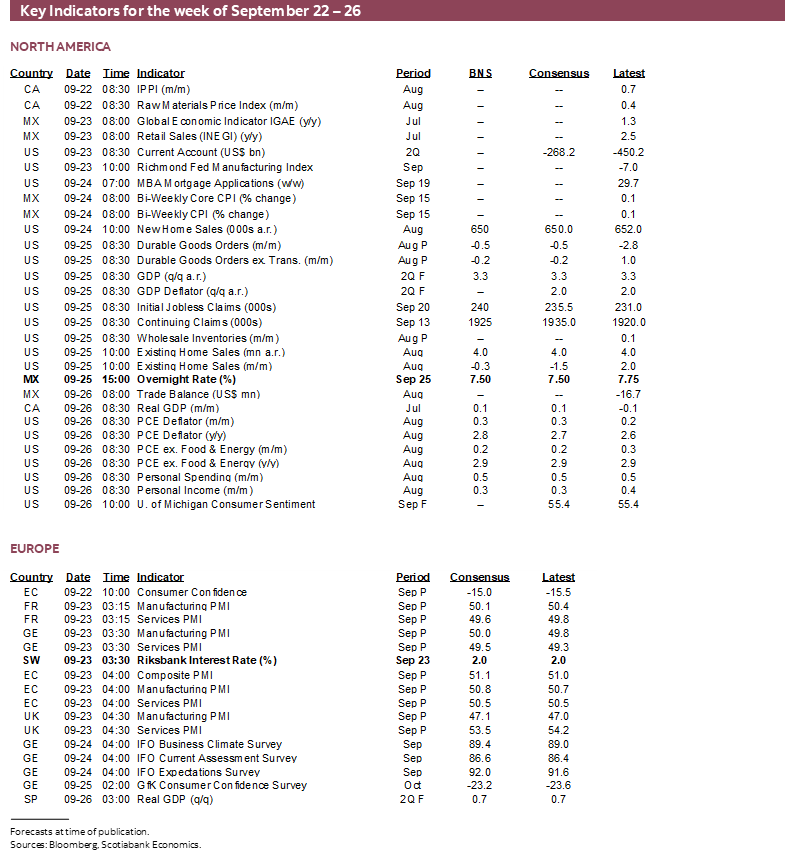

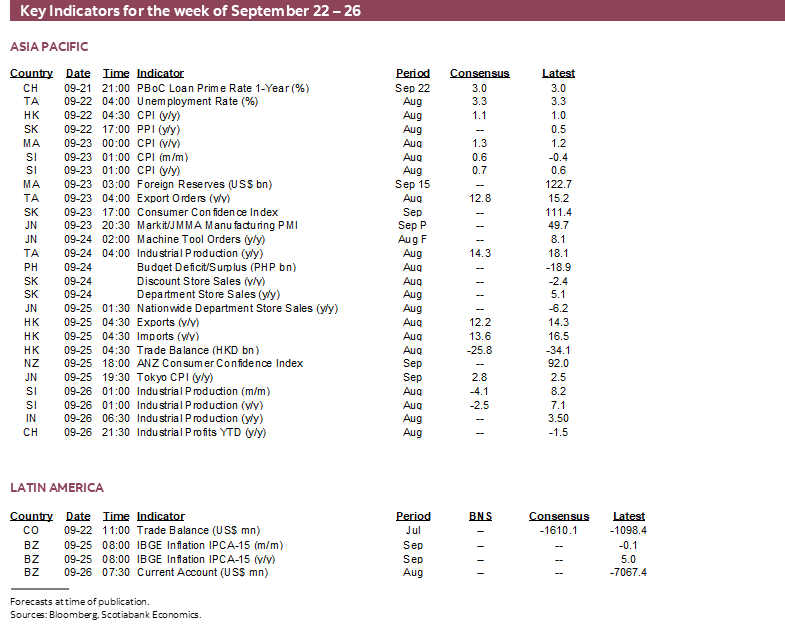

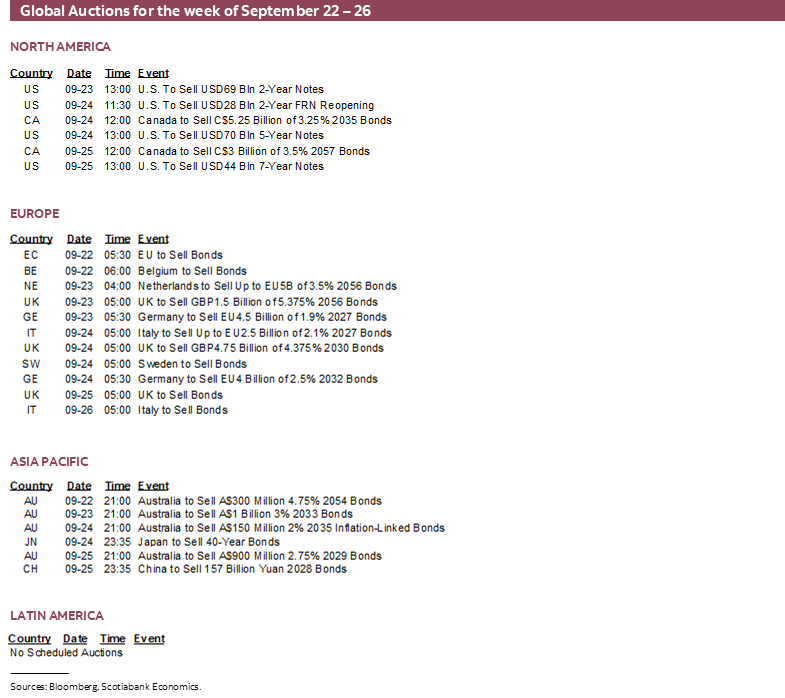

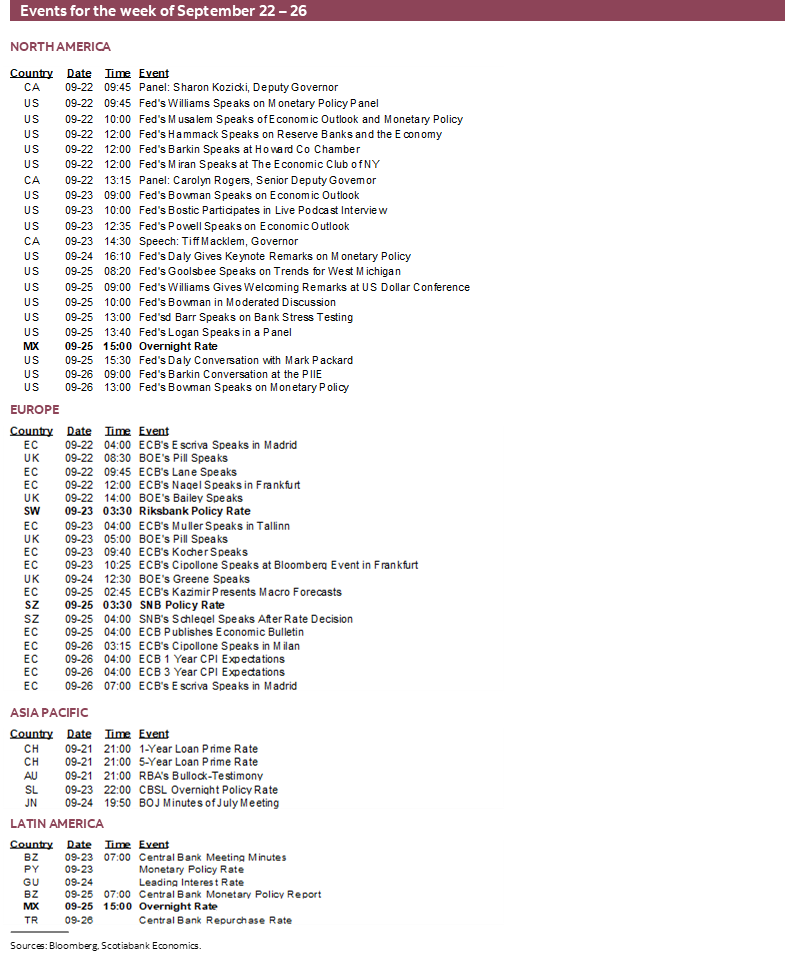

Next Week's Risk Dashboard

- ‘Reformists’ are under pressure

- Markets are rapidly overtaking Milei’s reforms

- Trump’s support is softening as policies become more binding

- Fed-speak: some motives are purer than others

- Canadian GDP barely chugging along

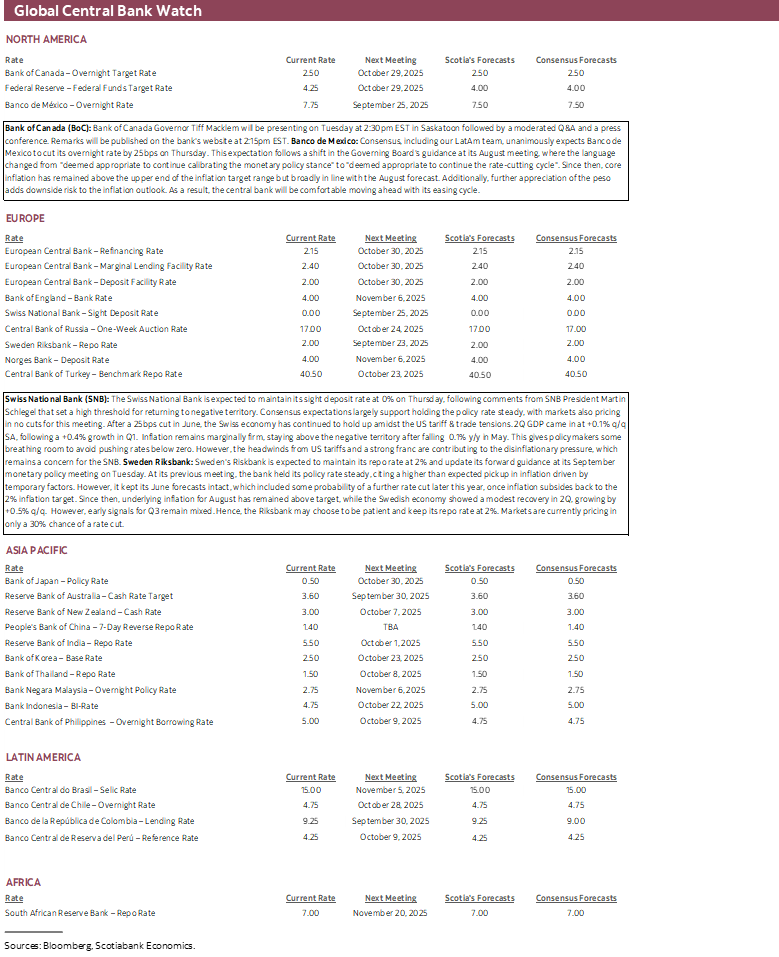

- BoC’s Macklem to speak on trade. Again.

- PMIs: EZ, US, UK, India, Japan, Australia

- US PCE: on the fence

- US GDP to be revised back to 2020

- SNB facing renewed negative rate debate

- Riksbank faces a tough call

- Banxico likely to follow the Fed, with some twists

Chart of the Week

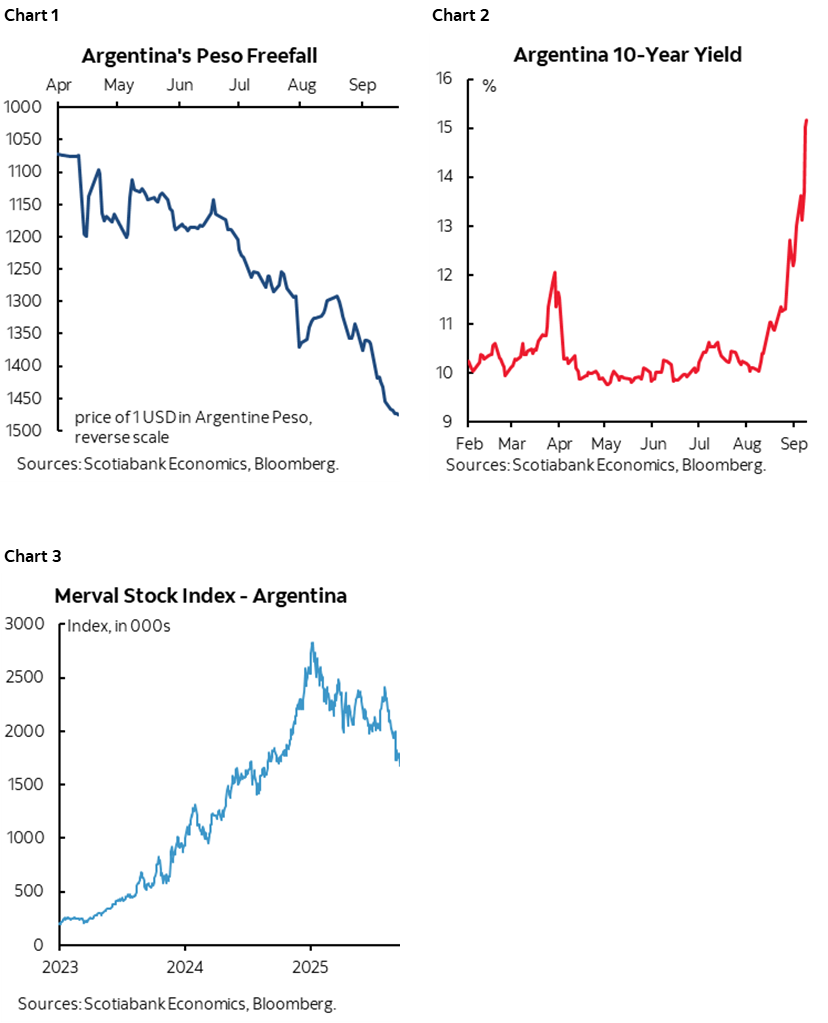

Is the ‘reformist’ party unravelling?

Argentina’s Javier Milei won election in 2023 and has enjoyed praise from similarly minded leaders elsewhere. Mr. Milei is in deepening trouble as the chainsaw used by the colourful Milei—and borrowed by Elon Musk—seems to be severely malfunctioning. Argentina’s peso is in freefall once more with chart 1 showing the official rate while market rates fall faster. So are its bonds as the 10-year yield has soared from just over 11% a few weeks ago to nearly 18% now (chart 2). Argentina’s Merval—the country’s main stock index—enjoyed a burst of optimism in the earlier days of Milei’s victory on November 19th 2023 up to the start of this year. It has since fallen by about 40% from the peak while nevertheless still retaining large gains for those who got in early (chart 3).

Milei once claimed to be supportive of dollarization. He’s now spending currency reserves at a frenzied pace to prop up the peso that is in freefall. Fixing at this exchange rate would risk returning the country to rampant hyperinflation which Milei promised to end. The very essence of his reforms are in jeopardy and with that the unfortunate hopes of Argentinians too used to policy failures.

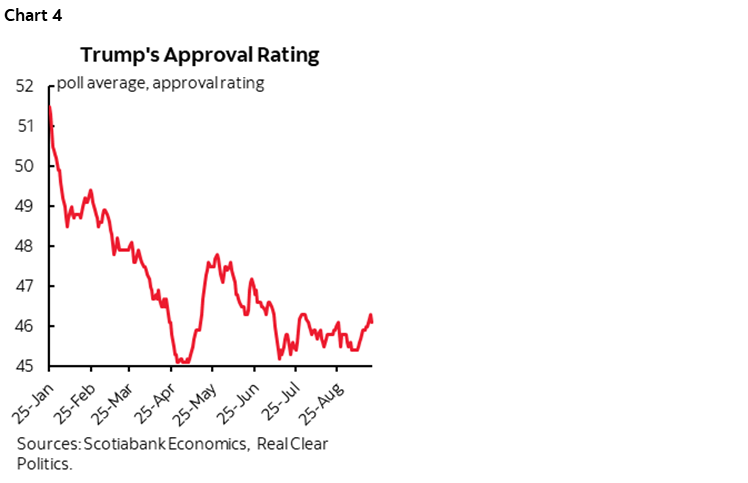

President Trump—who met with Milei shortly after the US election last November—has been strongly supportive of Milei’s reforms and pursued his own mixture of aggressive policy reforms. US trade policy is likely to be more growth-dampening into 2026 unless the Supreme Court successfully alters the course as soon as November. Ditto for immigration policy, including an expected move to essentially kill off the H-1B visa program for many applicants with a US$100k fee. The effects on labour supply across all skill levels is widely expected to materially harm US growth. This week will further amplify tensions at the central bank with a slew of speakers from the Chair to the dissenting Governor Miran and many others that seek to convince markets the debate is free of untoward influences.

Voters are taking notice. President Trump’s own support is well beyond the honeymoon stage with his base (chart 4), but not obviously low enough to spark concern especially given the nature of the US electoral college system.

Against this backdrop of larger forces will be a relatively more subdued week for global macro risk. Only three central banks will weigh in but watch them carefully. Negative rates may not be dead as tariff-related currency flows spark deflation risk for the SNB. Banxico is likely to continue easing but is walking a balancing act. Sweden’s Riksbank faces a decision on a knife’s edge. Fed-speakers are grappling with trying to support labour markets being harmed by tariff effects on hiring and immigration policy, while they are divided on inflation risk. Macro indicator risk will focus on Canadian GDP, US PCE inflation, and another batch of ‘soft’ data on orders, prices and hiring within global purchasing managers’ indices.

CANADA’S ECONOMY—BARELY CHUGGING ALONG

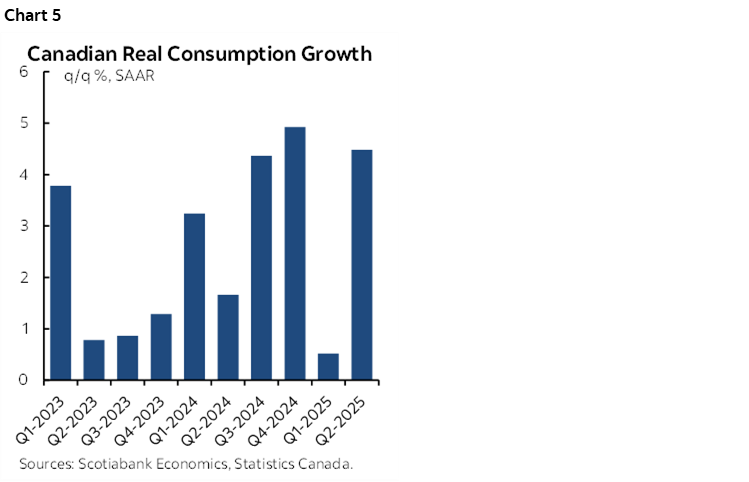

Canada watchers will have a better idea of how the economy is performing on Friday. A pair of monthly GDP figures will improve our tracking of growth during the third quarter. This follows a mixed prior quarter that saw GDP shrink due to trade and inventory effects, but the domestic economy soar with significant thanks to consumer spending (chart 5).

The pair of monthly GDP readings will include the final estimate for July along with details that were missing in the preliminary estimate, plus the preliminary estimate for August GDP.

Statcan had guided back on August 29th that the economy eked out 0.1% m/m growth in July. They noted that the bright spots were real estate, mining and quarrying and wholesale trade but retail trade was a soft spot. The final estimate may be revised but is likely to remain fairly soft. One key is that hours worked fell by -0.2% m/m SA; since GDP is hours times labour productivity it would take a surge in productivity and activity readings to drive significant growth. Higher frequency gauges are not indicating this happened.

August GDP might be slightly more encouraging, but we have light data to go by. August hours worked picked up a touch (+0.1% m/m SA, -0.2% prior) which supports GDP. Retail likely added a small amount to growth. Housing was mixed as starts fell back somewhat but the lagged effects of a four-month surge in new homes placed under construction could continue to offer a spending lift alongside the effects of another monthly gain in resales on ancillary services (lawyers, agents, lenders etc).

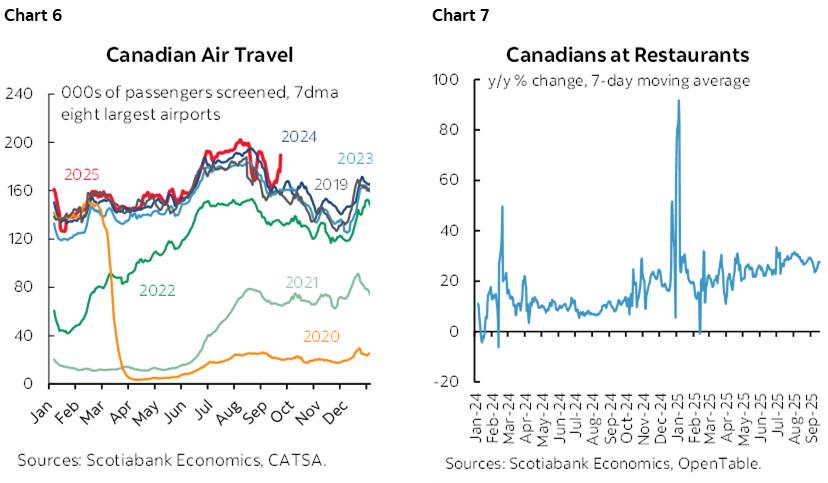

We can also point to select service sector readings, like soaring air travel (chart 6) and restaurant bookings (chart 7). Recall that retail sales in Canada only captured around 47% of total consumer spending; retail includes no services. Therefore, signs of robust spending on air travel, hotels, movies, concerts, sporting events, restaurants, bars, financial services etc also have to be taken into account in what is probably ongoing consumer resilience.

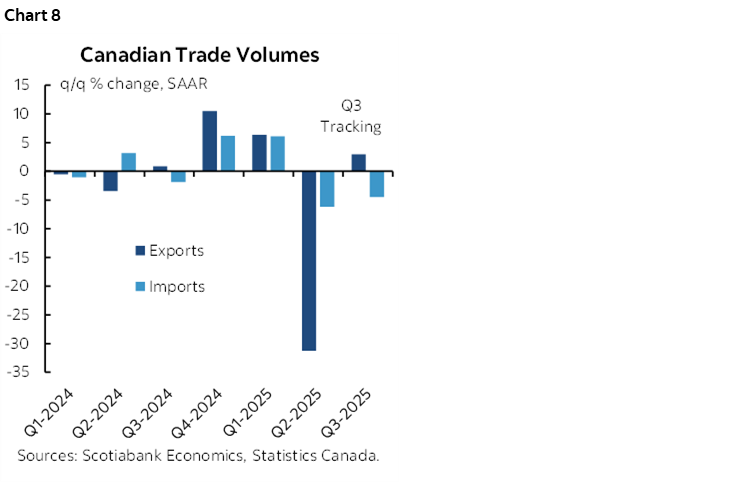

Overall, the economy is likely tracking soft growth of somewhere under 1% q/q at a seasonally adjusted and annualized rate in Q3. That’s using the monthly production-side GDP accounts. The expenditure-based GDP accounts that most forecasters focus upon could offer some upside if the high volatility in export volumes from 2024Q4 through 2025Q2 stabilizes in accordance with tracking to date (chart 8).

So where does all of that leave us? GDP is barely chugging along in Q3, but the GDP details matter. As the BoC’s latest statement noted, “Governing Council will be assessing how exports evolve in the face of US tariffs and changing trade relationships; how much this spills over into business investment, employment, and household spending; how the cost effects of trade disruptions and reconfigured supply chains are passed on to consumer prices; and how inflation expectations evolve.” A recap of the latest decision is here.

In short, GDP is one input, but not the be-all-and-end-all from a BoC policy standpoint. For one thing, let’s also see the federal budget on November 4th. For another, we’ve only just started the drama on the path to renegotiating the CUSMA/USMCA trade deal.

CENTRAL BANKS—TARIFFS RISK BRINGING BACK NEGATIVE YIELDING DEBT

Three central bank decisions and a whole mess of central bank talk will keep the space active after this past week’s torrent of activity.

Banxico—Follow the Fed, With a Few Twists

Mexico’s central bank weighs in with a policy decision on Thursday. A Reuters survey showed economists unanimously expecting a 25bps rate cut to 7.5%. That would extend the easing cycle to a cumulative 375bps.

Guidance provided at the August 21st meeting that accompanied a 25bps rate cut shifted more to the affirmative in replacing wording that policy was merely being ‘calibrated’ to now how it was “deemed appropriate to continue the rate-cutting cycle.”

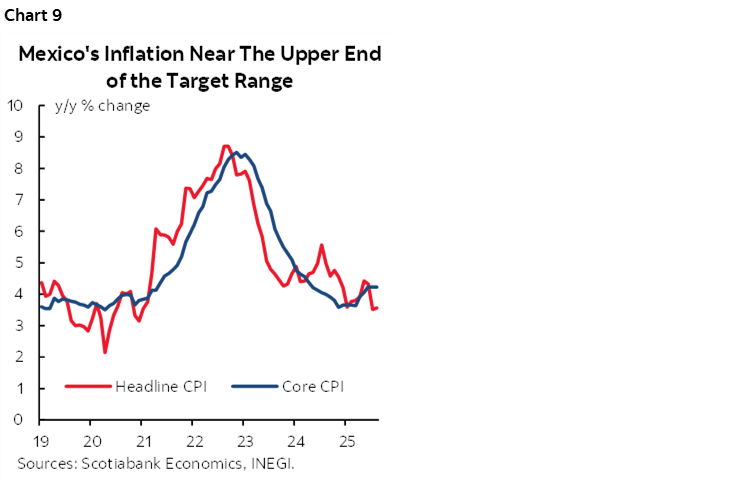

Another reason for the cut is that while it doesn’t always follow the Fed, Banxico frequently does so and the FOMC just restarted what we think will be a material easing campaign. US tariffs and uncertainty around USMCA negotiations add to motivations to ease. Recent data has been mixed as jobs and wages hold up quite firmly, but industrial output has fallen over the past couple of months. The peso has appreciated from about 20.8 to the dollar in April to 18.4 now. Such forces will nevertheless be accompanied by a weary eye turned toward core CPI inflation that has risen back to about 4¼% y/y over recent months (chart 9).

BoC’s Macklem to Speak on Trade—Again!

Canadian short-term interest rate markets will further consider the effects of policy announcements made by the Bank of Canada late on Friday afternoon to address funding market challenges (here).

Fresh off his latest tour de force, Bank of Canada Governor Macklem speaks Tuesday on ‘global trade and capital flows.’ The speech embargo lifts at 2:15pmET and there will be a press conference at around 3:45pmET following speech delivery and audience Q&A. Major new points are unlikely to be shared in relation to what was shared this past week (recap here) and other speeches. Trade is front and center in terms of BoC concerns for readily apparent reasons, hence why he has delivered so many speeches on it over about the past year (here, here, here and back here before the US-driven trade war).

Competing Fed-Speak

Several Federal Reserve officials hit the trail to deliver post-decision takes on monetary policy and the outlook. We’ve already heard from some. Chair Powell will give a speech on the economic outlook on Tuesday. NY Fed President Williams, KC President Musalem, Cleveland’s Hammack, and Richmond’s Barkin speak Monday. Governor Bowman and Atlanta’s Bostic appear Tuesday. San Fran’s Daly (Wednesday) will be followed by each of Chicago’s Goolsbee, Williams (again), Bowman (again), Governor Barr and Dallas President Logan all on Thursday. Richmond’s Barkin and Bowman (again) wrap it up on Friday. There may be more.

But since he stuck out, more of the focus may be upon Federal Reserve Governor and government loaner Stephen Miran who will deliver a speech at the Economic Club of New York on Monday (12pmET). He pledged to explain his dissenting vote in favour of a 50bps cut this past week and another 100bps before year-end. He shared some of his views in media interviews on Friday and in my view he’s more of a media factor than someone whom markets will treat seriously.

Miran’s argument is that he did not have time to be more persuasive with his FOMC colleagues since he was confirmed right before the meeting and therefore if only others had heard his views he could have convinced the whole lot of them. That’s debatable, given explanations of his views that he provided in Senate testimony and on other occasions. All of his colleagues could see Miran coming from a mile away.

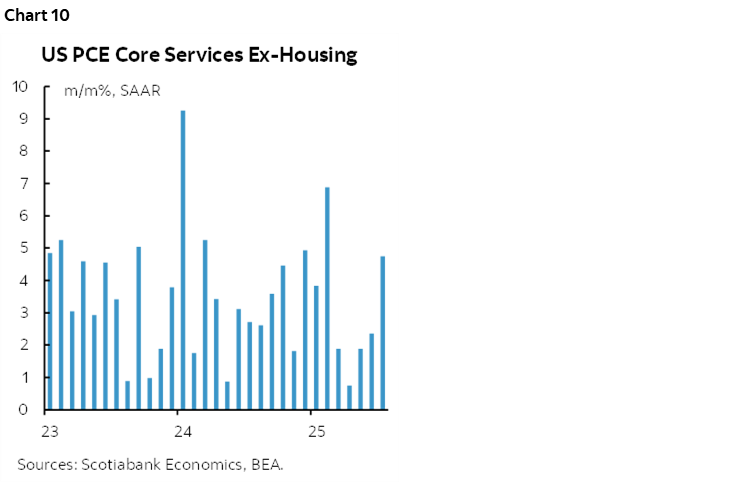

He may be right on shelter cost disinflation due to drastically tighter immigration policy which is an admission by a Trump official that Americans’ home prices are at risk from immigration policy. Shelter is an important 35% part of inflation measures, but where much of the uncertainty around inflation driven by services resides is in the ex-shelter and energy services component that is one-quarter of the CPI basket (chart 10).

But Miran’s views on tariffs are far too strident and too narrow. He dismisses any evidence that tariffs are driving inflation and any prospect that they may in future. There are the usual counterarguments to this view. There is some evidence in hard data and especially soft data that tends to lead hard data (like ISM-prices, or NFIB prices). It’s far too soon to evaluate the effects of tariffs given all the fits and starts and very recent full application. Mitigating factors against tariff pass through into prices in the short-term can include swallowing them in profit margins, selling down inventory at pre-tariff prices, uncertainty over whether to adjust pricing models if tariffs are permanent or temporary, etc. We don’t know if tariff pass-through will fizzle out or spark second- and third-round effects on other prices, wages, and considerations like productivity and the supply side of the economy. Further, tariffs are merely one source of potential pressure on costs and prices from supply chain turmoil and border frictions that have massively increased over the years and that could drive elevated inflation risk for years to come. Think Brexit. Think Trump 1.0 tariff-light that drove some prices higher (eg. appliances), but was too limited to have a macro effect while nevertheless costing jobs by multiple studies. Think the pandemic. Think geopolitical conflicts like Ukraine or the Red Sea shipping lanes or the Middle East and hopefully not the Taiwan Strait. Like Trump 2.0 tariff-heavy. Add to that a potentially massive global increase in spending on defence and infrastructure and the complicated demand and supply-side effects.

Supply chain economics befuddle people who study them all the time. Key is whether decades of unidirectional outsourcing to produce in the lowest cost markets when border frictions were manageable is now at a nascent stage of pivoting toward accepting higher operating costs in order to lower financial distress costs including lost sales or outright bankruptcy. It’s not something to be evaluated by a single inflation reading; that’s just ridiculous myopia. It’s likely to be a multi-quarter, multi-year, and perhaps multi-decade phenomenon. Policymakers need to be very careful in this environment and leave the table pounding behind trade ideas to the so-inclined elements on the street.

In any event, Miran may well be gone after the January FOMC meeting and hence before the March FOMC and updated SEP at that meeting. Unless, of course, Mr. Miran’s efforts toward persuading everyone is oriented toward persuading the one man who must nominate someone not presently on his winnowed list of three (Hassett, Warsh, Waller). In the meantime, markets will continue to question how independent Miran’s views truly are; saying President Trump didn’t tell him how to vote is insufficient relative to the motivation to get the job in the first place.

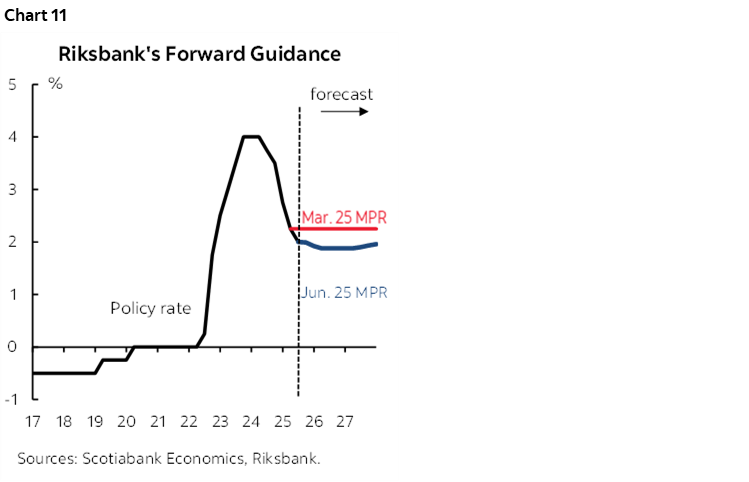

Riksbank—Oh What’s a Central Bank to Do?!

Sweden’s central bank will deliver an updated policy decision on Tuesday alongside updated explicit forward guidance.

Consensus is divided. The median forecast is for a hold, but barely so as just under half of forecasters expect a 25bps cut. Markets have priced a roughly one-in-three chance at a cut.

The last time the Riksbank offered projections in June they included a chance at a cut over the remainder of 2025 (chart 11). That guidance was repeated in August’s policy decision that stated the Executive Board “still sees some probability of a further interest rate cut this year.” That could mean now, or the November 5th or December 18th decisions.

The evidence has been mixed since the August meeting. Underlying inflation removing more volatile items edged lower to 2.9% y/y in August. Growth in Q2 was slightly firmer than expected at 0.5% q/q SA. That may be bumped up since June GDP was revised sharply higher (1.4% m/m from 0.5%) but July GDP is tracking a small decline. The job market has been weakening as the unemployment rate now stands at 8.8% from a cycle trough of 6.8% about three years ago and on a fairly steady upward trend.

Few may fault the central bank for whatever decision it makes at this juncture.

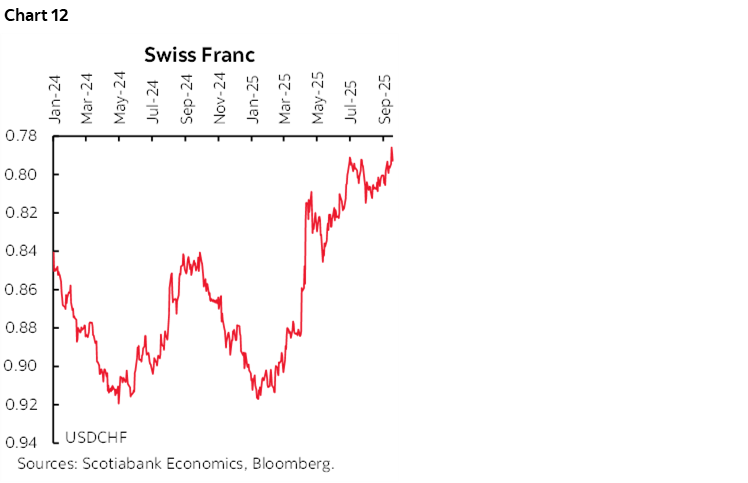

SNB—No to Negative Rates?

The Swiss National Bank updates its policy stance on Thursday. All but one in consensus expect the central bank to hold its policy rate at 0% with one consulting outlier expecting -0.25%. SNB exited negative rates in September 2022.

Negative rates should not be ruled out. The SNB has been battling franc strength all year long with no clear signs it is subsiding (chart 12). CHF has appreciated by about 14% to the dollar in 2025 and earlier rate cuts have failed to take the wind out of its sails. Given high import propensities in the Swiss economy, this serves to add to downside pressure on expected future inflation.

Inflation is already nonexistent in the Swiss economy. CPI stands at 0.2% y/y with core at 0.7%. That prices are not going up may sound welcome to consumers, but deflation wouldn’t be either given its potentially nasty consequences. Expectations that prices could keep falling risk driving a self-fulfilling prophecy through postponed purchases into an environment when prices are expected to be lower.

The Swiss rates curve is braced for low inflation and very low to negative rates to persist. The two-year yield stands at -21bps. The ten-year yield is at just +14bps. There is basically no material inflation risk or term premia built into the curve.

As such, Switzerland may be anomalous, or hopefully not a renewed sign of pressures to come in the global financial system. From a peak of about US$18.4 trillion in 2020, global negative yielding debt has since collapsed. The drivers of the Swiss dilemma may be idiosyncratic as markets have sought CHF as a safehaven during trade wars and in light of Trump’s massive tariffs against the country. They cannot, however, be fully ignored.

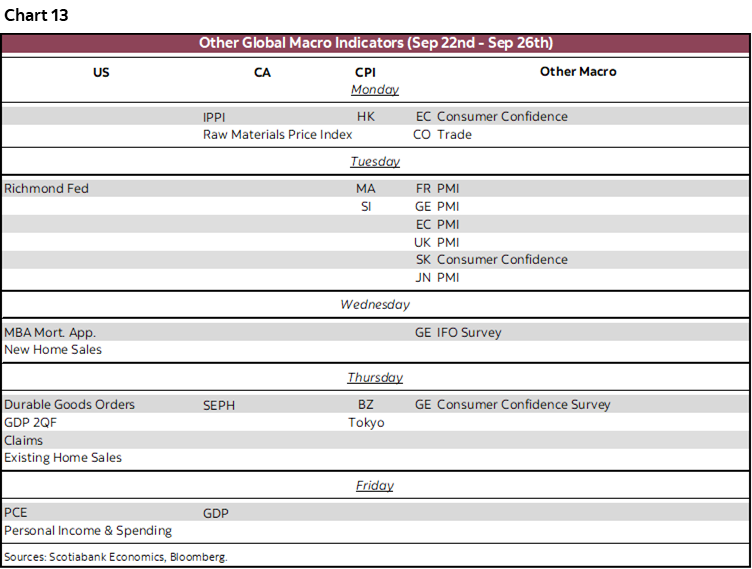

GLOBAL MACRO—PMIs AND US INFLATION

Chart 13 summarizes other key global releases. There won’t be many this week. In fact, only two examples may really stand out.

First is the batch of purchasing managers indices that provide a rich array of information on measures like new orders, hiring attitudes, and prices in manufacturing and service industries. Australia kicks it off Monday evening (eastern time) followed by India a few hours later, then France, Germany and the Eurozone tally. The UK releases early on Tuesday morning followed by the US several hours later. Being September readings we’ll have a particularly keen eye on price signals but with the usual caution it’s still very early days for tariff and broader supply chain effects.

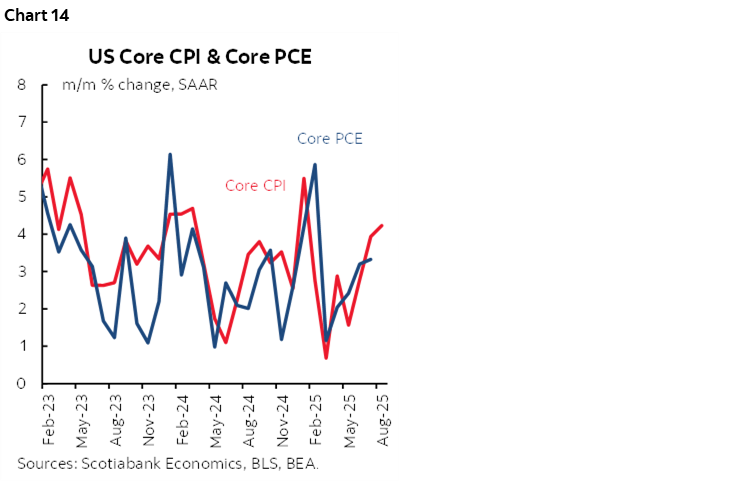

The Fed’s preferred inflation reading is the other key reading this week along with annual and Q2 GDP revisions back to 2020 that will also reflect downard revisions to job market readings from April 2024 to March 2025 (Thursday). Friday’s core PCE inflation measure for August is likely to climb by 0.2% m/m SA but our calculations are somewhat on the fence between 0.2 and 0.3. They take into account core CPI of 0.3% m/m SA (chart 14), plus weight differences on some categories in CPI versus PCE, plus the limited number of producer price categories that then get incorporated into PCE inflation. Calculations are shown in chart 14. These are not the only adjustments to be made which adds to some uncertainty. PCE, for example, allow for more rapid substitution effects away from rising prices toward other choices than CPI because PCE adjusts spending weights dynamically versus once a year for CPI. That could matter a fair bit amid tariff turmoil.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.