Next Week's Risk Dashboard

• BoC preview

• ECB to push back?

• Is US consumer confidence a warning shot?

• Earnings fan out with big names

• CBs: Brazil, Colombia to hike, BoJ to snooze

• GDP: US, Canada, EZ, Mexico, Sweden, SK, Taiwan

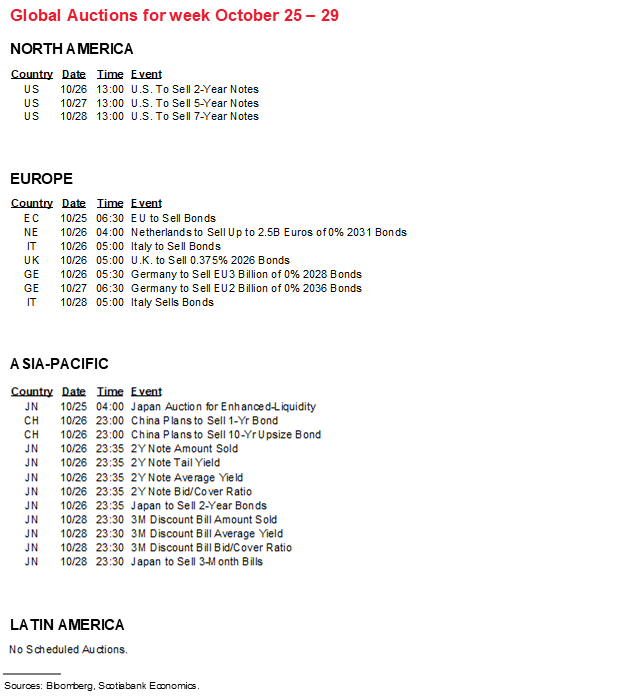

• Inflation: US, EZ, Australia, Japan

• Other macro

Chart of the Week

BANK OF CANADA—THE GOVERNOR’S BALANCING ACT

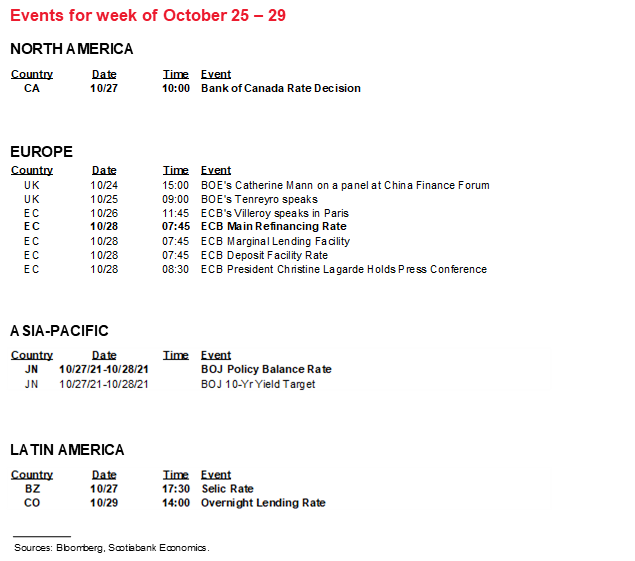

The Bank of Canada fires off its full salvo of communication tools on Wednesday. It starts with the statement at 10amET, the Monetary Policy Report including fresh forecasts and analysis at the same time, and then Governor Macklem’s press conference at 11amET for around an hour or so. In what may be a symbolic indication of the BoC’s thinking these days, they will return to holding an in-person lock-up for (vaccinated) journalists under embargo just like the good old times. Thanks, but I’ll watch from here!

Governing Council faces a delicate balancing act this time around. The Governor’s speech on September 9th (here) likely set up a move toward the reinvestment phase of the BoC’s quantitative easing program at this meeting. The result would reduce the C$2 billion/week rate of purchases in the Government of Canada secondary bond market to about C$1–1.5 billion/week spread in the primary and secondary markets. The intent is to target a roughly stable portfolio in the face of lumpy maturities that will have the bonds dropping off the balance sheet at a fairly rapid pace (chart 1). The reinvestment phase is loosely forecast to last through 2022 at a minimum and likely lasting through at least several of the first few rate hikes.

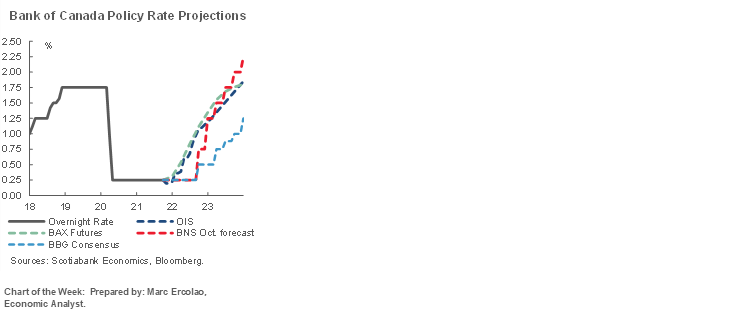

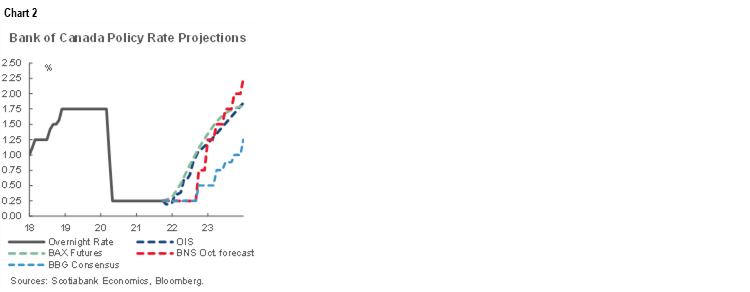

Which brings us to what to expect by way of policy rate guidance. The Governor is likely to walk a fine line between attempting to tamp down market pricing toward a rate hike as soon as March/April, versus remaining committed toward rate hikes later in 2022. That could present opportunity to fade market pricing for an early hike in terms of the risk-reward trade-off to what is priced. Our forecast is shown in chart 2 in relation to market proxies drawn from the bankers’ acceptance futures market and the OIS market and the consensus of other economists. We remain less aggressive than markets toward the starting point with a first rate hike still forecast only for next July, broadly in line with the priced path toward the end of 2022 into early 2023 and modestly higher than markets by the end of 2023. The consensus of economists is likely stale compared to our forecasts and poised for possible adjustment, but remains materially lower than our forecast.

Why would the Governor lean against an early hike? He’s likely to keep his options open, but to do so in nuanced fashion. The Governor has guided all along that he will not raise the policy rate until slack has been eliminated. That’s because the BoC holds its output gap framework nearer and dearer to its heart as a guide to expected sustainable future inflation than some other central banks. In the wake of the Q2 GDP disappointment, the mild negative revision to Q1 GDP and the need to lower their Q3 GDP forecast from 7.3% in the July MPR to several percentage points lower, the BoC would need to materially revise its potential GDP estimate lower to offset the implications for wider economic slack to this point than previously expected and yet the Governor lacked conviction toward this when he recently stated that there are good reasons to adjust estimates of potential GDP in both directions. It may punt material amounts of growth into future quarters and still indicate closure of spare capacity by 2022H2 which would be a signal to markets they are offside pricing for a hike by April.

Furthermore, the credibility of the BoC’s forward rate tool is at stake. The Governor needs to think ahead to the strategic implications into future shocks if he were to suddenly hike despite slack in the economy. Recall that one of the powerful ways in which monetary policy worked far better than the BoC imagined during the cycle was because households believed guidance that rates would be on hold for years. That guidance has already been brought forward materially to 2022H2. If the BoC violates its own guidance now, then perhaps no one will believe them in future downturns. If it hikes with slack still prevalent, it risks a dumpster fire around its whole exit framework with markets potentially seeing the BoC as spooked enough to bring forward even more aggressive rate hike pricing.

Still, that hikes are coming seems inevitable. Canada is a world leader on vaccination rates and will become more so with the kids slated for vaccination likely toward year-end. Jobs have been fully recouped and perhaps the unemployment rate is already below estimates of structural unemployment amid nascent evidence of wage pressures. GDP is forecast to fully recover the pandemic hit by the end of this year. Mild further fiscal stimulus may be forthcoming in a combination of the Fall statement and the Winter budget. Canada is turning away from lockdowns toward alternative pandemic-management tools like vaccine passports, vaccine requirements and restricted entry. The country is also benefiting from a strong gain in the terms of trade.

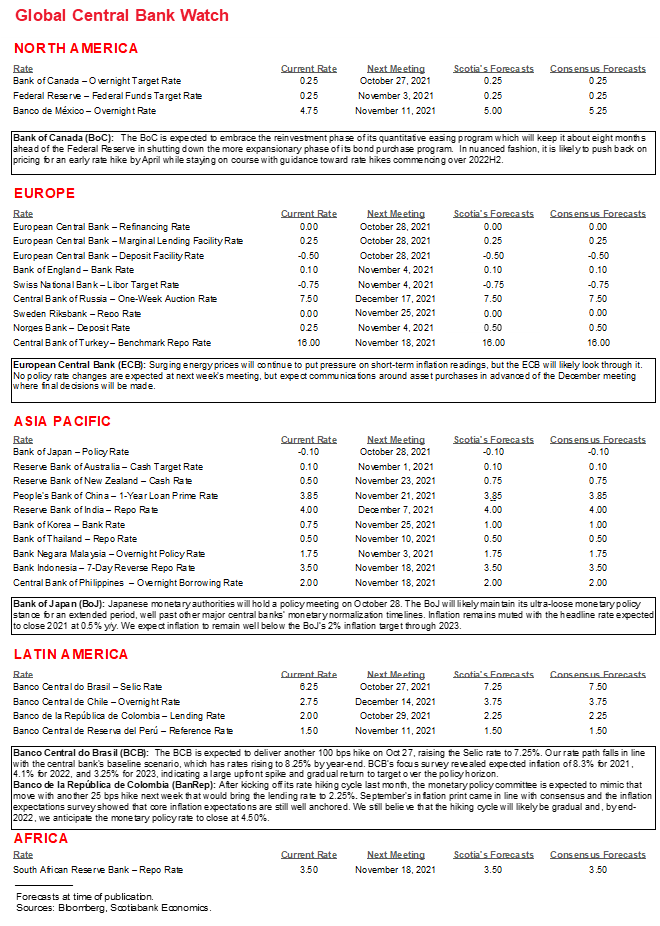

Still, for an explicitly inflation-targeting central bank, it’s the 2% that matter the most, so to speak. Rather, it’s the BoC’s 1–3% flexible inflation target range that is in focus. Back in July, the BoC forecast that inflation would rise to 3.5% y/y 2021Q4 and yet inflation will probably land around a percentage point higher. With our current forecasts of 2.9% y/y in 2022Q4 and 2.7% y/y in 2023Q4, we also think the BoC needs to raise its inflation forecast from 2% in 2022Q4 and 2.4% in 2023Q4, but it may be unlikely to go quite that high while burying its reaction function in the inflation profile.

The trillion-dollar question concerns when/if the BoC expects supply chain and reopening pressures on inflation to ebb, and when it forecasts capacity constraints to take over in setting a floor to inflation rates. The Governor is likely to re-emphasize his view that inflation will take a while longer to cool, but that supply chain and reopening effects (and idiosyncratic drivers in my opinion) will dissipate around a similar time frame to when a Phillips curve set of inflation drivers takes over in keeping the BoC sustainably on its inflation target. By the time it has that conviction, it’s likely to be later than markets presently think.

If so, then the BoC is already in run hot mode, likely to stay there for a little while longer, but when it has greater confidence that more durable inflation drivers are ahead, it is likely to withdraw the punchbowl at a fairly rapid clip. Like potato chips, one or two rate hikes would leave any inflation-targeting central bank’s hunger unsatiated. To be meaningful, the first stage of the hike cycle is likely to involve a rapid move off the lower bound through a meaningful number of initial hikes.

OTHER CENTRAL BANKS—TESTING LAGARDE

The ECB decision on Thursday could be the most significant meeting to global markets. It is fairly widely expected that President Lagarde will lead an effort to push back on pricing for hikes to the -0.5% deposit rate. At present, markets are pricing most of a 10bps hike by next summer, though a return to a zero rate is well down the road (chart 3). Expect lots of talk of base effects, transitory drivers and slack in terms of its inflation logic going forward.

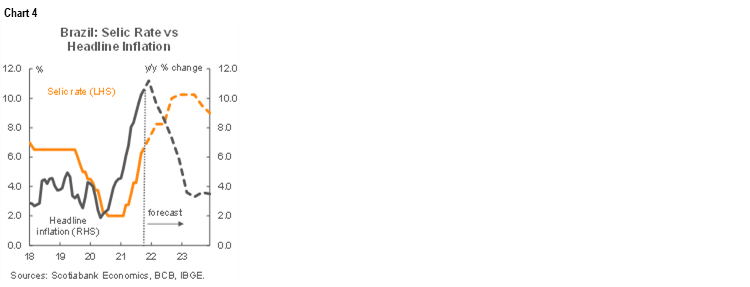

Brazil’s central bank is expected to hike its Selic rate from 6.25% by another 100–150bps on Wednesday. Inflation has climbed to 10.25% y/y which is the fastest pace since early 2016. Scotia expects the Selic rate to peak at just over 10% by the end of next year (chart 4).

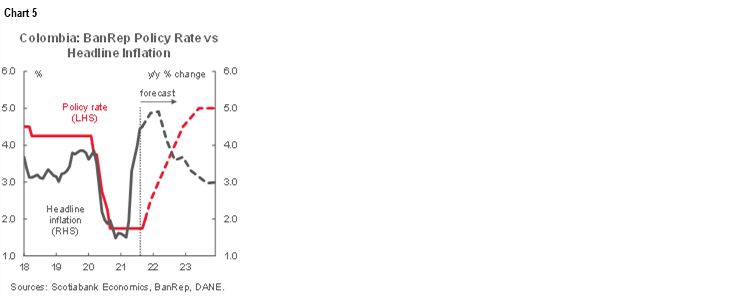

Colombia’s central bank is also forecast to raise its policy rate by another 25bps on Friday and set up a further likely hike of the same magnitude at the December meeting. Though it is running at a fraction of Brazil’s experience, inflation has climbed to 4.5% y/y with core at 3.0% which puts inflation above BanRep’s target range for headline inflation at 3% +/- 1%. Scotia forecasts the policy rate to peak at about 5% (chart 5).

The Bank of Japan is very likely to do little to nothing whatsoever later in the week at Thursday’s meeting.

EARNINGS—BIG NAME RISK

Earnings season intensifies across multiple jurisdictions. I’ll focus on the US and Canada.

157 S&P500 firms release Q3 earnings in what could be among the most important weeks of the prolonged season alongside the kick-off that was around financials. Breadth fans out into key names and segments whose surprises can impact multiple asset classes including names such as Facebook, Twitter, Alphabet, GM, Ford, eBay, Starbucks, Amazon, Merck, 3M, UPS, GE, Boeing, Caterpillar, Apple, Mastercard, Microsoft, Visa.

North of the border brings out 36 Canadian earnings releases by TSX-listed firms including names such as Shopify, Bombardier, Shaw, SNC, Fortis, West Fraser.

MACRO REPORTS—WHAT IS US CONSUMER CONFIDENCE TELLING US?

The round-up of global macro readings on tap for next week is skewed toward a collection of GDP and inflation figures from across multiple regions, and there may be intensified interest in US confidence figures this time.

US releases will be fairly light but a few will be worth watching:

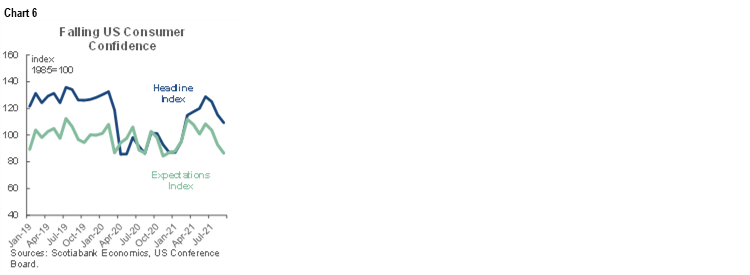

- Consumer confidence: The October reading from the Conference Board lands on Tuesday. It has been declining and this has sparked some concern over risks to the economic cycle (chart 6). Some, such as the authors of this paper, think its decline presages a US economic downturn. They point to how declines in the consumer expectations component predict downturns up to 1½ years in advance of their occurrence. They go on to argue that the decline in expectations suggests the US economy “is entering recession now even though employment and wage growth figures suggest otherwise.” Some of the media coverage left out the last bit! Having said that, it seems a stretch to me to argue that confidence gauges may be as useful now as the authors observe in the past. Developments during the pandemic have been highly distortionary. For instance, perhaps confidence overshot earlier this year when stimulus cheques were flying in multiple rounds and the decline of late is toward something that is still off the pandemic bottom but more realistic. Second, perhaps confidence is weak because of real and/or perceived inability to secure goods to buy amid damaged supply chains. Successive waves of COVID-19 infections could also be whipsawing confidence and lessening its reliability as a gauge of future economic activity. If COVID-19 cases wane, confidence could well recover and this gauge could be back to predicting an economic boom….

- GDP (Thursday): the first estimate for US Q3 GDP growth arrives on Thursday. We’re a touch above consensus at 3½% q/q annualized growth.

- Inflation (Friday): The Fed’s preferred PCE inflation gauges for September arrive on Friday. They should broadly follow CPI with an estimate headline increase of 0.4% m/m that would lift the year-over-year rate to 4.5% while core inflation rides at 0.2% m/m and increases a tick to 3.7% y/y.

- Income and spending (Friday): Income growth probably faltered in September (0% m/m). The main estimated culprit is the elimination of the extra $300/week of supplemental jobless benefits for the remaining (mostly red) states that had not already opted out of the supplemental payments. It’s unclear if reduced supports will benefit job acceptance rates, but the experiment may have been interrupted by the Delta variant such that if cases continue to decline then it may become a purer experiment. Chart 7 shows estimated income gains over the duration of the year with the caveat that wild stimulus-fed swings have seriously swamped the y-axis! Spending probably grew at a healthy clip given the known gain in retail sales plus estimated growth in services spending.

- Durables (Wednesday): Durable goods orders probably fell by ~1½ % m/m in September in part based on steep declines in aircraft orders and ongoing challenges in the auto sector. Core orders (ex defense and aircraft) are estimated to have risen for a seventh consecutive month.

The US will also update new home sales for September (Tuesday) that should get a lift from a rise in model home foot traffic, the Richmond Fed’s manufacturing gauge (Tuesday), pending home sales (Thursday) and the advance merchandise trade balance for September (Wednesday).

Canada updates GDP for the month of August and provides tentative guidance for September. August GDP was previously guided to rise by 0.7% m/m. Apart from details and possible revisions to the August guidance, the new information is likely to be more concentrated upon September GDP. We know that hours worked were up by 1.1% m/m which is a strong positive for GDP defined as an identity that multiplies hours worked by labour productivity that is in turn defined as output per hour worked. As far as activity readings that could inform productivity, we need value added by sector and can only point to a limited subset of readings for a general flavour of what happened to GDP growth. Those readings are heavily skewed toward the goods sector of the economy and include a 4.5% m/m drop in housing starts, flash guidance for a 1.9% m/m drop in the value of retail sales, a 3.2% m/m drop in the value of manufacturing shipments, and a 0.9% m/m rise in home resales that could lift some of the ancillary services. Still, there is limited ability to track large parts of the service sector which could support the gain in hours worked and jobs to the benefit of the September GDP estimate.

Mexico’s economic growth probably cooled in Q3, which we will find out about when Q3 GDP arrives on Friday. After solid non-annualized growth of 1.5% q/q in Q2 for the fourth straight quarter, growth is expected to largely stall out in Q3 but the trend amid choppy data is what counts.

Eurozone CPI for October is forecast to rise by about ½% m/m that would take the year-over-year rate up toward 3 ¾%, while core inflation is estimated to stay just under 2% y/y. Year-ago base effects are contributing to peak core inflation pressures now through to December before the year-over-year rate is likely to decelerate again into the new year. Germany and Spain update inflation the day before, while France and Italy update on Friday.

The first estimate for Eurozone Q3 GDP growth arrives on Friday. Growth is expected to be just over 2% q/q at a seasonally adjusted but non-annualized pace as the economy continues to rebound from the mild contractions over 2020Q4–2021Q1. Sweden also updates Q3 GDP on Thursday which is expected to rise by about ¾% q/q non-annualized.

Q3 inflation figures from Australia (Wednesday) are expected to maintain persistent pressure despite expected deceleration in year-over-year headline inflation. Central tendency estimates including trimmed mean and weighted median CPI are expected to rise by ½% q/q non-annualized and lift the year-over-year rates closer to the bottom end of the RBA’s 2–3% target range for headline inflation that is expected to pull back closer to 3%.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.