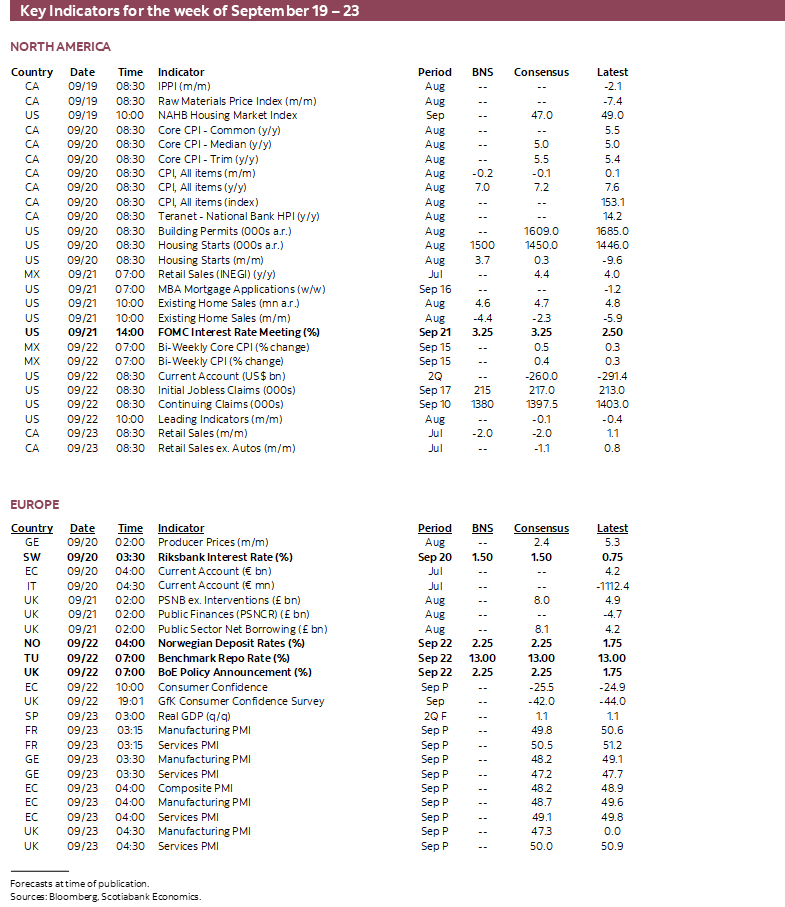

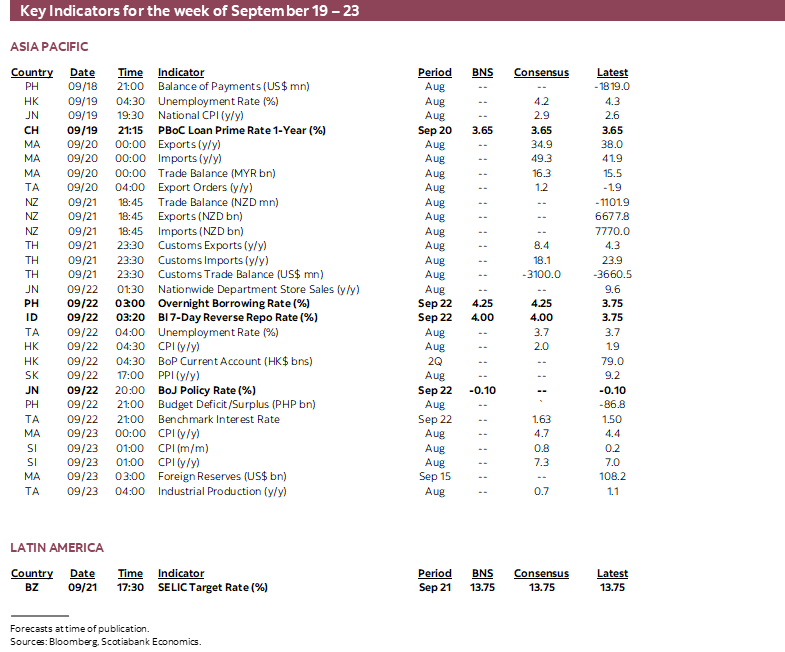

Next Week's Risk Dashboard

- Politics and the drivers and remedies of inflation

- FOMC: hike, dots, forecasts and reserves

- Canadian inflation: picking the right measures

- Bank of England: will it be 50 or 75?

- Global PMIs to inform growth, inflation, supply chains

- PBoC likely to hold

- BoJ will probably stand pat again

- Other CBs: Norges, SNB, Riksbank, SARB, Brazil, BSP, BI, Turkey

- Other macro readings

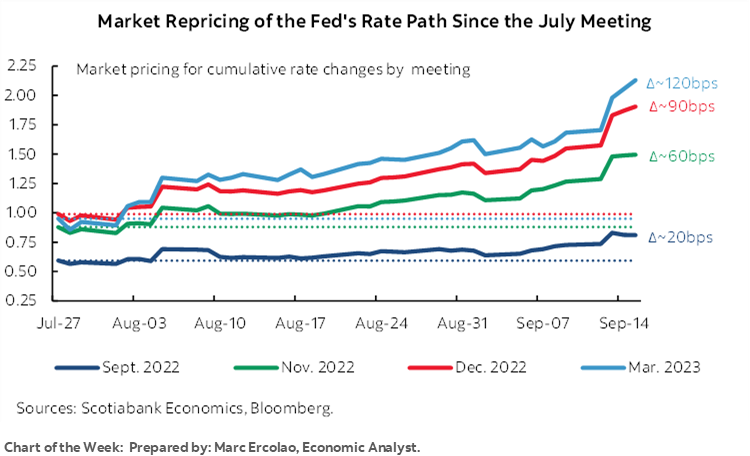

Chart of the Week

What’s driving inflation and who is responsible for it? Like everything else these days, the answer to this question has unfortunately become thoroughly politicized. Which of two main camps one belongs to explains differences in attitudes toward appropriate steps to combat inflation.

One narrative is that inflation is different than ever before because it’s all being imported from abroad through effects upon supply chains, reinforced by the war in Ukraine and driven by greedy corporations. You’ll tend to find this narrative within the elements on the left end of the political spectrum in both the United States and Canada. They argue to modestly varying degrees that there is zero evidence that the demand side drove any of the inflation, that stimulative fiscal and monetary policy played no role and that it’s unfair to argue that the response to stimulus by households drove prices higher in housing and consumption markets.

As an extension to their argument, they think that because stimulus didn’t drive any of this inflation and domestic consumers played no role, fiscal policy should therefore step into this imported price shock and distribute aid to help households with the cost of living because yet again they don’t believe that doing so will play any role in driving inflation because it didn’t in the first place. Because inflation is a highly regressive tax, they emphasize the need to focus aid upon lower- and middle-income households. Some even go so far as to say orthodox economic policy is making a mistake by tightening monetary policy.

This is the core narrative that leading politicians have advanced in saying that successive rounds of fiscal stimulus are not contributing to inflation and there still won’t be any impact upon inflation from stimulus efforts. This line of reasoning was used this past week as justification for the Canadian government’s decision to distribute another almost $5 billion of stimulus cheques before year-end. Don’t worry, it’s just to help folks, they won’t spend it and they won’t impact prices.

Now I think most folks who follow these things closely and especially more markets-oriented folks like readers of notes like this probably get that this is economic heresy in defiance of the facts. It smacks of vainglorious attempts at excusing policymakers for having caused much of this inflation.

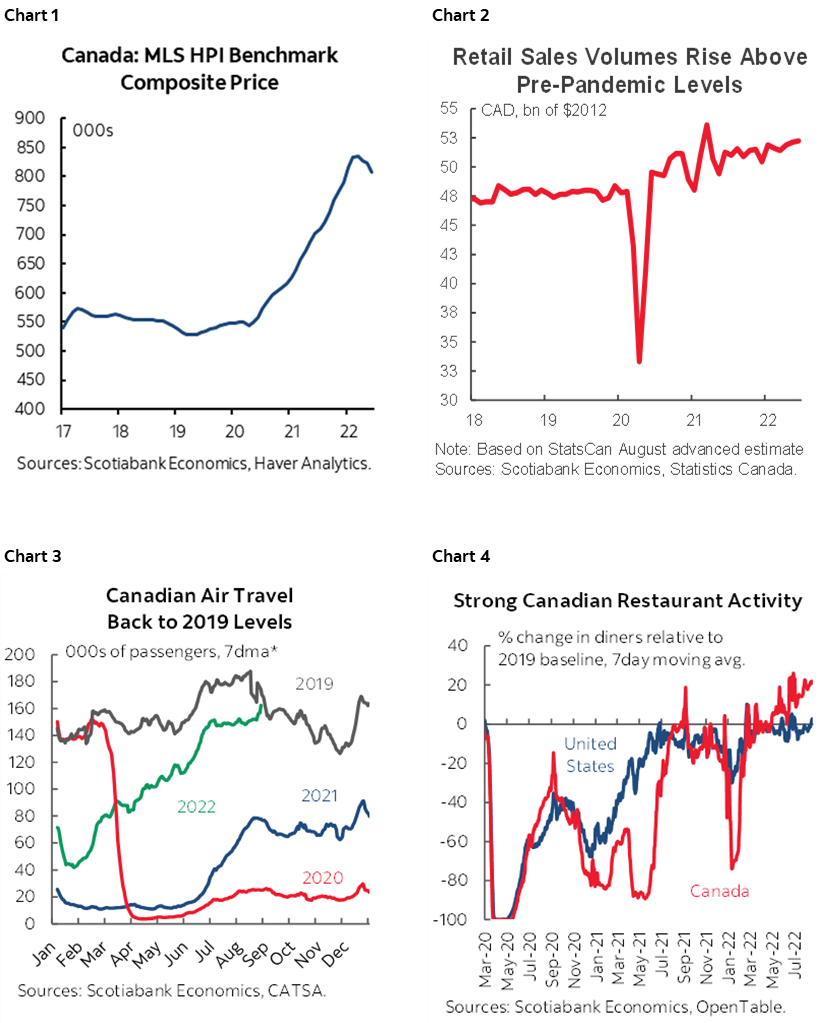

After all, we know that the demand side was lit up by stimulus and hence it hasn’t all been about just the impaired supply side. Econ 101 says that if you light up a torrent of demand then more spending chasing goods and services can light up prices. We see that in record housing activity. Housing has been overwhelmingly driven by domestic buyers responding to too-low-for-too-long interest rates and by heavy fiscal stimulus transfers. It was made unaffordable to lower- and middle-income households by such policies (chart 1) and yet instead of admitting that, governments have opted to point the finger at foreign buyers and tax them. Retail sales also soared to all-time record highs (chart 2). Restaurants have been packed (chart 3) and airplanes are full (chart 4). It’s even wrong for some to dismiss gasoline and food prices as exclusively driven by supply side issues since a recovery in mobility, miles driven, eating out and appetite for a wide variety of basic to higher-end groceries have been demand-side drivers.

If the story is more balanced between supply and demand drivers than some think and if stimulus played a heavy role in driving demand higher, then it’s logical to assume that the serial application of ongoing fiscal stimulus is likely to drive more spending and be unhelpful to the fight against inflation. Another $5 billion in government cheques was deliberately timed to hit accounts into the holiday shopping season which means it was meant to be spent. It is equal to about 8% of monthly retail sales, through the likely impact will be more spread out than across just one month and will also spill into services like spending at restaurants and bars. If the aim was not to stimulate the economy in order to put up strong numbers until the next Winter budget, then perhaps the amount could have been paid out in February—after holiday shopping, to pay down credit card bills, and with a couple of feet of snow on the ground across much of the country.

With that, the week ahead beckons, and with it more focus upon inflation figures and what a slew of central banks are doing about it.

CANADIAN INFLATION—FUN WITH NUMBERS

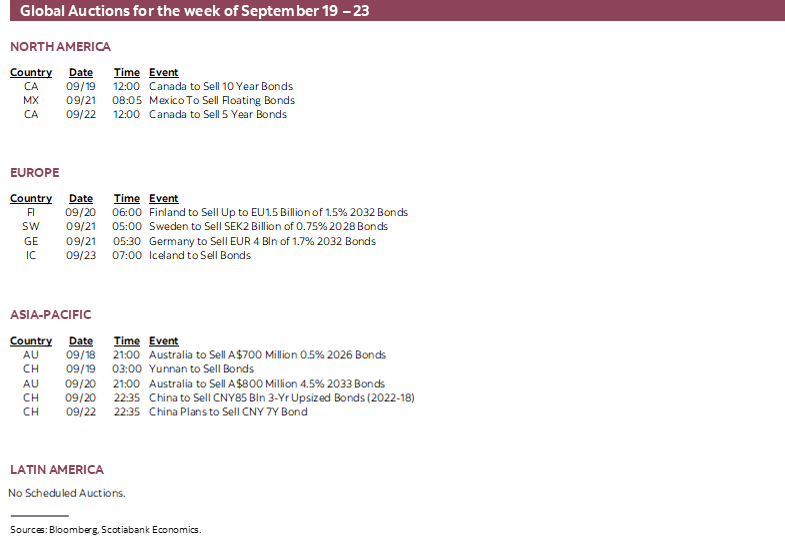

Inflation has been so much fun to markets of late—why not give it another whirl, right? We’ll see when Canada updates CPI for the month of August on Tuesday.

I’ve estimated a -0.2% m/m drop in seasonally unadjusted headline CPI that translates into a flat m/m seasonally adjusted reading. That should be enough to bring the year-over-year rate down to 7.0% y/y. That would continue the deceleration from a peak rate of 8.1% y/y in June.

There are a few reasons to be cautious about interpreting this as evidence that inflation is coming off the boil:

- First, the year-over-year rate would be expected to decelerate to 7.4% from 7.6% the prior month solely due to changing year-ago base effects (ie: the impact of resetting the year-ago comparison month to the next month’s price index). Forward looking monetary policy shouldn’t be affected by year-ago price changes, as crazy as that sounds in relation to a lot of the talk on inflation these days!

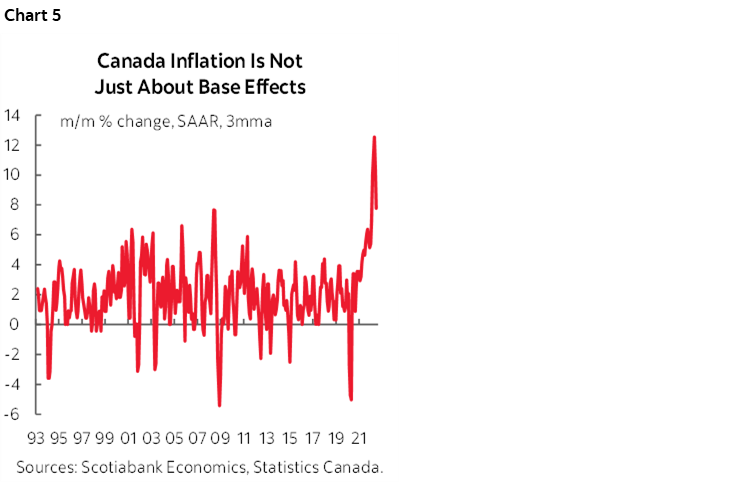

- Secondly, and as an extension of the prior point, we need to look at measures that are not influenced by year-ago base effects like m/m seasonally adjusted and annualized changes in measures of inflation including headline CPI (chart 5) but also traditional measures of core CPI that just remove food and energy and that have remained hot.

- Third, August is usually a light month for seasonality in CPI which matters because economists are polled for seasonally unadjusted prices. I’ve assumed a mild -0.1% m/m NSA drag on prices from seasonal influences. Judgement on inflationary pressures should not rest upon a measure that is typically light at this time of year.

- Fourth, the softness is expected to be almost all about gasoline prices. They fell by nearly 9% m/m in seasonally unadjusted terms which would be enough to drag 0.4 percentage points off m/m CPI. If that’s the main source of weaker prices while the rest of the CPI basket stays hot, then it will be dismissed.

- Fifth, it’s also likely that declining natural gas prices will subtract from the month-over-month change in CPI given the decline in the Alberta hub benchmark that has fallen since June but with the caveat that it is firming so far through September. If forecasts for a threepeat la Nina effect come true, then global natural gas prices could drift higher through winter especially given spillover effects of Europe’s deepening challenges.

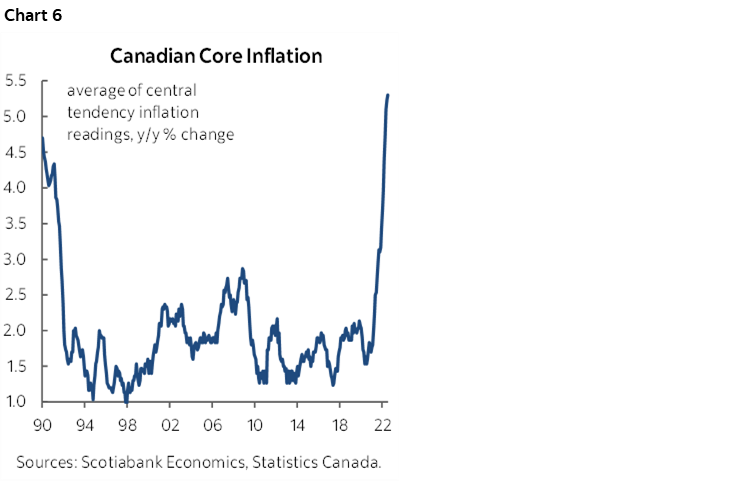

All that means that the focus has to be upon other drivers of inflation in order for CPI to matter. I’ve already mentioned one of them above (simple core inflation annualized). That turns our attention to the BoC’s central tendency measures including weighted median CPI, trimmed mean CPI and common component CPI, plus other gauges of core inflation. The average of these measures has continued to increase even as headline CPI has ebbed in year-over-year terms and may be vulnerable to another spike in August’s numbers (chart 6). Why?

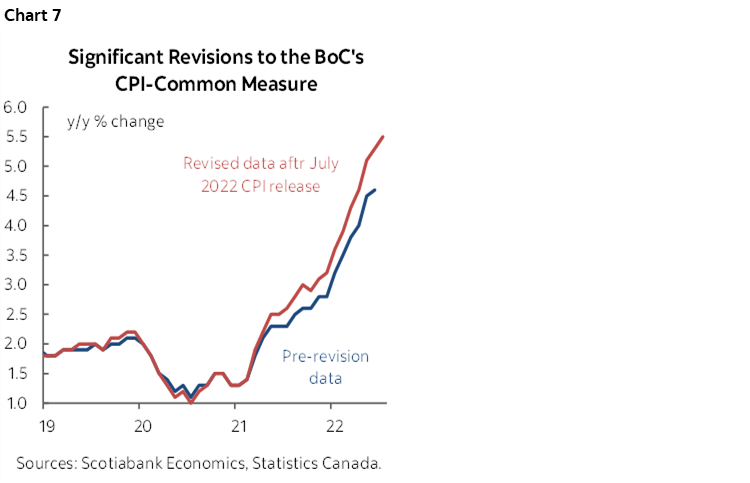

Common component CPI is determined by a factor-driven model that keeps getting subjected to upward revisions with each release over the past year (chart 7). That could be because it is influenced by the mean and variability of headline CPI and so the model is constantly updated with each new release. I’m still not sure of the value of a measure of inflation that gets revised each time new headline inflation estimates arrive.

Also recall that trimmed-mean CPI and weighted median CPI as reported are not influenced by year-ago spot base effects like headline CPI is. That’s because of the way they are calculated by using month-over-month price changes on a rolling 12-month basis as inputs into the calculations. Therefore, these measures won’t swing around as much as year-over-year spot price changes evolve and won’t be under a downward drift like headline CPI.

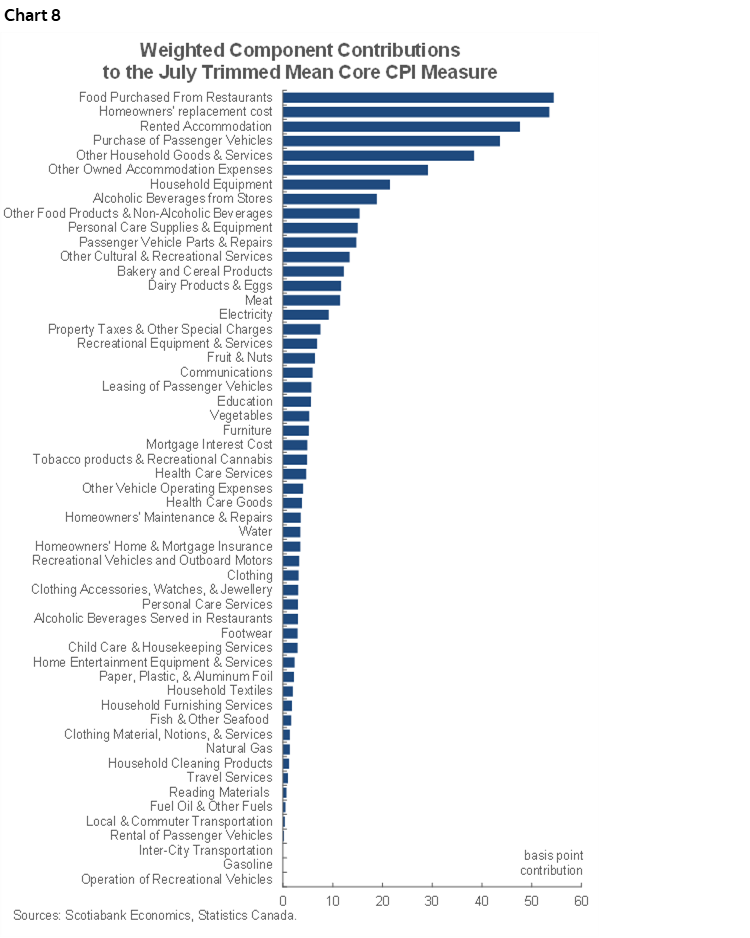

Several of the core drivers of these measures likely remain under upward pressure. Chart 8 shows the weighted contributions to trimmed mean CPI by our calculations. The top categories that are contributing the most to this measure of inflation are not ones like gasoline or natural gas prices but are much more widespread.

FEDERAL RESERVE—OF DOTS AND RESERVES

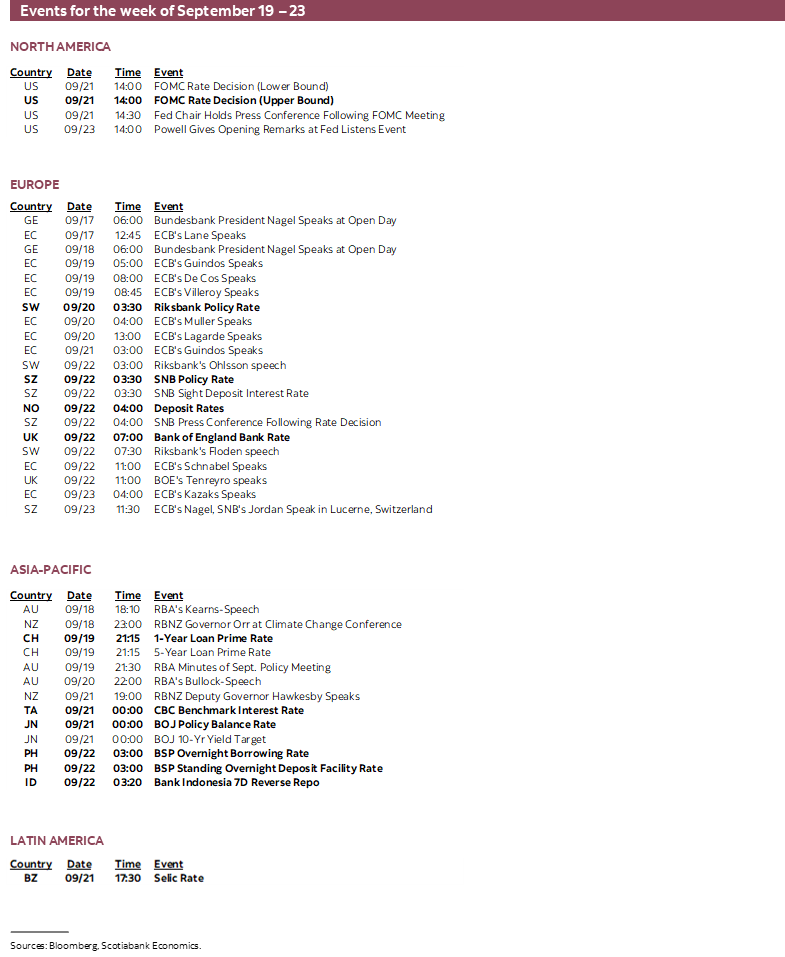

A full suite of communications will be delivered at the conclusion of the FOMC’s two-day meeting that starts on Tuesday and culminates in the delivery of the policy statement and Summary of Economic Projections including the ‘dot plot’ of policy rate projections (2pmET) followed by Chair Powell’s press conference. JayPow will speak again on Friday.

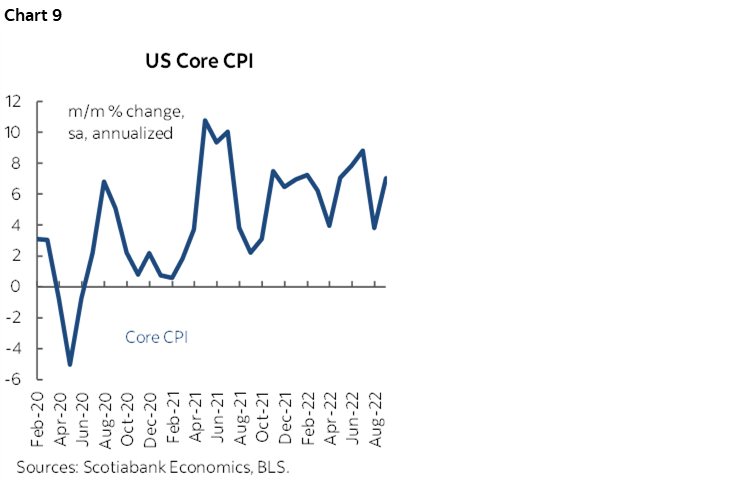

Scotia Economics expects a hike of 75bps this week that would lift the fed funds target range to 3.0 – 3.25%. Markets are already priced for this move. There is likely a high bar for a larger move of 100bps that the FOMC has thus far resisted out of concern that it could be too abruptly destabilizing to markets. There is probably also a high bar set against undershooting 75bps with a hike of only 50bps in the wake of strong core CPI inflation (chart 9) that rocked markets this past week. Undershooting with a half-point hike could perversely ease financial conditions unless it is accompanied by more hawkish forward rate guidance than markets are already pricing, in which case: why not just deliver a bigger hike now? The FOMC probably doesn’t want to see financial conditions ease.

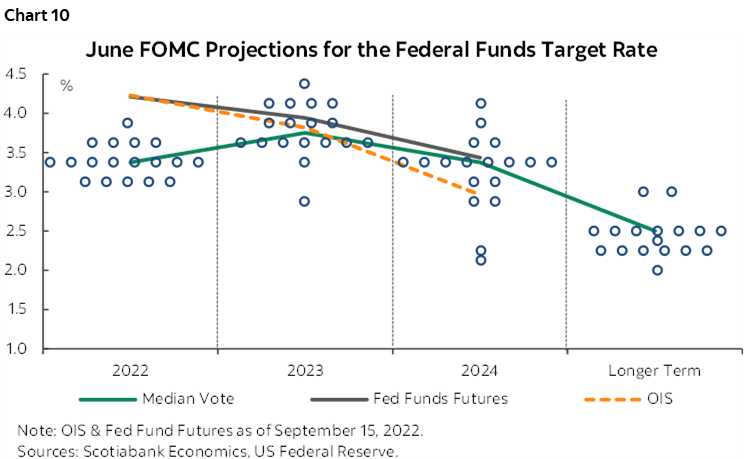

On forward guidance, I’m expecting the median FOMC participant to raise the not-forecast forecast fed funds rate range from 3.25–3.5% to over 4% this year and to keep it at this peak through 2023. The addition of 2025 to the forecasts adds a new wrinkle in that how quickly the FOMC sees coming off an overshoot of its estimated neutral rate range over 2024–25 may inform easing bets. Markets are onside in the near-term but less so later on (chart 10). The dots are also unlikely to guide that there may be rate cuts next year, whereas markets are priced for the return of policy easing later in the year. It’s unlikely that the FOMC wishes to signal plans to ease when it has yet to get inflation under control. It’s also unlikely that sending an easing signal that aids financial conditions would be compatible with the goal of bringing inflation under control at this point.

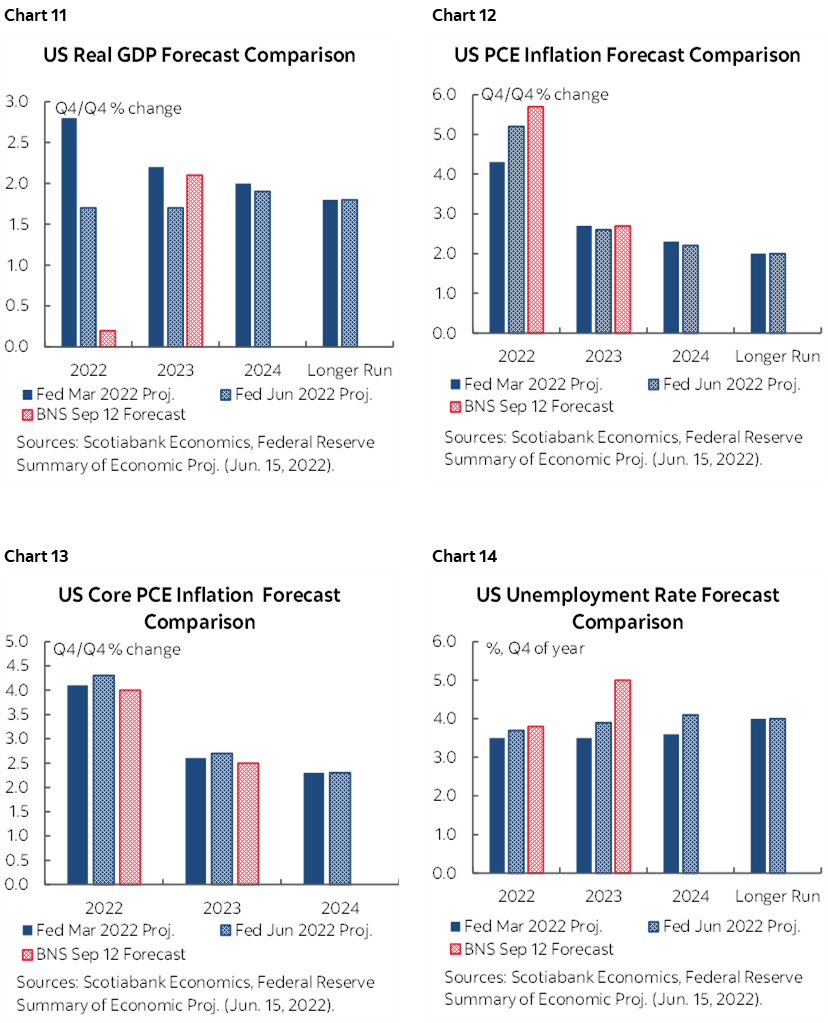

There will have to be material forecast changes at this meeting. The FOMC’s median projection for growth this year is too high but our own growth forecast for next year may be higher than their comfort zone (chart 11). The FOMC also has to raise inflation forecasts for this year at a minimum (chart 12) but we feel they may not face a major adjustment to core PCE inflation projections (chart 13). We will also watch for likely upward adjustment in the unemployment rate projection into next year (chart 14) which would contribute to informing the Fed’s current beliefs around recession risk and the durability of strong employment gains.

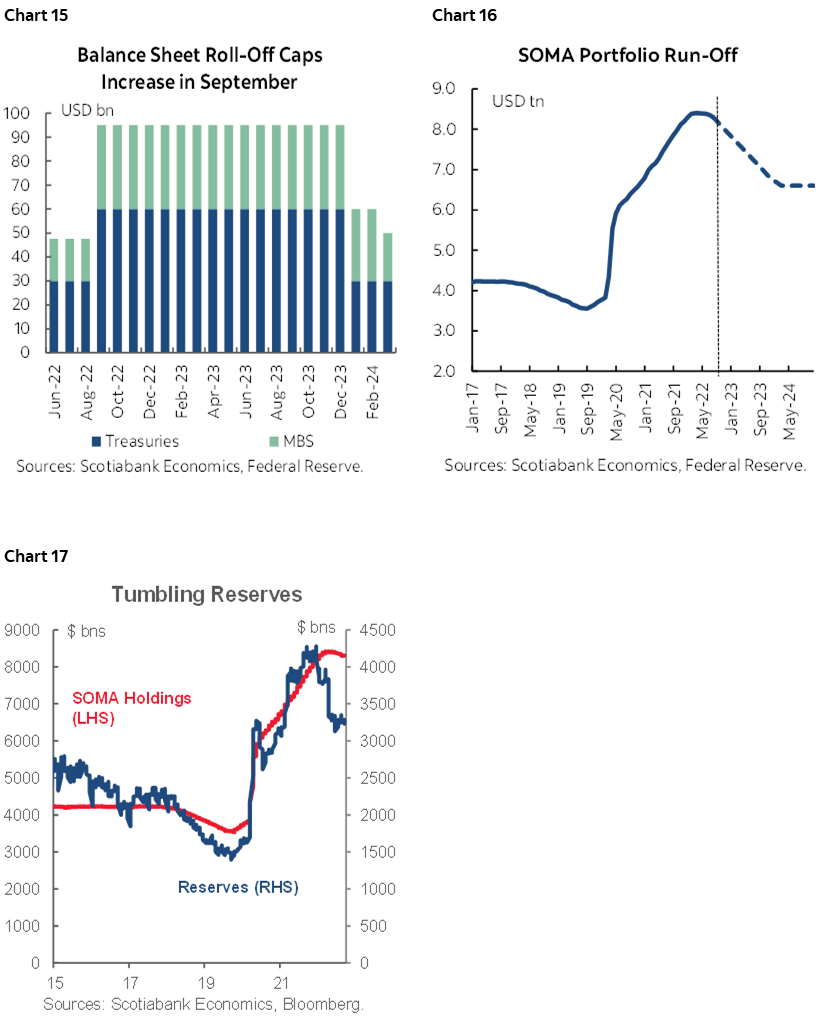

Balance sheet policies are assumed to remain intact. The Fed’s peak rate of roll-off of maturing holdings of Treasuries and MBS has been hit starting this month at a $90B/mth rate split between $60B per month of Treasuries and $35B/mth of MBS. We think that peak rate of roll-off will persist until early 2024, at which point it will be tapered and transition toward flat-lining holdings (charts 15, 16). That may be somewhat sooner than FOMC officials currently believe. This action is draining reserves from the banking system at a relatively rapid pace (chart 17). Powell recently indicated no appetite for inducing a world of scarce reserves and this may have intimated that as the Fed approaches the New York Federal Reserve’s estimated US$2–2½ trillion definition of ample reserves, it may pivot away from Quantitative Tightening (QT). It’s probably premature to expect material discussion around this issue in the press conference, but markets are likely to be on closer watch for further information over coming meetings since the speed with which reserves are unwound within the system could affect financial market functioning and appetite for risk.

GLOBAL CENTRAL BANKS—MERCY!

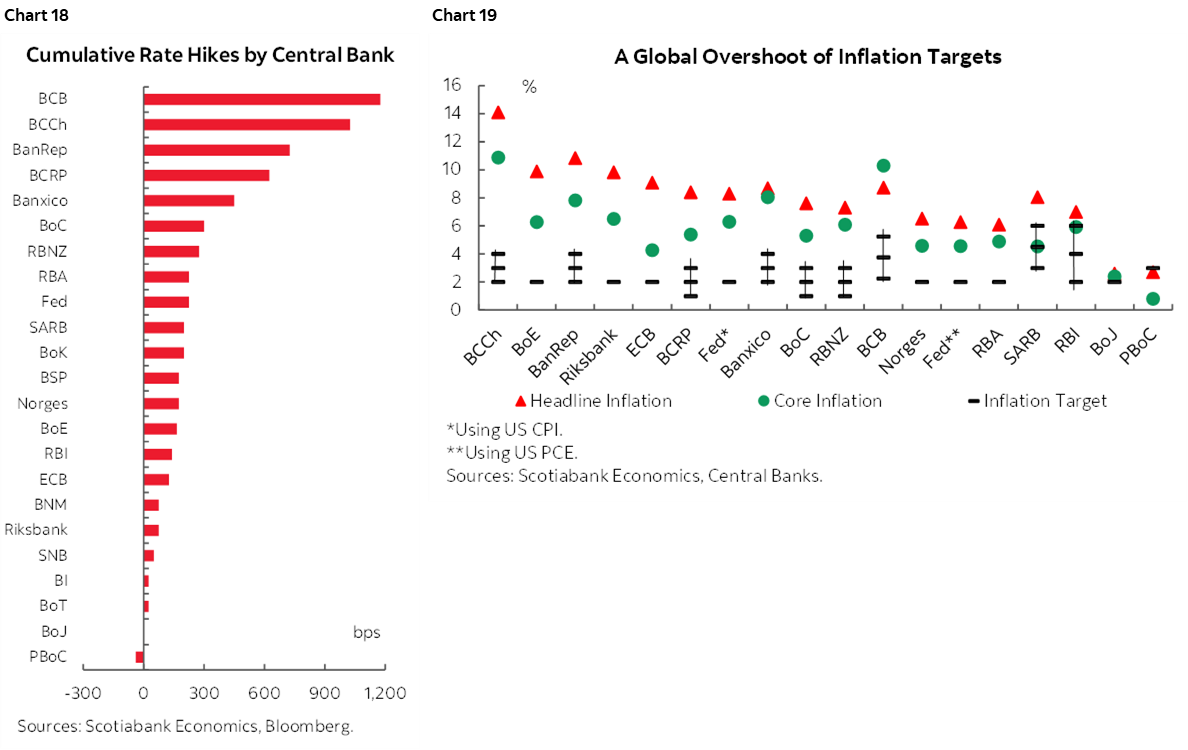

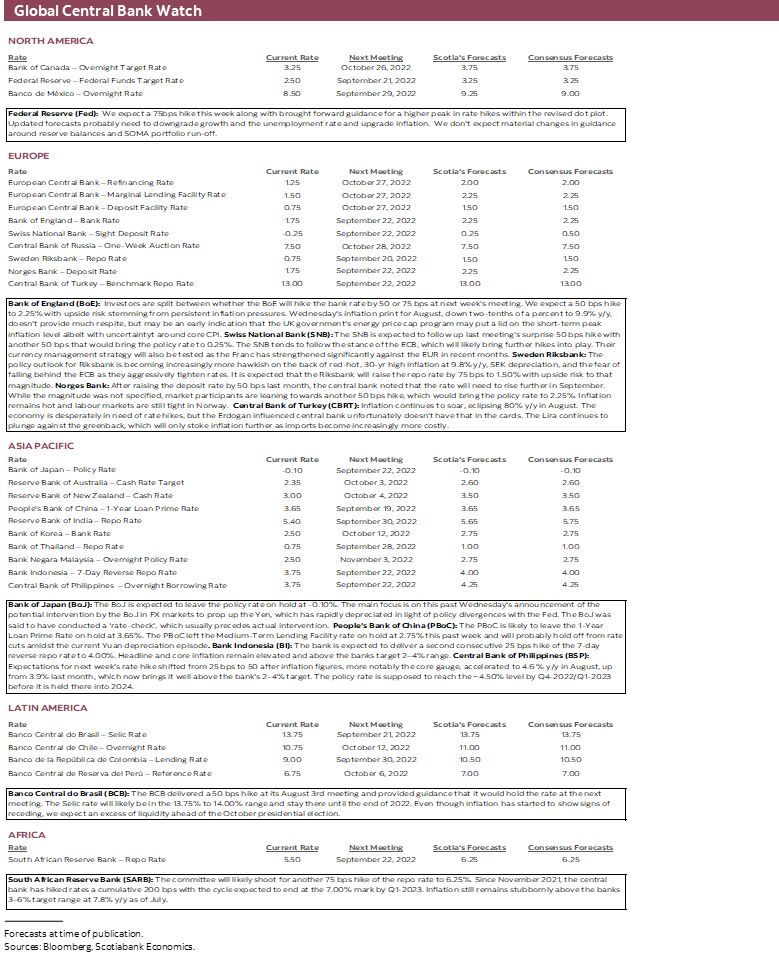

I sure hope you love hearing your local central bankers jawbone plans to counter inflation by raising borrowing costs. Otherwise, I’m afraid it may be a rather long week for all as a deluge of global central bank decisions lies ahead. Most will be weighing in after the Federal Reserve with decisions concentrated toward the end of the week. Please see the highlights below in chronological order and with Marc Ercolao’s assistance. More to come over the week’s publications and chart 18 ranks the cumulative rate hikes to date by central bank. Chart 19 shows where each central bank stands on inflation relative to its target.

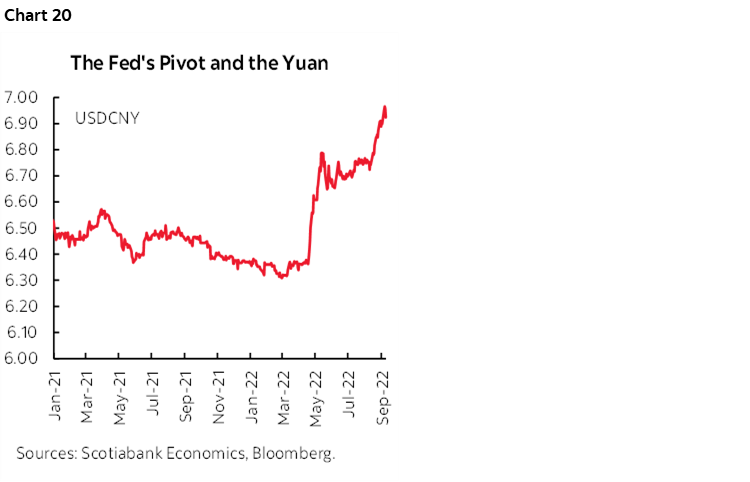

- People's Bank of China (Monday): The PBoC is likely to leave its 1-year and 5-year Loan Prime Rates on hold at 3.65% and 4.3% respectively. The PBoC left the Medium-Term Lending Facility rate on hold at 2.75% this past week and will probably hold off from rate cuts as it strives to manage the yuan’s slide (chart 20).

- Sweden’s Riksbank (Tuesday): The policy outlook for Riksbank is becoming increasingly more hawkish on the back of red-hot, 30-yr high inflation at 9.8% y/y, SEK depreciation, and the fear of falling behind the ECB as they aggressively tighten rates. It is expected that the Riksbank will raise the repo rate by 75 bps to 1.50% with upside risk to that magnitude.

- Banco Central do Brasil (Wednesday): The BCB delivered a 50 bps hike at its August 3rd meeting and provided guidance that it would hold the rate at the next meeting. A minority still think that it may deliver a small hike perhaps informed by the past week’s more aggressive pricing of the Fed funds rate path. The Selic rate will likely be in the 13.75% to 14.00% range and stay there until the end of 2022. Even though inflation has started to show signs of receding, we expect an excess of liquidity ahead of the October presidential election.

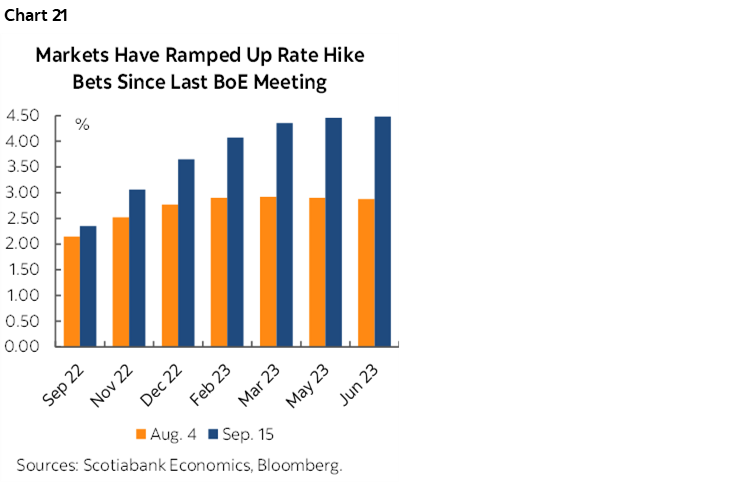

- Bank of England (Thursday): Economists are split on whether the BoE will hike the bank rate by 50 or 75 bps at next week's meeting with markets priced by 75bps (chart 21). Wednesday's inflation print for August, down two-tenths of a percent to 9.9% y/y, doesn't provide much respite, but may be an early indication that the UK government's energy price cap program may put a lid on the short-term peak inflation level while the outlook for core inflation may have been perversely raised by this effort.

- Swiss National Bank (Thursday): The SNB is expected to follow up last meeting's surprise 50 bps hike with another 50–75 bps hike that would bring the policy rate to 0.25%–0.5%. The SNB tends to follow the stance of the ECB, which will likely bring further hikes into play. Their currency management strategy will also be tested as the Franc has strengthened significantly against the EUR in recent months.

- Norges Bank (Thursday): After raising the deposit rate by 50 bps last month, the central bank noted that the rate will need to rise further in September. While the magnitude was not specified, market participants are leaning towards another 50 bps hike partly informed by the forward rate path published in the June Monetary Policy Report, which would bring the policy rate to 2.25%. Inflation remains hot and labour markets are still tight in Norway. Refreshed guidance on the forward rate path will be closely monitored with this week’s updated Monetary Policy Report.

- Central Bank of Turkey (Thursday): Inflation continues to soar, eclipsing 80% y/y in August. The economy is desperately in need of rate hikes, but the Erdogan-run central bank doesn't have that in the cards, unfortunately. The Lira continues to plunge against the greenback, which will only stoke inflation further as imports become increasingly more costly.

- Bank of Japan (Thursday): The BoJ is expected to leave the policy rate on hold at -0.10%. The main focus is on this past Wednesday's announcement of the potential intervention by the BoJ in FX markets to prop up the Yen, which has rapidly depreciated in light of policy divergences with the Fed. The BoJ was said to have conducted a 'rate-check', which can precede actual intervention although bond buying actions sent a mixed signal. The BoJ is likely to look through the implications of a weaker yen because it would be viewed as only delivering transitory progress toward the elusive inflation goal. On that note, Monday’s CPI update is likely to continue to accelerated toward 3% y/y with CPI ex-fresh food and energy at a more subdued pace of half that rate.

- Bank Indonesia (Thursday): BI is expected to deliver a second consecutive 25 bps hike of the 7-day reverse repo rate to 4.00%. Headline and core inflation remain elevated and above the banks target 2–4% range.

- Central Bank of Philippines (Thursday): Expectations for next week's BSP rate hike shifted from 25 bps to 50 after inflation figures, more notably the core gauge, accelerated to 4.6 % y/y in August, up from 3.9% last month, which now brings it well above the bank's 2–4% target. The policy rate is supposed to reach the ~4.50% level by Q4-2022/Q1-2023 before it is held there into 2024.

- South African Reserve Bank (Thursday): The committee will likely shoot for another 75 bps hike of the repo rate to 6.25%. Since November 2021, the central bank has hiked rates a cumulative 200 bps with the cycle expected to end at the 7.00% mark by Q1-2023. Inflation remains stubbornly above the banks 3–6% target range at 7.8% y/y as of July.

In addition, there will be a significant line-up of ECB speakers over the week including President Lagarde, Schnabel, Muller, Kazaks, Lane, De Cos, Villeroy, Guindos and Nagel, although the next ECB meeting is a long way off on October 27th. RBA minutes arrive on Monday and then Deputy Governor Bullock will speak the next day.

OTHER MACRO—PMIs IN FOCUS

Much of the rest of the week’s focus will be upon a select few global economic indicators.

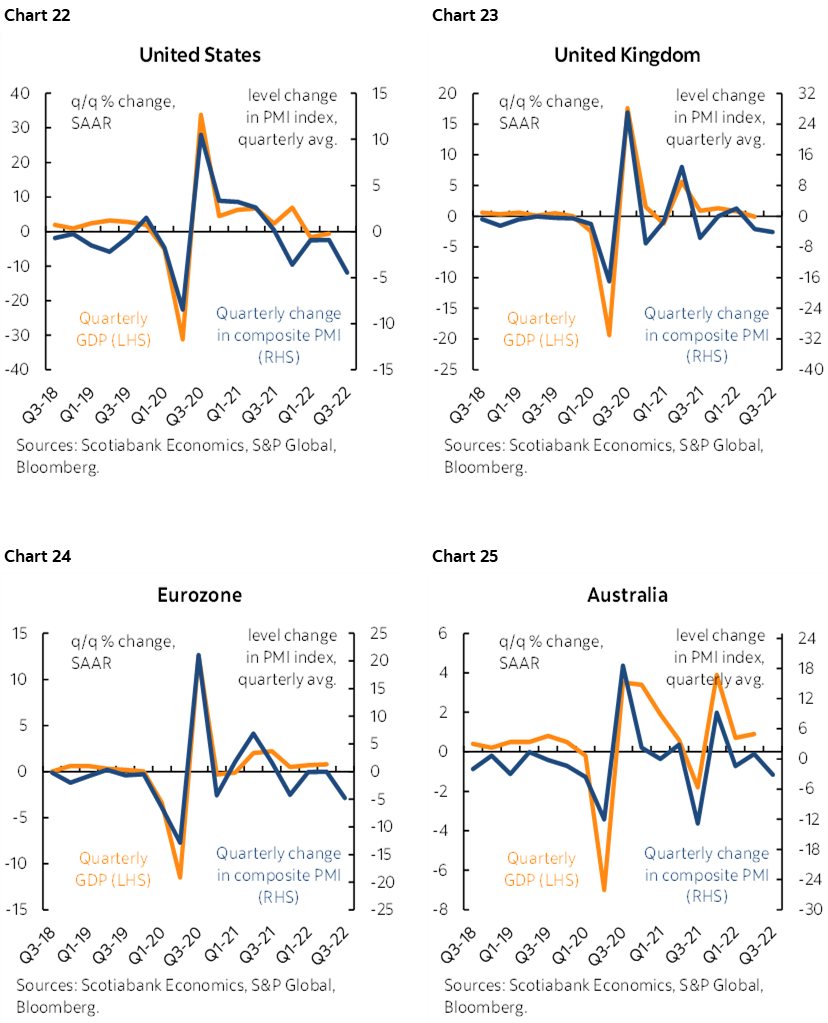

At the top of the list will be the monthly parade of global purchasing managers’ indices that inform everything from current quarter growth tracking to momentum across order books and inflationary signals. They all arrive toward the end of the week and charts 22–25 depict the trends in changes across the PMIs and GDP growth for the UK, Eurozone, US and Australia. Note that the US gauge is not the Fed’s preferred ISM metrics that more closely track activity in just the domestic US economy.

Canada updates retail sales for July on Friday but we already have advance guidance that prepares us for a weak number around -2% m/m. Since that’s a nominal estimate, controlling for inflation will probably mean that the volume of sales fell by more. Bear in mind that this summer saw a rotation of demand toward services relative to goods consumption and that services are not well captured in retail sales. Therefore, retail sales cannot be solely relied upon as a measure of strength in consumer spending.

US releases will be light and keep the focus upon the Fed. We only get housing starts (Tuesday) and existing home sales (Wednesday) for the month of August and will be watching for whether initial jobless claims retain their trend improvement on Thursday.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.