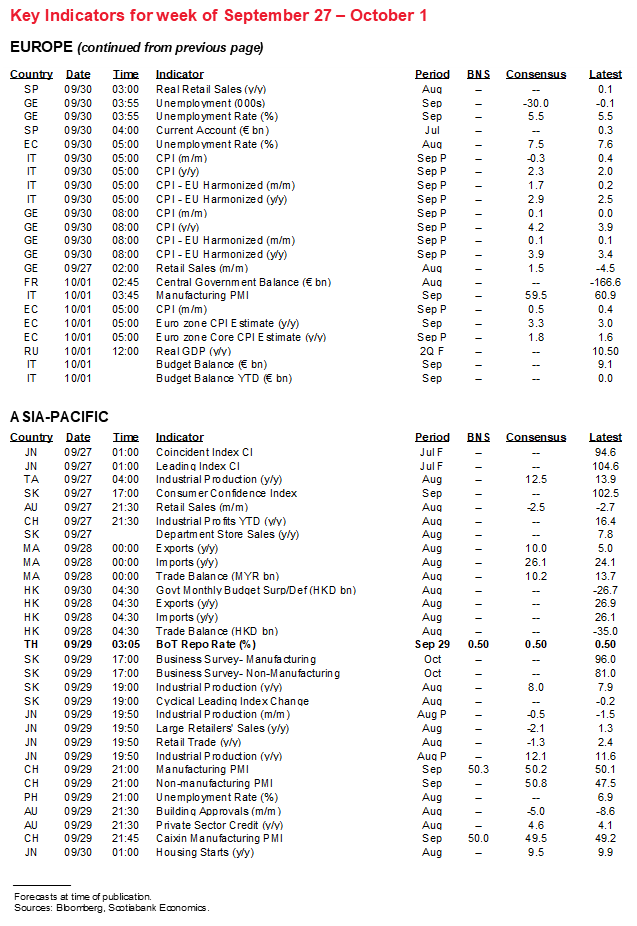

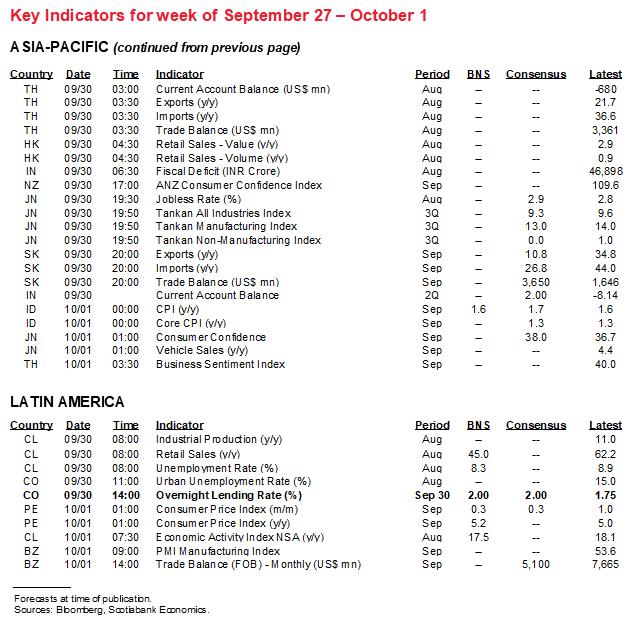

Next Week's Risk Dashboard

• Evergrande

• US debt ceiling

• Choosing Merkel’s successor

• CBs: Banxico, BanRep, BoT

• Powell, Yellen to testify

• PMIs: US, China, India, Mexico, Brazil

• GDP: Canada, US Q3-r, UK Q2-r

• Inflation: US (PCE), Eurozone, Peru

• Other US macro

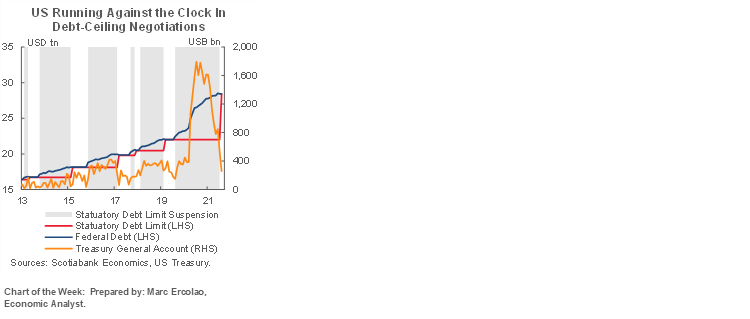

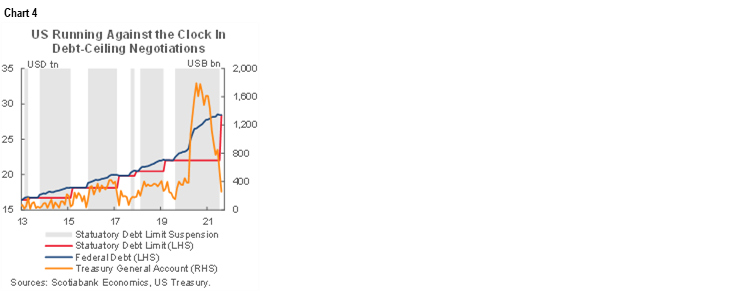

Chart of the Week

Global markets are entering crunch time for two major risks overhanging markets. How they may evolve will involve placing markets at the mercy of China’s leadership and the US Congress. Toss in uncertainty around who leads Germany post-Merkel, some central bank highlights, how much wind Eurozone CPI will put beneath the hawk’s wings and several global macro readings and say good bye to September with some trepidation toward how it all hands off to October.

NOT LOOKING SO GRAND(E)

The week’s dominant market risk may rest in the hands of Chinese authorities. Broad confidence across markets and Chinese savers in how Chinese authorities and company management handle the potential demise of China Evergrande Group could be key. The struggling property conglomerate remains the subject of speculation over the impact its troubles may have upon China’s financial markets, banks, real estate markets and the potential for systemic risk to global markets.

At the point of distributing this publication, Evergrande had not yet made an US$83.53 million payment on 8.25% US$ bonds due in 2022. There is a 30-day grace period on such payments and so it is not in technical default on the issue. A further payment of US$45.17 million is due on a 9.5% 2024 US$ bond on Wednesday and there are multiple coupon payments due over coming weeks (chart 1).

Uncertainty around the risk of default will coincide with the transition to China’s National Day on Friday that kicks off Golden Week during which Chinese markets will be shut until the following Thursday. The arrival of this holiday in the context of Evergrande’s issues could either be fortuitous or calamitous. It could afford the opportunity to achieve a more durable solution with all the ducks lined up while domestic markets are shut and hence along the lines of banking holidays during global banking crises (this is not yet one in China). Or, it could have the opposite effect if position covering into holidays winds up fanning market risks with foreign markets left to react during the Chinese holiday and with Chinese markets playing catch-up upon return.

I don’t know the answer to that especially given how complicated the issues would be within a western democracy, let along China’s unique system. With considerable trepidation, a few balanced thoughts are offered for your consideration.

One argument for discounting Evergrande’s issues with heavy debt and low liquidity is that its challenges are idiosyncratic and therefore they don’t pose systemic risk. Other property developers in China have sounder finances and don’t cross regulators’ “red lines” on measures like debt growth, debt-to-assets, debt-to-equity and working capital. Evergrande’s violation of those red lines is acute and unique to the firm.

This argument doesn’t necessarily resonate so well with, oh, say, a Canadian economist who recalls what can happen when a large, concentrated property developer fails like in the early 1990s. Circumstances were different then in multiple respects, but the failure was in the context of growing weakness in global commercial real estate markets and the further weakness to come. Idiosyncratic stresses can still spark systemic risk particularly if mismanaged.

In addition to this example, whether because of poor judgement, weak controls, ill fortune and/or nefarious deeds, idiosyncratic problems at select Wall Street firms ultimately blew the GFC wide open. The Fed’s role—and former Chair Bernanke’s subsequent acknowledgement of mistakes—in allowing failure and the subsequent finger pointing that sparked a broad market run (versus physical runs on banks in the 1930s) must be acknowledged as a reminder of the present importance attached to how China’s authorities respond. As President Xi Jinping seeks to alter past ways in which China has addressed such stresses, it’s worth noting the fine line between imposing discipline as a means of reducing moral hazard versus courting disaster. Evergrande could be the litmus test of where this balance sits and hence inform the composition of near-term and longer-term risks.

Another argument is that China’s banking system is sufficiently well capitalized to handle risks. China’s banking system has a Tier One Capital Ratio of almost 12% and it has been trending higher over about the past decade. This is higher than it was in the US banking system into the GFC, but not that much higher (chart 2). In any event, a liquidity event is not necessarily well informed by capital ratio positions.

A further point is that most of the exposure to Evergrande sits at Chinese banks that hold about one-quarter of Evergrande’s debt. The largest Chinese banks may be better situated than smaller banks’ exposures, and banking systems elsewhere— particularly in the US and Europe—have much more limited exposures. Still, most of the savings of Chinese households remain tied up in China’s financial system and hence lack diversification. It is their confidence that is acutely important and the Chinese leadership has not always understood this point in timely fashion.

Ultimately it will come down to how the authorities manage Evergrande’s problems and what impact this may have upon Chinese confidence. Continuing to flood the system with liquidity as the PBOC has been doing (chart 3) will be among the important tools to be relied upon. Learning from the Fed and former Chair Bernanke’s admission that in hindsight it didn’t do enough in the early days of the crisis may be important. Standing ready to employ other tools—perhaps preceding decisions on the future of the firm—and setting a limit to imposing discipline against moral hazard risks will be key.

Whatever the outcome, the main point here is to be on guard. Markets shouldn’t have carte blanche faith in a system that has had crisis points such as around the time of the Chinese stock market bubble in 2015–16, or the banking liquidity crisis a couple of years before that. The rigid nature of its system and limits on convertibility have sparked prior rushes to the exits by Chinese savers and markets. China should learn from the mistakes that others made at potential crisis inflection points.

US DEBT CEILING—MISMATCHED INCENTIVES

Well, here we are again. The world is watching partisan dysfunction unfold in the US Congress as negotiations over how to keep the government open and avert potential disruption to markets go down to the wire again. What else is new. Most seasoned political observers tend to simply shrug and say that’s the way Washington rolls and in the end after considerable drama it tends to get the job done. There is very low risk of default but non-negligible risk of at least a temporary government shutdown should a funding arrangement not be in place before the end of the week.

Most countries tend not to consider gambling with how to fund basic government operations and it’s unthinkable across advanced societies in the modern era to court even the slightest risk of default. Most countries let voters choose the administration and let the administration come up with a budget proposal that then needs to be passed by a majority of votes in its legislature.

Not the US. A budget exercise is a mere formality. Off-budget bills frequently push the budget margins often by trillions of dollars over time. Concepts like the Byrd amendment and budget reconciliation then enter the picture. Can’t reach a bipartisan agreement? Use the ace in the hole and go it alone; the GOP would prefer that so as to try to deny the Dems the opportunity of reaping the benefits to economic growth into the mid-terms and to distance themselves from heavy spending after having taken their turn. Sundry appropriations bills then have to release funding to government departments. If that’s not enough, then every so often there is a tussle over raising the debt ceiling against the sum total of allowed public debt, a concept that has become abused versus its original motives to help fund the war efforts through WWI and WWII.

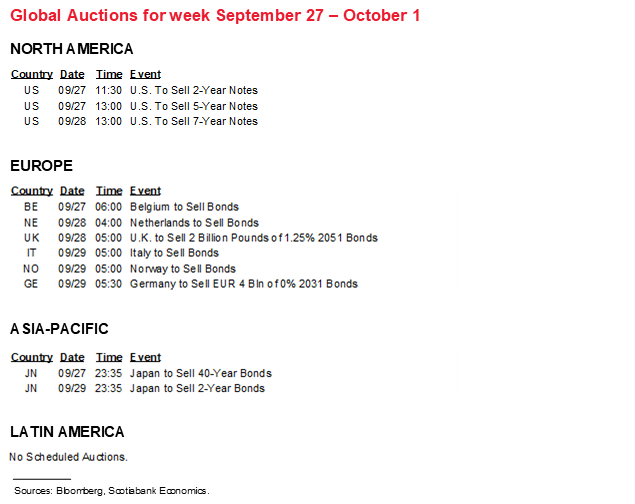

A lot is resting on this in such fashion as to potentially fill an entire publication on its own. Everything from the future of a US$1 trillion infrastructure deal, a US$3.5 trillion package of social spending and targeted tax measures, appropriating funds to keep the government open past Thursday and then moving on to raising or suspending the US$28.4 trillion debt ceiling (chart 4) by enough to get past next year’s mid-terms and avoid risk of technical default hangs in the balance. There are multiple scenarios for how this gets done next week and over subsequent weeks before time runs out on the ability to avert default against a hard lending cap sometime in October or maybe by November.

BUNDS AND MERKEL’S SUCCESSOR

German Chancellor Angela Merkel announced in 2018 that she wouldn’t seek another term in office and this Sunday’s election will choose her successor. In a sense, it will be like the recent Canadian election in that voting during a pandemic with significant numbers of mail-in ballots may not yield broad results right away (through they did in Canada’s case). We certainly won’t find out Merkel’s successor right away.

Merkel’s party—the Christian Democratic Union—chose Armin Laschet to take over leadership. He will go up against Olaf Scholz who leads the Social Democratic Party that has been at times an awkward coalition partner to the CDU. Less likely outcomes would see the Green Party’s Annalena Baerbock bounce toward victory with even lower odds likely attached to the Free Democratic Party or far right Alternative for Germany party winning. The greatest number of seats could be won by either the CDU or SDP (chart 5).

While the composition of the Bundestag may be determined before markets open on Monday unless it’s a tight outcome that comes down to counting mail-ins, we may not know Merkel’s successor for quite some time. The need to form a coalition government and pick who will be the face of it could be a protracted contest well after voting has completed. Like the Canadian election, at stake is the size and scope of potential fiscal policy actions and how that could influence supply of bunds—not to mention the challenge of filling Merkel’s shoes as not only a capable domestic leader but also a European and global stateswoman.

CENTRAL BANKS—HIKERS AND HOT SEATS

Across major global central banks, the dominant focus is likely to be upon the PBOC’s actions in the aforementioned Evergrande context. We’ll hear from others, but their incremental impact upon market tone is likely to be fairly low. Three regional central banks will deliver decisions including two in Latin America and one in Asia.

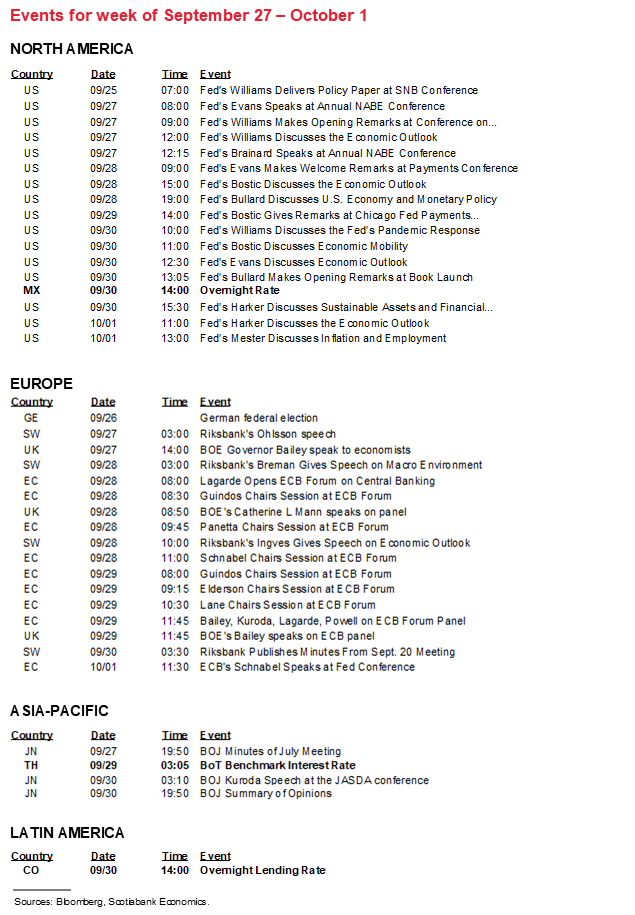

The ECB holds its annual ECB Forum on Central Banking online on Tuesday and Wednesday. The agenda is here. It’s her show, so ECB President Lagarde will kick it off with introductory remarks at about 8amET on Tuesday. She will also participate in a moderated policy panel starting at 11:45amET on Wednesday alongside other heavy hitters including Fed Chair Powell, BoE Governor Bailey and BoJ Governor Kuroda.

Chair Powell is likely to need throat lozenges by week’s end. His appearance at the ECB conference will be bookended by testimonials before Congress. On Tuesday at 10amET he will join Treasury Secretary Yellen to provide CARES Act testimony before the Senate Banking Committee. They press rewind and do it over again before the House Financial Services Committee on Thursday at the same time.

Powell could face aggressive questioning on several fronts. A recap of the decisions that were made at the recent FOMC meeting is available here. Strong questioning around internal compliance matters is very likely from both sides of the political spectrum in light of the controversy surrounding the trading activities of the Presidents of the Boston and Dallas district banks. Why annual disclosures were not further explored by the Board, whether any compliance line was crossed and whether poor judgement was demonstrated independent of compliance violations will be hot button issues.

Powell is likely to be grilled about inflation and his complete 180˚ turn from arguing it was purely base effect driven earlier in the year toward now saying the price stability part of the Fed’s dual mandate has been met amid concern toward supply chain risks. He may also be questioned about an apparent shift in thinking on how monetary policy should manage inclusive growth; until not long ago, Chair Powell was delivering speeches that implied the Fed wouldn’t tighten until it had a fully inclusive labour market rebound whereas his latest press conference (rightly) downplayed the ability of monetary policy to affect such outcomes and emphasized an upbeat posture toward nearer term job markets. Whether the Fed Chair was too sanguine toward Evergrande’s risks may be probed further alongside his views on the debt ceiling and funding. Powell ducked such questions before the press this past week, but whether he gets away with that before Congress may be a different matter and not just because Chair Bernanke made it clear in July 2013 he wouldn’t taper if deep uncertainty around fiscal policy was hanging in the air.

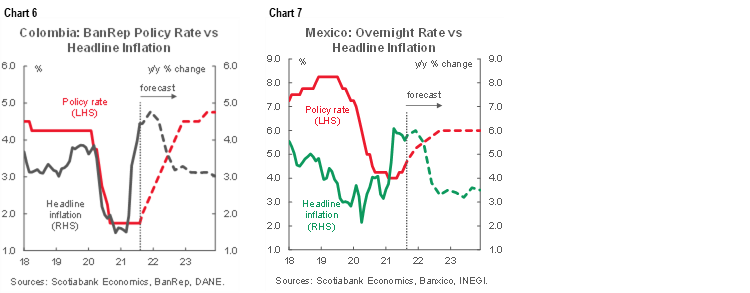

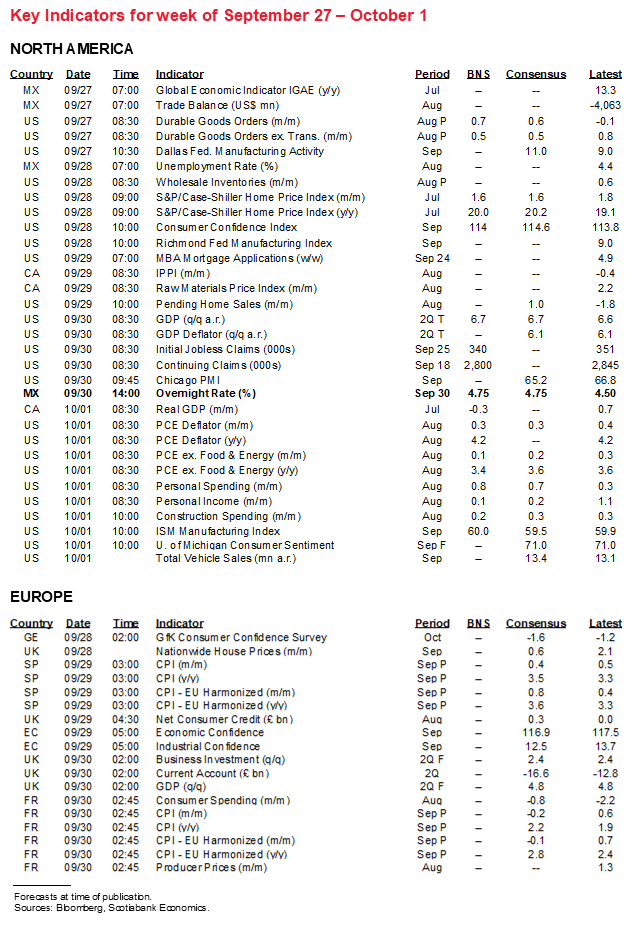

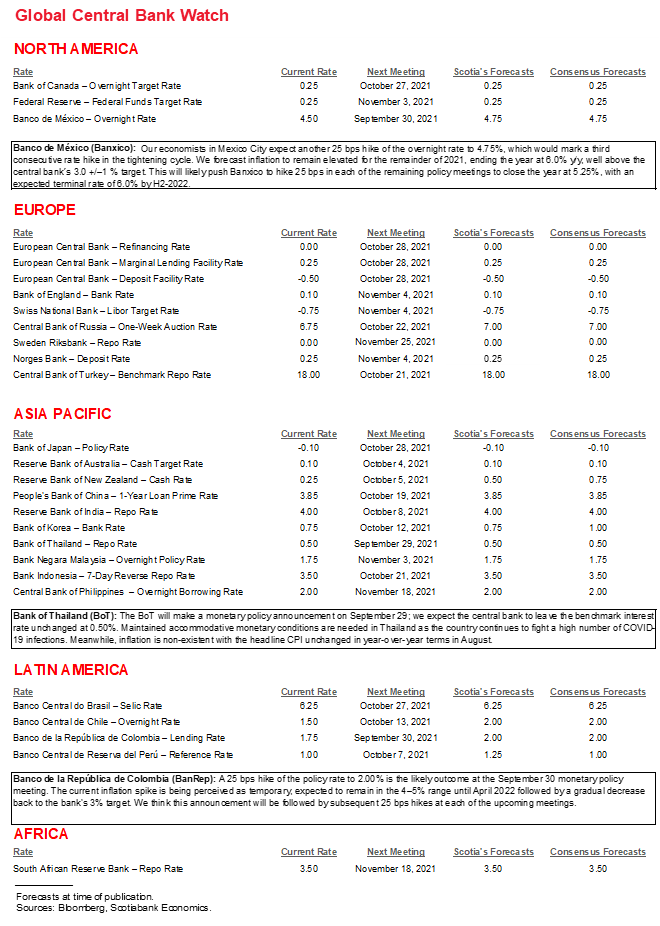

Thursday is also expected to bring a pair of LatAm central bank hikes and at the exact same time of 2pmET no less! In alphabetical order, Colombia’s BanRep is expected to hike by 25bps to 2%. Mexico’s Banxico is also expected to hike by 25bps to 4.75%. Both central banks’ policy rates and inflation rates including forecasts are shown in charts 6 & 7). Banxico commenced a hiking cycle with the shock hike in June and next week could make it three in a row. The cycle started with Deputy Governor Heath arguing that inflation was underestimated (“screwed up” as he put it) and that “perhaps we have a problem that’s a bit more structural that we need to focus on.” Since then, we’ve seen inflation pull off a peak of 5.8% y/y to 5.6% in August while remaining well above the 3% +/- 1% target range, but core inflation has continued to climb to 4.8% y/y. Our Mexico City economists expect the overnight rate to climb to 5% by the December 16th meeting on the path to a 6% peak over the first half of next year.

Unlike Banxico, BanRep’s expected 25bps hike to 2% would be the first of the cycle. Like Banxico, however, the catalyst is upward pressure on inflation. Core inflation sits at 3.1% y/y and headline inflation of 4.4% remains above the upper band of BanRep’s 3% +/-1% target range.

No policy change is expected to be delivered by the Bank of Thailand on Wednesday.

GLOBAL MACRO REPORTS

Purchasing managers’ indices from China and the US will be closely followed. China’s state version of the composite PMI (Wednesday night ET) is expected to rebound as services move marginally out of contraction. The US ISM manufacturing gauge (Friday) could face upside risk from the prior month’s strong growth signals if the gains in regional surveys like the Philly and Empire measures are any indication.

Canadian markets will be quiet for most of the week and then bonds will shut on Thursday for the first ever National Day for Truth and Reconciliation. The stock market will remain open. Then Canadian GDP lands for July with preliminary August guidance. StatCan had guided -0.4% m/m in its ‘flash’ guidance on August 31st. There has been limited new information since then. July housing starts fell by 3.3% m/m, but we don’t know what construction figures were being assumed. August data has included a 0.1% m/m rise in hours worked, a 0.5% ‘flash’ estimate for manufacturing sales and a 3.9% m/m drop in housing starts.

The other main US releases will include the following:

- Durable goods orders during August (Monday): Supply chain issues and capacity constraints will probably continue to feed gains in core capital goods orders excluding defence and air. Boeing’s mild pick-up in plane orders in August compared to July could add to the gain in total durable goods orders.

- The Conference Board’s consumer confidence for September (Tuesday): Will it stabilize after dropping in August? Part of the uncertainty surrounds what happened to hiring and we won’t learn that until payrolls arrive but watch the jobs availability and inflation signals.

- Inflation, spending and incomes during August (Friday): July registered a strong gain in income growth as the Biden administration’s child benefit cheques began arriving. The cheques will continue to arrive but the impact on income growth should subside while nevertheless driving strong trend growth. That’s one reason why consumption is expected to grow at an accelerated pace as the already known strong gain in the retail sales control group (+2.5% m/m) is likely to be moderated by services consumption due to the rise of the Delta variant. The Delta variant might also see the Fed’s preferred inflation gauge moderate in line with the already known CPI figures for August.

Hawks will likely circle above the ECB building in Frankfurt on Friday when the Eurozone inflation add-up lands. Previews will be offered by releases from Spain (Wednesday), Germany, France and Italy (Thursday). Core is expected to rise above 3% y/y for the first time since October 2008. Base effects are a considerable part of it all and will continue to drive the year-over-year rate higher until at least year-end. The rise cannot be dismissed as simply driven by soft starting points for year-ago prices, however, as monthly gains have also been sizeable. The full recovery in market-measures of inflation expectations has been among the concerns of some of the ECB’s more hawkish voices (chart 8).

PMIs are also due out in Mexico (Friday), Brazil (Friday) and with Japan’s Q3 Tankan report adding to growth sentiment signals on Thursday.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.