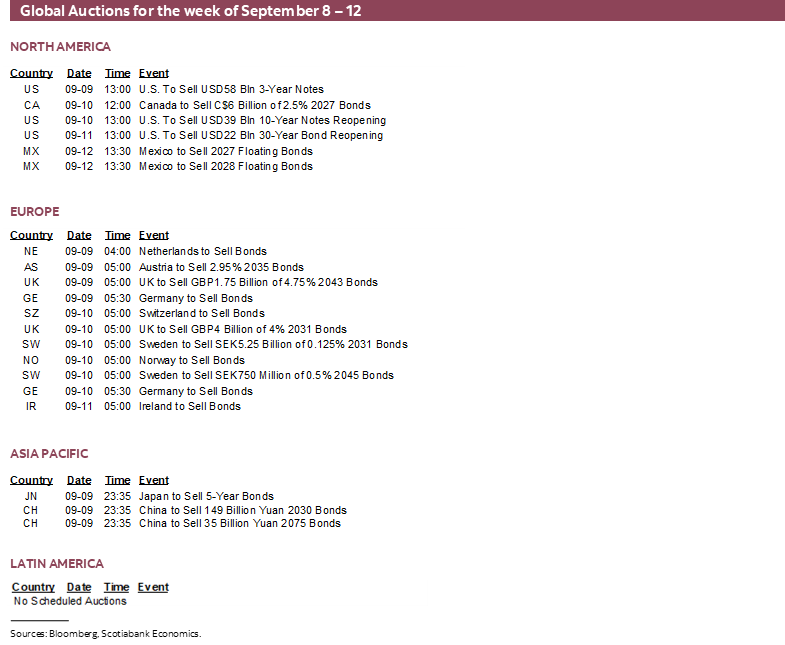

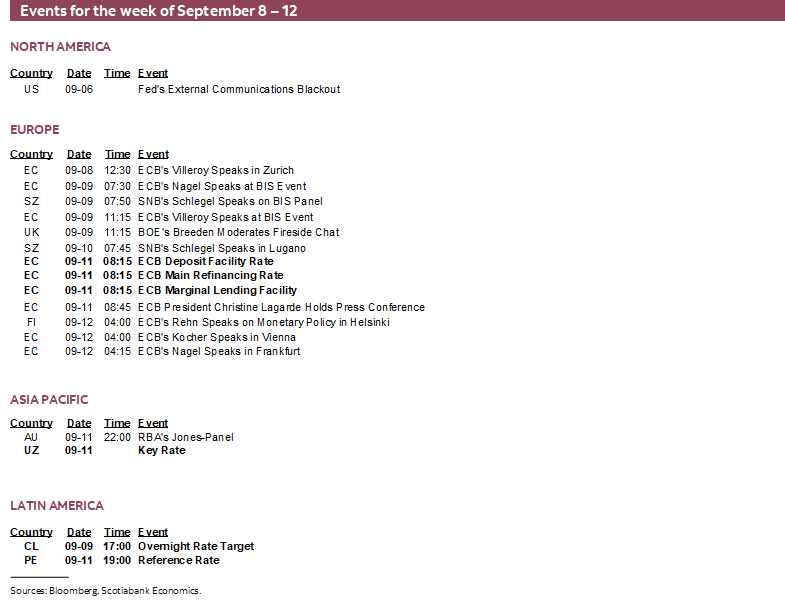

Next Week's Risk Dashboard

- BoC forecast change

- Soft US payrolls reinforced a September cut…

- …but US CPI & PPI could inform the dots

- ECB expected to hold as members’ bias scatters

- BCCh likely to hold after CPI

- BCRP might cut

- Mexican CPI may inform Banxico’s next move

- BCB’s pause likely to be reinforced by Brazilian inflation

- China still has no inflation

- Norges Bank’s cut guidance faces inflation update

- RBI likely to look through temporary up-tick in inflation…

- …with GST cut passthrough coming

- UK data dump to refresh Q3 growth tracking

- Turkey’s central bank remains the wild west

- Russian central bank expected to ease

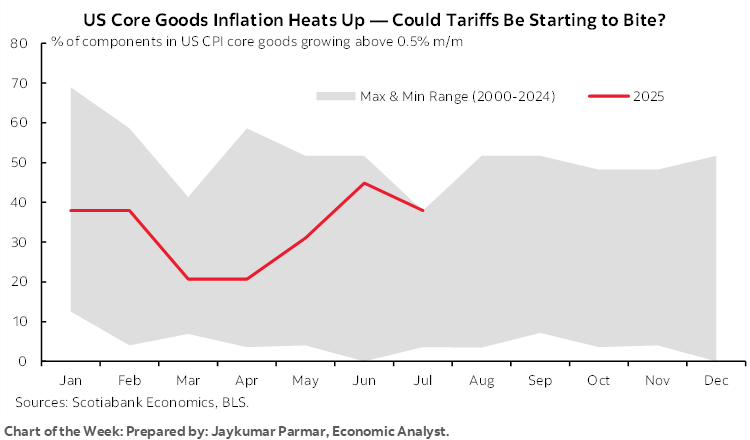

Chart of the Week

Is inflation risk as fictitious as the thought of Kawhi Leonard (allegedly) being paid tens of millions to plant trees in L.A.? Sorry, jilted Raptors basketball fan here.

But seriously, it introduces the importance of the week’s key expected developments. Amid uncertainty over next steps to be undertaken by global central banks, the week’s inflation reports could be significant to policy expectations. US CPI and PPI will dominate attention, but reports out of China, several LatAm economies (Mexico, Chile, Brazil), Norway and India will matter to their markets.

Several central banks will also weigh in this week including the ECB, and central banks in Peru, Turkey and Russia.

Most of this is a warm-up to the following week’s developments not least of which being decisions by the Federal Reserve and Bank of Canada that will spend this week in blackout.

In their cases, however, the momentum has clearly shifted toward rising concern about the state of the job markets in both countries (here, here). That’s not to be confused with dismissing inflation risk, but it clearly rebalances the risks facing monetary policy actions. And what happens to the US labour market tends to happen to Canada’s (chart 1), like conjoined twins with one of them in frequent denial. We’ve changed our forecast for the Bank of Canada as noted in the earlier link.

An added twist in the case of the US is the politics. The Trump administration is clearly setting out to stack the deck on the Fed’s Board of Governors; if they don’t get what they expect, then the district Presidents are vulnerable at the end of February. That’s totally out of sample stuff and crossing a line. Yet, while he makes some valid points, so is this by way of inviting a trespassing charge.

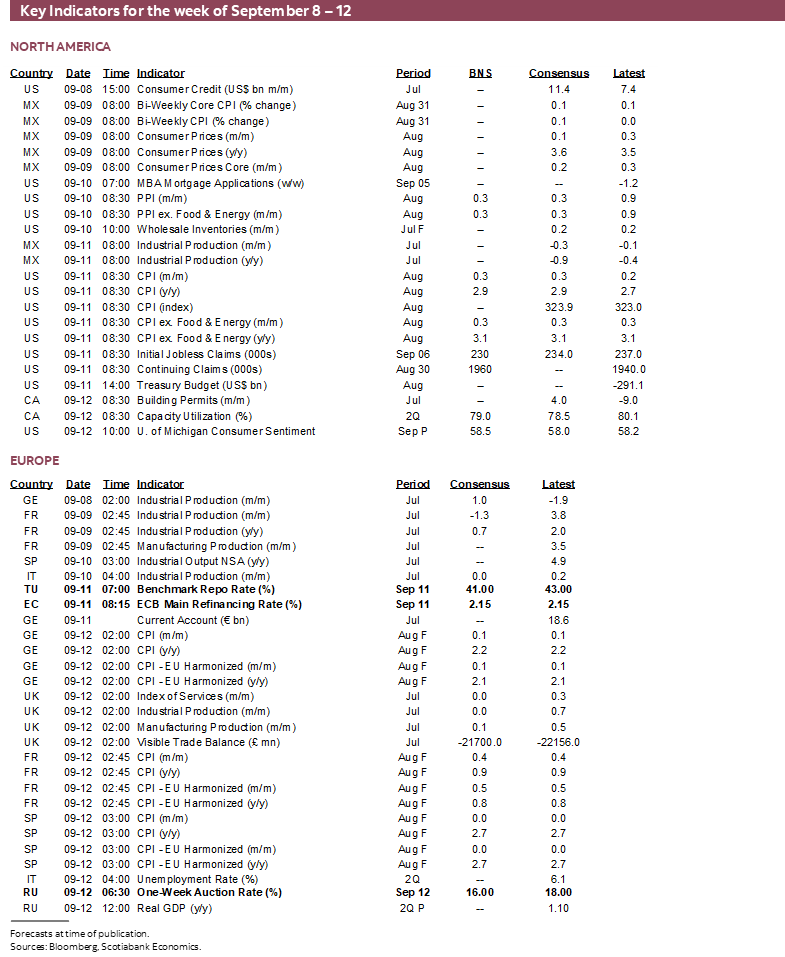

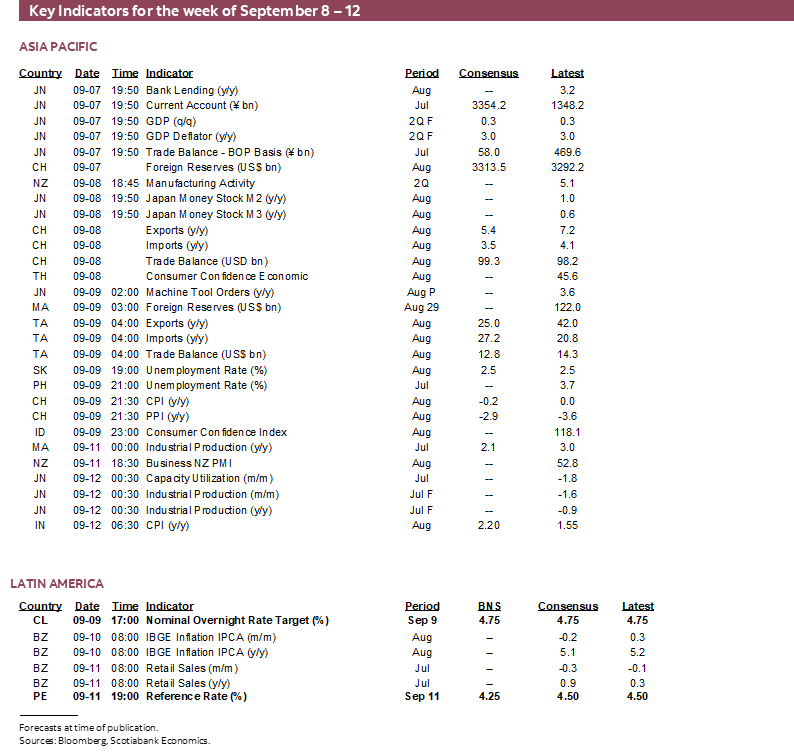

GLOBAL INFLATION—MOST EYES ON THE U.S.

Several central banks will be keeping a close eye on inflation readings this week ahead of pending decisions. They’re covered below in chronological order.

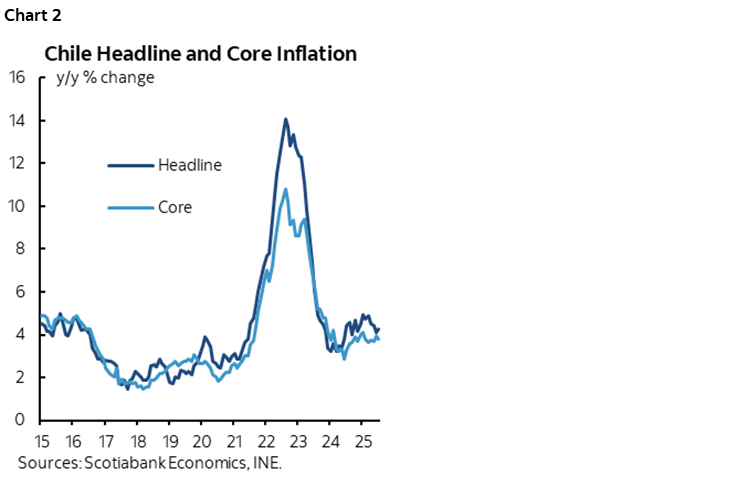

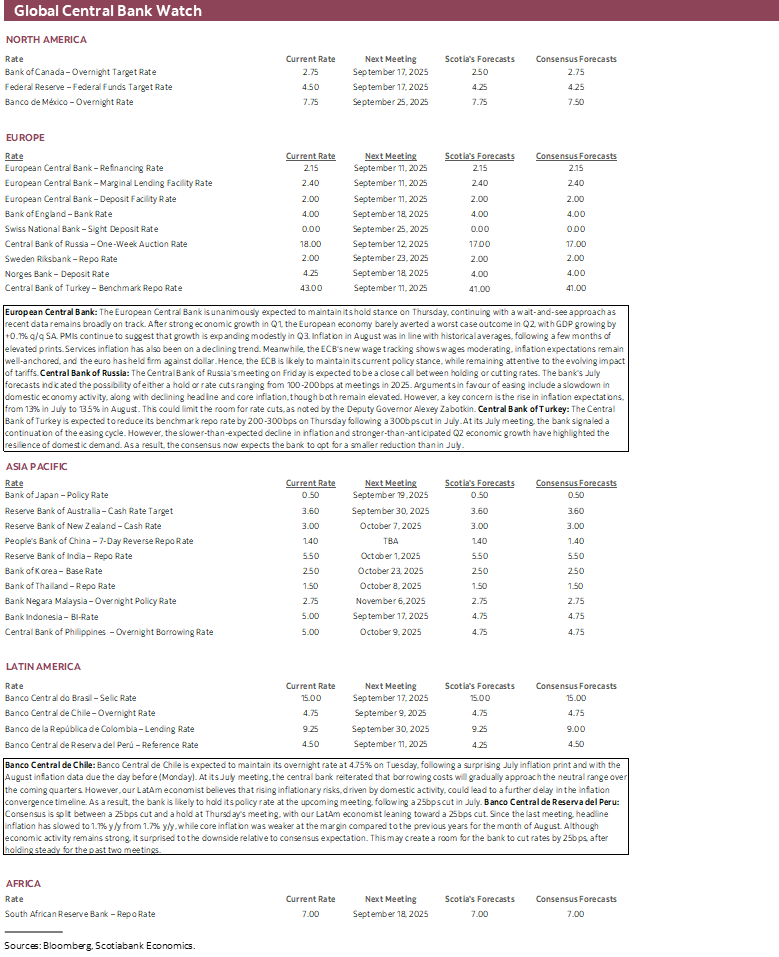

Chile—CPI to Tee Up BCCh’s Next Move

BCCh delivers its next policy decision on Tuesday. CPI for August arrives the day before. Inflation is running at 4.3% y/y with core at 3.8% (chart 2). After a larger than seasonally unusual rise of 0.9% m/m NSA in July, most expect a reading for August of about 0.2–0.3% m/m which would keep the year-over-year rate little changed. BCCh targets inflation within a 2–4% range. On the face of it, one might expect the central bank to retain a tight policy stance. It cut, however, on July 28th, and while most expect it to hold this week, a concern has been the health of the labour market as the unemployment rate has edged up this year to 8.7% while some slack is forecast to drive inflation lower over time.

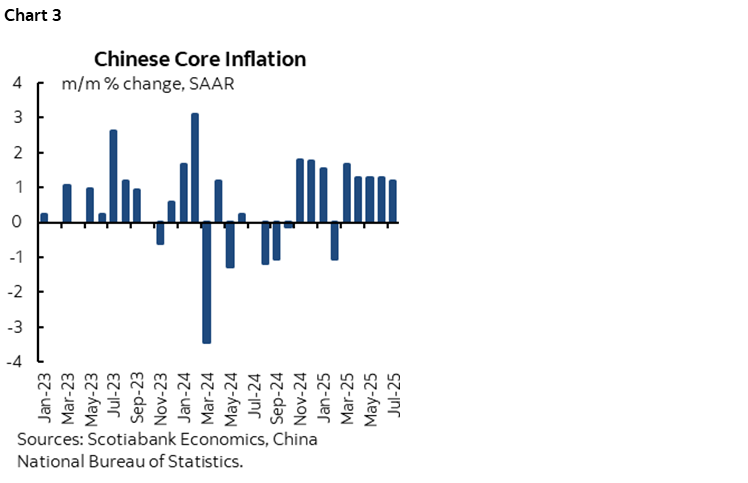

China—What Inflation?

China has no inflation. And it doesn’t care. CPI is running at 0% y/y with commodity-sensitive producer prices down by -3.6% y/y. Core CPI excluding food and energy is at 0.8% y/y. Even higher frequency core inflation is tame (chart 3). Tuesday’s figures are not expected to drive material improvement. The PBOC has adopted a fairly slow pace of monetary easing since late 2021. The key 5-year Loan Prime Rate that influences the property market has fallen from 4.65% back then to 3.5% now. Yuan appreciation so far this year risks further dampening inflation pressures into next year. A dilemma, however, is whether monetary easing would help or make for worse stability effects; stocks have been soaring, demand for money is relatively rate inelastic amid still falling house prices, and policy easing could wind up moving through channels that create imbalances.

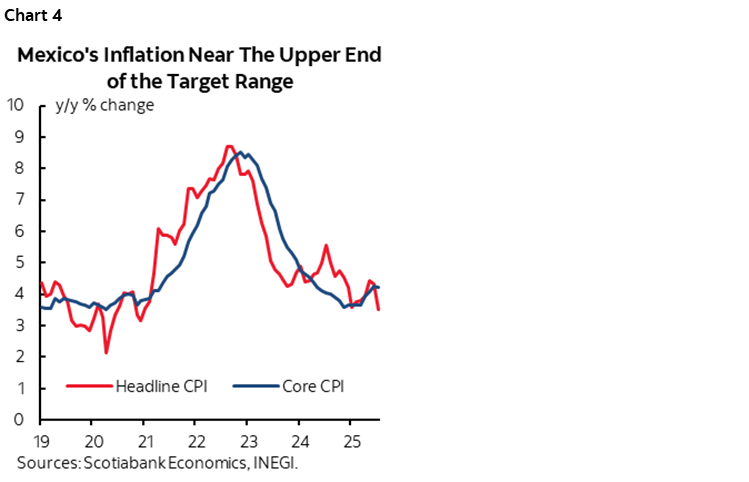

Mexico—Relief on the Way?

On Tuesday, Mexico will release the last inflation report before Banxico’s next policy decision on September 25th. Little change is expected in the year-over-year headline (3.5%) and core (4.2%) rates of inflation. Mexico releases CPI figures on a bi-weekly basis and so estimates for the monthly reading often carry little intrigue. Banxico targets inflation at 2% and so present rates wouldn’t appear to support easing which, alongside his view on inflation risks, is why Deputy Governor Heath has dissented against recent policy easing (chart 4). The majority has a data dependent easing bias because some slack in the economy, possibly lighter supply shocks and the peso’s sharp appreciation to the dollar this year are expected to bring inflation toward 2% later in 2026.

US—The Better Half?

By next Thursday we will have a fresh round of evidence on how the Federal Reserve’s dual mandate goals are tracking. We have fresh evidence on the job market (here) and will get inflation reports.

US CPI will be updated with August figures on Thursday with producer prices due out the day before. The combination will help to inform tracking for the Fed’s preferred PCE inflation gauges that are due out on September 26th—nine days after the policy decision.

Federal Reserve Governor-nominee Stephen Miran’s remark that there is no evidence of tariff-induced inflation clearly went too far—especially for one who could be influential over monetary policy and is supposed to be open-minded. The 0.9% m/m jump in producer prices during July and 0.6% rise ex-food and energy shocked markets. Several of the categories could be reasonably viewed as being influenced by tariffs such as the jump in food and energy, core goods ex-food and energy, trade services and transportation and warehousing. That might be a tough act to follow in August’s report versus monitoring the trend, but a further mild rise of about 0.3% m/m SA is expected.

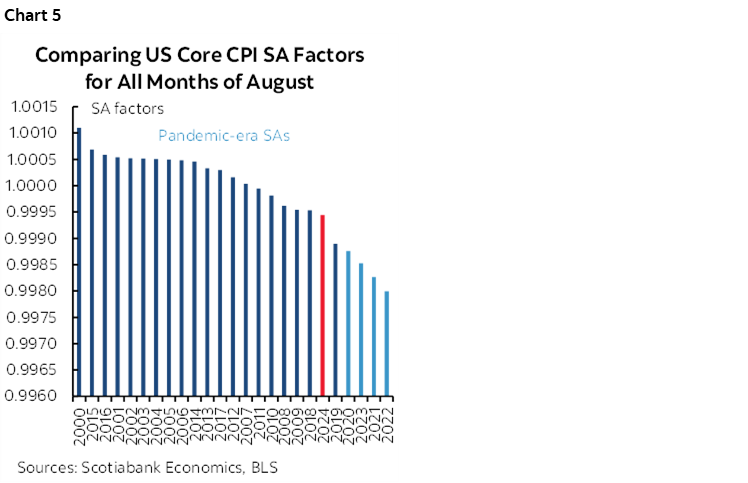

CPI is estimated to rise by 0.3% m/m SA for both headline and core measures. A key question will be the potential trade off between core services prices, tariff effects and shelter inflation. A complicating factor is that there remains a recency bias to how seasonal adjustment factors are calculated and that for this time is likely to mean an artificially low SA factor (chart 5).

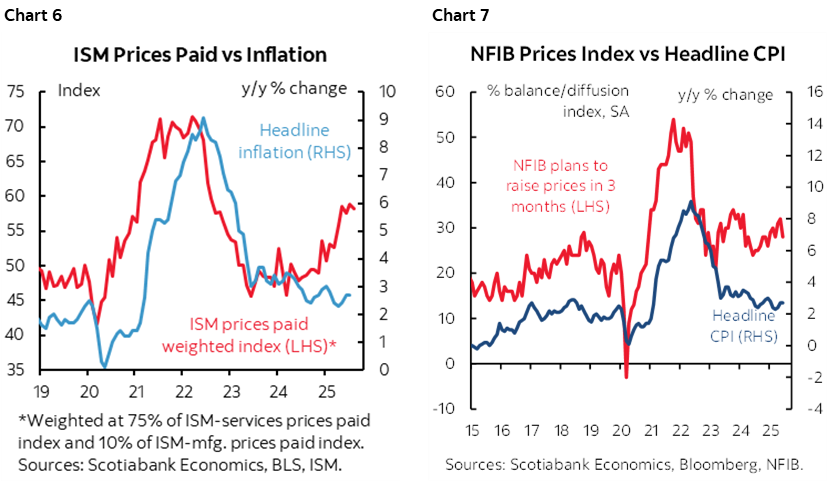

At some point in the not too distant future, soft data is indicating rising and lagging risk of higher inflation readings (charts 6, 7).

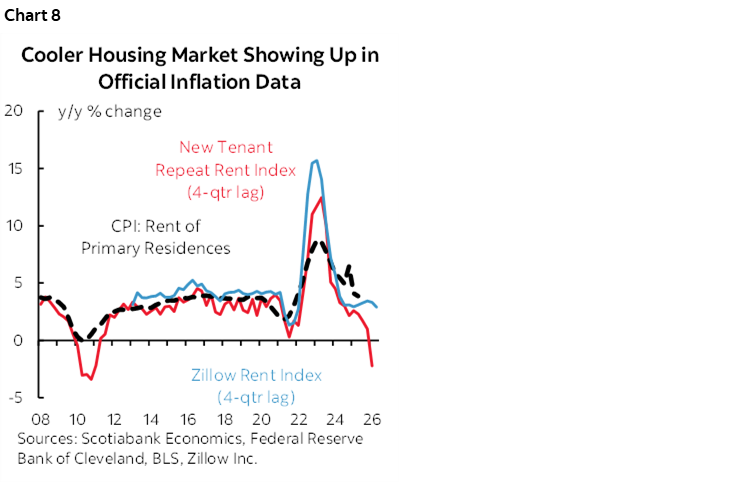

Shelter inflation is on the downswing and with possibly more to come (chart 8). Recall, however, that services excluding services related to housing and energy spiked sharply higher by 0.5% m/m SA for the hottest reading since January. That may moderate this time, but strength in the services sector such as the ISM-services gauge and its pick-up in new orders and prices might suggest otherwise. Airfare and housing-related insurance have been among the hotter categories.

Core goods inflation has been running at about a 2½% m/m SAAR pace and some categories—like spiking prices for household furnishings and recreation goods—may be warm because of imported components.

Big-ticket items are estimated to post continued trend gains in owners’ equivalent rent and rent of primary residence, plus slightly softer than seasonally normal vehicle prices.

Nowcast estimates are based on very little information, but the Cleveland Fed’s estimate points to 0.3% gains for both total CPI and core CPI.

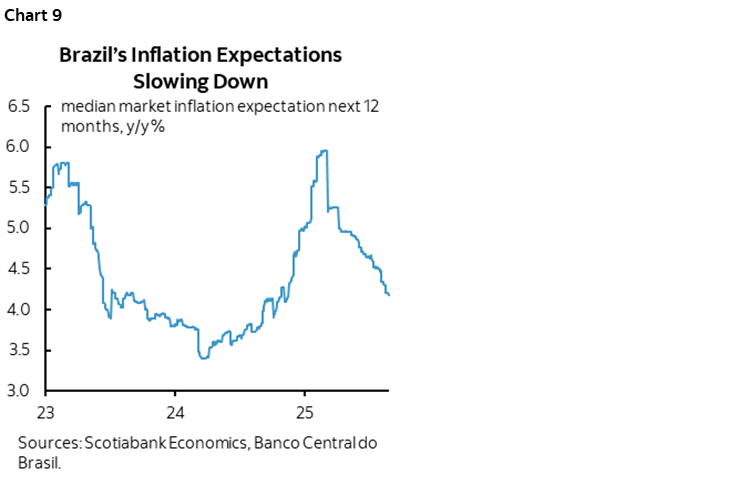

Brazil—Done Enough?

Brazil refreshes inflation for the month of August on Wednesday ahead of the Banco Central do Brasil decision just hours after the Fed’s communications on the 17th. Inflation has been running above 5% y/y alongside elevated inflation expectations (chart 9). BCB has been aggressively hiking since last September and taken the Selic rate up by 450bps over this period. It signalled a shift at its last meeting on July 31st, however, when the prior outsized pace of hikes gave way to a smaller 25bps move accompanied by guidance that a potential hold for “a very prolonged period” could ensue. BCB has transitioned toward giving time to see how its highest policy rate since 2006 succeeds in bringing inflation down.

Norway—A High Bar to Knock Guidance Off Course

Norges Bank will deliver its next policy decision the day after the Fed. Markets are roughly 80% priced for a cut. Wednesday’s CPI figures for August may further inform the odds and influence fresh macro projections to be provided at its upcoming meeting.

Underlying inflation has been stuck around 3% y/y this year. With three meetings left in the year, what markets are going by in pricing further easing is the comment in the August decision that said developments since June when guidance pointed to “one or two additional rate cuts” this year have been unfolding largely as expected.

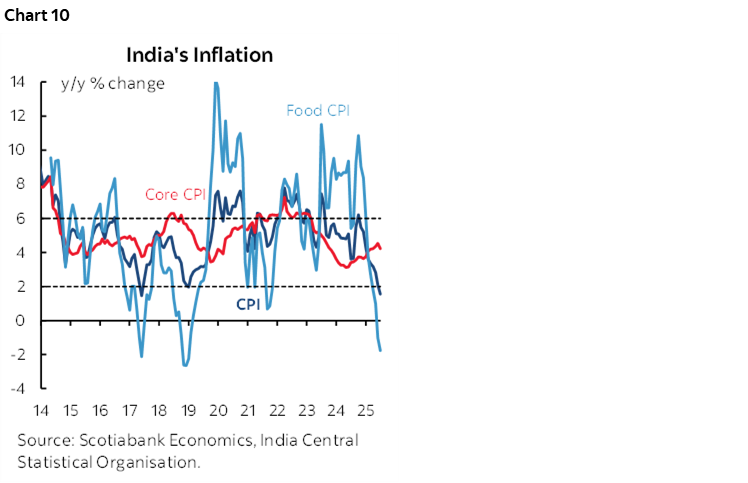

India—Looking Through?

The last inflation reading before the Reserve Bank of India’s policy decision on October 1st arrives on Friday. Markets are priced for no change after the August hold.

Inflation is expected to bounce back from low levels to above 2% y/y (chart 10). That is expected to be temporary, however, as the government is reducing the Goods and Services Tax effective September 22nd by shifting to two rates of 0–5% from 12–18% on multiple goods, and 18% from 28% on other goods along with a 40% tax on ‘super luxury’ and ‘sin’ goods. The aim is to stimulate in offsetting fashion to Trump’s tariffs against Indian imports. Local analysts believe inflation could push lower by around a full percentage point due to the GST changes. Key, however, will be incidence effects; core measures of inflation that exclude indirect taxes picked up somewhat when Canada offered temporary sales tax relief at the end of last year and earlier this year.

Normally a central bank would look through the effects of changes in indirect taxes, but some forecasters believe that the GST cut could motivate RBI easing.

GLOBAL CENTRAL BANKS—REGIONAL UNCERTAINTIES

The Federal Reserve and the Bank of Canada will be in communications blackout ahead of their decisions on September 17th. No major central bank is expected to rock the boat this week, but regional central banks might.

Chile’s central bank has already been covered earlier in the context of the week’s CPI update. The rest follow.

ECB—On Hold

The European Central Bank is universally expected to hold its deposit rate at 2% on Thursday. Markets are fully priced for a hold at this meeting and the next one at the end of October with only a slim chance of a further cut afterward. The consensus of economists agrees.

The ECB has already chopped its key rate in half since the end of last year. Opinions on next steps are divided across Governing Council members.

Moderates, like Estonia’s Müller, prefer to “take the time and monitor” new information. France’s Villeroy flags “very well controlled” inflation.

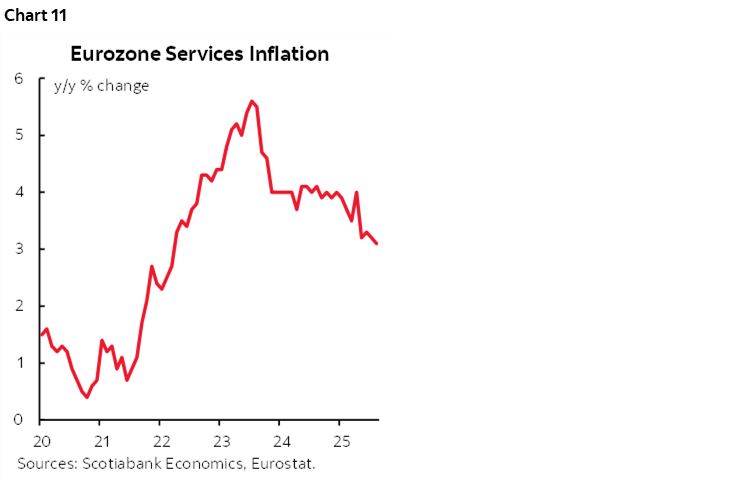

More hawkish minded members, like Board member Schnabel, think “we may be already accommodative and therefore I do not see reason for a further rate cut.” Acting member from Slovenia, Primoz Dolenc, noted that after a hold this time, the policy rate “could go in either direction” in future. Hawkish members can point to the fact that core inflation in m/m terms remains relatively high of late compared to like months of seasonally unadjusted figures and services inflation remains sticky (chart 11).

More dovish voices somewhat atypically come from the north with Finland’s Rehn “there are more downside risks to inflation” ahead.

New forecasts to be provided at this meeting will provide a balanced sense of where the consensus of policy markets stands on the path ahead.

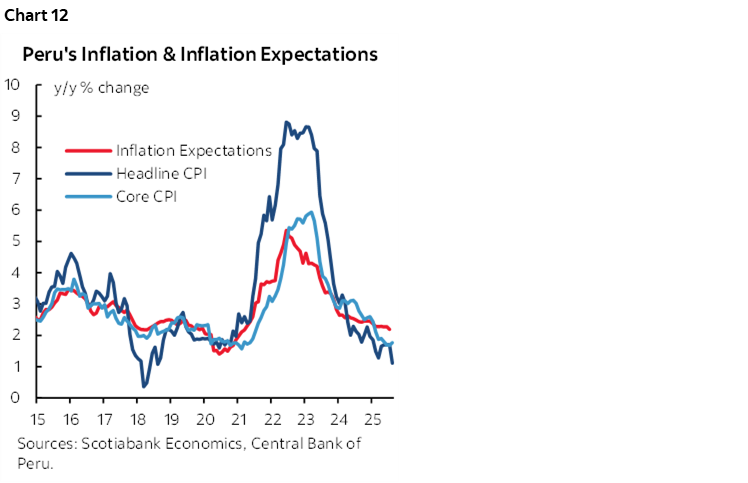

BCRP—To Cut or Not

Peru’s central bank is expected to cut by 25bps on Thursday according to our LatAm-based economists. Consensus is somewhat divided between a cut and a hold. It would be the first reduction since May.

The case for a cut includes little to no inflation. Lima CPI is running at just 1.1% y/y with core CPI at 1.8%. That puts both measures beneath the mid-point of the 1–3% inflation target zone. Expecctations have also ratcheted lower. Chart 12.

The case for a hold is to allow more time to evaluate risks to trade policy—including court challenges to US tariffs—and a mild pick-up in growth albeit that the economic activity index for June climbed to 4 ½% y/y largely because of a shift in the comparisons toward a lower base effect the prior June.

CBT—Good Luck

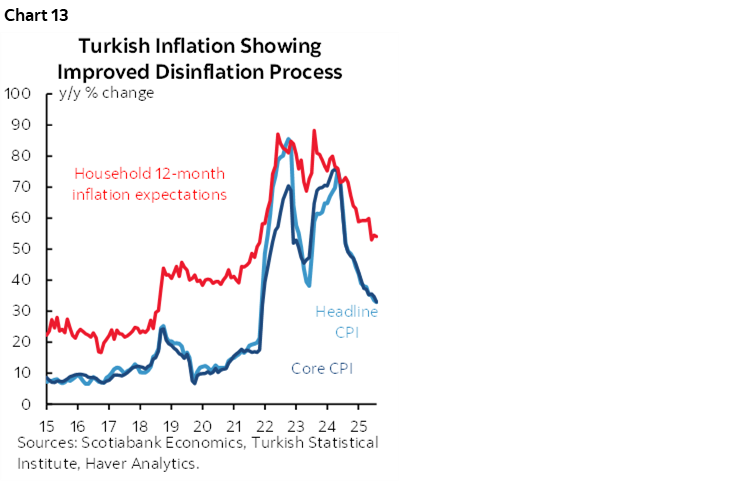

Pity anyone who has to try to forecast this central bank. The rate path over the past year looks like a game of Tetris with random zigs and zags. That’s what you get with a volatile administration as a lesson to other countries. Ahem.

Anyway, CPI inflation still stands at about 33% y/y with core the same. It has been ebbing throughout the past year from a peak of about 76%. So, cut, right? Some expect that outcome. One caveat is that expectations remains very high (chart 13).

Except that the Turkish lira is still sinking in value and that poses ongoing risk of imported price inflation. The lira is down 14% to the buck so far this year. Politics and court challenges that have affected the opposition drove a crisis of confidence that sent the BIST 100 equity index down about 6%. So, don’t cut because of inflation risk. Cut to inject confidence into local markets. Or, like me, shrug and look elsewhere to a less wonky market.

Russia—From Russia with (No) Love

Russia’s central bank is expected to cut again on Friday. It has eased from a key rate of 21% back in April to 18% now amid expectations that another mega cut could be delivered now. Why? Inflation is falling, with CPI at ‘only’ 8.8% y/y and core slipping to 8½%. Further relief may be in store as economic growth sinks to just 1% y/y.

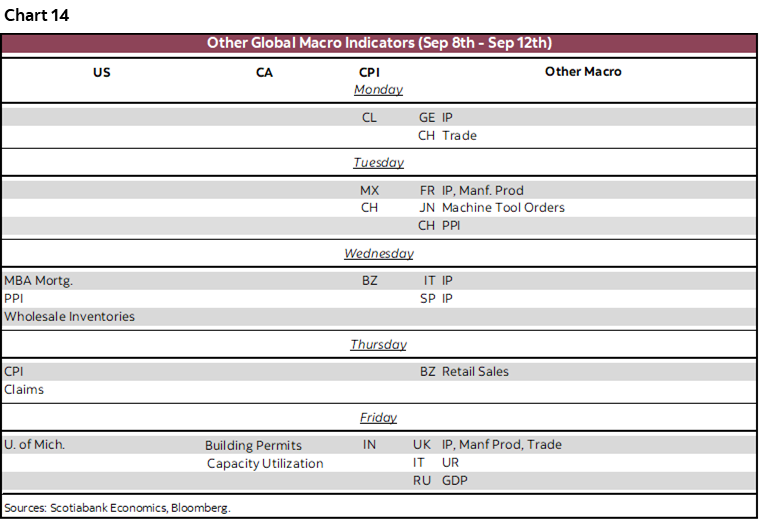

GLOBAL MACRO—UK IN FOCUS

The rest of the global macro line-up is summarized in chart 14.

The main stand-out feature will be the monthly UK data dump on Thursday. July’s readings for GDP, industrial output, services activity, construction output and trade will materially inform tracking of Q3 momentum after paltry growth of 0.3% q/q SA nonannualized in Q2.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.