- Two weeks into the Russian invasion of Ukraine, the costs of the war are mounting. While the long-term effects of the war are unclear, the economic impacts are coming into focus—higher inflation, increased financial volatility, and greater uncertainty.

- Higher commodity prices represent a potential favourable terms-of-trade shock to Latam commodity producers. But the benefits of that shock have to be weighed against higher global interest rates and possible “sudden stops” in capital flows as investor sentiment shifts to “risk-off” mode.

- Moreover, the long-term consequences for the global economy are unknown. The longer the geopolitical situation remains fraught, the greater the risks to global supply chains.

In the two weeks following Russia’s unprovoked, unwarranted, and unwise invasion of Ukraine thousands of lives have been lost and thousands more lives shattered, geopolitical fault lines have widened, and economic uncertainty has spiked. What was expected to be a short, surgical strike has instead become a costly contest of wills with unexpected outcomes. Most significant, rather than divide democratic countries, the invasion has led them to unite behind severe sanctions that nobody could have predicted just weeks ago.

The longer the war goes on, the higher its cost. And while the long-term impacts of the war are unclear, the economic consequences are coming into focus.

The most immediate effect is higher inflation. Oil and other commodity prices have spiked in anticipation of supply disruptions as sanctions against Russia take effect. At almost 8% in February, US inflation is at a 40-year-high. Even before the latest inflation data was released, Fed Chair, Jay Powell, had said that policy rates would be headed higher. The ECB, meanwhile, in what Scotiabank’s Derek Holt describes as a “hawkish pivot”, has signaled that it is scaling back its bond-buying program and could suspend its asset purchase program in the third quarter if inflation does not moderate.

With the full effects of higher commodity prices—from base metals to wheat and other cereals—feeding through to final goods and foodstuffs, near-term price pressures are likely to remain high. Provided central banks adhere to their price stability targets, however, these pressures can be expected to dissipate over time as supply responses kick in and demand is constrained. In this respect, while the current situation evokes unwelcome memories of the oil price shocks of the 1970s and the stagflation that followed, strong monetary policy frameworks that anchor inflation expectations should prevent a reprise of that experience. That is not to say that the path of inflation won’t be higher than originally expected in January. As Mark Twain observed, “History never repeats itself, but it does often rhyme.”

At the same time, the orchestrated application of comprehensive sanctions against Russia can be expected to generate a range of financial knock-on effects. In the first instance, these costs will fall on the Russian people, who have seen the ruble crash in value and Russian sovereign and corporate bonds downgraded to junk status. These effects will spill over to other markets and other assets. For example, banks and other financial institutions holding Russian bonds and with sizeable loan exposures will have to write down these portfolios. Global banking’s lending capacity will of course be affected, with implications for those imposing sanctions, but those effects are likely to be small in relation to the costs of financial autarky that Russia will experience.

Because Russia’s foreign exchange reserves held in other central banks have been frozen, and its access to global capital markets effectively blocked, the long-term prospects for the Russian economy look bleak indeed. Other countries can be expected to help Russia evade the sanctions regime, either for profit or because they view their long-term geopolitical interests as being aligned. But these countries take a risk in doing so. The longer that the war drags on, the greater the likelihood that countries perceived to be thwarting (or those simply not supporting) the sanctions could become subject to a range of economic penalties. That possibility could entail the breakage of global supply chains, the reshoring of production, and the loss of export markets.

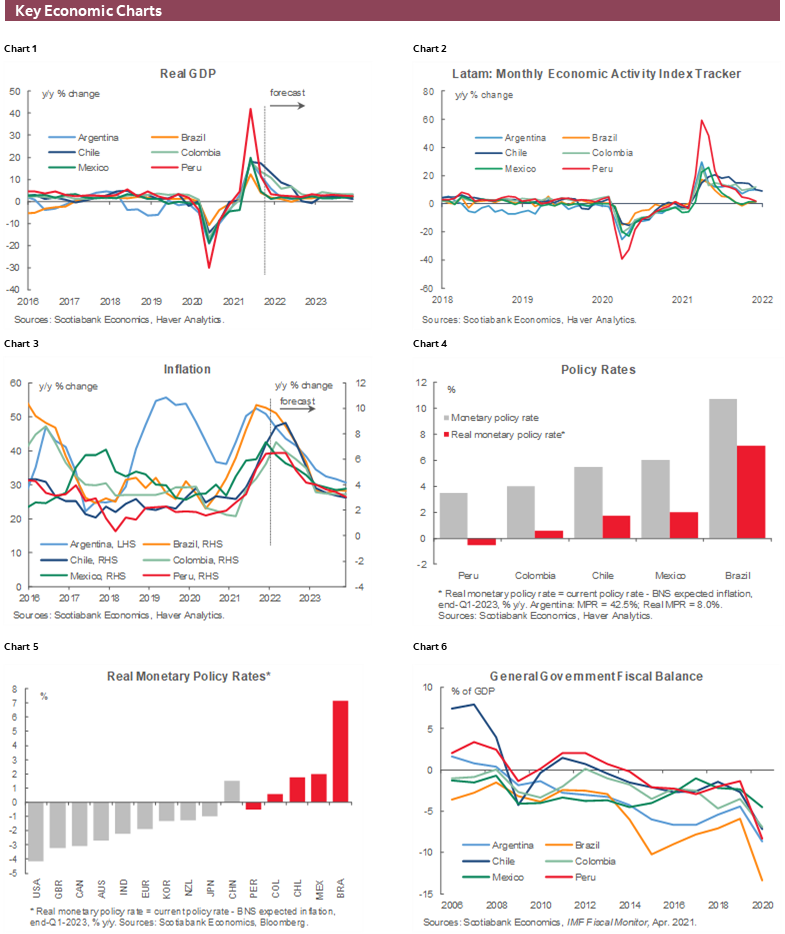

KEY ECONOMIC CHARTS

With inflation higher, advanced country central banks poised to hike rates, and investor risk appetite alternating between risk-on and risk-off modes, Latam countries face a far less felicitous external financial environment. That said, higher commodity prices could offset those effects. In this respect, Latam growth is expected to converge on pre-pandemic levels over the course of 2022 (chart 1), despite the increase in uncertainty with respect to the global economy and markets. Monthly economic activity indexes, which are broadly tracking this profile (chart 2), will be closely monitored in the weeks ahead for possible signs of departure from it.

Inflation has soared as economies in the region rebounded from pandemic-induced troughs (chart 3). But as noted above, central banks around the globe remain committed to price stability, Latam central banks included, and Scotiabank’s economists in the region expect inflation to gradually return to target over the next eighteen months or so. Consistent with this commitment to price stability, key policy rates across the region have been raised to keep inflation expectations firmly anchored (chart 4). Except for Peru, policy rates are now positive in inflation-adjusted terms. In this respect, they are ahead of the monetary policy tightening curve (chart 5).

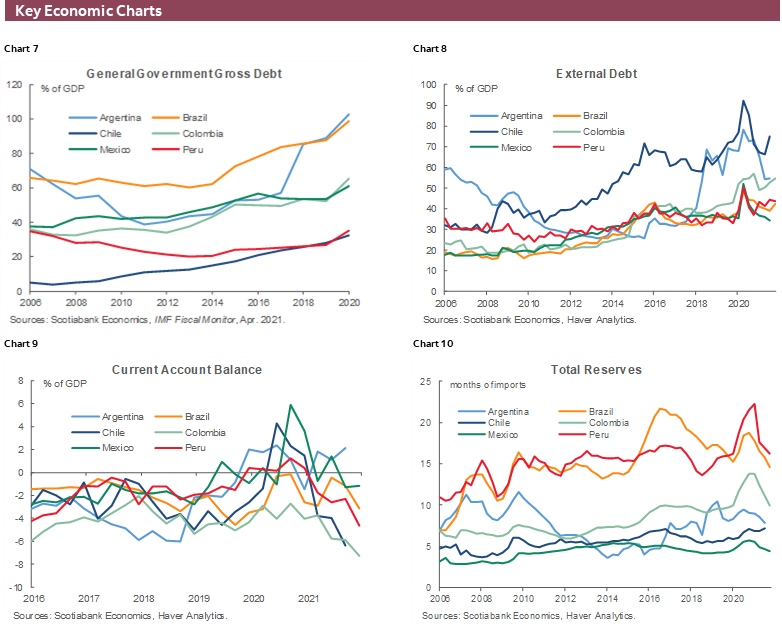

A favourable terms-of-trade shock from higher commodity prices could generate fiscal revenue windfalls, which would allow faster progress in terms of strengthening public finances. Fiscal balances across the Latam region deteriorated because of the extraordinary supports provided during the pandemic (chart 6). Many governments have already announced plans to narrow deficits and return to pre-pandemic fiscal paths; in Colombia, meanwhile, reforms to buttress long-term fiscal sustainability have been announced. Doing so would contain gross debt as a share of GDP (chart 7) and assist in the management of external debt (chart 8).

At the same time, a favourable terms-of-trade shock would contain current account deficits (chart 9), which have widened significantly in the case of Chile and Colombia, and bolster international reserves (chart 10). Smaller current account deficits and higher reserves would buffer Latam countries from adverse shifts in investor risk appetite, an important consideration in a less benign global financial environment.

KEY MARKET CHARTS

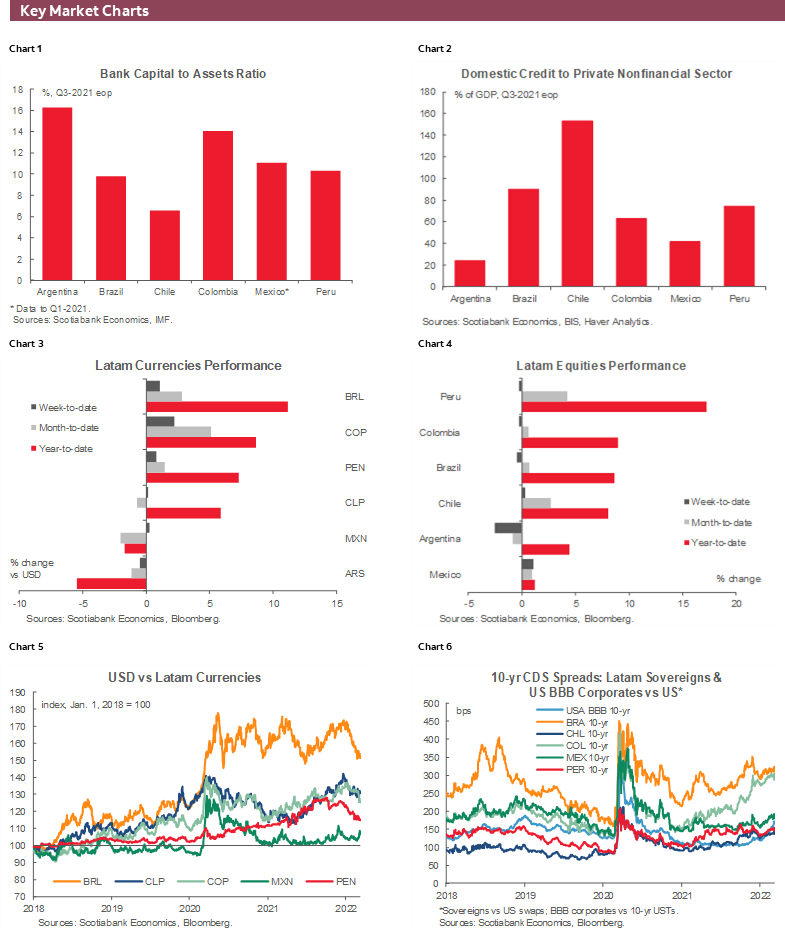

High commodity prices have also had an impact on Latam financial markets. Since the start of the year, most regional currencies have appreciated against the US dollar, as geopolitical risks mounted (chart 3). Mexico, which is no longer a net oil exporter, and Argentina are the exceptions to this rule. Equity markets have likewise risen despite the increase in uncertainty, with gains recorded across the region (chart 4). Peru stands out in this regard. The strong performance may be attributable to a reduction in political risk, as the president has attempted to steer a more moderate course, though as Scotiabank’s team in Lima have repeatedly pointed out there is no lack of political uncertainty.

Financial market developments should also be viewed in long-term perspective. In this regard, the appreciation of the PEN since mid-2021 stands out (chart 5), while the Chilean and Colombian currencies have depreciated in tandem with their widening current account deficits. At the same time, while Mexico’s peso depreciated sharply at the outset of the pandemic in March 2020, consistent with the shock absorber role under inflation-targeting, and quickly returned to its pre-pandemic trading level, the Brazilian real has traded in a persistently higher range since March 2020. Similarly, while CDS spreads on Latam sovereign bonds widened significantly early in the pandemic, most have narrowed considerably except for those of Brazil and Colombia (chart 6).

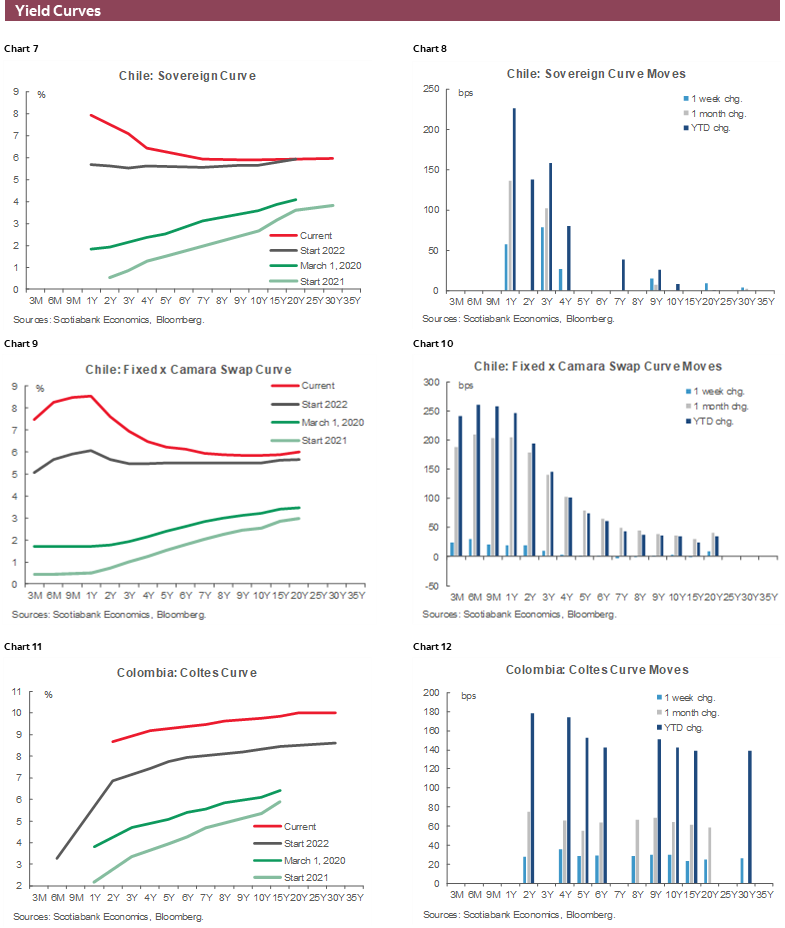

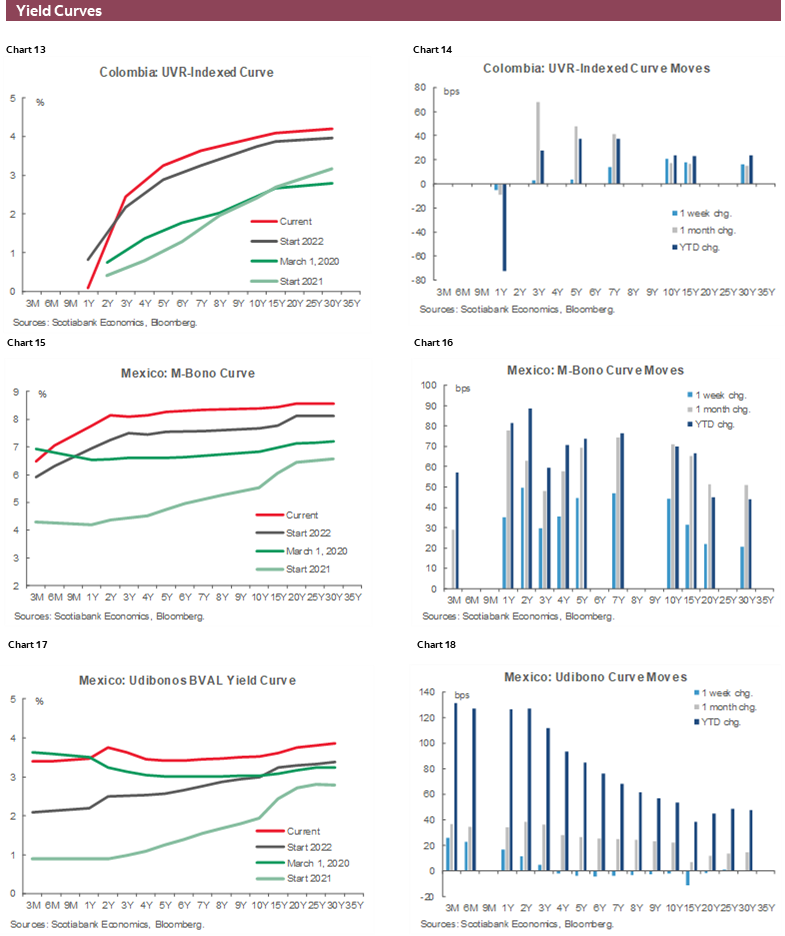

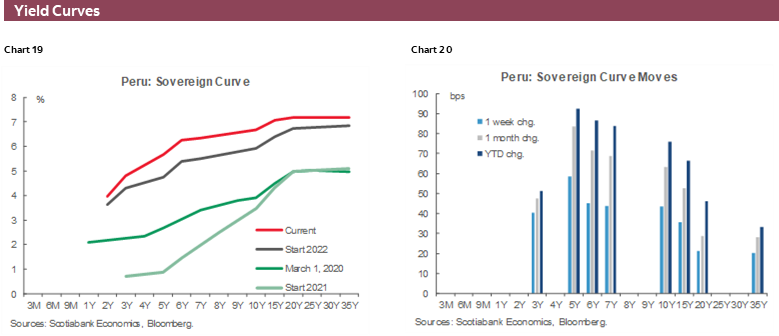

YIELD CURVE CHARTS

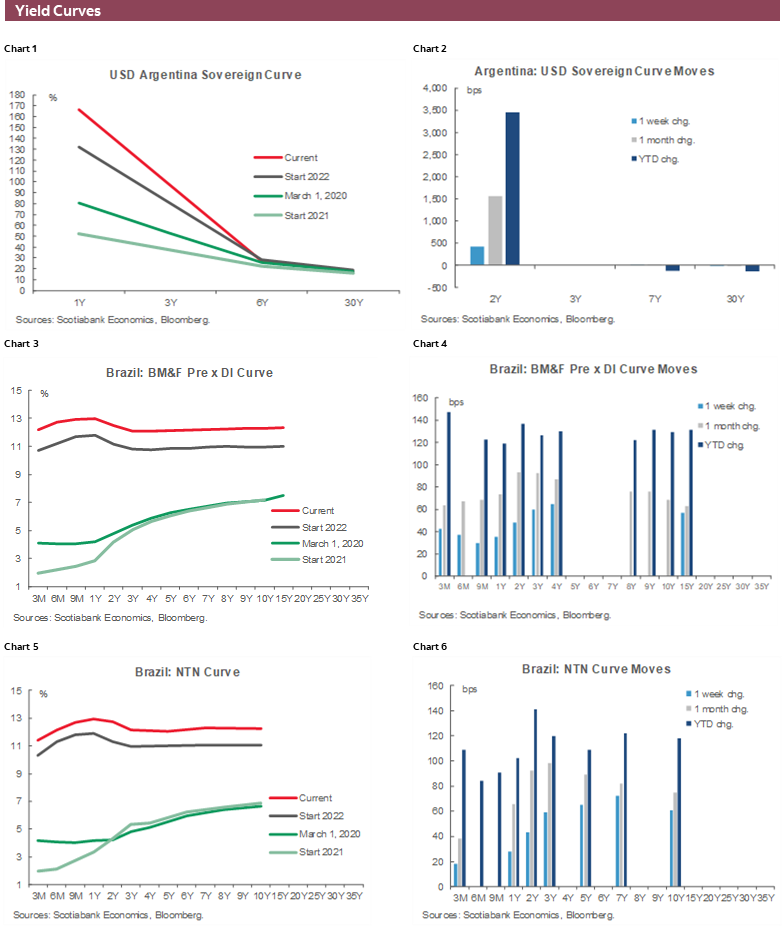

Sovereign yield curves have shifted higher across the Latam region since the start of 2022 (charts 1–20). Argentina’s curve remains highly inverted, with the negative slope progressively increasing over time. Brazilian and Mexican sovereign curves have flattened, with the short-end pricing in the higher short-term rates needed to contain inflation. Chilean yield curves, meanwhile, have inverted since the start of the year, possibly signalling an expected growth slowdown. In contrast, Colombia’s and Peru’s sovereign curves continue to slope upwards, as interest rates have risen across the maturity spectrum.

KEY COVID-19 CHARTS

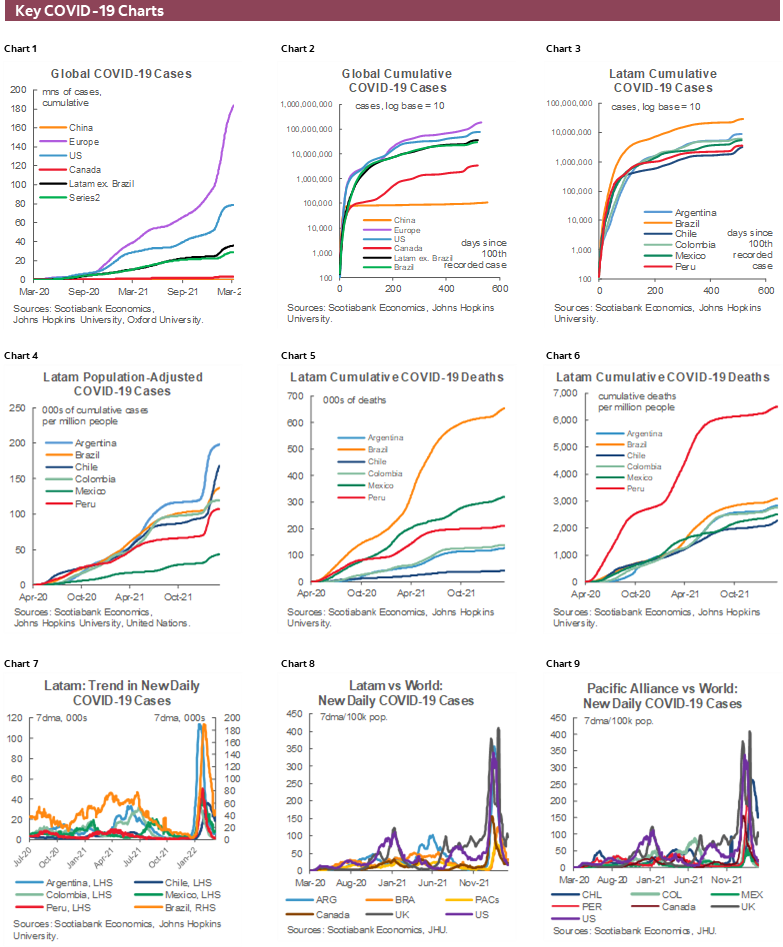

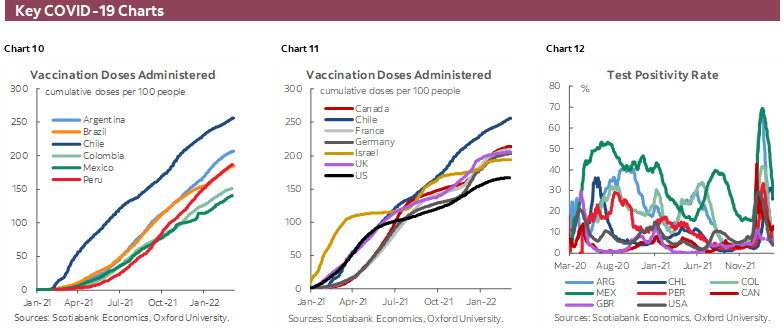

While the war in Ukraine has generated new uncertainties with respect to global economic prospects, the news from the pandemic front is encouraging. Key COVID-19 monitoring charts (charts 1–12) show sharp declines in cases in the region (chart 7) and around the globe (chart 8). Vaccination programs continue, with Chile leading the region (chart 10) and the world (chart 11) in terms of doses administered. Meanwhile, test positivity rates have fallen from the highs recorded only a few weeks ago (chart 12).

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Forthcoming |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

| COSTA RICA | |

| Website: | Click here to be redirected |

| Subscribe: | estudios.economicos@scotiabank.com |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.