Next Week's Risk Dashboard

• Canadian election

• CBs: Fed, BoE, BoJ, PBOC, Norges, Riksbank…

• …BCB, BI, BSP, SARB, SNB, CBCT, Turkey

• PMIs: US, EZ, UK, Australia, Japan

• OECD outlook

• Other macro

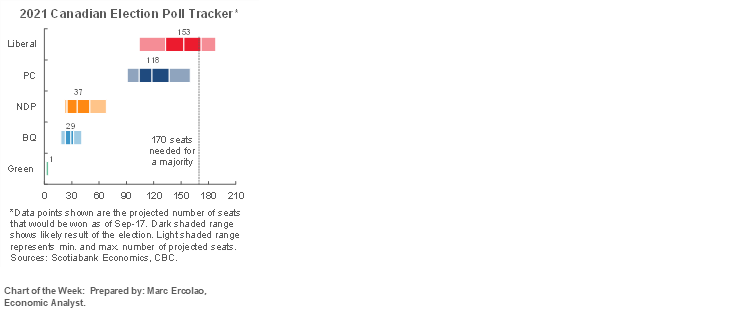

Chart of the Week

My oh my, September’s return kicks into higher gear for global markets next week. There should be something that strikes everyone’s fancy whether it be one or more of the over a dozen global central bank decisions, Canada’s election drama and possible consequences for markets and the BoC, and a sprinkling of global market data. It all starts close to home on Monday.

CANADIAN ELECTION—HOW TO WATCH RESULTS, MARKET EFFECTS AND THE BANK OF CANADA

Finally, the longest short election campaign in Canadian history is coming to a close! A veritable cottage industry of policy wonks and wannabes live for this day, but should market participants? What follows is an attempt to lay out the parameters for consideration toward assessing market outcomes at first and over time.

When to Expect Results

The first question is when will results be known? The common narrative is that we won’t know on election night and it could take days to find out, but that’s not necessarily true and not least because that narrative assumes pollsters might actually get this event right! Perhaps have a back-up option…. Pollsters know their business, but uncertainties around voter turn-out, how honest disclosure of voting intentions may prove to be when it comes time to checking the box, and the greater difficulty of translating popular votes into seat projections are a few of the challenges that plague their trade. Thus, it would be imprudent to strongly advise market participants to simply go to bed on Monday evening across the affected time zones on the assumption they needn’t watch their market positions until the next and subsequent days.

The counts for votes cast in person on election day and in person at advance polls will start to be released on Elections Canada’s web site and shortly thereafter by media outlets once local polls close. In a big country like Canada that spans multiple time zones this process can take a while. The first polls to shut on Canada’s east coast will do so by 7:00pmET in Newfoundland followed by the rest of Atlantic Canada at 7:30pmET. These early votes may be particularly skewed toward the Liberals based upon present polling and may therefore provide potentially misleading signals that market participants should be inclined to discount.

Then there will be a fairly long gap until results from vote-rich central Canada and then through the Prairies will start arriving by shortly after 9:30pmET. If the polls are wrong—not that this ever happens!—and it’s a runaway majority outcome, then we might essentially know the results of the election around this time just by virtue of the population densities in central Canada in which case folks in western Canada stop eating poutine for a week. If the results are tight by this point, however, then it may come down to a nail-biting finish as the last polls shut in BC by 10pmET and results will begin to arrive soon thereafter. It’s across western Canada where the Conservatives are polling highest which may prove to be the swing factor for a minority outcome. A longer pandemic voting experience whereby anyone in line by the close of polls must be counted could delay results everywhere and so you may see broadcasts of lines outside polling stations.

Then it’s down to counting the mail-in ballots which will happen starting a day after the election once they’ve been validated. The mail-in counting process could take several days, but it’s not impossible that the election results will be known on Monday night based on advance voters and day-of voters. That’s partly because the number of mail-in ballots requested (1.00 million)—while still a record—came in a lot lower than what Elections Canada had previously expected (2–3 million). Further, only about 707 thousand kits had been received back by Elections Canada up to and including Thursday September 16th before sending this publication and it’s safe to assume that some amount will not be sent back, like if they awaken to the fact that Doug Henning isn’t on the ballot. Further, there were more advance voters (5.8 million) like me who voted between September 10th – 13th than in the 2019 general election (4.9 million). It’s also unclear whether fewer than expected mail-in ballots will mean more people showing up to vote on election day or reduced voter turn-out in aggregate given, oh, the pandemic and general voter skepticism. In 2019 there were 18.35 million votes cast out of 27.4 million eligible voters and so something closer to 19 million turning out this time would mean we should know ~18 million of those votes on election night.

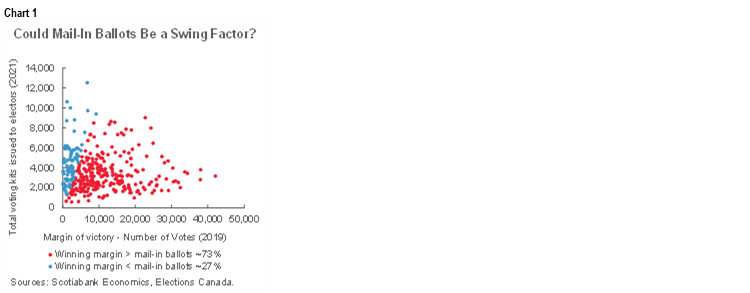

If the seat counts are looking really tight, then the mail-in ballots could easily be the swing factor in the results and appear similar in that regard to the 2020 US election, minus some of the nuttier considerations! It’s going to come down to lining up the vote count in ridings with the most mail-in ballots requested. A lot of ridings could be swung in either direction by mail-ins.

Chart 1 shows a way of considering this by taking the margin of victory by riding in the 2019 election and mapping it onto the number of mail-in ballots requested by riding in this election. 27% of ridings had a narrower margin of victory in 2019 than the 2021 count of the number of mail-in kits requested as shown by the blue dots in the chart.

Financial Markets

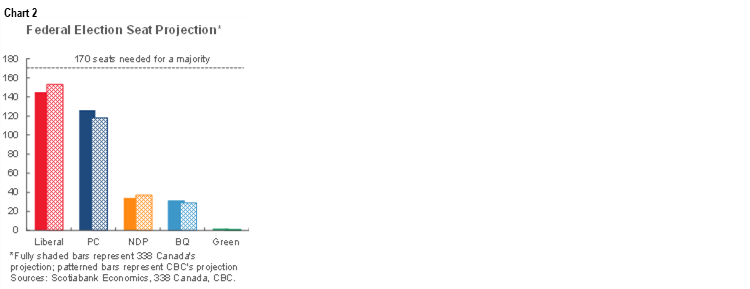

What would surprise international investors in the currency and bonds? That’s difficult to glean from market data, but starting with tongue-in-cheek, one indication may be derived from bets placed through foreign bookies like here. Foreign bettors think the Libs are a slam dunk and much more so than local polling results indicate (chart 2). Then again, they may not be the best informed. Foreign bettors also think that Chrystia Freeland and Manitoba MP Candice Bergen are running for PM and have the same odds of winning as either the NDP or BQ leaders! Caveat emptor… Then again, if you buy lottery tickets, then a small payment can yield a big pay-off on the Conservatives, not that I’m condoning betting!

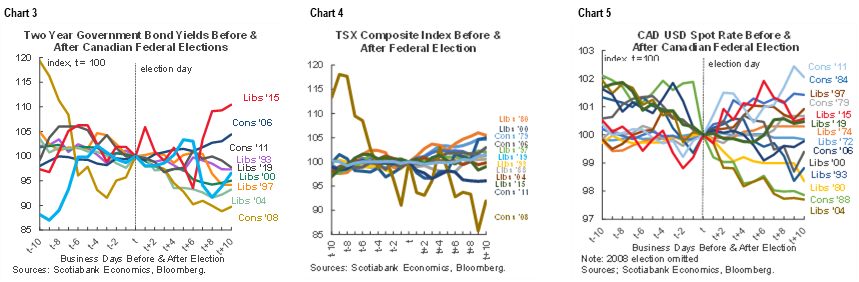

Charts 3–5 show the impacts of past elections on bonds, stocks and the TSX in the days leading up to and following the election results. Whether this one offers any clearer market outcome depends critically upon high uncertainty in the immediate aftermath of the election.

A clear majority outcome could boost the currency and raise bond yields by emboldening either the Liberals’ or Conservatives’ plans to pursue more expansionary fiscal policy. Recent momentum toward a depreciating currency over recent weeks may further motivate such a reaction versus a currency on a strengthening trend. That may well be the initial market response until uncertainty creeps back in that could make it wise to take profits. A second market reaction would likely consider uncertainties like whether the lower likelihood of a coalition with the left wing NDP can result in less pressure on expansionary fiscal policy, or if a Conservative or Liberal majority chooses to keep some spending powder dry toward faster deficit repair and leaving something in the cupboard for down the road. It would also establish up to a 5-year term in office for the winner and likely create resulting political stability.

A minority outcome’s market effects are much trickier to assess in first, second and subsequent market responses. For one thing, if it takes a while to be revealed then the outcome could overlap with other important global factors such as Wednesday’s FOMC communications, other global central bank decisions and global macro releases.

For another, Canada has had 14 minority governments since Confederation that have tended to be relatively short-lived with terms in office between about nine months and up to about three years. The margin of victory for a minority outcome may inform whether the Liberals concede or seize the incumbent advantage of being offered the first chance to strike a coalition on NDP/BQ terms. PM Trudeau’s own political future could hang in the balance if his own party rises up and in the process tosses the Liberals into a leadership race. A Conservative minority could quickly face a confidence vote around a Throne Speech or budget.

Thus, take the stated platforms and what they may mean to markets with a rather large grain of salt and not just because of the common gap between actions and words of politicians. The added uncertainty surrounds how the chess pieces are moved in the immediate aftermath of the vote count. There are simply too many moving parts of the puzzle to make bold statements on what to expect from markets on the back of this election versus monitoring conditions as they evolve. The election aftermath could well be best viewed as best suited to volatility pricing.

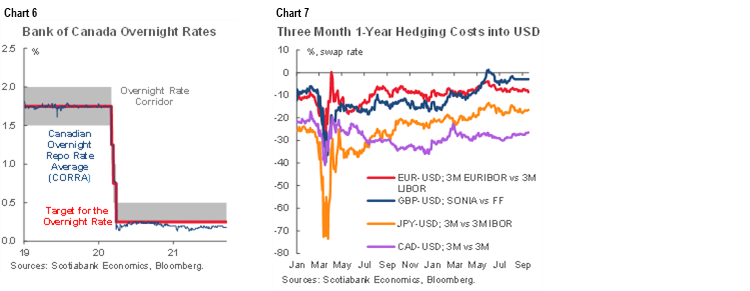

At the end of it all, however, much grander forces than the election will continue to drive the degree of domestic and international appetite for Canadian assets. I’ve never heard a bond PM tell me in modern times that they buy Canadian bonds because they like the net debt to GDP ratio. With an important caveat, the dominant reason to do so in today’s global bond market is to pick up yield net of funding costs relative to other global duration plays and possibly net of currency hedging costs if relevant depending upon the client. Are international investors still getting paid by some of their central banks to borrow money and invest wherever? Yep. Are funding costs—particularly for domestic accounts—to hold Canada bonds attractive such as measures derived from repo markets? Yep, and with market pressures still driving market rates to marginally undershoot the policy rate (chart 6). Swap market funding also enters the picture and FX hedging costs are relatively stable for those international accounts that choose to hedge currency exposures (chart 7).

Besides, let’s face it, little ol’ Canada is about 1–2% +/- of most things that matter in global markets and so there just isn’t that much time spent by global PMs on trying to weave through election implications for local bonds relative to the reward in a global portfolio and the risk of being wrong.

The market effects could be more clearly expressed in terms of sector implications given wide variations across the parties on matters such as pipelines, mortgage market proposals, regulated prices, taxes on bank profits and other considerations such as the Conservatives proposal to sweep away the Liberals’ approach to carbon policies in favour of a carbon tax of $170/tonne only if the EU and US do so first. Here too, however, we would need to see rhetoric turn into policy.

The Bank of Canada

Now as for that caveat. What about the impact on the Bank of Canada and hence shorter-term rates and the currency? That’s going to take a while to inform and set against the base case outlook for spare capacity to shut by 2022H2 before incorporating the victor’s policy platform.

Don’t expect any sudden pivot from the BoC. That’s not how they roll. The BoC generally does not tend to incorporate revised fiscal policy plans until it has seen a budget proposed and passed. The 2019 election was held later (October 21st) and followed by a Fall fiscal update on December 16th. The election is earlier this year and so a Fall budget update could also arrive earlier this time (depending on the aforementioned chess game) before a full budget sometime over Winter and likely in February or March. A bounty of riches to be spent due to faster-than-expected revenue growth could result in an earlier Autumn statement this time. Thus, at the earliest, the BoC may begin to incorporate revised fiscal assumptions in the January 2022 MPR forecasts but more likely in the April 2022 MPR forecasts.

When it gets to that point, what’s the forecast risk to incorporating revised fiscal policy projections into what they mean for estimates of spare capacity? Applying both parties’ platforms could result in a slightly faster rate of closure of the output gap than the base case shown in chart 8 that uses our current forecast for actual GDP growth and the BoC’s July MPR estimates for potential GDP growth. The Conservatives’ platform could be slightly more stimulative in the nearer term, but not by terribly much that would sustainably throw off what’s shown in the chart.

In any event, slightly faster closure of a highly uncertain and malleable variable like the output gap might gradually reinforce a path toward hiking the policy rate and perhaps a touch faster but with appropriate cautions. What cautions against getting too carried away with this is a) the BoC will want to see evidence of the kind of growth forecast incorporated into the projections and with a lot of other more dominant moving parts behind the forecast, b) the estimates of potential growth are hugely uncertain which leaves us more closely monitoring actual wage and price signals, and c) the platforms may not turn into reality not just because of actions versus words but also because of uncertainty around how the chess pieces may evolve toward determining either a majority outcome or a coalition or an independent and fragile minority.

Thus, the honest answer is that we can speak to risks and scenarios around first- and second-round market responses, but I find it would be irresponsible to clients to feign clarity on sudden and sustained market responses to the election and its aftermath. Like ourselves, you’ll just have to monitor the results and see how check mate slowly evolves and assess the attractiveness of volatility pricing. If the players don’t like the way the game’s evolving, then whoopsie daisy, there go the pieces!

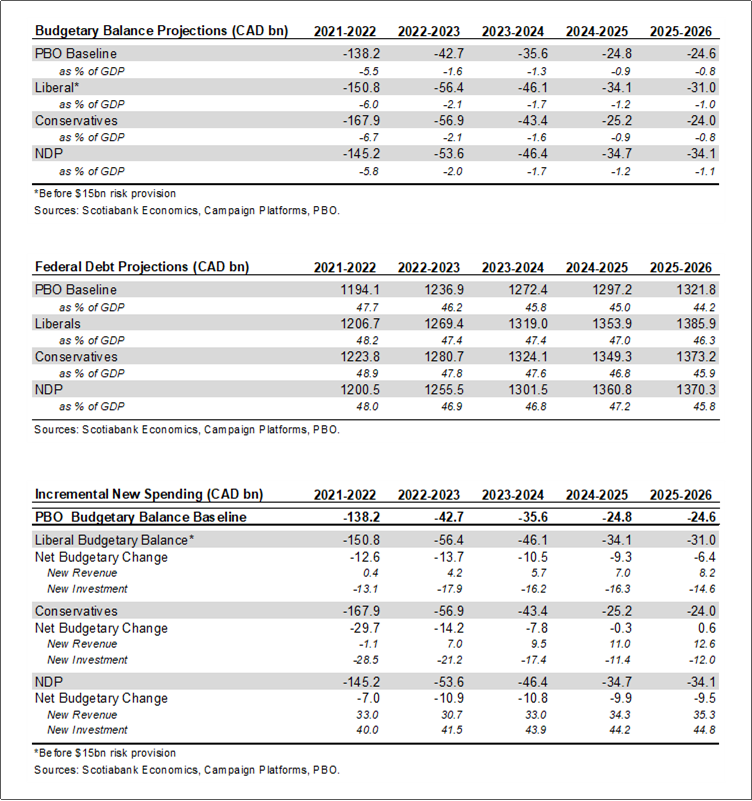

For a fuller perspective see Rebekah Young’s piece here, the summary of fiscal platforms in the accompanying table and also the accompanying appendix that includes a summary table of platform differences that matter to economy watchers and market participants.

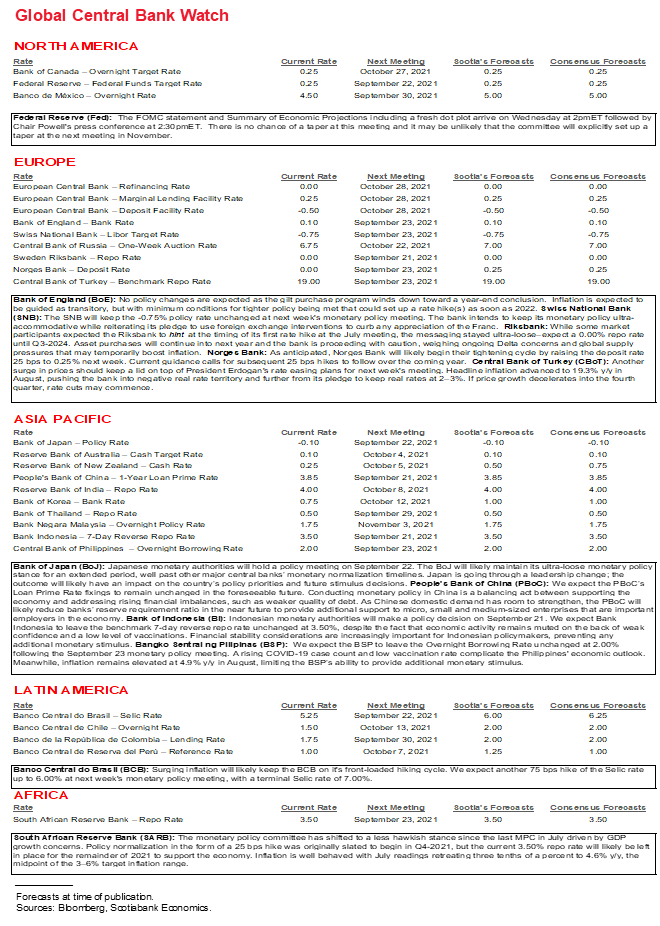

CENTRAL BANKS—THE FED, AND THE REST

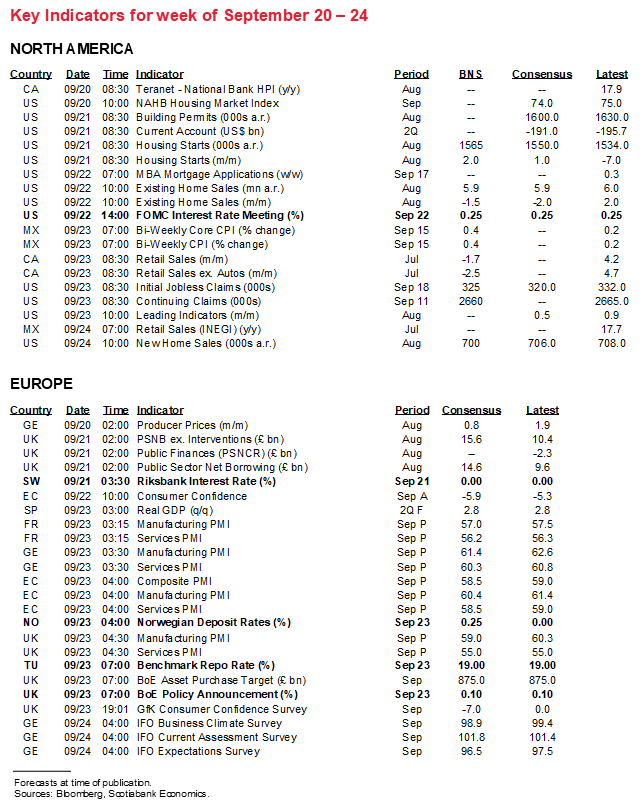

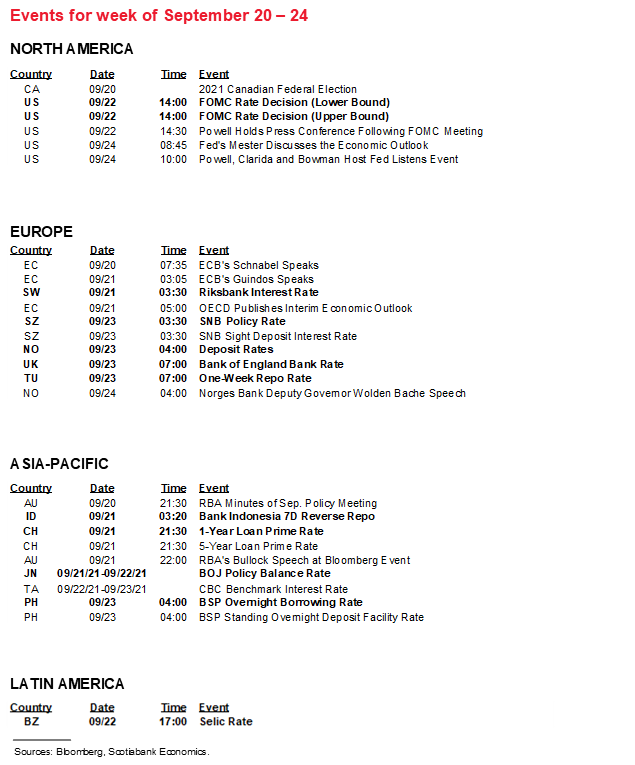

Oh come on! I thought global central bankers spoke with each other! Clearly not, as many of them jammed their policy decisions all at once into this coming week. The one that matters the most is the Fed on Wednesday. A brief rundown follows and with more to follow in morning and intraday notes as the week unfolds.

Federal Reserve—No to September, Conditional Taper Later

A full suite of communications will be delivered on Wednesday at the conclusion of the FOMC’s latest two-day meeting. The statement arrives at 2pmET Wednesday along with a revised Summary of Economic Projections including the latest Rorschach ‘dot’ plot followed by Chair Powell’s presser at 2:30pmET for around an hour or so.

There are four things to watch for. One is taper guidance. Two is any changes to timing rate hikes either in pictures or language. Three is changes to forecasts. Four is critically the soft guidance around whether the Fed has more or less confidence in the evolving macroeconomic picture.

There is 0% chance of a taper at this meeting and we probably won’t see the FOMC explicitly setting up a taper at the next meeting just yet either. The FOMC emphasizes how it will communicate tapering plans well in advance. All that the Fed has indicated so far is that it plans to reduce $120B/mth of Treasury ($80B) and MBS ($40B) purchases “this year.” There are three meetings left in the year including this coming one. When the Fed has chosen to indicate more imminent action it has tended to use some variation of ‘soon’ in its language but has yet to do so. Powell’s speech a few weeks ago could have been used to tee-up September but stopped short (recap here). Instead, Powell acknowledged that he thinks the “substantial further progress” test “has been met for inflation” but not for maximum employment.

Powell also conditioned his guidance by saying “if the economy evolved broadly as anticipated, it could be appropriate to start reducing the pace of asset purchases this year.” The current environment may lend added caution in the wake of a softer-than-expected CPI inflation reading for August, a softer-than-expected nonfarm payrolls gain in August, the rise of the Delta variant that may be starting to settle down, and the ongoing debt ceiling drama.

On the latter matter, the Fed has generally been quiet this time around. This stands somewhat in contrast to 2013 when the debt ceiling and government shutdown issues resulted in holding off on tapering until the December meeting. The sequence of Fed references to the ceiling back then was summarized here. Unlike Chair Bernanke, Chair Powell has not explicitly said he would not add monetary policy risk by tapering if fiscal policy risks became amplified, but it’s getting harder for him to pretend the issue isn’t out there and hope it just goes away. Here is a reminder of what Bernanke said in his July 18th 2013 testimony before the Senate Banking Committee:

"One of the reasons that the economy has been so slow in the early part of 2013 is because of fiscal factors. It's hard to judge how long those factors will last. But if the economy begins to move beyond that point and fiscal restraint becomes somewhat less pronounced then we should see as you said a pick-up in growth. We're obviously going to look at the data, it's a committee decision (on whether to taper QE in September), and it's going to depend on whether we see the improvement which I described." [ed. emphasis added.]

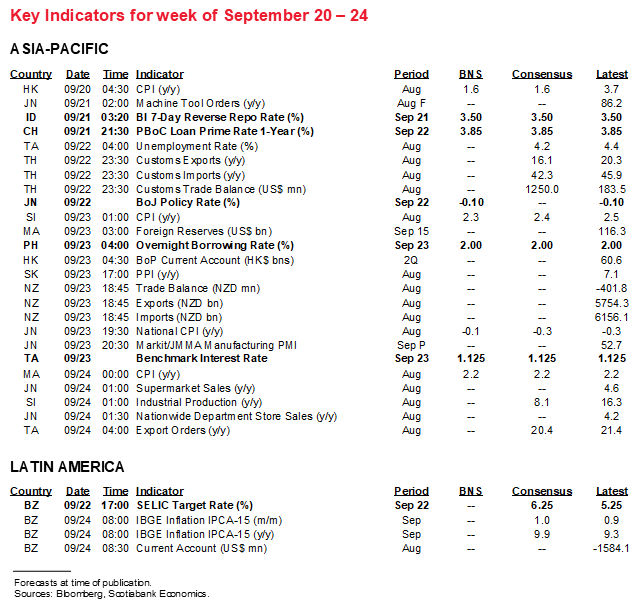

Expectations for the rest of the central banks on tap are briefly recapped below:

- People’s Bank of China (Tuesday): No changes are expected to the one-year (3.85%) and five-year (4.65%) Loan Prime Rates that serve as the de facto policy rates.

- Bank Indonesia (Tuesday): No change is expected to the seven-day reverse repo rate of 3.5%. Not fomenting rupiah instability in the face of Federal Reserve effects on EM risk appetite continues to hang in the air as a policy risk.

- Riksbank (Tuesday): Key here will be whether Sweden’s central bank reacts to the recent spike in the underlying CPI inflation rate for August (2.4% y/y, consensus 1.9%) by altering its forward guidance playbook that to date has guided holding the repo rate unchanged until at least 2024. The central bank may still be stinging from having prematurely tightened in the past and wait to monitor further inflation readings and other developments.

- Brazil (Wednesday): Banco Central do Brasil is widely expected to hike by at least another 100bps on Wednesday. The central bank said in its August statement that it “assumes a path for the Selic rate that rises to 7.0% in 2021, remains at this level during 2022 and drops to 6.5% during 2023.” At 5.25%, there are only three remaining meetings over which to get up to 7% this year in an effort to normalize policy stimulus while seeking to counter inflation risk. Brazil has hiked by 325bps already since March.

- BoJ (Wednesday): No policy changes are expected. Political instability in the wake of PM Yoshihide Suga’s resignation and the gradually improving trend in new COVID-19 cases offer mixed risks to a sidelined central bank.

- CBCT (Thursday): No change is expected to the 1.125% benchmark rate.

- Philippines (Thursday): No change is expected to the 2% overnight borrowing rate.

- Norges Bank (Thursday): Norway is expected to witness its first rate hike since September 2019, after which it slashed its deposit rate to 0% during the pandemic. The August 19th statement stated “it will soon be appropriate to raise the policy rate from today’s level.” This followed guidance in the June Monetary Policy Report (here) that stated “the policy rate will most likely be raised in September.” Watch for revisions to the projected policy rate path that anticipated ending 2024 at 1.5%.

- SNB (Thursday): No change is expected to the -0.75% policy rate. After the ECB’s decision to reduce the pace of bond purchases and thus extend recent weekly tapering, what the central bank guides about the depreciation in the franc will be the thing to watch.

- BoE (Thursday): The BoE is on track to end its bond purchases by the end of this year and is unlikely to adjust this target. The MPC is expected to vote unanimously to hold Bank Rate at 0.1% and 8–1 with Saunders dissenting again in favour of ending purchases earlier. Higher-than-expected recent inflation is likely to be guided as a transitory occurrence with more emphasis placed upon nearer term growth uncertainties on the path toward tightening policy perhaps as soon as next year.

- Turkey (Thursday): No change is expected to the 19% one-week repo rate, but if any central bank tends to surprise with volatile shifts set against a domineering political background then this one is it.

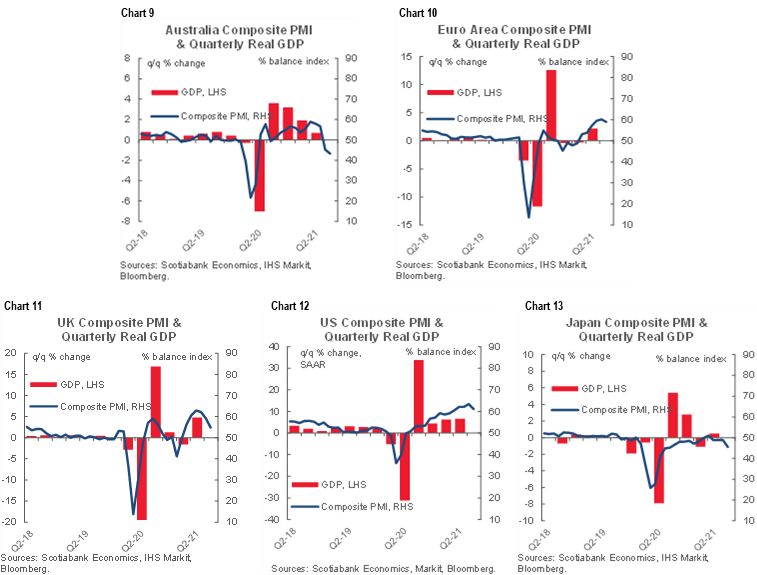

THURSDAY IS PMI DAY!

Global growth momentum will be informed by a heavy round of purchasing managers’ indices for September.

All of them land on Thursday. One might excuse so many central bankers for having too many players on the ice all at once, but Markit has a near monopoly in producing global PMIs and even at that it couldn’t spread them out. The connections to GDP growth are shown in charts 9–13. Australia arrives first on their morning (North American Wednesday evening), and then early in the European morning on Thursday we’ll get the UK, French, German and Eurozone readings followed by the US Markit PMIs into the US morning and lastly Japan’s Jibun PMIs on Friday morning (Thursday evening N.A.).

THE OTHERS

The rest of the global line-up will be fairly light. Highlights will include:

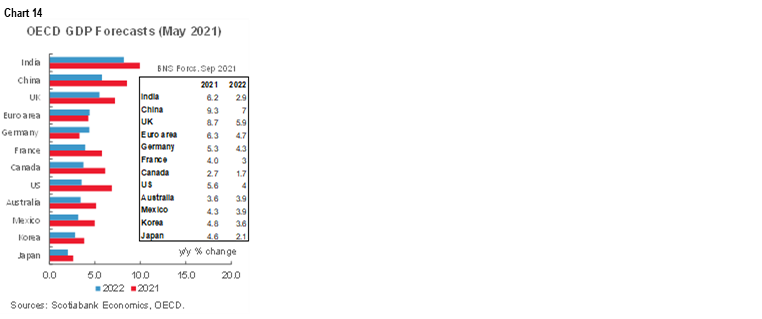

- The OECD updates its global forecasts on Tuesday. Chart 14 compares their last forecast round to our current forecasts to indicate where the refreshed direction of risks may lie.

- Canada updates retail sales for July and provides preliminary guidance for August on Thursday. July’s advance guidance pointed to a 1.7% m/m drop and we tracked a rise in auto sales by contrast to the US. The implication may be that retail sales ex-autos fell by more despite reopening effects, or perhaps because of them since retail sales do not include spending at restaurants, bars, hotels, airlines etc. There may therefore have been a diversion of budgets toward spending categories not reflected in retail sales.

- US releases will be light and focused upon housing. Housing starts for the month of August could post a rebound from the prior month’s sharp drop on Tuesday. Existing home sales are likely to be soft in the wake of recent declines in pending home sales (Wednesday) while new home sales will probably follow prospective home buyers’ foot traffic lower again (Friday).

- Other than Brazil’s central bank decision, Latin American markets will be largely watching from the sidelines with a particular eye on the Fed. Brazil’s mid-month inflation update for September (Friday), Mexican retail sales for July (Friday) and Argentina’s Q2 GDP (Tuesday) are the only releases on tap.

- Japan and Malaysia update CPI for August toward the end of the week. Germany updates IFO business confidence for September on Friday.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.