- War in Ukraine, higher inflation resulting from supply-side and commodity price shocks, and fears of a possible escalation in geopolitical tensions increase uncertainty with respect to the global outlook.

- Despite these concerns, however, there may be reason for optimism that growth is possible in a time of uncertainty.

- That felicitous outcome may be the case for the Latam region, where early action by central banks to safeguard their price stability commitments could be paying a growth dividend.

Russia’s ill-conceived and poorly executed invasion of Ukraine, now in its fourth month, continues to impart uncertainty to the global economy. Higher inflation, resulting from a spike in energy prices, concerns that advanced country central banks were behind the tightening curve—requiring more aggressive interest rate hikes that could possibly lead to recession—and fears of an escalation in the fighting beyond the two principal combatants cloud the economic outlook. Yet, despite the miasma of doubt that masks near-term prospects, and which accounts for the selloff in markets in April and May, there are reasons for modest optimism.

Growth, it seems, is possible in a time of uncertainty. The case for optimism stems in part from the market’s muted reaction to clear indications that the major central banks “get it,” that they are prepared to move as needed to protect price stability commitments. In this respect, higher short-term inflation should not become entrenched in expectations, preventing a possible wage-price spiral that could impair long-term growth. In the US, for example, expectations appear to remain well anchored even with the sharp increase in inflation observed over the past six months or so. While markets expect inflation to remain high over the short-term, inflation is expected to ease back over the medium-term. Meanwhile, absent additional supply-side shocks to global supply chains or further commodity price hikes, base effects should begin to exert an influence on inflation. There is even reason to hope that pressure from the White House, coupled with the enlightened self-interest of key oil producers, may provide some relief from high world oil prices. OPEC is not served by a global recession that quashes energy demand.

KEY ECONOMIC CHARTS

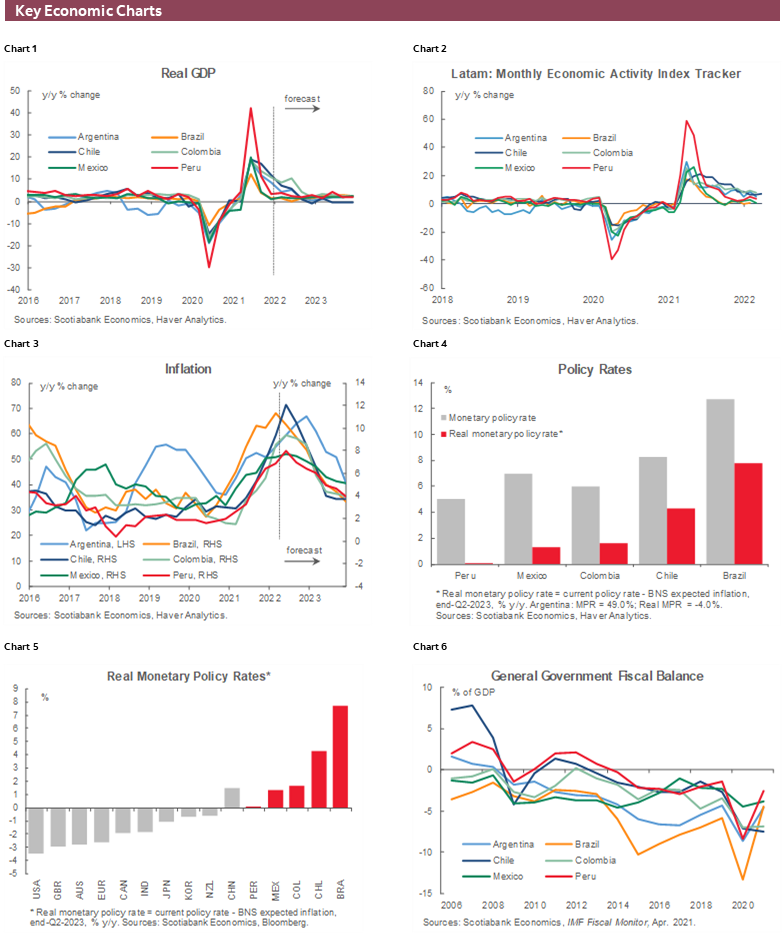

For Latam countries, recent data releases support the contention that growth is possible in a time of uncertainty. Scotiabank economists in the region continue to expect growth to gradually slow from the high rates recorded in 2021 following the severe contraction of 2020 (chart 1). For the most part, they anticipate growth to converge on pre-pandemic rates over the next year or so. While the risk of recession remains a possibility, it is judged to be modest, with high-frequency activity indicators suggesting continued growth (chart 2). Indeed, recent surprises have, if anything, been on the positive side.

High inflation (chart 3) remains a challenge—albeit one that Latam central banks began tackling well before their advanced country counterparts. That early action signaled a credible commitment to their inflation targets. And with central banks intent on price stability, Scotiabank teams anticipate inflation rates across the region to gradually return to their respective target ranges over time.

Talk of price stability without the requisite tightening actions would provide little reassurance. Latam central banks have backed up tough talk with concrete policy actions, however, progressively raising key policy rates over the past year. Policy rates are now positive in real (after-inflation) terms across the region (chart 4), significantly so in the case of Brazil and Mexico. In this respect, they are ahead of most of their international peers (chart 5), reflecting their proactive approach to price stability. Scotiabank economists are quick to note that further rate rises are likely before the end of the current tightening cycle. In the case of Peru, policy rate hikes have been combined with increases in reserve requirements.

Sustained growth together with the winding down of pandemic supports has helped bring down fiscal deficits across the region (chart 6). As the last edition of the Latam Weekly highlighted, government fiscal support to the most vulnerable and measures that protected household and corporate balance sheets likely provided a solid foundation for robust recovery. But with recovery transitioning into expansion, such supports should be withdrawn consistent with fiscal rules designed to ensure the sustainability of public finances over the medium-term.

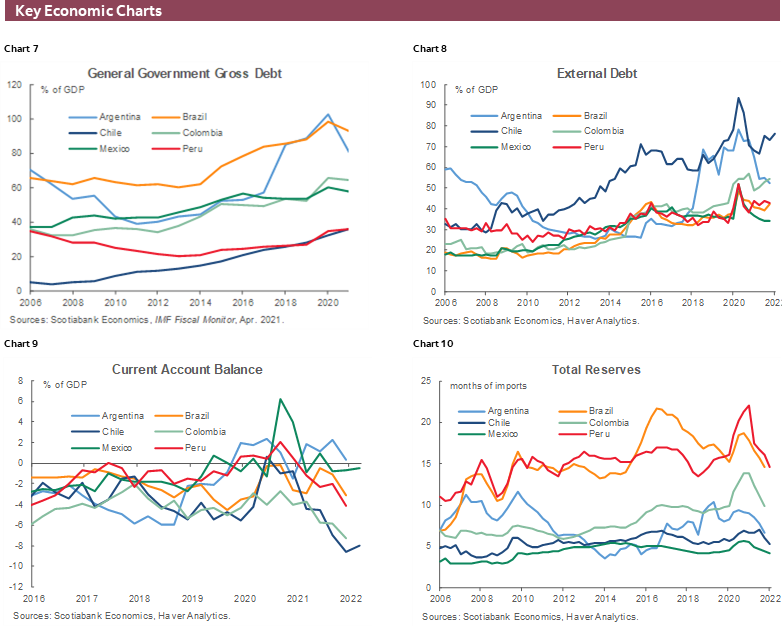

Fiscal rules that constrain debt as a share of GDP (chart 7) can also help to limit external debt as a share of GDP (chart 8). Both indicators are closely watched by investors; in a time of uncertainty, they become even more important metrics. In the context of shifts in investor risk appetite and portfolio rebalancing animated by higher advanced country interest rates, as has been the case over the past month or so, current account deficits (chart 9) and the level of international reserves (chart 10) are also closely monitored as indicators of financing needs and liquidity, respectively. While Colombia’s current deficit is large, our team in Bogota notes that it is expected to narrow over the year as a share of GDP given strong growth, and large FDI flows financing the current account deficit reflect inflows that add to productive capacity.

KEY MARKETS CHARTS

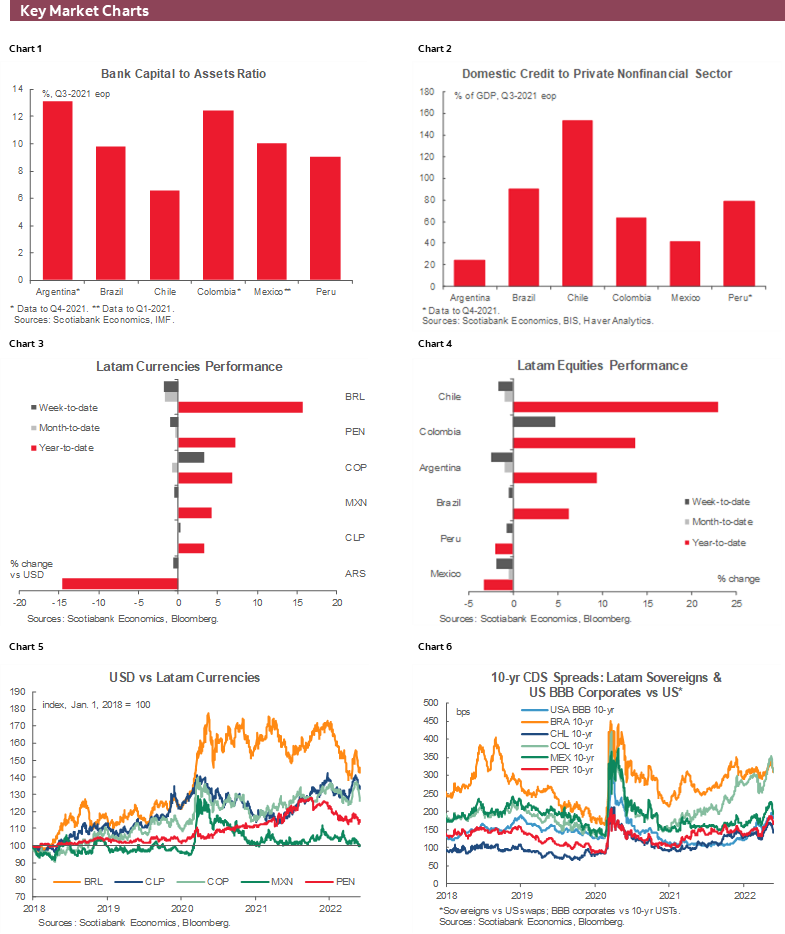

Latam financial markets have performed well in an uncertain global economy. Currencies across the region except for the Argentine peso have appreciated against the US dollar since the start of the year (chart 3). In some respects, this performance is a surprise given that past episodes of Fed tightening have generally been accompanied by steep depreciations (which can fuel price pressures through exchange rate pass-through effects). But as noted above, early, and clearly communicated, policy moves by central banks likely anchored expectations with respect to inflation, supporting currencies, while higher rates provided positive interest rate differentials. Equity markets have likewise risen in most of the region since the start of the year (chart 4), with Chile’s market leading the region and the markets in Mexico and Peru down, possibly reflecting heightened levels of political uncertainty that cloud the investment climate. The effects of political uncertainty may also be visible in a longer-term perspective on currencies (chart 5) as well as sovereign debt CDS spreads (chart 6), which shows a marked widening in Colombia likely reflecting uncertainties surrounding the presidential elections. With that uncertainty now likely to dissipate following the results of the first round of voting on May 29, that spread may narrow.

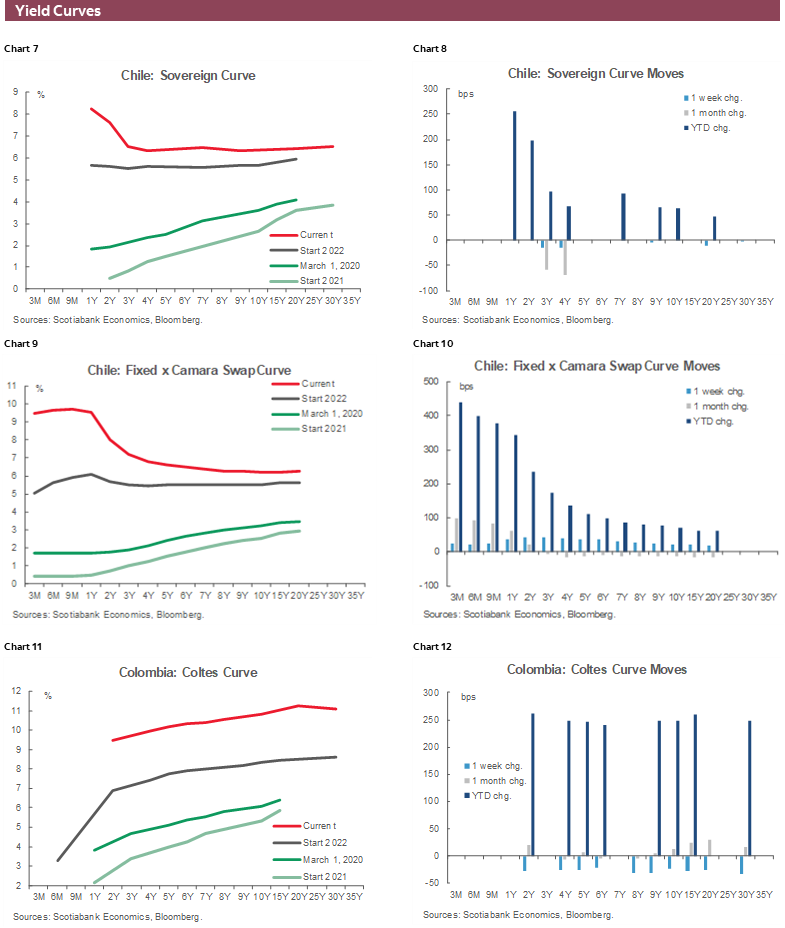

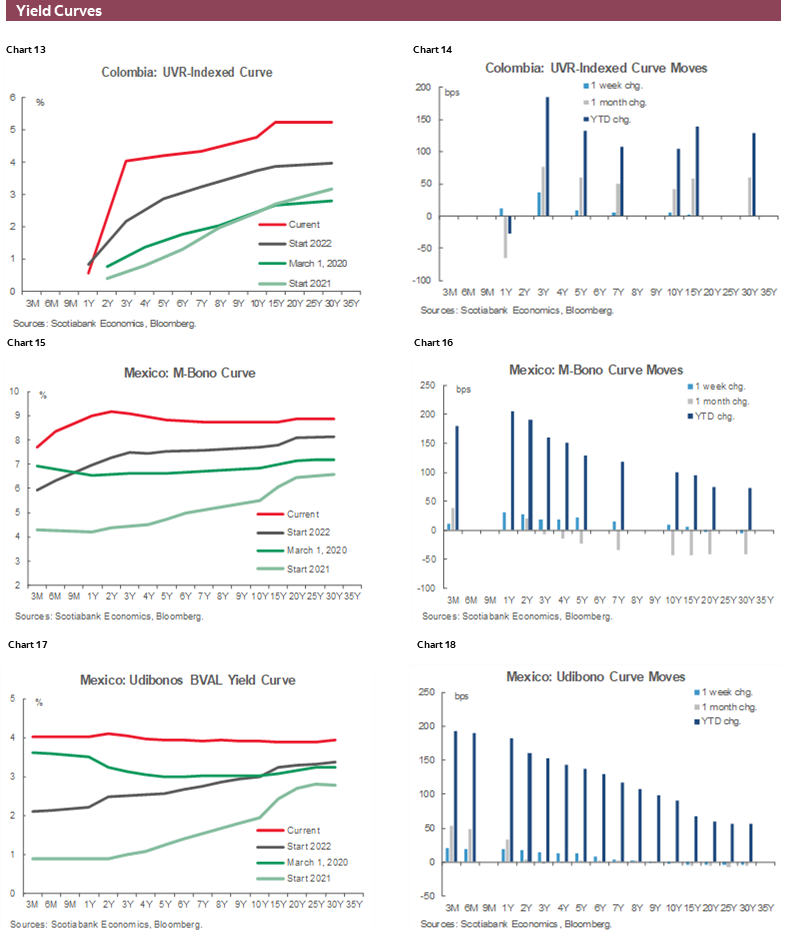

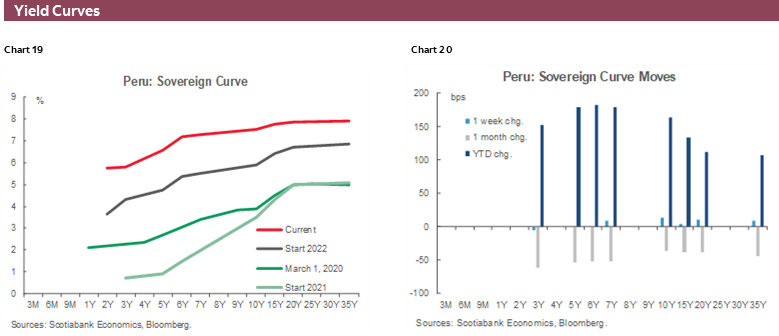

YIELD CURVE CHARTS

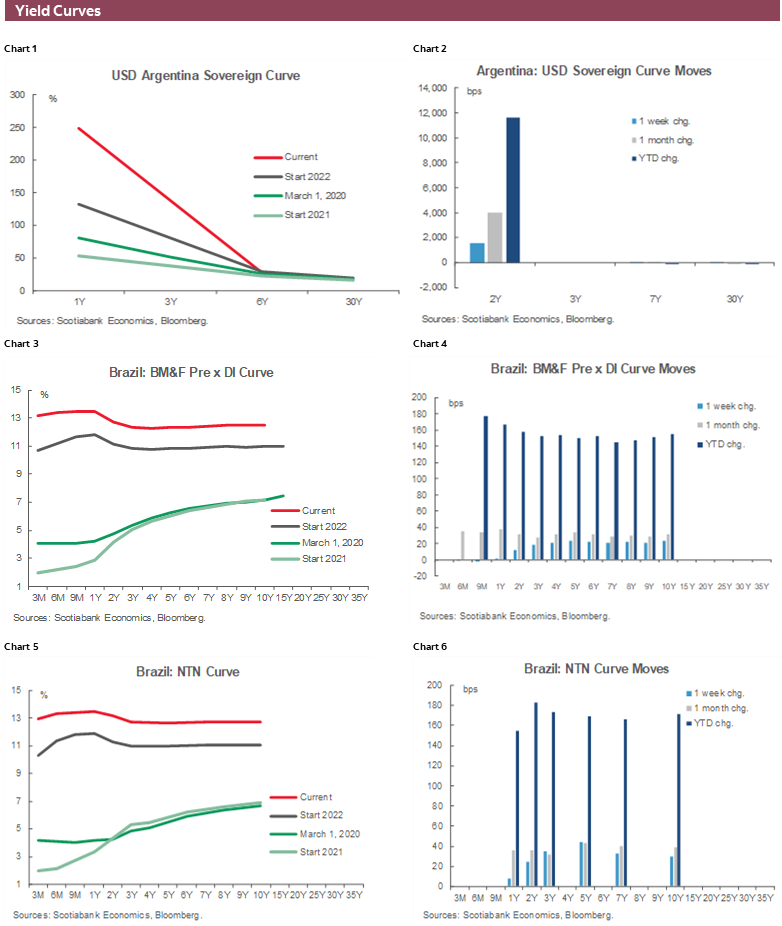

Yield curves across most of the Latam region are inverted or flat, with Colombia and Peru exceptions. While the former configuration is thought to provide early warning of a possible recession in advanced economies, that statistical regularity has not been investigated as thoroughly with respect to emerging markets; in any event, there are yet no signs of impending recession.

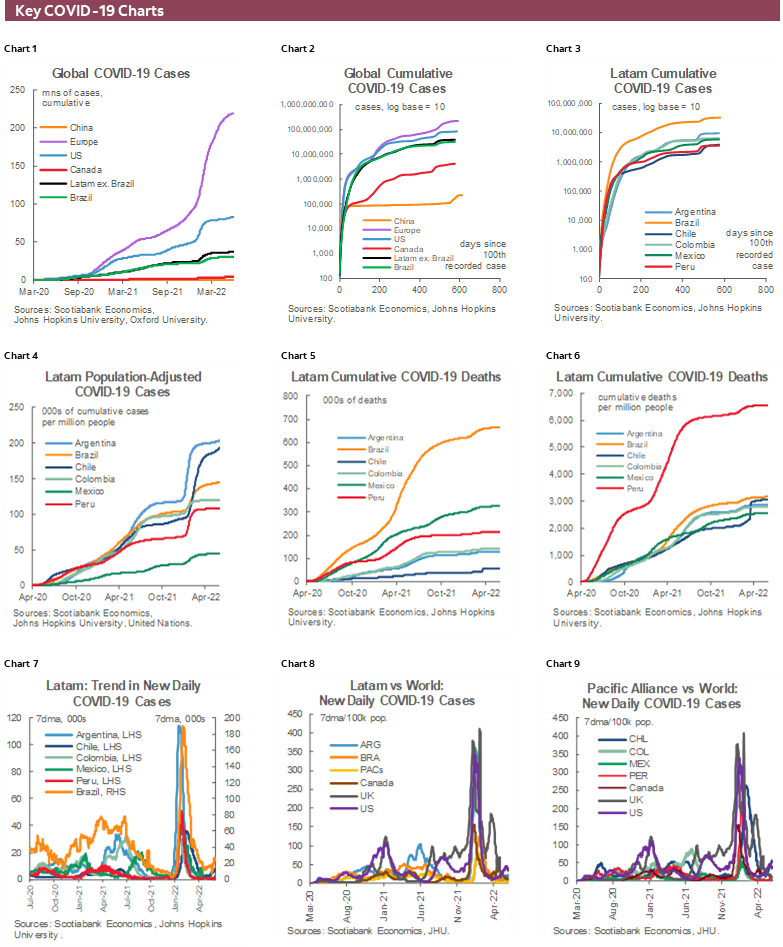

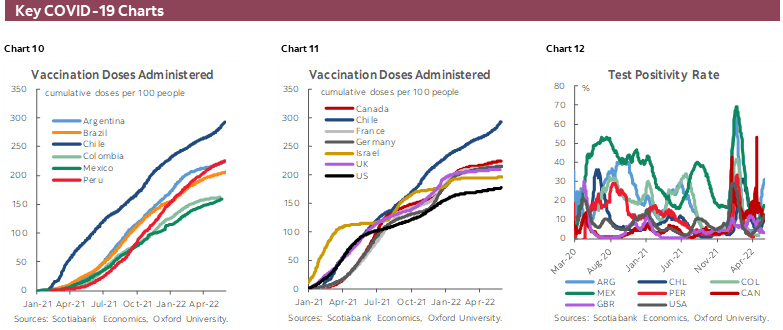

COVID-19 CHARTS

War in Ukraine and the threat of higher inflation have largely pushed the pandemic from the headlines. Rising cases in several parts of the world and China’s determined implementation of its “zero-COVID-19” policy show that COVID-19 remains a public health concern, one that can still have economic repercussions. Key monitoring charts are provided below.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Forthcoming |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

| COSTA RICA | |

| Website: | Click here to be redirected |

| Subscribe: | estudios.economicos@scotiabank.com |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.