Next Week's Risk Dashboard

- Markets will monitor US holiday shopping

- Market pressures on the BoC risk reigniting inflation

- Canadian governments are driving inflation and rate hikes…

- …and cutting prematurely would embolden them to spend more

- Premature BoC cuts would worsen housing affordability

- Canadian federal fiscal update will probably heap on more spending…

- …but the provinces and municipalities are the bigger causes of inflation

- Canadian inflation to focus upon core gauges

- BoC’s Macklem to speak on inflation’s costs

- FOMC minutes will probably be stale

- PMIs to inform Q4 global growth

- Argentina’s election could create spillover effects

- Riksbank may hike again

- So will Turkey’s central bank

- Chinese banks to leave LPRs unchanged

- RBA minutes will probably be stale

- Bank Indonesia might hike

- SARB expected to be on hold

- Global macro

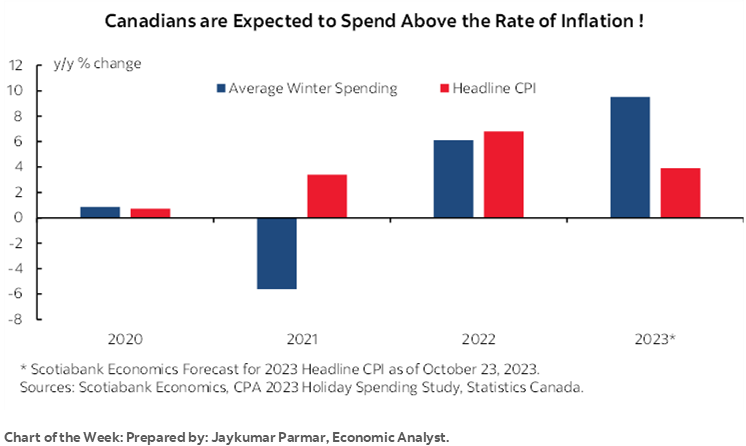

Chart of the Week

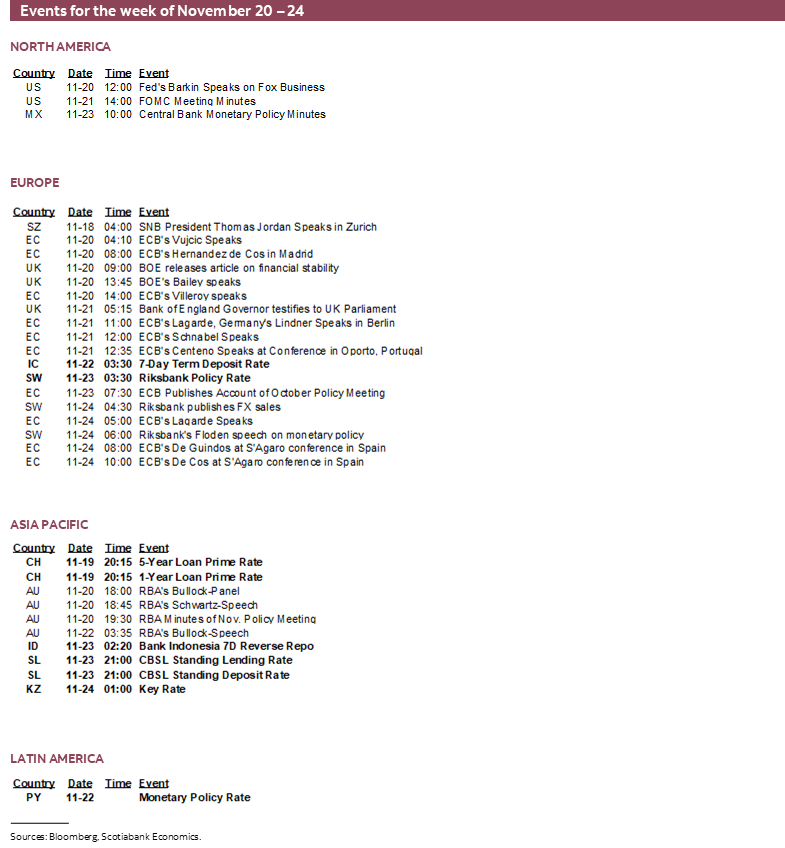

Global markets will primarily focus upon how the US holiday shopping season is kicking off and hence how the US consumer is behaving as an important driver of world growth. FOMC minutes, a round of global purchasing managers’ indices, potential spillover effects of Argentina’s election upon neighbouring markets, several regional central bank decisions, and a few other data gems are also on deck.

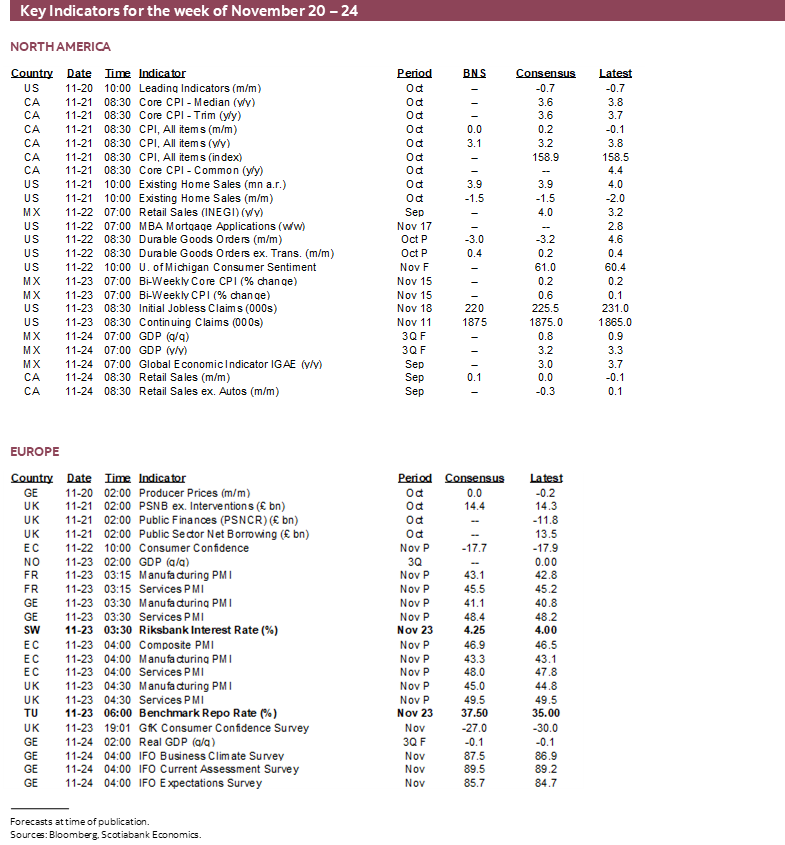

Canada will be a focal point in what could be an intense two days of price action on Tuesday and Wednesday before local markets experience a drop off in liquidity as the US goes on its Thanksgiving break. CPI, a Federal Budget update and then a potentially key speech by BoC Governor Macklem will pack in a fair amount of new information to the nearer term outlook. Some may be looking for the overall takeaway to drive an emboldened belief in pricing near-term rate cuts. That risks being highly premature and making the pain incurred to date having been all for naught if only to reignite the pressures that have driven inflation to date while trend core inflation gauges remain too hot. Canadian market developments this week may be a test of what faces other global central banks into 2024.

CANADIAN INFLATION—KEY WILL BE CORE READINGS

Canada updates CPI for the month of October on Tuesday morning. It’s the last inflation report before the BoC’s next decision on December 6th sans MPR. It could set a new trend in the gauges that matter, or light them up again and with potential consequences for the policy bias.

I’ve estimated that headline CPI will land flat (0% m/m NSA) and at -0.1% m/m at a seasonally adjusted rate. That’s not the figure that will matter though.

Headline is likely to be dragged lower by a 0.3% weighted NSA drag from lower gasoline prices while food prices will probably offer little net effect.

What will matter is the month-over-month trimmed mean and weighted median measures of CPI. Forget the year-over-year rates that don’t capture the freshest information as they compound weighted m/m price changes over the full twelve-month period. I once tried to forecast these measures, but that is next to impossible to do in the way that matters most which is to predict the m/m rate of change in the average of those measures at a seasonally adjusted and annualized rate. Models that seek to forecast change in these measures over time have wide forecast bands around them and are totally unsuited toward predicting shorter-run variations.

The problem is that the calculations are extremely sensitive to the price that lands at the 50th percentile of the 55 CPI components (weighted median) and to exactly what should be lopped off the 20% top and bottom of the basket (trimmed mean). We just don’t have adequate information on the 55 price components going into it, let alone how they may have been revised.

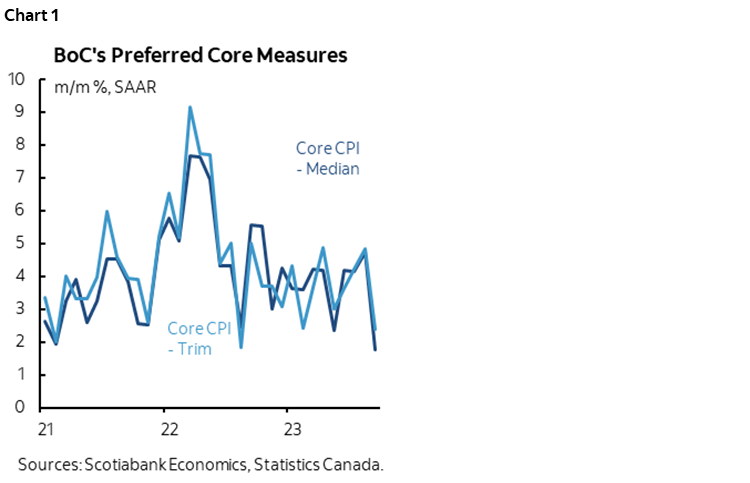

Chart 1 shows how volatile these measures have been. September’s readings fell back to 1.75% m/m SAAR and 2.4% m/m SAAR for weighted median and trimmed mean respectively. While it didn’t happen immediately, the days after that prior release saw Canada’s front-end become richer as the two-year GoC yield fell from about 4.9% toward under 4½% now. That reversed the market whippiness around the prior prints for August released on September 18th that landed at about 4 ¾% m/m SAAR for both measures and drove a sharp increase in the two-year yield.

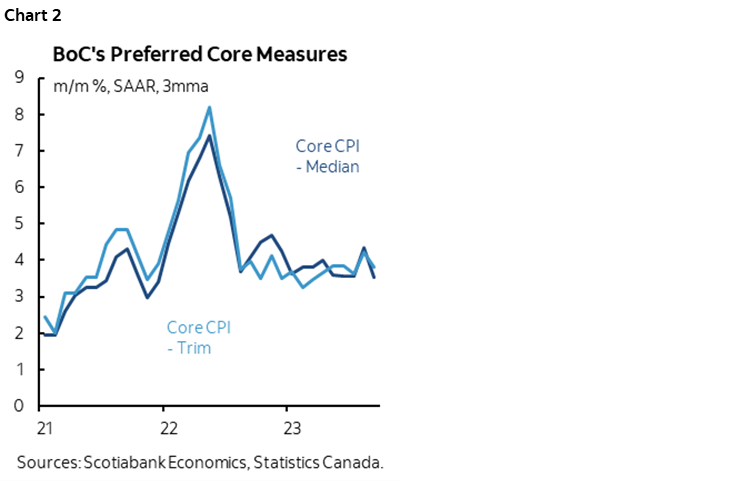

Markets are overly sensitive to the latest readings in both directions. They need to look at trends as the BoC tends to do. On that count, the three-month moving average of the m/m SAAR rates of increase in these measures are shown in chart 2. They average at 3.7% which is progress compared to peak rates of increase in the 6–8% m/m SAAR range through the Spring of 2022, but hardly light and still well above what is necessary in order to give the BoC confidence that it is moving toward sustainably achieving its 2% headline inflation target.

WILL BOC’S MACKLEM LEAN AGAINST EASING EXPECTATIONS?

The CPI update will be taken alongside other evidence on the path to the next BoC decision such as the November 30th Q3 GDP print and the next day’s update on growth in jobs and wages during November plus market developments.

In the meantime, however, BoC Governor Macklem will weigh in the day after CPI with a speech titled “The cost of high inflation.” This will land at 11:30amET and will be followed by a full press conference at 1pmET. He didn’t choose as his topic mortgage resets or a soft economy or any such allusions. He chose high inflation and its costs as the focal point which is probably an immediate tip with respect to the tone.

This has spawned all manner of speculation toward why the Governor has chosen to weigh in with a speech with that title the day after CPI and the Fall budget update. The possibilities may include the following points.

The BoC has a lot of economists and access to information including through Statcan economists and perhaps they are bracing for an upside surprise. That could make it an opportune moment at which to reinforce inflation concerns.

The opposite case is that perhaps they expect a weak print and wish to lean against markets getting too far ahead of themselves on pricing rate cuts.

An entirely different (and more reasonable imo) possibility is that the Governor wants to dissuade markets from being so obsessed with the latest readings. The Governor won’t lock horns with markets in any specific way, but he may speak to the magnitude and duration of evidence that is required before giving the BoC enough comfort to pivot. To date, that guidance has been that they expect inflation to arrive at 2% over 2025H2 and may begin easing in advance of this in a way that implies perhaps as soon as 2024H2, but probably not Springtime.

A further possibility is that Macklem will be speaking the day after—in fact, hours after—Minister Freeland delivers the government’s Fall fiscal and economic update. Macklem wagged a finger at governments for spending so much and making his job more difficult in his last press conference. If Freeland adds yet more spending as is likely, then perhaps he’ll escalate some of the concern.

What Governor Macklem may indirectly seek to do is to lean against market pricing for rate cuts to begin arriving within the next 4–5 months as markets are pricing. Cutting so soon would be a terrible policy error in my view.

To cut that soon means teeing it up in advance and hence driving a further richening of 2s and 5s on the path between now and then. A lower 5 year GoC yield would flow through mortgage rate cuts. That would be right into two very seasonal things if one knows anything at all about Canada.

Winter Budgets

Macklem just wagged a finger at Federal and provincial governments for current plans to grow spending and complicating the job of getting inflation on target. A recent piece by Scotia Economics (here) reinforces the magnitude of rate hikes that have been required to counter the inflationary consequences of government spending at all levels but particularly by provincial and municipal governments, some of which have been sharply critical of the BoC’s rate hikes. To then set up a cut as they are delivering Budgets from about February to April/May would send a signal to governments not to worry as much about their interest expense and projected bond yields.

One of the ways in which monetary policy works to tighten conditions and to bring inflation lower is to raise interest expense for the public sector and dampen its other spending. To reverse this would light up that other spending that needs no such help—especially with a Federal election looming some time by October 2025 and with the current government sharply down in the polls. Governments may not like it—as indicated by their sharp political criticisms of the BoC—but I expect the Governor to show his steely resolve toward cooling inflationary pressures on all fronts including run away government spending.

The Spring Housing Market

To set up a cut by March/April in advance would put downward pressure on the 5-year fixed mortgage rate through the mortgage pre-approvals season commencing around 2024Q1. Good one. Repeat what they did last year with the premature pause that contributed (along with the US regional banking crisis) to the 5s rally and lowered fixed mortgage rates. That lit up the Spring housing market, putting further pressure upon household affordability and broader inflationary pressures. The BoC came back and hiked twice more right after.

This time the consequences could be more severe. One reason is that the Feds are adding housing stimulus and with higher transfers and subsidies likely on the way this week. Another is that we've had two years of excessive immigration into a housing market with no supply.

Mortgage Resets

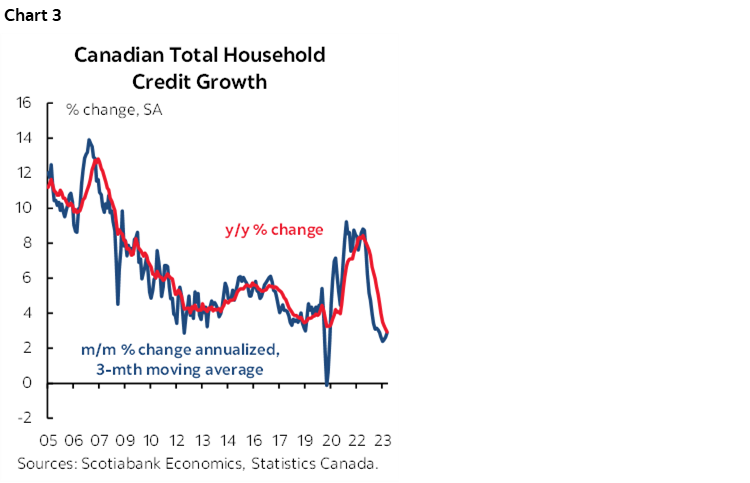

Some suggest that cuts will be required to address coming fixed rate mortgage resets and because household credit growth has slowed (chart 3). It has been similarly slow before and yet I think a flaw to that thinking is that the whole purpose of tighter monetary policy is to cause some pain in order to bring inflation durably lower. To then turn around and say ‘just kidding’ and deliver rate cuts would set the country back in its fight against inflation. If cuts prematurely reignite debt growth then all of this will have been for nothing and the regressive inflation pain will persist for longer and for the people who can least afford to deal with it.

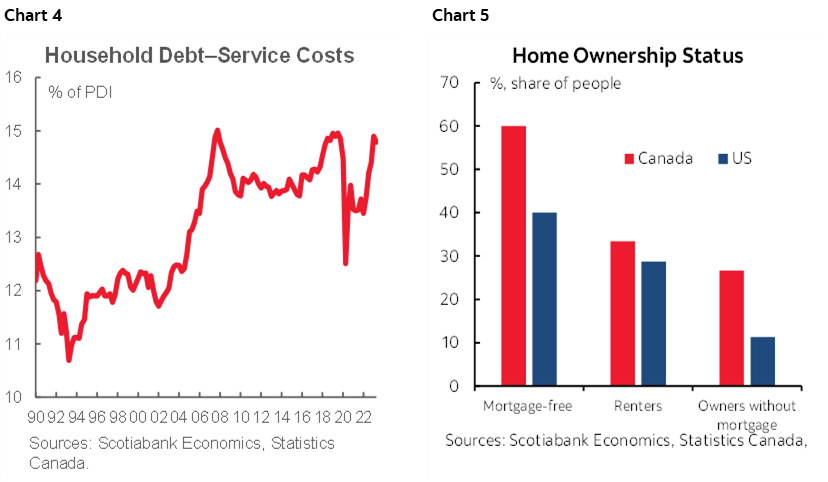

What impact may mortgage resets have upon the share of personal disposable income going toward total debt payments? At present, the share of PDI going toward all interest and principal payments on all types of household debt is about 15% (chart 4). 60% of households don’t even have a mortgage in Canada which is much higher than in the US (chart 5). I figure that this share of PDI spent on debt payments will rise to the high teens, depending upon what happens to wage growth that has been strong, and to mortgage rates that are bound to eventually come down even if not just yet. That’s a few percentage points higher from here but I cannot stress this calculation to be remotely close to some of the absurd claims that I’ve seen others making. In fact, I think some of them slipped by putting the decimal point on the change from here one spot too far to the right!

Consequences of a Policy Error

So now let's say they do cut by March/April and tee it up before then and play devil's advocate. Beyond the above points, what else could be the consequences?

I think it would be a policy error that would be followed by one of two things. The lower probability scenario following such a cut would be to have to come back and reverse it later when they realize what they've done in setting back progress toward lower inflation. The higher probability scenario would be to thwart chances at further, deeper cuts later. I'd rather they take their time, be patient, set a very, very high bar for timing cuts so that they can really deliver them later, rather than cut too early and potentially less later or never again.

All the while the relative central bank risks remain slanted toward greater trend inflation risk in Canada going forward than elsewhere in my opinion. This isn’t just a one-trick-pony mortgage resets narrative. I haven't seen anything to change that broader narrative that includes the following points.

BoC surveys continue to show unmoored inflation expectations at 3%+ for years to come. This is changing behaviour which makes it difficult to durably get inflation down to 2%.

As evidence of changed behaviour, wages are ripping at among the fastest pace anywhere, whether trend m/m SAAR average hourly earnings or wage settlements. One-third of Canada's workforce is unionized and still going through collective bargaining exercises cementing wage gains at 2–3 times the BoC's 2% inflation target for years to come. 10% unionization in the US. Pass through into other non-unionized sectors in Canada still awaits in a "hey, me too!" sense. IMF research supports this.

Productivity is downright shameful. Rapid wage growth and falling outright productivity reinforce one another in terms of inflation risk. Unit Labour Costs are skyrocketing.

Company pricing behaviour remains slanted toward passthrough. What nobody talks about is how this is occurring at the small business level that dominates the business community in Canada. Anecdotally every time I turn around I’m stunned at the price hikes that small businesses and the trades are passing through, but politics is solely focused upon large companies.

Fiscal policy remains excessively stimulative across all federal and provincial governments combined.

CAD remains undervalued.

The terms of trade remain supportive, including via energy prices. This serves as an imported positive income shock.

Supply chains remain pressured. They've improved on the industrial production side, but not in autos and housing where inventories are lean and these are the two biggest things most households buy.

Corporate balance sheets remain solid which is a support for job markets. So is the dominance of public sector hiring (one out of two jobs created since the pandemic began) absent any hint at fiscal austerity.

All tallied up, I continue to think the market is prematurely pricing cuts and still think there is excessive confidence that hikes are over. If it were me, I’d honestly keep hiking especially if markets continue to ease financial conditions at the pace at which we’ve been seeing of late; that risks setting us back to square one in the inflation fight and having to endure greater pain for longer.

CANADIAN FISCAL UPDATE—CONFUSING SUPPLY AND DEMAND

Canada’s federal government delivers its Fall economic and fiscal update on Tuesday. Expect more spending and lots of doublespeak. Prudence will be used to curiously describe lots of excess. A supply side focus will be emphasized to describe distorting subsidies in the billions of dollars.

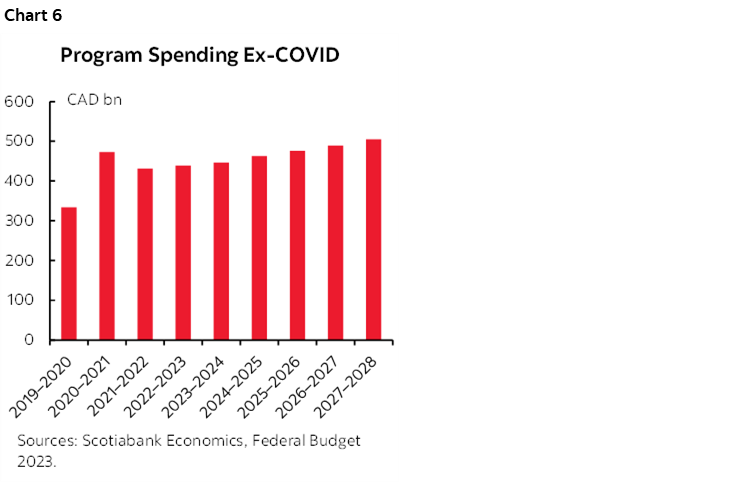

Even if not one further budgeted dollar of spending is added, there is still higher spending ahead. Micro efficiency goals won’t change that. Chart 6 shows the prior budget’s plan to increase program spending excluding COVID supports. From the pre-pandemic fiscal year of FY19–20 to the current one, spending was slated to increase by 105%. By FY 2028, program spending is projected to rise by a cumulative 170% over FY19–20 levels even if no further spending is added to this projection beyond what this past year’s Budget projected.

More spending is likely, along with bigger deficits. Minister Freeland has indicated that there will be a focus upon housing affordability with further housing measures including subsidies, and upon making lives more affordable which may mean more transfers and admonishing companies for allegedly driving inflation.

Further, the government has to incorporate new spending announcements since the last Budget including the aggressive settlement with striking Federal civil service workers earlier this Spring, subsidies to makers of batteries for electric cars at an enormous cost per job created to dubious benefit, and higher interest expense. At least the pharmacare program appears to be shelved for now as not even the NDP that supports the idea expects further developments at this time.

This update will be billed as being about 'supply, supply, supply' when more spending and excessive immigration levels are more about ‘demand, demand, demand’ that adds to inflation risk and with that BoC hike risk.

US HOLIDAY SALES—MORE SERVICES THIS TIME?

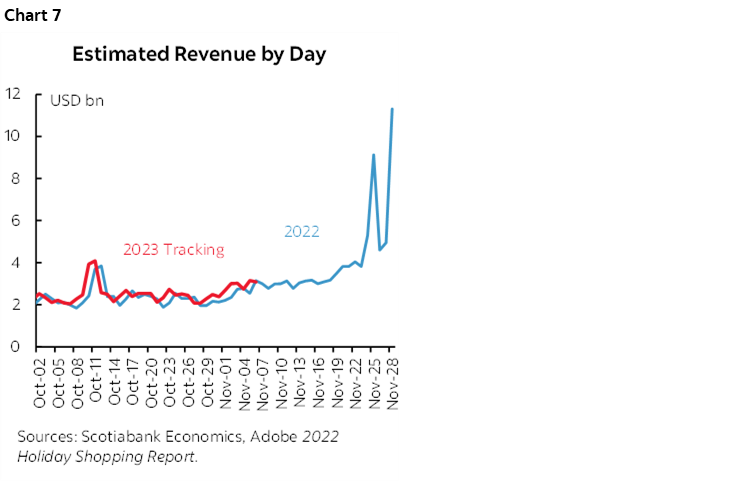

Eat, then shop. The great annual American tradition starts with Thanksgiving on Thursday. Markets may be sensitive to early sales tracking toward the end of the week and into the following week both at the individual company level and in broader terms while assessing the durability of consumer spending. So far, 2023 sales revenue is tracking closely to 2022 on a year-to-date basis (chart 7).

More retailers are opting not to open on Thanksgiving this year, but some will. Then Black Friday and Cyber Monday may inform holiday shopping momentum. US markets will be closed on Thursday and the bond market will close at 2pmET the following day.

The National Retail Federation forecasts nominal sales growth of just 3–4% y/y (here). They say they base this forecast upon an economic model related to jobs, wages, confidence, incomes, and consumer credit while weather may be a wildcard especially given the relatively strong El Niño this year. If they’re right, then this implies little to no growth in inflation-adjusted terms.

It’s also possible that this holiday season will be more about experiences and services spending versus goods spending notwithstanding the relatively balanced growth in these types of spending of late.

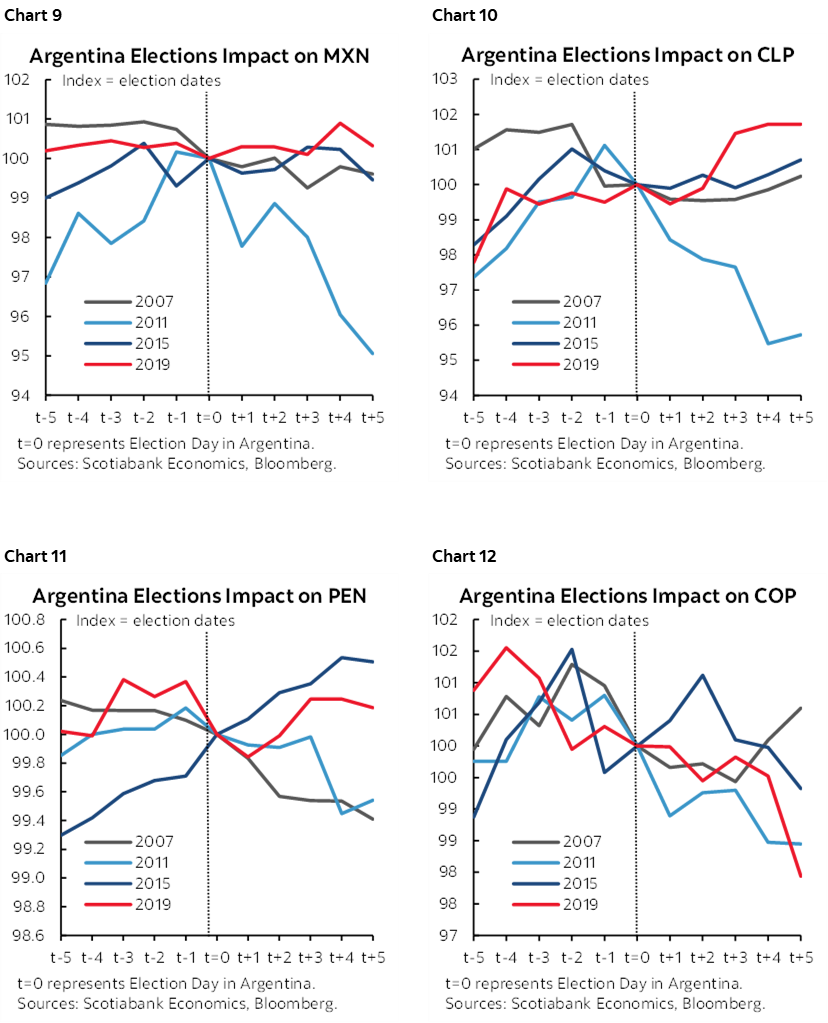

ARGENTINA’S ELECTION—SPILLOVERS?

Argentinians go to the polls again on Sunday to choose a President in the final run-off election. The two candidates offer radically different options and whomever ‘wins’ the prize will inherit a mess.

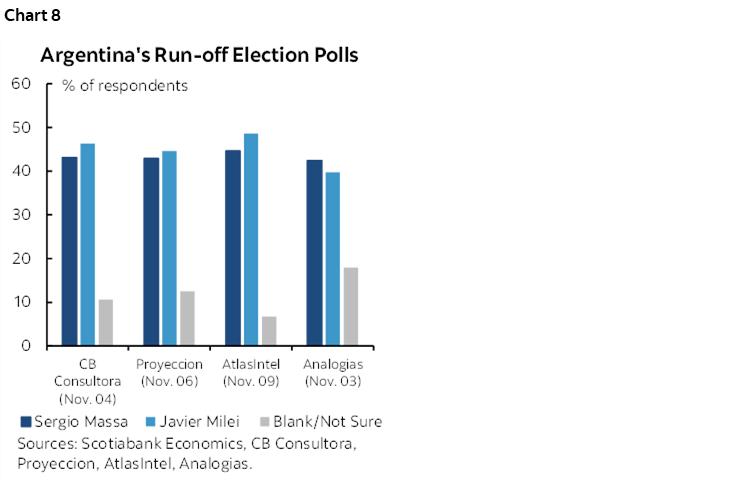

All three major polls are indicating that the libertarian candidate, Javier Milei, will be victorious over Sergio Massa, an economy minister in the current Peronist government (chart 8). Massa is offering much of the same that the current administration has been delivering. Milei would be a radical experiment if he follows through on abolishing the central bank and the currency in favour of using the dollar. The short-run market effect may evolve into something very different over time as either scenario is expected to be following by high risk of another default.

Most of our clients—and certainly my employer—probably have little interest in the direct outcome. I’m not sure we can say that so confidently about the potential short- and longer-run ripple effects upon other LatAm markets and the broader EM space. Charts 9–12 show what happened to some of the regional currencies following prior elections in Argentina. The election in 2011 brought in the left of center Front for Victory and President Cristina Fernández de Kirchner in a landslide victory and then announced foreign exchange controls to try to control capital flight. The result was to drive other regional currencies to appreciate to the dollar as one example of ripple effects.

CENTRAL BANKS—HIKES ON THE FRINGE

Global central banks will offer mostly regional market risk with probably little spillover across global markets. Several developments are briefly highlighted below.

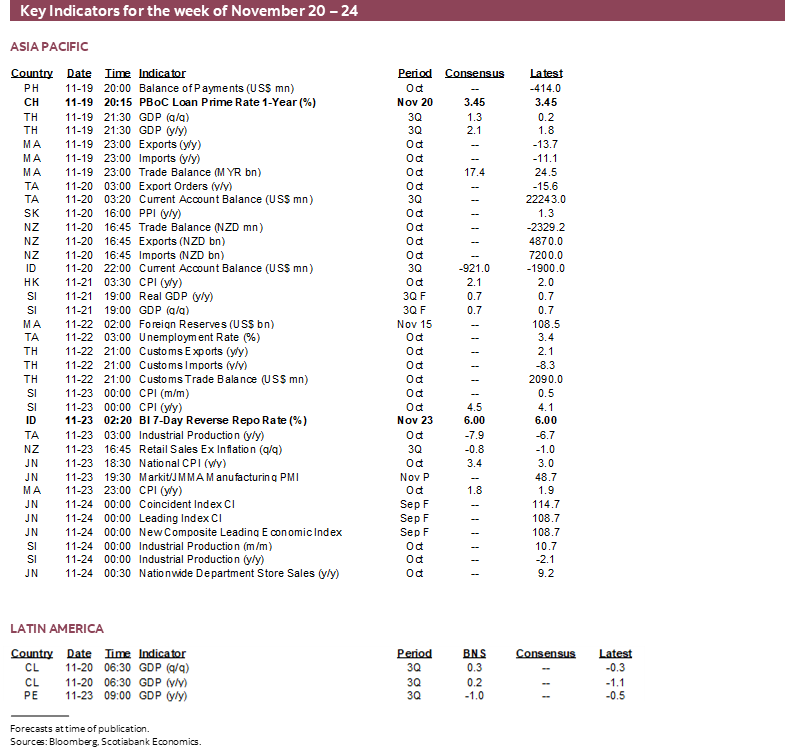

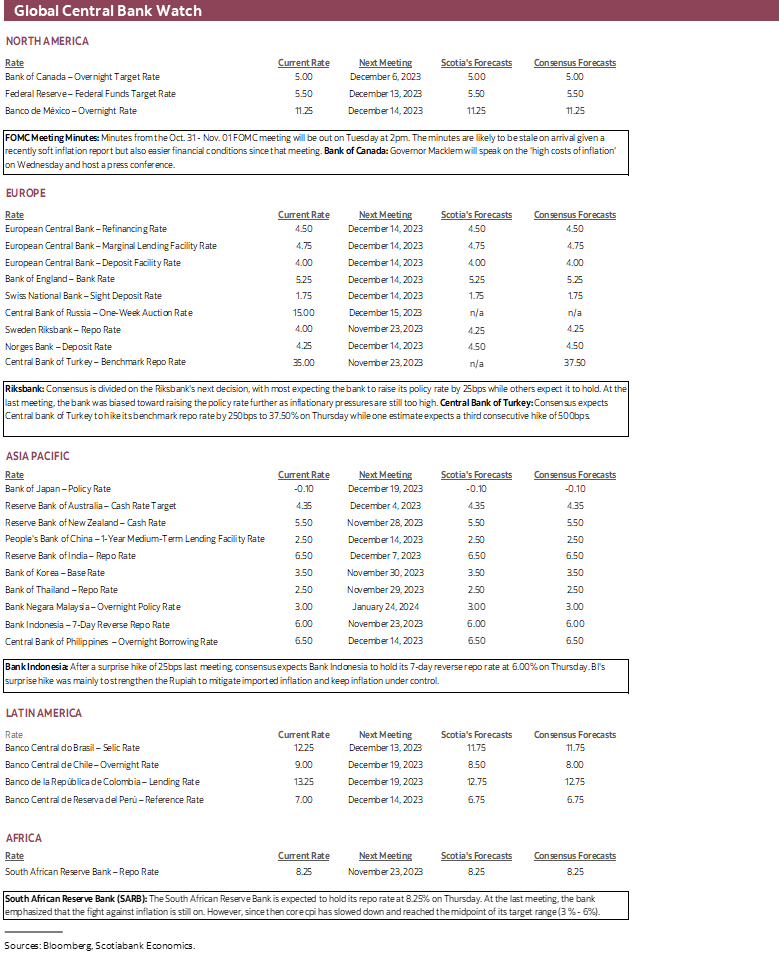

- China (Monday): After the PBOC recently held its Medium-Term Lending Facility rate, China’s banks are expected to leave the 1-year and 5-year Loan Prime Rates unchanged at 3.45% and 4.2% respectively.

- RBA minutes (Monday): Recall that the RBA hiked by 25bps on November 7th. The minutes are likely to offer further explanation of the reasoning. They may be somewhat stale, however, given the strong rise in wages during Q3 and the 55k increase in employment that occurred since that meeting.

- FOMC Minutes (Tuesday): A recap of what happened at the October 31st – November 1st meeting is here. The minutes may be stale after the market reaction to the recent CPI reading (recap here). The FOMC is likely keeping their powder dry to come back with a more substantive update on December 13th when they deliver their next decision along with a full forecast update including a fresh ‘dot plot’.

- Bank Indonesia (Thursday): A minority thinks that BI could hike its 7-day reverse repo rate 25bps to 6.25% in a continuation of the bias that sparked a surprise hike on October 19th. Inflation recently jumped to 2.6% y/y in October from 2.3% previously but with core inflation dipping to 1.9% y/y.

- Riksbank (Thursday): Consensus is split with just under half expecting a hold at 4% and just over half expecting a 25bps hike and there is also uncertainty over whether balance sheet plans will be adjusted to accelerate to pace of unwinding.

- SARB (Thursday): No policy rate change is expected on Thursday with the rate expected to remain at 8 ¼%.

- Turkey (Thursday): Another big rate hike is expected. By how much is anyone’s guess for an exceptionally volatile central bank dealing with a protracted currency crisis. The one-week repo rate presently stands at 35%.

GLOBAL MACRO—US, JAPAN LEADING THE PACK

The rest of the week’s line-up of macro indicators will be short but potentially impactful.

The monthly wave of global purchasing managers’ indices will inform Q4 GDP tracking, supply chain developments, hiring appetite and pricing pressures. Only the US and Japan are still in positive growth territory, but modestly so as their composite PMIs remain just above the 50 dividing line. Australia kicks it off on Tuesday followed by Eurozone and UK on Thursday and then Japan and the US S&P (not ISM) gauges on Friday.

Other than CPI, Canada will only update retail sales for September and October on Friday. Statcan already provided advance guidance on September’s tally when, on October 20th, they said sales were “unchanged.” While this report will fill in greater detail and possible revisions to the September tally, the new information is more likely to be focused upon advance guidance for October’s sales.

Given the holiday-themed week, US markets will face little by way of economic data to consider. Existing home sales for October (Tuesday) will probably post a small dip based upon softening pending home sales. Durable goods orders are expected to dip partly as Boeing’s plane orders dipped to a still high 123 in October from 224 in September. Weekly initial claims are due out on Wednesday instead of the usual Thursday given the holiday and will be monitored for signs that the recent mild increase isn’t the start of a trend.

A few countries will update GDP figures. Chile’s economy is expected to post low growth of 0.3% q/q SA nonannualized on Monday (0.2% y/y). Peru’s economy is expected to continuing contracting in year-over-year terms at -0.9% (Thursday). Norway is expected to stay on the plus side at 0.8% y/y (Thursday). Germany will revise Q3 growth that was initially reported at -0.1% q/q SA and fill in the details (Friday).

Japan’s national CPI reading for October will probably follow higher the already-released Tokyo measure on Thursday. Recall that the Tokyo core CPI measure climbed to 2.7% y/y (2.5% prior) but was soft in month-ago seasonally adjusted terms at +0.1% m/m.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.