- Recovery progressing, but risks remain and uncertainties with respect to growth and inflation cloud the outlook.

- Central banks in the region must carefully assess those risks in calibrating the pace at which to unwind expansionary monetary policy.

- COVID-19 remains a critical source of uncertainty. Indicators such as vaccine doses administered and test positivity rates may be useful guides.

KEY ECONOMICS CHARTS

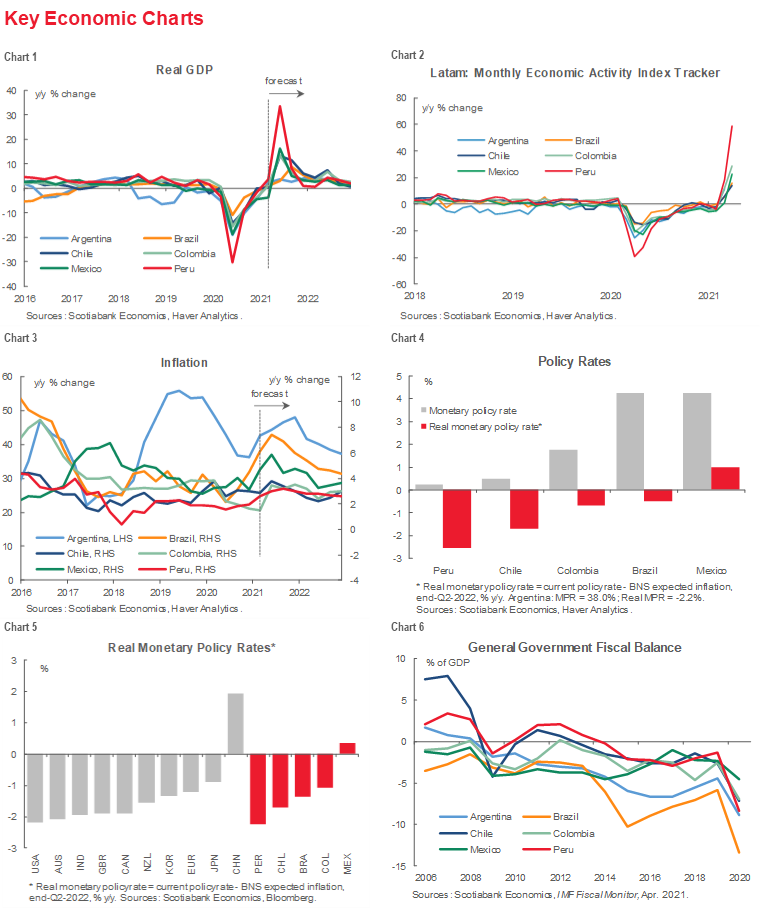

Latam economic recovery from the COVID-19 shock continues. Real GDP is projected to bounce back from the sharp contraction in 2020 across the region (chart 1), though progress is expected to be slower in Argentina.

The Monthly Economic Activity Index Tracker is signalling an especially robust recovery in Peru (chart 2). High year-over-year growth rates should be interpreted with caution, however, given base effects that result from comparing current levels of activity to levels depressed by stringent lockdowns imposed at the outbreak of the pandemic a year ago. Our team in Bogata note, for example, that the economic activity indicator increased 0.3% m/m on a seasonally adjusted basis and 28.7% y/y, but remains below its pre-pandemic level in February 2020.

At the same time, the outlook for the region is subject to several pandemic-related uncertainties. The re-imposition of a lockdown in Santiago could slow the pace of Chile’s recovery. And in Mexico, where April retail sales data fell -0.4% m/m on a seasonally adjusted basis in real terms after two consecutive monthly increases, a sharp rise in COVID-19 test positivity (see below) underscores the risks that remain.

Stronger growth and a range of temporary factors have pushed inflation higher (chart 3).

Economic recovery has been supported by extraordinarily supportive monetary and fiscal policies. Central banks across the region have driven key policy rates down (chart 4), which when adjusted for expected inflation are negative in “real” terms across most of the region. Mexico is the exception. The surprise 25 basis point increase by Banxico on June 24 reinforces that stance. Overall, real monetary policy rates in Latam countries broadly compare with rates of other central banks (chart 5).

As noted in the Latam Weekly published June 18, an unexpectedly hawkish dot plot chart of Fed governors’ beliefs with respect to future interest rate levels underscores the need for policy makers to assess the implications for future rates and carefully monitor the pace at with output gaps are closing.

This process was underway even before the Fed’s chart was published. In Chile, the central bank (BCCh) published minutes of its latest monetary policy meeting, held June 8, 2021. The BCCh’s Board voted unanimously to keep the monetary policy rate at 0.5%, confirming its’ gradual approach to normalizing rates, but discussed a possible 25 basis point increase. While the central bank is attuned to the possibility that robust growth could close the output gap faster than expected, risks related to COVID-19 and softer copper prices remain. Scotiabank economists in Santiago continue to expect that the BBCh will pull the trigger on the first rate hike at its’ meeting scheduled for October 13, 2021.

Similarly, Peru’s central bank (BCRP) raised its’ inflation forecast for 2021 from 2% to 3% at an annual rate in the monetary policy report released June 18. That puts expected inflation at the high end of the BCRP’s target band. Our team in Lima reports that, while the central bank cited temporary factors, particularly higher import prices, behind the rise, the BCRP removed the reference to a “prolonged period” of expansionary monetary policy. Nevertheless, Scotiabank economists expect the first rate hike in mid-2022.

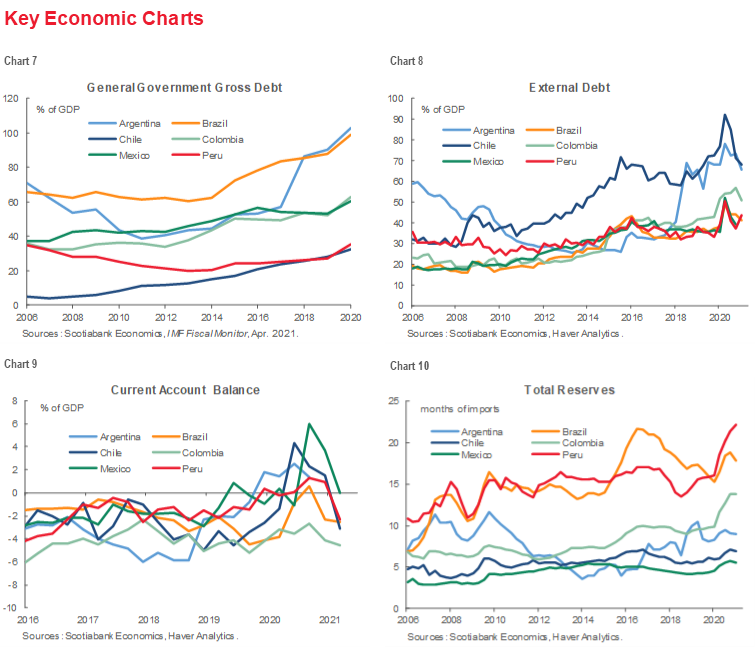

Fiscal policy across the region provided a counter cyclical impulse as the general government fiscal balances deteriorated sharply (chart 6). Fiscal measures partially cushioned vulnerable individuals from the pandemic shock and have contributed to economic recovery. Going forward, governments will have to closely watch debt sustainability indicators, such as general government gross debt (chart 7) and external debt (chart 8). Too rapid increases in external debt reflecting large current account deficits (chart 9) could undermine confidence, particularly if accompanied by a decline in reserve accumulation (chart 10).

FINANCIAL MARKET CHARTS

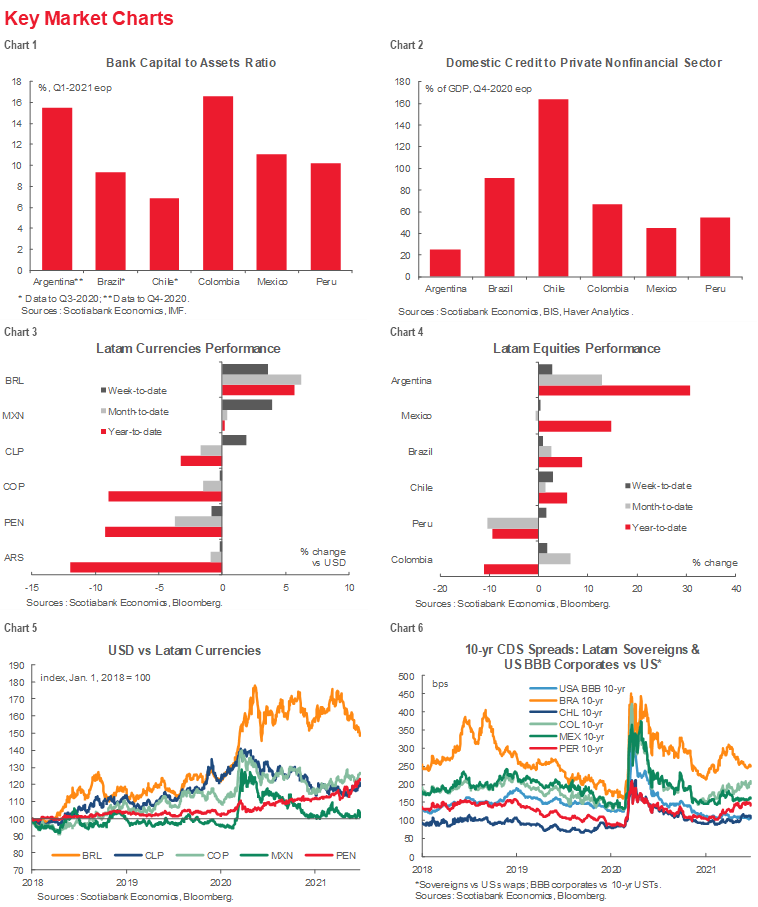

Such effects would likely spill over to financial markets, especially foreign exchange markets. Most Latam currencies have depreciated against the US dollar since the start of the year (chart 3), with the Brazilian real being an exception. Over a somewhat longer-term perspective, only the Mexican peso has remained stable valued against the US dollar (chart 5).

In contrast, equity markets have risen in most countries (chart 4). Markets have underperformed in Peru and Mexico, possibly reflecting political uncertainty associated with the presidential elections in former and the effects of nationwide protests that led to sporadic disruptions of production in the latter. Both factors may have eroded investor confidence.

Confidence effects may also account for developments in 10-year CDS spreads on Latam sovereign bonds versus US swaps (chart 6). Spreads on Colombian and Peruvian sovereigns widened in recent while those on other Latam sovereigns narrowed or remained broadly stable.

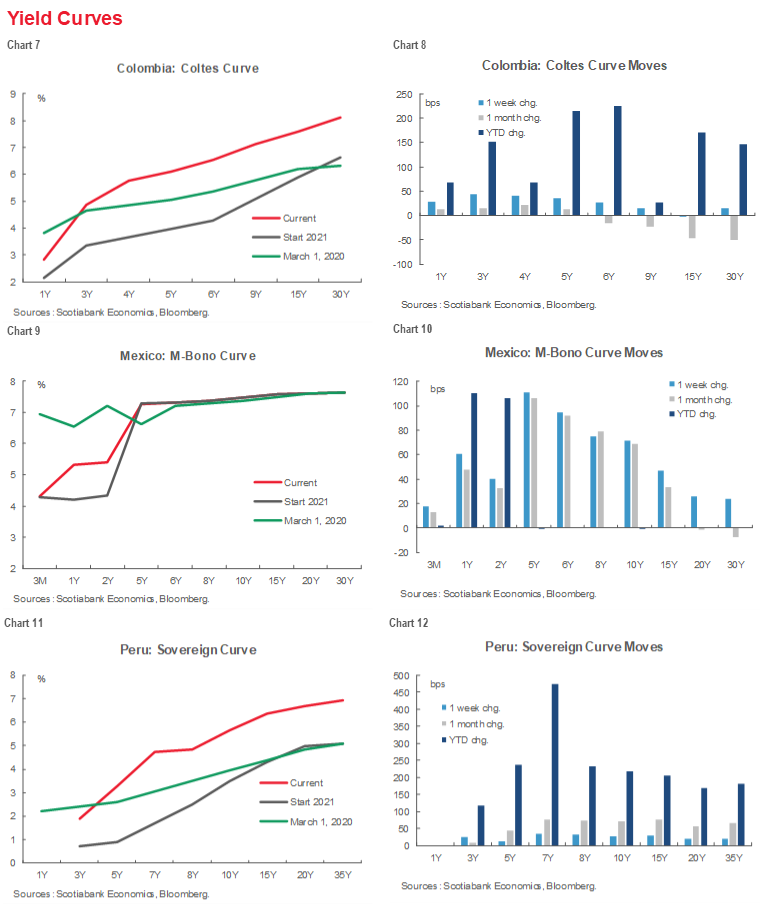

YIELD CURVES CHARTS

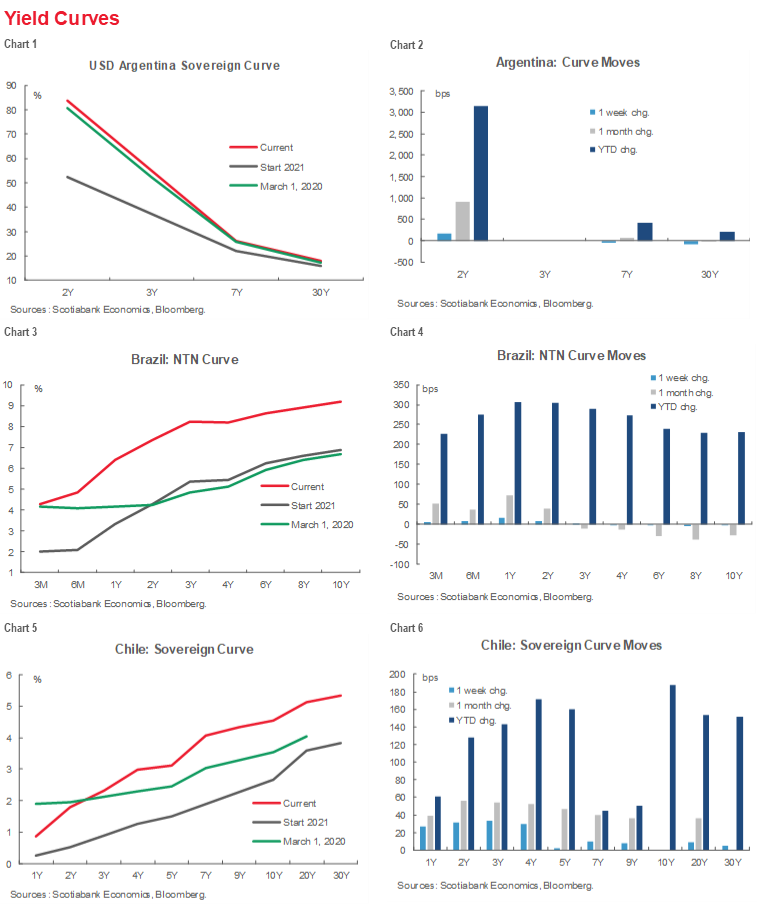

With inflation expectations on the rise, sovereign yield curves have generally shifted up across the region. Sovereign curves for Brazil (charts 3, 4), Chile (charts 5, 6) , Colombia (charts 7, 8) and Peru (charts 11, 12) have all moved higher across the maturity spectrum. Yield curves on Argentine (charts 1, 2) and Mexican sovereign bonds (charts 9, 10), in contrast, remain at roughly the same position at which they started the year.

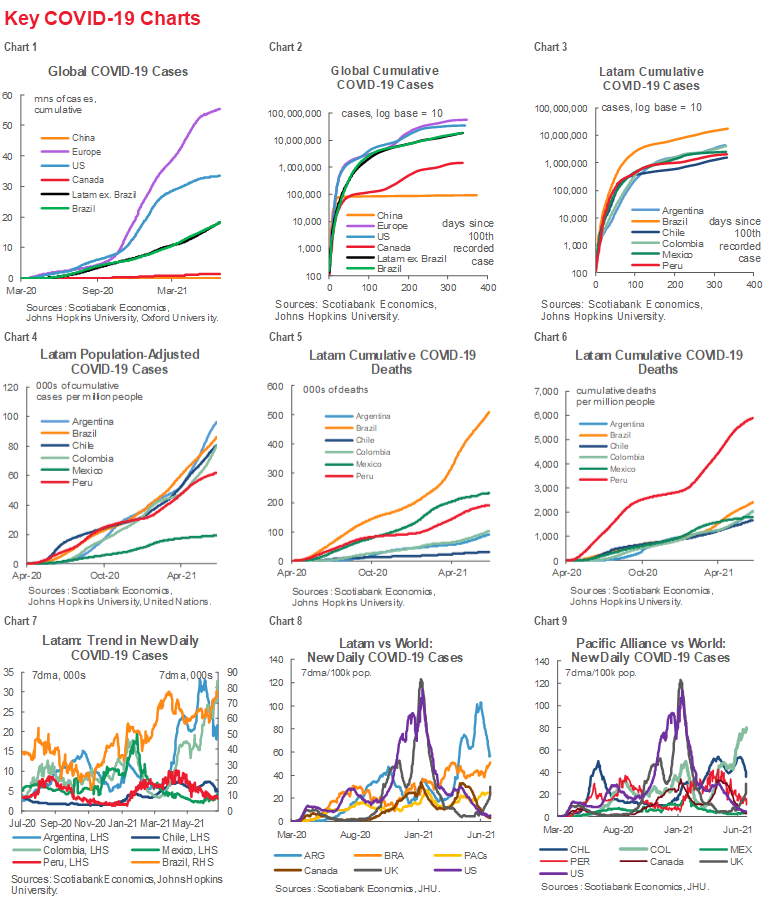

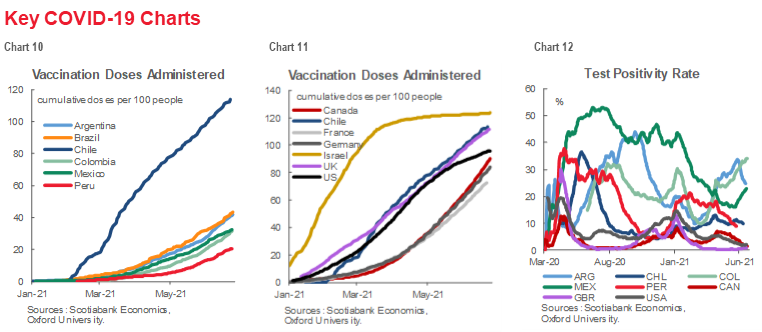

KEY COVID-19 CHARTS

In calibrating the pace at which to unwind extraordinary policy responses, central banks must carefully assess risks to the economy. As noted above, COVID-19 continues to pose threats to economic recovery. Charts 1–9 monitor the human toll of the pandemic; charts 10–12 provide insight on risks. Chile leads the region (chart 10) and most of the world (chart 11) in terms of vaccine doses administered. Declines in test positivity rates across most of the region (chart 12) is encouraging, though recent upticks in Colombia and Mexico warrant careful monitoring.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | carlos.munoz@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Forthcoming |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

| COSTA RICA | |

| Website: | Click here to be redirected |

| Subscribe: | estudios.economicos@scotiabank.com |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.