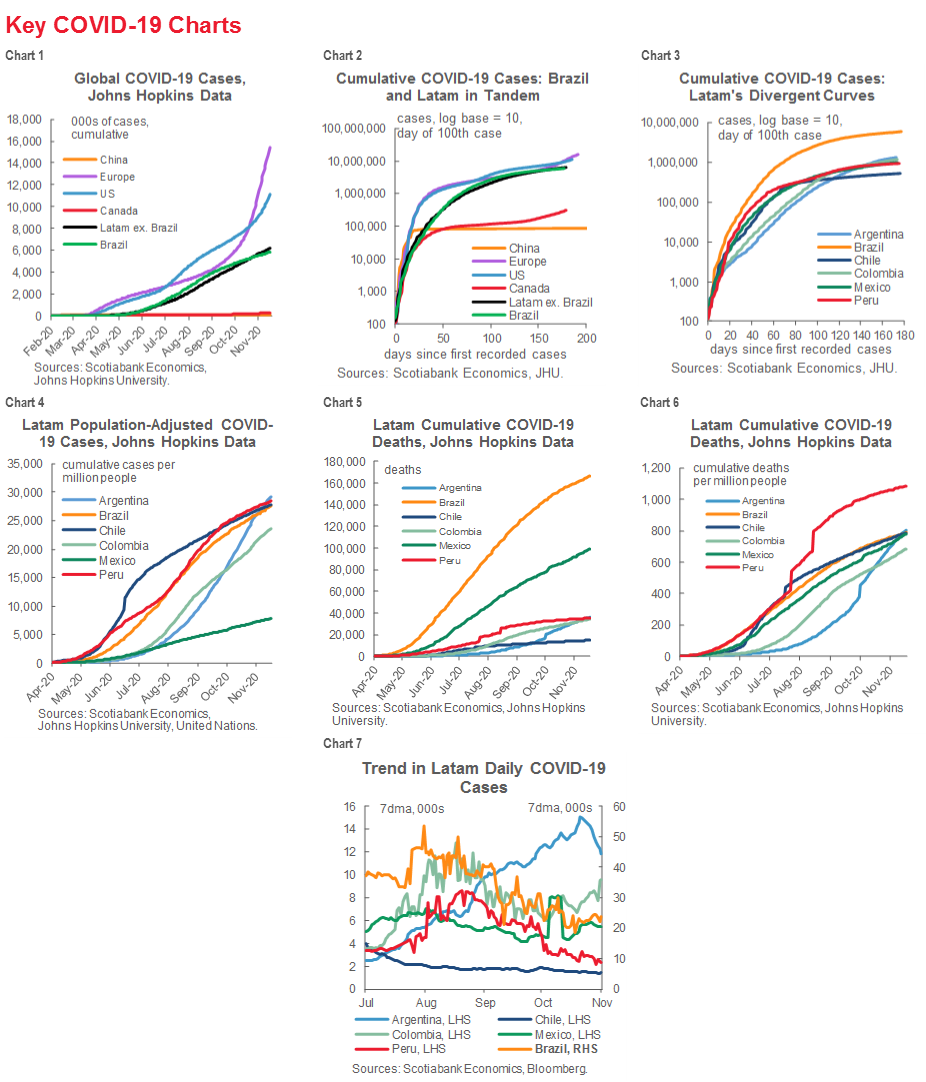

- COVID-19 numbers are surging in second and third waves in Europe, parts of Asia, and North America, but new case numbers are declining in much of Latin America. Our Key COVID-19 charts on p. 9 show that Latam’s COVID-19 curves are now substantially flatter than those in the US and Europe. Argentina’s surge in COVID-19 cases during Q3 stands as the outlier amongst its Latam peers, though numbers have also moved up recently in Colombia.

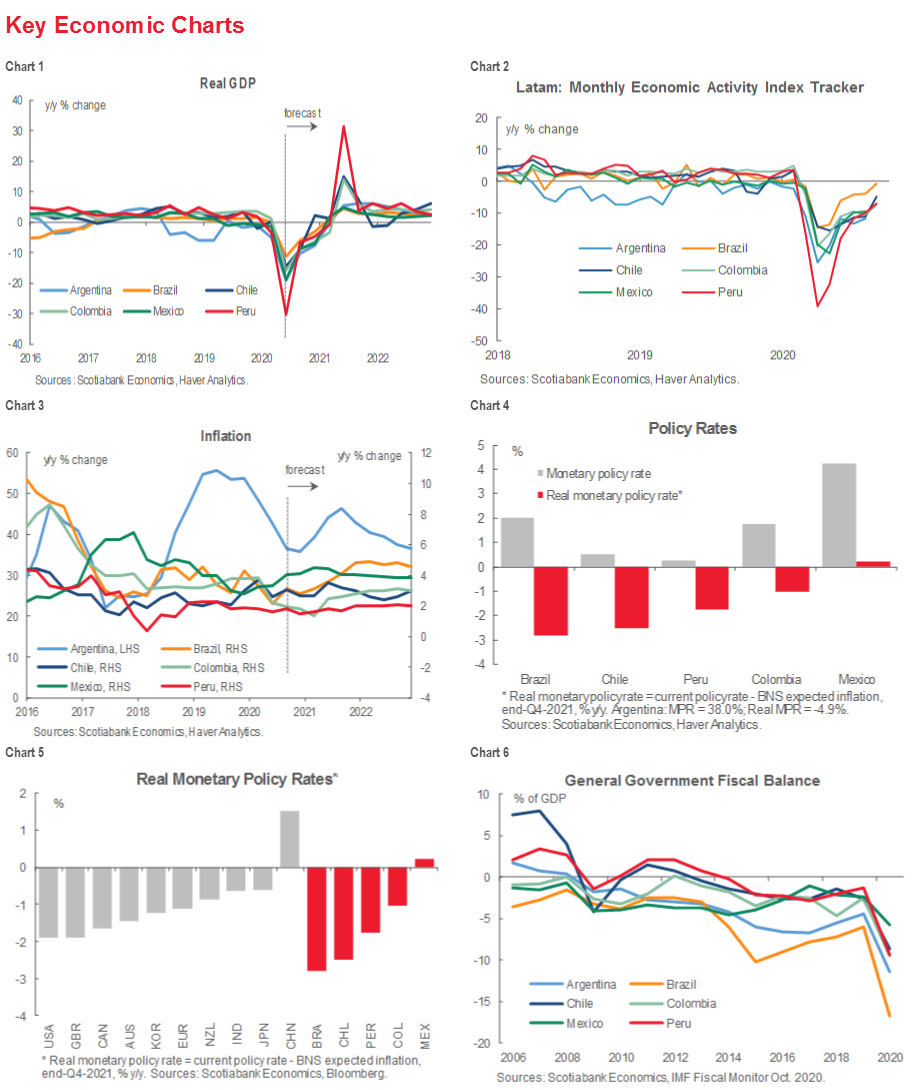

- Economic activity is set to continue recovering robustly into 2021 in most Latam economies. Our Key Economic Charts on pp. 3 and 4 show that monthly GDP proxies put the annual contraction in economic activity at less than -10% y/y in each of the Latam-6 as of September, with Brazil closest to a full recovery at -0.8% y/y. In 2021, we forecast growth to average 4.8% y/y in the Latam-6 compared with 4.0% y/y in the US.

- Inflation is forecast to remain muted in 2021 across the Latam-5 inflation targetters. Headline inflation is set to average 3.35% y/y in the Latam-5, well below the group’s average of 5.33% y/y for 2000 to the present. See chart 3 on p. 3. Argentina is, of course, the exception, with headline inflation set to stay at nearly 43% y/y in 2021.

- Monetary-policy rates in the Latam-5 inflation targetters should be on hold well into 2021. Although real rates are now well into negative territory in four of the Latam-5, with Mexico the one exception (see p. 3), muted price pressures mean that we expect the region’s inflation-targeting central banks to keep their key policy rates unchanged until at least Q2-2021, with Brazil’s BCB expected to lead the normalization of policy with a first hike at that point. Colombia’s data-dependent BanRep is projected to make a first rate increase in Q3-2021; central banks in Chile and Peru are forecast to remain on hold until Q4-2021; and Mexico’s Banxico isn’t expected to hike until early-2022. See our November 14 Latam Weekly for our full forecasts. Again, Argentina is an outlier having just implemented a 200 bps increase in the BCRA’s benchmark Leliq rate in response to headline inflation at over 3% m/m.

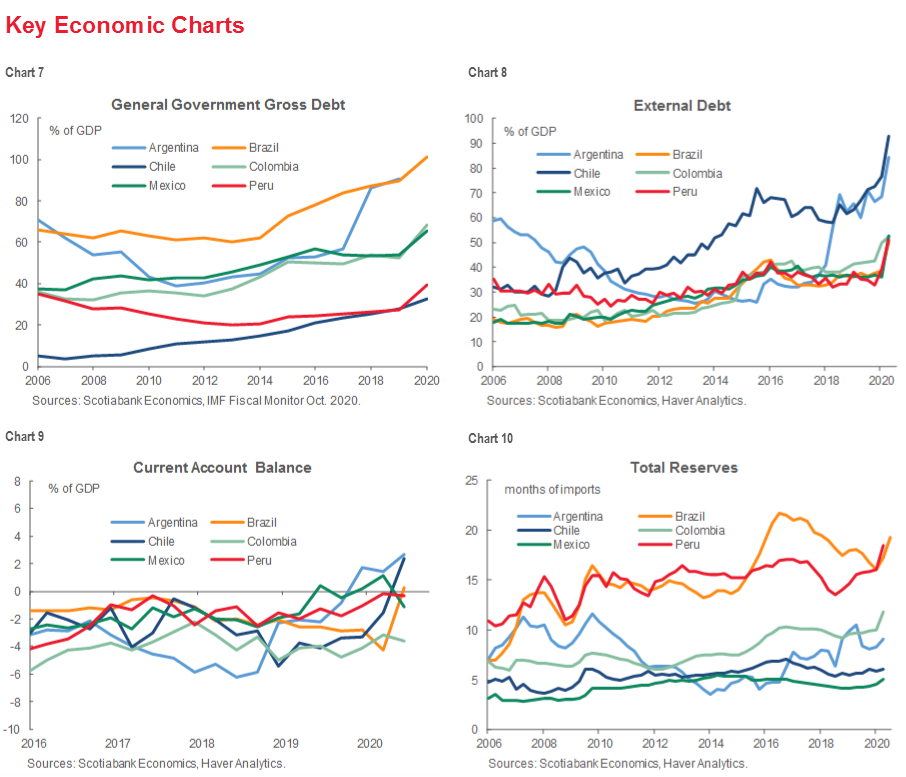

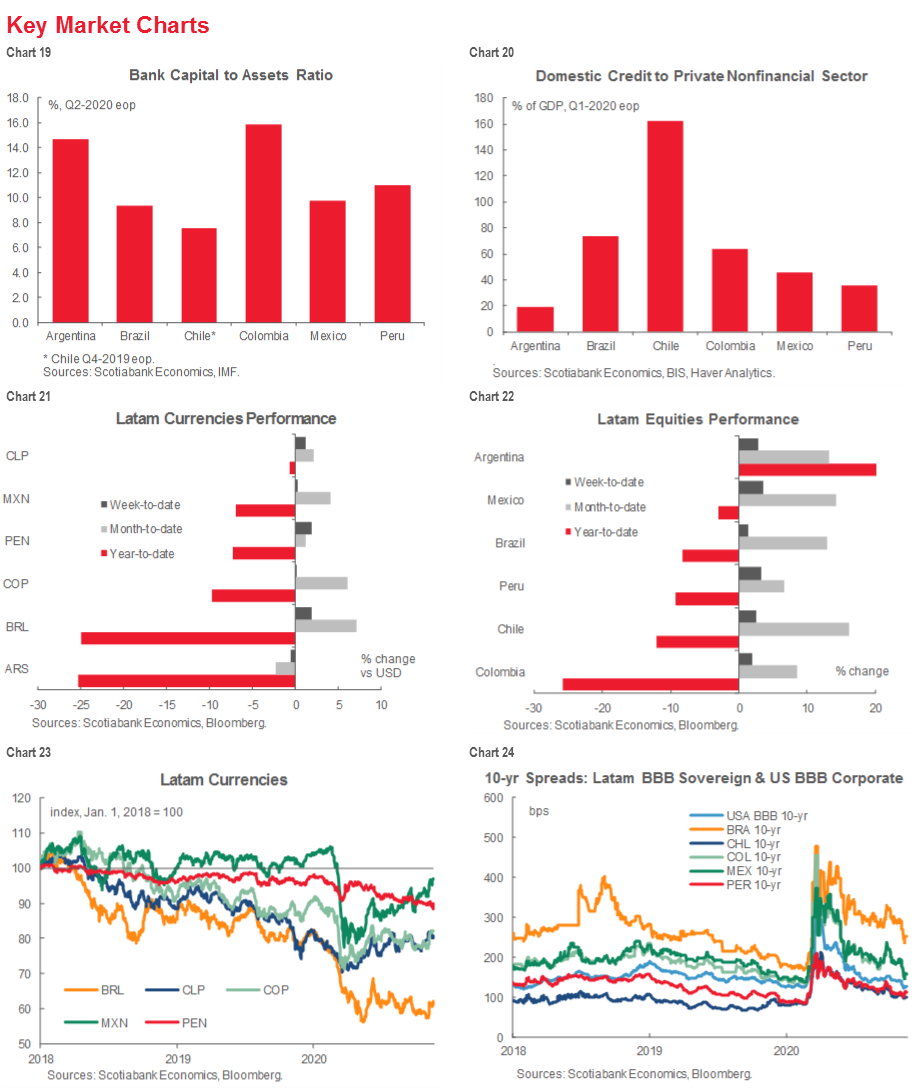

- External accounts have weathered the crisis fairly well as currencies been allowed to act as shock absorbers. In contrast with past crises, Latam’s authorities allowed their currencies to depreciate by as much as -25% (see chart 21, p. 8) this year as international capital flows pulled back and global commodity demand fell. As a result, current account balances and FX reserves have remained stable, as our charts on p. 4 highlight. That said, part of the stability in reserve coverage has been a by-product of much reduced domestic demand and smaller import flows even with substantial fiscal support.

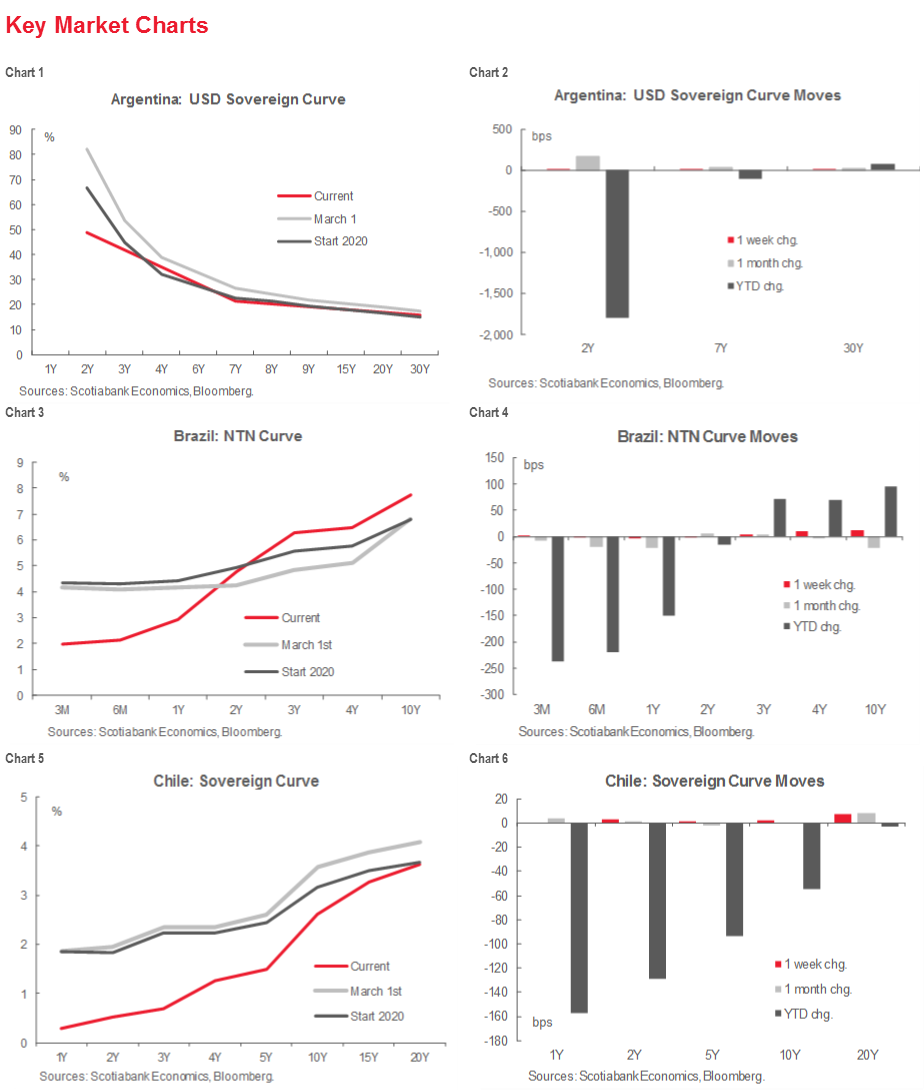

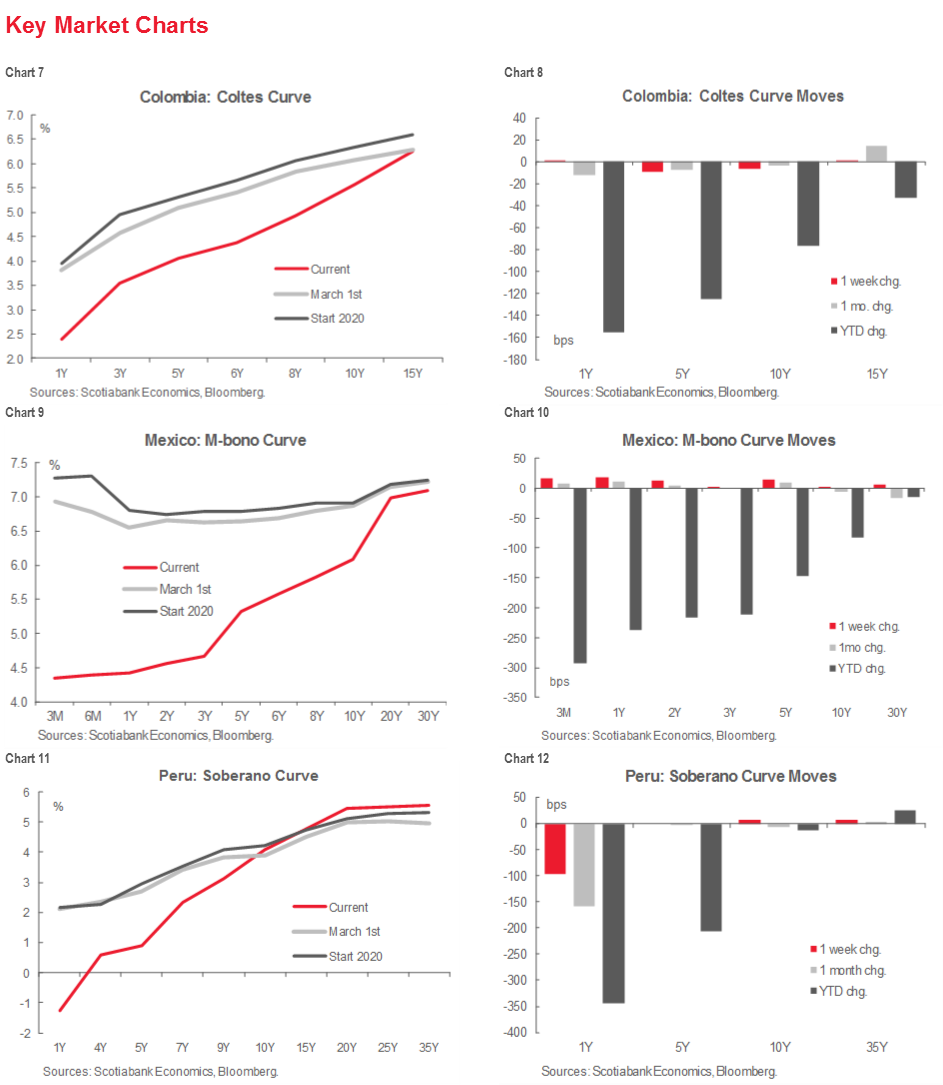

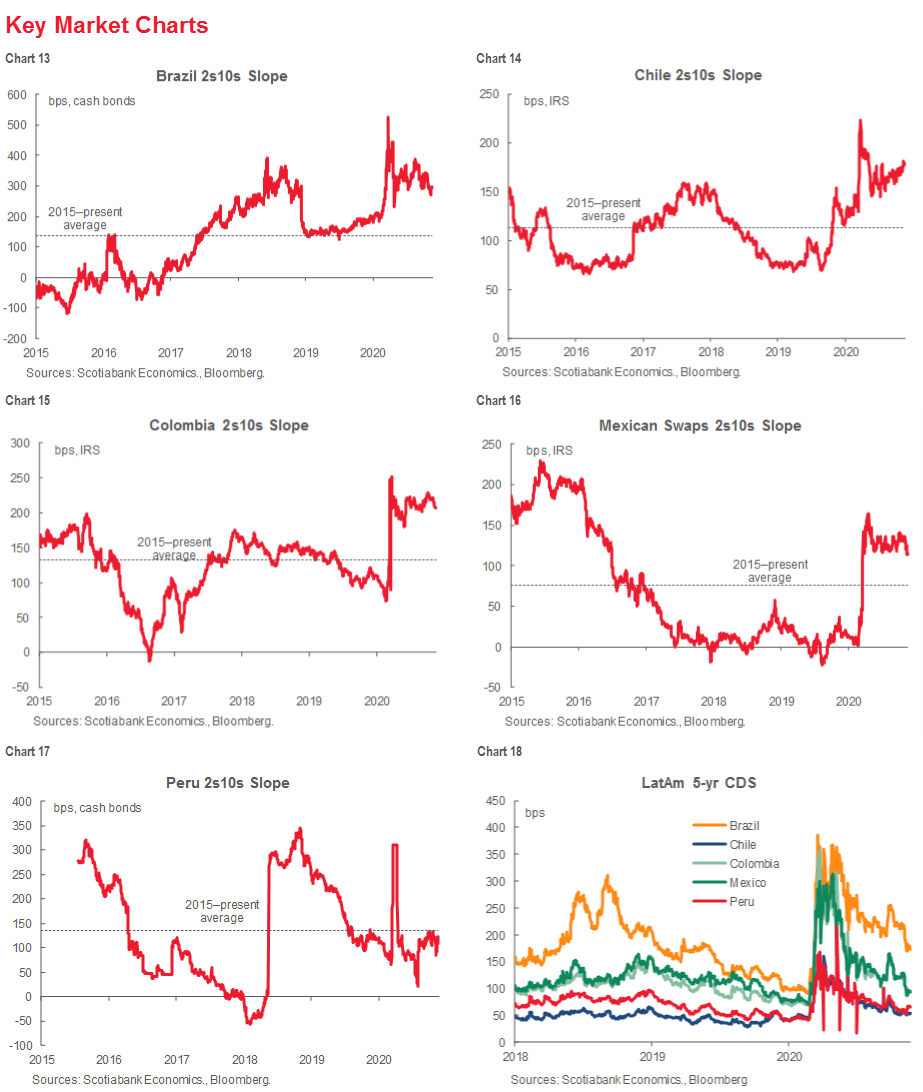

- Latam’s rates markets have come through 2020 with admirable resilience. Across the Latam-5 inflation targetters, our Key Markets Charts on pp. 5 through 8 underscore that long-term rates remained well-anchored this year as curves bull-steepened in response to policy-rate cuts. Across the Latam-5, 2s10s spreads have pulled back notably from their widest points at the onset of the pandemic; even with the recent onset of political turmoil in Peru, its 2s10s spread has remained just under its average of the last five years. CDS spreads have retraced about three-quarters of their H1-2020 sell-off (chart 18, p. 7) and even 10-year credit spreads have narrowed by up to 80% from their widest levels in Q2-2020 (chart 24, p. 8).

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | carlos.munoz@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Forthcoming |

| Subscribe: | pirajaj@colptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

| COSTA RICA | |

| Website: | Click here to be redirected |

| Subscribe: | estudios.economicos@scotiabank.com |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.