Next Week's Risk Dashboard

- Central bankers return in droves

- FOMC to deliver a hawkish pass

- BoE to hike as inflation, wages remain hot

- BoJ to stand pat

- Chinese banks unlikely to cut lending rates

- Canadian CPI to inch closer to BoC’s next decision

- BoC communications will probably be low risk

- PMIs: EZ, UK, Japan, Australia, US (not ISMs)

- UK core CPI isn’t cooling yet

- Norges Bank to hike, because they said so!

- Riksbank to reach terminal rate?

- SNB to hike

- Brazil’s central bank will cut again

- Turkey’s central bank can’t stop the lira’s plunge

- BSP could resume tightening

- BI, CBCT, SARB to hold

- Global macro readings

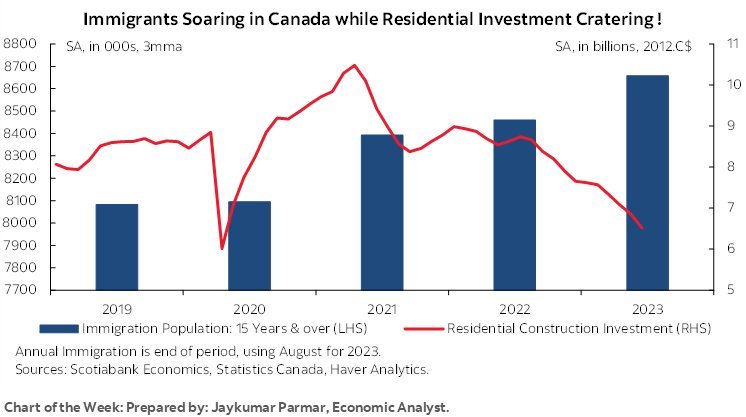

Chart of the Week

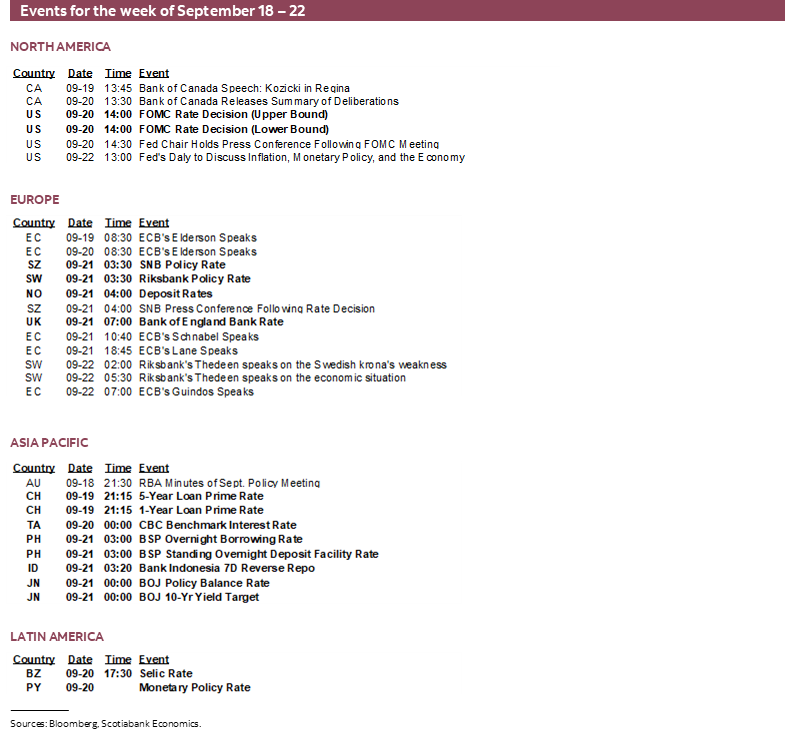

Global central bankers are back in full swing after working on their golf handicaps and raring to go with a heavy line-up of decisions and guidance that dominates calendar-based risk. Several gems are also on the docket by way of economic indicators. Off-calendar risk will track the UAW strike in the US economy, and progress toward hopefully averting a US government shutdown toward month-end.

GLOBAL CENTRAL BANKS—MONEPALOOZA

A tidal wave of global central bank decisions and communications arrives over the coming week. I’ll focus upon the major ones and provide brief highlights for the rest.

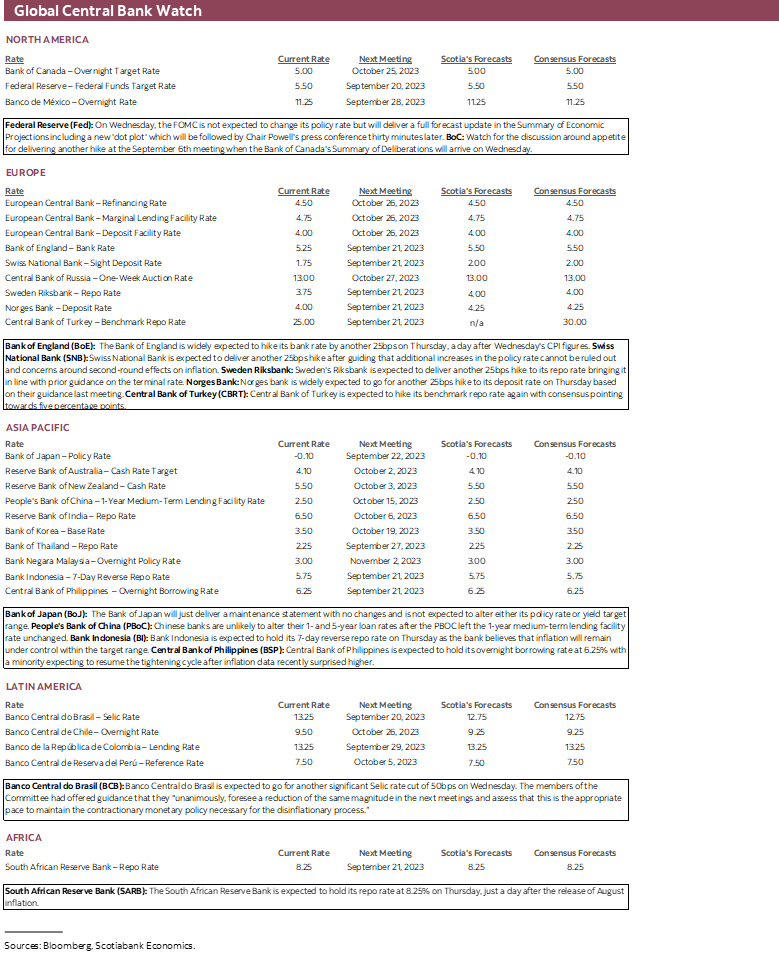

Federal Reserve—Because They Have To

On Wednesday, the FOMC will deliver a fresh policy decision at 2pmET accompanied by a statement and full forecast update in the Summary of Economic Projections including a new ‘dot plot.’ Chair Powell will follow with his press conference thirty minutes later.

No one really expects a change in the policy rate or balance sheet guidance at this meeting. Instead, it will focus upon tweaks to forward guidance on the policy rate, updated macroeconomic projections and guidance that Powell provides. This one is likely to be about buying time.

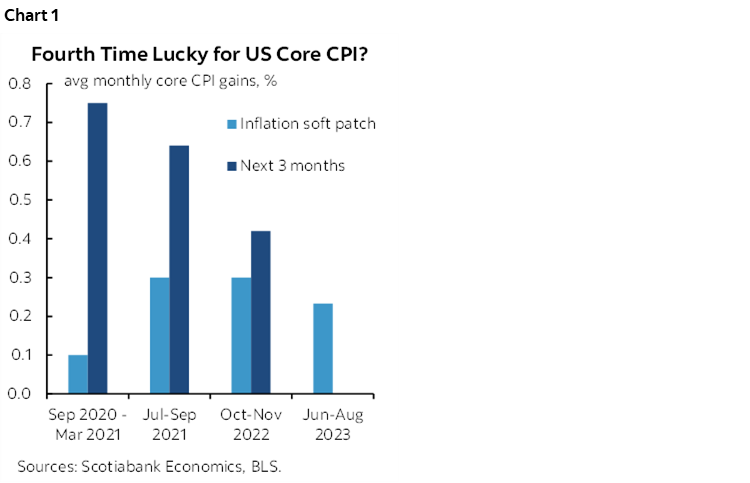

It’s possible that the FOMC leaves intact guidance that favours one more hike in this year’s dot plot which would carry over the residual hike that is still showing in the June dot plot. One reason for this is because the FOMC is likely fully aware of the fact that there have been three prior inflation soft patches during the pandemic that were subsequently followed by a reacceleration of inflationary pressures (chart 1). Another reason is to manage markets because the minute the FOMC signals conviction that hikes are definitely done is when traders with their itchy fingers pounce on the front-end and start pricing amplified easing bets. Now is likely too soon for the FOMC to consider such a move.

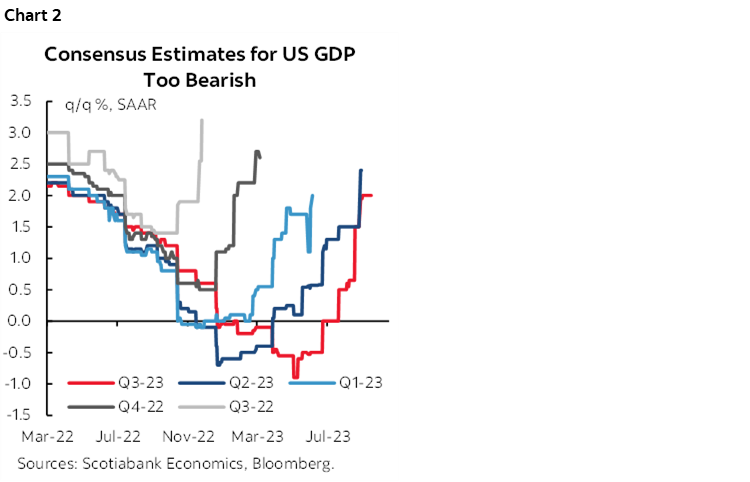

Why no change at this meeting though? After all, GDP growth is outpacing expectations and driving upward revisions to forecasts for the fifth straight quarter (chart 2). The FOMC, however, does not target GDP growth. It focuses upon its dual mandate of price stability and full employment and the connections to GDP growth can be tenuous at best.

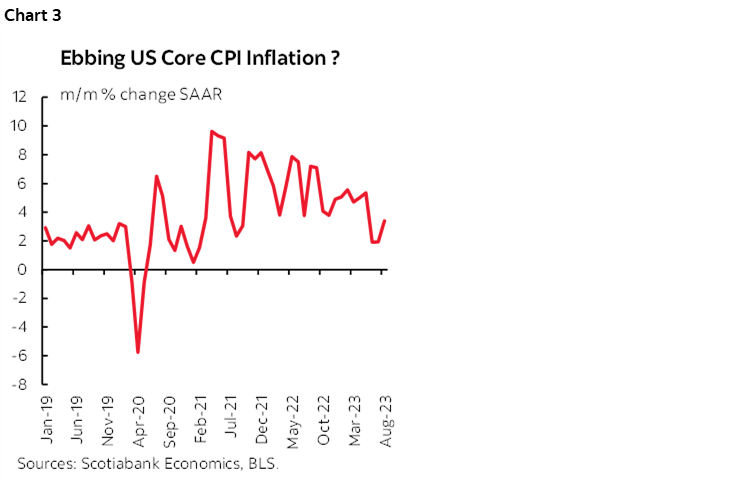

On that note, job growth is still decent, but cooler with the 3mo MA at only 150k and the unemployment rate is up a bit. That’s a far cry from the earlier pace of increases. Trend core CPI has softened over the past several months and so has core PCE (chart 3). This soft patch provides an opportunity to reflect, to reassess the outlook and to focus upon the lagging effects of policy moves to date while conditioning future decisions as highly data dependent in the fine-tuning stages for monetary policy.

Toss in the fact that the UAW is now on strike and a possible US government shutdown into October plus student loan payments shock and our best guess at Q4 GDP growth is tracking about 0% growth to err on the side of caution. After that we’ll see, since some of these shocks could reverse into early 2024 and therefore complicate the Fed’s ability to read the tea leaves.

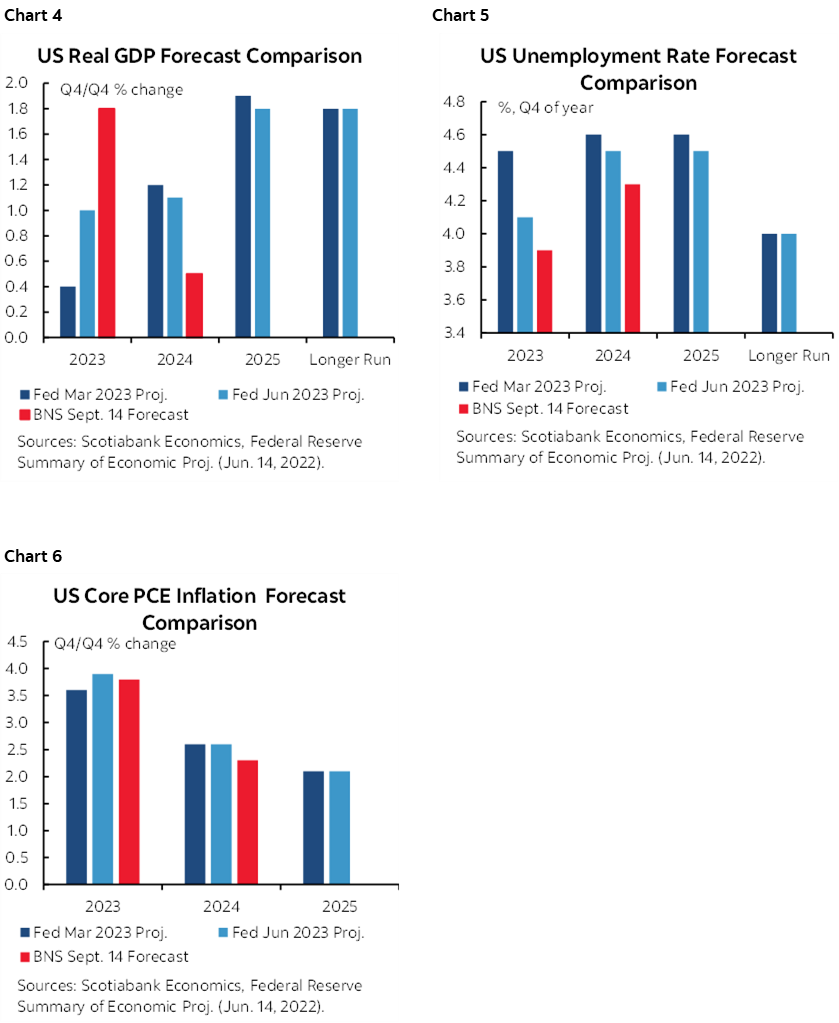

Forecast changes will have to be delivered. Our own forecasts are compared to the FOMC’s June projections in charts 4–6 and indicate that 2023 GDP growth may have to be revised higher, 2024 possibly lower, while the unemployment rate projections will have to be revised lower and core PCE inflation forecasts may only need to be tweaked.

On the dots into 2024–26, we’ll see what they do, but I think the best course of action may well be to leave well enough alone. The June plot showed only 75bps of cuts next year from the current 5.5% fed funds target rate and so there is little to be gained from reducing that amount and it’s probably premature to be adding to it.

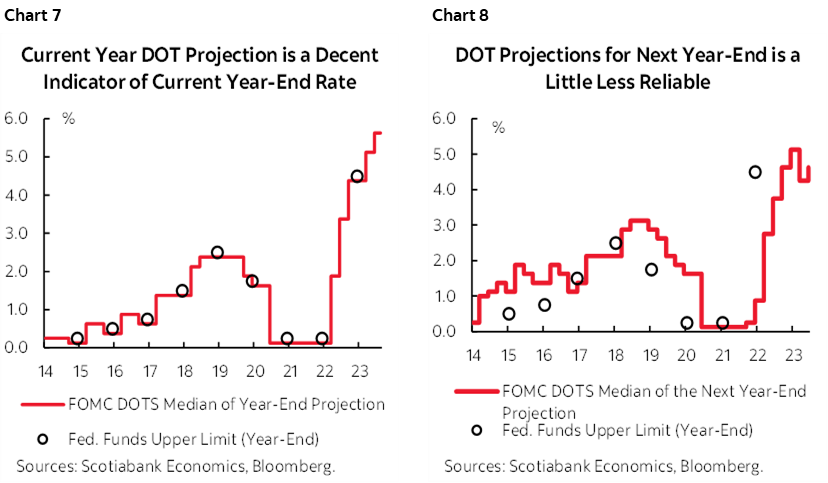

In any event, recall charts 7 and 8. The current year’s dots are worth following especially as the year progresses because they track actual decisions more closely than the outer year dots. Whatever market reaction to what is guided for 2024-onward is likely to fade pretty quickly. Markets are likely to view the FOMC as doing as much guesswork on how the policy rate may change that far out as anyone else.

Bank of England—Peak Rate?

The Bank of England is widely expected to hike Bank Rate another 25bps on Thursday. Consensus is nearly unanimous. Markets are mostly priced for it. A recent Reuters article put it well by saying “Now comes the challenge: how to pause monetary tightening without unleashing market exuberance about future rate cuts that would loosen financial conditions and revive price pressures.”

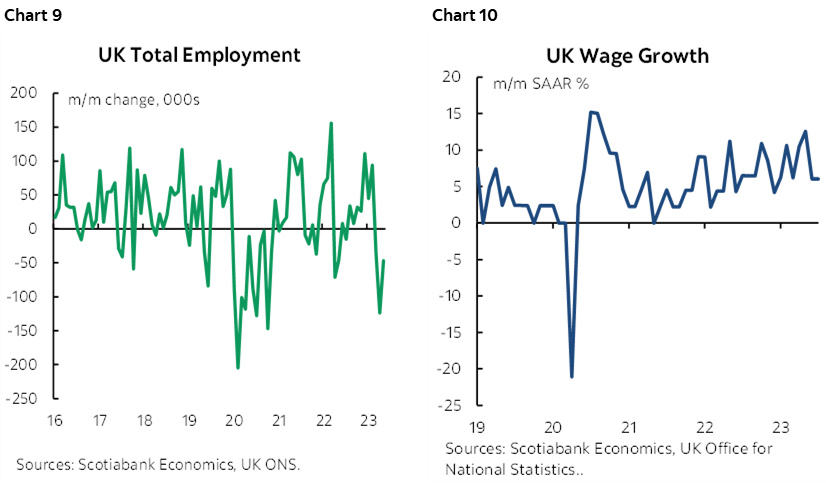

Wednesday’s CPI figures may further inform risks around the decision and possible forward guidance. Recent data has nevertheless soured. Employment has fallen for three months in a row up to July (chart 9). Fresher payrolls data up to August has flattened out over the past couple of months, putting a halt to a string of stronger gains. Wage growth is still strong but cooling and key is to look at it in month-over-month seasonally adjusted and annualized terms (chart 10). This rate is running at 6% which is somewhat cooler at the margin than the nearly 8% y/y rate.

The bias, if any, is likely to be expressed in the rather cagey terms that global central banks have been employing of late. They can’t tell markets they are done because of fear that markets will run with that and overshoot on rate cut pricing. They also don’t want to prematurely declare that inflationary pressures have been conquered. Expect a data dependent and noncommittal narrative.

Bank of Japan—How to Stir Volatility

No one expects the Bank of Japan to alter either its -0.1% target rate or its 10-year JGB yield target range of 0% +/-50bps with latitude toward tolerating a peak of 1% on Friday. There will be no further forecast updates after delivering them in July and with the next ones due in October. This should be a maintenance statement with no changes.

Anonymous BoJ officials indicated through Bloomberg that the BoJ feels markets went too far with Governor Ueda’s recent remarks. On September 8th, Ueda said moving away from the -0.1% negative policy rate before year-end was possible if wage pressures continue to build. His comments, they indicated, were merely oriented toward raising the possibility rather than indicating a base case scenario or delivering formal policy guidance.

Then again, it seems sensible to treat the risk seriously enough whether into year-end or 2024. The BoJ’s willingness to surprise markets has been apparent on two occasions in the past year and this may indicate that it believes the effects are more powerful when few expect change. Once was last December when they widened the JGB bands from +/-25bps to +/-50bps around 0% allegedly for technical reasons to improve market functioning. The other time was this past July when they signalled tolerance to allowing the 10-year yield to rise modestly above 0.5% by saying the range was a “reference” rather than a “rigid limit.” As of writing, the 10-year JGB yield sits at 0.71%.

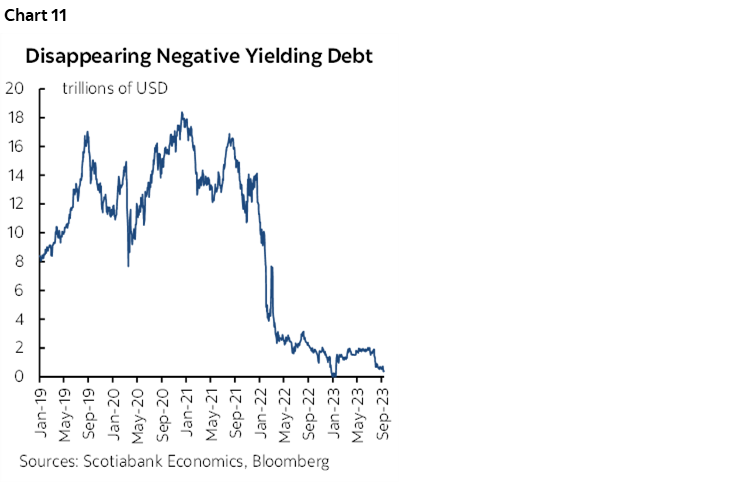

If and when the BoJ drops its negative rate policy, it would be the final nail in the coffin for negative yielding debt (chart 11). The carry effects into other global bond markets would likely motivate a global bond market sell off.

PBOC—Banks Likely to Hold

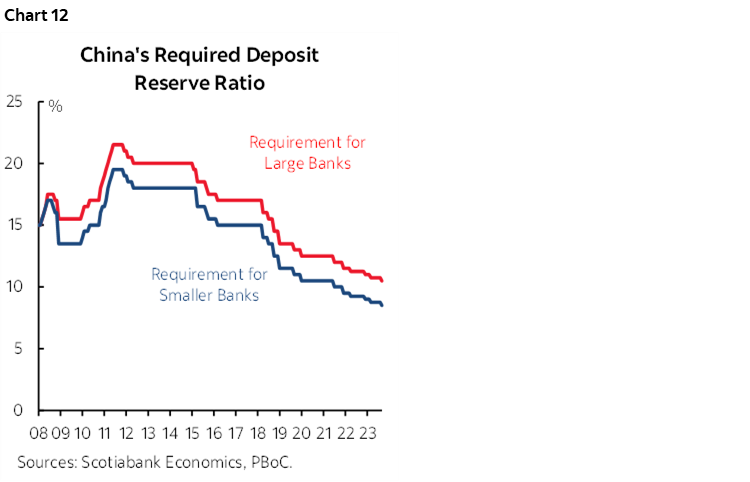

After no change in the PBOC’s 1-year Medium-Term Lending Facility Rate it’s probably unlikely that Chinese banks will alter their 1- and 5-year Loan Prime Rates on Tuesday. They are more focused upon the volume lift to their potential lending and funding prospects after the further 25bps cut to required reserve ratios for large and small banks (chart 12).

BoC’s Deliberations & Households

After leaving its policy rate on hold on September 6th while guiding that it may hike again (recap here), the aftermath of the decision will continue to reverberate through additional communications this week.

The BoC’s Summary of Deliberations arrives on Wednesday in the customary two-week lag to the decision itself. Watch for the balance of discussion around appetite for delivering another hike at this meeting. When asked if there was such a discussion during his September 7th press conference, Governor Macklem’s answer was to wait for the Summary of Deliberations. When asked whether further interest rate increases are necessary, Macklem said:

“We will take our decisions one at a time. We are prepared to raise the policy rate further if needed. So what is ‘if needed?’ We see the economy has entered a period of weaker growth that is needed to relieve inflation pressures, but inflation is still too high, and the downward momentum has slowed. We are concerned about the persistence of inflationary pressures. We will be carefully monitoring them. If we come to the conclusion that we haven't done enough, then we are prepared to do more but we don't want to do more than necessary.”

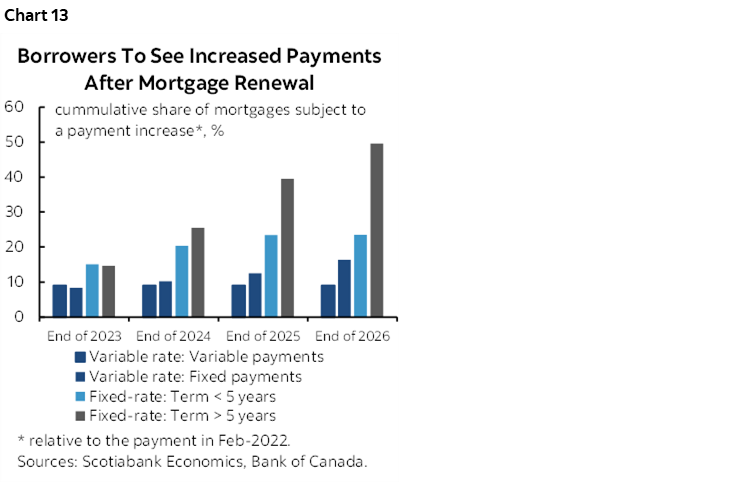

The day before the Summary will bring a speech by one of the BoC’s Deputy Governors, Sharon Kozicki. I have found Kozicki to be thoughtful and careful in her analysis and remarks including before she became a Deputy. She will speak about ‘how household differences have affected monetary policy since the onset of the Covid-19 pandemic.’ Text will be available at 1:45pmET but there will be no press conference. This could be a useful BoC speech. Potential topics that come to mind would include disaggregating measures of household finances in terms of liquidity and debt in both flow and stock terms. That could further inform how the BoC is looking at rate pass through effects and mitigants that might have affected the transmission effects and timing of monetary policy decisions thus far. She is also likely to reinforce the fact that the bulk of the fixed rate mortgage refinancings lie ahead (chart 13).

It's important to counterbalance this challenge. If incomes rise commensurate to what we are presently seeing for growth in wages and incomes then this could help debt serviceability through the reset period. If house prices continue to rise as they have been doing since Spring then resets will occur against the backdrop of higher home equity that can support refinancing. Supporting factors to the outlook include the economy’s rising terms of trade, soaring immigration, strong corporate balance sheets, ongoing movement toward applying further fiscal and regulatory stimulus by Federal and provincial governments, tight housing and auto inventories, and a thus far highly resilient US economy backed by the best measures for US household finances in decades.

Swiss National Bank—Ok, but Maybe We Shouldn’t

Thursday’s decision is expected to deliver a 25bps hike. Guidance at the prior meeting in June emphasized that “it cannot be ruled out that additional rises in the SNB policy rate will be necessary to ensure price stability over the medium term.” That decision emphasized concern around second-round effects on inflation. Still, with inflation running at 1.6% y/y and core CPI at 1.5% y/y it’s feasible that a potential hike will be delivered with a carefully dovish bias.

Riksbank—Hitting Peak Guidance

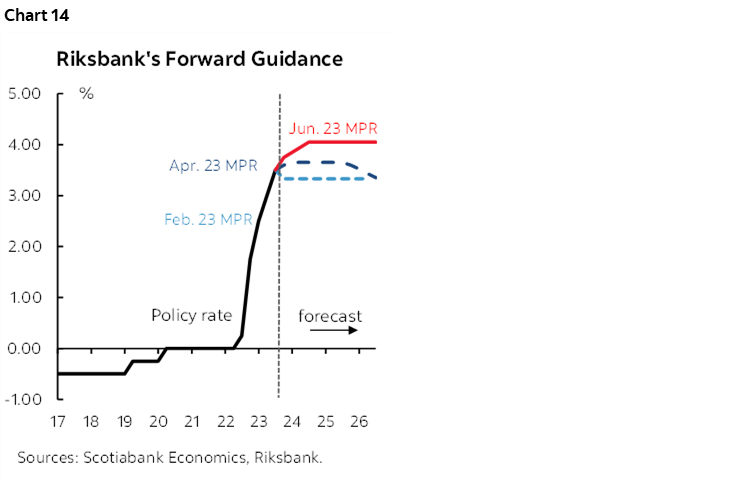

Sweden’s central bank is widely expected to hike its policy rate by another 25bps to 4% on Thursday. That would bring it in line with prior guidance on the terminal rate (chart 14). This might be the end of the tightening cycle, or very close to it. Underlying inflation ex-energy has pulled off to 7.2% y/y from a peak of 9.3% earlier this year.

Norges Bank—Easy Peasy

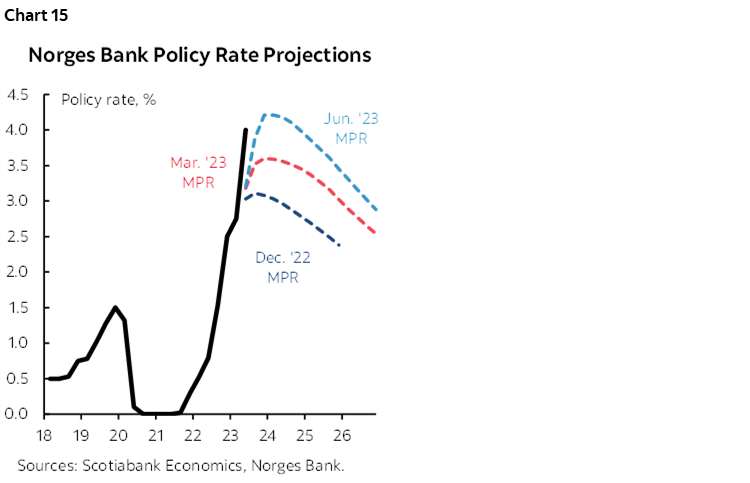

Thursday’s decision is widely expected to deliver another 25bps increase in the deposit rate. Why? Because they said so in September when they last hiked! Recall the guidance that the deposit rate “will most likely be raised further in September.” That would achieve the path laid out in the last formal guidance in June with updated guidance due at this meeting (chart 15). Governor Ida Wolden Bache reinforced this by saying that “If the economy evolves as currently anticipated, the policy rate will be raised further in September.”

What adds to a modest among of intrigue, however, is that August’s inflation cooled by more than expected with underlying inflation pulling off by -0.6% m/m and to 6.3% y/y (6.6% consensus) while the economy stalled by posting no growth in Q2 although it posted signs of a mild rebound in July.

Banco Central do Brasil—Well, This is Boring

Another significant rate cut is expected on Wednesday. The reason for the remarkable unanimity around the calls from various shops is because the guidance that was offered at the August 2nd decision when the Selic rate was cut by 50bps said “the members of the Committee, unanimously, foresee a reduction of the same magnitude in the next meetings and assess that this is the appropriate pace to maintain the contractionary monetary policy necessary for the disinflationary process.” I wish all central banks were this easy to forecast! Actually, nah, that wouldn’t be any fun.

Bank Indonesia—Zzzzzz

No change is expected to the 7-day reverse repo rate on Thursday. The rate has been stuck at 5.75% since the start of this year and BI believes that inflation will remain under control within the target range.

Bangko Sentral ng Pilipinas—Winding Up Again?

No change is expected to be applied to the 6.25% overnight borrowing rate on Thursday but a minority think there could be a resumption of the tightening cycle. Inflation recently surprised higher by jumping to 5.3% y/y (4.7% prior). That’s important because the prior decision in August warned that they are monitoring “the emerging risks to the inflation outlook” and were “ready to resume tightening when necessary” while judging the level of the policy rate to be “not that elevated.”

Central Bank of China Taiwan—Nah

Thursday’s decision is unanimously expected to leave the benchmark rate unchanged at 1.875%.

SARB—Extending the Pause

The South African Reserve Bank is expected to hold its repo rate at 8.25% on Thursday. They introduced a pause at the July meeting following ten straight increases. A wildcard may be the release of August inflation figures the day before the decision.

Turkey’s Central Bank—That Didn’t Work, So Try Again!?

You need an auctioneer to call this one! Turkey’s central bank is expected to hike its one-week repo rate again on Thursday. By how much, who knows, but the median guess is for a five percentage point hike to 30%. The focus remains upon attempting to repair credibility, restore price stability and stabilize the Lira. Even after the 7.5 percentage point hike on August 24th, the lira still depreciated by a cumulative amount of over 4% since then.

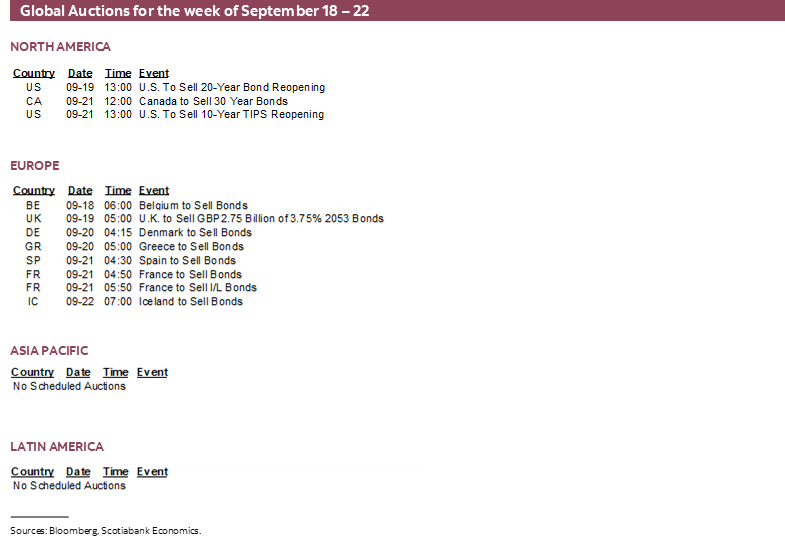

CANADIAN INFLATION—ONE SMALL STEP TO OCTOBER’S DECISION

Canada updates CPI inflation for August on Tuesday. It’s one of two inflation reports that the Bank of Canada will have to consider before its next policy decision on October 25th. It will also face another report on jobs and wages before that decision, plus it will update its own surveys of business and consumer attitudes in mid-October that will further inform the degree to which inflation expectations may continue to be unmoored. In other words, nothing will hang on this report alone versus how it fits into the broader suite of evidence that will also be considered.

I’ve estimated a headline rise of 0.3–0.4% m/m NSA that would lift the year-over-year rate from 3.3% in July to 4% in August. Shifting base effects explain some of the expected rise in the year-over-year inflation rate to 3.6% and this is because the year-ago comps are moving past the peak rates of price increases back then. Gas prices are expected to add to upside pressures.

What may add further upside could be potentially greater than usual gains in clothing and footwear prices as seasonal offerings change over and still firm contributions from service prices.

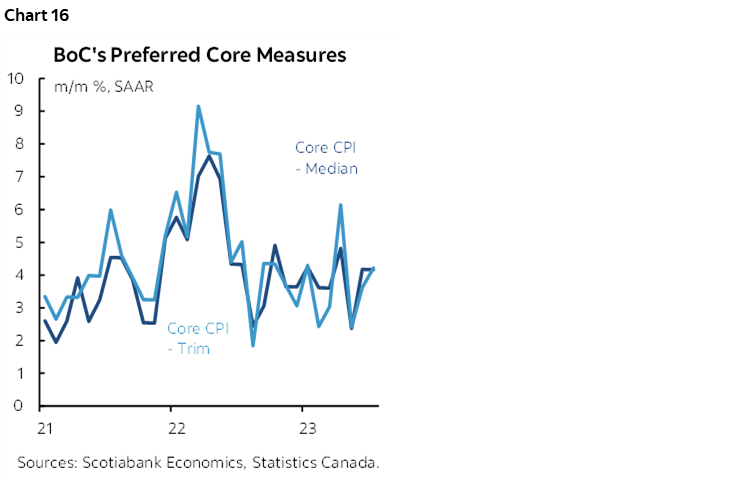

The main focus, however, will be upon the trimmed mean and weighted median measures of inflation that have been running far above the 2% headline target at the margin (chart 16).

GLOBAL MACRO—ANOTHER UK INFLATION ZINGER

Global purchasing managers indices and UK inflation ahead of the Bank of England’s decision are the main attractions over the coming week.

Purchasing managers will be updated by Japan and Australia on Thursday, and then the Eurozone, UK and US on Friday. The US measures, however, will not be the ISM gauges that the Fed watches more closely given their greater alignment toward the domestic economy. These measures can inform in-quarter GDP tracking and the composite gauges have been signalling contraction in the Eurozone, UK and Australian economies, growth in Japan, and stagnancy in the US global gauges. Their details on hiring attitudes and pricing plans can also capture market attention.

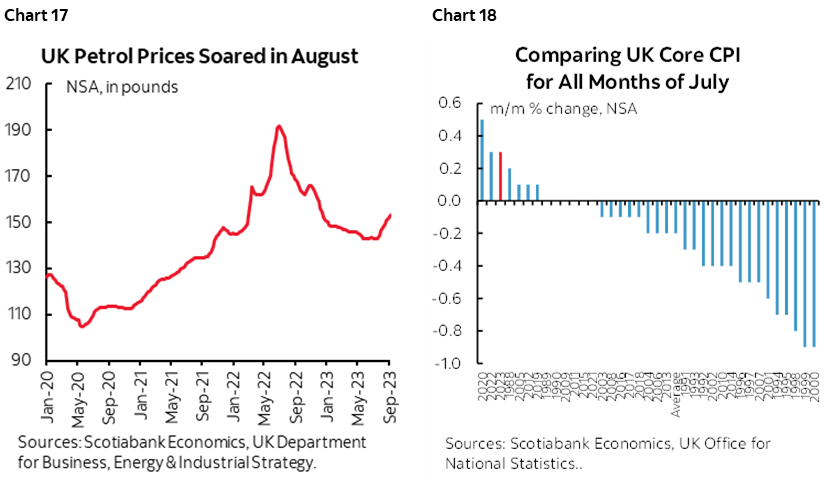

UK CPI inflation will get a strong lift from higher gasoline prices on Wednesday. Petrol prices soared during August and continue to rise in September (chart 17). CPI could rise by about ¾% m/m in seasonally unadjusted terms. More important will be core inflation both in terms of the present reading, but also in terms of concern that rising energy prices and wages could spawn ongoing upward pressure on other prices. There is no reason to believe that core price inflation has eased recently (chart 18). Also watch UK retail sales on Friday given expectations for a mild rebound from the prior month’s drop.

Canadian markets will be primarily influenced by external events such as the wave of central bank decisions, plus CPI and BoC communications. There will also be modest data risk to consider. Housing starts for August could stabilize with upside risk after heavy rains impeded construction during the prior month in major parts of the country such as southern Ontario and eastward. Retail sales will be watched for whether they modestly add to rebound evidence following gains in hours worked, manufacturing shipment volumes and wholesale trade volumes. Statcan previously guided that the dollar value of sales was tracking a small gain but there is always high revision risk to this estimate.

The Fed will dominate US market considerations as data risk will be generally low. Housing starts for August kick it off on Tuesday and might soften. Weekly jobless claims have been trending low and the Philly Fed’s regional manufacturing gauge will be monitored to see if it follows the Empire measure higher (Thursday). Existing home sales could stabilize following the prior month’s drop (Thursday). S&P’s global purchasing managers indices for September wrap it up on Friday.

Watch Eurozone CPI revisions and details for August on Tuesday. Japan reports CPI on Thursday and Malaysia is out the next day. After slipping into technical recession, New Zealand may return to slow growth in Q2 (Wednesday). LatAm markets will be quiet outside of Brazil’s central bank decision with just Mexican retail sales (Thursday) and bi-weekly CPI (Friday) to consider.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.