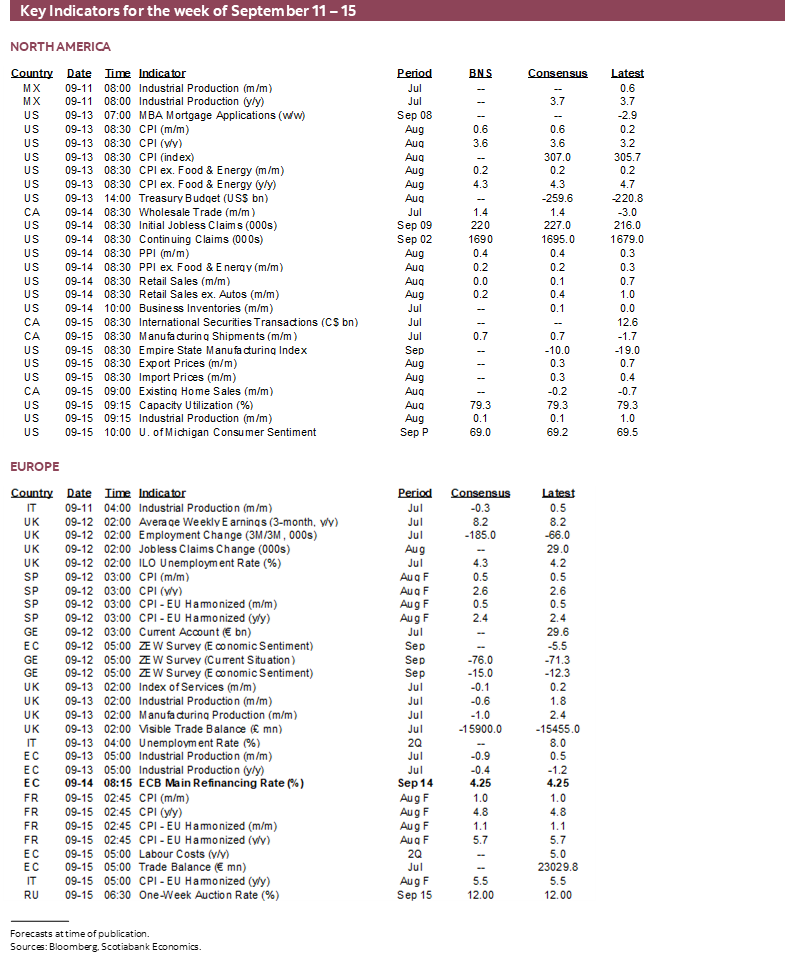

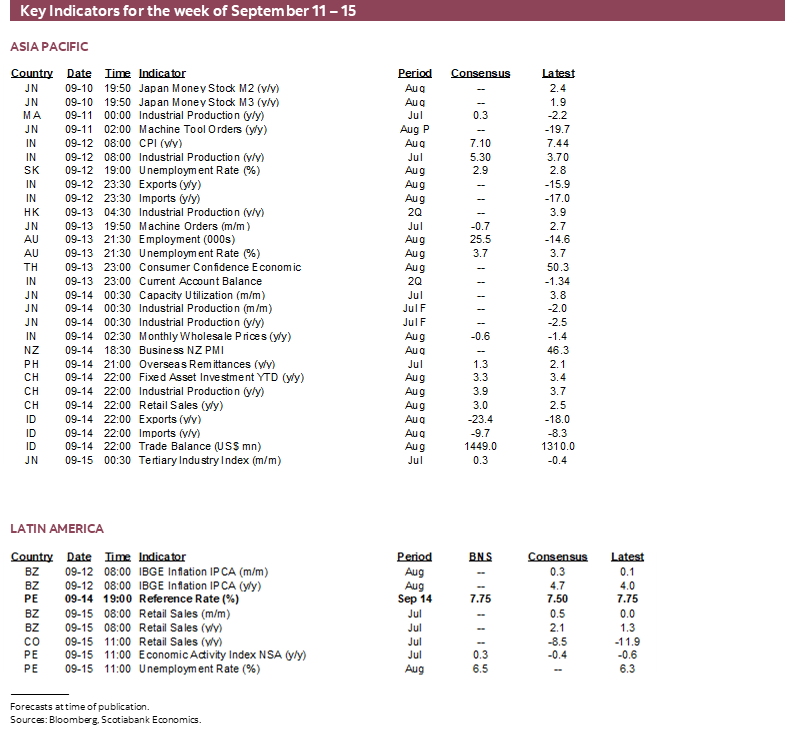

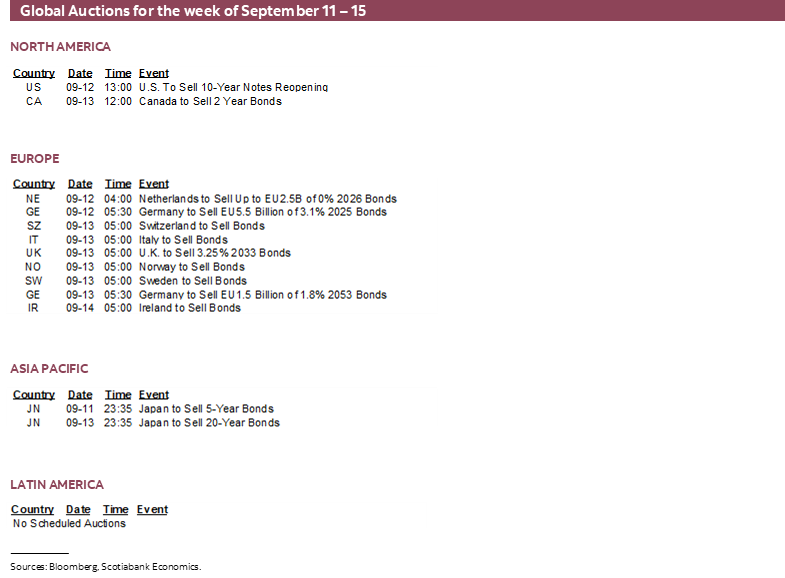

Next Week's Risk Dashboard

- Meddling with the Bank of Canada wouldn’t be costless

- US CPI inflation likely to reinforce a Fed pause

- The ECB decision is on a knife’s edge

- PBOC expected to hold

- Is China’s “deflation” gone already?

- China macro to inform downside risks

- US retail sales were probably soft

- Australia’s jobs might rebound

- UK jobs, wages to influence the BoE’s next decision

- Will Peru’s central bank join neighbours in cutting?

- Other global macro

Chart of the Week

The pressures facing global central banks are becoming more apparent after a protracted period of policy tightening and amid uncertainty over next steps. Recent developments in Canada put markets on heightened alert toward the risk of political meddling with the affairs of central banks ahead of decisions by the ECB, PBOC and Peru’s central bank. US CPI could inform the Federal Reserve’s next moves, while a wave of major global macroeconomic readings could motivate significant market volatility in a traditionally volatile month for risk appetite.

MEDDLING WITH THE BANK OF CANADA WOULDN’T BE COSTLESS

I have a proposal. If politicians truly support the Bank of Canada’s independence, then it seems to me that the most elegant solution would be to simply stop talking about it!

This past week’s developments rejected that advice. I think market participants need to treat seriously the risk that Canada’s politicians pose to the central bank including building upon momentum toward seeking to change its mandate in the years ahead. I’ll do so by highlighting recent developments in the context of prior ones and by explaining why it could be a big mistake to mess with the existing monetary policy framework.

International Precedence

There is precedence for governments changing the focus of central banks. This isn’t just in places like Turkey or this past week’s controversy in Poland. It has also happened in places where central banks have been successful, early adopters of inflation targeting practices.

Recall that in 2018, New Zealand’s Finance Minister changed the RBNZ’s mandate by adding employment alongside price stability. Some think that backfired in that perhaps the RBNZ’s aggressive policy tightening was subsequently amplified coming out of the pandemic because of soaring employment, although that’s unclear versus the greater likelihood that an early adopter of inflation targeting was focused upon inflation.

What happens, however, if in future New Zealand witnesses weakening employment alongside structurally persistent inflationary pressures in a very open economy? Will the RBNZ still defend its hard-won inflation fighting credentials? Or will the country pay an inflation premium in its borrowing costs on international markets because supporting employment has become more important?

The Thin Edge of the Wedge

Surely that couldn’t happen in Canada, right? After all, Governor Macklem reinforced the central bank’s independence this past week and Minister Freeland said she respected that. The problem is that actions by the Government have conflicted with this guidance.

In Canada, the controversy started in December 2021 with the Monetary Policy Framework Renewal agreement. A recap of what went down at that time is available here. The agreement had been delayed by the Finance Minister—driving speculation of disharmony between the BoC and the Finance Department—and then sprung in hastily organized fashion. It said that targeting low and stable inflation at a 2% pace over the medium-term is the central bank’s “primary” policy target, but for the first time ever the accompanying language added all sorts of muddled talk on full employment and inclusion goals that should be considered by the central bank.

I well recall the awkward press conference that was thoroughly dominated by the Finance Minister even on questions concerning the Governor’s subject matter of expertise. The addition of this muddled language sowed market confusion and prompted a dovish reaction at the time of the communications out of concern that lip service given to inflation targeting was now pivoting toward interference in the name of other policy goals of the Federal government. The C$ would lose about two cents to the USD by the time the dust settled over the next couple of days. This market reaction highlighted the sensitivity of financial markets to tweaking the mandate. Nothing really changed, yet everything changed by way of the effort to add the Finance Minister’s spin on what monetary policy should focus upon and for the first time ever in the long sequence of renewed agreements dating back to over three decades of inflation targeting at the BoC.

Did this change impact anything? I don’t think the fact that the BoC ignored inflation’s warning signs through 2020H2 and 2021 was because of this muddled set of tweaks to the renewal agreement. I think it just messed up its judgement and spent too much time listening to nonsense about base effects, gas prices, transitory drivers, misleading analysis that the type of inflation we were getting wasn’t the type they could or should confront etc. Scotiabank Economics was in the minority of voices strenuously arguing that inflation risk was being underestimated and that the BoC would be hiking much earlier and faster than its guidance at the time in favour of a multi-year hold.

Nevertheless, the optics around why the BoC was too dovish for too long are not incompatible with being excessively focused upon the job market that ultimately overshot full employment equilibrium. We heard both Macklem and Fed Chair Powell speak of fully inclusive job market recoveries throughout the too-easy-for-too-long period!

This Past Week’s Developments

Now enter this past Wednesday’s press release (here) as the next step and with further possible steps that I’ll get to. I think it was inappropriate for three reasons.

It shouldn’t have been released on the heels of a BoC policy decision in the first place.

The second paragraph intimated that the BoC is maintaining overly tight monetary policy relative to how the Minister defines inflation which is not how the BoC defines it. The Minister flagged inflation at 2.4% y/y excluding mortgage interest and the way it was written suggested that rates are therefore too high. The release basically said Finance knows better than the Bank of Canada when it comes to interpreting inflation statistics, and yet the measures of core inflation that the BoC uses don’t even include mortgage interest. Trimmed mean CPI and weighted median CPI have been excluding mortgage interest and are running at 4.2% m/m SAAR and 3½% on a trend basis. They are used as operational guides to achieving the 2% headline inflation target on a durable basis over time by focusing upon the breadth of underlying price pressures.

The Minister’s remark that she will “use all the tools at my disposal….to ensure that interest rates can come down as soon as possible” was either sloppily written, an error in judgement or a signal of what lies ahead. Interest rate policy is the domain of the central bank. Or perhaps the Minister meant that she will finally get spending under control in order to lessen the impact on inflation of ongoing fiscal stimulus provided by federal and provincial governments.

Provincial Premiers also joined the assault against the Bank of Canada. They carry no direct sway over the Bank of Canada but used their pulpits to attempt to apply pressure upon it. As with the Federal government, their criticism of rate hikes is rather rich since their excessive spending drove a material amount of the inflation that Canadians have faced and with it a material share of the rate hikes. A personal reminder of this came upon renewing my driver’s licence in Ontario for two years free of charge which will come in handy while dodging potholes.

The Next Milestones

The current inflation renewal agreement expires at the end of 2026. A new one will have to be crafted by that point. This will be after another Federal election that has to occur on or before October 20th 2025.

Meddling with the Bank of Canada’s mandate risks becoming a major issue on the campaign trail and could sow market instability. If the same government remains in office, then are the signals that are being sent paving the way for adjusting the Bank of Canada’s mandate? If another government is in place, then are we sleepwalking into whether there will be a new Governor on or before the expiry of Macklem’s seven-year term in June 2027? What policy bias may such a person have?

Either scenario risks sparking confusion and turmoil in markets and cannot be discounted.

The Dangers

Giving the Bank of Canada not only a dual mandate that expands from price stability to full employment but goes one step further in requiring it to achieve fully inclusive labour market outcomes poses several dangers.

For one, monetary policy’s strength lies in terms of controlling inflation as the best way over time to support maximum employment. Diverting its attention toward supporting employment in the short term could come at the expense of price stability. Achieving fully inclusive outcomes can be a valid goal for boardrooms who have shareholders to answer to and for governments who face voters, but the blunt instruments of interest rate policy and balance sheet management are not well suited to such goals and attempting to use them in such manner could carry costs.

Now fast forward to 2026 in Canada. Let’s say the job market has weakened or is weakening by then, but perhaps inflation is still persistent and being driven by changed structural drivers. Would the BoC be less resolute in its focus upon achieving price stability because whatever government is in place by that point after the next election opted to fiddle with its mandate?

There could be several consequences.

i) Markets and Inflation Risk

For one, the market consequences could pivot inflation risk higher in such fashion as to drive a steeper Government of Canada bond yield curve through dovish short-term implications but higher longer-run inflation risk. That, in turn, could harm term mortgage borrowers and the longer-term financing costs of governments themselves relative to the status quo. The Government of Canada’s average term to maturity on its debt is just under eight years. Raising market pricing for longer-term inflation risk could raise the Government’s funding costs with trickle down effects throughout the entire rates complex including provincial and local governments, corporations and households. That would stink in terms of timing given the forces that have driven higher bond yields.

ii) Productivity

I believe that while Canada has had a productivity challenge for many years, the more rapid worsening through the pandemic era owes itself in part to excessive labour market supports that were too big for too long. They kept people in forms of employment that were less in demand and away from filling job vacancies in other sectors when the nature of the economy shifted.

It’s possible that what is behind any desire to mess with the central bank’s mandate is to shift the policy burden toward it if job market conditions deteriorate over coming years. It may be fiscally more challenging to provide support to the job market and so pass the baton to the BoC.

That could worsen the productivity problem by once again interfering in market mechanisms. To a degree, policy should support jobs and the economy during downturns, but there is always a fine line between doing too much and too little. In the longer run, too much can sow greater imbalances by driving productivity downward and labour costs upward.

Worsening Existing Pressures

Canada, in my opinion, already faces enough macroeconomic challenges and rising macroeconomic imbalances.

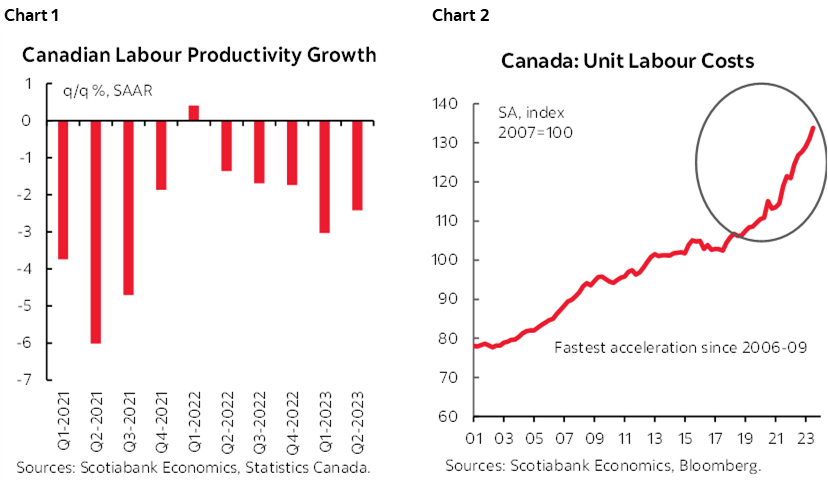

Productivity is in a tailspin (chart 1). Unit labour costs are soaring (chart 2). Its competitiveness is being severely strained relative to nearshoring winners like Mexico. This risks a hollowing out of what’s left of the manufacturing base or an even bigger bill footed by taxpayers as governments transfer more dollars to prop it up.

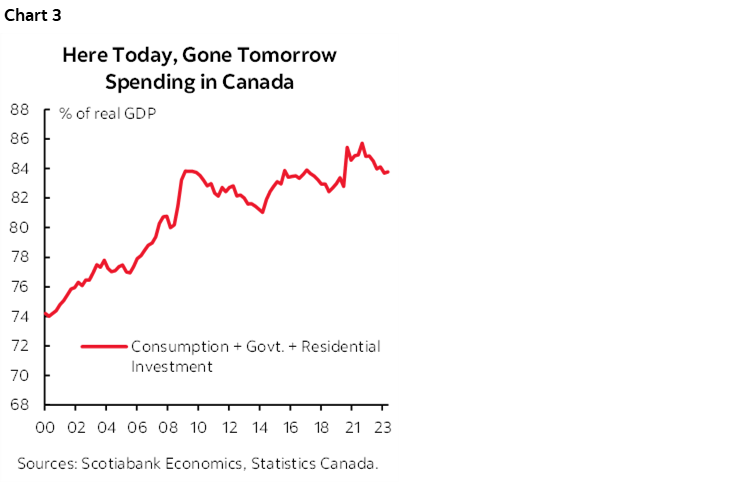

84% of GDP currently goes toward here-today-gone-tomorrow activities like consumption, housing and government spending which is up about ten percentage points in just over 20 years to a modern record high (chart 3). The fiscal policy bias remains pointed toward propping up this emphasis upon current consumption out of future potential.

One out of every two jobs created since the start of the pandemic have been in the public sector with nearly 200k more civil servants hired over this period.

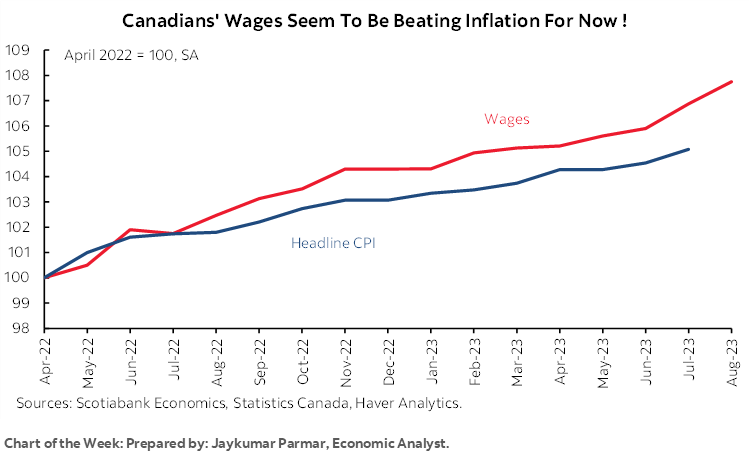

Inflation is still raging. Wage pressures remain pointed higher (recap here).

Alongside such deep-seated challenges to the country’s outlook, Canada does not need governments adding central bank meddling to the list. It would not be costless. It could drive worsened imbalances and the prospect of driving a financial crisis of confidence in the country cannot be ruled out.

Let me be clear that it is by no means certain that the BoC’s mandate will be changed. I would expect the central bank to put up a heck of a fight through the usual exhaustive ‘horse race’ between alternative mandates that pretty much always concludes that nothing’s better than 2%. I am saying, however, that the signals being sent and the international pressures on central banks including precedence to date merit paying very close attention to the dialogue around the Bank of Canada. We all have a stake in the outcome and being silent on the matter won’t guarantee a positive one.

US INFLATION—ROOM TO REFLECT AT THE FED

Another CPI inflation reading lands on Wednesday. August’s print has the potential to swing opinions on the FOMC into the September 20th decision, but I doubt it will. FOMC members have until Friday to submit their forecasts as input into an updated Summary of Economic Projections including the famed ‘dot plot’ and until the following Tuesday evening to submit changes on the eve of the decision.

Watch for a strong headline reading but soft core. I’ve gone with a 0.6% m/m seasonally adjusted increase in total CPI that would lift the year-over-year rate by about 0.4 points to 3.6%. Core CPI is estimated to rise by 0.2% m/m SA as the year-over-year rate ebbs by about 0.4 points to 4.3%.

Base effects should not materially impact the headline year-over-year rate but will continue to put downward pressure on core inflation benchmarked to what was happening at this time last year.

Gasoline prices will be a major driver of the jump in overall prices by adding several tenths of a percentage point to CPI.

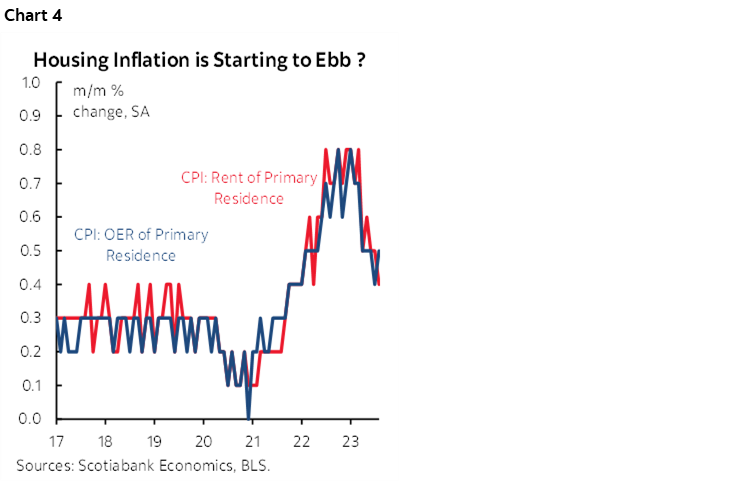

Shelter is likely to continue to trend toward being a lessening source of inflationary pressures as the lagging effects of weaker market rents increasingly drive weakening contributions to inflation from owners’ equivalent rent and rent of primary residence (chart 4). There has already been some of that as monthly gains in OER and rent have ebbed from the 0.6–0.8% m/m SA pace at the peak last year into early this year and toward 0.4–0.5% gains more recently, but there should be further weakening ahead.

Vehicle prices should offer relatively little effect in weighted contribution terms. Industry guidance adjusted for seasonality suggests new vehicle prices were up by about 1% m/m SA and used vehicle prices were up by 1–2%.

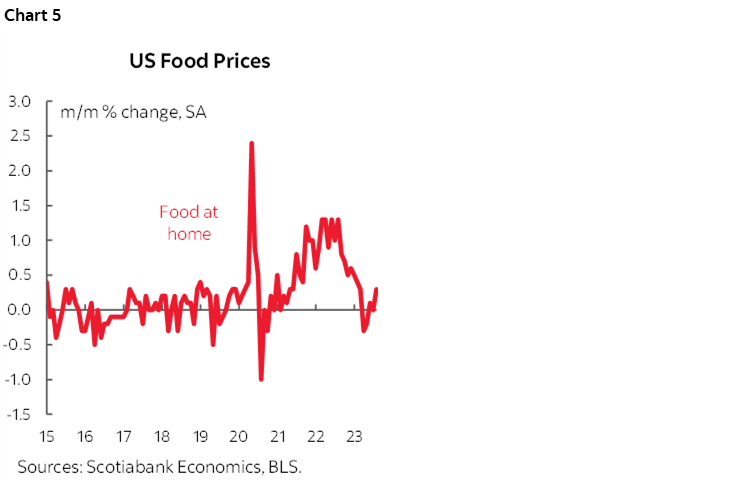

Ditto for food prices that should offer little effect in weighted terms and this effect has become more subdued (chart 5).

Key may be whether the deceleration in core services CPI continues (chart 6).

There is little seasonality in core prices during August and so there is not much of a difference between seasonally adjusted and unadjusted influences this time.

FOMC implications

If my estimate—which this time is close to the current consensus—proves to be on the mark, then it would be the fourth straight month of soft underlying inflation. The increases in June and July were both just under 0.2% m/m SA, the 0.4% rise in May had little breadth beyond used vehicle prices, and this month could be another 0.2% reading. When annualized, the trend rate is close to 2%.

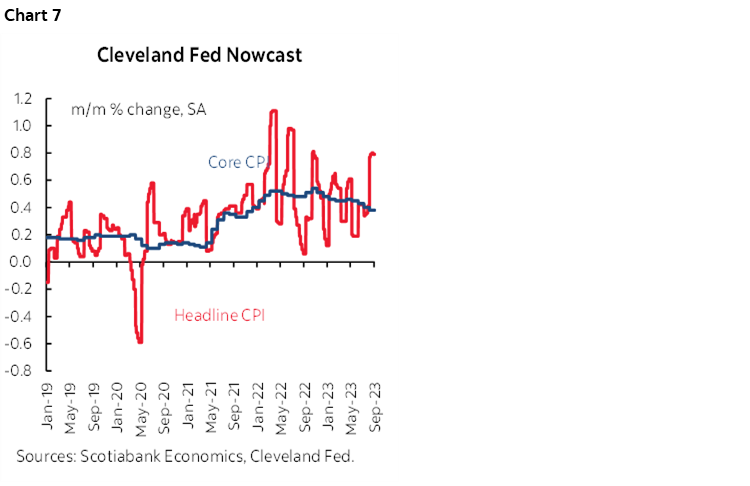

That trend could reinforce expectations that the FOMC holds in September in favour of evaluating data, market developments and other factors into the next decision on November 1st. It would probably take a material upside surprise to core CPI estimates to be impactful and along the lines of the Cleveland Fed’s ‘nowcast’ (chart 7), albeit the case that it has been overestimating inflation for some time now.

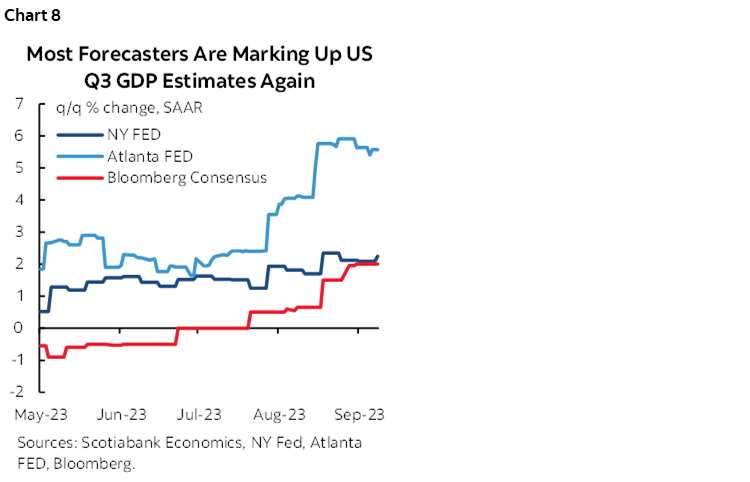

On the other side of this debate is Q3 GDP tracking. Forecasters and nowcasters are duking it out over who has the better estimate within wide ranges. The Atlanta Fed’s nowcast is tracking 5.6% q/q annualized GDP growth. The NY Fed’s recently rejuvenated nowcast is estimating 2¼%. Consensus estimates are scattered in between, but everyone is marking up their estimates for yet another time this quarter (chart 8). This leans toward resilience and if it continues then it could buoy further job gains and inflationary pressures.

GDP, however, doesn’t necessarily align with the Fed’s focus upon its dual mandate of price stability and full employment. Job growth is still decent, but cooler with the 3mo MA at only 150k and the unemployment rate is up a bit. Trend core CPI has softened.

This soft patch in employment and inflation is why about three quarters of consensus thinks hikes are over and markets are pricing a modest chance at one final hike sometime later this year. The FOMC is likely to be more careful and require a longer period of tame inflation and milder job gains in order to be convinced that imbalances won’t show up again in future.

For now, however, Fed guidance doesn’t sound like it’s in a great big rush to hike again. My reading of comments from officials is that they see little to be lost if they skip this time to evaluate more information. It probably doesn’t matter that we haven’t heard from Chair Powell in quite some time because he was previously clear in stating that the era of mom and dad holding junior’s hand to cross the street has transitioned toward treating everyone as adults. Data sensitive adults. Still, I doubt that he’d be comfortable totally shocking the market on any one decision especially at this fragile point for market risk appetite.

CENTRAL BANKS—DOWN TO THE WIRE

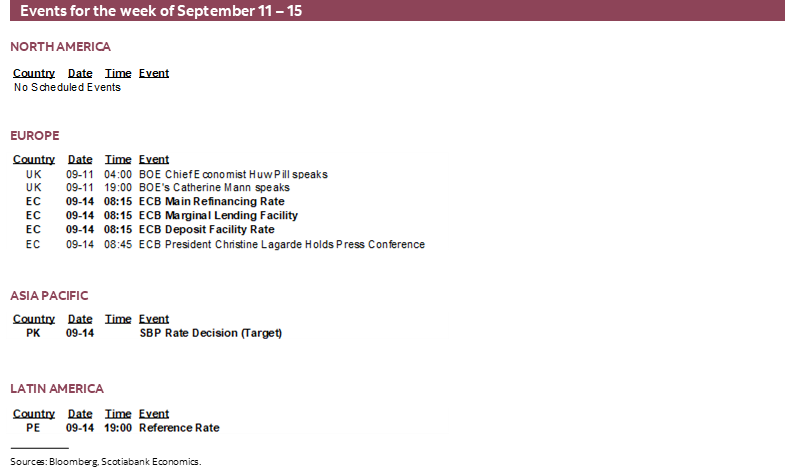

Key central banks start to deliver policy decisions this week and one or both of the ECB and PBOC could be impactful to world markets amid uncertainty toward what they may elect to do.

ECB—Heads or Tails?

The European Central Bank delivers a fresh policy decision on Thursday. The risks surrounding what they may do appear to be finely balanced. Markets are pricing less than 50% odds that a 25bps hike may be delivered. Slightly less than half of the consensus at the time of writing expect a 25bps hike.

ECB policymakers’ guidance has been mixed. The ECB’s account of the July Monetary Policy Meeting that was released on August 31st provided no clear guidance on what decision may lie ahead:

“Members also assessed the level and persistence of underlying inflation as being a source of concern, although it was acknowledged that indicators of underlying inflation had been broadly stable in recent months”

“Any further tightening had to be assessed meeting by meeting, on the basis of the incoming data and a ‘risk management approach’”

Hawks like Germany’s Joachim Nagel lean against a pause. He recently said “It’s for me much too early to think about a pause. We shouldn’t forget inflation is still around 5%. So this is much too high. Our target is 2%. So there’s some way to go.” Nevertheless, Joachim and some other hawks will not get a vote at this meeting.

Others, like the Netherlands’ Klaas Knot, have said markets “maybe” underestimating the chance of a hike this week. He also recently said “It’s quite crucial in the disinflation process toward 2% by the end of 2025 that wage growth decelerates visibly.” If I look at the current wage agreements, they are still pretty far off longer-run compatibility with a 2% inflation target plus half a percent productivity growth. We’ve reached the finessing phase of the tightening cycle. Tightening—a further hike—is still a possibility, but not a certainty.”

Governing Council member Peter Kazimir recently said he leans toward a hike because “It’s a more straightforward and efficient solution. Markets receive a clearer indication about the likely terminal rate, and we have more time to evaluate whether inflation is on a sustainable downward path toward our target.”

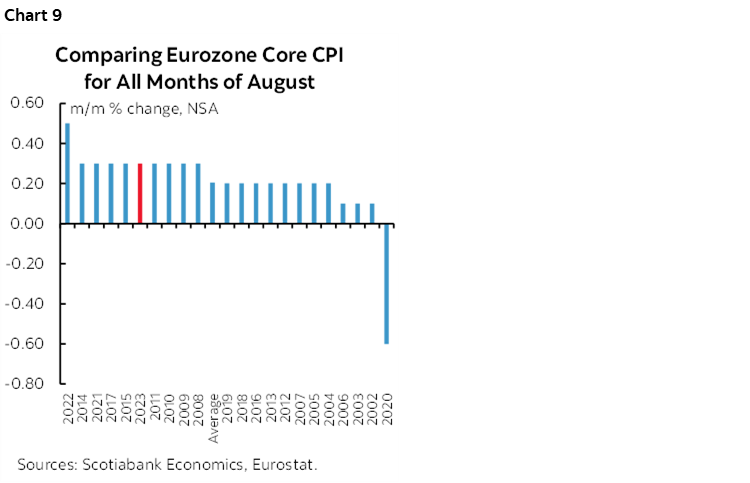

Throughout it all, core inflation remains hotter than seasonally normal (chart 9) but not as hot as prior months.

So there you go. See you Thursday. With low conviction.

PBOC—Not So Fast

China’s central bank is not expected to change its key policy rate on Thursday evening (ET). That doesn’t mean it’s impossible given its openness to surprising markets and the multitude of challenges facing the Chinese economy. It would, however, be rare for a back-to-back cut to be delivered after the 15bps reduction that surprised consensus on August 14th.

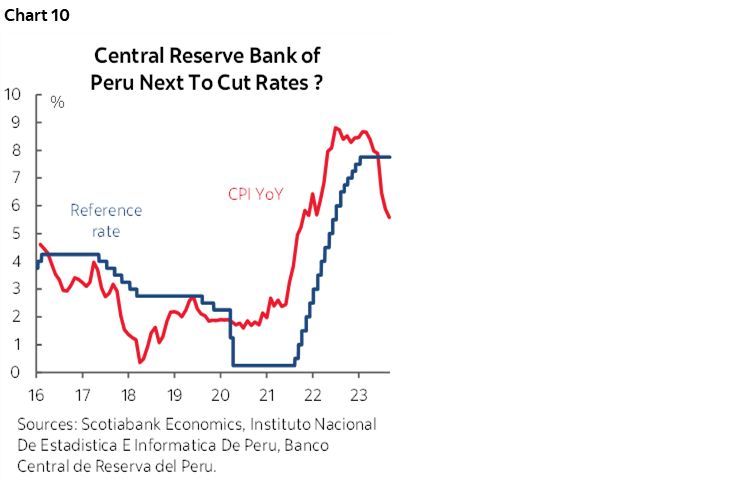

Banco Central de Reserva del Peru—Another LatAm Domino May Fall

Speaking of divided consensus calls, Peru’s central bank may follow other LatAm central banks like Brazil’s and Chile’s and cut its reference rate by 25bps on Thursday. Not all are convinced. The country’s economy has weakened with GDP down by a mild -0.5% y/y in Q2. Inflation is ebbing with core CPI at 3.8% y/y, down from a peak of almost 6% although headline inflation remains elevated (chart 10). Whether that’s enough progress or not is unclear, but expect guidance that progress is indeed being made toward an easing bias.

GLOBAL MACRO—AN ACTIVE CALENDAR

The global line-up of macro releases will offer up several gems out of the US, China, the UK and Australia.

US macro reports will focus upon CPI as noted above, but also retail sales for August (Thursday). A soft print is likely. Auto sales were down 4.5% m/m SA but prices were up a bit according to industry sources which might slightly insulate the drag effect. Gas prices were up 6.7% m/m and could add 0.5 ppts to the value of retail sales. Core sales excluding autos and gas could face downside risk after the large 1% rise the prior month. Recall that retail sales underrepresent services toward which American consumers have been shifting.

The US will also update producer prices for August (Thursday) that should post a mild rise in core prices and a bigger gain in headline due to energy influences. Industrial production (Friday), the UMich consumer sentiment reading for September (Friday), the Empire manufacturing gauge that kicks off the regional surveys (Friday) and weekly jobless claims that recently fell will all round out the release calendar.

China will update a wave of macro reports. As this note is being published, we await CPI for August. The -0.3% y/y drop in July prompted deflation headlines and this reading is expected to perhaps come back into positive territory which could make it awkward for the bandwagon that hopped on the July print. I still think deflation is not what is happening in China (here).

China’s aggregate financing during August will test the response to cuts in borrowing costs and reserve requirements (Thursday). Industrial production, retail sales, fixed investment and the jobless rate during August will inform the ongoing degree of downside risks to China’s economy.

The UK will update job market readings on Thursday including the change in total employment and wages in July plus the change in the number of payroll employees during August. It also releases monthly GDP for July on Wednesday and the services index on the same day.

Canada faces a light line-up in the wake of the rebound in jobs (here) after the BoC’s decision to hold (recap here). On the docket may be improved readings on the economy. Statcan’s advance guidance pointed to wholesale trade being 1.4% m/m higher in July (Thursday) and manufacturing sales being 0.7% m/m higher that same month (Friday). Existing home sales during August push into what for many is the deadzone on the calendar toward the end of summer and just before school starts.

Australia will be trying to rebound from a 15k drop in employment that followed two large prior gains when August figures arrive on Wednesday evening (ET).

CPI figures will be updated by Norway (Monday), India (Tuesday), Sweden (Thursday), Brazil (Tuesday) and Argentina (Thursday).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.