As the COVID-19 pandemic and Latam’s response to it continue to evolve, this edition of the Latam Weekly also marks some small shifts in our macroeconomic coverage of the region in response to requests from our readers. The Markets Report section has been hived off into a standalone publication that will be published on ScotiaView by our Latam Strategy team for institutional investors and corporate clients. Our Latam chart packs on the progress of the COVID-19 pandemic, key economic indicators, and market pricing will be updated fortnightly in a separate report from Scotia Economics for our Latam subscribers; it will also be posted on our public website.

FORECAST UPDATES

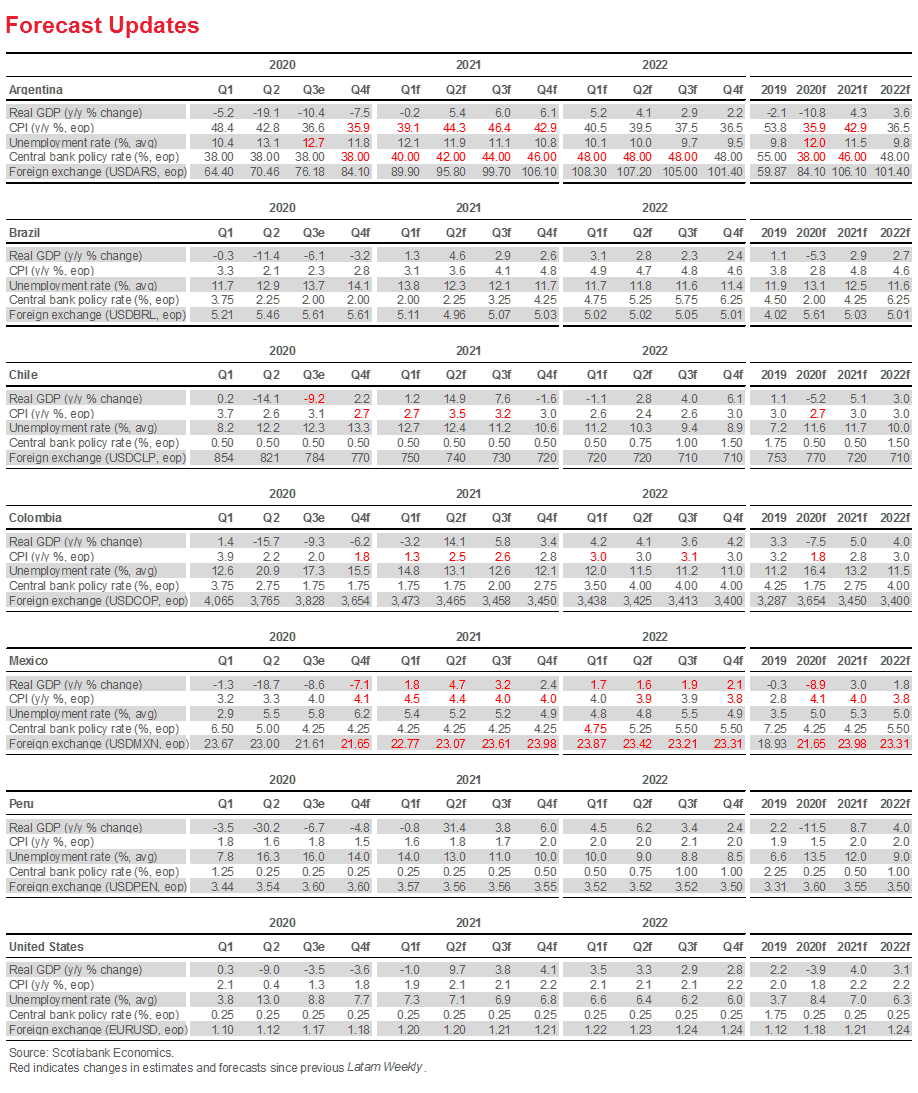

Our Latam outlook remains broadly stable, with substantive changes only in Argentina in response to a reversal of the BCRA’s recent cuts to its benchmark interest rate as FX pass-through starts to boost inflation and negotiations begin in earnest with the IMF.

ECONOMIC OVERVIEW

As Q3 growth numbers put a spotlight on the ongoing state of Latam’s recovery, central banks catch their breath ahead of extended pauses across the Latam inflation targetters.

COUNTRY UPDATES

Concise analysis of recent events and guides to the fortnight ahead in the Latam-6: Argentina, Brazil, Chile, Colombia, Mexico, and Peru.

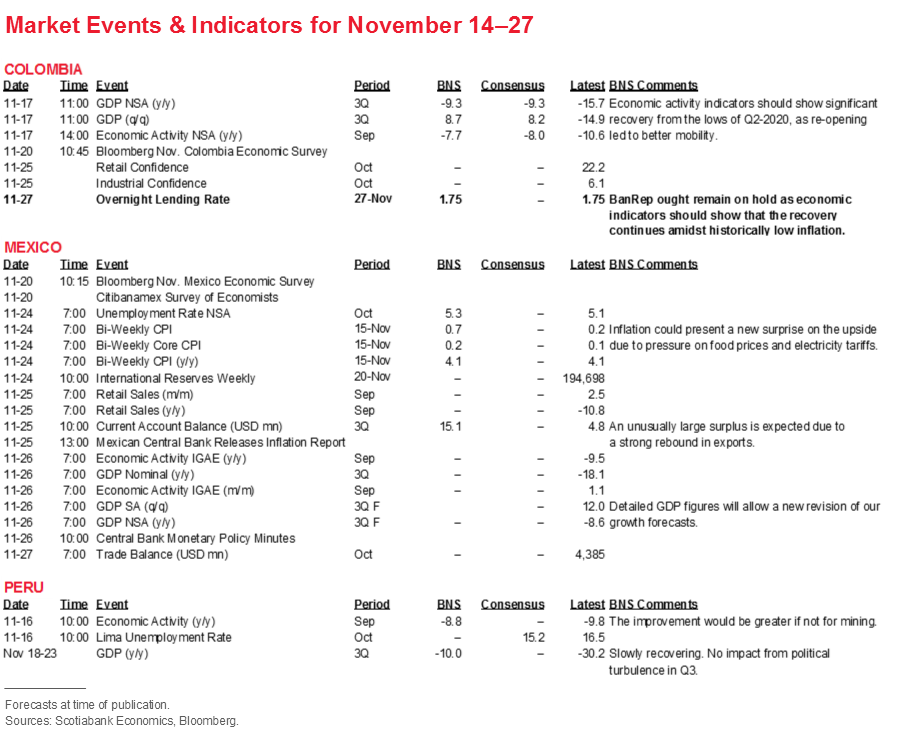

MARKET EVENTS & INDICATORS

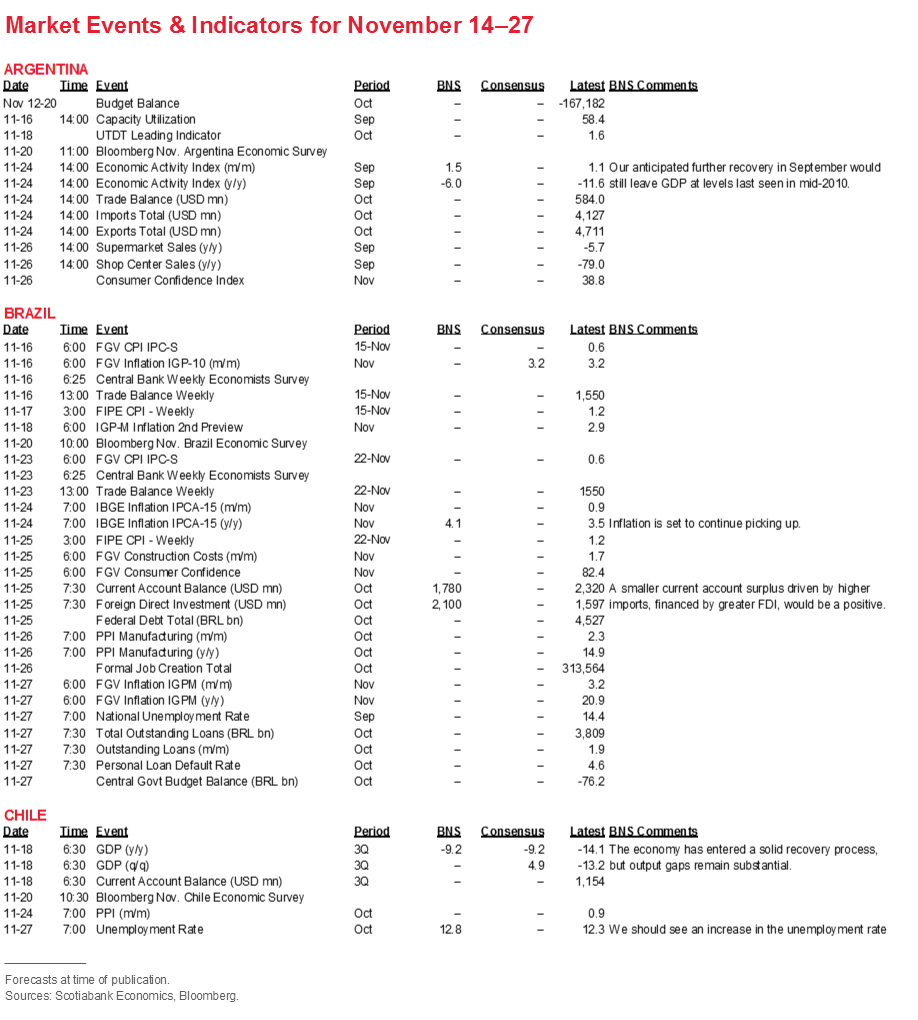

Risk calendar with selected highlights for the period November 14–27 across our six major Latam economies.

Economic Overview: An Extended Pause

Brett House, VP & Deputy Chief Economist

416.863.7463

Scotiabank Economics

brett.house@scotiabank.com

Limited forecast revisions focus on a turn toward more orthodox policymaking amidst IMF negotiations in Argentina, and fine-tuning in Chile, Colombia, and Mexico.

Q3 growth numbers put a spotlight on the ongoing state of Latam’s recovery.

Central banks catch their breath ahead of extended pauses across the Latam inflation targetters.

FORECAST UPDATES: SMALL ADJUSTMENTS IN OPPOSING DIRECTIONS

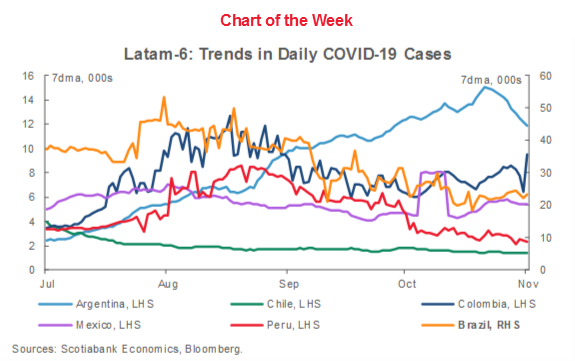

While the rest of the world grapples with renewed spikes in COVID-19 numbers, the pace of the pandemic continues to slow across most of the Latam-6 (see Chart of the Week, p. 1) and our Latam outlook remains broadly stable. Given that our forecasts are more constant than they were at the start of the lockdown, changes will continue to be marked in red in our main Forecast Updates table (p. 2), but successive revisions since March will no longer be recapitulated, as has been the case in past editions of the Latam Weekly.

Substantive changes to our forecasts are limited to Argentina, with some fine-tuning in our projections for Chile, Colombia, and Mexico.

Argentina. This past week, the BCRA reversed the -200 bps in cuts it made to its benchmark Leliq rate in October, bringing the benchmark back up to 38% as FX pass-through starts to boost inflation and negotiations begin in earnest with the IMF. We have raised our inflation outlook for the next year and brought forward further interest-rate hikes from the BCRA as the authorities begin at least a nod toward more orthodox policymaking.

Chile. Inflation in Chile has been edged up for the next four quarters in response to October’s upside surprise. Still, we expect the BCCh to look through what we think is a transitory increase in prices driven by a temporary boost to consumption fueled by pension fund withdrawals and keep the policy rate on hold for several quarters.

Colombia. In contrast, our team in Bogota shaved the inflation outlook for the next 12 months in Colombia after October’s downside surprise that they ascribe to some one-offs and statistical artefacts. We still expect the BanRep to stay on an extended hold.

Mexico. Our team in CDMX narrowed slightly its forecast contraction for real GDP in 2020 on the back of recent data prints, but kept its expectation in place of a relatively soft recovery in 2021 and 2022. The marginally better growth outlook for 2020, combined with recent price data, translates into the forecast for end-2020 headline inflation moving up from 3.9% y/y to 4.1% y/y, keeping it above Banxico’s target range.

This revision adds conviction to our Mexico City team’s view that inflation will keep Banxico’s Board on hold until early-2022; it also implies a slightly stronger MXN than previously forecast as further rate cuts gets priced out.

MACRO DATA: GROWTH UPDATES

GDP data for Q3 are set to dominate macro-data risk events over the coming two weeks, with Q3 prints due from Colombia (Nov. 17), Chile (Nov. 18), and Peru (Nov. 18 to 23), with an update on preliminary estimates also due in Mexico (Nov. 26). Monthly GDP proxies for September are scheduled from Peru (Nov. 16), Argentina (Nov. 24), and Mexico (Nov. 26), though they’re of limited utility in Peru and Mexico since they arrive more or less contemporaneously with their Q3 GDP prints. Unsurprisingly after Q2’s disastrous numbers, we expect strong rebounds in Q3, but real GDP levels will remain between 6% and 15% below pre-pandemic levels across the Latam-6. See our Market Events & Indicators risk calendar at the back of this report for a full risk calendar.

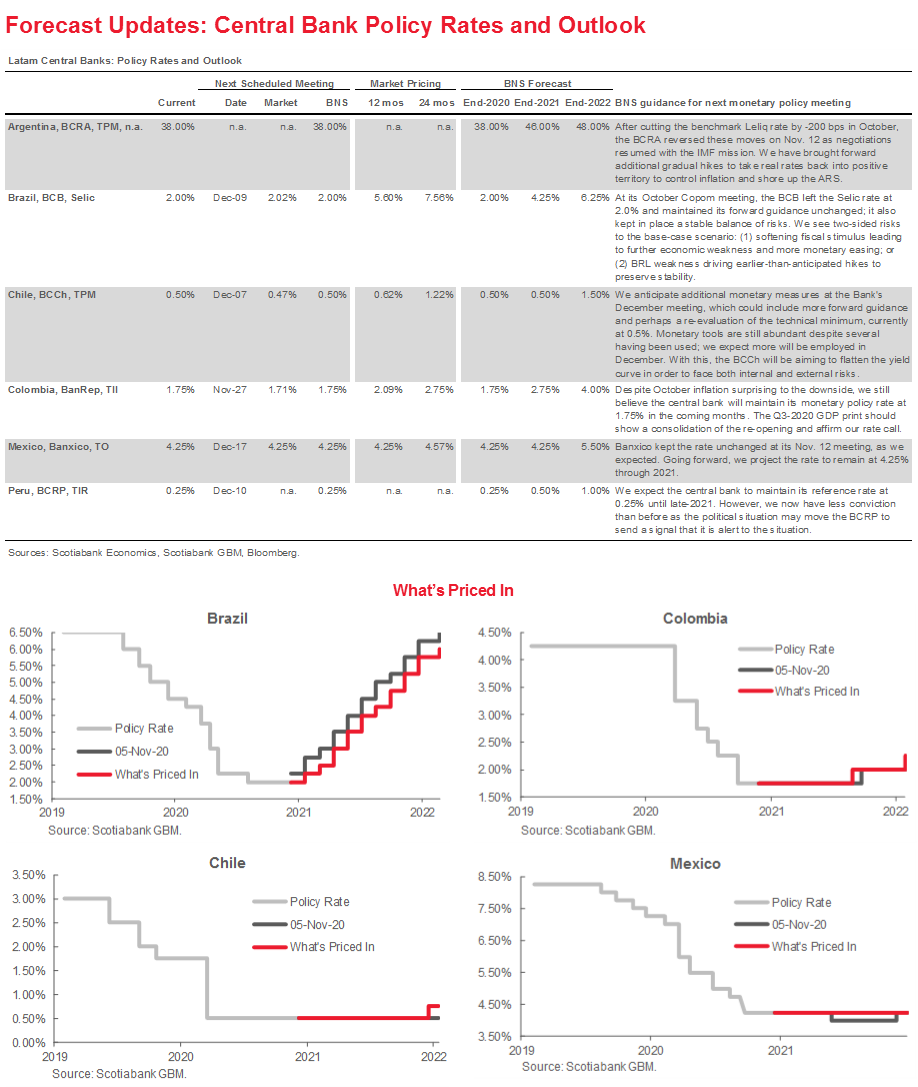

CENTRAL BANKS: HOLDING PATTERNS WITH THE BANREP ON DECK

Although we are likely to see ad hoc moves by Argentina’s BCRA to shore up demand for the ARS over the coming weeks, Colombia’s BanRep is the only Latam-6 central bank that has a regularly scheduled monetary-policy decision or publication release during the next fortnight (see Central Bank table, p. 3). The region’s other central banks all have scheduled monetary-policy meetings in the first half of December where all four are expected to keep rates on hold. Brazil is the only case where markets are pricing a return to interest rate hikes early in 2021 (see What’s Price In? charts on p. 3)

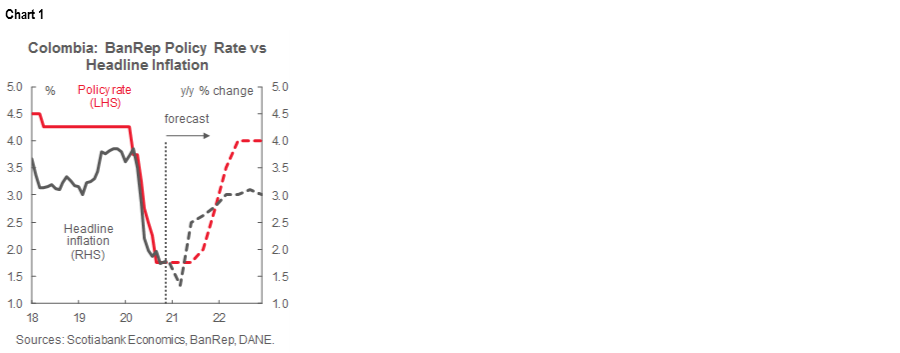

The Board of Colombia’s BanRep is scheduled to hold its next monetary-policy meeting on Friday, November 27, 2020 and our team in Bogota expects the benchmark rate to be held at 1.75% for a second consecutive month. In fact, we maintain our call that the monetary policy rate will remain on hold at 1.75% for the rest of the year and into the first half of 2021 (chart 1). We don’t expect headline inflation to reach the BanRep’s 3% target until Q1-2022 (see Forecasts table, p. 2). Consequently, the first hike from the BanRep is projected for late-Q3-2021.

At its last meeting on Friday, October 30, the BanRep Board voted unanimously to hold its benchmark interbank rate at a record low 1.75%. The unanimity of the decision underscored a forward-looking message of rate stability after the 4-3 split decision to cut from 2.00% to 1.75% at the September Board meeting. The minority at the September meeting had preferred to stay on hold owing to concerns about the pandemic and the possible evolution of public debt under additional easing.

In the Board’s October 30 statement, members noted that inflation expectations have risen, while fiscal measures, the new re-opening plan, and low interest rates should help the economic recovery. Nevertheless, the Board continued to eschew explicit forward guidance, noting that while the 1.75% policy rate keeps the monetary stance “expansive”, it is “prudent to maintain its current posture while waiting for new information on shocks and the evolution of variables that affect policy reactions.”

The minutes from the meeting, which were released on Tuesday, November 3, highlighted a relatively favourable forward-looking scenario, as the Board anticipated a slightly better GDP growth outlook for 2020 than their previously projected range between -6% y/y and -10% y/y (we forecast -7.5% y/y). The Board emphasized that accelerated re-openings, fiscal support, and the liquidity provided by the central bank should sustain the economic recovery. Additionally, the minutes highlighted that recent external current-account dynamics have led to lower financing needs; nevertheless, the Board saw the augmentation of the IMF FCL as a positive development amidst volatile times. On the negative side, the Board indicated that the labour market remained a concern and that the second COVID-19 wave has increased uncertainty around monetary policy. All in all, the minutes re-affirmed the data-dependent, "wait- and-see approach" of the Board during an economic recovery accompanied by huge labour-market challenges and still-substantial pandemic-related volatility.

The quarterly Monetary Policy Report, also published on Tuesday, November 3 revised the outlook for real GDP growth in 2020 to the upside from -8.5% y/y to -7.6% y/y in a range between -9% y/y and -6.5% y/y, close to our -7.5% y/y forecast. On the inflation side, BanRep staff revised its forecast to the upside to 1.9% y/y and 2.6% y/y in 2020 and 2021, respectively, from the previous expectations of 1.5% y/y and 2.3% y/y. The upward revision reflected offsetting effects from weaker demand on one hand and, on the other, higher biosecurity-related costs and greater FX pass-through effects. We expect CPI inflation at 2.0% y/y by the end of 2020 and 2.8% y/y by 2021 (again, see Forecasts table, p. 2) However, annual inflation should decline temporarily between February and April due to statistical base effects from food inflation; this should be seen as a transitory episode before inflation moves up a convergence path toward the 3% target in 2021.

Since the October 30 meeting and the publication of the minutes and quarterly report, inflation surprised to the downside, slowing from 0.32% m/m in September to -0.06% m/m in October; this pulled annual inflation down from 1.97% y/y in September to 1.75% y/y, further below the 2% y/y to 4% y/y range around the 3% y/y target (chart 2). We expect the BanRep to look through this anomalous print. October inflation was dampened by one-off effects from a month of atypical data collection on post-secondary tuition fees that DANE doesn’t expect to be repeated in November. However, we could see further soft price prints in the short term owing to an extraordinary combination of a VAT holiday and some special programs to stimulate household consumption. Base effects could also bring down year-on-year inflation numbers in Q1-2021, but annual inflation rates are expected move consistently upward later in 2021.

For now, headline inflation trends support keeping the policy rate at 1.75% for the rest of 2020 and well into 2021. We still forecast next year’s annual inflation rate to converge to a level slightly below BanRep’s 3% target by end-2021.

USEFUL READING

Mexico has seen record remittance flows over recent months, and with the ongoing recovery in the US these transfers are likely to continue and will play a critical role in sustaining Mexican domestic demand and financing its balance of payments. The Fed’s Higgins and Klitgaard provide a round-up on remittance flows to Mexico, Central America, and the Caribbean in the blog post cited below.

Matthew Higgins and Thomas Klitgaard, “Has the Pandemic Reduced U.S. Remittances Going to Latin America?,” Federal Reserve Bank of New York Liberty Street Economics, November 9, 2020: https://libertystreeteconomics.newyorkfed.org/2020/11/has-the-pandemic-reduced-us-remittances-going-to-latin-america.html

COUNTRY UPDATES

Argentina—The Fund is Back in Town

Brett House, VP & Deputy Chief Economist

416.863.7463

brett.house@scotiabank.com

With the arrival of the IMF mission in Buenos Aires this past week, the Argentine authorities indicated that they will be seeking to replace their existing Stand-By Arrangement (SBA) with new borrowing under the IMF’s Extended Financing Facility (EFF)—an implicit admission that the economy is significantly off-track compared with the projections in the IMF’s March debt-sustainability analysis (DSA) and its June update. The move squares with our long-held view that Argentina would have to do more than simply rollover its USD 44 bn in outstanding borrowing with the IMF. Instead, a new EFF loan is likely to provide additional resources to help plug the authorities’ fiscal gaps—and extend the horizon over which IMF resources would need to be repaid. EFF credits are usually disbursed over three years, but may be extended to a four-year period in cases, such as Argentina’s, where deep, structural reforms are required. The EFF’s grace and amortization periods are both longer than under an SBA: loans under an SBA are repaid over 3¼–5 years, while credits disbursed under an EFF can be repaid over 4½–10 years.

Negotiation of an EFF loan also intensifies the reform agenda that the IMF is likely to demand from Argentina in return for additional, longer-term support. IMF adjustment programs normally focus on four key areas: fiscal policy, monetary policy, the external sector, and the real economy. On the fiscal front, adjustment equivalent to at least 3 ppts of GDP would be needed to get back in line with the DSA’s deficit outlook and begin phasing out the Treasury’s nearly continual reliance on transfers from the BCRA for financing. While central bank financing of fiscal deficits has become globally ubiquitous in response to the pandemic, the IMF mission will likely insist on bringing growth in M2 down under 20% y/y in the near- to medium-term in order to curb inflation and provide some underpinning to the ARS. A devaluation of the Argentine peso is inevitable under what will likely be a renewed effort to align the official USDARS exchange rate and blue-chip swap rate, and boost exports. Finally, the IMF will likely look for significant structural reforms to reduce distortions in the tax system, encourage investment, and boost productivity. Efforts by Economy Minister Guzman this past week to move forward on reforms to the public-pension system likely mark a first step in this policy agenda—but we still expect discussions with the IMF to be drawn out as the authorities are unlikely to agree easily to the baseline demands the Fund is likely to make.

In macro data due for release over the coming two weeks, the September GDP proxy, due on Tuesday, November 24, stands out as the most important print. On the basis of leading indicators, we expect sequential growth to accelerate slightly from August’s 1.1% m/m to 1.5% m/m in September. This would narrow the annual contraction in real economic activity from -11.6% y/y in August to -6.0% y/y in September (chart). Although a consistent and marked improvement from the nadir of the lockdown in April, this would still leave real GDP at levels on par with those seen in mid-2010, a testament to Argentina being the only country amongst our Latam-6 that has truly experienced another lost decade.

October trade numbers, also out on Tuesday, November 24, are likely to show a further erosion in the trade surplus owing to higher imports and constrained exports as (1) domestic demand continues to recover; (2) importers bring forward foreign purchases as a channel to access relatively cheap US dollars through the official markets; and (3) exporters hold back on foreign sales in anticipation of a step-wise devaluation in the ARS.

October leading indicators, out on Wednesday, November 18, and November’s consumer confidence index, to be released on Thursday, November 26, should show Argentina’s near-term economic prospects moving upward, but at a slowing pace.

Brazil—Brazilian Growth Continued to Rebound Strongly from the COVID-19 Shock, but Fiscal Constraints Limit Future Support

Eduardo Suárez, VP, Latin America Economics

52.55.9179.5174 (Mexico)

esuarezm@scotiabank.com.mx

The Brazilian economy continues to rebound strongly from the COVID-19 shock, boosted by consumption-related items. Retail sales once again had a strong showing in September, with a +7.3% y/y print versus +6.2% y/y in August, but was slightly below the consensus +8.4% y/y. Manufacturing has also been robust, but it’s worth bearing in mind that Brazil’s manufacturing sector is much more domestically oriented than that of other countries in the region, such as Mexico, and hence part of the strength is also related to stimulus. The aggressive stimulus package the government has delivered to face the effects of COVID-19 has been an important reason for the rapid recovery. However, that stimulus is set to end over the next 1½ months. How much more room is there to deliver additional rounds of stimulus?

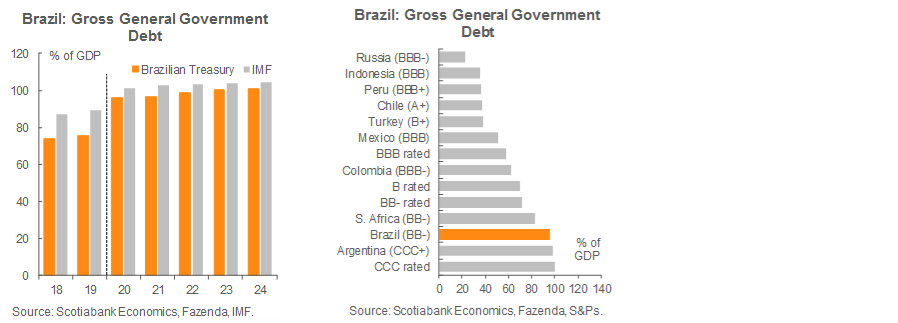

Depending on whether we go by IMF definitions and projections, or by the Brazilian Treasury’s, gross general government debt will peak at around 105% of GDP (IMF) or 100% of GDP (Treasury, first chart), both already at very high levels for an EM and consistent with junk-rated countries (second chart). Assuming an average cost of that debt of around 7% (380 bps less than the average 5yr rate for Brazilian government BRL nominal debt over the past 10 years), the combination of debt service and pensions would absorb about 25–30% of the public sector’s revenues. This makes a comprehensive fiscal reform urgent and suggests that fiscal space in Brazil is increasingly bumping against its ceiling. Another problem is growth. The Brazilian FinMin estimates the country’s potential growth rate at 2.5% y/y, which we see about 50 bps lower. Unless the country improves its potential, debt dynamics will likely continue to get more omplicated.

The next couple of weeks will be relatively quiet on the data front, but we do get IPCA-15, where we expect food price inflation to continue to exert some modest upwards pressure and trigger a breach of 4% (still on the lower bound of the BCB’s target). In addition, we are scheduled to receive balance of payments data for October, where we expect the country’s robust domestic demand to lead to a modest reduction in the current account surplus.

Chile—Inflation Exceeds All Forecasts; Bill to Approve a Second Withdrawal of Pension Funds Moves Forward in Congress

Jorge Selaive, Chief Economist, Chile

56.2.2939.1092 (Chile)

jorge.selaive@scotiabank.cl

Carlos Muñoz, Senior Economist

56.2.2619.6848 (Chile)

carlos.munoz@scotiabank.cl

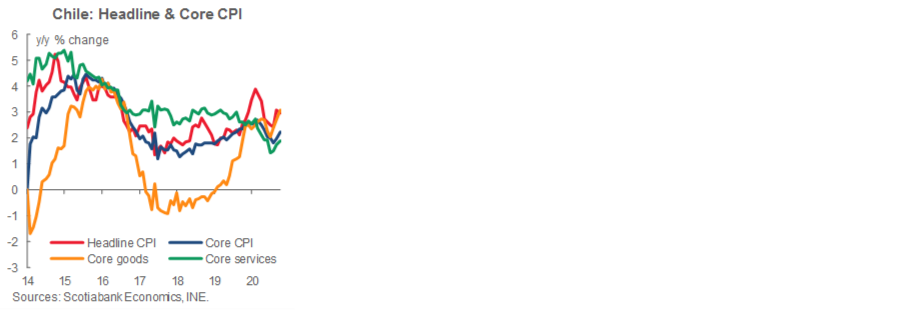

October CPI, released on November 6, jumped 0.7% m/m (3.0% y/y, chart)—more than double the market projection (0.3% m/m). On the one hand, we observed the expected contributions from the increase in the stamp tax and higher prices of fuels. Likewise, food and beverages increased due to demand and seasonal factors, without posing a surprise. With that, about 0.3 ppts are explained. Those who assigned the inflationary "surprise" to food would have made the wrong diagnosis. The most striking hike corresponds to the strong increase in durable goods. The price of the new cars category rose a historical 2.1% m/m (incidence of 0.06 ppts) and, at the same time, experienced a historical increase in sales (the second-best October in history in terms of sales). Clothing and footwear also experienced very relevant increases in 25 of the 28 products of the division. The strong upward pressure on consumption caused by the withdrawal of pension funds generated a transitory but very significant pressure on the demand for non-essential goods. Finally, restaurants and miscellaneous goods and services explain 0.2 ppts of inflation. Among them, the rise in food consumed outside the home (+1.3% m/m, incidence of +0.04 ppts) and ready-to-go dishes (+1.7% m/m, incidence +0.03 ppts) stand out, evidencing the higher disposable income of households.

On Tuesday, November 10, the Chamber of Deputies approved by a vast majority the bill to allow a second withdrawal of pension funds; 130 votes in favour, 18 against and 2 abstentions was the final count, which had several Congresspeople from the Government coalition supporting the bill. The current bill allows the withdrawal of a second 10% of pension funds, under the same conditions as the first one. Some Deputies discussed the possibility that high-income people pay taxes on the withdrawal, but that suggestion was ultimately rejected. We estimate that the amount to be withdrawn would be less than the central bank’s figure of USD 19 bn withdrawn after approval of the first bill. About two million people withdrew all of their funds from the pension system under the first withdrawal a few months ago; this second withdrawal would leave a total of about 4 million people without pension funds. The discussions that will take place in the Senate over the following weeks will be key.

In its Financial Stability Report, released on Wednesday, November 11, the Central Bank of Chile expressed its concern about the prolongation of the economic shock in the international and local financial system. In particular, the CB claims that persistent low growth could transform liquidity problems into solvency complications. In this context, the exceptional situation puts pressure on sovereign debt, due to the implementation of supportive fiscal programs. The rate of sovereign indebtedness represents a vulnerability, given the pressure of spending and the reduction in the capacity to generate income, especially if there were a scenario with tighter financing conditions and where economic activity did not rebound.

In the upcoming weeks, we will keep monitoring the second withdrawal of pension funds bill, that will be discussed in the Senate. Earlier estimations point that this bill too will be approved. On November 18, National accounts data will be published. We estimate GDP fell -9.2% y/y in the third quarter, evidencing that the economy has entered a solid recovery process, but output gaps remain given the contraction in GDP observed due to the pandemic. Then, on November 27, we will know the employment figures for October, where we expect an increase in the unemployment rate, as more people are entering the workforce compared to the jobs that are being created. We expect the unemployment rate to remain in double digits throughout 2022.

Colombia—How Much Further Could the COP Appreciation Go, and What Does It Mean for the Macro Scenario?

Sergio Olarte, Head Economist, Colombia

57.1.745.6300 (Colombia)

sergio.olarte@co.scotiabank.com

Jackeline Piraján, Economist

57.1.745.6300 (Colombia)

jackeline.pirajan@co.scotiabank.com

After the “resolution” of the US election, rather positive vaccine trial results, and affirmed credit rating at investment grade for Colombia, the USDCOP rapidly converged to our expected level for Dec 2020 of 3,650. That said, it is an excellent opportunity to review what macroeconomic fundamentals are saying for the exchange rate and what could be expected in the coming months.

From the macroeconomic perspective, the COVID-19 pandemic shock led to an unprecedented interruption of regular world economy functioning as most of the governments opted for strong isolation measures to contain the virus’ spread. Economic policy response also involved higher fiscal expenditures, which led to an unprecedented increase in the debt burden. All of those components increased the risk premium in EM asset prices. On the other side, as Colombian economic activity and world trade froze, the balance of payments showed a narrower current account deficit, with enough financing from public debt monetization, which constitutes a downside pressure for the FX.

That said, structural arguments pointed to an FX equilibrium level higher than pre-pandemic expectations but lower than we saw in the pre-US election period. In fact, since August, the COP underperformed by 200 pesos on average from what our fundamental model suggests, something that we attribute to a non-measurable extra risk premium on emerging markets assets. However, it is worth emphasizing that—despite the US election results and vaccine announcement leading the USDCOP to an expected level—risks in the medium-term remain. Those risks are related to the COVID-19 second wave and what it could mean for the economic activity recovery, some geopolitical events in the region, and domestically, the remaining structural challenges for the fiscal consolidation.

Therefore, despite the rapid appreciation in recent days, we keep our base case scenario of 3,654 pesos by Dec-2020, although further reductions in USDCOP could take place if the macroeconomic scenario is structurally better and less risky than the current one, which for now has a low probability. In the short term, Government monetization of external debt would lead to further downward movements, but again, we consider that lower levels are sustainable only in a better macro scenario.

All in, despite recent appreciation of 5% in the last two weeks, we do not yet see a motivation to change our view on the COP. We think that recent strong appreciation was more due to lower risk aversion due to recent events such as the US elections and COVID-19 vaccine, which brought the COP to a more structural level. Therefore, in terms of monetary policy we do not see major changes in our scenario of policy rate stability at least for nine months. In terms of fiscal policy, we think debt/GDP ratios are lower than projected in the fiscal framework since depreciation has been lower than government expectations, which can help to bring a bit more confidence to Colombian assets. However, we do not think that market concerns on long-run debt sustainability will change just because of this recent FX appreciation.

Mexico—Losing Momentum

Mario Correa, Economic Research Director

52.55.5123.2683 (Mexico)

mcorrea@scotiacb.com.mx

In the present stage of the economic crisis triggered by COVID-19, the numbers from economic activity will reveal if the economy is gathering traction after the rebound or if it is losing momentum. There are some contrasts among different indicators, but the most relevant ones tilt the balance towards weakness.

On the positive side of the balance, remittances totaled USD 3.6 bn (up 15.1% y/y) in September, which meant accumulated remittances during January–September amounted to just shy of USD 30 bn (up 10.0% y/y)—record numbers for both the ninth month of the year and the first nine months of the year. The continuous and favourable evolution of the flow of remittances reflects the positive generation of employment in the United States. Also positive were the auto industry exports and production in October. The number of units produced was 8.8% higher than a year ago, while exported units grew 8.2% y/y, mainly driven by the US economic recovery. On the other hand, domestic auto sales fell -21.3% y/y in October, reflecting a weak internal market. The most relevant components of internal demand—private consumption and gross fixed investment—presented weak numbers in August. According to INEGI, internal private consumption grew 1.8% m/m in August which, under more usual circumstances could be considered a strong pace but, considering that this indicator remained 13.1% below the level a year ago, the final reading is of weakness. It will take several years for private consumption to recover to pre-pandemic levels, and we should not forget it is the heaviest component of internal demand.

August’s gross fixed investment (GFI) data showed a 5.7% m/m sa gain, a further recovery from July’s 3.5% m/m increase. This is the third consecutive month where monthly GFI growth remained on positive ground, a reflection of the ongoing resumption and normalization of activities. Still, in the annual comparison, this produced only a small lift from -21.3% y/y in July to -17.4% y/y. Productive investment is set to remain weak, due mainly to a poor business environment and heavy uncertainty over regulatory changes. Investment in machinery and equipment contracted at a steeper rate, going from -18.1% y/y in July to -20.6% y/y in August. Its two major components, domestic and imported goods, fell by -23.1% y/y and -22.7% y/y, respectively; and construction investment spending softened its annual decline from -23.8% y/y to -15.0% y/y, with both of its major components recording slightly smaller annual contractions—the residential sub-index went from -21.9% y/y in July to -7.5% y/y in August, and non-residential construction rose from -25.7% y/y in July to -21.9% y/y in August.

Domestic private consumption advanced at a slower pace in its seasonally adjusted monthly measurement in August. Growth slowed from 5.4% m/m in July to 1.8% m/m, even though the process of re-opening the country's economic activities continued. This confirmed that domestic demand remained weak, as we had anticipated. Total private consumption was still down -14.2% y/y in August, the largest contraction for any August since at least 1994. We continue to expect weak domestic private consumption growth for the rest of the year as consumers are set to remain cautious in light of the highly uncertain economic environment and weak expectations in the labour market.

October headline inflation was 0.61% m/m, which was above analysts’ average forecast of 0.52% m/m, reaching 4.09% y/y, just above the upper limit of Banxico’s target range for a third consecutive month (chart). Core inflation slowed as it registered a monthly change of 0.24% m/m, in line with the average anticipated by the analysts’ consensus and below September’s monthly 0.32% m/m gain. By sub-components, merchandise inflation decelerated from 0.42% m/m to 0.29% m/m between September and October. Meanwhile, services inflation (0.18% m/m) remained moderate; however, its downward trend slowed as the sector continued re-opening. The price index for the Minimum Consumption Basket, which is designed to monitor price variations in subsistence expenses, registered a gain of 0.71% m/m and 4.47% y/y in October; in the same month of 2019, the corresponding figures were 0.71% m/m and 2.56% y/y.

October data for the auto sector painted a mixed picture of the industry in its fifth month of re-opening. Vehicle production and exports showed gains compared with 2019, but domestic sales remained down. Light auto production grew 8.8% y/y in October, up from -5.5% y/y in September. From January to October, 2.4 mn units were assembled, down -25.0% y/y compared to the same period YTD in 2019. Exports of vehicles grew in annual terms for the first time since July 2019, accelerating from -13.1% y/y in September to 8.8% y/y in October. During January to October, 2.2 mn units were exported, which represented a decrease of -26.3% y/y YTD compared to a year earlier; and domestic sales of new vehicles eased their annual contraction from -22.8% y/y in September to -21.3% y/y in October, which left domestic demand the weakest part of this auto triptych. During the first ten months of the year, 748.5k units were sold, which represented a decline of -29.6% y/y with respect to the same period YTD in 2019. These results point to a still-slow recovery in domestic vehicle sales in the months ahead. This contrasts with better-than-anticipated results in production and exports, which are benefiting from the relatively positive environment in the US and Canada.

In Banxico’s Survey of Expectations for October, private-sector economic analysts have edged back their expectations for 2020’s GDP contraction for a third consecutive time, on this occasion from -9.82% y/y to -9.44% y/y. However, the economic rebound expected in 2021 was also notched down from 3.26% y/y to 3.21% y/y. Expectations for both headline and core inflation at the end of 2020 increased to 3.92% y/y (previously 3.89% y/y) and 3.92% y/y (previously 3.90% y/y), respectively. For the end of 2021, both headline and core inflation forecasts increased marginally to 3.60% y/y (previously 3.57% y/y) and 3.48% y/y (previously 3.47% y/y). We emphasize that, on the horizon where monetary policy operates, both headline and core inflation expectations remain within Banxico’s target range. Exchange-rate projections for the end of 2020 and 2021 strengthened from the September survey and the Mexican currency is expected to end 2020 at USDMXN 21.74 (previously USDMXN 22.14) and end 2021 at USDMXN 22.05 (USDMXN 22.33). As for monetary policy, most analysts anticipate that the interbank funding rate will be below the current target rate (4.25%) at the end of 2020 and for all 2021. Regarding the factors that could hinder Mexico’s economic growth in the next six months, the most-cited issues were related to domestic economic conditions (45%), governance (22%), and external conditions (19%).

Banco de Mexico surprised financial markets and most analysts in their last monetary policy decision on November 12, leaving the overnight interest rates unchanged at 4.25%, which was our call, while almost everybody was anticipating a -25 bps reduction (chart, again). There was a divided decision, with one Board member voting for a cut to 4.00% on the reference interest rates. Banxico mentioned that inflationary expectations for 2020 had increased, that recent inflation performance—both in the general and the core indexes—implied a slight increase in the expected trajectories and that, considering the need to consolidate a descending trajectory for general and core inflation towards the 3% target, the Board decided to keep the reference rate at the current level. After this decision it is likely that, unless inflation behaves very favourably, the easing cycle has ended.

Finally, Fitch Ratings affirmed the sovereign credit at BBB- with a stable outlook, arguing a consistent macroeconomic policy framework, relatively stable and robust external finances and government debt/GDP projected to stabilize at levels in line with the BBB median. They also mentioned that tax revenues have outperformed expectations and the authorities have sought to minimize borrowing in 2020, and they expect that public debt ratios will remain higher than pre-crisis levels but that the administration will maintain a tight fiscal stance and likely implement a tax reform in 2022, limiting risks to the credit profile from deteriorating public finances and supporting the Stable Outlook. It is worth noting that the Fitch rating for Mexico—just at the edge of the investment grade—is the lowest among the three global agencies.

For the coming weeks, all the relevant economic information will be concentrated in the week starting on November 23. The detailed numbers for Q3 GDP as well as the Global Indicator of Economic Activity for September will be released, and they will allow the next important revision on the outlook. We will also have the next quarterly report from Banxico, where they present their economic forecasts, and the minutes of the last monetary policy decision, which will let us know how they are reading the economy and what could be the next steps for monetary policy. Inflation for the first half of November will be a relevant piece of data for Banxico, and it is likely it will present a new surprise on the upside. We will also receive the unemployment rate for October, retail sales for September and balance of payments figures for Q3.

Peru—The Brief Merino Government, Rocked by Protests and Rolled by Congress

Guillermo Arbe, Head of Economic Research

51.1.211.6052 (Peru)

guillermo.arbe@scotiabank.com.pe

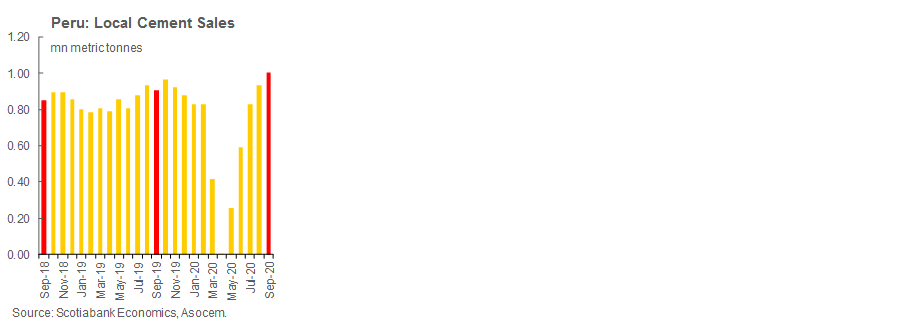

GDP growth for September will be released by Monday, November 16, just after the release of this publication. Our expectation is of an -8% to -9% y/y contraction. With this, GDP will have fallen around -10% y/y, in 2020-Q3. Third quarter GDP and other macro numbers will be released on Friday, November 20. Recent growth indicators have been mixed. Cement demand in September rose nearly 10% y/y (chart), and both mortgage loans and home sales have surpassed year-ago levels. Electricity demand reached year-ago levels in October, but has slipped back into mildly negative territory so far in November. The persisting mobility restrictions for Sundays and night-time business are probably playing a role. On a brighter note, government investment increased 6.6% y/y in October, according to statements by the authorities. This would be the first month of positive growth since the lockdown. Terms of trade have also continued improving, following a trend in place since June. Gold, silver, copper and zinc prices are all outperforming expectations.

On November 12, the Central Bank maintained its reference rate at 0.25%. We still do not expect any change until late-2021. However, we now have less conviction in our view, given recent political events. A deterioration in the political situation could conceivably motivate the BCRP to choose to send a signal that it has the economy’s back, by lowering the reference rate further. The counterargument is that inflation continued defying gravity in early November, with prices trending again towards 1.9% y/y. Meanwhile, financial markets, including the FX, have turned moderately bearish due to political events. The PEN has returned to USDPEN 3.65 levels and is once again pushing against its record weakest values. We wouldn’t be surprised if it breaks through. The political scenario is clearly a risk for our forecast of 3.60 at year-end.

The elephant in the economics room is, obviously, the political environment. Ongoing events should impact our forecasts to some extent, but it seems premature to venture new numbers when so much is in flux. The political, economic and business environment has been changing quickly and unpredictably. Until things settle, visibility in terms of economic impact will be low. Hopefully, a new political equilibrium will be reached that mollifies public opinion and provides enough stability to be able to last until the April 11 elections with a modicum of equanimity. If so, then the normal concerns will come back into play, such as to what extent a possibly now subdued Congress will continue following a populist agenda, and what will be the specifics of the new government’s economic policy.

The political, economic and business environment has certainly changed with the new government. The challenge that the Merino government faces is to gain credibility, respect, and the trust of public opinion. Until it does, the political situation risks continuing to be unsettled. The new Cabinet is experienced, not overly political, and is fairly independent of Congress. However, that does not appear to be enough to generate the credibility the government needs. José Arista, the new Minister of Finance, is pro-market. His strength is in day-to-day operational management. The challenge Arista faces is to demonstrate his willingness to take a strong stance against populist initiatives emanating from Congress. Furthermore, we are hopeful that Arista’s experience in public office will help reduce the transition period towards normalizing an active execution of policies and budgetary spending.

There is a persisting risk that Congress feels free to implement a populist agenda, with little opposition from the Presidency, or that this agenda could expand outside of the relatively limited economic issues of interest to Congress. Interestingly, however, the government—apparently due to pressure from public opinion—seems to be distancing itself from Congress on key issues. Pressure from public opinion has led the government to 1) pledge to honour the elections schedule, 2) refrain from including any member of Congress in the Cabinet, and 3) promise to respect the education reform. The protests have also aligned international institutions in taking a vigilant attitude towards the Merino government. Hopefully, the government will continue to be sensitive to public opinion when it reviews congressional initiatives once the protests lapse. Congress will have its own chance to express its opinion regarding the Cabinet when the Cabinet requests its vote of confidence, as required by law, presumably during the week of November 16.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | carlos.munoz@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Forthcoming |

| Subscribe: | pirajaj@colptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

| COSTA RICA | |

| Website: | Click here to be redirected |

| Subscribe: | estudios.economicos@scotiabank.com |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.