Next Week's Risk Dashboard

- Renewed debt ceiling theatrics

- Missing balance in Canada’s mortgage debate

- CDN fiscal Q2 bank earnings due

- The BoC is in a race against the clock

- FOMC minutes could inform pause versus hike bias

- RBNZ to hike again

- BoK, BI and Turkey to extend pauses

- SARB to hike again

- Global PMIs to inform growth tracking, inflation risk

- US core PCE is still sticky

- UK inflation still breaking records?

- Tokyo CPI to inform BoJ pivot risks

- US consumer spending backed by income gains

Chart of the Week

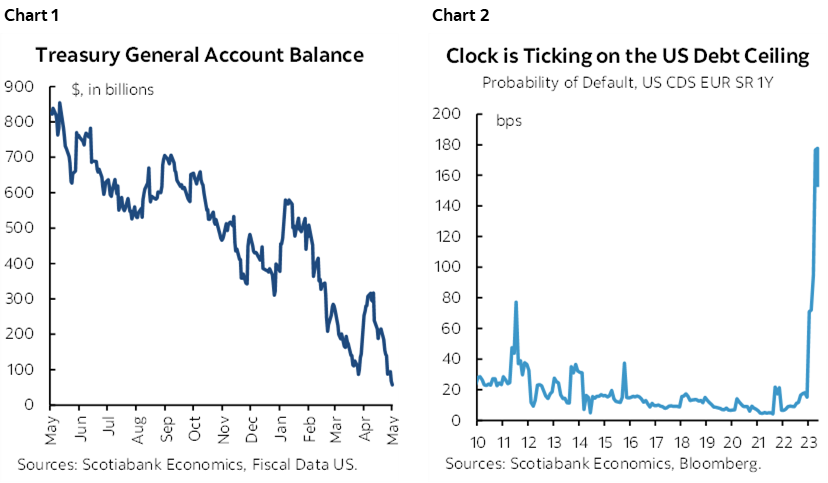

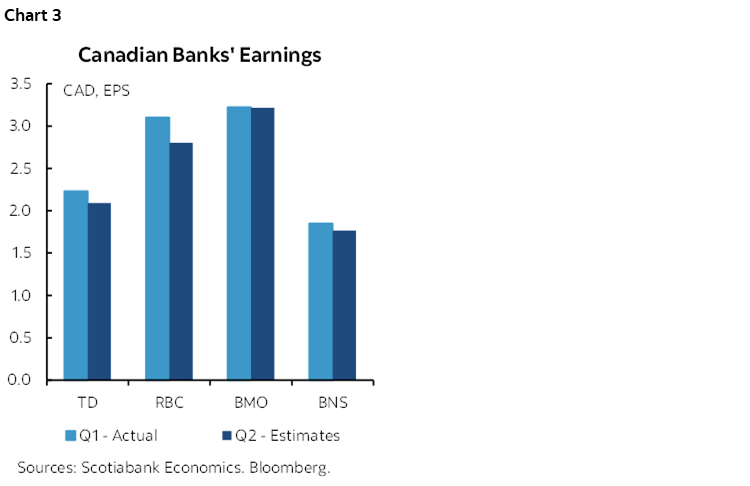

The coming week will place much of the focus upon debt ceiling negotiations in Washington. It is the last full week during which to strike an agreement and have enough time to pass votes in the House of Representatives and the Senate before Treasury Secretary Yellen’s June 1st marker on the calendar, after which the potential risks and difficult decisions intensify. Negotiations stalled as this past week drew to a close because Republican members of the negotiating team walked out. The US Treasury’s cash position is rapidly falling (chart 1) as the cost of insuring against default on US government debt obligations remains high (chart 2).

Otherwise, the calendar of catalysts for potential swings in global markets will be relatively light with the focus upon FOMC minutes, Canadian bank earnings, a select few regional central banks, and a modest number of top shelf macro indicators.

CANADIAN BANKS—APPLYING BALANCE TO MORTGAGE AND HOUSING RISKS

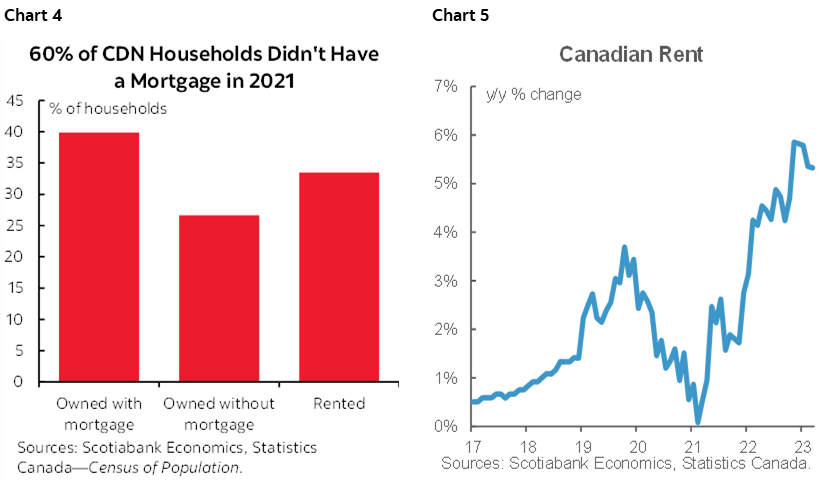

Canadian banks will release earnings reports for their second fiscal quarters with most of the action arriving on Wednesday and Thursday.

Chart 3 compares Q1 and Q2 earnings per share in the seasonally unadjusted way of reporting the figures. BNS (my employer) kicks it off on Wednesday in the pre-market with consensus at the time of writing calling for EPS of $1.77. They will be followed by BMO that morning ($3.22). CIBC releases the next day ($1.64) along with RBC ($2.80) and TD ($2.09). Canadian Western Bank wraps it up on Friday ($0.77). National Bank and Laurentian Bank release the following week.

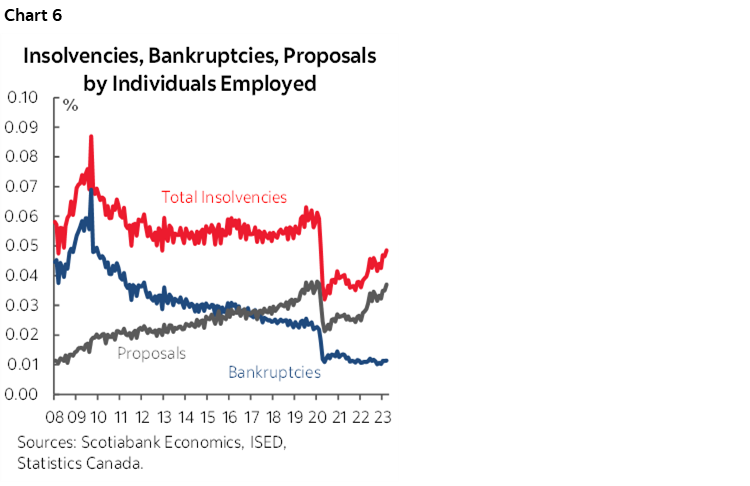

One issue that is a point of focus remains the mortgage and housing markets. I have found that some of the commentary that attracts the greatest attention is overly shrill sounding and sensational. There is a more balanced case based upon a few points as follows.

- 60% of households in Canada don’t even have a mortgage according to Census data (chart 4). 27% own their homes outright without a mortgage. 33% rent and while they have seen increases in rents, on average across the country CPI shows more modest increases than the payments shock coming to some mortgages (chart 5).

- Of the 40% of households who own their homes with a mortgage, it’s the tail of the distribution that is the most pressured who took out new mortgages or refinanced at the peak for house prices and the trough in borrowing costs over 2020–21. As variable rates get repriced higher, households are driving higher proposals to work with lenders, but bankruptcies remain rock bottom (chart 6). As fixed rate resets work through the mortgage market over 2025–26 at peak rates, bear in mind that affected households will have a few years of income growth and the opportunity to make adjustments.

- First-time homebuyers have had the opportunity to amass larger down payments as they have been sidelined and waiting to pounce upon cheaper prices in a one-two- lift to the amount of equity they can put in their homes.

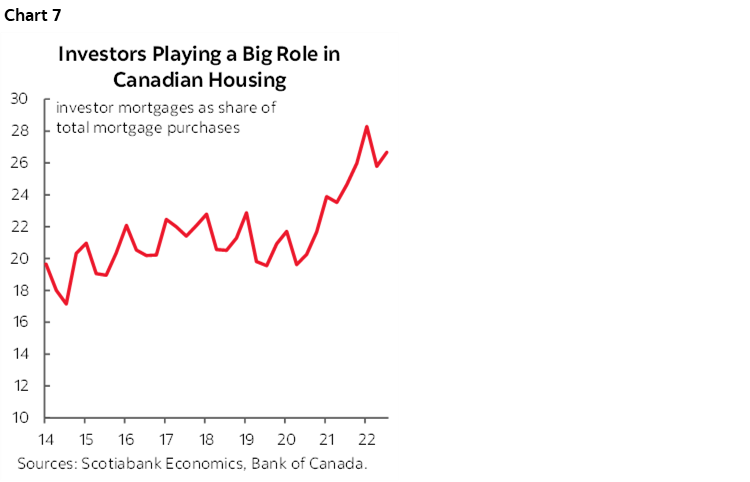

- Investors have been accounting for about one-in-four new mortgage purchases according to the Bank of Canada (chart 7). There is an awful lot of own-to-rent activity in Canada and speculation toward potential capital gains alongside vacation property purchases.

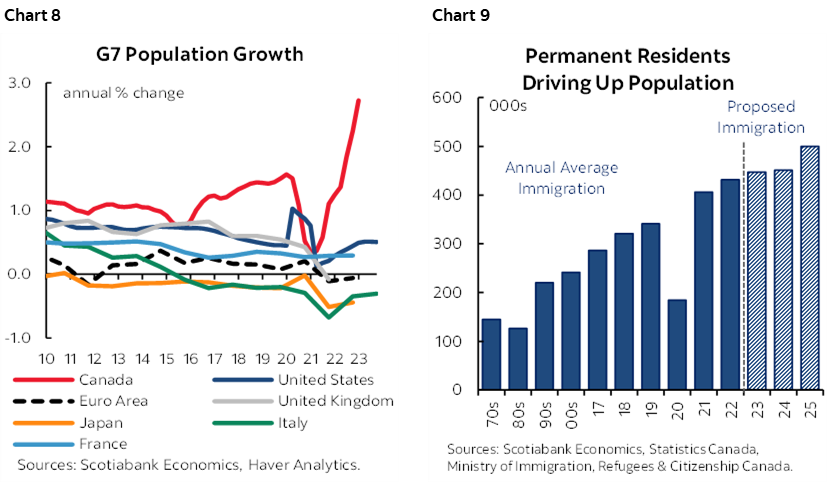

- Higher immigration is flooding into a market at a pace that is driving the fastest population growth among major economies (chart 8) as immigration targets rise (chart 9).

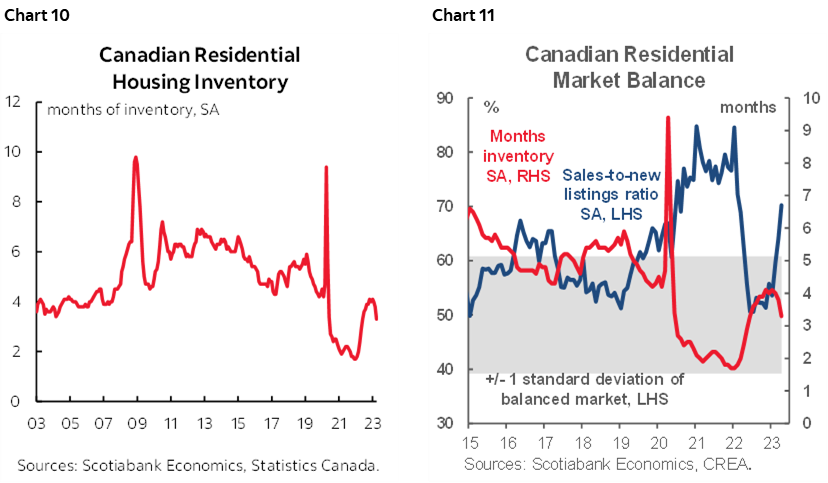

- This influx of immigrants is going into a housing market with little supply (charts 10, 11). This infusion of demand into a market with basically no supply and where the supply side adjusts with long lags will persistently pressure house prices. Housing strengths in an economy that remains in excess demand with very tight labour markets could be among the factors that I think will foment another round of pressures on core inflation.

The caveat to housing upsides is that when combined with sticky core inflation it means that the Bank of Canada’s job is probably not done. Governor Macklem remarked at the end of this past week that he is concerned about upside risks to inflation. I’ve been arguing for many weeks that the BoC prematurely paused its policy rate back in January and that the risk is toward further tightening. This past Wednesday I put out this street-leading note post-CPI indicating there was a high chance of hiking at the June meeting and if not then at the July meeting.

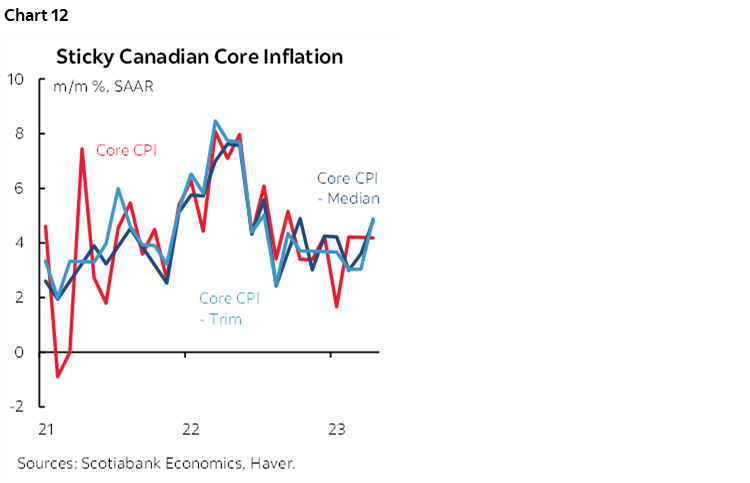

When properly looked at across the suite of core inflation readings in m/m annualized terms, the only period in which inflation ebbed was over 2022H1. Since then—and despite well over a year-and-a-half’s worth of bond market tightening—the figures have been remarkably sticky and with the latest readings all in the 4–5% range (chart 12). If the BoC focuses upon ebbing year-over-year rates then Governor Macklem will commit the exact same error he made in 2021 when he dismissed inflation as a mere by-product of soft year-ago prices, only in reverse this time.

Time is of the essence here and it would be a mistake for the BoC to delay any further. We expect the US debt ceiling negotiations to avoid the exceedingly low risk of default and would find it curious if anyone has default as a base case for the Hollywood actors in Congress. I don’t think that the BoC should wait to hike again since with each passing month that housing heats up further and core inflation remains well above the BoC’s 2% headline target it becomes more and more likely that such developments run away from the central bank’s ability to control them. They become ingrained in the mentality of households, businesses, governments and markets and controlling inflation back down to the 2% target becomes difficult to do which the BoC’s own surveys of business and household inflation expectations are already telling them alongside signals from recent collective bargaining actions across public sector and airline employees. A resilient and stable banking system should lend comfort to the BoC to do what it takes to crush inflation risk with more determined action.

CENTRAL BANKS—POWELL TALKS, GOP WALKS

Minutes to the May 2nd – 3rd FOMC meeting and four regional central bank decisions should offer fairly modest risk to markets.

FOMC Minutes—Enabling the GOP

Recall that on May 3rd the FOMC hiked the fed funds policy rate by 25bps and left options open into the June meeting (here). Wednesday’s minutes to that meeting will explore the breadth of opinion around whether to continue with a hiking bias or to take a breather and this will be informed by the frequency of citations around opinions that are expressed in the minutes.

This past Friday, Chair Powell remarked that “we can afford to look at the data and the evolving outlook to make careful assessments.” It could be argued this heightens the emphasis upon key data before the June 14th–15th meeting and with core PCE, another core CPI and nonfarm payrolls and wages all ahead of that meeting. It could also be argued that Chair Powell would prefer to tap out for a time and evaluate conditions. A third option is that Powell is using this language to leave open optionality around uncertainty toward how debt ceiling negotiations are going. Of course, the Fed Chair can’t say he’s perhaps standing down due to the debt ceiling without emboldening Congress to be more laid back in debt negotiations. It’s a tad coincidental that the GOP walked out of negotiations at literally the same time that Powell was speaking on Friday.

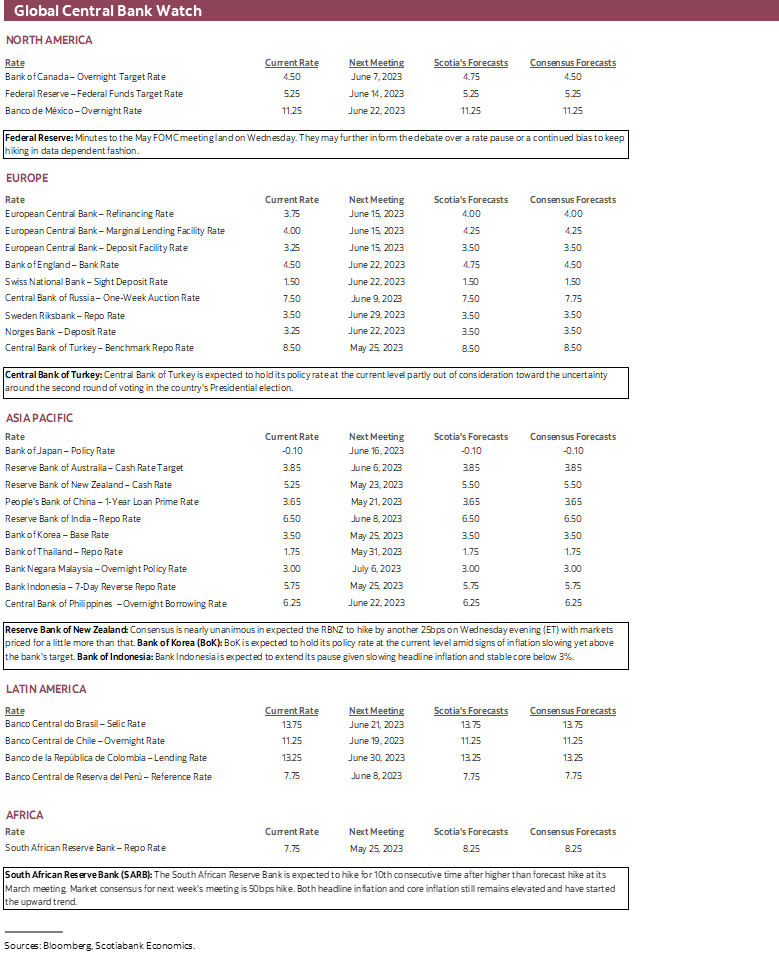

RBNZ—Sounds Familiar!

Consensus is nearly unanimous in expecting New Zealand’s central bank to hike the official cash rate by a further 25bps on Wednesday evening (ET). Markets are priced for a little more than a quarter-point hike. The parallel to the Bank of Canada is somewhat striking in that some local shops have argued that the central bank should hike due to the immigration catalysts that lift demand more quickly than any impact upon supply. You could add to this the effects of expansionary fiscal policy that is similar in the two countries. The RBNZ may follow the Budget’s removal of a recession forecast and perhaps reinforce higher-for-longer inflation risk.

Bank of Korea—Hawkish Guidance?

Thursday’s BoK decision is widely expected to extend the policy rate pause at a 7-day repo rate of 7½%. The prior decision on April 10th was marked by guidance against market pricing for rate cuts this year with a majority of members remaining open to further tightening if needed. Any repeat of such sentiment could be modestly impactful given what has since been pushed-out pricing for rate cuts.

Bank Indonesia—Still on Hold

Indonesia’s central bank is expected to hold its 7-day reverse repo rate unchanged at 5.75% again on Thursday. Core inflation is running within the 2–3% headline target range as overall inflation has been falling from a peak of about 6% last September toward about 4¼% now.

Turkey—In Erdogan’s Shadow

Turkish central bankers are a rarity in the world of monetary policy for their total lack of job security compared to the practically tenured academic-style appointments elsewhere. Don’t expect that to change on Thursday when the central bank delivers another rate decision that is widely expected to hold the one-week repo rate at an unchanged 8.5%. With the second-round of Turkey’s Presidential election being held on the following Sunday, at stake is any potential policy pivot. President Erdogan’s rather unorthodox policy has pursued overly easy monetary policy that debased the lira and drove imported inflation. Should he win the second-round election then Turkish assets are likely to extend the pain following the first round results.

SARB to Hike

Most economists expect South Africa’s central bank to hike by 50bps on Thursday. High inflation and a soft currency are motivating a continued tightening bias.

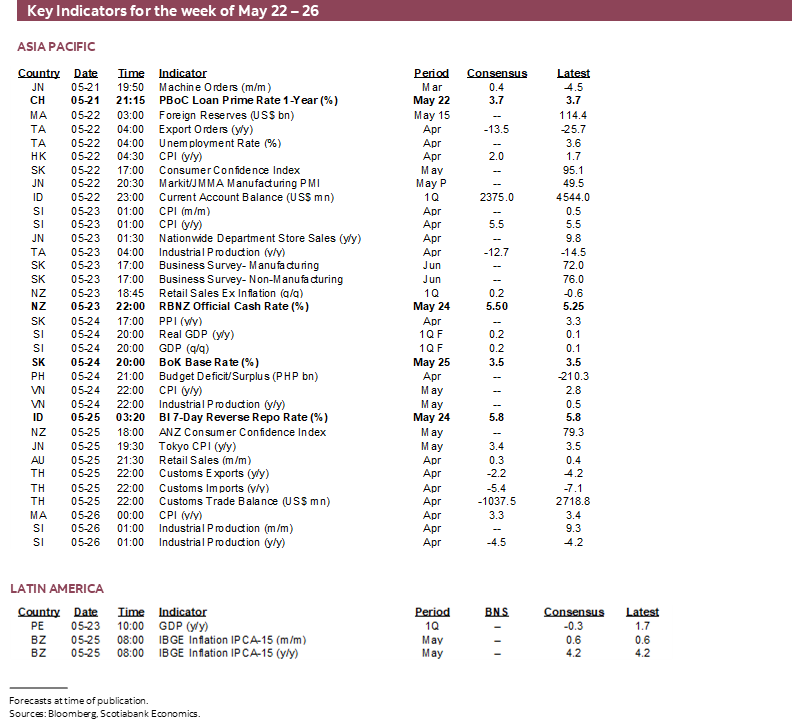

GLOBAL MACRO RELEASES

Data risk will principally focus upon purchasing managers indices and inflation updates.

Purchasing managers’ indices can offer insight into current quarter GDP growth tracking. Australia and Japan will update theirs first on Monday evening (eastern time as always in this report) and will be followed by the Eurozone, UK and US readings the next day. Since services are a much bigger share of GDP than manufacturing across these countries it’s mildly encouraging that their strengths are significantly offsetting manufacturing sector challenges (charts 13, 14). In all cases, the composite PMIs continue to indicate economic growth into Q2.

Canada’s macro calendar will be very light. The week starts off with markets shut for the Victoria Day holiday aka the unofficial start of summer, before bank earnings take over. Albertans will be able to vote starting on Tuesday through Saturday in advance of the May 29th election so watch for rolling polls. Only producer prices (Tuesday) and the seriously lagging payrolls report for March (Thursday) are on tap.

The other main US macro reports will include the following:

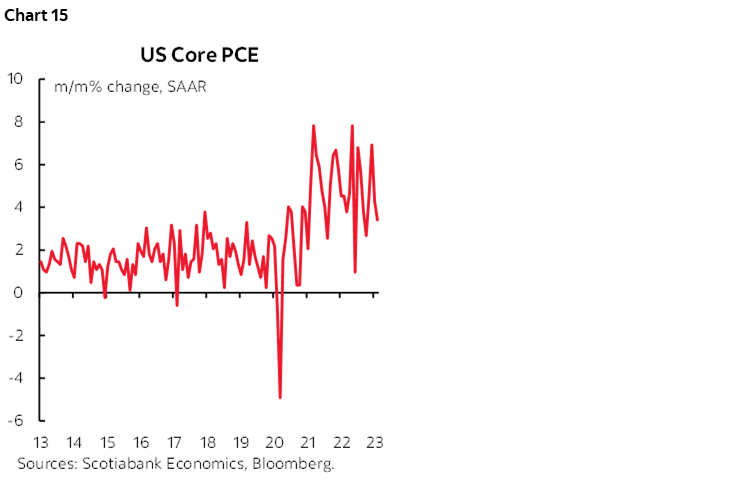

- The Fed’s preferred inflation gauge for April arrives on Friday alongside consumer income and spending estimates. Core PCE inflation is expected to rise by 0.3% m/m with a stable year-over-year rate of 4.6% and broadly follow the already known core CPI reading. The different methodology of PCE including its much lower weight on shelter and owners’ equivalent rent than in CPI can reveal surprises. The Cleveland Fed’s ‘nowcast’ is a tick higher than my estimate. It’s likely that the reading will continue to demonstrate that inflation remains too hot in a continuation of the trend shown in chart 15.

- Total consumer spending is expected to post a decent 0.5% m/m SA gain in April backed by healthy income growth of 0.4% m/m (Friday). We already know that the retail sales control group (ex-autos, gas, building supplies) was up by 0.7% m/m SA and that serves as input into total consumption that may be supported by ongoing gains in services spending.

- Friday’s durable goods report might be on the softer side until explosive growth in new plane orders likely raises it in the next report.

- Housing data will bring out new home sales for April (Tuesday) and the pending home sales reading for the same month (Thursday) which serves as a leading indicator for existing home sales.

- Q1 GDP is expected to be left unrevised on Thursday at about 1.1% q/q SAAR in the second revision.

- Thursday’s initial claims will hopefully build upon the recent improvement after Massachusetts revealed earlier problems with fraudulent claims which is where the prior run-up had been focused.

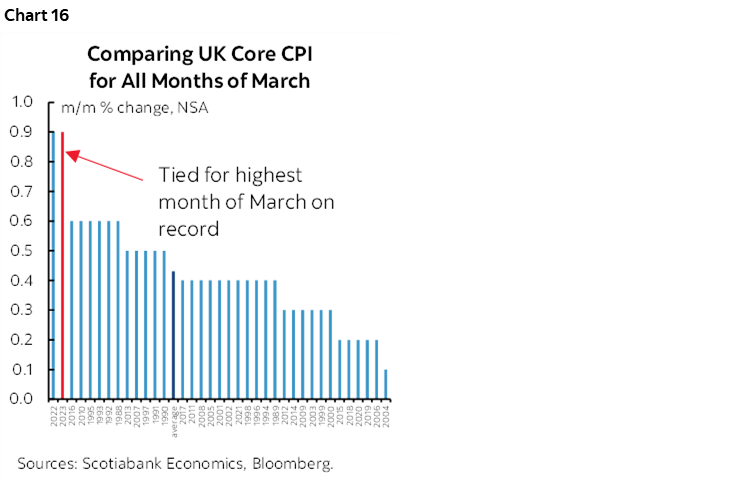

UK CPI inflation (Wednesday) is coming off one of the hottest months of March on record (chart 16) in what has been a general pattern so far this year. Another hot one is expected with CPI expected to climb by 0.7% m/m. Most expect the year-over-year headline rate to ebb to just over 8% from 10.1% but that’s due to year-ago base effects especially on fuel as the core CPI year-over-year measure is expected to hold at just over 6%. Retail sales (Friday) are expected to mildly rebound from the prior month’s weakness.

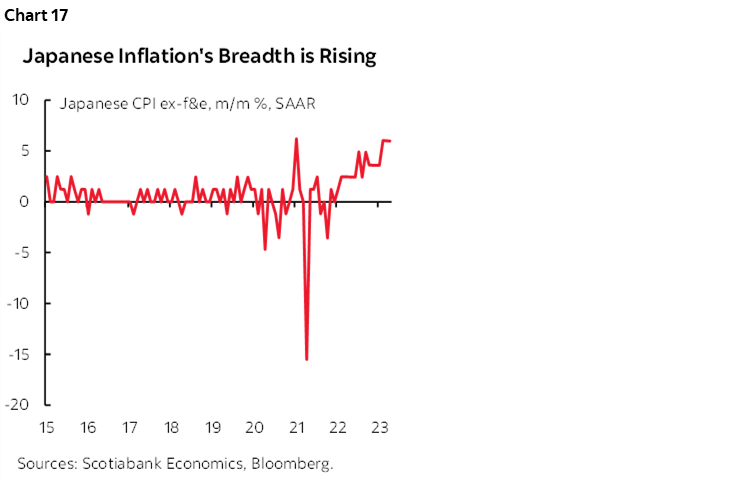

Additional evidence of rising Japanese inflation lands with the Tokyo CPI gauge for the month of May on Thursday. There are increasingly convincing signs that Japanese inflation may motivate a BoJ pivot this year. National CPI ex-f&e in m/m SA terms was tied with two other months for the hottest increases since a temporary blip in 2014 (chart 17). There is a trend toward rising m/m core CPI SA gains over the past year that indicates that inflation’s breadth is fanning out. The implication is that the path to the mid-June BoJ meeting is being marked by reason to upgrade inflation forecasts in the context of ongoing speculation toward a policy pivot at some point.

Also watch for Germany’s IFO business confidence measure (Wednesday), Australian retail sales during April (Thursday) and New Zealand’s Q1 retail sales (Tuesday).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.