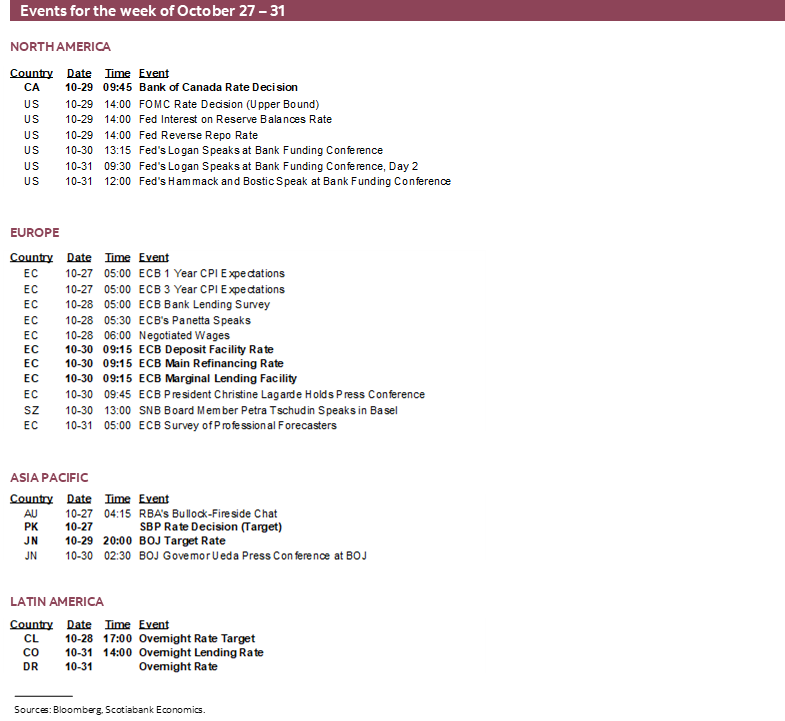

Next Week's Risk Dashboard

- US policy uncertainty hit record highs…

- …even before flaring Canada-US tensions

- Fed preview: -25bps, end QT, reinforce September dots

- BoC preview: -25bps, careful guidance

- US, Canadian earnings ramp up…

- …with the main focus on US tech

- ECB to stand pat

- BoJ to hold, updated forecasts key

- BCCh to stand pat

- Ditto for BanRep

- Canadian GDP: Still adding slack

- Milei’s make-or-break midterms

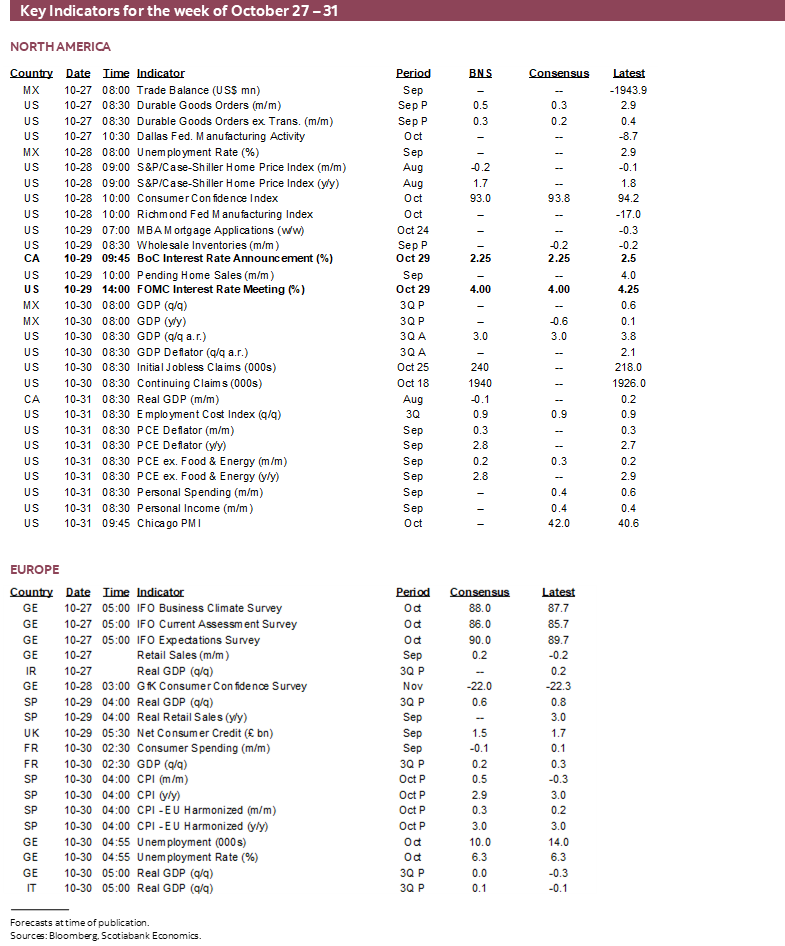

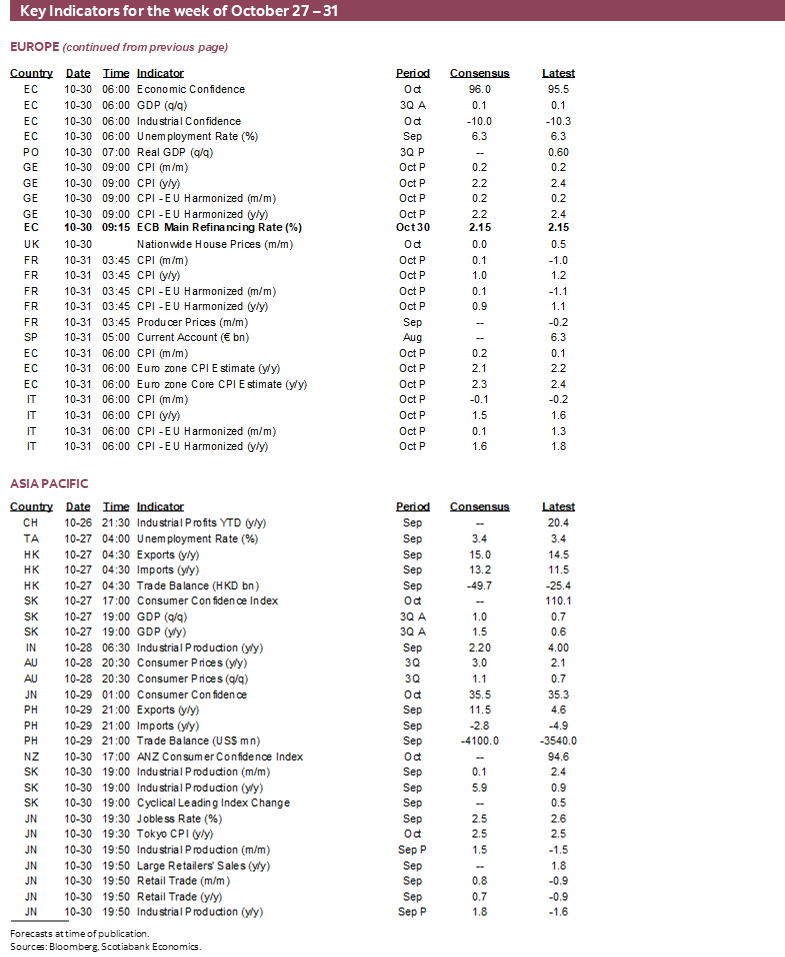

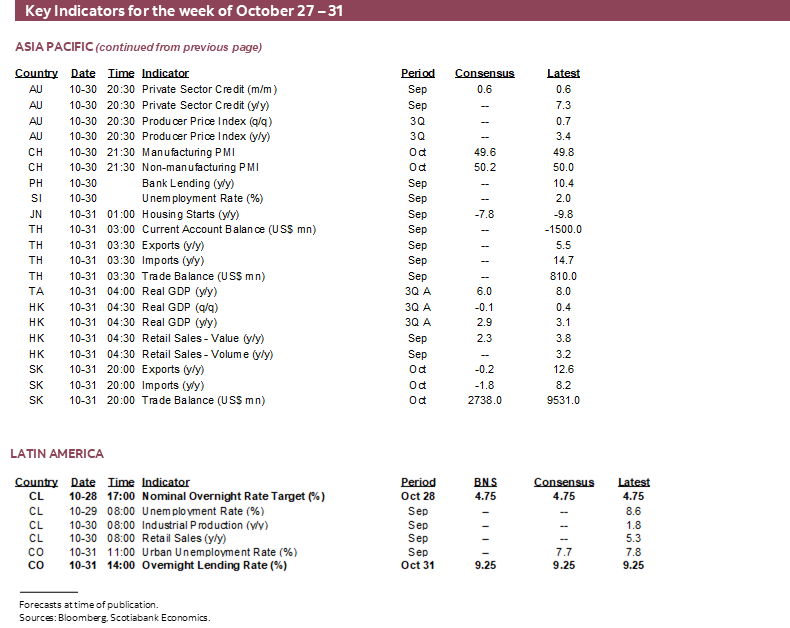

- Global data

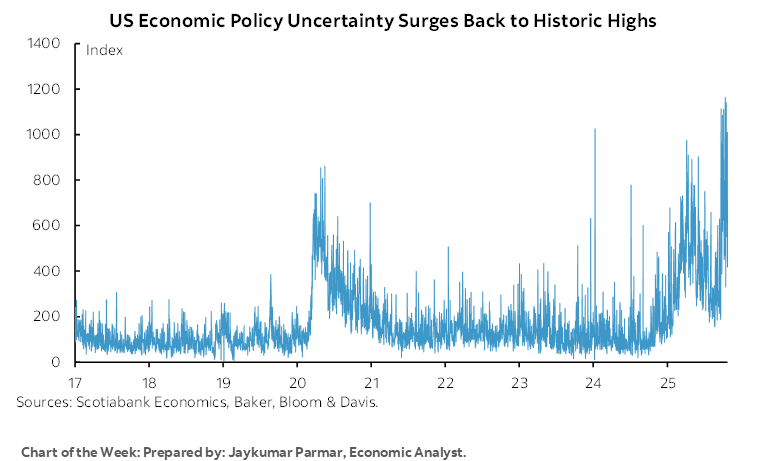

Chart of the Week

The coming week is going to be significantly dominated by central bank decisions combined with a wave of ‘Mag7’ earnings and data releases. Each of the Fed, BoC, ECB, BoJ, and central banks in Chile and Colombia will weigh in. Ongoing developments in Canada-US relations may also figure prominently. The world has changed a great deal since former President Reagan’s speech about the virtues of free trade and against tariffs in 1987 such that Canada and the US are more tightly integrated than ever before which raises the risks to both sides of failing to work toward an agreement that addresses concerns on both sides. As the front cover chart of the week depicts, US policy uncertainty indices are flaring to record highs which will cost growth both in the US and abroad.

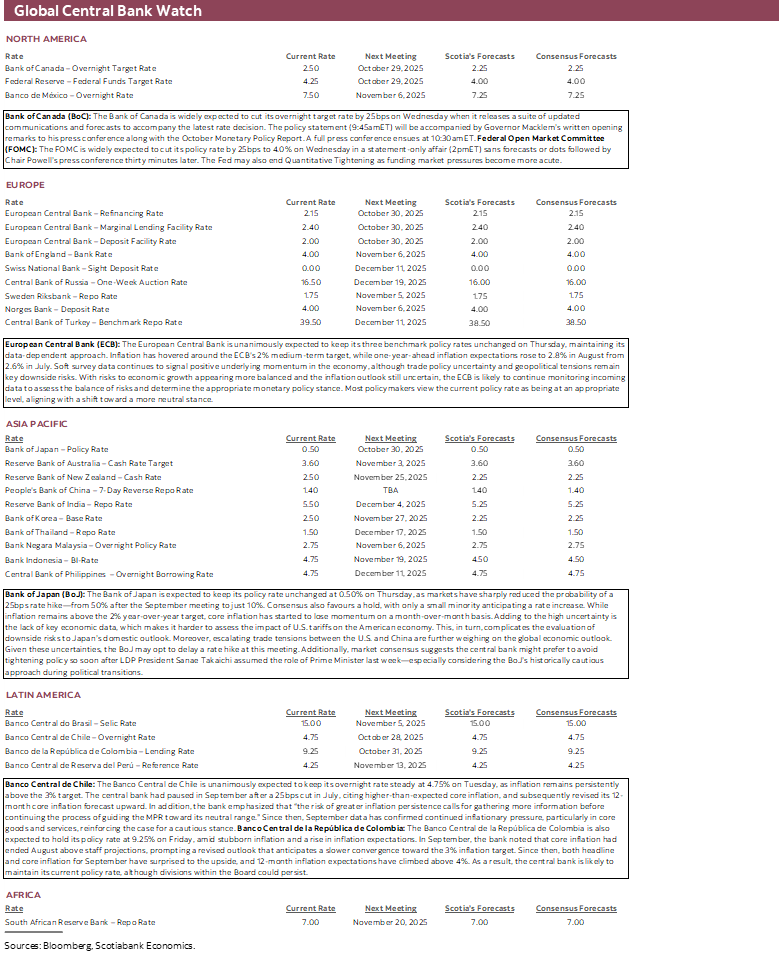

FOMC—FUMBLING IN THE DARK

The FOMC is widely expected to cut its policy rate by 25bps to 4.0% on Wednesday in a statement-only affair (2pmET) sans forecasts or dots followed by Chair Powell’s press conference thirty minutes later. The next updated Summary of Economic Projections including a fresh dot plot of members’ rate expectations will arrive at the December meeting.

This would bring cumulative easing from the 5½% policy rate peak to 150bps and with considerably more to come.

FOMC Still Focused More on Jobs than Inflation Risk

The modus operandi continues to involve a pivot toward greater concern about downside risk to the job market while looking through at least near-term risk to inflation. Recall Chair Powell’s quote at the September press conference:

“We kept our policy at a clearly restrictive level over the course of this year. That's because the labour market was in a strong position. I can no longer say that. The risks were clearly tilted toward inflation. I would say they're moving toward equality, or greater equality which suggests we should be moving in the direction of neutral.”

This is reminiscent of the pandemic when Chair Powell ignored inflation evidence and emphasized the need to target fully inclusive maximum employment, except that the nature of today’s shocks is materially different.

Of course, judging the current state of the Fed’s dual mandate is nearly impossible because of missing data for both jobs and inflation. Jobs because we don’t have nonfarm payrolls for September. Inflation because we don’t have the Fed’s preferred PCE gauges or part of the necessary ingredients in producer prices while the CPI estimate has a huge data quality problem. About 40% of the CPI basket was estimated using proxy methods that use prices in other cities/regions in lieu of shortfalls elsewhere or using prices for somewhat different goods where data can’t be obtained and all due to cuts to the BLS’s budget. Compounding this is ongoing doubt toward the role played by seasonal adjustment factors in tamping down core inflation as explained here.

The fact that we don’t have fresh readings for nonfarm payrolls likely won’t matter much to Powell given the previously weakening trend for employment growth including sharp downward annual revisions to March payrolls and weakness since then. One caveat to this view is that the breakeven rate for monthly nonfarm payroll creation has slowed toward very low numbers, maybe zero, possibly even negative in light of highly restrictive immigration policy and its effects on both population and labour force expansion.

Powell Likely to Indicate Continued Backing of the Previous Projections

Chair Powell will be asked whether the SEP and dot plot in September still applies. He’s likely to indicate that it does. Powell said on October 14th that “it is fair to say that the outlook for employment and inflation does not appear to have changed much since our September meeting four weeks ago.” He’s likely to have something similar to say this time, perhaps buttressed by a slightly softer than expected reading for core CPI. Therefore, while sounding cautious toward data—or the absence thereof—and developments, he is likely to passively reinforce the Committee’s guidance to expect another 25bps rate cut in December.

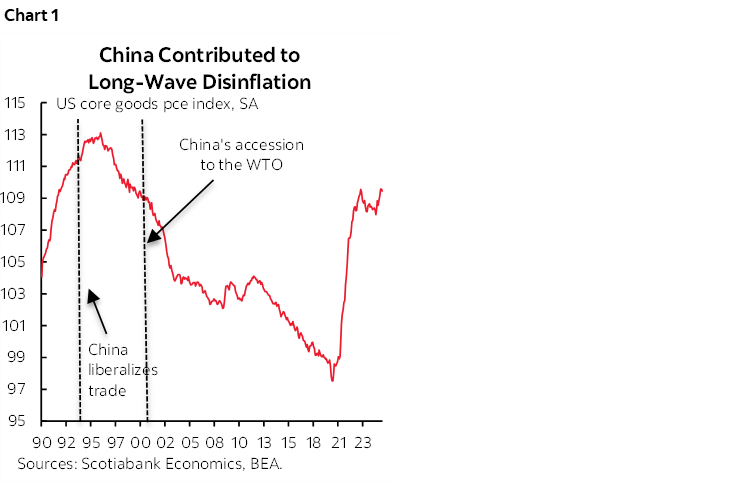

As for inflation, the FOMC is at risk of falling victim to myopia once more. We won’t settle the debate about what happens to inflation from tariffs as a subset of much broader and more complicated supply chain challenges with short-term price data. This is multi-year stuff folks within supply chains that are notoriously complicated and that evolve slowly over time. For instance, to play the flipside of today, had you rejected the possible effects on US inflation of China’s trade liberalization in the 1990s and accession to the WTO in 2001 by only looking at a handful of monthly inflation readings back then, the result is that you would have misjudged the next two decades of disinflationary pressures (chart 1).

The End of QT

The more meaningful development could be around the balance sheet in the wake of Powell’s speech titled “Understanding the Fed’s Balance Sheet” (here). Recall the following guidance with emphasis added:

“Our long-stated plan is to stop balance sheet runoff when reserves are somewhat above the level we judge consistent with ample reserve conditions. We may approach that point in coming months, and we are closely monitoring a wide range of indicators to inform this decision. Some signs have begun to emerge that liquidity conditions are gradually tightening, including a general firming of repo rates along with more noticeable but temporary pressures on selected dates.”

Pressures on market funding conditions have become more acute, leading to the base case likelihood that the Fed announces the end of quantitative tightening at this meeting. Chart 2 shows funding spreads over fed funds. Chart 3 shows falling reserves. Chart 4 shows that excess reserves parked at the Fed in overnight RRP have fallen to nothing. Some of this is liquidity drain is due to the Treasury’s focus upon replenishing the General Account that was depleted by the earlier funding spat and doing so through bills issuance that mopped up liquidity. The Fed could err on the side of viewing funding pressures as partly driven by perhaps underestimating optimal reserves and hence end QT now.

BANK OF CANADA—ANOTHER CUT COMING

Wednesday morning will offer the full deal from the Bank of Canada when it releases a suite of updated communications and forecasts to accompany the latest rate decision. The policy statement (9:45amET) will be accompanied by Governor Macklem’s written opening remarks to his press conference along with the October Monetary Policy Report. A full press conference ensues at 10:30amET.

Pretty much everybody who is anybody in the forecasting community expects the BoC to cut by 25bps, bringing the overnight rate to 2.25%. Markets are priced for about an 85% probability of a cut. That would bring cumulative easing from the 5% policy rate peak to 275bps of cuts. At 2.25%, the overnight rate would be basically zero in inflation adjusted terms, or even negative—depending upon whether we use trailing CPI inflation or core inflation, or measures of expectations drawn from surveys of forecasters, businesses and consumers.

The case for additional easing is not airtight but includes the following points.

- They’d need good arguments against a cut that I don’t think they have in relation to disappointing the over 80% priced probability of a 25bps cut. From a risk-reward standpoint, it may be more difficult to justify holding than to cut and, if they agree, sound like they’re shifting to the sidelines.

- Core inflation measures are in the range on a higher frequency m/m SAAR basis for a while now.

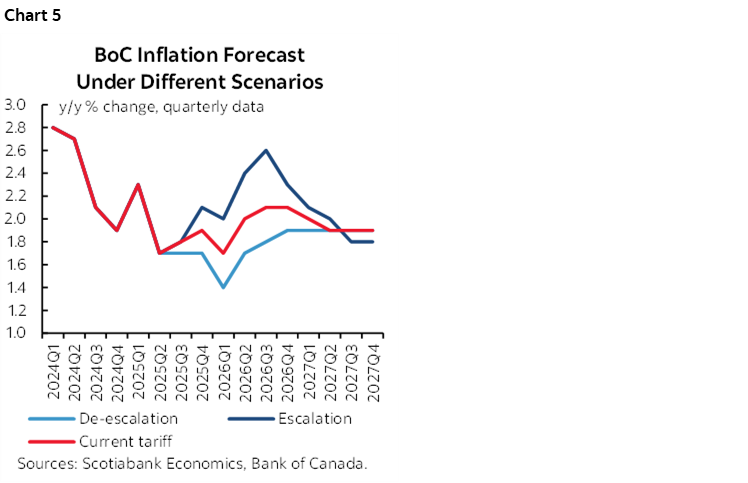

- Their July MPR expected inflation to be around 2% by the end of 2026 in the current tariff scenario. Developments since then likely have them thinking there is more downside to that forecast than upside, ergo give it a nudge. In particular, if trade negotiations are stalled or if tensions should escalate, then the BoC may lean further toward the lowest of its inflation scenarios in the July MPR (chart 5). Governor Macklem has indicated the BoC will revert back to providing a base case central forecast in the October MPR which may or may not prove appropriate given trade tensions.

- One cut doesn't do it given my longstanding bag of chips metaphor and that you can’t just pull one chip out of the bag.

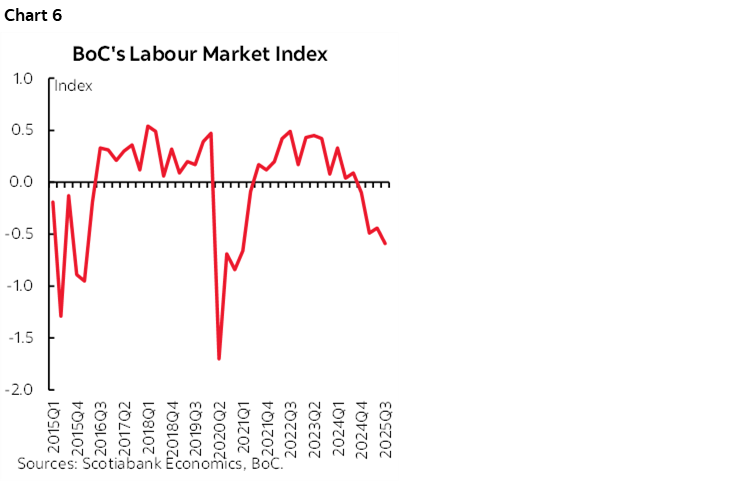

- Jobs rebounded, but the BoC always fades just one spot number for the volatile household survey and the trend is weak. The BoC’s broad labour market index is rapidly falling to levels not seen since 2021 (chart 6).

- GDP is weakening with basically no growth being tracked in Q3 so slack continues to open up. On the one hand, that's why they were cutting from last July to this March in anticipation of a souring economy. Plus, the economy is broadly tracking their expectations in the July MPR. But key may be Macklem’s ongoing guidance they expect a slight improvement in growth by at rates still below the economy’s potential GDP growth rate which means more slack opening up over time.

- You could argue the Budget's influences both ways. Wait to see if PM Carney is going to prime the pump a lot, versus act now because it might be optically harder to act after the Budget is presented and passed. I think at this juncture, the BoC will say they want to err on the side of combining policy measures.

- Macklem is a dove at heart. I rarely take him seriously when he jawbones inflation risk. He’s a labour market guy at heart as he was when delivering fully inclusive speeches as Senior Deputy Governor under BoC Governor Carney at the time and more recently in the pandemic.

- Trade policy uncertainty will be elevated for a long time yet especially in light of recent developments.

- The case for an unlikely but not impossible hold at this meeting could be based on the following points:

- the real policy rate is zero and we're already well within the neutral r* range.

- Financial conditions are buoyant. There is no financial crisis notwithstanding persistent risks.

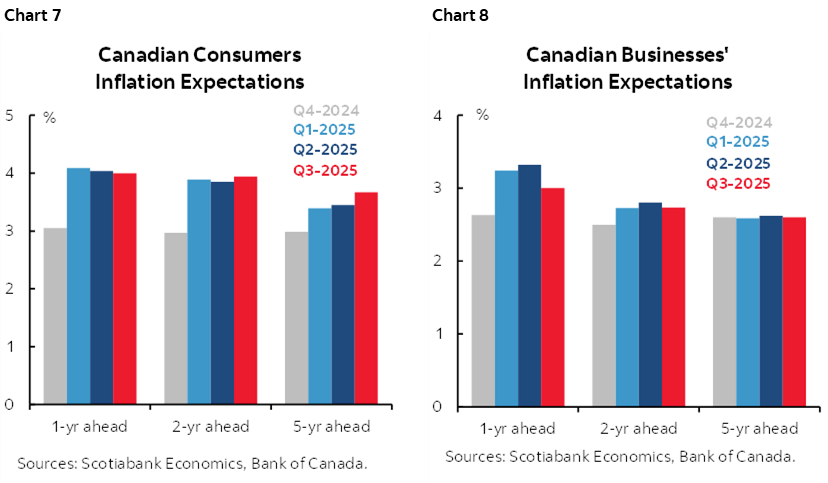

- Inflation expectations remain elevated (charts 7, 8).

- Monetary policy entails lagging effects and we’re still inside the full pass through of 250bps of rate cuts that began in June of last year through to March of this year. Give it time for a zero real rate to work through.

- there are more drivers of inflation risk than just output gaps. Costs are under upward pressure through the whole value-added supply chain. Labour settlements are too hot, productivity is not, inventories are high, and supply chains are at a highly nascent stage of being revamped in the US-driven global trade war and revamping them entails higher costs. Someone pays those higher costs. Sensible incidence effects would have one thinking everyone will share in it including higher prices for consumers in a longer wave sense.

- the tariff shock to Canada is often exaggerated. The effective tariff rate has bumped up to 6%. USDCAD over 1.40 is doing what a flexible exchange rate should do to help assuage the shock to the terms of trade. Remove the tariffs on the most affected narrow sectors, and the tariff shock is tiny given the high CUSMA/USMCA compliance rate.

- Canada has the lowest tariff shock against any notable US trade partner by far. Anything can happen to CUSMA/USMCA but you can't conduct monetary policy when the outcome could be bimodal in nature.

- Recent developments in Canada-US trade relations including the suspension of negotiations may have driven greater conviction in Ottawa that bigger deficit-financed measures are needed.

The way to balance the pros and cons to cutting at this meeting may be through a generally neutral-hawkish sounding and noncommittal bias. That could be as simple as continuing to strike out the reference in the July statement to how “there may be a need for a reduction in the policy interest rate” as they did in the September statement or strengthening this message in such fashion as to indicate more gradual assessments in future.

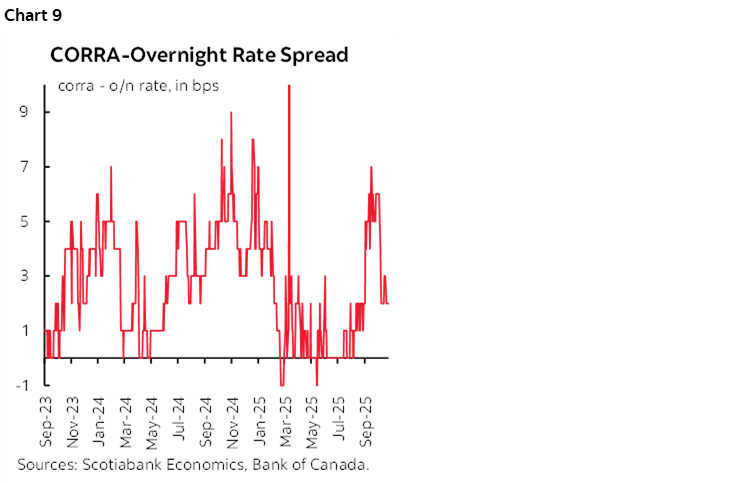

As for balance sheet measures, the BoC’s policy toolkit and market developments have succeeded in tamping down the spread between the market measure of the policy rate (CORRA) and the policy rate itself (chart 9). This likely implies no need for further adjustments at this time as the BoC monitors any spillover effects into Canadian funding markets from what the Federal Reserve may do later in the day.

BOJ—PATIENCE

The Bank of Japan issues a policy statement late on Thursday evening eastern time and will be followed by Governor Ueda’s press conference in the early morning (~2–3amET).

No policy rate change is expected but refreshed forecasts and guidance could be impactful. Markets are priced for no rate change at this meeting but about half of a quarter-point cut in December and full cut pricing by early 2026 at either the January or March meetings.

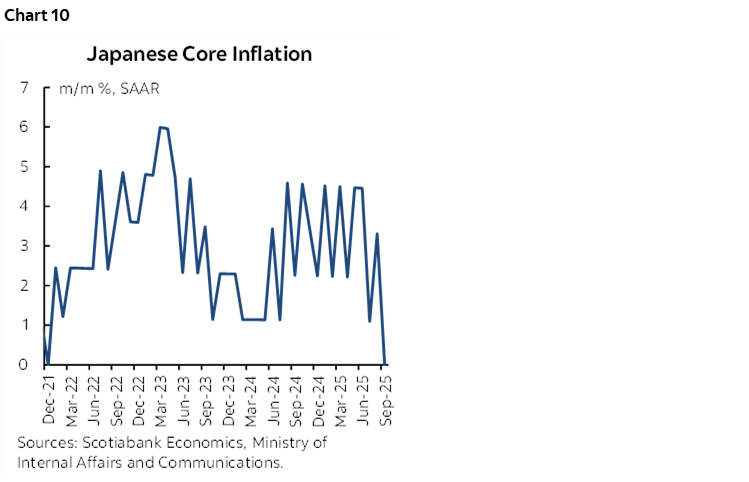

Acting now with further policy tightening would be affronted by weakening underlying inflation. Japanese core CPI was flat in m/m seasonally adjusted and annualized terms during September. It’s just one data point, but it’s a sudden deceleration to the weakest reading since December 2021 (chart 10). Core inflation has slowed on a three-month moving average basis. That’s key because the BoJ has previously said it “will hike when the outlook matches our forecast.” Well, it’s not.

As for the future, the BoJ’s forecasts will be closely watched for whether it repeats expectations for core CPI to land just beneath 2% by the end of next year and hit 2% the year after. Until the BoJ has greater confidence it is on track in this regard it may continue to be reticent to tighten further.

ECB—HOLDING PATTERN

The European Central Bank is also not expected to make any policy changes on Thursday. Markets are priced for no policy rate change and consensus unanimously expects a hold at a deposit rate of 2%.

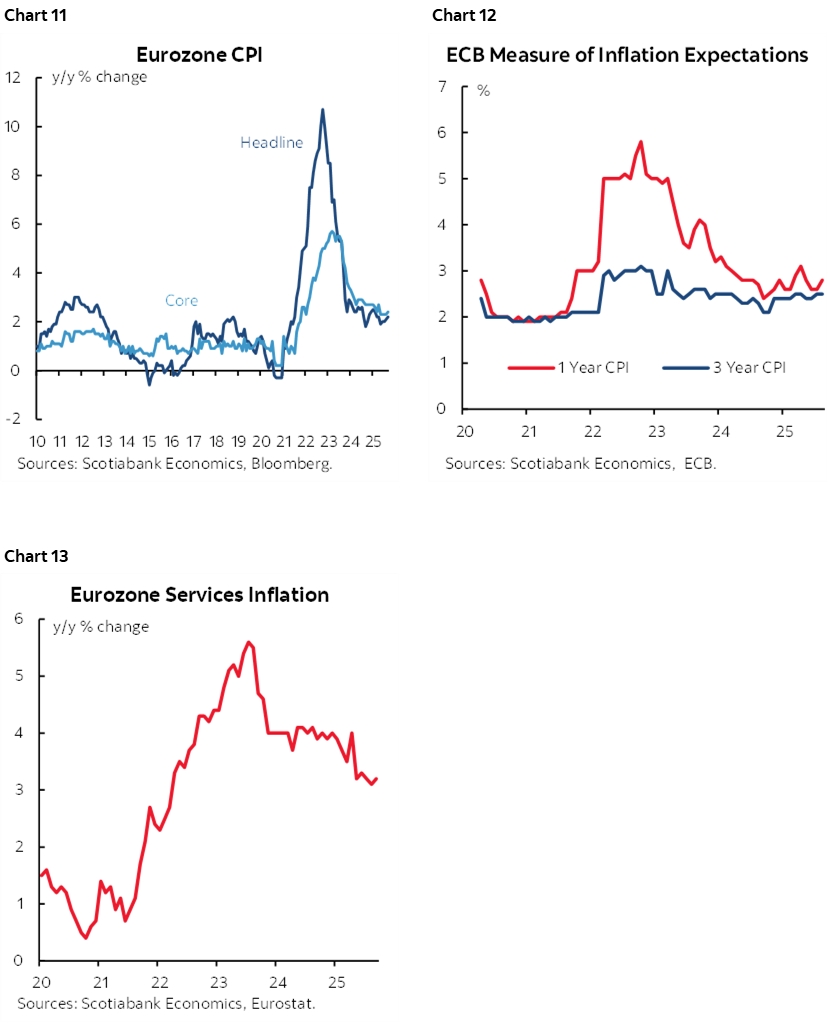

Core CPI inflation has come down to 2.4% y/y and is within the ECB’s 2% headline target zone (chart 11). Measures of inflation expectations are also just north of 2% (chart 12). 200bps of easing have brought the policy rate toward a neutral rate range while underlying inflation details like services inflation still indicating underlying concerns (chart 13).

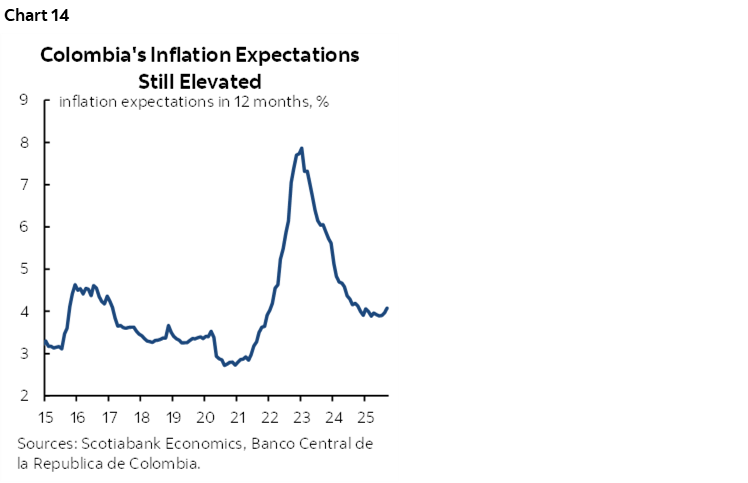

BANREP—INFLATION IS JUST TOO HIGH

Colombia’s central bank is widely expected to remain on hold at an overnight lending rate of 9¼% on Friday. It has been on hold since its last rate reduction in April. Inflation remains too high to contemplate further easing at this juncture. CPI is running at 5.2% y/y with core inflation just a hair beneath 5%. Inflation expectations also remain elevated (chart 14).

BCCH—HERE TOO!

Chile’s central bank is also unanimously expected to leave its overnight rate unchanged at 4.75% on Tuesday late in the day. Here too inflation is running too hot at 4.4% y/y (chart 15). Recall that BCCh also indicated patience when it said in its last decision that “the risk of greater inflation persistence calls for gathering more information before continuing the process of guiding the MPR toward its neutral range.”

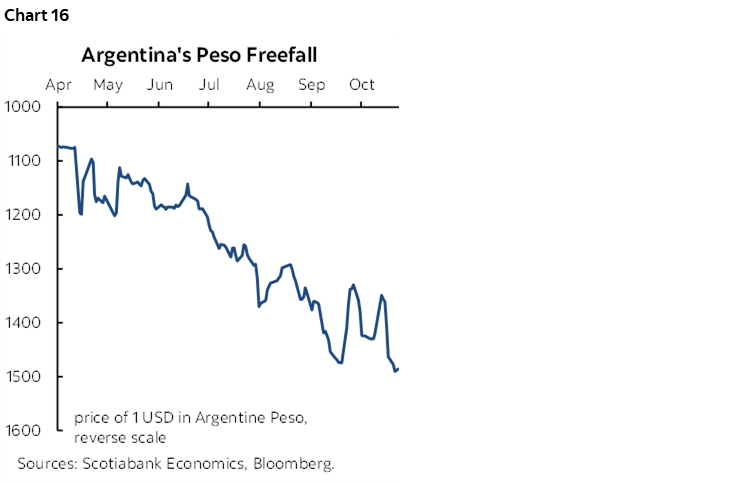

ARGENTINA’S ELECTION—ARE YOU IN OR OUT?

Argentina’s Legislative mid-term elections will be held on Sunday. It’s make or break time for President Milei’s reforms depending upon the outcome. Ditto for Argentina’s markets.

Half of the seats (127 of the 257) in the Chamber of Deputies and a third of the seats (24 of the 72) in the Senate will be elected. Milei's party—La Libertad Avanza—has been polling ahead of the Peronists represented by Fuerza Patria but not by much. A weak showing by Milei’s party could further damage the peso (chart 16) especially in light of President Trump’s guidance that “If he wins, we’re staying with him. And if he doesn’t win, we’re gone.”

CANADA’S ECONOMY—STILL ADDING SLACK

We’ll get a more complete picture of the performance of the Canadian economy when GDP figures arrive on Friday. August and September estimates will firm up estimates for overall Q3 GDP.

The August figures will include revisions to the initial guidance from Statcan that the economy was “essentially unchanged” that month. My tracking points toward a mild dip of -0.1% m/m SA. The figures for August will also include sector details. Statcan had said that “Increases in wholesale trade and retail trade were offset by decreases in mining, quarrying, and oil and gas extraction, manufacturing, and transportation and warehousing.”

Key, however, may be the first estimate for September sans details. There is very little information available for the month. We know that hours worked dipped by -0.2% m/m SA and since GDP is hours times labour productivity this points to downside risk. Retail sales also reversed August’s gain while existing home sales also dipped but vehicle sales accelerated.

The overall picture is one of an economy that may be posting very little growth in Q3. Based on monthly GDP estimates, growth could be around ¾% q/q SAAR after GDP contracted in Q2 despite strong consumption and strong final domestic demand.

As a consequence, Canada’s economy continues to open up a modest amount of slack.

EARNINGS—MAG7 RESULTS WILL BE KEY

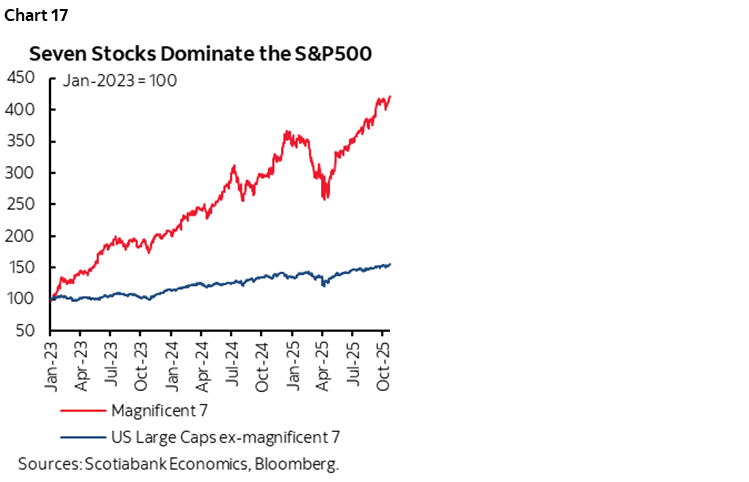

About 160 firms listed on the S&P 500 deliver Q3 earnings this week in a rapid intensification of and broadening of the season. Given the dominant role played by the ‘Magnificent Seven’ stocks in driving S&P performance (chart 17) it is their results that may matter most. Apple, Meta Platforms, Alphabet, Amazon, and Microsoft are among the key tech names to watch for their earnings, guidance, and further insights into AI-related tech spending.

Canada’s earnings season also intensifies with about 50 TSX-listed firms poised to release earnings over the week. Banks October 31st year-end and any funding implications will result in earnings releases for this important segment of the credit and equity markets only by the first week of December.

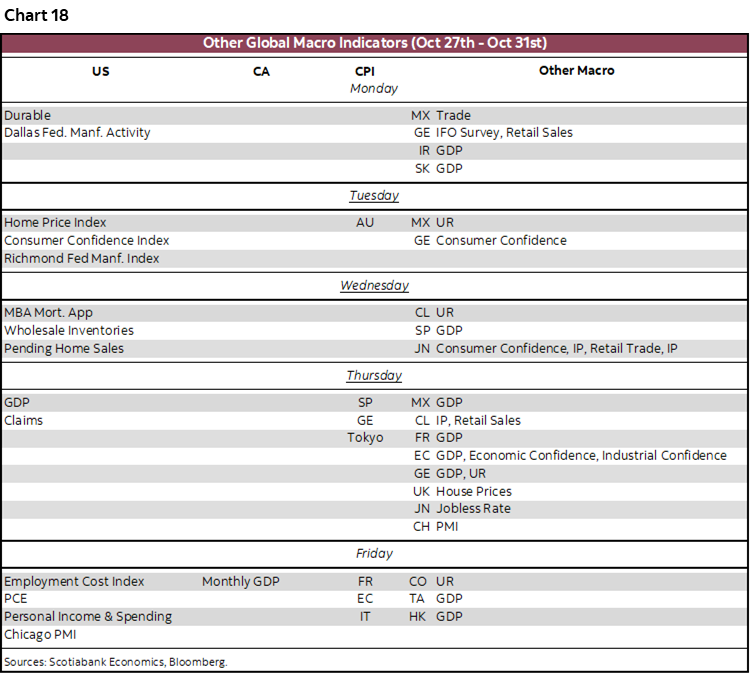

GLOBAL MACRO

See chart 18 for a listing of the key indicators due out this week from across the world with the caveat that yet again most of the US data including Q3 GDP will continue to be held up by the US government shutdown.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.