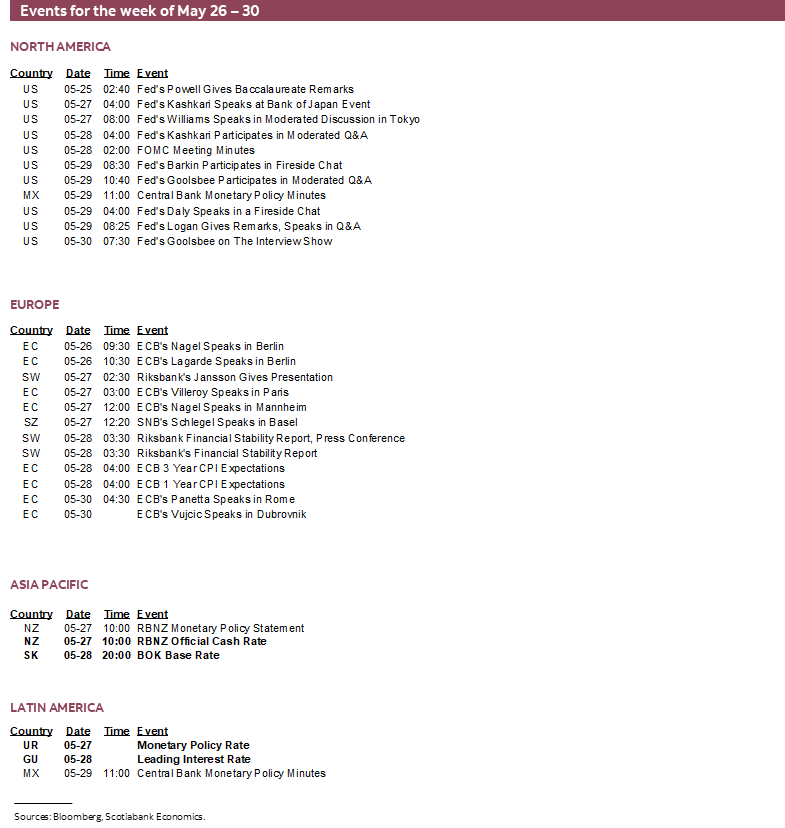

Next Week's Risk Dashboard

- Trade risks move to front and center again…

- …as the US Budget bill will take months to resolve

- OPEC+ to entertain another production cut

- US core PCE: Higher, and lower

- Canada’s Throne Speech may contain a few more policy nuggets…

- …that buy time until Fall

- Canadian GDP could continue to demonstrate resilience, for now

- Why Canadian core inflation is sticky

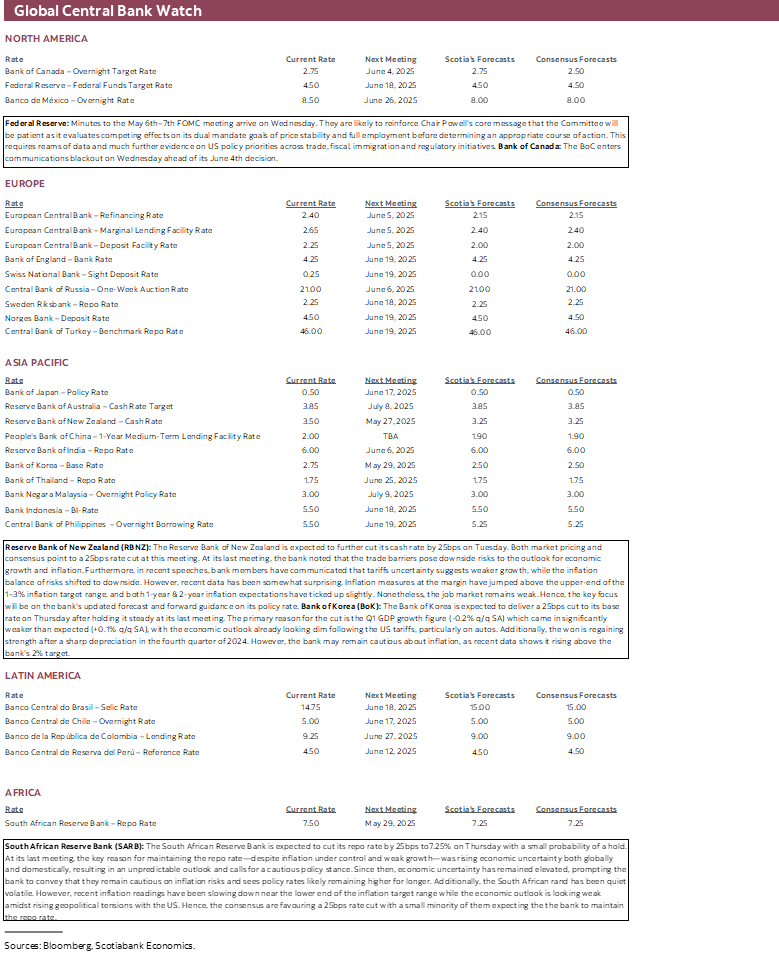

- FOMC minutes to repeat patience

- Eurozone core CPI expected to cool

- Tokyo core CPI is on a hot streak

- Aussie CPI likely to further embolden RBA’s cut

- RBNZ to cut

- BoK going for an even 100

- SARB to cut after rand benefits from Ramaphosa’s discipline

- Other global macro

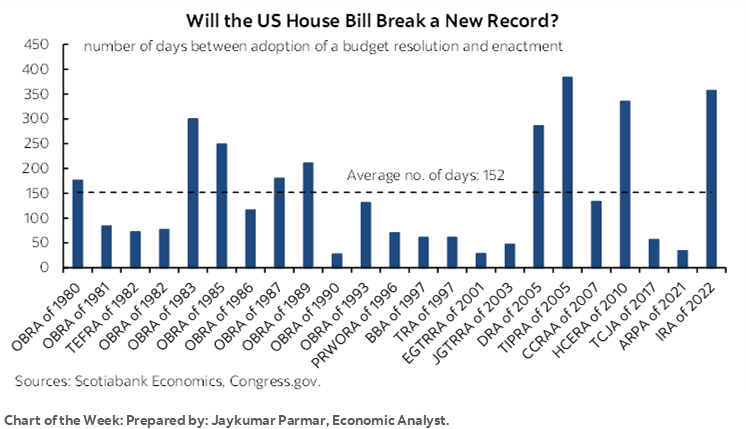

Chart of the Week

Americans may need the Memorial Day long weekend to rest up ahead of an active week for global developments!

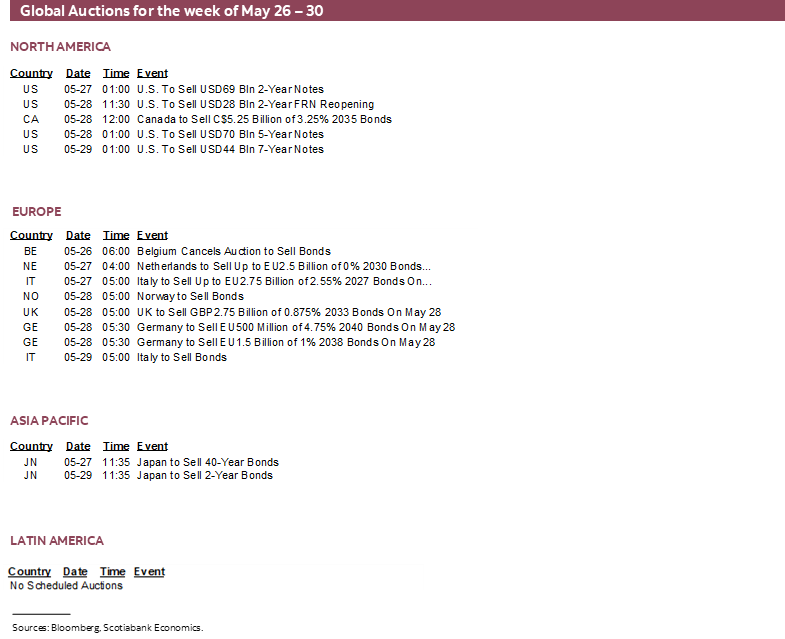

Off-calendar risks are omnipresent and could include further escalation of US-Europe trade wars after Trump’s threat to impose a 50% tariff on June 1st. The pivot coincides with entering fiscal policy limbo as the House budget reconciliation bill now faces a deeply skeptical Senate that will drag out next steps over coming weeks. Jay Parmar’s chart of the week shows how long budget reconciliation bills take to go from adoption to enactment; buckle up, it’s going to take a long while from here. These folks estimate that the House bill would lift GDP by a cumulative 0.4% over ten years, thus severely challenging the administration’s false claim it would raise growth rates to 3%, and they estimate that the bill widens deficits by US$2.8T (ie: doesn’t pay for itself) and in highly regressive fashion.

Plenty of calendar-based risks could lie ahead as well. One is the OPEC+ virtual meetings on Wednesday to review production quotas over 2025–26 that may result in cutting production targets for July at the full meeting on June 1st. Each of the US, Eurozone, Japan and Australia will update inflation readings. Three regional central banks may deliver cautious-sounding rate cuts as the FOMC minutes continue to signal patience and the BoC goes into blackout. Canada’s economy will be a focus on Friday, but what to do about risks to the outlook and sovereignty will be the focus of Tuesday’s Speech from the Throne to open the 45th session of the Canadian Parliament. Shall it be the King, or the Edmonton Oilers that unite Canadians?

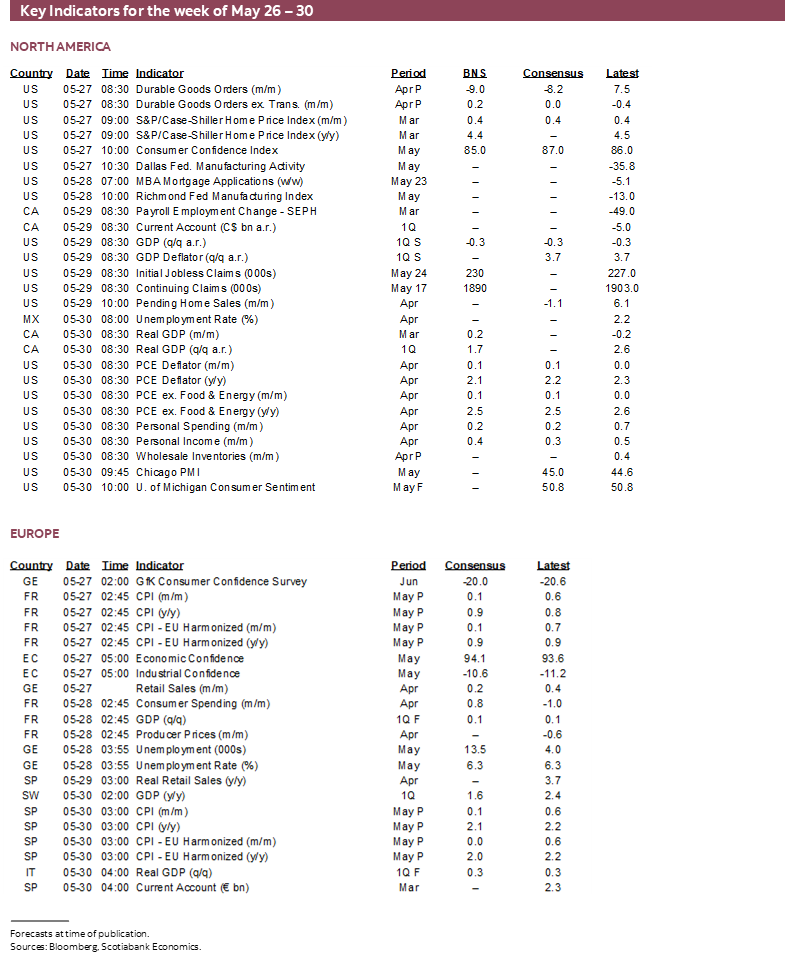

GLOBAL INFLATION—INFORMING PATIENCE

A quartet of inflation readings will sweep across major world markets this week. For the most part, they are likely to remain relics of a bygone pre-tariff era, but they could incrementally inform central bank scorekeeping on the path toward evaluating much more important readings in future months and quarters. The readings out of the US, Eurozone, and Japan are not expected to result in nearer term policy implications while the Australian update is likely to merely reaffirm the RBA’s cut.

US PCE—Higher, and Lower

Friday brings out the FOMC’s preferred inflation readings—the price deflators for total consumption and core spending excluding food and energy.

Headline and core PCE prices are expected to be up by 0.1% m/m SA. That would land them both a tick below CPI and core CPI. One reason is that a little will be shaved off the CPI estimates by virtue of the different weights used on components in PCE versus CPI. Another reason is that the components from the producer price index that are included in PCE but not CPI will also shave a little off the CPI readings upon translation into PCE.

The year-over-year rates would therefore land at 2.1% for total PCE (from 2.3%) and 2.5% for core PCE (from 2.6%).

A caveat is that there may be a slight upward revision to March PCE and core PCE stemming from upward revisions to PPI and core PPI measures. March PCE could be revised up a tenth to 0.1 and core PCE up a tenth to 0.1. That could be enough to lift Q1 core PCE revisions the day before up to 3.6% q/q SAAR from 3.5% initially, and total PCE up to 3.7% from 3.5%.

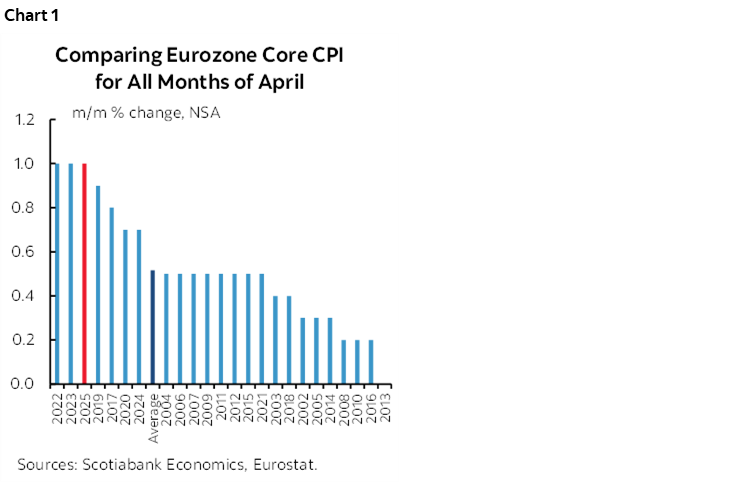

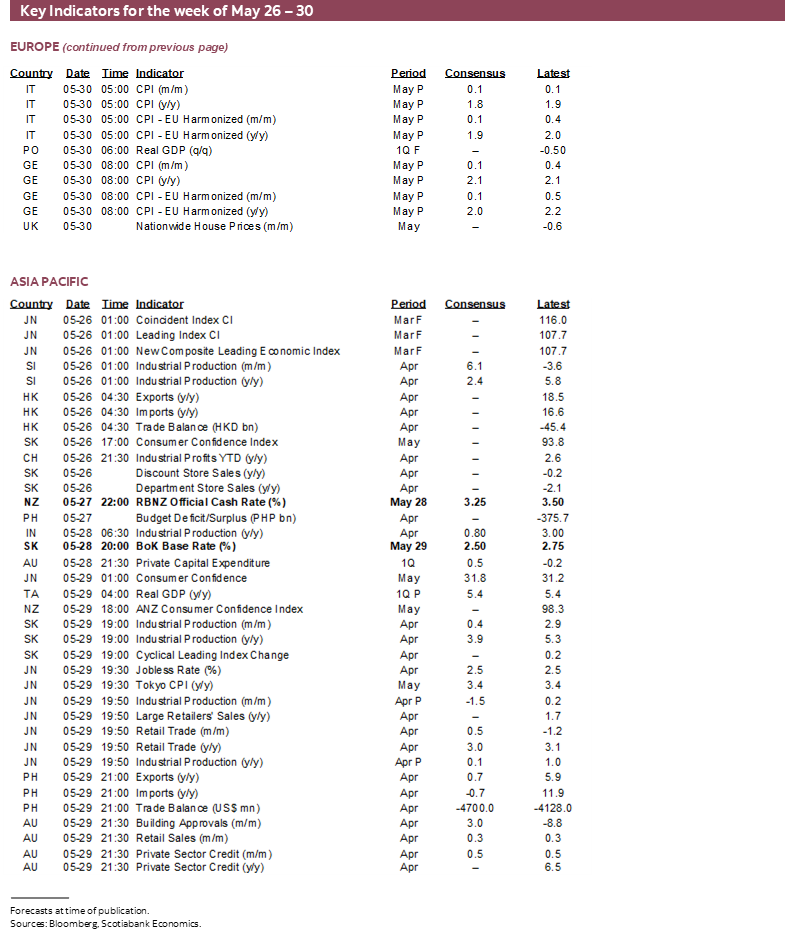

Eurozone CPI—A Stable Path Ahead?

The Eurozone tally doesn’t arrive until the following week, but by Friday we should have an advanced understanding of how May CPI is lining up for the whole of the Eurozone.

France kicks off the estimates on Tuesday and then Germany, Italy and Spain release on Friday. Cooler readings are generally expected compared to the prior month’s 0.6% m/m seasonally unadjusted surge.

It would take big surprises to impact pricing for about 50bps of ECB cuts through to year-end that would bring the policy rate toward 1.75%. Markets are priced for another 25bps cut on June 5th. Minutes to the ECB’s April policy meeting noted that “Inflation was expected to hover close to the inflation target of 2% for the remainder of the year.” The minutes noted that “uncertainty, the appreciation of the euro and the decline in oil and gas prices would further dampen the inflation outlook in the near term” but that “over the medium term, the picture for inflation remained more mixed.” The next ECB forecast update is expected with the June decision.

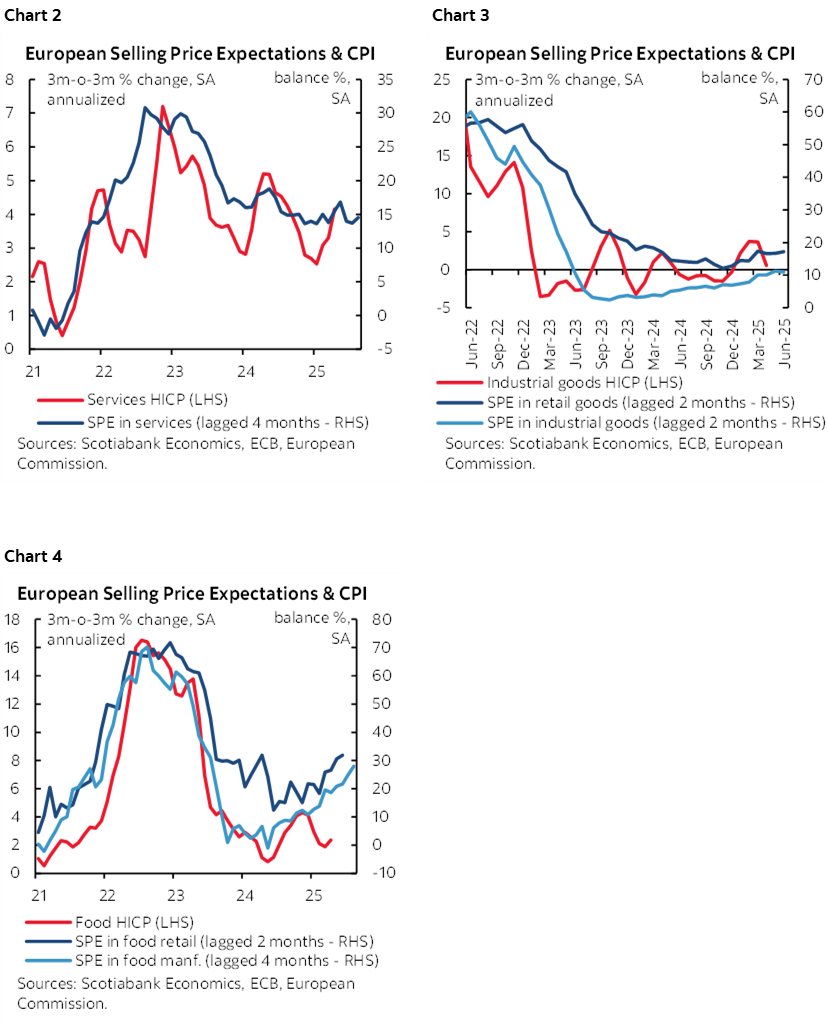

That said, core inflation in April was relatively warm ahead of May’s update (chart 1). Offsetting this in the minds of ECB officials is that the Commissions’ Business and Consumer Survey’s measures of selling price expectations generally point to little incremental near-term pressure outside of food prices (charts 2–4). Whether that remains the case significantly depends upon the course of EU-US trade developments. If Europe doesn’t retaliate, then further disinflation risk may lie ahead, whereas if it does, then greater imported price pressures could complicate the picture somewhat.

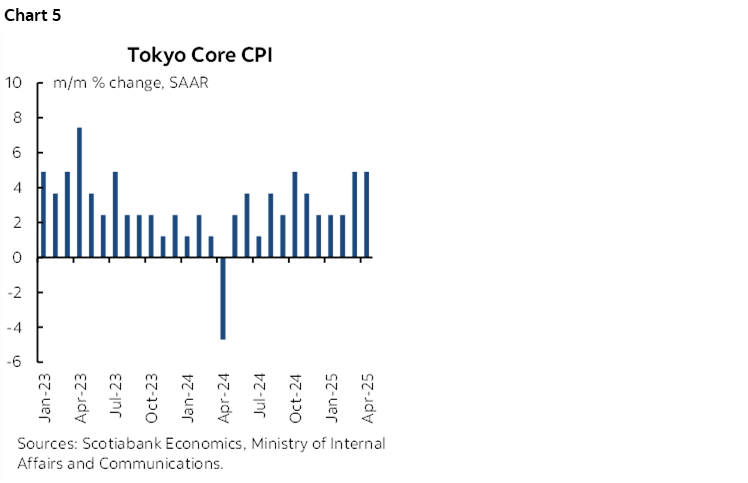

Tokyo CPI—Another Hot One Could Confront the BoJ’s Caution

Thursday evening’s (Friday in Japan) reading of the Tokyo CPI gauge for May could continue to buoy near-term inflationary pressures.

The April y/y core CPI measure jumped from 2.4% to 3.4%. It may fall back again this week, since the April jump was significantly driven by the year-ago cut to school fees that drove a low year-ago base effect.

That wasn’t the only driver, however, and key will be whether momentum in core CPI on a m/m basis is maintained. As chart 5 shows, Tokyo core CPI has risen by 4.9% m/m SAAR in each of the prior two months.

In any event, the BoJ’s increased caution toward the outlook presently means that nothing starts to be priced for a further BoJ hike until toward year-end.

Aussie CPI—Emboldening the RBA

The RBA’s recent 25bps rate cut could be further emboldened by Tuesday’s CPI reading for April. It is expected to drop again from 2.4% y/y the prior month. The next quarterly CPI figures for Q2 may be more influential when they arrive on July 29th in between the next decisions on July 8th and August 12th.

CANADA’S THRONE SPEECH—THROW BACK, OR A NEW ERA?

The last time a British monarch read Canada’s Speech from the Throne to mark a new session of Parliament was nearly a half century ago. PM Carney has resurrected the tradition as King Charles III will read it on Tuesday at around 11amET for up to half an hour.

Support for the monarchy in Canada is mixed at best (here). The symbolism of ties to the British Empire as insurance against Trump’s assaults was weakened by UK PM Starmer’s extension of open arms to Trump.

Regardless, some will question the message that kind of seems like ‘hey, we’re not a 51st state, we’re still a colony!’ The challenge to Canadians lies in asserting their identity in the modern era by not merely enslaving it anew to someone else.

Others may point to how the last time a British Monarch delivered this Speech—Queen Elizabeth II in 1977—the context was partly around sovereignty on the path toward repatriating the Constitution in 1982, although the government of Pierre Trudeau wasn’t especially enamoured of the monarchy.

Nevertheless, the Speech is a generally worded wish list that is high on platitudes and short on specifics in terms of the new session’s goals. Expect it to contain a symbolic nod of support to the former colony, and maybe there will be a focus on the King’s wardrobe and token Canadiana accoutrements. This is a good piece on the process and timing steps for the duration of the current sitting of Parliament that expires on June 20th.

There is only so much that the Carney administration has committed to delivering in the short-term before delivering a full Budget in the vaguely defined window of sometime this Fall. It’s possible that fiscal stimulus equates to 1%+ of GDP, thereby substituting fiscal policy easing for monetary policy easing. Ways and means legislation is expected to deliver Carney’s promised 1% tax cut to the lowest income bracket. Fiscal numbers have to be updated in the Government Expenditure Plan and Main Estimates (past issues here) and approved before skipping out for Summer; they will lay out funding needs and plans before the grander package of initiatives later.

That means that the outlines of policy priorities in the Speech are likely to be general in nature before presenting bills, debating them, and then passing them by Fall. Expect generalities on interprovincial trade barriers and broad fiscal policy plans.

A key emerging uncertainty is the plan for defence spending and how it fits into the government’s desire to strike a new economic and security arrangement with the US. The clear goal here is to tie Canada more closely to the US despite the rhetoric of how everything has fundamentally pivoted away from the US. Carney has committed Canada to achieving the NATO agreement of 2% of GDP spent on defence by 2030.

What’s unclear is whether this also includes recent ‘Golden Dome’ discussions with the Trump administration. Canadians have a right to know much more about the reliability of the technology behind an elaborate space-based missile defence system, the likely efficacy now and against future technologies, whether or not it would escalate geopolitical risks including through a new arms race or worse, and the costs. Yes, the costs. To date, all we know is that Trump has said Canada would pay its ‘fair share’—whatever that means. As previously explained in daily notes, this could be tens or even hundreds of billions of dollars and Canadians should know how the government would plan on funding such an initiative. Further, if this is the cost to getting the US to de-escalate tariff wars, then how much faith can Canadians have in any such agreement with the US given the erosion of the worthiness of the US signature?

CANADA’S ECONOMY—AND WHY INFLATION REMAINS STICKY

GDP for Q1 and the start of Q2 will inform the starting point for capacity pressures of relevance to the Bank of Canada before heading into the consequences of the global trade war that the US started.

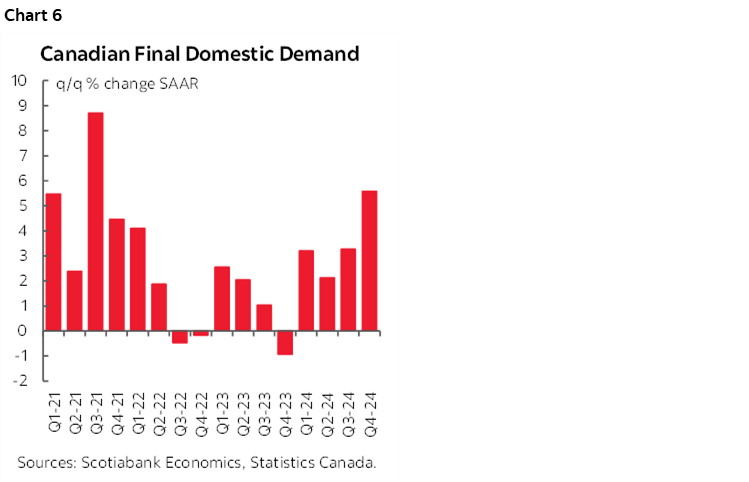

Q1 GDP is estimated to have grown by 1.7% q/q SAAR. March GDP is estimated to have grown by 0.2% m/m, or one-tenth quicker than Statcan initially guided with its preliminary estimate on April 30th. The preliminary estimate for April GDP will also be provided sans details, and is very tentatively estimated to have grown by 0.3% based on limited readings such as a solid gain in hours worked but also the possibility of a small and temporary lift from the election. You will want to remove inventory and import leakage effects to get around tariff front-running influences and focus on final domestic demand that was previously been trending strongly (chart 6).

If all that comes to fruition, then it could leave Q2 GDP tracking growth of around 1½% q/q SAAR.

The effects would mean that slack in the economy remained quite small. The output gap ended 2024 at around –½% of GDP. The BoC’s April MPR estimated that slack was between 0% and 1% in 2025Q1. One of the perennial difficulties lies in how to estimate the supply side, namely potential GDP.

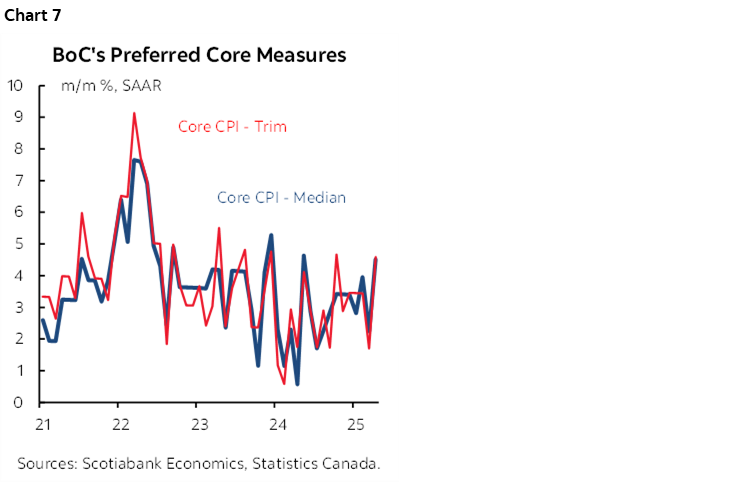

This view that there may be no, or very little slack in the economy, along with other arguments, could help to understand why core inflation remains sticky at elevated levels. There just isn’t enough disinflationary slack to be driving inflation lower, especially in light of the lagged effects. Gaps are often overstated drivers of inflation anyway in my view. April’s trimmed mean and weighted median CPI measures came in at about 4½% m/m SAAR and the trend has been too warm for a lengthy period (chart 7).

Other possible reasons for sticky inflation readings are as follows:

- Canadian monetary policy is roughly neutral, maybe either slightly restrictive or slightly stimulative based on a 2.25–3.25% neutral rate range. It’s feasible that the Bank of Canada has already gone a little too far with its policy easing which has been my bias for some time now.

- Depending upon how one defines the real policy rate, it has either fallen back toward estimates of the real neutral rate, or below if survey-based expectations are used.

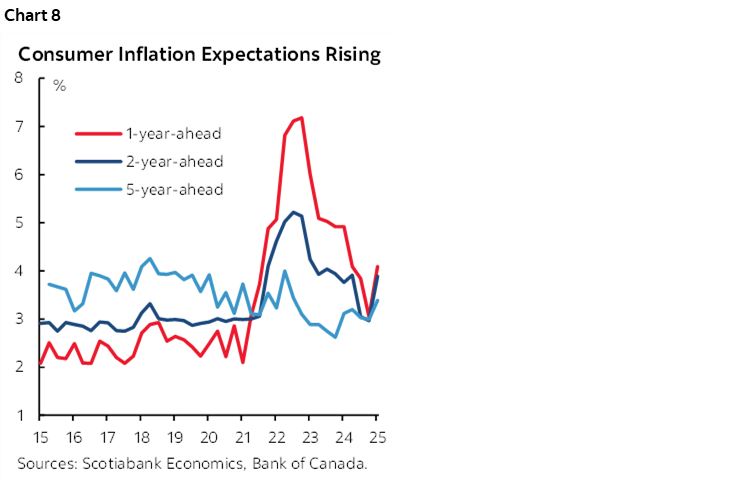

- On the latter note, inflation expectations remain high in Canada and there is evidence that when this is the case it’s more likely to perpetuate inflation risk (chart 8).

- fiscal policy continues to prime the pump in serial fashion and we expect stimulus measures in the near-term (like the Canada Day tax cut) will increase in a Fall budget. We could get stimulus equal to 1%+ of GDP.

- It’s not only capacity considerations in Canada that matter. The US economy remains in excess aggregate demand that gives pricing power to US exporters. The degree of integration of the Canadian and US economies means that passes across the border into still elevated inflation readings in Canada.

- Canadian consumption has been trending strongly and provided little to no reason to firms to ease up on prices. In inflation-adjusted terms, consumer spending grew by 3.6% q/q SAAR in 2024Q1, 1% in Q2, 4.2% in Q3, and 5.6% in Q4. Growth is likely softer to nonexistent now, but mainly on the goods side as services remain buoyant partly on a reallocation of travel budgets toward the domestic market.

- Increased border risk to global supply chains in a more fragmented world takes years to be fully incorporated, resulting in higher costs being passed on.

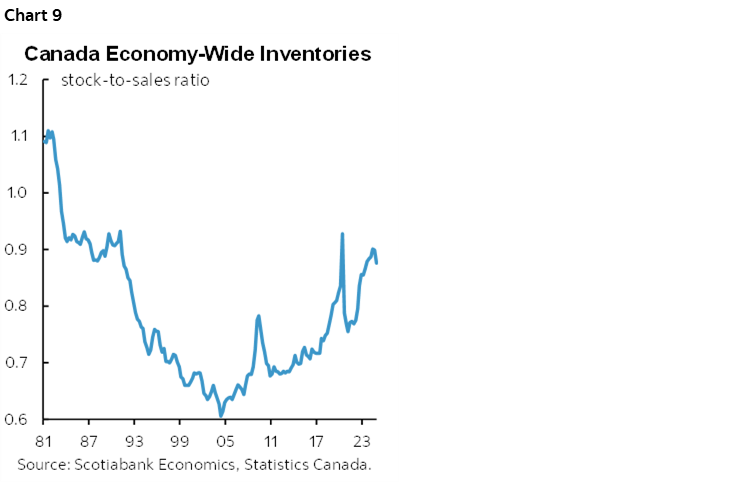

- As an offshoot of the supply chain argument, inventory buffers have been pushing higher and the costs are getting passed along (chart 9).

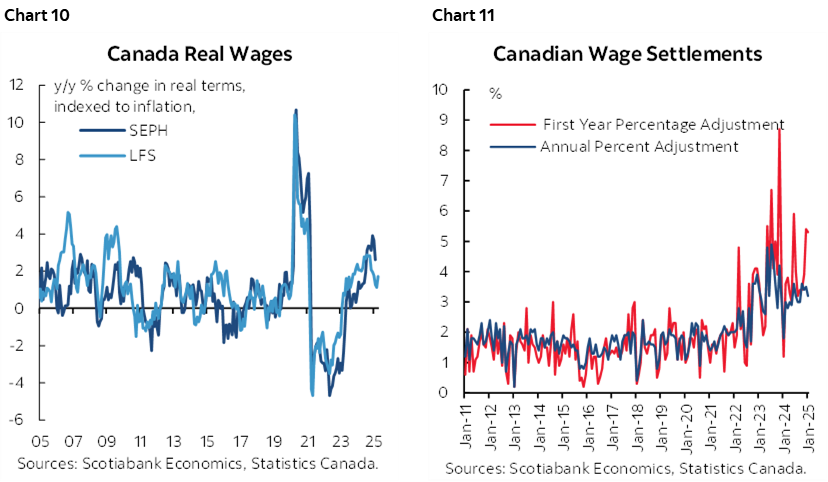

- wage growth is excessive relative to productivity growth and this may be part of what is passing along some of the effects into prices. Chart 10 shows various wage growth measures. Chart 11 shows wage settlements in collective bargaining agreements that are very important to Canada where about 30% of the workforce is unionized versus about 10% in the US. High wage growth and poor labour productivity growth combine to reinforce labour market supports for inflation.

- CAD depreciation passes through slowly with modest effects as USDCAD went from 1.20 in 2021 to 1.45 and back down to about 1.39 now. Each 10% trade weighted depreciation adds an estimated few tenths to CPI temporarily.

- Tariffs are a very recent influence and likely to roil inflation readings across N.A. as the effects ripple through supply chains, but it’s a big stretch to argue they have been meaningfully influential to date.

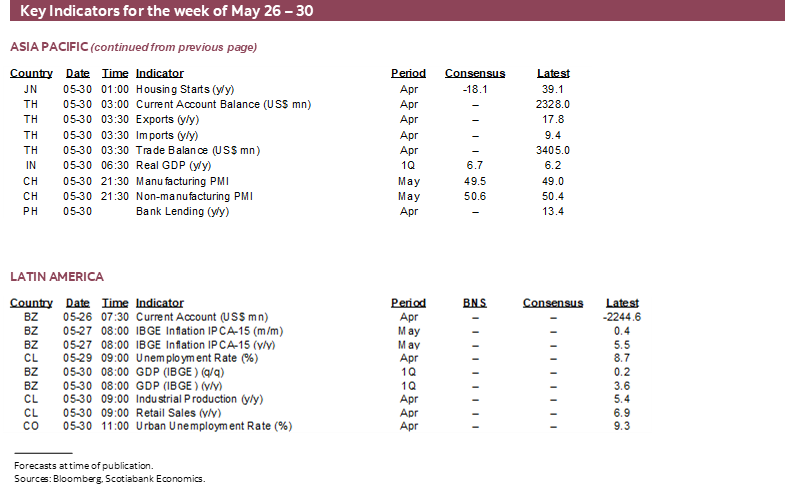

CENTRAL BANKS—REGIONALS TO EASE WITH CAUTION

Three regional central banks will weigh in with decisions this week as the Federal Reserve releases minutes to the May FOMC meeting minutes and the BoC goes into communications blackout ahead of its June 4th decision.

RBNZ—A Cautious Cut

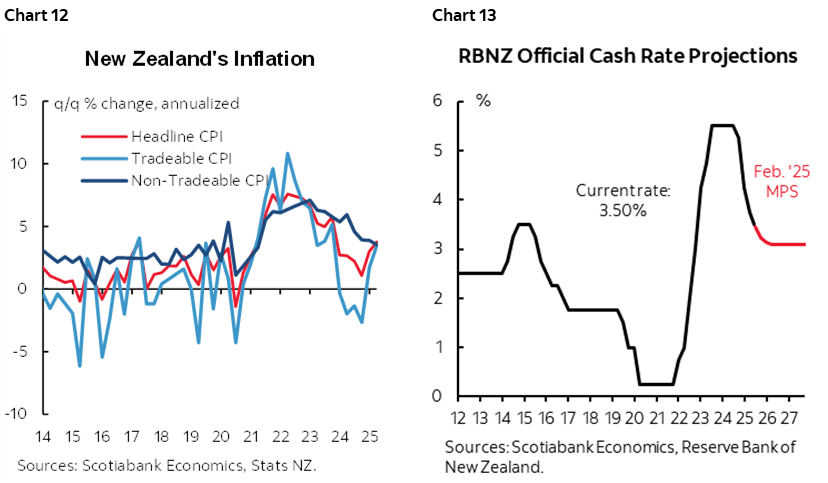

Markets and consensus are aligned toward expecting New Zealand’s central bank to cut by 25bps on Tuesday. Recent central bank remarks have mentioned that "the balance of risks has shifted to the downside" regarding inflation. This is entirely a forward-looking view partly on informed perspectives and one part on a lark. Q1 CPI figures were still quite warm (chart 12) while inflation expectations have edged up. We’ll get freshened forecasts including explicit forward guidance compared to the prior round (chart 13).

Bank of Korea—Going for an Even 100

Consensus unanimously expects another 25bps base rate cut from the Bank of Korea on Thursday. That would deliver a cumulative 100bps of easing since the BoK began to cut in October last year.

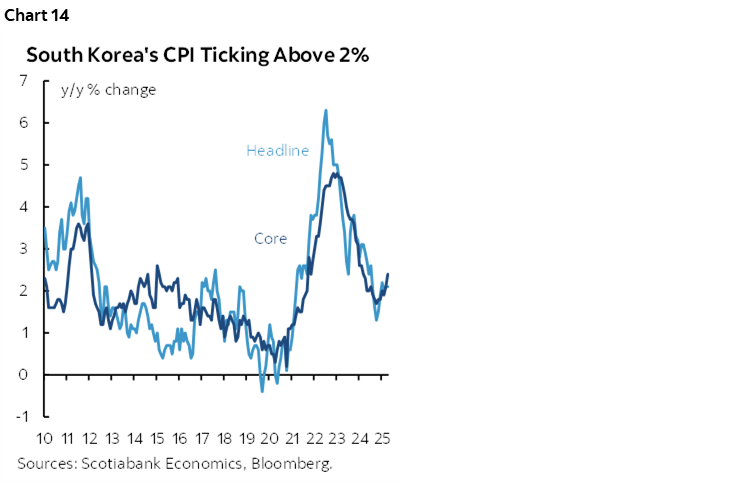

Expect forward guidance to be cautious if it does cut again after pausing at the prior meeting. Q1 GDP contracted by -0.2% q/q nonannualized, with the dip driven by manufacturing and construction while even services were flat. However, core CPI inflation has been back on an upswing over recent months to a still modest 2.4% y/y ahead of the fuller impact of US-motivated global trade wars on domestic inflation (chart 14).

SARB—Much Has Changed

Most expect the South African Reserve Bank to cut 25bps to 7.25% on Thursday. A minority expects a hold. A slight weakening of core CPI inflation to 3% this past week may have tipped the balance to a cut as it extends the downward trend over the past two years. A great deal has changed in the world since the last decision way back on March 20th when SARB held. The rand has slightly appreciated since then and readings like retail sales and manufacturing output have been weakening. Trump’s deplorable ambush of President Ramaphosa this past week was based on distorted and false facts, but Ramaphosa showed composure and discipline that supported the currency whereas he could well have turned the spotlight back on US race issues.

FOMC Minutes—Counting the Ways to Say ‘Patience’

Minutes to the May 6th–7th FOMC meeting arrive on Wednesday. They are likely to reinforce Chair Powell's core message that the Committee will be patient as it evaluates competing effects on its dual mandate goals of price stability and full employment before determining an appropriate course of action. This requires reams of data and much further evidence on US policy priorities across trade, fiscal, immigration and regulatory initiatives.

OTHER GLOBAL READINGS

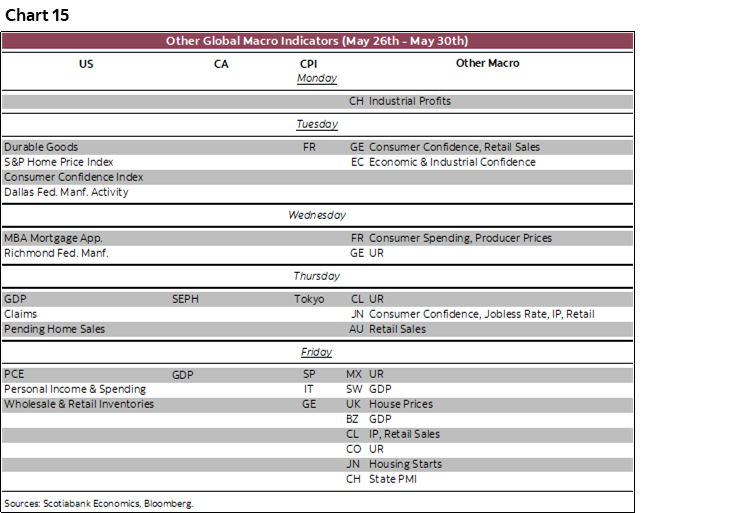

Chart 15 summarizes the rest of the global line-up of releases not already covered.

Key US highlights will be Friday’s US consumer spending figures that are expected to be weak alongside decent income growth, Tuesday’s consumer confidence figures that may dip again, and Tuesday’s durable goods orders.

Relatively minor other gauges will mainly emphasize consumer spending figures for April such as Australian retail sales (Thursday), Japanese retail sales (Thursday), French consumer spending (Wednesday) and maybe German retail sales.

China refreshes the state’s PMIs shortly after this note is being published.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.